Dental Apex Locator Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 125.16 Million |

| Market Size (2031) | USD 168.22 Million |

| Growth Rate (2026 - 2031) | 6.09% CAGR |

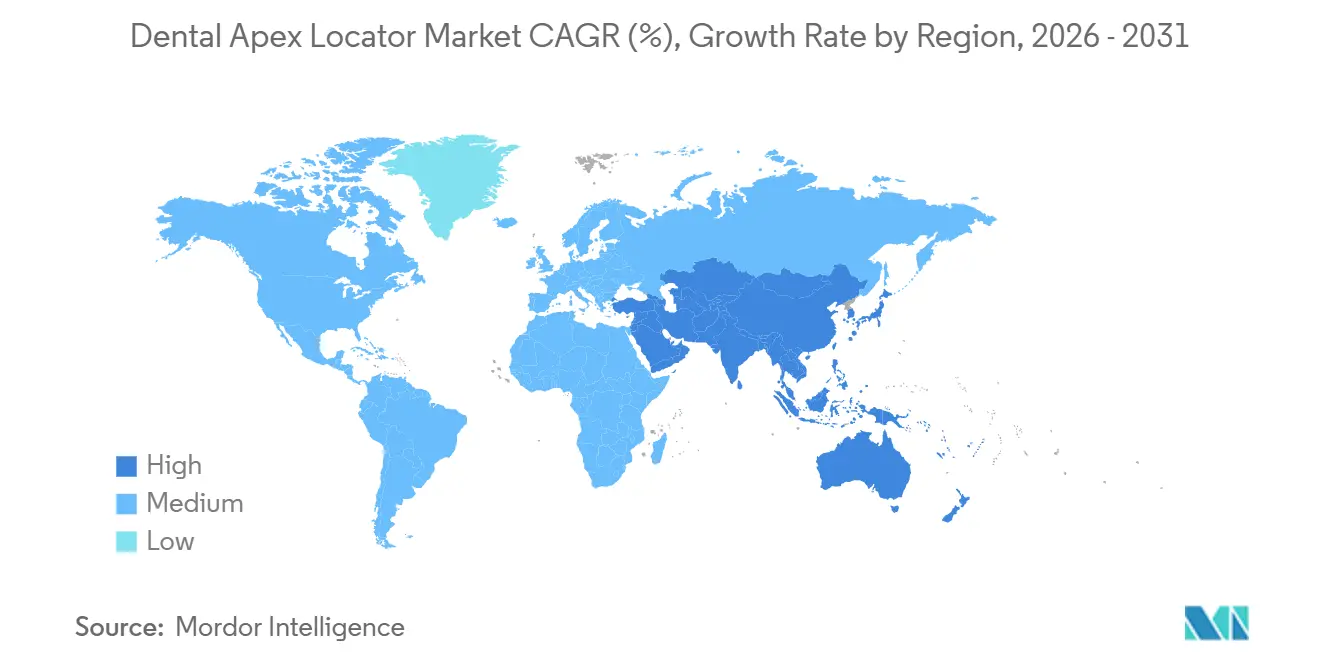

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Dental Apex Locator Market Analysis by Mordor Intelligence

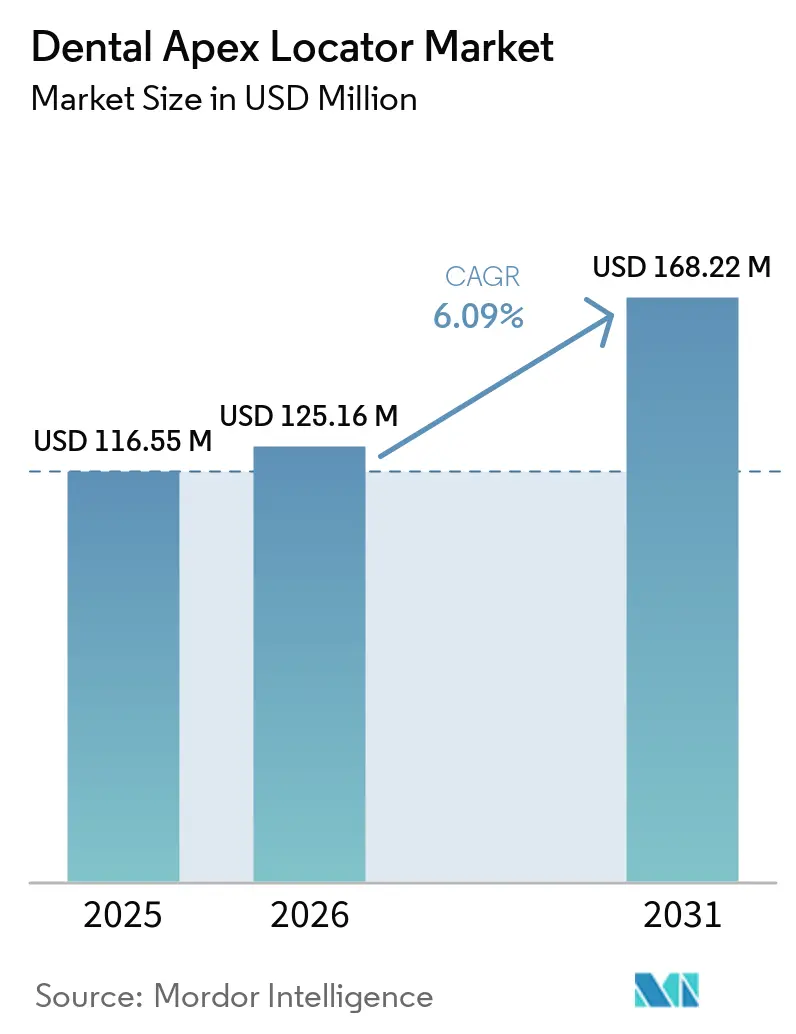

The Dental Apex Locator Market size is expected to increase from USD 116.55 million in 2025 to USD 125.16 million in 2026 and reach USD 168.22 million by 2031, growing at a CAGR of 6.09% over 2026-2031.

Higher procedure volumes from untreated caries and aging populations are sustaining equipment demand in high-income and middle-income countries. This trajectory is underpinned by procedural-volume pressure: the World Health Organization confirms that more than 2 billion people suffered from dental caries in permanent teeth as of 2025, while CDC surveillance shows 21% of US adults aged 20–64 carry at least one untreated cavity[1]World Health Organization, “Oral Health Fact Sheet,” World Health Organization, who.int. Clinical adoption is shifting toward integrated systems that pair apex locators with endodontic motors to reduce chair time and improve consistency in working length determination. Connectivity features, such as Bluetooth and cloud sync, add documentation and quality assurance value that supports multi-clinic and referral workflows. Device bundling with chairs, motors, and imaging systems is common in new clinic builds, which influences price tiers and purchase timing. Institutional policies around electromagnetic compatibility continue to shape usage scenarios, especially for patients with cardiac implantable devices, which tempers hospital uptake compared with private clinics.

Key Report Takeaways

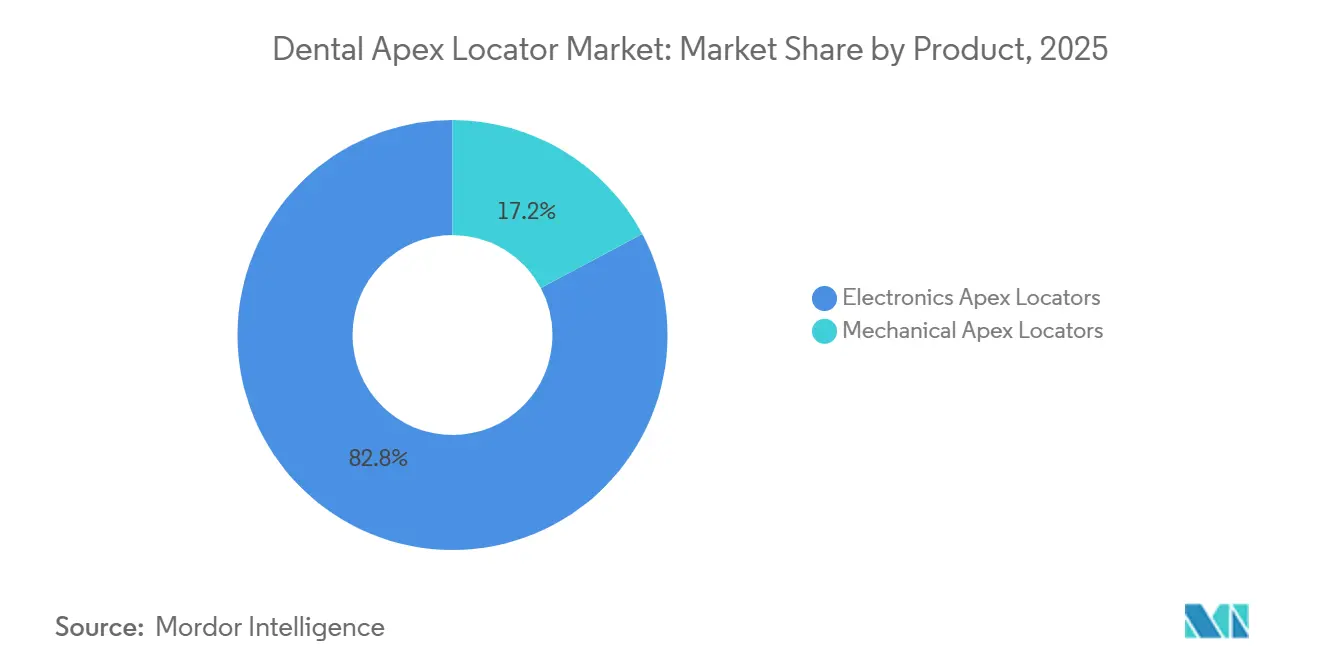

- By product, electronics apex locators led with 82.79% revenue share in 2025, and are projected to expand at a 6.34% CAGR through 2031.

- By technology, impedance-based systems accounted for 67.90% in 2025 and are expected to grow at a 7.12% CAGR to 2031.

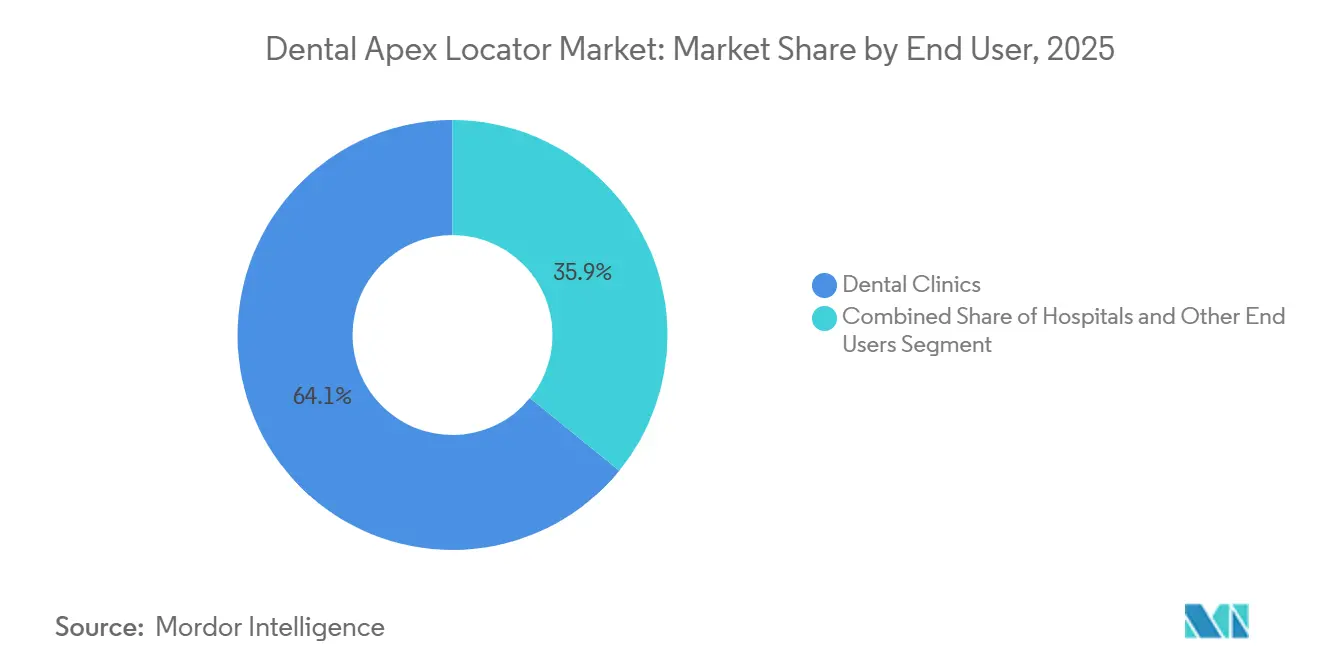

- By end user, dental clinics represented 64.13% in 2025 and are expected to record the highest growth at a 6.83% CAGR through 2031.

- By geography, North America held 44.56% in 2025, while Asia-Pacific is projected to post the fastest expansion at a 7.25% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Dental Apex Locator Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising root canal procedure volumes from caries prevalence and aging populations | +1.8% | Global, with the highest intensity in North America and Europe | Medium term (2-4 years) |

| Integration with endodontic motors and digital dentistry improves workflow and outcomes | +1.5% | North America and Europe, early adoption in Asia-Pacific premium clinics | Short term (≤ 2 years) |

| Expansion of dental clinics and dental tourism increases equipment uptake | +1.2% | Asia-Pacific core with spill-over to the Middle East | Long term (≥ 4 years) |

| Dental education and continuing training embed EAL use in clinical curricula | +0.9% | National, with early gains in North American and European dental schools | Long term (≥ 4 years) |

| Connectivity (Bluetooth/Cloud), enabling documentation and QA workflows | +0.7% | North America, Western Europe, urban Asia-Pacific | Medium term (2-4 years) |

| HF-conduction modules and 2-in-1 apex locator + pulp tester expand use-cases | +0.5% | Global, particularly multi-specialty clinics in North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Root Canal Procedure Volumes from Caries Prevalence and Aging Populations

A high global burden of dental caries is now translating into steady case inflows for endodontic treatment, which lifts demand in the dental apex locator market. Public health surveillance confirms a meaningful share of United States adults live with untreated cavities, and prevalence is higher in older cohorts, supporting persistent procedure volumes that align with electronic working length measurement. In 2026, population aging remains a structural trend, with public health agencies projecting a larger share of people over 60 by mid-century, which correlates with more complex restorative and endodontic care over time. Specialist-led practice models are more common in the United States, where endodontists handled a larger fraction of root canal procedures in 2024 than earlier in the decade, which reinforces the use of apex locators in precision workflows. Survey data also show patients often prefer saving a natural tooth with root canal treatment over extraction, which sustains referral volumes to endodontic specialists. Meanwhile, patient preference has shifted decisively toward tooth preservation. The 2025 AAE consumer survey found 94% of adults prioritize retaining natural teeth, and 71% of root-canal recipients preferred the procedure over extraction[2]American Association of Endodontists, “AAE 2024-2025 Annual Report,” American Association of Endodontists, aae.org. Together, these factors maintain an equipment replacement cycle that favors advanced locators and integrated motor-plus-locator systems.

Integration With Endodontic Motors and Digital Dentistry Improves Workflow and Outcomes

Integrated motor-plus-apex-locator systems are streamlining length determination and shaping, which reduces chair time and consolidates equipment footprints in operatories. Dentsply Sirona’s Motor and Apex Module received United States clearance and enables real-time length readings during active instrumentation, with predicate-supported safety and performance claims, reflecting regulator comfort with integrated designs. Manufacturers pair brushless motors, torque control, and auto-reverse at preset apical targets with locator feedback, which lowers the need for manual pause-and-measure steps and radiographic checks. The result is faster canal negotiation and more consistent working length control across wet and dry conditions, which increases the clinical utility of apex locators in multi-visit and single-visit protocols. These systems also align with digital dentistry ecosystems that integrate imaging, planning, and documentation to support multi-clinic operations and referral coordination. As interoperability improves, integrated platforms become a default choice for specialists and high-throughput clinics in the dental apex locator market.

Expansion of Dental Clinics and Dental Tourism Increases Equipment Uptake

Clinic expansion in growth corridors, combined with steady inflows of cross-border patients, continues to support capital purchases that include apex locators in bundled packages. New facilities often standardize their equipment lists across chairs, motors, sterilization, and diagnostic systems, which creates a clear path to integrate apex locators early in the fit-out. Multi-site providers and referral networks prefer consistent device models and connectivity features to support training, maintenance, and data flow, which favors modern locator designs over legacy units. Dental tourism hubs in Asia are upgrading infrastructure to compete for high-acuity treatments, and that competition raises the baseline for endodontic equipment in private clinics. Practices that position for international patients emphasize efficient, technology-supported care pathways for complex cases, and integrated locator-motor systems fit these requirements. This environment sustains multi-year purchasing patterns that keep the dental apex locator market on a steady growth path.

Dental Education and Continuing Training: Embed EAL Use in Clinical Curricula

Universities and teaching clinics are expanding facilities and updating curricula to embed electronic working length determination as a core clinical skill. Several U.S. academic institutions have announced clinic investments that include modern operatories and integrated endodontic workflows, which create hands-on exposure to apex locator use among trainees. Academic programs use clinical rotations to reinforce device proficiency under supervision, setting norms that graduates bring into private practice. Industry-sponsored programs and continuing education modules further reinforce locator best practices in shaping sequences and retreatments. These efforts now extend to documentation and device maintenance protocols, which help operators understand how to sustain accuracy over time. The result is a pipeline of clinicians who default to electronic measurement instead of tactile or radiographic length estimation, supporting stable replacement demand in the dental apex locator market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High device cost and total cost of ownership for advanced models | -0.8% | Asia-Pacific, Latin America, Africa | Medium term (2-4 years) |

| Regulatory approval and evidence requirements slow new model launches | -0.6% | Global, heightened impact in the European Union and the FDA jurisdictions | Short term (≤ 2 years) |

| EMC/pacemaker cautions and hospital policies constrain usage scenarios | -0.3% | Developed markets with high CIED prevalence | Long term (≥ 4 years) |

| Accuracy variability with anatomy and user training needs | -0.4% | Emerging markets with limited specialist density | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Device Cost and Total Cost of Ownership for Advanced Models

Price tiers separate standalone apex locators from integrated motor-plus-locator systems, which influences adoption in price-sensitive settings. Catalog benchmarks show integrated systems can cost more than standalone units, and that differential can slow purchase decisions for small independent clinics even when the efficiency gains are clear. Replacement parts, batteries, and maintenance add to total cost of ownership over several years, which encourages careful staging of equipment purchases. Where bundles are negotiated, clinics may prioritize chairs, imaging, or sterilization first, which can defer locator upgrades to later quarters. Distributors address these hurdles by offering refurbished or certified pre-owned units with limited warranties to pull forward adoption. Despite the cost headwinds, manufacturers continue to emphasize reliability, support, and workflow savings to justify integrated systems in the dental apex locator market.

Regulatory Approval and Evidence Requirements Slow New Model Launches

Regulatory reviews for new or modified apex locator systems introduce multi-month lead times that influence product roadmaps and launch sequencing. In the U.S., 510(k) filings must demonstrate substantial equivalence to predicate devices using applicable bench standards and lab data, which guides engineering and documentation priorities. A recent clearance for an integrated motor and apex module highlights how suppliers package multiple functions in a single control unit and validate them through standardized testing. In the European Union, MDR transition milestones require sustained quality system attention, which diverts resources from net-new product introductions in the near term. Vendors respond with platform extensions and software updates that preserve core device architecture while adding features that do not trigger fresh clearances. This regulatory dynamic helps explain why connectivity, usability, and integration improvements often outpace sweeping hardware redesigns in the dental apex locator market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Electronics Apex Locators Anchor Growth, Mechanicals Persist in Budget Niches

Electronics apex locators captured 82.79% of the dental apex locator market share in 2025 and are projected to grow at a 6.34% CAGR through 2031, reflecting broad clinician preference for accuracy, integration, and connectivity. Within this slice of the dental apex locator market size, leading products combine multi-frequency impedance measurement with noise management to stabilize readings in wet canals. Integrated battery designs, compact contra-angle heads, and smooth user interfaces support continuous measurement during shaping and retreatments across a range of canal anatomies. Manufacturers highlight charge longevity per treatment cycle, improved torque control in paired motors, and preset apical targets that activate auto-reverse to reduce over-instrumentation risk. Standalone electronic locators remain relevant where clinicians prefer separate motor and locator units for cost or modularity reasons. In these settings, menu simplicity and durable clips are valued alongside accuracy.

Mechanical apex locators continue to serve budget-constrained users, including clinics that prioritize low upfront costs and minimal maintenance. Although mechanicals carry lower acquisition prices, moisture sensitivity and the lack of integrated controls limit usage in complex cases compared with electronic systems. As integrated motor-plus-locator packages gain traction, mechanical devices risk ceding further ground where clinicians want consolidated footprints and fewer workflow interruptions. That said, mechanical units function as durable backups where power reliability is variable or where basic functionality suffices. In markets with wide price dispersion, distributors promote both tiers to match clinic budgets and case mixes. This tiering helps sustain access while reinforcing electronics as the default in the dental apex locator industry.

By Technology: Impedance-Based Systems Leverage Multi-Frequency Algorithms for Wet-Canal Accuracy

Impedance-based systems held 67.90% in 2025 and are expected to post the fastest growth at a 7.12% CAGR through 2031, driven by multi-frequency algorithms that help maintain accuracy in fluid-filled canals. Within this portion of the dental apex locator market size, suppliers use DSP-based analysis to reduce noise and stabilize tip-to-apex distance indications under NaOCl or blood. Product designs also emphasize intuitive screens, color-coded guidance near the apical constriction, and quick auto-calibration to simplify chairside use. Third-generation and later devices are consistently reported to outperform radiography alone for apical accuracy, which concentrates R&D on usability and integration rather than core measurement physics. As predicate devices in recent clearances skew toward multi-frequency models, regulatory familiarity supports this trajectory. These advantages keep impedance-based platforms at the center of the dental apex locator industry.

Frequency-based designs account for the remaining share and grow at a slower pace as they are more sensitive to canal moisture and may require additional drying steps for stability. Their simpler architecture and lower prices maintain relevance for cost-focused buyers and for clinics that prefer to separate measurement from shaping systems. Training can narrow performance differences for specific case types, but most high-throughput practices prefer the reliability and integration benefits of impedance-based products. As device ecosystems expand to include app-based documentation and motor control, single-frequency devices typically bridge as entry-level options. This dynamic preserves a tiered landscape where multi-frequency devices anchor premium adoption while frequency-based models serve budget and backup roles. Over the forecast, connectivity and integration features are likely to widen the gap in perceived value.

By End User: Dental Clinics Drive Volumes via DSO Consolidation and Tourism Infrastructure

Dental clinics accounted for 64.13% in 2025 and are projected to grow the fastest at a 6.83% CAGR through 2031, reflecting consolidation, standardized equipment lists, and digital workflows. Within this share of the dental apex locator market size, multi-site providers prioritize consistent device models to streamline training, stocking, and maintenance. Integrated motor-plus-locator systems reduce chair time and simplify working length control across associate dentists and endodontists, which increases perceived return on investment. Private clinics also emphasize patient experience and throughput, which supports continuous measurement features during shaping. App-based documentation helps clinics coordinate with referring practices and insurers, improving post-procedure auditing and case note completeness. These drivers help clinics sustain planned upgrades and replacements, even as broader capital cycles affect timing.

Hospitals and other end users maintain stable demand but at lower growth rates due to risk management protocols and competing equipment priorities. Apex locator use in hospital-affiliated clinics can be constrained by policies that consider patients with cardiac implantable devices and prioritize conservative workflows. Academic institutions, mobile units, and research centers continue to invest in modern operating rooms and electronic measurement training to expand capacity and workforce readiness. Vendors support these segments with training modules, refurbishment options, and integration pathways that fit existing IT environments. Together, these choices keep institutional demand present but secondary to private clinic growth. Over time, standardization and evidence accumulation may narrow the adoption gap between settings in the dental apex locator market.

Geography Analysis

North America led in 2025 with 44.56% revenue share, supported by robust specialist networks, advanced operatory infrastructure, and stable reimbursement pathways for endodontic care. A recent U.S. clearance for an integrated motor and apex module reflects ongoing regulatory momentum for connected multi-function endodontic systems. Patient preference for preserving natural teeth continues to reinforce root canal volumes, which strengthens the utilization of apex locators in specialist and high-throughput general practices. Insurance claims data from the American Association of Endodontists reveals that the share of endodontic treatments performed by endodontists climbed from 34.6% in 2020 to 44.4% in 2024, reflecting specialist adoption of precision measurement tools and workflow-integrated systems[3]Dental Tribune International. "Insurance data indicates rise in specialist endodontic care in U.S.”. Replacement cycles in mature clinics, combined with connectivity upgrades, support mid-single-digit growth through 2031. Training programs and continuing education sustain device proficiency across new graduates and experienced clinicians, which further stabilizes usage. These ingredients anchor steady demand in the dental apex locator market.

Europe maintains a sizeable share with strong clinical standards and high technology adoption across private clinics and group practices. MDR transition milestones encourage device updating, which supports replacement purchases for models that align with current conformity requirements. Training and academic investments help embed electronic working length determination as standard-of-care for complex cases. In markets with aging populations and high dental-awareness, procedure volumes remain robust for endodontic treatments. Vendors with established brands in Germany, the United Kingdom, France, Italy, and the Nordics compete on accuracy claims, integration readiness, and service models. These dynamics contribute to resilient mid-term demand in the dental apex locator market.

Asia-Pacific is the fastest-growing region through 2031, driven by private clinic expansion and the growth of cross-border patient flows into regional hubs. Group practice development and technology-forward clinic designs create an early path for integrated motor-plus-locator systems, which aligns with rising procedural complexity. Local manufacturers with ISO 13485-certified facilities increase access to lower-cost options, which broadens the installed base. As training and referral networks mature, clinics in urban centers integrate app-based documentation features to manage larger caseloads and collaborate with labs and imaging centers. Competitive intensity encourages packaged purchases, with chairs, sterilizers, motors, and apex locators bundled under unified service agreements. This combination of access, pricing, and integration fuels higher growth in the dental apex locator market.

Competitive Landscape

The competitive environment features established multinational brands alongside agile regional players that compete on integration, connectivity, and pricing. J. Morita’s Root ZX lineage remains a prominent reference in clinical discussions, with compact models and integrated systems that emphasize consistent length readings across wet and dry canals. Dentsply Sirona advances a broad endodontic portfolio highlighted by an integrated motor and apex module, combining real-time length feedback with motor control and documentation readiness. Envista’s Kerr brand focuses on user-friendly interfaces and compatibility with popular file systems to align with daily practice needs. Collectively these approaches position incumbents to defend premium segments of the dental apex locator market.

A set of specialized competitors differentiates through cost optimization, connectivity, and modular integration strategies. Woodpecker Medical and similar manufacturers emphasize performance-per-dollar with DSP processing, compact form factors, and integrated features that support efficient shaping workflows. VDW and COLTENE integrate locators within larger endodontic ecosystems, linking motors, obturation devices, and software to create cohesive user experiences. NSK’s iPex line and related motor products continue to evolve with firmware updates and ergonomic refinements for chairside use. Forumtec’s Bluetooth-enabled designs reflect the market’s shift toward wireless operation and configurable displays. These offerings expand buyer choice in the dental apex locator market.

Distributors and value-oriented brands support access with entry-level and refurbished options, along with training and support that reduce barriers to adoption. Catalogs list standalone locators and integrated motor-plus-locator units with transparent feature sets and pricing, helping clinics align equipment choices to case complexity and capital plans. Select models add pulp vitality testing to locator functions, further consolidating tools and shortening chair time. Vendors emphasize connectivity, battery longevity, clear display thresholds near the apical constriction, and compatibility with popular file systems. As integration and data capture become standard, suppliers prioritize reliability and service responsiveness to help clinics meet documentation and QA expectations. This expands the installed base while reinforcing premium differentiation in the dental apex locator market.

Dental Apex Locator Industry Leaders

-

COLTENE Group

-

Dentsply Sirona

-

J. MORITA CORP

-

Nakanishi inc.

-

Woodpecker Medical Instrument Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2024: Dentsply Sirona has introduced two new endodontic solutions in the US: the X-Smart Pro+ endodontic motor with an integrated apex locator and the Reciproc Blue file.

- February 2024: J. MORITA USA has unveiled the Root ZX3 apex locator along with a new HF (high-frequency) module, marking the latest generation in its renowned apex locator line. This advanced system enhances canal treatment by integrating high-frequency technology, offering dentists a more precise and innovative approach to endodontic therapy.

- June 2023: J. MORITA USA, one of the global leaders in endodontics, proudly introduces the Tri Auto ZX2+, an advanced cordless endodontic handpiece featuring a built-in apex locator. This upgraded device now supports reciprocating files and incorporates the next-generation Optimum Glide Path 2 (OGP2) mode, delivering enhanced safety, precision, and ease of use for clinicians.

Global Dental Apex Locator Market Report Scope

A dental apex locator is an electronic device used in endodontics to determine the precise working length of a root canal by locating the apical foramen, the natural opening at the root tip of a tooth. By measuring electrical resistance or impedance within the canal, it helps dentists avoid over- or under-instrumentation, ensuring accurate cleaning, shaping, and filling of the canal. This technology improves treatment success rates, reduces reliance on radiographs, and enhances patient safety and comfort during root canal procedures. The Dental Apex Locator Market Report is Segmented by Product (Electronics Apex Locators, Mechanical Apex Locators), Technology (Frequency-based, Impedance-based), End User (Dental Clinics, Hospitals, Other End Users), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The Market Size and Forecasts are provided in Terms of Value (USD) for all the above segments.

| Electronics Apex Locators |

| Mechanical Apex Locators |

| Frequency-based |

| Impedance-based |

| Dental Clinics |

| Hospitals |

| Other End Users (Academic & Research Institutes, Mobile Dental Units, and Among Others) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Electronics Apex Locators | |

| Mechanical Apex Locators | ||

| By Technology | Frequency-based | |

| Impedance-based | ||

| By End User | Dental Clinics | |

| Hospitals | ||

| Other End Users (Academic & Research Institutes, Mobile Dental Units, and Among Others) | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the dental apex locator market growth outlook to 2031?

The dental apex locator market size is USD 125.16 million in 2026 and is projected to reach USD 168.22 million by 2031 at a 6.09% CAGR.

Which product segment leads and which grows the fastest?

Electronics apex locators lead with 82.79% in 2025 and are also the fastest-growing at a 6.34% CAGR through 2031.

What technology type is most adopted in the dental apex locator market?

Impedance-based systems hold 67.90% in 2025 and are projected to grow at a 7.12% CAGR, reflecting clinical preference for multi-frequency accuracy in wet canals.

Which end user will contribute the most to new unit uptake?

Dental clinics represent 64.13% in 2025 and are expected to record the highest growth at a 6.83% CAGR through 2031 due to consolidation and digital workflows.

What factors could restrain hospital adoption?

Electromagnetic compatibility considerations for patients with cardiac implantable devices lead hospitals to use conservative protocols, which can shift some procedures to hand files and radiographs.

Which regions are likely to see the fastest growth in the dental apex locator market?

Asia-Pacific is projected to grow the fastest through 2031, supported by private clinic expansion, technology-forward fit-outs, and growing referral networks.

Page last updated on: