Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 21.99 Billion |

| Market Size (2031) | USD 28.21 Billion |

| Growth Rate (2026 - 2031) | 5.12% CAGR |

| Fastest Growing Market | Europe |

| Largest Market | Asia Pacific |

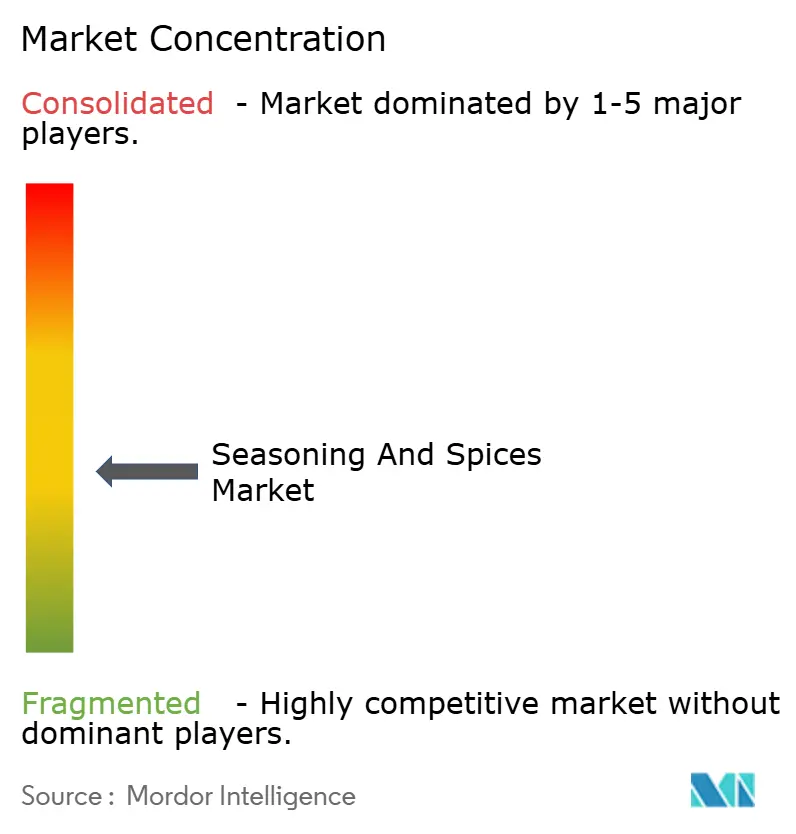

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Seasoning and Spices Market Analysis by Mordor Intelligence

The spices and seasonings market size was valued at USD 20.92 billion in 2025 and estimated to grow from USD 21.99 billion in 2026 to reach USD 28.21 billion by 2031, at a CAGR of 5.12% during the forecast period (2026-2031). The market is undergoing significant transformation as consumers increasingly seek natural ingredients with health benefits, particularly immunity-boosting spices like turmeric, ginger, and garlic. Manufacturers are now prioritizing transparent sourcing and natural ingredients, driven by the industry's emphasis on clean label initiatives and sustainability practices. As culinary preferences globalize, there's a heightened demand for ethnic spice blends and fusion flavors. In response, manufacturers are crafting innovative combinations that seamlessly merge traditional ethnic flavors with contemporary taste preferences. The recent surge in home cooking has further propelled the use of diverse spices and seasonings in kitchens. Moreover, the pervasive influence of social media and cooking shows has familiarized consumers with global cuisines, spurring them to experiment with novel spice combinations. This transformation in the spices and seasonings market mirrors a broader shift in global food consumption, where a growing health consciousness intertwines with a spirit of culinary exploration.

Key Report Takeaways

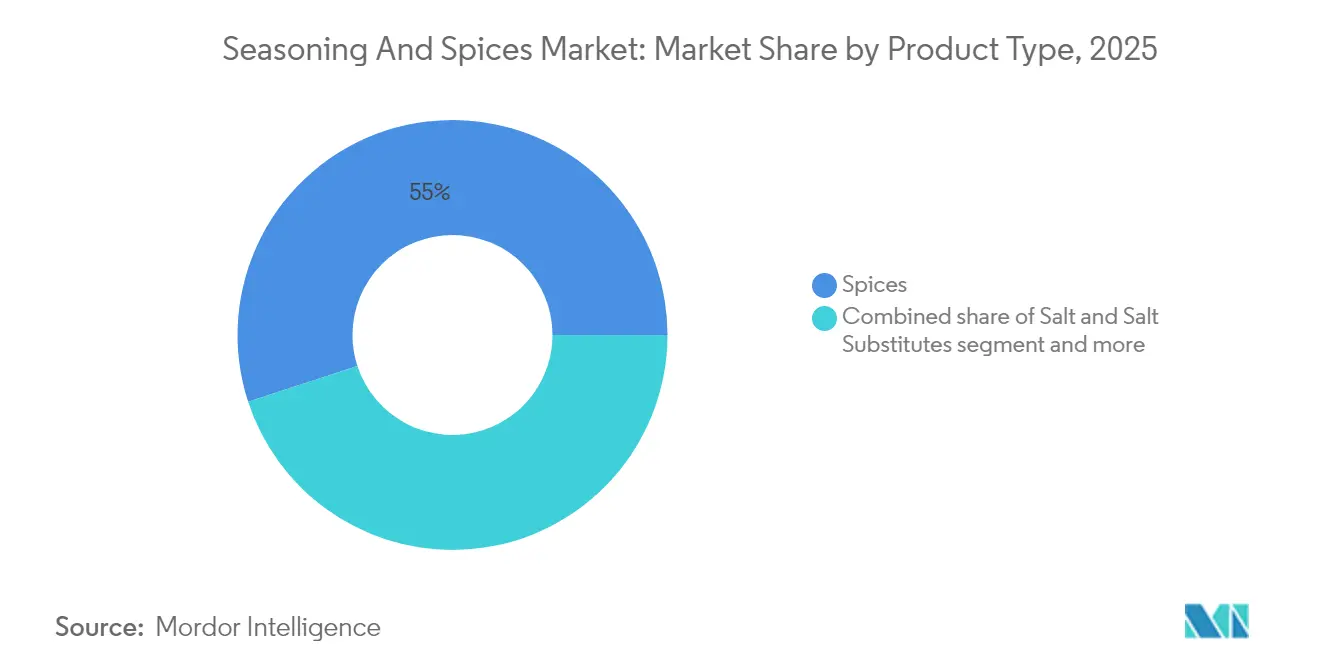

- By product type, spices led with a 55.02% share of the spices and seasonings market in 2025, while herbs and seasonings are forecast to advance at a 6.56% CAGR to 2031.

- By category, conventional items held 80.47% of the spices and seasonings market share in 2025, and organic products recorded the fastest trajectory with a 7.25% CAGR through 2031.

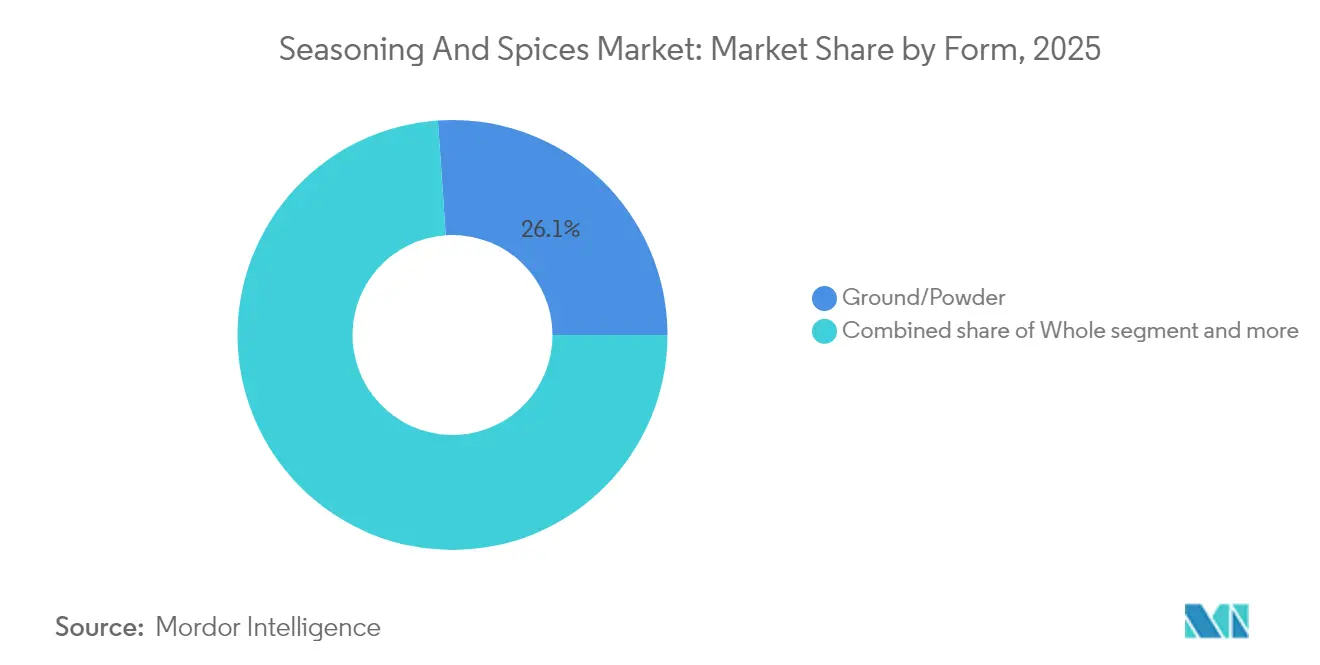

- By form, ground and powder products captured 26.08% of the spices and seasonings market size in 2025 and are projected to expand at a 5.63% CAGR by 2031.

- By application, meat and seafood accounted for 28.88% of the spices and seasonings market size in 2025, while savory snacks are expected to rise at a 6.85% CAGR to 2031.

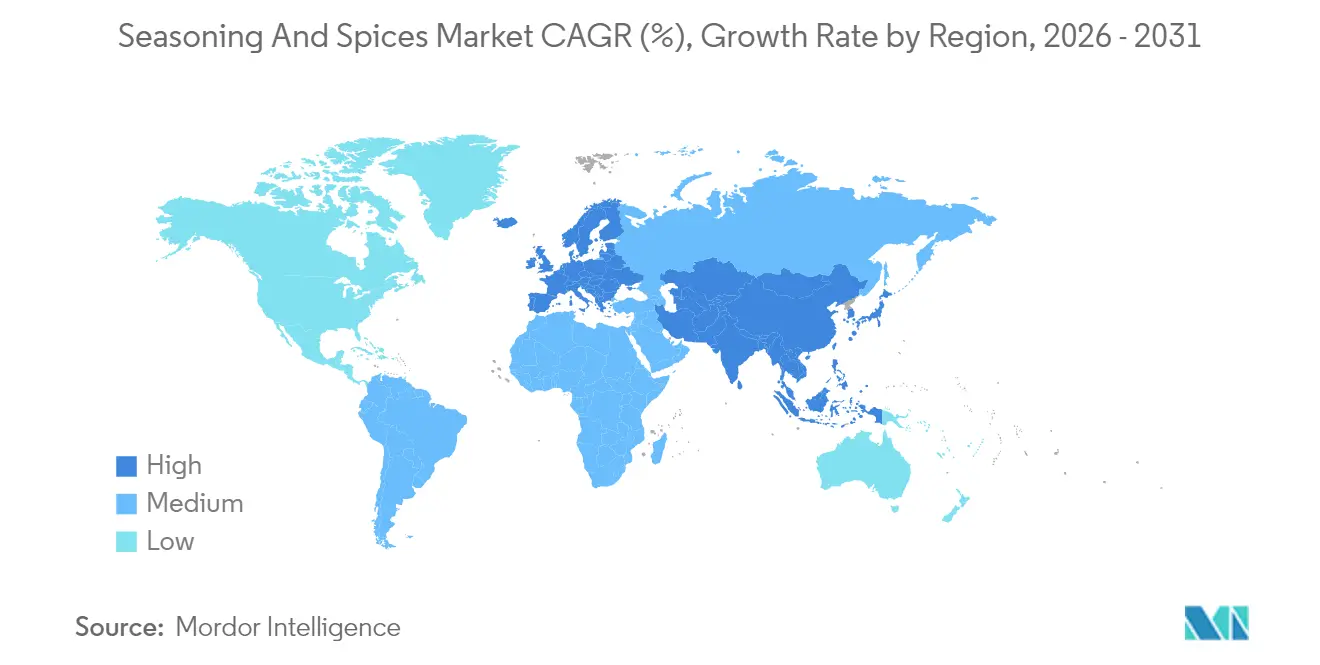

- By geography, Asia-Pacific commanded 38.28% of the spices and seasonings market share in 2025; Europe exhibits the highest growth outlook at a 6.61% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Seasoning and Spices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth of processed and convenience food surges demand for seasoning and spices | +1.2% | Global, strongest in North America and Asia-Pacific | Medium term (2-4 years) |

| Growing trend for organic and clean-label spice products | +0.8% | Europe and North America, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Increasing awareness of health benefits associated with spices drives growth | +0.7% | Global, led by developed markets | Long term (≥ 4 years) |

| Rise in consumption of ethnic food among consumers surges demand | +0.9% | North America and Europe, spillover to Asia-Pacific urban centers | Medium term (2-4 years) |

| Expansion of quick-service restaurants and foodservice chains boosts demand | +0.6% | Global, emphasis on emerging markets | Short term (≤ 2 years) |

| Technological advancements in spice processing and packaging | +0.4% | Global, concentrated in manufacturing hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growth of Processed And Convenience Food Surges Demand for Seasoning and Spices

Increasing demand for spice blends across various food applications, including savory snacks, ready meals, and sauces, is driving robust growth in the global market. The market's expansion is closely tied to the growth of the processed and convenience food industry, where spices are essential ingredients for flavor enhancement. Consumer preferences, particularly in urban areas with busy lifestyles, have led to increased consumption of ready-to-eat meals and frozen foods, prompting food manufacturers to incorporate diverse spice blends for unique flavor profiles. Complex flavor combinations, especially those featuring turmeric, coriander, and warm brown spices, are gaining significant traction in global markets. This trend is reflected in international trade data, with the Observatory of Economic Complexity reporting that global spice trade reached USD 3.57 billion in 2023, marking an 8.1% increase from USD 3.3 billion in 2022 [1]Source: Observatory of Economic Complexity, “Spices,” oec.world. The sector has maintained steady growth, with a five-year annualized growth rate of 3.96%. As consumer demand for diverse and authentic flavors continues to rise, the spice blend market is expected to maintain its growth trajectory, offering opportunities for both established players and new entrants in the market.

Growing Trend For Organic And Clean-Label Spice Products

The clean label trend has evolved significantly in the spice industry, extending beyond basic ingredients to encompass flavorings and extracts, with natural herbs and spices gaining prominence.Growing consumer preference for premium and functional spices such as Cardamom is further supporting demand across food, beverage, and health-focused applications. This transformation is primarily driven by increasing consumer awareness and demand for transparency in food products, leading to structural changes in spice procurement and certification processes. According to FAO's World of Organic Agriculture 2024 report, organic agriculture is now practiced in 188 countries, with over 96 million hectares of agricultural land managed organically by at least 4.5 million farmers [2]Source: FiBL & IFOAM, “The World of Organic Agriculture 2024,” fao.org. The impact is particularly evident in the replacement of synthetic flavor enhancers with natural spice extracts, creating opportunities for suppliers of standardized natural alternatives. As consumers demonstrate a willingness to pay premium prices for certified organic and clean-label spices, manufacturers are expanding their organic product portfolios, implementing stricter quality control measures, and improving their sourcing practices. This shift has also prompted companies to provide detailed information about origin, processing methods, and sustainability initiatives, aligning with consumer preferences for minimally processed products without artificial additives.

Increasing Awareness of Health Benefits Associated With Spices Drives Growth

The intersection of spice consumption with preventive healthcare is creating new market segments that extend beyond traditional culinary applications into functional food and nutraceutical categories. Consumer awareness of spices' anti-inflammatory and antioxidant properties is driving product innovation in health-focused formulations, particularly in markets with aging populations and rising healthcare costs. According to the National Library of Medicine supports the beneficial effects of culinary doses of spices like cardamom, cinnamon, chili, fenugreek, garlic, ginger, nigella seeds, and turmeric in preventing and treating metabolic syndrome and associated disorders [3]Source: Na-Young Park et al., “Metabolic Syndrome Modification by Culinary Spices,” National Library of Medicine, ncbi.nlm.nih.gov . The COVID-19 pandemic accelerated this trend as consumers sought immune-boosting ingredients, leading to increased consumption of spices like ginger, garlic, and black pepper. Specific spices demonstrate targeted health benefits, such as cardamom, ginger, and turmeric show potential for inflammation management, whereas garlic, ginger, and turmeric for blood lipid control, and cinnamon, ginger, and fenugreek for blood glucose regulation. This growing recognition of spices as natural sources of beneficial compounds has expanded market opportunities, particularly in dietary supplements and functional foods.

Rise in Consumption of Ethnic Food Among Consumers Surges Demand

The increasing popularity of ethnic and international cuisines among consumers worldwide is significantly influencing the spices and seasonings market. Consumers are actively exploring diverse food cultures, particularly Asian, Mediterranean, and South American cuisines, which traditionally incorporate various spices and seasonings. Social media platforms and cooking shows have enhanced consumer awareness about different culinary traditions and ingredients. Additionally, the growing immigrant population in various regions has introduced local communities to new flavors and cooking styles. The rising number of international restaurants and the availability of ethnic food products in supermarkets have made these flavors more accessible to consumers. This shift in consumer preferences toward authentic global flavors has prompted food manufacturers to expand their spice and seasoning product portfolios to meet the increasing demand.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price volatility of raw materials due to climate and supply issues | -0.9% | Global origin belts | Short term (≤ 2 years) |

| Adulteration and quality concerns in unregulated markets | -0.6% | Global ports and transit corridors | Medium term (2-4 years) |

| High cost of organic and premium spice variants | -0.4% | Developing regions | Long term (≥ 4 years) |

| Limited shelf life of certain natural spices restricts growth | -0.3% | Origin-specific species such as vanilla, cardamom | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Price Volatility of Raw Materials Due To Climate And Supply Issues

The spices and seasonings market faces significant challenges due to the volatility in raw material prices, primarily driven by climate change and supply chain disruptions. Extreme weather conditions, including droughts, floods, and unpredictable rainfall patterns, directly affect crop yields and quality of spices like black pepper, cardamom, and vanilla. Supply chain issues, such as transportation delays, labor shortages, and geopolitical tensions, further contribute to price fluctuations. These factors force manufacturers to maintain higher inventory levels and adjust their procurement strategies, impacting their operational costs and profit margins. Additionally, the seasonality of spice cultivation and harvesting creates periodic supply-demand imbalances, leading to price variations throughout the year. The industry's heavy reliance on specific geographic regions for certain spices also increases vulnerability to regional climate events and local market dynamics.

Adulteration And Quality Concerns In Unregulated Markets

Adulteration in the spices and seasonings market poses a significant challenge, particularly due to the high value of these products and complex global supply chains that make authenticity verification difficult. The absence of stringent quality control measures in developing regions has led to widespread contamination issues, including the presence of foreign materials, artificial colors, and prohibited substances. Local vendors often compromise quality standards to maintain competitive pricing, resulting in substandard products entering the market. The lack of proper testing facilities and enforcement mechanisms in many regions further exacerbates this problem. These quality concerns create significant consumer trust issues that can impact entire market segments, ultimately constraining the market's growth potential. The vulnerability of spices to adulteration and the difficulty in tracing their origins through complex supply chains continue to challenge industry stakeholders.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Spices Drive Volume While Herbs Capture Premium Growth

Spices dominate the market with a 55.02% share in 2025, underscoring their essential role in global cuisine and food processing applications. This leadership position is built on the universal demand for fundamental spices such as pepper, turmeric, and chili across diverse culinary traditions and industrial uses. The segment's strength is complemented by the rapid growth of herbs and seasonings, which are projected to expand at a 6.56% CAGR through 2031. Meanwhile, salt and salt substitutes occupy a specialized segment that addresses health-conscious consumer preferences and regulatory requirements for reduced sodium content in processed foods.

The herbs and seasonings category exemplifies the convergence of health consciousness and culinary sophistication in modern food consumption patterns. This segment's growth is propelled by increasing consumer demand for natural flavor enhancement solutions and the ongoing premiumization of convenience foods. The expansion reflects a broader market shift toward products that deliver both complex flavor profiles and perceived health benefits, indicating a sustained trend in consumer preferences for wholesome, flavorful food options.

By Category: Organic Segment Outpaces Conventional Growth Despite Smaller Base

Conventional products command a dominant 80.47% market share in 2025, leveraging their established distribution networks and price competitiveness across mass market applications. The segment maintains its strong position through scale economies and established customer relationships, particularly in foodservice and industrial applications where cost considerations often outweigh organic certification. However, the organic segment's robust 7.25% CAGR significantly outpaces the overall market growth rate, signaling an emerging shift in consumer preferences toward premium, health-conscious offerings.

The organic segment's expansion is driven by increasing retail availability and the development of dedicated supply chains that ensure consistent quality and pricing. This growth differential reflects evolving consumer priorities and their willingness to pay premiums for perceived quality and environmental benefits. The narrowing growth gap between conventional and organic segments indicates that organic products are steadily transitioning from niche to mainstream acceptance, particularly among younger consumers and in developed markets.

By Form: Ground Products Lead While Innovation Drives Diversification

Ground and powder products dominate the spice market with a 26.08% share in 2025 and are projected to grow at a 5.63% CAGR through 2031, driven by their versatility across consumer and industrial applications. This segment's prominence stems from its suitability for mass production, extended shelf life, and seamless integration into processed foods. While whole spices maintain their position in foodservice operations and among consumers seeking intense flavors, the ground segment's growth reflects the increasing industrialization of food production and consumer demand for convenience in home cooking. The market also includes crushed spices, flakes, and paste forms, which represent innovative formats designed for specific applications and convenience.

Technological advancements in spice processing, particularly in grinding techniques and packaging innovations, enable manufacturers to preserve flavor integrity while extending product shelf life. The development of paste and liquid formats addresses the foodservice industry's requirements for products that integrate easily into large-scale production processes while ensuring consistent flavor delivery. These innovations, combined with improved preservation methods, support the ground segment's market leadership while meeting evolving consumer and industrial needs for quality, convenience, and reliability in spice products.

By Application: Meat Segment Dominates While Savory Snacks Drive Growth

Meat and seafood applications dominate the spices market with a 28.88% share in 2025, underscoring their essential role in protein preparation across global cuisines and processed meat products. The segment's prominence stems from the expansion of quick-service restaurants and the industrialization of meat processing, where standardized spice blends ensure consistent flavor delivery. Additionally, this segment's growth is further propelled by the increasing global protein consumption and the emergence of plant-based alternatives that require sophisticated seasoning to achieve authentic taste profiles.

The market landscape is experiencing a notable shift as savory snacks emerge as the fastest-growing application segment, projected to grow at a 6.85% CAGR through 2031. This rapid growth reflects evolving consumption patterns and the snack industry's continuous innovation in flavor development. While traditional applications such as bakery and confectionery, soups and noodles, and sauces maintain steady growth patterns, the savory snacks segment's acceleration is primarily driven by consumer demand for bold flavors and the ongoing premiumization of snack foods.

Geography Analysis

Asia-Pacific holds the largest market share at 38.28% in 2025, primarily due to India's position as the world's leading spice producer and the region's deeply rooted spice consumption culture. The region's competitive advantage stems from its direct access to major spice-producing areas, well-established supply chain networks, and a growing middle-class population. This combination of factors creates a robust market environment that continues to strengthen the region's position in the global spice trade. Moreover, Asia-Pacific, celebrated for its deep-rooted culinary traditions, weaves spices into its age-old recipes and everyday cooking, echoing a rich gastronomic legacy.

Europe demonstrates the highest growth potential with a projected CAGR of 6.61% through 2031, driven by strict sustainability requirements and increasing demand for clean-label products. The region's emphasis on traceability and organic certification creates opportunities for premium product positioning and higher profit margins. While North America maintains steady growth through ethnic food adoption and foodservice expansion, Europe's trajectory reflects a fundamental shift toward quality-focused consumption patterns.

South America and the Middle East and Africa represent emerging markets with considerable growth potential, supported by increasing urbanization rates and rising consumer incomes. These regions are experiencing significant development in their food processing industries, which further drives spice demand. The global spice market's geographic distribution highlights distinct regional variations in consumption patterns, regulatory frameworks, and competitive landscapes, while demonstrating the universal appeal and necessity of spices in global cuisine.

Competitive Landscape

The spices and seasonings market demonstrates moderate fragmentation, creating opportunities for both established companies and new entrants to gain market share through distinct strategies. The industry landscape includes global leaders such as Kerry Group, Olam Group, Sensient Technologies, and Cargill Incorporated, alongside regional specialists like MDH Spices, who maintain strong positions in key origin markets. The competitive environment is shaped by vertical integration strategies, sustainability initiatives, and technology adoption, particularly focusing on supply chain transparency and operational efficiency.

The industry exhibits a clear trend toward consolidation and partnership-driven growth, with companies actively pursuing vertical integration and collaborative innovation to enhance their market positions. Companies are increasingly focusing on integrating technology, particularly in processing automation and supply chain transparency, to achieve competitive advantages through digital transformation initiatives.

Emerging opportunities in the market center on the convergence of health, sustainability, and authentic flavor experiences, creating potential for companies to position spices as functional ingredients rather than simple taste enhancers. The increasing demand for ethnic flavors and clean-label products has opened new avenues for specialized suppliers who can deliver authentic taste profiles while meeting sustainability and traceability requirements. This trend particularly benefits suppliers who can combine traditional authenticity with modern sustainability practices and transparent supply chain operations.

Seasoning and Spices Industry Leaders

Ajinomoto Co., Inc.

Olam Group

Kerry Group Plc

Cargill Incorporated

Sensient Technologies

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: McCormick introduced Aji Amarillo Seasoning, available temporarily through online purchases. Aji Amarillo, meaning 'yellow chile pepper,' is a traditional Peruvian pepper native to South America and essential in Peruvian cooking.

- November 2024: Afia, an Eastern Mediterranean food company, has launched a new line of Mediterranean spices. The product range includes premium blends such as Za'atar, Shawarma, and Baharat 7 Spice. The Mediterranean Pantry Spice Gift Set offers individual spices including Sumac, Dried Mint, and Aleppo Pepper.

- August 2024: The Baltimore Ravens partnered with McCormick to create a new seasoning called Blackbird Spice. The seasoning will be featured on stadium menu items, including popcorn.

Global Seasoning and Spices Market Report Scope

Spices and seasonings are widely used to add flavor, aroma, color, and taste to food & beverages, and sometimes act as preservatives or antibacterial agents. The global seasoning and spices market (henceforth referred to as the market studied) is segmented by product type, application, and geography. Based on product type, the market is segmented into salt and salt substitutes, herbs and seasonings, and spices. Based on herbs and seasonings, the market is further sub-segmented into thyme, basil, oregano, parsley, and other herbs. Based on spices, the market is further segmented into pepper, cardamom, cinnamon, clove, nutmeg, turmeric, and other spices. Based on the application, the market is segmented into bakery and confectionery, soup, noodles, pasta, meat and seafood, sauces, salads, and dressing, savory snacks, and other applications. By geography, the market is segmented into North America, Asia-Pacific, South America, Europe, Middle East & Africa. For each segment, the market sizing and forecasts have been done on the basis of value (in USD million).

By Product Type

| Salt and Salt Substitutes | |

| Herbs and Seasonings | Thyme |

| Basil | |

| Oregano | |

| Parsley | |

| Mint | |

| Other Herbs | |

| Spices | Pepper |

| Cardamom | |

| Cinnamon | |

| Clove | |

| Nutmeg | |

| Chilli Pepper | |

| Sesame | |

| Turmeric | |

| Other Spices |

By Category

| Conventional |

| Organic |

By Form

| Whole |

| Ground/Powder |

| Others (crushed, flakes, paste, etc.) |

By Application

| Bakery and Confectionery |

| Soups, Noodles and Pasta |

| Meat and Seafood |

| Sauces, Salads and Dressings |

| Savory Snacks |

| Other Applications |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Salt and Salt Substitutes | |

| Herbs and Seasonings | Thyme | |

| Basil | ||

| Oregano | ||

| Parsley | ||

| Mint | ||

| Other Herbs | ||

| Spices | Pepper | |

| Cardamom | ||

| Cinnamon | ||

| Clove | ||

| Nutmeg | ||

| Chilli Pepper | ||

| Sesame | ||

| Turmeric | ||

| Other Spices | ||

| By Category | Conventional | |

| Organic | ||

| By Form | Whole | |

| Ground/Powder | ||

| Others (crushed, flakes, paste, etc.) | ||

| By Application | Bakery and Confectionery | |

| Soups, Noodles and Pasta | ||

| Meat and Seafood | ||

| Sauces, Salads and Dressings | ||

| Savory Snacks | ||

| Other Applications | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the spices and seasonings market?

The market stands at USD 21.99 billion in 2026 with a projected rise to USD 28.21 billion by 2031.

Which region leads the spices and seasonings market?

Asia-Pacific holds the largest share at 38.28% due to substantial production and strong domestic consumption.

Which segment is growing fastest within the market?

Savory snacks register the highest application CAGR at 6.85% through 2031, driven by flavor innovation

How significant is organic adoption in spices?

Organic products, though forming a smaller base, grow at 7.25% CAGR, outpacing the broader market.

Page last updated on: