Market Overview

| Study Period | 2021 - 2031 |

|---|---|

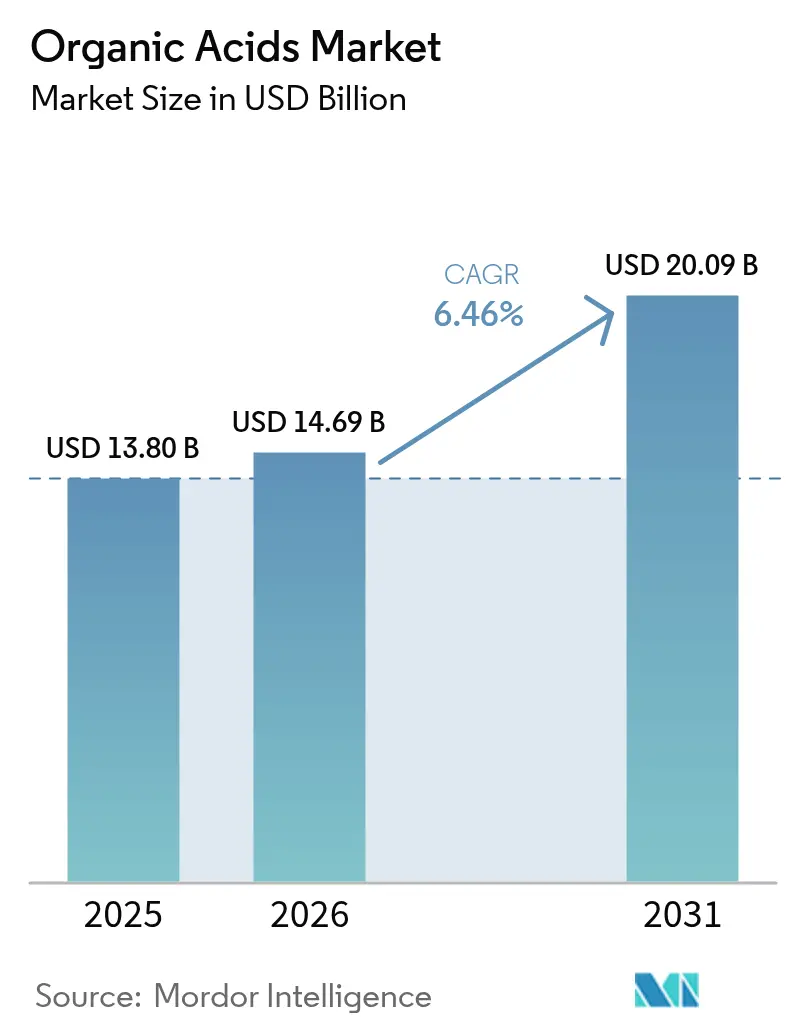

| Market Size (2026) | USD 14.69 Billion |

| Market Size (2031) | USD 20.09 Billion |

| Growth Rate (2026 - 2031) | 6.46% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Organic Acids Market Analysis by Mordor Intelligence

The organic acids market size in 2026 is estimated at USD 14.69 billion, growing from 2025 value of USD 13.80 billion with 2031 projections showing USD 20.09 billion, growing at 6.46% CAGR over 2026-2031.This growth is largely driven by a notable transition from petrochemical methods to bio-based fermentation processes, alongside an increasing demand for clean-label products across food, polymer, and pharmaceutical sectors. Organic acids, which include acetic acid, citric acid, lactic acid, and others, play a crucial role in various applications such as food preservation, flavor enhancement, and pH regulation. The shift toward bio-based production methods is gaining traction due to environmental concerns and the need for sustainable alternatives. Additionally, the rising consumer preference for natural and clean-label products is pushing manufacturers to adopt organic acids in food and beverage formulations. In the polymer and pharmaceutical industries, organic acids are increasingly used for their functional properties, such as acting as intermediates in chemical synthesis and enhancing product performance. This growing adoption across diverse value chains underscores the market's robust expansion during the forecast period.

Key Report Takeaways

- By product type, acetic acid led with 33.72% of organic acids market share in 2025, while succinic acid is forecast to expand at a 9.52% CAGR through 2031.

- By source, petrochemical routes held 60.98% revenue share in 2025, whereas bio-based acids are projected to grow at an 10.93% CAGR to 2031.

- By form, liquid accounted for 58.21% revenue share in 2025, while dry/powder forms are projected to grow at a 6.44% CAGR to 2031.

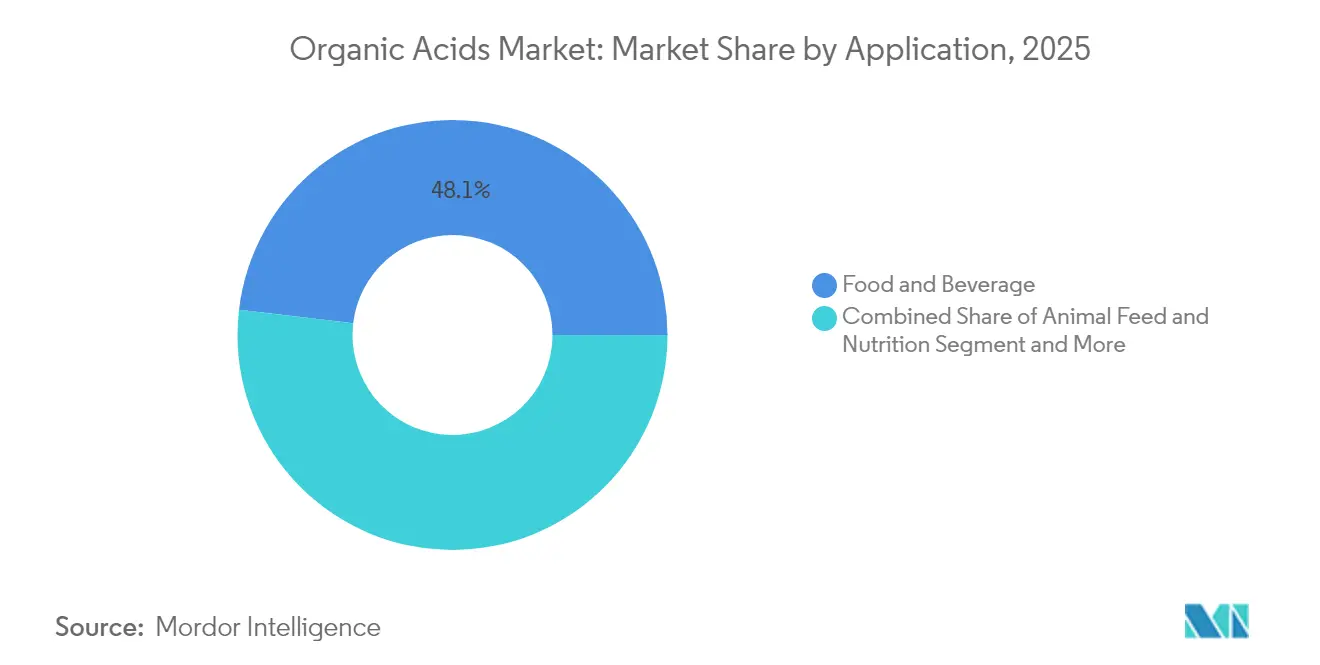

- By application, food and beverages accounted for 48.12% share of the organic acids market size in 2025; polymers and bioplastics are advancing at an 11.32% CAGR to 2031.

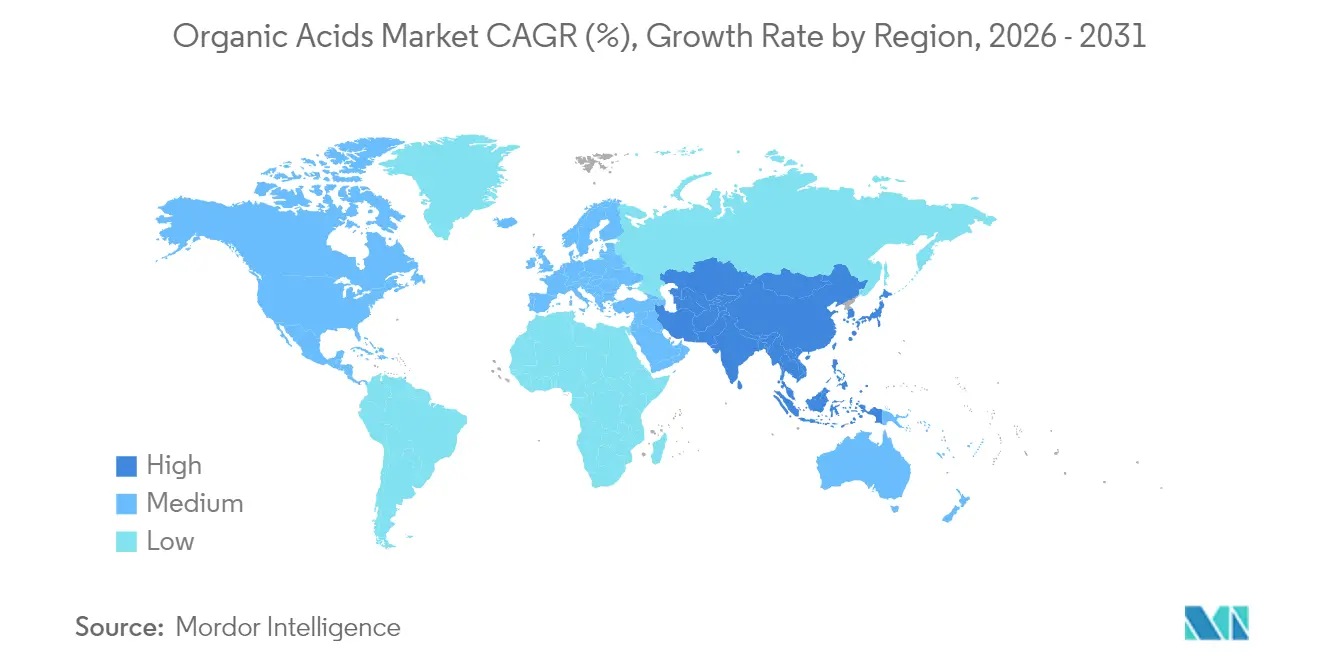

- By geography, Asia-Pacific commanded 30.08% revenue share in 2025 and is forecast to record a 9.29% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Organic Acids Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Uptake of Acetic Acid in Vinyl-Acetate-Monomer for Solar-EVA Films | +1.2% | Global, with concentration in Asia-Pacific and North America | Medium term (2-4 years) |

| Pharmaceutical‐grade Lactic Acid Demand for Injectable Drug Formulations | +0.8% | North America and Europe, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Expansion of Citric-acid-based Natural Preservatives in Clean-Label Beverages | +0.9% | Global, led by North America and Europe | Short term (≤ 2 years) |

| Growth of Succinic Acid as a Building Block for Bio-PBS and Bio-BDO | +1.1% | North America and Europe, with emerging presence in Asia-Pacific | Long term (≥ 4 years) |

| Feed‐grade Formic and Propionic Acids Adoption for ASF-Free Swine Diets | +0.6% | Global, with emphasis on Asia-Pacific and Europe | Medium term (2-4 years) |

| Use in Animal Feed as Antibiotic Alternatives | +0.7% | Global, particularly in regions with antibiotic restrictions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Uptake of Acetic Acid in Vinyl-Acetate-Monomer for Solar-EVA Films

The rapid growth of the photovoltaic industry has significantly increased the demand for acetic acid in the production of vinyl acetate monomers (VAM). EVA encapsulant films, which are essential for improving the durability and efficiency of solar panels, drive this demand. Producers can now manufacture commercial-grade VAM from renewable feedstocks by utilizing the non-catalytic cracking of soybean oil. This innovative process generates acetic acid as a valuable co-product that complies with the stringent quality requirements of the solar industry. By adopting this bio-based production pathway, manufacturers address sustainability mandates while diversifying supply chains to reduce reliance on petrochemical-derived VAM. Additionally, integrating ethylene derived from renewable ethanol with bio-based acetic acid establishes a fully sustainable VAM production route. This advancement enables organic acid producers to capitalize on premium pricing opportunities in the rapidly expanding solar market.

Pharmaceutical‐grade Lactic Acid Demand for Injectable Drug Formulations

The demand for pharmaceutical-grade lactic acid is a significant driver in the organic acids market, particularly due to its increasing application in injectable drug formulations. Lactic acid, known for its biocompatibility and biodegradability, is widely used in the pharmaceutical industry to enhance drug delivery systems. According to the U.S. Food and Drug Administration (FDA), the adoption of lactic acid in drug formulations aligns with stringent safety and efficacy standards, making it a preferred choice for injectable drugs [1]Source: United States Food and Drug Administration, "Drug Therapeutics & Regulation in the U.S.", www.fda.gov. Additionally, the World Health Organization emphasizes the importance of such biocompatible compounds in improving patient outcomes, especially in critical care medications. Moreover, the increasing prevalence of chronic diseases such as diabetes and cardiovascular disorders has led to a surge in demand for injectable drugs, further driving the need for pharmaceutical-grade lactic acid. According to the Centers for Disease Control and Prevention (CDC), the prevalence of total diabetes was 15.8% in all adults in the United States in 2023[2]Source: Centers for Disease Control and Prevention, "National Diabetes Statistics Report", www.cdc.gov, highlighting the growing need for effective drug delivery systems. This growth is expected to directly impact the demand for lactic acid in pharmaceutical applications.

Expansion of Citric-acid-based Natural Preservatives in Clean-Label Beverages

The expansion of citric-acid-based natural preservatives is emerging as a significant driver in the organic acids market. These preservatives are increasingly preferred in clean-label beverages due to their natural origin and multifunctional properties, such as enhancing flavor, maintaining pH balance, and extending shelf life. The demand for clean-label products has grown significantly over the last few years, driven by consumer preference for transparency and natural ingredients. Research from CBI, the Ministry of Foreign Affairs, highlights this trend, projecting that clean-label products will rise from constituting 52% of portfolios in 2021 to over 70% in 2025 and 2026 [3]Source: CBI Ministry of Foreign Affairs, "Which trends offer opportunities," www.cbi.eu.. Additionally, the Food and Agriculture Organization (FAO) highlights that citric acid is one of the most widely used organic acids globally, with applications spanning food, beverages, and pharmaceuticals. This trend aligns with the growing regulatory emphasis on reducing synthetic additives in consumables, further propelling the adoption of citric-acid-based solutions in the beverage industry.

Growth of Succinic Acid as a Building Block for Bio-PBS and Bio-BDO

The growing demand for succinic acid as a building block for bio-based polymers, such as Bio-PBS (Polybutylene Succinate) and Bio-BDO (1,4-Butanediol), is driving the organic acids market. Succinic acid, derived from renewable feedstocks, is increasingly being utilized in the production of biodegradable and sustainable materials. This trend aligns with the global shift toward reducing dependency on fossil fuels and minimizing environmental impact. The use of succinic acid in Bio-PBS enhances the polymer's biodegradability and mechanical properties, making it a preferred choice in packaging, agriculture, and other applications. Similarly, its role in producing Bio-BDO, a key intermediate for various industrial applications, further underscores its importance in the bio-based chemicals sector. The rising adoption of bio-based alternatives across industries is expected to propel the demand for succinic acid, thereby contributing significantly to the growth of the organic acids market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent VOC Directives Limiting Petro-based Acrylic and Adipic Acids | -0.9% | North America and Europe, with emerging regulations in Asia-Pacific | Short term (≤ 2 years) |

| Over-capacity and Price Compression in Chinese Low-purity Citric Acid | -0.7% | Global, with primary impact in Asia-Pacific | Medium term (2-4 years) |

| Environmental Concerns with Synthetic Acids Hindering Market Growth | -0.5% | Global, with stricter enforcement in developed markets | Long term (≥ 4 years) |

| Technological and Infrastructural Barriers Hampering Market Growth | -0.8% | Global, with acute challenges in developing markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent VOC Directives Limiting Petro-based Acrylic and Adipic Acids

The organic acid market is experiencing significant restraint due to stringent Volatile Organic Compound (VOC) directives imposed on petro-based acrylic and adipic acids. These directives aim to reduce environmental pollution and promote sustainability by limiting the use of petrochemical derivatives that contribute to VOC emissions. VOCs are known to have adverse effects on both human health and the environment, including contributing to ground-level ozone formation and air quality degradation. As a result, regulatory bodies across various regions, including North America, Europe, and Asia-Pacific, have implemented strict guidelines to curb VOC emissions, directly impacting the production and usage of petro-based acrylic and adipic acids. Manufacturers in the organic acid market are facing challenges in complying with these regulations, which may lead to increased production costs due to the need for advanced technologies and processes to meet compliance standards. Additionally, the restrictions are driving the industry to explore and adopt alternative raw materials, such as bio-based feedstocks, which are more environmentally friendly but often come with higher costs and scalability issues.

Environmental Concerns with Synthetic Acids Hindering the Market Growth

Environmental concerns regarding the use of synthetic acids are significantly restraining the growth of the organic acid market. The production and disposal processes of synthetic acids often result in adverse environmental impacts, such as water and soil contamination, greenhouse gas emissions, and ecological degradation. These environmental risks have led to the implementation of stringent regulations by governments and increased monitoring by environmental organizations, creating additional compliance burdens for manufacturers. Furthermore, the growing awareness among consumers about the environmental footprint of synthetic acids has shifted demand toward more sustainable and eco-friendly alternatives, such as organic acids. This shift has intensified the pressure on manufacturers to innovate and adopt greener production methods, which often require substantial investments and longer timelines. Consequently, these factors collectively hinder the growth trajectory of the organic acid market, posing significant challenges for stakeholders across the value chain.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Acetic Acid Dominates While Succinic Surges

In 2025, acetic acid holds a dominant 33.72% market share in the organic acids market, maintaining its leadership position. This dominance is attributed to its extensive applications across various industries, including textiles, food and beverages, and pharmaceuticals. Acetic acid plays a critical role in the production of vinyl acetate monomer (VAM), which is a key precursor for manufacturing adhesives, paints, and coatings. Additionally, its use in the production of acetic anhydride, terephthalic acid, and acetate esters further enhances its demand. The compound's versatility and widespread demand across end-user industries continue to drive its growth and solidify its position as a market leader. The increasing focus on industrial applications and the rising demand for VAM in emerging economies are expected to further bolster the growth of acetic acid in the coming years.

Succinic acid, on the other hand, is emerging as the fastest-growing segment in the organic acids market. It is projected to register a robust CAGR of 9.52% during the forecast period of 2026 to 2031. This growth is primarily fueled by its increasing adoption as a building block for biodegradable polymers, which are gaining traction due to rising environmental concerns and regulatory support for sustainable materials. Succinic acid is also used in the production of resins, coatings, and personal care products, further contributing to its expanding market presence. Moreover, advancements in bio-based production technologies have made succinic acid a cost-effective and renewable alternative to petroleum-based chemicals.

By Source: Bio-based Segment Outpaces Petrochemical Origins

In 2025, petrochemical sources dominated the organic acids market, holding a significant 60.98% share. These sources continue to play a crucial role in meeting the high demand for organic acids across various industries, including food and beverages, pharmaceuticals, and chemicals. The established infrastructure for petrochemical production and the relatively lower production costs contribute to their strong market position. However, concerns regarding environmental sustainability and fluctuating crude oil prices may pose challenges to the growth of petrochemical-based organic acids in the coming years.

On the other hand, bio-based sources of organic acids are expected to grow at an impressive CAGR of 10.93% during the forecast period. This growth is driven by increasing consumer preference for sustainable and eco-friendly products, along with stringent environmental regulations encouraging the adoption of renewable resources. Bio-based organic acids are derived from renewable feedstocks such as corn, sugarcane, and other biomass, making them a more sustainable alternative to petrochemical sources. Advancements in biotechnology and fermentation processes are further enhancing the efficiency and scalability of bio-based organic acid production, positioning this segment as a key growth driver in the market.

By Application: Food and Beverages Lead While Polymers and Bioplastics Surge

In 2025, the food and beverage sector dominates the organic acids market, accounting for a significant 48.12% share. Organic acids are extensively utilized in this sector due to their multifunctional properties, including preservation, flavor enhancement, and pH regulation. These acids help extend the shelf life of products, maintain their quality, and improve taste, making them indispensable in processed foods, beverages, and ready-to-eat meals. The growing consumer preference for convenience foods and beverages, coupled with the increasing focus on food safety and quality, continues to drive the demand for organic acids in this sector. Additionally, the rising trend of clean-label products and natural ingredients has further boosted the adoption of organic acids, as they align with consumer demand for healthier and more transparent food options.

On the other hand, the polymers and bioplastics sector is emerging as a high-growth segment in the organic acids market. This sector is projected to register an impressive 11.32% CAGR from 2026 to 2031, fueled by the rising demand for biodegradable and sustainable packaging solutions. Organic acids serve as key raw materials in the production of bioplastics, offering an eco-friendly alternative to conventional plastics. The increasing emphasis on reducing plastic waste, supported by stringent environmental regulations and growing consumer awareness, is expected to propel the adoption of organic acids in this sector during the forecast period. Furthermore, advancements in bioplastic technologies and the growing investments in research and development are enhancing the efficiency and scalability of bioplastic production.

By Form: Liquid Dominates While Dry Formats Gain Ground

In 2025, liquid organic acids dominate the organic acids market with a 58.21% market share. Their widespread adoption is attributed to their ease of handling, which simplifies industrial processes, and their lower production costs compared to other formats. These advantages make liquid organic acids a preferred choice across various industries, including food and beverages, pharmaceuticals, and chemicals. The consistent demand for liquid organic acids is expected to sustain their significant market share during the forecast period, driven by their versatility and cost-effectiveness in large-scale applications. Furthermore, advancements in production technologies are likely to enhance the efficiency and quality of liquid organic acids, further solidifying their position in the market.

On the other hand, dry or powdered organic acids are projected to witness substantial growth from 2026 to 2031, with a robust CAGR of 6.44%. This growth is fueled by their longer shelf life, ease of transportation, and suitability for applications requiring precise dosing, such as animal feed and food preservation. The powdered format's ability to maintain stability under varying environmental conditions makes it an attractive option for manufacturers. Additionally, the increasing focus on sustainable and eco-friendly solutions has spurred interest in bio-plastic applications, where organic acids play a crucial role as raw materials. The rising demand for powdered formats and bio-plastic applications is expected to drive innovation and expand the market's scope during the forecast period.

Geography Analysis

In 2025, Asia-Pacific dominated the global organic acids market, holding the largest regional market share of 30.08% and registering the fastest growth with a projected CAGR of 9.29% through 2031. This dual leadership stems from the region's robust manufacturing ecosystem and the rising consumption patterns of its expanding middle-class population. The demand for organic acids is particularly strong in food, pharmaceutical, and industrial applications, driven by increasing urbanization and changing consumer preferences. China, as a key producer in the region, faces challenges such as overcapacity and ongoing trade disputes, which could impact its market dynamics. However, India and Southeast Asian countries are emerging as significant growth contributors, supported by rapid economic development, favorable government policies, and alignment with global sustainability standards.

North America continues to maintain a strong foothold in the organic acids market, underpinned by its technological advancements in bio-based production and a regulatory framework that prioritizes sustainability and high-quality standards. The region has witnessed substantial investments in fermentation capacity, addressing previous infrastructure gaps and enabling more efficient production processes. The demand for organic acids in North America is further bolstered by the growing adoption of bio-based alternatives across various industries, including food and beverages, pharmaceuticals, and agriculture. The region's focus on innovation and sustainability has positioned it as a leader in the development of advanced organic acid solutions, catering to both domestic and international markets. These factors ensure North America's continued prominence in the global market landscape.

Europe, with its mature organic acids market, emphasizes premium applications and strict regulatory compliance. The region's stringent environmental standards create opportunities for bio-based producers, as industries increasingly shift towards sustainable and eco-friendly solutions.The demand for organic acids in Europe is driven by their applications in food preservation, pharmaceuticals, and industrial processes, where quality and sustainability are paramount. Meanwhile, South America and the Middle East & Africa represent emerging opportunities in the global organic acids market. These regions benefit from economic development and abundant agricultural resources, which provide a strong foundation for organic acid production and consumption.

Competitive Landscape

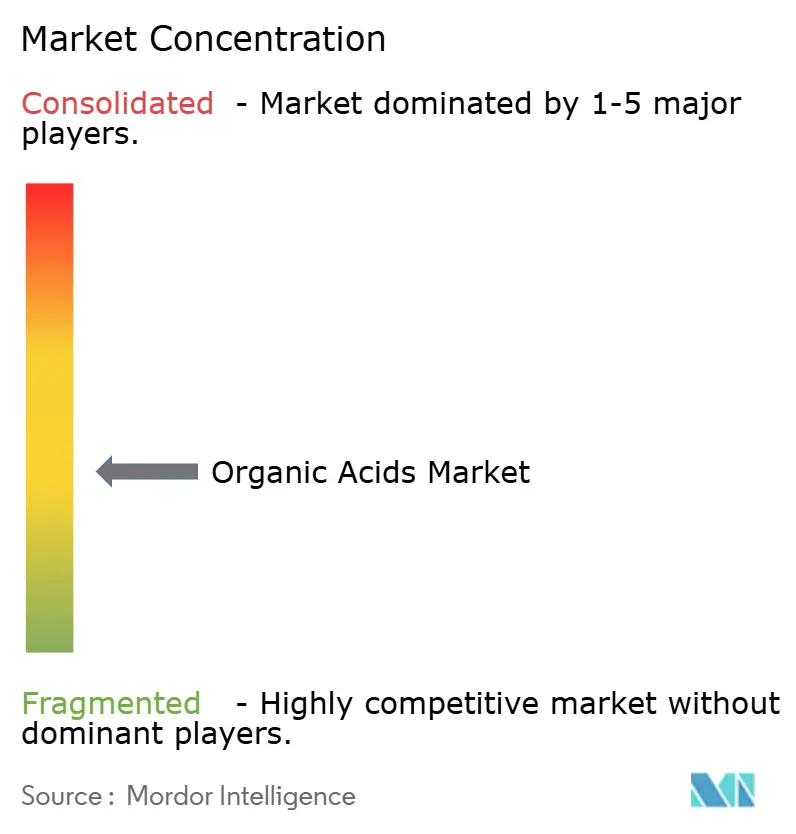

The organic acids market, on a global scale, demonstrates moderate fragmentation. This level of fragmentation creates significant opportunities for market share consolidation, particularly through strategic acquisitions and capacity expansions. Companies are leveraging advanced technological capabilities and expanding their geographic presence to strengthen their competitive positions. Established players, such as BASF, are focusing on sustainable production technologies to align with evolving consumer preferences and regulatory requirements, thereby maintaining their market leadership. The market's competitive nature is further fueled by the increasing demand for organic acids across industries such as food and beverages, pharmaceuticals, and agriculture, which drives companies to innovate and differentiate their offerings.

Industry leaders are adopting differentiated strategies to stay ahead in this competitive landscape. BASF, for instance, is heavily investing in innovative and sustainable production methods to reduce environmental impact while meeting the growing demand for organic acids across various applications. These strategies not only enhance operational efficiency but also cater to the increasing emphasis on sustainability within the market. Additionally, established players are focusing on expanding their production capacities and entering new markets to capitalize on the rising demand in emerging economies. Such initiatives by key players are setting benchmarks for the industry, compelling competitors to innovate and adapt to remain relevant.

Meanwhile, emerging disruptors are challenging the dominance of incumbents by leveraging novel production technologies and forming strategic partnerships. Solugen, a notable example, has collaborated with ADM to produce bio-based organic acids using proprietary fermentation processes. These processes are designed to eliminate traditional CO2 emissions, offering a more environmentally friendly alternative. Such advancements by new entrants are intensifying competition and driving the market toward more sustainable and innovative solutions, reshaping the competitive dynamics of the global organic acids market. Additionally, these disruptors are focusing on niche applications and customized solutions to cater to specific customer needs, further diversifying the competitive landscape.

Organic Acids Industry Leaders

-

BASF SE

-

Cargill, Incorporated

-

Archer Daniels Midland Company

-

Nippon Shokubai Co., Ltd.

-

DSM-Firmenich AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Solugen broke ground on a biomanufacturing facility in Marshall, Minnesota, in partnership with ADM, with production capacity of up to 120 kilotonnes per annum for low-carbon organic acids, expected to avoid emissions of up to 18 million kilograms of CO2 annually.

- November 2024: BASF, a global leader in the chemical industry, has partnered with Acies Bio to strengthen its position in the bio-based chemicals market. This collaboration focuses on enhancing the sustainable production of fatty alcohols by utilizing fermentation technology. The process incorporates renewable methanol, aligning with BASF's commitment to sustainability and innovation.

- October 2024: Evonik is restructuring its keto and pharma amino acid business to strengthen its focus on key growth areas. As part of this initiative, the company is evaluating strategic options for its production sites located in Ham, France, and Wuming, China. This move aligns with Evonik's broader strategy to optimize its portfolio and enhance operational efficiency in its core business segments.

- May 2024: Innovad Group strengthened its position in Brazil's nutritional feed additives market by acquiring Oligo Basics, a prominent Brazilian feed additive supplier. This acquisition expands Innovad's portfolio, particularly in organic acid-based products, and reinforces its commitment to delivering innovative solutions in the animal nutrition sector within the region.

Global Organic Acids Market Report Scope

Organic acids are organic compounds that exhibit acidic properties, primarily due to the presence of a carboxyl group (-COOH).

The global organic acid market has been segmented by type, source, application, form and geograohy. Based on product type, the market is segmented into acetic acid, citric acid, lactic acid, succinic acid, malic acid, propionic acid, formic acid, fumaric acid & maleic acids and others. By appliccation the market is segmented into food & beverages, animal feed & nutrition, pharmaceuticals & healthcare, personal care & cosmetics, industrial chemicals & intermediates, polymers & bioplatsics and others. By source, the market is segmented into bio-based, petro-chemical and hybrid/co-product streams. By form, the market is segmented into liquid, and dry crystal powder. Also, the study provides an analysis of the organic acid market in the emerging and established markets across the globe, including North America, Europe, Asia-Pacific, South America, and the Middle East & Africa.

By Type

| Acetic Acid |

| Citric Acid |

| Lactic Acid |

| Succinic Acid |

| Malic Acid |

| Propionic Acid |

| Formic Acid |

| Fumaric and Maleic Acids |

| Others (Benzoic, Gluconic, Adipic, etc.) |

By Source

| Bio-based |

| Petro-chemical |

| Hybrid/Co-product Streams |

By Application

| Food and Beverages |

| Animal Feed and Nutrition |

| Pharmaceuticals and Healthcare |

| Personal Care and Cosmetics |

| Industrial Chemicals and Intermediates (VAM, PTA, Acrylates, etc.) |

| Polymers and Bioplastics (PLA, PBS, PHA) |

| Others (Textiles, Lubricants, Electronics) |

By Form

| Liquid |

| Dry/Crystal/Powder |

Geographic Analysis

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific |

| By Type | Acetic Acid | |

| Citric Acid | ||

| Lactic Acid | ||

| Succinic Acid | ||

| Malic Acid | ||

| Propionic Acid | ||

| Formic Acid | ||

| Fumaric and Maleic Acids | ||

| Others (Benzoic, Gluconic, Adipic, etc.) | ||

| By Source | Bio-based | |

| Petro-chemical | ||

| Hybrid/Co-product Streams | ||

| By Application | Food and Beverages | |

| Animal Feed and Nutrition | ||

| Pharmaceuticals and Healthcare | ||

| Personal Care and Cosmetics | ||

| Industrial Chemicals and Intermediates (VAM, PTA, Acrylates, etc.) | ||

| Polymers and Bioplastics (PLA, PBS, PHA) | ||

| Others (Textiles, Lubricants, Electronics) | ||

| By Form | Liquid | |

| Dry/Crystal/Powder | ||

| Geographic Analysis | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

Key Questions Answered in the Report

What is the current value of Organic Acids Market?

The Organic Acids market is valued at USD 14.69 billion in 2026 and is forecasted to reach USD 20.09 billion by 2031.

Which region holds the largest share of the Organic Acids market?

Asia-Pacific leads with a 30.08% share in 2025, driven by the region's developed manufacturing facilities.

Which product segment is expanding fastest?

Succinic Acid is projected to grow at a 9.52% CAGR during 2026-2031.

Which application segment holds the major share in the Organic Acids Market?

Food and Beverages held a major share of 48.12% in 2025.

Page last updated on: