Organic Deodorant Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Market Size (2025) | USD 7.08 Billion |

| Market Size (2030) | USD 10.12 Billion |

| Growth Rate (2025 - 2030) | 6.32% CAGR |

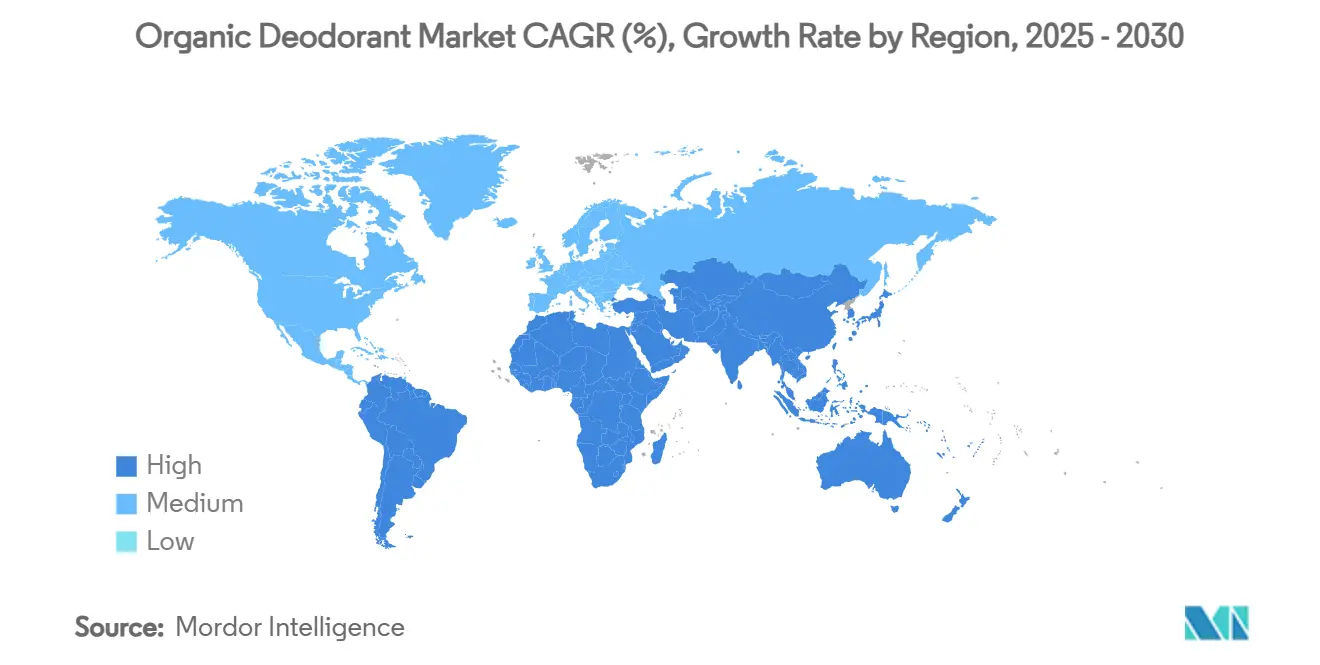

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

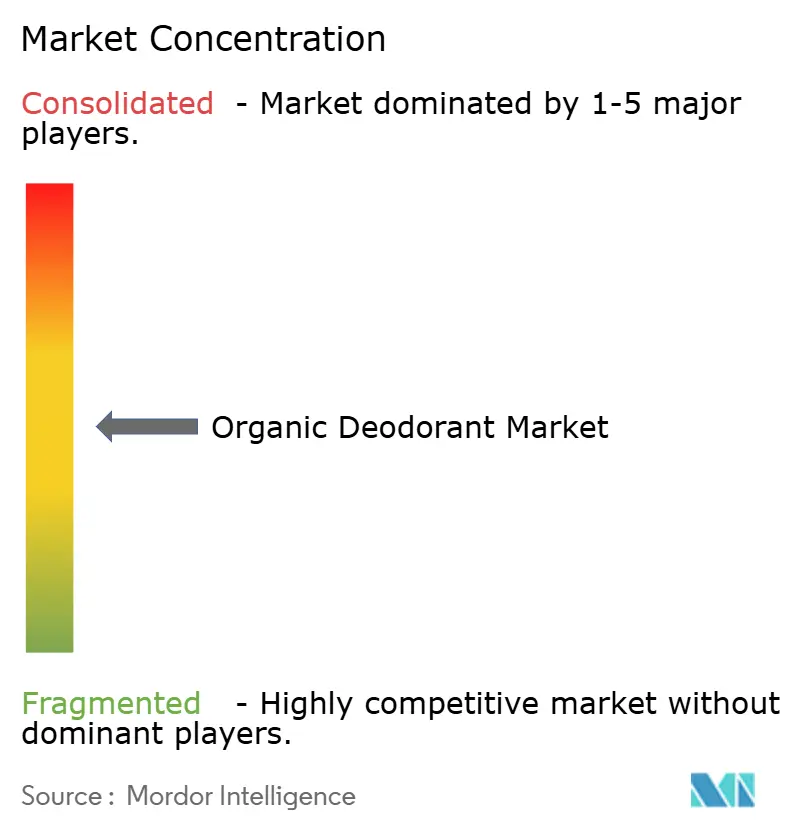

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Organic Deodorant Market Analysis by Mordor Intelligence

The organic deodorants market size stands at USD 7.08 billion in 2025 and is forecast to reach USD 10.12 billion by 2030, expanding at a 6.32% CAGR. As consumers increasingly favor aluminum-free personal care products and as stricter ingredient disclosure rules come into play, retail shelves are being reallocated towards certified items, reflecting a shift in consumer priorities. Brands are adeptly turning health concerns into pricing power, as seen in their embrace of multinational acquisitions, refillable stick concepts, and microbiome-friendly actives. These strategies not only enhance brand performance but also help bridge the efficacy gap with traditional antiperspirants, addressing consumer demand for safer and more effective alternatives. With a digital-first approach to distribution, brands are expanding their global footprint, leveraging online platforms to reach ingredient-savvy consumers who conduct extensive research before making a purchase. This trend underscores the growing importance of transparency and accessibility in the personal care market. Consequently, established players in the category are grappling with fragmentation, facing competition from nimble newcomers who focus on underserved demographics, eco-design, or functional botanicals. These agile entrants are capitalizing on niche markets and sustainability trends, further intensifying competition within the industry.

Key Report Takeaways

- By product type, sprays held 46.83% of organic deodorants market share in 2024 and sticks are forecast to post the fastest 8.20% CAGR between 2025-2030 as refillable formats gain wider distribution in North America and Europe.

- By end user, women accounted for 57.51% of the 2024 volume, whereas the men’s segment is set to record a 9.14% CAGR to 2030, underpinned by male grooming premiumisation in urban Asia-Pacific.

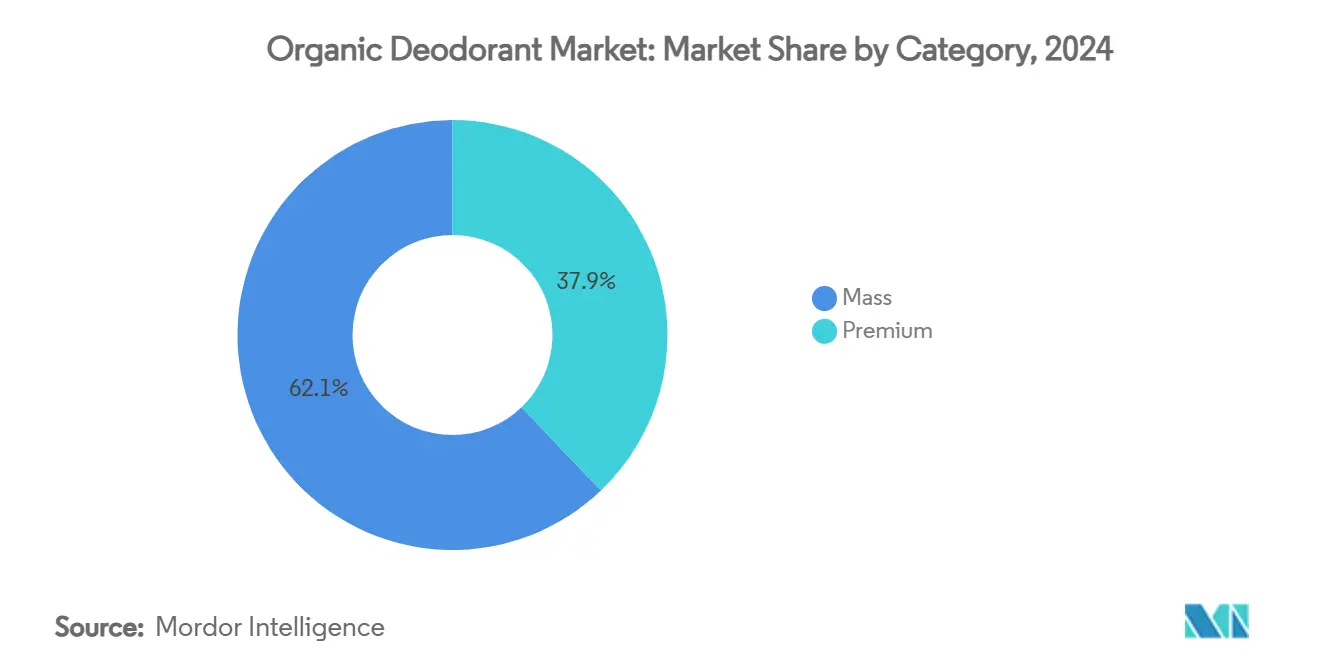

- By category, mass-market ranges represented 62.14% of the 2024 turnover and will grow at 5.7% CAGR; premium lines will expand at a sharper 8.44% CAGR as clean-label benefits justify higher prices.

- By distribution, supermarkets and hypermarkets retained 39.62% of 2024 sales, but online retail is expected to deliver a 9.01% CAGR through 2030, helped by subscription programmes and ingredient education.

- By geography, North America commanded 32.17% revenue share in 2024, while Asia-Pacific is projected to grow the fastest at an 8.93% CAGR thanks to rising disposable incomes and new cosmetic labelling rules in China.

Global Organic Deodorant Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aluminum-free personal care adoption | +1.2% | North America and EU | Medium term (2-4 years) |

| Expansion of natural and organic shelf space | +0.8% | North America, EU, emerging Asia-Pacific | Short term (≤ 2 years) |

| Premiumisation and multinational acquisitions | +1.1% | Global | Long term (≥ 4 years) |

| E-commerce and DTC clean-beauty brands | +0.9% | North America, China | Short term (≤ 2 years) |

| Microbiome-friendly formulations | +0.7% | North America and EU | Medium term (2-4 years) |

| COSMOS/USDA certification incentives | +0.6% | EU and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising shift to aluminum-free personal care

As consumers become more aware of the potential risks associated with aluminum, their purchasing decisions are increasingly leaning towards botanical actives that deodorize without obstructing sweat glands. This shift is driven by growing concerns about aluminum accumulation in the body and its potential long-term effects. The FDA's restrictions on certain aluminum compounds, as outlined in 21 CFR 350.10, bolster safety narratives that marketers adeptly translate into premium product positioning, emphasizing health-conscious choices. Younger consumers, prioritizing preventive health measures, scrutinize ingredient lists with greater diligence, rendering aluminum-free claims a baseline expectation rather than a unique selling point in established markets. Additionally, clinical journals have highlighted disruptions in the microbiome due to prolonged exposure to aluminum salts, lending further credibility to the push for cleaner alternatives. These findings resonate with health-conscious consumers who are increasingly seeking products that align with their wellness goals. While the movement has its strongest foothold in North America and Europe, urban areas in Asia are witnessing a rapid adoption, fueled by social commerce and education led by influencers. This trend is particularly evident in metropolitan regions where digital platforms and influencer marketing play a pivotal role in shaping consumer preferences.

Expansion of natural and organic shelf space in mainstream retail

In 2024, French supermarkets surpassed specialist outlets in organic personal care sales, underscoring the shift of organic visibility from aspirational to essential. This transition highlights the growing consumer preference for convenience and accessibility in purchasing organic products. Major grocery chains across France, Germany, the U.S., and Japan are allocating more shelf space to certified SKUs, driven by store-level data highlighting enhanced margins and increased shopper loyalty. By prioritizing certified products, these retailers are not only meeting consumer demand but also strengthening their competitive positioning in the market. This shelf expansion creates a positive feedback loop: heightened trials boost sales velocity, which in turn validates the need for even more shelf space. Additionally, the increased visibility of certified SKUs encourages consumer trust and repeat purchases, further solidifying their market presence. Meanwhile, smaller brands, once sidelined from physical distribution, are now achieving national prominence through private-label collaborations, escalating the competition on price and value. These partnerships enable smaller players to leverage the distribution networks of larger retailers, ensuring broader reach and improved market penetration.

Premiumization and acquisitions by multinationals

Global conglomerates are increasingly turning their attention to the organic deodorants market, aiming to enhance the quality of their portfolios. In a notable move, Unilever acquired Wild for a hefty USD 290 million in 2025, adding to its string of acquisitions that began with Schmidt’s Naturals. These multinationals bring not just capital but also international distribution channels and robust research and development infrastructures. This backing not only accelerates clean-label innovations but also amplifies marketing efforts, enabling brands to scale rapidly and meet growing consumer demand for sustainable and natural products. On the flip side, independent founders view these lucrative exits as a testament to their brand's equity, often using the proceeds to reinvest in new ventures or expand their entrepreneurial footprint. While this consolidation on the supply side creates hurdles for new entrants by raising competition and entry barriers, it simultaneously broadens consumer choices with premium product extensions, catering to diverse preferences and fostering market growth.

Regulatory incentives for COSMOS/USDA organic certification

Certification standards not only bolster consumer confidence but also shape market dynamics, often favoring established organic brands by erecting barriers to entry. COSMOS certification mandates that products comprise a minimum of 95% organic plants and 20% total organic ingredients. This sets distinct quality benchmarks, helping consumers discern authentic organic products from those with dubious claims. The USDA National Organic Program, overseen by the U.S. Department of Agriculture, encompasses personal care items with agricultural ingredients. It permits certified products to flaunt organic labels, contingent on their organic content percentage. Meanwhile, NSF/ANSI 305 standards cater to products boasting at least 70% organic ingredients. This offers a certification avenue for formulations that, due to certain chemical processes, can't meet USDA's stringent criteria[1]Source: U.S Food & Drug Administration, "Cosmetics, Body Care, and Personal Care Products", www.ams.usda.gov. Such certification frameworks not only foster consumer trust but also carve out competitive advantages for certified brands. Achieving certification demands hefty investments in supply chain verification and quality systems, a challenge for many smaller competitors.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher price points vs. conventional products | -1.4% | Emerging markets worldwide | Short term (≤ 2 years) |

| Performance skepticism on odour protection span | -0.9% | High-humidity regions | Medium term (2-4 years) |

| Supply-chain volatility in botanical extracts | -0.8% | Source-dependent regions | Medium term (2-4 years) |

| Baking-soda sensitivity issues | -0.5% | North America and EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Higher price points versus conventional products

Organic deodorants, often priced 50-100% higher than their conventional counterparts, face significant adoption hurdles in price-sensitive markets. These premium prices are driven by elevated raw material costs, limited production scales, and unavoidable certification expenses, which cannot be fully offset through operational efficiencies. This pricing disparity becomes particularly problematic in emerging markets, where consumers with constrained disposable incomes are less inclined to pay a premium for health benefits that may not provide immediate results. Additionally, the lack of widespread consumer awareness about the long-term advantages of organic products further limits market penetration in these regions. With mass market positioning holding a 62.14% share in 2024, organic brands must prioritize the development of cost-effective formulations and manufacturing processes. Such strategies are essential not only to compete with conventional alternatives but also to maintain the integrity of their organic certifications while addressing the affordability concerns of a broader consumer base.

Performance skepticism (shorter odour-protection span)

Consumer concerns about the shorter efficacy duration of natural antiperspirants, compared to their aluminum-based counterparts, hinder trials and curtail repeat purchases, especially among users prioritizing performance. Clinical studies juxtaposing aluminum lactate and aluminum chloride antiperspirants show that while 88% of users favor the tolerability of natural alternatives, almost half find conventional products superior for odor control[2]Source: VICTORIA UNIVERSITY OF WELLINGTON, "Comparison of novel aluminium lactate versus aluminium chloride-based antiperspirant in excessive axillary perspiration: First prospective cohort study", onlinelibrary.wiley.com . EEMCO's efficacy assessment guidance underscores the importance of standardized testing to substantiate deodorant claims. However, many organic brands, lacking the resources for in-depth clinical trials, struggle to counteract performance skepticism. Research on natural antiperspirants highlights a dearth of scientific backing for plant-based sweat reduction claims, leaving a credibility void that competitors readily exploit in their marketing. In response, brands are channeling investments into efficacy studies and reformulations, all while educating consumers on the differing performance expectations between organic and conventional products.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: sprays dominate, sticks accelerate

In 2024, sprays dominate the organic deodorant market, capturing 46.83% of the segment. Their widespread appeal stems from consumer familiarity and the comprehensive coverage they offer, ensuring an even application across the underarm area. This preference underscores established consumer habits that prioritize convenience and extensive coverage. Such attributes are particularly valued in humid climates, where all-day protection is paramount. Sprays are lauded for their user-friendliness and their capacity to provide a swift, uniform layer of deodorant. While alternative formats are emerging, many users still gravitate towards sprays, valuing their efficiency and dependability. This entrenched position highlights sprays' enduring significance in daily personal care routines.

On the other hand, sticks are emerging as the fastest-growing segment, boasting a projected CAGR of 8.20% through 2030. This surge is primarily fueled by a heightened awareness of sustainability among consumers. Many are now gravitating towards products that not only minimize packaging waste but also prevent over-application. Sticks are favored for their precise application and are increasingly linked with innovative, eco-friendly packaging solutions, including refillable systems and biodegradable tubes. Moreover, sticks resonate with environmentally conscious consumers who seek effective products that align with their values and reduce their ecological footprint. Recent studies bolster the appeal of sticks, showcasing the antimicrobial properties of ingredients like xylityl sesquicaprylate at a 0.35% concentration[3]Source: Multidisciplinary Digital Publishing Institute, "Deodorant Efficacy of Xylityl Sesquicaprylate Vehiculated into Roll-on and Stick Prototype Formulations", www.mdpi.com. Additionally, while roll-on formats are often lumped together with sticks in consumer preferences, their strong acceptance in clinical trials enhances the credibility of both liquid and solid natural deodorants, extending beyond just sprays.

By End User: women remain core, men surge

In 2024, women dominated the organic deodorants market, holding a 57.51% share. This trend mirrors the established purchasing habits often seen in beauty aisles. Brands tailor their offerings to cater to specific female life stages: adolescents lean towards gentle scents, pregnant women prioritize endocrine-free formulations, and peri-menopausal consumers seek effective hormonal odor control. Such segmentation underscores brands' commitment to understanding diverse female needs. Women's enduring loyalty to organic personal care products not only drives the market but also fosters a robust environment for innovation and product development.

Meanwhile, the male segment, though smaller in 2024, is the organic deodorant market's fastest-growing group, with a projected 9.14% CAGR through 2030. Traditionally, men hesitated to adopt organic deodorants, doubting their performance. Yet, this mindset is shifting, thanks to the influence of grooming influencers on social media and a gym culture that champions wellness and natural products. Men are now poised to drive significant growth, accounting for about one-third of the market's expansion by 2030. Furthermore, as consumers gravitate towards minimalistic and shared toiletry options, gender-neutral SKUs are gaining popularity. This shift highlights the importance of male and inclusive product strategies in seizing opportunities within the organic deodorant market.

By Category: mass retains volume, premium outperforms

In 2024, mass-positioned SKUs dominated the organic deodorants market, raking in 62.14% of the total turnover. Their success can be attributed to widespread supermarket availability and appealing price points, usually set below USD 8, making them accessible to a diverse consumer base. While prioritizing affordability, suppliers face the challenge of upholding stringent ingredient purity standards. This necessitates adept sourcing and scaling of organic starches and seed oils to meet demand without inflating costs. The mass segment enjoys robust distribution channels, bolstered by a consistent consumer preference for dependable, everyday personal care products. Such extensive availability not only guarantees steady sales but also cements its leading market position. As competition heats up, brands are increasingly navigating the tightrope between cost-effectiveness and the rising consumer demand for ingredient transparency and natural formulations.

On the other hand, the premium segment, with price tags exceeding USD 15, is set to emerge as the fastest-growing category, boasting an estimated CAGR of 8.44% through 2030. This surge is fueled by innovations like refillable packaging, resonating with eco-conscious consumers. Premium offerings tout microbiome-friendly attributes and partner with artisan fragrance houses, crafting unique scent profiles that set them apart. Eye-catching packaging, such as metal tins and exclusive scent releases, amplifies their appeal, especially in specialty beauty retail, driving up basket values. These premium products draw in consumers who value luxury, effectiveness, and ethical considerations, allowing brands to enjoy elevated profit margins. The segment's growth highlights a shift in consumer preferences, leaning towards tailored and sustainable organic deodorant experiences.

By Distribution Channel: brick-and-mortar stays vital, e-commerce scales

In 2024, supermarkets and hypermarkets dominated the organic deodorants market, accounting for 39.62% of total revenue. These traditional retail channels play a crucial role in introducing products to first-time buyers. Their high foot traffic, combined with strategic cross-merchandising of related personal care items, often leads to impulse purchases. Category captains are actively securing secondary placements near natural cosmetics sections, boosting visibility and shopper engagement. The widespread accessibility and convenience of these outlets solidify their status as the go-to choice for consumers delving into organic deodorants. Their established presence and the trust they've garnered from shoppers provide brands with a potent platform to foster consumer awareness and loyalty. While newer channels are on the rise, supermarkets and hypermarkets continue to hold a dominant position in the personal care retail arena.

On the other hand, the online retail segment is set to emerge as the fastest-growing distribution channel, boasting a robust CAGR of 9.01% through 2030. This surge can be attributed to advanced digital marketing tactics, such as algorithmic advertising and influencer affiliate programs, which adeptly target and engage pivotal consumer demographics. Furthermore, the rise of auto-replenishment subscription models not only enhances convenience but also curbs customer churn by ensuring consistent product availability. Health-and-beauty specialist chains serve as vital trust-building platforms, where trained advisers enlighten consumers about certification logos and product advantages, seamlessly linking physical and digital shopping realms. The fusion of online platforms with tailored support and digital engagement tools positions e-commerce as a vibrant growth catalyst for the organic deodorants market. Brands harnessing these digital innovations are poised to broaden their reach, strengthen consumer ties, and seize emerging market prospects.

Geography Analysis

In 2024, North America holds a commanding 32.17% share of the market, a testament to its consumers' mature understanding of organic personal care benefits and a well-established retail infrastructure that champions premium product distribution. This regional dominance is largely attributed to an early embrace of aluminum-free alternatives, spurred by a health-conscious populace and a push for regulatory transparency, empowering consumers to make informed choices. Furthermore, regulatory bodies like the FDA, overseeing cosmetic labeling, and the USDA, setting organic certification benchmarks, fortify the market's premium positioning while upholding stringent product quality and safety standards.

Asia-Pacific is on a rapid ascent, boasting an 8.93% CAGR projected through 2030. This surge is fueled by a burgeoning middle class with disposable income and a heightened urban awareness regarding ingredient safety. Notably, the Chinese market stands out, with government mandates pushing for clearer cosmetic labeling. This has amplified the demand for products boasting verifiable ingredient claims and robust safety profiles. Additionally, the region's expanding e-commerce landscape empowers direct-to-consumer brands, allowing them to cater to consumers in search of specialized organic formulations, often absent from conventional retail outlets.

Europe's organic personal care market enjoys steady growth, bolstered by established markets and regulatory endorsements like the COSMOS certification, which bolsters consumer trust. The continent's deep-rooted sustainability ethos not only fuels demand for eco-friendly packaging but also for ethically sourced ingredients, resonating with broader environmental, social, and governance values. Meanwhile, South America and the Middle East and Africa stand at the cusp of a burgeoning opportunity. Here, urbanization and rising disposable incomes are expanding the market for premium organic personal care products. However, challenges like price sensitivity and a nascent distribution infrastructure temper the pace of growth.

Competitive Landscape

The organic deodorants market is moderately concentrated, allowing emerging brands to seize market share through innovation and targeted positioning. Meanwhile, established players leverage their distribution scale and brand recognition for a competitive edge. Strategic patterns highlight two main tactics: multinational corporations are acquiring successful organic brands to enhance their premium portfolios, while independent brands are using direct-to-consumer models to foster customer relationships and sidestep traditional retail hurdles. Unilever's acquisitions of Schmidt's Naturals and Wild underscore this acquisition-centric strategy, and brands like Native, which was acquired by P&G, showcase how an organic stance can pave the way for a successful premium market entry.

There are untapped opportunities in demographic segments like men's grooming and specialized formulations that cater to specific skin sensitivities or climate conditions, areas where conventional products often fall short. New entrants are increasingly turning to microbiome science and sustainable packaging as key differentiators. They're also forging direct customer ties through subscription services and tailored formulation strategies.

Technology adoption is leaning more towards ingredient innovation than on manufacturing automation. Successful brands are channeling investments into clinical research, aiming to validate their efficacy claims and counteract performance skepticism, a hurdle for market growth. Patent activities highlight a focus on innovations, particularly in methods that tackle persistent odors using enzymatic compositions and biofilm mitigation techniques.

Organic Deodorant Industry Leaders

-

Unilever PLC

-

Procter & Gamble Co

-

Colgate-Palmolive Co

-

Beiersdorf AG

-

Weleda AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Blessed Beez unveiled its new line of 100% natural and organic deodorants, offering flavors like Geranium, White Rose, Lavender, and Sweet Orange. These products are available for purchase across the United Kingdom and other platforms. The launch highlights the brand's commitment to providing eco-friendly and skin-friendly personal care solutions, catering to the growing demand for sustainable products in the market.

- June 2025: Francesco Palmieri introduced a new deodorant made with natural ingredients in the United States. This launch aligns with the increasing consumer preference for natural and chemical-free personal care products, emphasizing the brand's focus on health-conscious offerings.

- April 2025: Kafx Body, a market player, rolled out its new watermelon deodorant, crafted from natural ingredients. The product is designed to appeal to consumers seeking refreshing and fruity scents, while also addressing the need for natural and effective deodorant options.

- August 2024: Nectar Botanicals debuted its organic and natural deodorant butter, available in Jasmine and Lime flavors. This Bicarb Soda Free Natural Deodorant boasts a delicate blend of jasmine absolute and zesty lime essential oil, ensuring you feel fresh and confident throughout the day. The product launch reflects the brand's dedication to offering innovative and gentle alternatives for individuals with sensitive skin.

Global Organic Deodorant Market Report Scope

| Sprays |

| Sticks |

| Roll Ons |

| Others |

| Women |

| Men |

| Unisex |

| Mass |

| Premium |

| Supermarkets/Hypermarkets |

| Health and Beauty Stores |

| Online Retail Stores |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Netherlands | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Indonesia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type | Sprays | |

| Sticks | ||

| Roll Ons | ||

| Others | ||

| By End User | Women | |

| Men | ||

| Unisex | ||

| By Category | Mass | |

| Premium | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Health and Beauty Stores | ||

| Online Retail Stores | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Netherlands | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Indonesia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the organic deodorants market in 2025?

The organic deodorants market size is USD 7.08 billion in 2025.

What is the expected growth rate for organic deodorants through 2030?

The category is projected to expand at a 6.32% CAGR from 2025-2030.

Which product type grows fastest over the forecast period?

Stick formats will post the highest 8.20% CAGR, driven by refillable packaging and precise application.

Why is Asia-Pacific considered the prime growth region?

Strengthening disposable incomes, strict Chinese labelling laws, and high e-commerce penetration give Asia-Pacific the highest 8.93% CAGR outlook.

Page last updated on: