Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

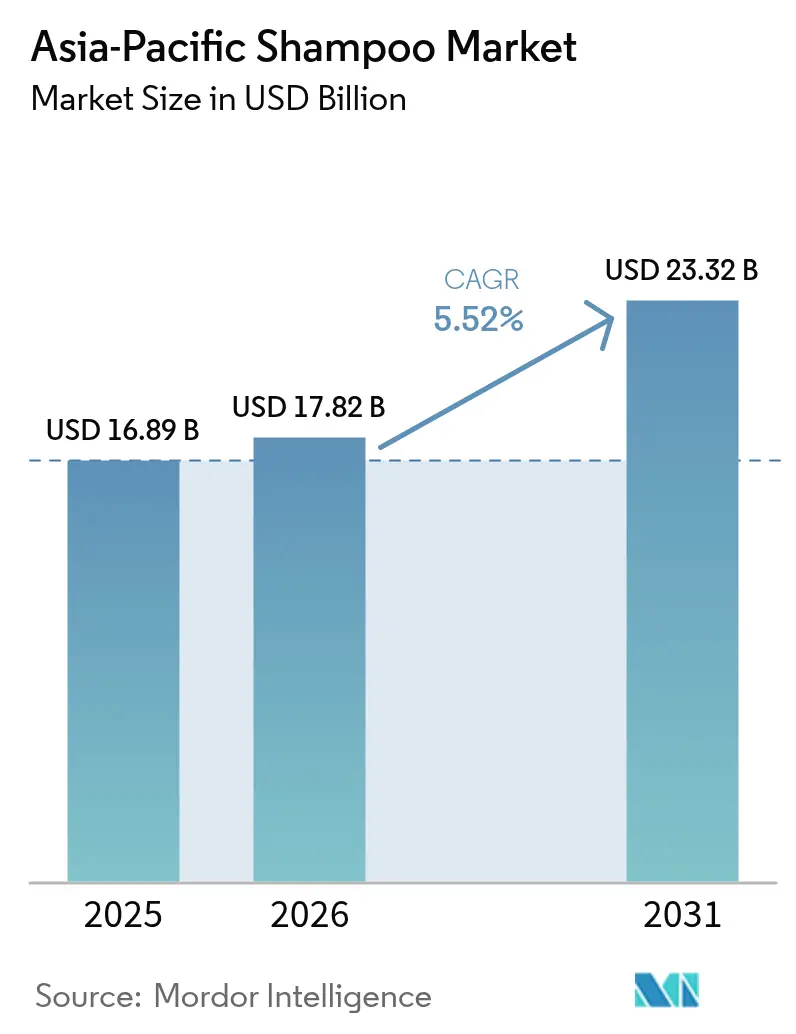

| Base Year Market Size (2025) | USD 16.89 Billion |

| Market Size (2026) | USD 17.82 Billion |

| Market Size (2031) | USD 23.32 Billion |

| Growth Rate (2026 - 2031) | 5.52% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Asia-Pacific Shampoo Market Analysis by Mordor Intelligence

The Asia-Pacific shampoo market size is expected to grow from USD 16.89 billion in 2025 to USD 17.82 billion in 2026 and is forecast to reach USD 23.32 billion by 2031 at 5.52% CAGR over 2026-2031. This growth reflects digital-native consumers who reevaluate ingredient lists and purchasing channels in tandem. Premiumization momentum, rising demand for botanical actives, and omnichannel retail adoption accelerate value creation even as mass-market sachets preserve everyday volumes. China remains the revenue anchor, but South Korea delivers the fastest trajectory, helped by K-beauty exports and domestic e-commerce sophistication. Ingredient transparency, refill formats, and circular-economy packaging have moved from differentiation to necessity as regulators tighten oversight of synthetic surfactants and single-use plastics. Competitive intensity is moderate; global conglomerates retrofit legacy portfolios while regional specialists leverage culturally resonant botanicals to win first-time switchers.

Key Report Takeaways

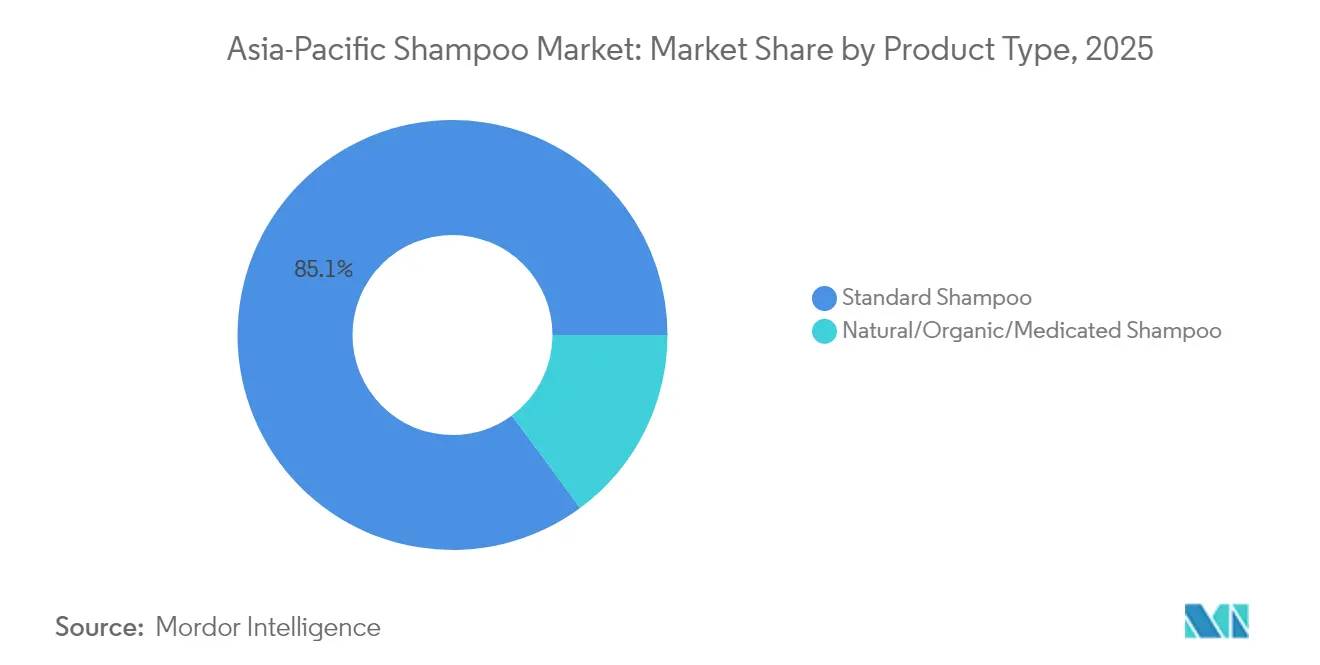

- By product type, standard formulations held 85.12% of the Asia-Pacific shampoo market share in 2025; natural, organic, and medicated variants are forecast to expand at a 5.99% CAGR through 2031.

- By hair concern, specific-purpose variants captured 52.01% revenue share in 2025, while anti-dandruff and scalp-health offerings post the fastest 5.78% CAGR to 2031.

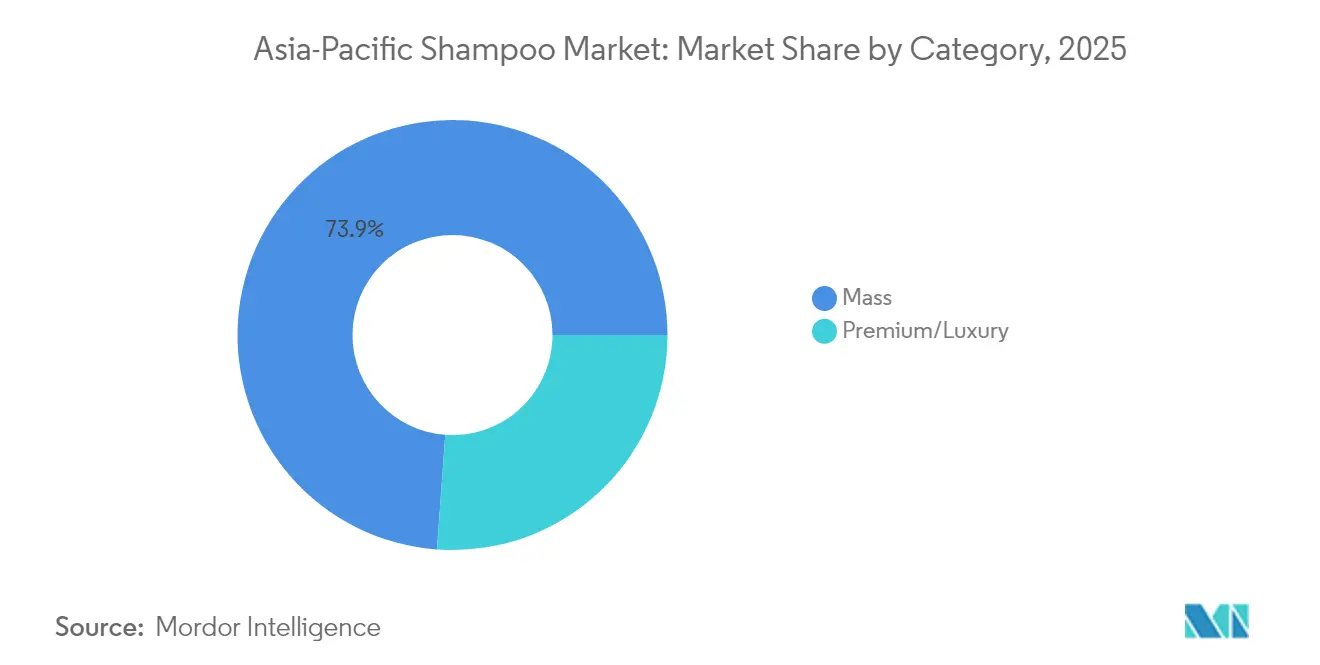

- By category, the mass tier commanded 73.85% share of the Asia-Pacific shampoo market size in 2025; premium and luxury shampoos record the highest projected 6.07% CAGR through 2031.

- By distribution, supermarkets and hypermarkets led with 41.75% share in 2025, whereas online retail advances at a 6.25% CAGR between 2026-2031.

- By country, China contributed 32.86% of regional sales in 2025; South Korea is the quickest-growing geography at a 6.03% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Shampoo Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for organic and natural shampoos due to awareness of chemical harms | +1.2% | China, India, Japan, South Korea, Australia | Medium term (2-4 years) |

| Increasing preference for ayurvedic and herbal ingredients | +0.9% | India, Southeast Asia with spillover to Australia | Medium term (2-4 years) |

| Demand for targeted solutions like anti-dandruff, hair loss, and scalp health products | +1.4% | Regional, with concentration in China, Japan, South Korea | Short term (≤ 2 years) |

| High millennial and Gen Z population driving grooming trends | +1.1% | Regional, strongest in Indonesia, India, China | Long term (≥ 4 years) |

| Growing popularity of hair coloring boosting specialized shampoo needs | +0.6% | China, Japan, South Korea, urban centers in Southeast Asia | Medium term (2-4 years) |

| Innovation in premium, sustainable, and eco-friendly formulations | +0.8% | Japan, South Korea, Australia, Singapore, urban China | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising demand for organic and natural shampoos due to awareness of chemical harms

The Asia-Pacific shampoo market is witnessing a strong rise in demand for organic and natural shampoos fueled by growing consumer awareness of the potential harms associated with chemical ingredients. Consumers in the region, especially in countries like India, China, and Japan, are increasingly favoring products with herbal and plant-based ingredients known for their safety and efficacy. According to NSF International, 74% of consumers considered organic ingredients important in personal care products in 2024 [1]Source: NSF International, "Consumers consider personal care organic ingredients important", nsf.org, highlighting the significant weight buyers place on clean, toxin-free formulations. This trend aligns with a broader preference for wellness-oriented, sustainable, and eco-friendly products, supported by the rise of e-commerce and social media influence. The emphasis on transparency, ingredient authenticity, and certification adds to consumer confidence in organic shampoos. With sustainability and health driving purchase decisions, the organic and natural shampoo segment is poised for robust growth in the Asia-Pacific market.

Increasing preference for ayurvedic and herbal ingredients

The Asia-Pacific shampoo market is experiencing robust growth fueled by the increasing consumer preference for ayurvedic and herbal ingredients. In countries like India, China, and Japan, traditional formulations with botanicals such as neem, amla, aloe vera, and shikakai are surging in popularity as safer alternatives to synthetic shampoos. Rising awareness of chemical-related scalp irritation and hair damage has shifted demand toward plant-based products offering nourishment and vitality. For instance, brands offering herbal shampoos with traditional ingredients like onion peel oil and Japanese matcha boast an impressive 80% user satisfaction rate after just 5-6 washes [2]Source: Detoxie, “Hard Water Relief, Hair Fall Control & Pro Growth Shampoo,” detoxie.in. This aligns with cultural affinity for natural remedies and regulatory support for transparency. Brands are innovating with these extracts, driving premiumization and market expansion.

Demand for targeted solutions like anti-dandruff, hair loss, and scalp health products

Demand for targeted solutions like anti-dandruff, hair loss, and scalp health products is a major driver in the Asia-Pacific shampoo market. Rising urbanization, pollution, stress, and dietary shifts have heightened prevalence of scalp issues and hair thinning across countries like India, China, and Japan. Consumers increasingly seek shampoos with active ingredients such as zinc pyrithione, ketoconazole, biotin, and caffeine for clinically proven efficacy. As highlighted by the Research Journal of Pharmacy and Technology, these formulations now feature scientifically validated ingredients such as ursolic acid and diosgenin [3]Source: Manju Bhargavi N. et al., “Estimation of Ursolic Acid and Diosgenin in Herbal Hair Oil Formulations,” Research Journal of Pharmacy and Technology, rjptonline.org. This personalization trend aligns with beauty influencers and social media promoting specialized routines for dandruff control and follicle strengthening. Brands are innovating with multifunctional formulas combining cleansing and treatment benefits, capturing premium segments. E-commerce expansion further boosts accessibility to these niche products.

High millennial and Gen Z population driving grooming trends

The Asia-Pacific shampoo market benefits significantly from its high millennial and Gen Z population, which constitutes over 40% of the region's total demographics and actively drives grooming trends. These digitally native cohorts prioritize self-expression through personalized hair care, influenced by K-beauty, social media influencers, and platforms like TikTok and Instagram. Urban millennials seek premium formulations for scalp health and styling, while Gen Z embraces gender-neutral, sustainable shampoos aligning with clean beauty values. This demographic shift boosts demand for multifunctional products like volumizing and color-protecting variants, with e-commerce enabling trial of niche brands. Grooming has evolved from basic hygiene to a lifestyle statement, enhancing confidence and professional appeal in competitive job markets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of counterfeit products damaging brand reputation | -0.7% | China, India, Southeast Asia, particularly cross-border e-commerce | Short term (≤ 2 years) |

| High pricing of premium shampoos limiting penetration | -0.5% | Indonesia, Thailand, India, Philippines | Medium term (2-4 years) |

| Consumer skepticism toward synthetic formulations | -0.4% | China, India, Australia, urban centers in Southeast Asia | Medium term (2-4 years) |

| Regulatory challenges on chemical ingredients and claims | -0.3% | China, India, South-east Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Proliferation of counterfeit products damaging brand reputation

Counterfeit shampoo products are causing significant challenges in the Asia-Pacific market, severely impacting brand reputations and eroding consumer trust. This issue is particularly prevalent in countries like India and China, where counterfeit shampoos often replicate premium brands. These fake products are manufactured using substandard or harmful ingredients, which can lead to scalp irritation, hair damage, and other serious health risks. The problem is exacerbated by the widespread availability of these counterfeits on e-commerce platforms and informal distribution channels. These channels often target price-sensitive consumers, especially during festive seasons and periods of high demand, when purchasing activity surges. The presence of counterfeit products undermines the efforts of genuine brands that invest heavily in research, development, and quality control to ensure product safety and efficacy. When consumers unknowingly purchase and use counterfeit shampoos, their negative experiences, such as adverse reactions or poor performance, are often mistakenly attributed to the original brands. This misattribution further damages the reputation of legitimate companies, creating a ripple effect that impacts their market share and long-term growth prospects.

High pricing of premium shampoos limiting penetration

High pricing of premium shampoos significantly limits market penetration in the price-sensitive Asia-Pacific shampoo market. While affluent urban consumers in China and South Korea embrace luxury formulations with advanced actives and salon-inspired benefits, mass-market buyers in India, Indonesia, and Vietnam prioritize affordability over sophistication. Premium products often cost 5-10 times more than standard variants, creating barriers for the region's expanding middle class still grappling with income disparities. This pricing gap restricts premium segment growth to under 25% share despite higher margins, as consumers opt for local or mass brands offering comparable cleansing at lower costs. E-commerce trials and mini-sizes help test waters, but widespread adoption hinges on economic upliftment. Brands counter with tiered pricing and promotions, yet high costs continue constraining overall premiumization momentum. Regulatory import duties on luxury imports further exacerbate accessibility challenges in developing markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Standard Formulations Dominate but Natural Variants Accelerate

The standard shampoo segment dominated the Asia-Pacific shampoo market in 2025, capturing 85.12% of the market share. This dominance is largely due to entrenched consumer habits, where consumers prefer familiar, widely available products. Multinational brands benefit from extensive distribution networks spanning supermarkets, hypermarkets, and convenience stores, ensuring easy accessibility for a broad demographic. These channels also offer competitive pricing and frequent promotions that reinforce consumer loyalty. The combination of brand strength, price-point accessibility, and traditional retail presence solidifies standard shampoos as the volume leaders in this region. Despite growing interest in alternatives, these products remain staples for everyday hair care needs across diverse markets in the region.

In contrast, natural, organic, and medicated shampoos represent the fastest-growing segment, expected to expand at a CAGR of 5.99% through 2031. This growth is propelled by increasing regulatory support favoring ingredient transparency and consumer demand for clean, safer cosmetic products. Rising awareness about chemical sensitivities and environmental sustainability encourages consumers to shift towards herbal and medicated formulations. These shampoos appeal especially to health-conscious urban consumers who prioritize product efficacy alongside safety and sustainability credentials. Brands investing in innovation around certification, organic sourcing, and eco-friendly packaging gain traction in this expanding niche. The segment's growth reflects a broader trend toward premiumization and natural beauty in the Asia-Pacific market.

By Hair Concern: Specific-Purpose Variants Outpace General Offerings

Specific-purpose shampoos, including those formulated for anti-dandruff, volumizing, strengthening, and regrowth benefits, held a significant 52.01% share of the Asia-Pacific shampoo market in 2025. This segment is expanding rapidly, with a CAGR of 5.78% projected through 2031, outpacing the growth of general or multi-purpose variants. The rising demand for these specialized shampoos is driven by consumers' increasing focus on addressing particular hair and scalp issues with effective, targeted solutions. Brands are capitalizing on this trend by investing in clinically backed formulas and marketing campaigns that highlight specific benefits, such as dandruff control and hair thickening. This segment attracts health-conscious consumers who seek personalized hair care tailored to their unique needs.

The general or multi-purpose shampoo segment continues to serve the bulk of everyday hair cleansing needs across diverse consumer groups in the Asia-Pacific region. These shampoos are favored for their versatility and cost-effectiveness, making them accessible across various market tiers and retail channels. With entrenched consumer habits endorsing their use for routine hair care, these products maintain substantial market presence. However, this segment faces competition from more innovative, problem-focused products growing in popularity. Despite this, general shampoos play a crucial role by offering simple, reliable cleansing solutions and often serve as a gateway for consumers to try specialized variants.

By Category: Mass Segment Anchors Volume While Premium Tier Expands

The mass category shampoo segment dominated the Asia-Pacific shampoo market in 2025, commanding a substantial 73.85% share. This leadership is primarily driven by the wide availability and affordability of mass-market shampoos, which appeal to the broad consumer base across developing and developed countries in the region. These products are extensively distributed through supermarkets, hypermarkets, convenience stores, and drugstores, ensuring easy access for everyday consumers. Promotional pricing and strong brand presence in this category reinforce its position. Additionally, the mass category caters to basic hair cleansing needs, making it a staple for most households. Its value-oriented approach makes it highly competitive in price-sensitive markets.

Meanwhile, the premium and luxury shampoo segment is the fastest-growing in the Asia-Pacific region, projected to achieve a 6.07% CAGR through 2031. This category is fueled by rising disposable incomes and the increasing willingness of consumers to pay more for enhanced benefits such as salon-quality formulations, natural ingredients, and eco-friendly packaging. Affluent urban consumers are drawn to these innovative products offering specialized hair care solutions tailored to individual needs. Furthermore, the premium segment benefits from strategic marketing efforts, including influencer endorsements and personalized product experiences. The growth of e-commerce platforms also facilitates premium product accessibility, expanding reach beyond traditional retail.

By Distribution Channel: Online Retail Surges as Omnichannel Becomes Essential

Supermarkets and hypermarkets dominated the Asia-Pacific shampoo market distribution in 2025, securing 41.75% of the market share. This commanding position stems from their high footfall, which attracts a diverse consumer base seeking one-stop shopping experiences. Impulse purchases are common in these outlets due to strategic product placement near checkouts and eye-catching displays. Promotional visibility through in-store deals, end-cap merchandising, and loyalty programs further drives volume sales. These channels excel in mass-market penetration, particularly in urban and semi-urban areas across China, India, and Southeast Asia. Their established logistics and shelf space agreements with multinational brands solidify their role as volume anchors.

Online retail stores, however, represent the fastest-growing distribution segment, projected to expand at a 6.25% CAGR through 2031. This surge reflects profound structural shifts in consumer behavior toward digital convenience and home delivery amid urbanization and busy lifestyles. E-commerce platforms offer personalized recommendations, exclusive deals, and subscription models that enhance customer retention. The rise of mobile shopping apps and social commerce in markets like India and Indonesia accelerates accessibility for younger demographics. Brands leverage data analytics for targeted advertising, boosting premium and niche product sales online. Ultimately, online channels are transforming distribution dynamics with scalability unmatched by traditional retail.

Geography Analysis

China held the largest share of the Asia-Pacific shampoo market in 2025, accounting for 32.86% of the regional market. This dominance is fueled by its vast population exceeding 1.4 billion, which represents a huge consumer base across multiple income levels. Rising disposable incomes, especially in tier-1 and tier-2 cities, have accelerated the premiumization trend, with more consumers willing to try higher-end, specialized shampoo products. The country's rapidly developing retail infrastructure, coupled with increasing urbanization, further supports consistent market growth. Domestic brands alongside global players benefit from this dynamic, competing on innovation and affordability. Additionally, regulatory frameworks supporting product safety and efficacy encourage consumer confidence in new launches.

South Korea represents the fastest-growing geography in the Asia-Pacific shampoo market, projected to expand at a 6.03% CAGR through 2031. This rapid growth is propelled by the global popularity of K-beauty, which has brought significant attention to South Korea’s haircare innovations and formulations. South Korean brands are strong exporters, leveraging digital marketing and social media influence to gain traction internationally. The domestic market is also evolving with a focus on advanced ingredients, scalp health, and eco-friendly packaging. Consumer enthusiasm for trend-driven, technologically advanced shampoos ensures ongoing growth. Government support for beauty exports and research also plays a key role in solidifying South Korea’s leadership in the premium shampoo segment.

Other important markets in the region include India, Japan, and Indonesia, each contributing uniquely to Asia-Pacific’s haircare landscape. India’s market is expanding rapidly, driven by increasing urbanization, rising disposable incomes, and a surge in demand for herbal and ayurvedic shampoos that cater to diverse hair types. Japan maintains a mature and sophisticated market with a preference for high-quality, science-backed products, including medicated shampoos that address specific scalp issues. Indonesia is characterized by a large, youthful population that seeks affordable yet effective shampoo options, fueling volume growth. Together, these countries complement China and South Korea's market dynamics, enabling sustained growth and innovation throughout the Asia-Pacific shampoo market.

Competitive Landscape

The Asia-Pacific shampoo market is moderately fragmented, reflecting a competitive environment where large multinational conglomerates coexist with agile regional specialists. Key global players such as Procter & Gamble, Unilever, Kao Corporation, L'Oréal, and Shiseido dominate significant market portions through robust brand portfolios, extensive research and development capabilities, and well-established distribution networks. These multinational giants leverage their scale to innovate continually, ensuring compliance with evolving regulatory standards and addressing diverse consumer preferences across the region. Their global presence also allows them to deploy strategic marketing campaigns and partnerships, maintaining brand loyalty and competitive advantage.

Alongside these global leaders, regional specialists like Dabur, Marico, Himalaya Drug Company, and Amorepacific represent critical players in the Asia-Pacific shampoo market ecosystem. These companies capitalize on deep local market knowledge, emphasizing herbal, natural, and ayurvedic formulations that resonate with the region’s traditional preferences. They are often more agile in responding to emerging trends and niche demands, such as increasing consumer interest in organic and clean-beauty products. Their focused product lines cater to cultural and demographic nuances which multinational brands may find challenging to address comprehensively. This coexistence of large and local players fosters dynamic competition and diversified offerings within the market.

To capture the evolving consumer landscape, incumbents are pursuing dual strategies. They are reformulating their existing shampoo portfolios to incorporate clean-beauty credentials, including the use of natural ingredients and eco-friendly packaging, thereby meeting rising consumer demand for transparency and sustainability. Simultaneously, they are launching premium sub-brands targeting the trade-up segment that desires high-performance, personalized, and innovative hair care solutions. This approach enables brands to maintain relevance across multiple consumer segments, from value-seeking mass markets to affluent urban shoppers seeking luxury experiences.

Asia-Pacific Shampoo Industry Leaders

-

L'Oréal S.A.

-

Unilever PLC

-

Kao Corporation

-

The Procter & Gamble Company

-

Shiseido Company, Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: CavinKare launched Meera Rice Kanji Shampoo in India, strategically positioned to address the functional consumer need for long-lasting hair conditioning between washes. The product, formulated with natural rice kanji and aloe vera, claims to provide conditioning effects lasting up to 72 hours.

- October 2024: Kao Corporation launched "The Answer," a premium hair care brand designed to strengthen its position in the high-quality hair care market. Targeting women who value advanced hair care technology and ingredient transparency, the line includes a shampoo suitable for all hair types and three treatments focusing on hydration, repair, and glossiness.

- September 2024: Kao Corporation collaborated with SCG Chemicals Thailand to produce low-carbon shampoo bottles for its Feather brand, integrating circular-economy initiatives into core operations. The partnership demonstrates how Japanese manufacturers are vertically integrating sustainability across supply chains.

Asia-Pacific Shampoo Market Report Scope

Shampoo is a basic hair care product used to clean hair. Different types of shampoos are available in the market according to hair type. The Asia-Pacific Shampoo market is segmented by product type, distribution channel, and geography. Based on product type, the market is segmented into 2-in-1 shampoo, anti-dandruff, kids shampoo, medicated shampoo, and other shampoos. Based on the distribution channel, the market is segmented into supermarkets/hypermarkets, specialty stores, online retail stores, pharmacies/drugstores, and other distribution channels. The market is segmented based on geography into China, Japan, India, Australia, and the Rest of Asia-Pacific. For each segment, the market sizing and forecast have been done based on value (in USD million).

By Product Type

| Standard Shampoo |

| Natural/Organic/Medicated Shampoo |

By Hair Concern

| General/Multi-purpose | |

| Specific Purpose | Anti-Dandruff and Scalp Health |

| Volumizing and Thickening | |

| Strengthening and Repair | |

| Hair Regrowth and Hair Repair |

By Category

| Mass |

| Luxury/Premium |

By Distribution Channel

| Supermarkets / Hypermarkets |

| Convenience/Grocery Stores |

| Online Retail Stores |

| Other Distribution Channels |

By Country

| China |

| India |

| Japan |

| Australia |

| Indonesia |

| Philippines |

| South Korea |

| Thailand |

| Singapore |

| Rest of Asia-Pacific |

| By Product Type | Standard Shampoo | |

| Natural/Organic/Medicated Shampoo | ||

| By Hair Concern | General/Multi-purpose | |

| Specific Purpose | Anti-Dandruff and Scalp Health | |

| Volumizing and Thickening | ||

| Strengthening and Repair | ||

| Hair Regrowth and Hair Repair | ||

| By Category | Mass | |

| Luxury/Premium | ||

| By Distribution Channel | Supermarkets / Hypermarkets | |

| Convenience/Grocery Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Country | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| Philippines | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

Key Questions Answered in the Report

What is the current value of the Asia-Pacific shampoo market?

The market is valued at USD 17.82 billion in 2026 and is forecast to reach USD 23.32 billion by 2031.

Which country shows the fastest growth in regional shampoo sales?

South Korea posts the highest CAGR at 6.03% through 2031.

How large is the natural and organic shampoo segment?

Natural, organic, and medicated variants are expanding at a 5.99% CAGR and steadily lifting share from the 14.88% base recorded in 2025.

Which distribution channel is growing the quickest?

Online retail stores advance at a 6.25% CAGR, outpacing supermarkets and hypermarkets.

What sustainability initiatives influence purchase decisions?

Recycled-plastic packaging, refill pouches, and low-carbon bottles from vendors such as Colgate-Palmolive and Kao now shape stocking decisions at eco-focused retailers.

Page last updated on: