Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 7.89 Billion |

| Market Size (2026) | USD 8.24 Billion |

| Market Size (2031) | USD 10.27 Billion |

| Growth Rate (2026 - 2031) | 4.49% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Shampoo Market Analysis by Mordor Intelligence

Europe shampoo market size in 2026 is estimated at USD 8.24 billion, growing from 2025 value of USD 7.89 billion with 2031 projections showing USD 10.27 billion, growing at 4.49% CAGR over 2026-2031. Within this expansion, Germany contributes the largest country-level share while Poland records the quickest pace, underscoring how demographic aging, premiumization, and stricter product-safety laws are reshaping product portfolios. Specialty offerings most notably natural, organic, and medicated formats outperform mass formulations, helped by salon endorsements, water-saving claims, and dermatologist validation. Tightening rules on microplastics, siloxanes, and sustainable sourcing raise compliance costs but simultaneously favor well-capitalized brands that can reformulate rapidly. Retail dynamics are bifurcating: supermarkets anchor volume, yet online channels led by social commerce capture incremental growth as refill packs and solid bars migrate smoothly to e-commerce.

Key Report Takeaways

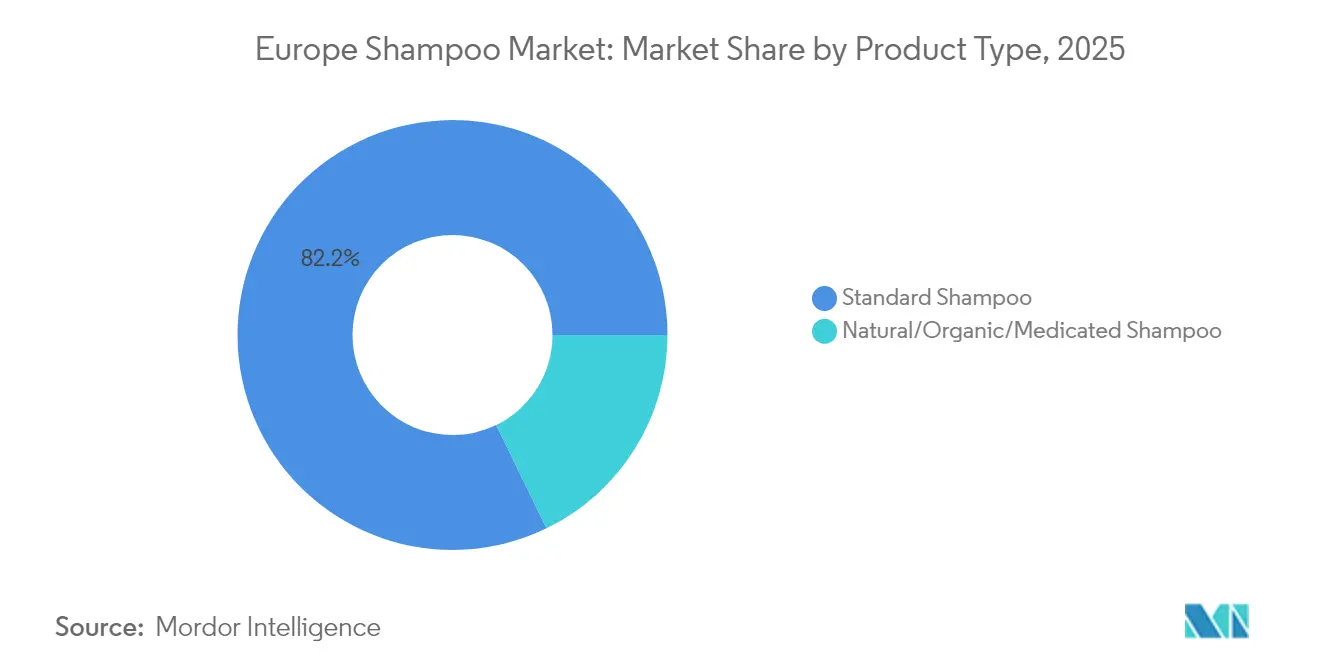

- By product type, standard shampoo held 82.20% of Europe shampoo market share in 2025, whereas natural, organic, and medicated variants are advancing at a 6.26% CAGR through 2031.

- By hair concern, general/multi-purpose products retained 62.65% share of Europe shampoo market size in 2025; specific-purpose formulas such as anti-dandruff and volumizing solutions are accelerating at a 5.78% CAGR to 2031.

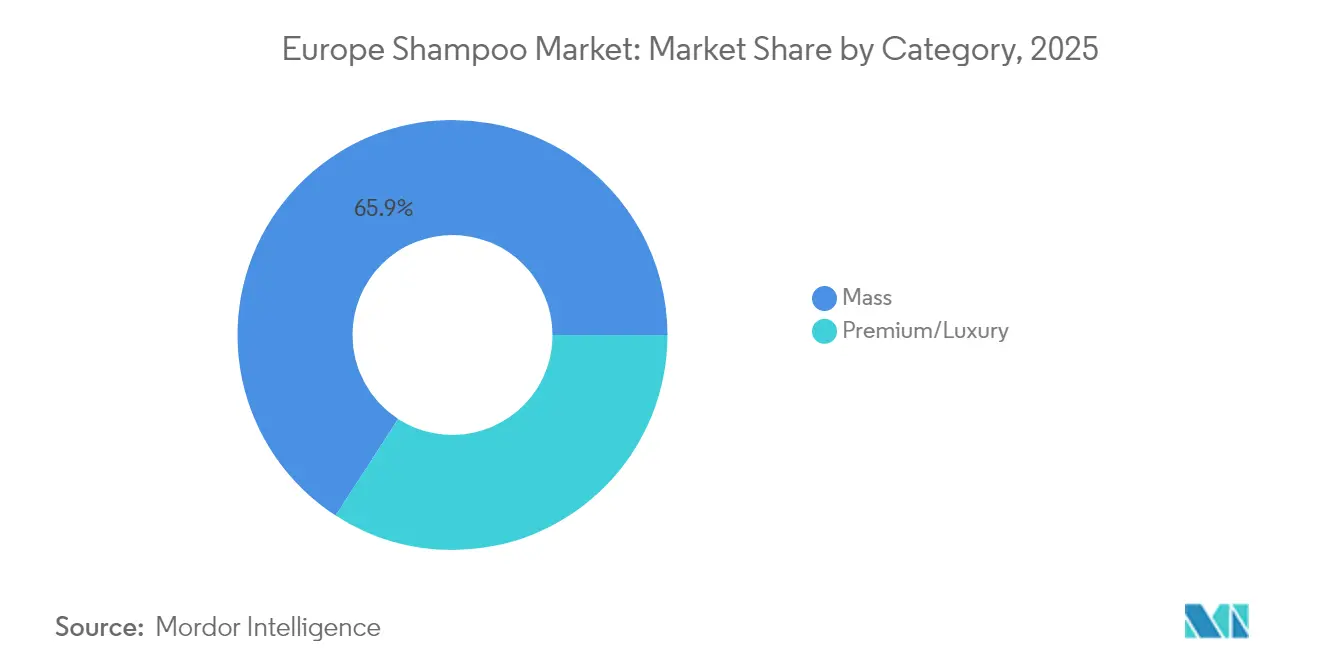

- By category, the mass segment captured 65.85% revenue share in 2025, while premium and luxury lines are forecast to grow at 5.92% CAGR, the fastest among all price tiers.

- By distribution channel, supermarkets and hypermarkets controlled 36.15% of 2025 sales, yet online retail is predicted to post a 5.87% CAGR, the strongest across channels.

- By country, Germany accounted for 22.95% market share in 2025: Poland is projected to grow at a faster CAGR of 6.66% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Shampoo Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising focus on scalp and hair health, boosting demand for specialized and medicated shampoos | +0.8% | Germany, France, United Kingdom, Nordics; spillover to Poland and Spain | Medium term (2-4 years) |

| Strong consumer shift toward natural, organic, sulfate-free and "clean" formulations | +1.2% | Germany, France, Netherlands, Belgium, Sweden; accelerating in Poland and Italy | Short term (≤ 2 years) |

| Premiumization and salon-inspired products increasing average spend per consumer | +0.9% | Germany, United Kingdom, France, Benelux; emerging in Poland and Spain | Medium term (2-4 years) |

| Aging population and rising incidence of hair fall and scalp issues driving medicated ranges | +0.7% | Germany, Italy, France, Spain, Sweden; demographic pressure across all EU27 | Long term (≥ 4 years) |

| Increasing number of salons and barbershops supporting professional and retail shampoo sales | +0.5% | Poland, Germany, France, United Kingdom, Netherlands; urban clusters in Spain and Italy | Medium term (2-4 years) |

| Preference for sustainable, low-waste and recyclable or refillable packaging | +0.6% | Germany, France, Netherlands, Sweden, Belgium; regulatory push Europe-wide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising focus on scalp and hair health, boosting demand for specialized and medicated shampoos

Growing consumer awareness of scalp and hair health is increasingly driving the demand for specialized and medicated shampoos in Europe. Consumers are shifting from basic cleansing products toward formulations that address specific concerns such as dandruff, hair loss, oily scalp, and sensitivity. According to a 2023 report by the National Institute of Health, hair loss in European men can begin as early as puberty, with a lifetime prevalence estimated to be approximately 80% [1]Source: National Center for Biotechnology Information, "Male-pattern hair loss: Comprehensive identification of the associated genes as a basis for understanding pathophysiology", pmc.ncbi.nlm.nih.gov .Rising pollution levels, stress, and frequent styling habits have intensified scalp-related problems, further strengthening demand for functional solutions. Dermatologist-recommended and clinically tested shampoos are gaining traction due to their perceived efficacy. Brands are investing in research to incorporate active ingredients like biotin, zinc pyrithione, salicylic acid, and natural botanicals for targeted benefits. The trend aligns with holistic beauty and wellness movements emphasizing long-term scalp care. Men’s grooming and aging hair segments are contributing new growth opportunities. Overall, scalp and hair health focus is reshaping the Europe shampoo market landscape toward therapeutic and problem-solving innovations.

Strong consumer shift toward natural, organic, sulfate‑free and “clean” formulations

In Europe, there is a strong and growing consumer shift toward natural, organic, sulfate-free, and "clean" shampoo formulations driven by increasing awareness of product safety, ingredient transparency, and sustainability. Consumers increasingly prefer shampoos made with gentle, plant-based ingredients like aloe vera, coconut oil, and tea tree, which nourish hair and scalp without harsh chemicals. Vegan and cruelty-free certifications add further appeal, especially among ethical and environmentally conscious buyers. Retailers are expanding their offerings online and offline, supported by influencer marketing and consumer education on clean beauty. According to research by the CBI ministry of foreign affairs, clean-label products are expected to make up over 70% of product portfolios in 2025 and 2026, rising from 52% in 2021 [2]Source: CBI Ministry of Foreign Affairs, “Which trends offer opportunities,” cbi.eu, underscoring the increasing prioritization of clean, natural product ranges. This consumer preference is reshaping the shampoo market toward more sustainable, health-conscious, and transparent brand innovations. Ultimately, the focus on clean, natural formulations continues to drive new product development and market expansion across Europe’s personal care sector.

Premiumization and salon-inspired products increasing average spend per consumer

The Europe shampoo market is witnessing robust premiumization, as consumers gravitate toward salon-inspired, high-quality products that promise superior performance and luxury experiences. This trend elevates the average spend per consumer through advanced formulations featuring ingredients like argan oil, keratin, and hyaluronic acid, alongside elegant packaging and professional-grade efficacy. A 2023 survey by Professional Beauty highlighted the scale of this shift, revealing that UK consumers spend an average of GBP 4,600 annually on wellness-related products, including shampoos, reflecting deeper integration into self-care routines [3]Source: Professional Beauty, “Brits spend over £4.5K on self-care annually”, professionalbeauty.co.uk . Personalized solutions for concerns like damage repair and volume enhancement further justify higher price points, appealing to affluent demographics. E-commerce and subscription models from direct-to-consumer premium brands foster loyalty and recurring expenditure. Overall, this driver is propelling market value growth, with premium segments outpacing mass-market options across Europe.

Aging population and rising incidence of hair fall and scalp issues driving medicated ranges

The aging population in Europe, coupled with a rising incidence of hair fall and scalp issues, is significantly driving demand for medicated shampoo ranges. Age-related hair thinning and hair loss are increasingly common due to longer life expectancy and demographic shifts, with over 21.6% of the EU population aged 65 and above. Male pattern baldness affects around 40% of men by their mid-30s, and hair fall concerns extend to women, many of whom experience thinning with age or due to conditions like Polycystic Ovary Syndrome (PCOS). This growing prevalence is fueling demand for specialized shampoo products formulated to address scalp health, strengthen hair follicles, and reduce hair loss. Innovations in active ingredients and clinically proven formulations are attracting older consumers seeking effective therapeutic solutions. Market players are expanding medicated and targeted hair care portfolios to meet this demographic trend.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent EU cosmetic and chemical regulations raising formulation and compliance costs | -0.9% | EU27-wide; acute in Germany, France, Netherlands, Sweden (high enforcement) | Short term (≤ 2 years) |

| Market saturation and intense competition among global, local and private-label brands | -0.7% | Germany, United Kingdom, France, Italy, Spain; mature markets with limited shelf space | Medium term (2-4 years) |

| Volatile raw material and packaging costs pressuring manufacturer margins | -0.6% | EU27-wide; supply-chain dependencies on palm oil, oleochemicals, PET | Short term (≤ 2 years) |

| Price-sensitive consumers in some markets limiting premium segment growth | -0.4% | Southern Europe (Italy, Spain, Greece), Eastern Europe (Poland, Romania, Bulgaria) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent EU cosmetic and chemical regulations raising formulation and compliance costs

Stringent EU cosmetic and chemical regulations are raising formulation and compliance costs for shampoo manufacturers, acting as a market restraint in Europe. The EU Cosmetics Regulation (EC No 1223/2009) and its recent updates, including the Omnibus VII Regulation (EU 2025/877), introduce new prohibitions and restrictions on substances considered carcinogenic, mutagenic, or toxic for reproduction (CMR), expanding the banned ingredients list as of September 2025. These regulatory changes require urgent reformulation, updated toxicological assessments, and rigorous supplier management to ensure ingredient purity and compliance. Manufacturers must also revise labeling to reflect allergen and safety information accurately. The increasing demand for transparency and adherence to sustainability and safety standards further complicates product development and supply chain management. Consequently, these strict regulations elevate production costs, limit ingredient options, and may delay new product launches, collectively restraining market growth and innovation in the Europe shampoo sector.

Market saturation and intense competition among global, local and private‑label brands

The market is characterized by intense competition among global multinational corporations, local brands, and private-label products. Major players like L'Oréal SA, Procter & Gamble, Unilever PLC, Kao Corporation, and others hold a dominant presence, leveraging extensive distribution networks and aggressive marketing strategies to maintain market leadership. Simultaneously, local and niche brands compete by focusing on regional preferences and natural or organic product offerings, creating a fragmented and highly competitive landscape. Private-label brands from supermarket chains increasingly challenge premium brands through lower-priced alternatives, intensifying price competition. This saturation results in limited shelf space and heightened pressure on innovation and differentiation. Market players often engage in mergers, acquisitions, and partnerships to consolidate their positions, but these strategies also highlight the challenges of penetrating the market for new entrants. Overall, the saturated nature and fierce rivalry in the market act as significant restraints on growth and profitability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Standard Formulations Anchor Volume, Naturals Capture Growth

The standard shampoo segment dominated the Europe shampoo market in 2025, holding an impressive 82.20% market share. This strong market position can be attributed to entrenched consumer habits favoring familiar, accessible products available at competitive price points. Standard shampoos benefit from their wide availability, especially through supermarkets and hypermarkets, which are the principal distribution channels. Their affordability and proven efficacy make them a staple in most households across the region. Furthermore, the consistent presence of these shampoos on store shelves reinforces consumer trust and brand loyalty. Despite the rising interest in alternatives, conventional shampoos remain the backbone of the product portfolio for many leading brands.

On the other hand, the natural, organic, and medicated shampoo segment is recognized as the fastest-growing category within the Europe market, expanding at a CAGR of 6.26% through 2031. Growth is primarily driven by increasing consumer awareness of the benefits tied to 'clean beauty' products and the endorsement of these formulations by dermatologists. This segment appeals to health-conscious consumers who prioritize ingredient transparency and seek shampoos free from harsh chemicals. Moreover, trends in premiumization and sustainability, including eco-friendly packaging and ethically sourced ingredients, are propelling demand in this space. Brands investing in innovation within this segment see strong consumer engagement and loyalty, particularly among younger demographics.

By Hair Concern: Specific-Purpose Treatments Outpace Multi-Purpose Staples

The general or multi-purpose shampoo segment held the largest share of the Europe shampoo market in 2025, capturing 62.65% of the market. This segment serves the everyday cleansing needs of a broad demographic, making it a staple product in many households. Consumers rely on these shampoos for their versatility and effectiveness in routine hair care. The widespread availability of these products across multiple retail channels enhances their accessibility and appeal. Additionally, familiarity and trust in general shampoos contribute to their dominant market position. Their competitive pricing further entrenches them as the go-to choice for the majority of consumers across the region.

Conversely, the specific-purpose shampoo segment, which includes anti-dandruff, volumizing, strengthening, and hair-regrowth formulas, is the fastest growing, expanding at a compound annual growth rate of 5.78% through 2031. This growth is spurred by increasing consumer demand for targeted hair care solutions backed by clinical evidence. Influencer-led awareness campaigns also play a significant role in educating consumers about the benefits of these specialized shampoos. As consumers become more discerning about their hair needs, products addressing specific concerns gain traction. The combination of scientific validation and strong marketing efforts supports sustained growth in this segment. Consequently, specific-purpose shampoos are carving a growing niche in the Europe shampoo market landscape.

By Category: Mass Dominance Persists, Premium Gains Traction

The mass-category shampoos commanded a dominant 65.85% of the Europe shampoo market share in 2025. This leadership stems from their emphasis on accessibility through key distribution channels like supermarkets, hypermarkets, and drugstores. These outlets prioritize promotional pricing strategies that appeal to cost-conscious consumers across diverse demographics. The segment's strength lies in its broad availability, ensuring it meets the daily hair care needs of the majority. Brand loyalty is reinforced by consistent shelf presence and value-driven marketing campaigns. Overall, mass shampoos remain the cornerstone of the market due to their affordability and widespread reach.

In contrast, the premium and luxury shampoo lines represent the fastest-growing segment, projected to expand at a 5.92% CAGR through 2031. Affluent consumers are increasingly trading up to these products, drawn by advanced salon-inspired technologies that deliver superior performance. Features like refillable packaging align with rising sustainability demands and eco-conscious preferences. This growth reflects a broader premiumization trend among higher-income households seeking personalized hair care experiences. Innovation in formulations, such as natural extracts and customized solutions, further accelerates adoption. As a result, luxury shampoos are steadily gaining ground in a market shifting toward quality over quantity.

By Distribution Channel: Supermarkets Anchor Volume, Online Surges

In 2025, supermarkets and hypermarkets secured the largest distribution share in the Europe shampoo market at 36.15%. These channels thrive on high foot traffic from everyday shoppers seeking convenience and one-stop solutions. Promotional intensity, including frequent discounts and bundled offers, drives impulse purchases and volume sales. Private-label penetration further bolsters their dominance by providing affordable alternatives that align with budget-conscious consumers. Their established infrastructure ensures broad geographic coverage across urban and suburban areas. As a result, these outlets remain the primary anchor for shampoo volume in the region.

Meanwhile, online retail stores represent the fastest-growing distribution segment, projected to expand at a 5.87% CAGR through 2031. This growth reflects surging e-commerce adoption amid digital-savvy consumers prioritizing home delivery and personalized recommendations. Platforms offer extensive product variety, including niche brands unavailable in physical stores. Competitive pricing, subscription models, and loyalty programs enhance customer retention and repeat purchases. The shift is accelerated by mobile shopping apps and seamless integration with social media influencers. Ultimately, online channels are reshaping distribution dynamics with unmatched scalability and data-driven targeting.

Geography Analysis

Germany commanded the largest share of the Europe shampoo market in 2025, holding 22.95% of the total. This dominance is anchored by the country's mature retail infrastructure, which includes extensive networks of supermarkets, hypermarkets, and specialty stores. German consumers exhibit strong brand loyalty and a preference for high-quality, scientifically validated products from leading players like Schwarzkopf and L'Oréal. The nation's high disposable incomes support consistent demand across mass and premium segments alike. Regulatory standards ensure product safety and innovation, further solidifying market leadership. Overall, Germany's established ecosystem makes it the cornerstone of the regional shampoo landscape.

Poland emerged as the fastest-growing country in the Europe shampoo market, projected to expand at a 6.66% CAGR through 2031. This rapid growth stems from rising disposable incomes among an expanding middle class, enabling greater spending on personal care. Increasing salon density caters to heightened grooming awareness and professional services demand. Demographic shifts, including urbanization and a youthful population, fuel adoption of diverse shampoo variants. E-commerce penetration and modern retail formats accelerate product accessibility in emerging urban centers. As a result, Poland is poised to significantly reshape the competitive dynamics of the market.

Other key countries like the United Kingdom, Spain, Italy, and France also play vital roles in the Europe shampoo market. The United Kingdom maintains a strong position through its sophisticated e-commerce channels and consumer focus on natural formulations. Spain benefits from tourism-driven demand and a preference for affordable mass-market options. Italy stands out for premium and luxury shampoos, supported by its fashion-forward culture and production capabilities. France drives innovation with salon-inspired products and sustainability trends, appealing to eco-conscious buyers. Collectively, these nations contribute substantial volume while exhibiting steady growth aligned with regional averages.

Regulatory Landscape

The EU Cosmetic Products Regulation (EC) No 1223/2009 governs cosmetic shampoos across Europe, requiring a responsible person, safety substantiation, and compliance with ingredient restrictions in annexes informed by SCCS opinions.

In 2026 the European Commission adopted Regulation (EU) 2026/78, applicable May 1, 2026, tightening prohibitions for substances classified as CMR and adjusting limits for certain preservatives and related substances, driving reformulation and labeling diligence for both mass and premium shampoos. Regulation (EU) 2026/909 then amended the cosmetics annexes with new ingredient prohibitions and updates to fragrance restrictions, increasing ongoing compliance workload; in June 2026 the European Parliament and Council reached a chemicals omnibus package to simplify cosmetics, labeling (CLP-related), and other rules, signaling steps toward more flexible digital labeling and faster phase-outs for prohibited CMR substances once formally adopted.

Competitive Landscape

The Europe shampoo market displays a moderately fragmented competitive landscape, dominated by a handful of global majors that leverage their scale to maintain equilibrium amid intense rivalry. Companies such as L'Oréal, Unilever, Procter & Gamble, Henkel, and Beiersdorf hold commanding positions through extensive portfolios spanning mass, premium, and specialized products. These players benefit from superior economies of scale, enabling aggressive investments in research and development to innovate formulations like natural, sulfate-free, and sustainable options. Their global footprint ensures robust supply chains resilient to disruptions, while strategic mergers and acquisitions with local brands enhance market penetration.

A key pillar of their dominance lies in unparalleled research and development capabilities, driving continuous product differentiation tailored to European consumer preferences. L'Oréal leads with brands like Garnier and Elseve, focusing on personalized, AI-driven hair diagnostics and clean beauty lines such as Source Essentielle, which emphasize 99% natural-origin ingredients. Unilever counters with Dove and Sunsilk, prioritizing affordability and inclusivity for mass segments while expanding into eco-friendly refillable packaging. Procter & Gamble's Pantene and Head & Shoulders excel in clinical-backed solutions for dandruff and damage repair, backed by extensive consumer testing data. Henkel's Schwarzkopf and Beiersdorf's Nivea target premium salon-inspired technologies, appealing to affluent demographics seeking volumizing and strengthening effects.

Distribution prowess further cements their competitive edge, with optimized networks spanning supermarkets, e-commerce, and professional salons for maximum reach. These majors achieve high shelf visibility through private-label partnerships and promotional campaigns in high-traffic hypermarkets, which hold significant volume shares. Sustainability initiatives, such as recyclable packaging and carbon-neutral production, align with EU green mandates, enhancing brand equity among eco-conscious millennials and Gen Z. While niche players emerge in organic niches, global giants' financial muscle and data analytics ensure they dictate pricing, trends, and market evolution.

Europe Shampoo Industry Leaders

-

The Procter & Gamble Company

-

Unilever PLC

-

L'Oréal S.A.

-

Kao Corporation

-

Beiersdorf AG

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

European market opportunities center on formats and claims that reduce regulatory friction while differentiating performance, notably waterless formats (bars and powders) and refill-oriented systems that align with circularity and packaging reduction objectives. The EU Packaging and Packaging Waste Regulation (PPWR) introduces concrete direction for packaging redesign through mandatory recyclability targets by 2030 and per-capita packaging waste reduction targets (5% by 2030 and 15% by 2040 vs. 2018), pushing brands to prioritize mono-material designs, higher recycled content, and scalable refill packs that translate well to online retail.

Manufacturing and supply chain upgrades create whitespace for faster innovation cycles and localized supply in high-growth pockets such as Poland. Beiersdorf initiated a EUR 300 million expansion of its Poznan production center in June 2025 to double capacity to 500 million units, signaling intensified competition on speed-to-market and quality. Laboratoires Pierre Fabre announced in May 2026 an investment of nearly EUR 50 million to expand and modernize its Avène-les-Bains site with next-generation automation, reinforcing the push toward higher-value, scalp-focused propositions under tighter EU ingredient oversight.

Recent Industry Developments

- April 2026: Unilever launched Dove Scalp + Hair Therapy, extending Dove into scalp-first shampoos and signaling a strategy to deepen scalp-care positioning. The rollout increases competition in problem-solution segments and reinforces the emphasis on clinically framed claims in mass-premium channels.

- June 2025: Beiersdorf started expanding its Poznan production center with a EUR 300 million investment to double output capacity to 500 million units. The project strengthens regional supply for personal care categories and supports faster replenishment and packaging or formulation changeovers in a market shaped by tightening sustainability and ingredient compliance demands.

- July 2024: Unilever highlighted its TRESemme shine-boosting technology work tied to trend-led hair looks, reinforcing the role of performance narratives in mainstream shampoo innovation. This supports the premiumization playbook in supermarkets and e-commerce by translating salon-referenced benefits into scalable retail ranges.

Research Methodology Framework and Report Scope

Market Definition and Coverage

The market is defined as revenues generated from shampoo products sold for hair cleansing and related scalp care across Europe, counted at the point of sale through retail and professional channels, in current USD.

Scope exclusions: This sizing excludes hair conditioners, styling products, hair colorants, and salon services where shampoo is only used as part of a bundled treatment.

Segmentation Overview

-

By Product Type

- Standard Shampoo

- Natural/Organic/Medicated Shampoo

-

By Hair Concern

- General/Multi-purpose

-

Specific Purpose

- Anti-Dandruff and Scalp Health

- Volumizing and Thickening

- Strengthening and Repair

- Hair Regrowth and Hair Repair

-

By Category

- Mass

- Luxury/Premium

-

By Distribution Channel

- Supermarkets / Hypermarkets

- Convenience/Grocery Stores

- Online Retail Stores

- Other Distribution Channels

-

By Country

- Germany

- United Kingdom

- France

- Italy

- Spain

- Belgium

- Poland

- Sweden

- Netherlands

- Rest of Europe

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with building the shampoo demand context and the country-level retail backdrop across Europe. We rely on public statistics and reference series such as Eurostat household consumption and trade tables, UN Comtrade customs data, and national statistical offices for key countries.

To keep the model grounded, we also review sources such as European Commission chemicals and cosmetics related guidance, industry association releases for personal care and retail, and peer reviewed dermatology and cosmetic science journals for usage and product claim trends. Company annual reports, investor presentations, and press releases are used to map brand portfolios, channel priorities, and pricing direction. Where needed, we also use paid subscriptions for company financials and intelligence, news and financials, import and export shipment level checks, and patent databases to validate innovation and ingredient shifts. These desk research sources are illustrative only, and many other public references were used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary interviews and short surveys were used to pressure-test desk assumptions on pricing ladders, promo intensity, channel mix, and what shoppers are shifting to across Europe. Inputs were taken from brand and private label stakeholders, distributors and retailers, participants in the ingredient and packaging ecosystem, and industry experts, and then aligned across Western Europe, Nordics, and Central and Eastern Europe so gaps do not concentrate in one geography.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 14% | |

| Mid tier: 53% | Functional/Unit leaders: 35% | |

| Smaller Players: 14% | Managers: 51% |

Market-Sizing & Forecasting

Sizing starts from a top-down build where national hair care and personal care expenditure, retail turnover indicators, and trade flows are used to reconstruct the shampoo demand pool by country, and then rolled up to Europe. Those totals are then checked through selective bottom-up approximations, such as sampled price per ml by format and channel multiplied by observed sales throughput patterns, before adjustments are finalized.

A few inputs that matter a lot in shampoo are average selling price movement by mass and premium tiers, private label penetration in modern trade, online share in beauty and grocery, claims-led mix shifts (like anti-dandruff or hair fall), and pack size and format changes that affect value per wash. When data is patchy for smaller countries or niche formats, we bridge it using peer-country proxies and distributor feedback, and then re-balance to match the regional totals.

For forecasting, we primarily use scenario analysis supported by trend smoothing. Macro indicators, inflation and promo normalization, and channel mix expectations from interviews are translated into price and volume paths. The final forecast is reviewed to ensure growth stays consistent with realistic consumption and pricing drivers, rather than only extending a historical CAGR.

Data Validation & Update Cycle

Outputs are validated through multiple checks so outliers are caught early, including year-on-year variance scans by country and a reconciliation against independent signals such as retail expansion trends, import dependence shifts, and ingredient driven premiumization. When a number looks off, we re-check the assumption trail, revisit source notes, and re-contact experts if the gap connects to pricing, channel shares, or category definitions.

Before sign-off, the model and write-up are reviewed in more than one analyst pass so the arithmetic and the story stay aligned. Reports are refreshed annually, and interim updates are made when a material event affects Europe-wide demand, supply, or pricing. Right before delivery, a final review is completed so clients receive the latest updated view.

Mordor Intelligence's Europe Shampoo Market Size Measured Against Other Published Estimates

Published sizes for the Europe shampoo market do not always match because each publisher makes different calls on what counts as shampoo, which countries are included, and whether values are measured at retail shelves or closer to manufacturer realizations. Differences also come from how pricing is handled in high inflation years and how much weight is given to online discounting versus list prices.

In our work, the main gap drivers are usually scope and pricing logic, where some estimates fold in adjacent hair cleansing items or treat salon use as part of the market even when it is not sold as a shampoo product. Another common reason is currency timing and update cadence, since older FX assumptions or pre-normalization promo levels can lift or compress the base year. This is why we separate pack size effects and country mix changes before converting and aggregating values, a modeling choice applied by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 7.89 B (2025) | |

| Independent Research House A | USD 7.56 B (2025) | Uses a longer forecast window and typically leans more on historical trend extension, which can keep near-term price normalization and channel mix shifts under-modeled for the base year. |

| Industry Publisher B | USD 9.60 B (2025) | Appears to apply broader category coverage and higher assumed value per unit, which can happen when adjacent cleansing formats or premium pricing benchmarks are blended into shampoo totals. |

The spread in the table mainly comes from what is counted inside the shampoo basket and how price progression is applied across mass and premium tiers. By keeping the inputs tied to observable country demand signals and by documenting each conversion step, we get a figure that is easier to replicate and reconcile when clients compare it with other published numbers.

Key Questions Answered in the Report

How fast is the Europe shampoo market expected to grow through 2031?

It is projected to expand at a 4.49% CAGR, reaching USD 10.27 billion by 2031.

Which product formats are gaining the most traction with European consumers?

Natural, organic, and medicated shampoos lead growth at a 6.26% CAGR as clean formulations and scalp-health claims resonate strongly.

Which country offers the highest growth opportunity for shampoo makers?

Poland shows the quickest pace, forecast at a 6.66% CAGR, driven by rising incomes and a dense salon network.

What distribution channel is expanding fastest for shampoo sales?

Online retail, fueled by social commerce such as TikTok Shop, is recording a 5.87% CAGR across the region.

How are sustainability regulations affecting shampoo packaging strategies?

EU rules on single-use plastics and recycled content push brands toward refill pouches, solid bars, and high-PCR bottles, accelerating eco-design investment.

Page last updated on: