Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

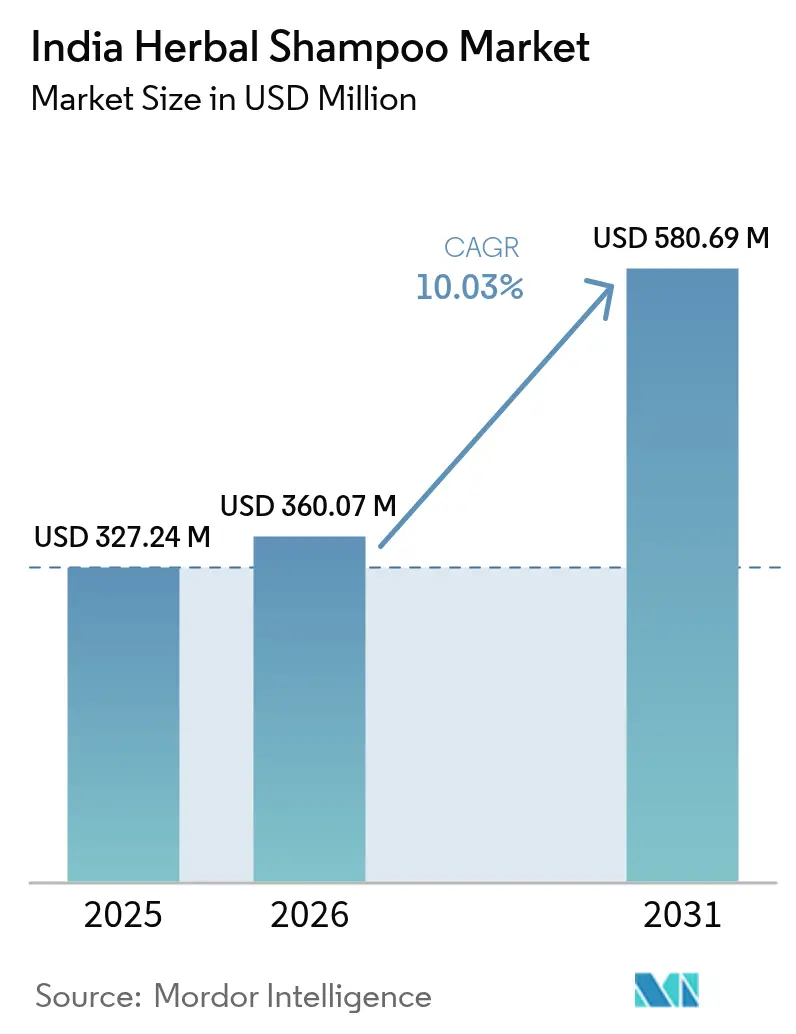

| Base Year Market Size (2025) | USD 327.24 Million |

| Market Size (2026) | USD 360.07 Million |

| Market Size (2031) | USD 580.69 Million |

| Growth Rate (2026 - 2031) | 10.03% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Herbal Shampoo Market Analysis by Mordor Intelligence

The India herbal shampoo market size was valued at USD 327.24 million in 2025 and estimated to grow from USD 360.07 million in 2026 to reach USD 580.69 million by 2031, at a CAGR of 10.03% during the forecast period (2026-2031). This growth is buoyed by rising disposable incomes, governmental backing for Ayurvedic products, and the adoption of clean-label formulations. New product launches, enhanced supply chains via the “One Herb, One Standard” initiative, and the clinical endorsement of botanicals, like the redensyl-enhanced onion extract, are driving consumer acceptance. While established players refine extraction technologies for heightened bio-active potency, emerging digital brands are engaging younger audiences through influencer collaborations and direct sales. Collectively, these dynamics not only underscore a trend towards premiumization but also broaden the appeal of herbal solutions, reaching beyond their traditional user base.

Key Report Takeaways

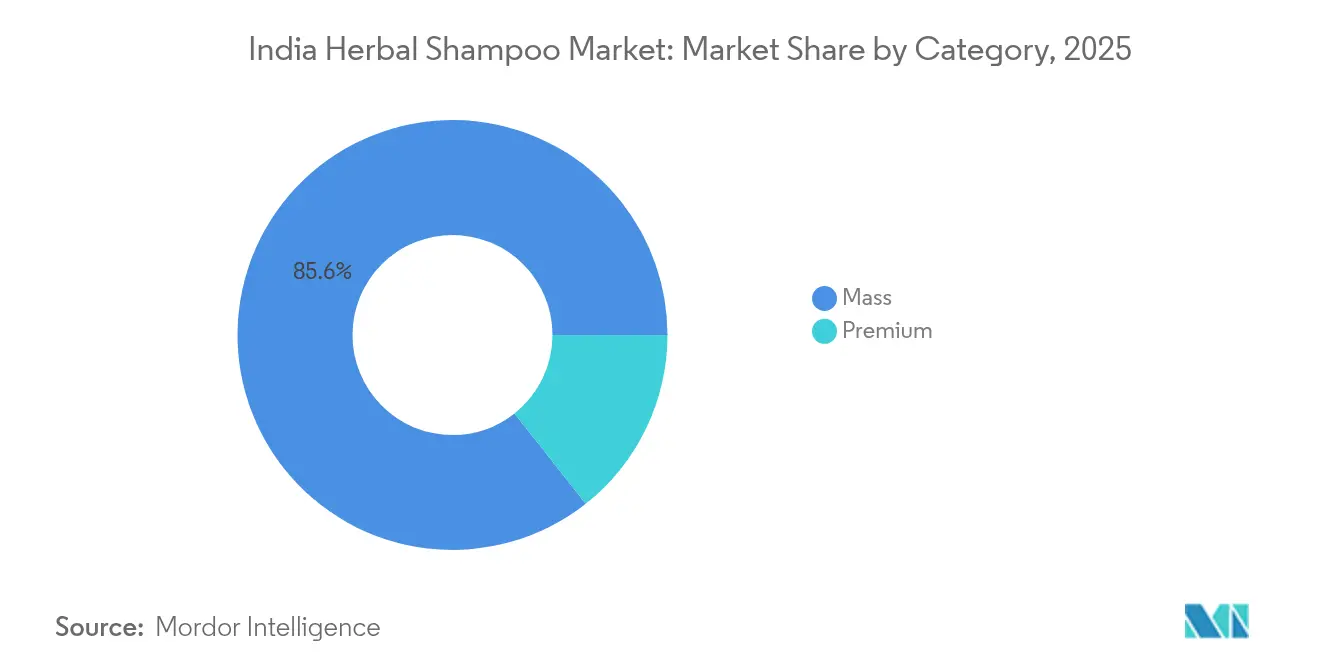

- By category, the mass segment led with 85.64% revenue share of the India herbal shampoo market in 2025, whereas premium lines are advancing at a 10.58% CAGR through 2031.

- By end user, adults accounted for a 93.05% share of the Indian herbal shampoo market size in 2025, while the children’s segment posted the fastest 11.35% CAGR to 2031.

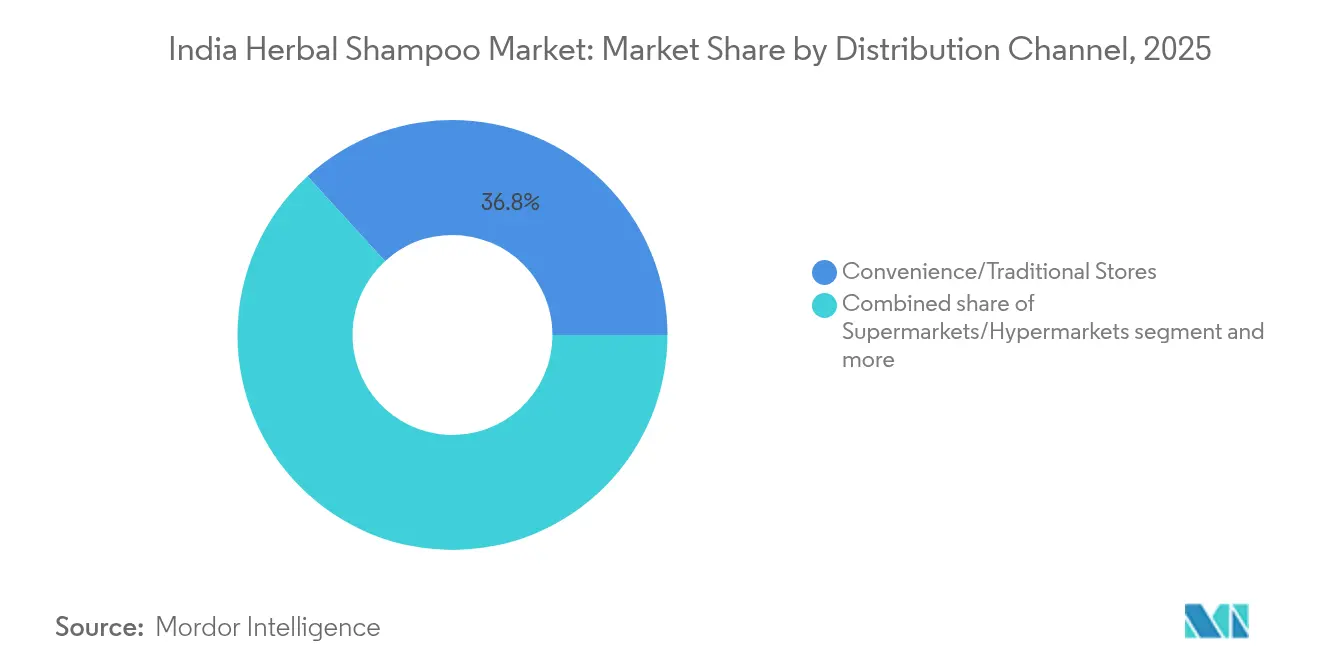

- By distribution channel, convenience and traditional stores captured 36.78% of the Indian herbal shampoo market share in 2025; online retail is expected to expand at a 12.08% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Herbal Shampoo Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Demand for chemical-free and natural formulations | +2.8% | Pan-India, stronger in urban metros and Tier-1 cities | Medium term (2-4 years) |

| Preference for anti-hair loss and scalp treatment solutions | +2.1% | National, with higher adoption in North and West India | Long term (≥ 4 years) |

| Brand innovation, premiumization, and influencer-led marketing | +1.9% | Urban centers, expanding to Tier-2/3 cities | Short term (≤ 2 years) |

| Demand for products customized by hair type and concern | +1.4% | Metro cities, gradually penetrating smaller towns | Medium term (2-4 years) |

| Government AYUSH promotion and tax incentives | +1.2% | National, with manufacturing clusters in Gujarat, Karnataka | Long term (≥ 4 years) |

| Shift toward sulfate-free and paraben-free variants | +0.8% | Urban India, spreading to semi-urban markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Demand for chemical-free and natural formulations

In 2024, industry surveys indicated that most beauty and personal care consumers in India now consciously prefer organic products. This shift extends beyond branding or promotional narratives; it's clearly reflected in actual buying patterns. For instance, brands offering herbal shampoos, especially those with traditional ingredients like onion peel oil and Japanese matcha, boast an impressive 80% user satisfaction rate after just 5-6 washes[1]Source: Detoxie, “Hard Water Relief, Hair Fall Control & Pro Growth Shampoo,” detoxie.in. Urban millennials and Gen-Z consumers, recognized for their careful examination of ingredient labels and strong preference for transparency, are at the forefront of this shift. In turn, companies are responding by reformulating existing products and launching new variants. These innovations avoid synthetic sulfates, parabens, and artificial fragrances, favoring instead clinically validated botanical ingredients.

Preference for anti-hair loss and scalp treatment solutions

Modern dermatological research is increasingly drawing from traditional Ayurvedic knowledge, leading to the emergence of a new category of therapeutic herbal shampoos. As highlighted by the Research Journal of Pharmacy and Technology, these formulations now feature scientifically validated ingredients such as ursolic acid and diosgenin[2]Source: Manju Bhargavi N. et al., “Estimation of Ursolic Acid and Diosgenin in Herbal Hair Oil Formulations,” Research Journal of Pharmacy and Technology, rjptonline.org. Furthermore, analytical methods are being crafted to guarantee consistent potency across batches. Brands are strategically repositioning hair-growth as a prestige offering, reformulating hair-loss treatments with botanically derived, clinically validated formulas, as noted by Cosmetics Business Hair Care Trends 2024. This clinical strategy directly tackles the rising concerns of hair fall among urban Indian consumers, especially in cities where pollution and stress are prevalent. By merging traditional ingredients like bhringaraj and nagarmotha with contemporary delivery systems, these products not only resonate with heritage but also promise tangible results.

Brand innovation, premiumization, and influencer-led marketing

Herbal shampoo brands are being discovered and trialed in new ways, thanks to digital-first marketing strategies. Beauty and personal care brands are turning to social media as their main advertising avenue, finding particular success with content-to-commerce tactics for herbal products. Nykaa, with its 7.4 million unique visitors and a network of over 5,500 creators, is harnessing authentic user-generated content and reviews to boost product trials, as highlighted in the GrowthX Nykaa Analysis. Brands are increasingly leaning into experiential marketing, emphasizing multisensory packaging and tech-driven interactions to forge emotional connections. This strategy resonates especially well with herbal products, where attributes like natural fragrances and unique textures convey benefits more powerfully than conventional ads.

Government AYUSH promotion and tax incentives

AYUSH's systematic approach to standardizing herbal products is fostering a more favorable business climate for compliant manufacturers. The "One Herb, One Standard" initiative has established quality benchmarks for key ingredients in herbal shampoos, thereby minimizing supply chain uncertainties and promoting consistent product formulations[3]Source: Ministry of AYUSH, “AYUSH Initiatives and Programs,” ayush.gov.in. Tax incentives and promotional policies are helping to bolster domestic manufacturing. Notably, companies like Indus Valley Cosmetics are channeling investments, with a USD 4.8 million commitment to research and development facilities in 2024. Meanwhile, the regulatory framework, anchored in BIS standards for cosmetics and AYUSH licensing, not only upholds product quality but also erects barriers to entry. This position establishes players adept in compliance for sustained market leadership.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Counterfeit herbal claims and weak standardization | -1.8% | National, particularly affecting rural and semi-urban markets | Medium term (2-4 years) |

| Supply volatility of certified organic botanicals | -1.4% | Manufacturing clusters in Karnataka, Gujarat, Maharashtra | Long term (≥ 4 years) |

| High formulation cost versus synthetic shampoos | -1.1% | Price-sensitive segments across Tier-2/3 cities | Short term (≤ 2 years) |

| Lack of standardized quality certification | -0.9% | National, with regulatory gaps in enforcement | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Counterfeit herbal claims and weak standardization

Unverified herbal claims and insufficient ingredient validation are fueling consumer distrust and may be constraining market expansion. The FDA’s warnings regarding heavy metal contamination in Indian herbal products highlight persistent quality control shortcomings, issues that also extend to cosmetic formulations. In the absence of clear, uniform standards defining what constitutes “herbal” or “natural” in products such as shampoos, inferior offerings can easily mislead buyers, ultimately undermining the credibility of reputable manufacturers. This lack of standardization is especially problematic in rural and semi-urban markets, where limited awareness of quality markers enables counterfeit products to gain traction through aggressive pricing strategies.

Supply volatility of certified organic botanicals

Climate variability and the restricted cultivation of medicinal plants pose significant challenges to sourcing certified organic botanicals. According to research from the Medicinal Plants Supply Chain, key ingredients, including ashwagandha and other Ayurvedic herbs, face price volatility and availability constraints, disrupting manufacturing schedules. While the National Medicinal Plants Board promotes contract farming and sustainable harvesting practices, these initiatives remain in their infancy, leaving manufacturers exposed to supply disruptions. Furthermore, the demand for consistent chemotype and potency levels in herbal extracts complicates matters, necessitating advanced supply chain management capabilities that smaller players often lack.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Category: Mass Segment Dominance Amid Premium Acceleration

In 2025, mass-market herbal shampoos dominate with an 85.64% market share, underscoring the price-sensitive tendencies of Indian consumers who seek value. Yet, the premium segment is on a robust growth trajectory, boasting a 10.58% CAGR through 2031. This surge is fueled by rising disposable incomes and a growing consumer inclination to invest in perceived quality and efficacy. Notably, haircare constituted about 10% of the luxury beauty market in 2023, highlighting the premiumization trend, as noted in the Luxasia-Kearney Luxury Beauty Report.

Established players like Patanjali and Dabur, with their vast distribution networks and aggressive pricing, dominate the mass segment, using economies of scale to keep prices in check. Meanwhile, premium brands are carving out distinct identities, emphasizing clinical formulations, eco-friendly packaging, and a nod to heritage. Companies like Forest Essentials and Kama Ayurveda are successfully navigating niche markets, steering clear of direct price competition. The rise of D2C brands in the premium arena is reshaping the competitive landscape. Notably, Mamaearth is adeptly straddling the line between mass and premium, leveraging digital-first tactics and a commitment to transparent ingredient communication.

By End User: Adult Dominance with Emerging Children's Market Potential

In 2025, adults command a dominant 93.05% share of the market, underscoring their pivotal role in household personal care decisions. Meanwhile, the children's segment, though smaller, is on an upward trajectory, expanding at an 11.35% CAGR through 2031. Heightened parental concerns over chemical exposure and a growing awareness of scalp sensitivity in young users largely fuel this growth. Supporting this trend, pediatric dermatology research underscores the advantages of gentle, natural formulations for developing scalp and hair follicles. In response, companies are rolling out specialized formulations tailored to children's needs, featuring tear-free solutions and mild cleansing agents sourced from traditional ingredients like shikakai and reetha.

Adults continue to lead in volume growth, diversifying products to tackle concerns such as premature graying, hair thinning, and various scalp conditions. Regional preferences within the adult demographic reveal distinct tastes: North Indian consumers lean towards oil-based treatments, while South Indian markets show a pronounced preference for herbal extracts and Ayurvedic solutions. The children's market, with its vast untapped potential, is witnessing a surge, especially as millennial parents gravitate towards natural alternatives over conventional products. This shift presents a golden opportunity for brands adept at communicating the safety and efficacy of their offerings.

By Distribution Channel: Traditional Retail Resilience Amid Digital Disruption

In 2025, convenience and traditional stores command a 36.78% market share, underscoring the enduring significance of physical retail in personal care purchases. Yet, online retail channels are surging, boasting a robust 12.08% CAGR projected through 2031. This trend highlights a shift in consumer shopping habits and underscores the potency of digital marketing. Notably, this evolution is most evident among younger consumers, with online apps capturing a substantial portion of beauty and personal care spending.

Supermarkets and hypermarkets play a pivotal role in introducing new herbal shampoo brands, offering in-store sampling and education on product benefits. Meanwhile, pharmacy and drug store channels are becoming increasingly relevant for therapeutic herbal formulations, especially those marketed as scalp treatment solutions, capitalizing on the trust associated with healthcare retail. Platforms like Nykaa are spearheading the online beauty and personal care market, while quick commerce players are revolutionizing the landscape with same-day delivery services. This rapid online expansion is compelling traditional brands to refine their digital strategies, all while preserving their physical retail presence.

Competitive Landscape

Market leadership in the Indian herbal shampoo sector is held by Dabur India, Himalaya Global Holdings, Patanjali Ayurved, Unilever’s Lever Ayush, and Honasa Consumer’s Mamaearth, collectively showcasing a moderate concentration profile. In October 2024, Dabur bolstered its position by acquiring Sesa Care for USD 38-42 million, introducing onion-seed and cocoa-protein variants to its Vatika line. Himalaya stands out with its ISO-certified organic facilities, catering to export-driven clients in the Gulf and ASEAN regions. Patanjali, expanding its Haridwar capacity by 40%, not only defends its price leadership against private-label competition but also launches sulfate-free products targeting urban consumers.

Unilever, with its new standalone Beauty and Wellbeing division, underscores its commitment to natural products. Its Lever Ayush range has adopted 60% recycled HDPE packaging and is utilizing AR-based scalp scanners in select malls for tailored solutions. Mamaearth, a digital pioneer, invests an additional USD 15 million into backward integration, ensuring stable botanical sourcing and securing premium turmeric extracts from Erode's contract farms. Meanwhile, smaller players like Detoxie are carving out a niche, targeting urban residents with hard-water challenges, thanks to their patent-pending chelation complexes.

Strategically, major players are prioritizing clinical validation: Dabur is funding randomized trials on bhringraj, Unilever is partnering with IIT-Madras for neem active nano-encapsulation, and Himalaya is pursuing provisional patents for enzyme extraction methods. Innovations in packaging, such as biodegradable cellulose shampoo bars and aluminum-free refill canisters, address waste reduction goals. While influencer-driven newcomers are swiftly gaining traction through social media, they face the challenge of investing in GMP-compliant facilities to meet stringent AYUSH licensing standards. This dynamic landscape not only fuels competition but also elevates performance standards across the Indian herbal shampoo market.

India Herbal Shampoo Industry Leaders

Dabur India Ltd.

Patanjali Ayurved Ltd.

Himalaya Global Holdings Ltd.

Unilever PLC (Lever Ayush)

Honasa Consumer Pvt. Ltd. (Mamaearth)

- *Disclaimer: Major Players sorted in no particular order

Geography Analysis

India's herbal shampoo market is shaped by regional characteristics, influenced by cultural preferences, climate conditions, and economic development. In the northern states, especially Punjab, Haryana, and Uttar Pradesh, there's a pronounced preference for oil-based herbal treatments. Traditional ingredients like amla and bhringaraj are favored, underscoring the regions' deep-rooted Ayurvedic practices. Major manufacturing clusters in Gujarat and Karnataka bolster the supply chain. Companies such as Patanjali utilize their Haridwar facility, while Himalaya operates from Bangalore, both efficiently catering to national markets. In the west, states like Maharashtra and Gujarat are more open to premium herbal formulations and innovative ingredients, a trend buoyed by higher disposable incomes and urban lifestyles.

Southern states, especially Tamil Nadu and Kerala, have a pronounced cultural affinity for herbal and Ayurvedic products, leading to high adoption rates of traditional formulations. With an established infrastructure for cultivating and processing medicinal plants, local manufacturers enjoy a competitive edge. Consumers in these states possess a sophisticated understanding of herbal ingredients and their benefits. Additionally, Karnataka's status as a technology hub is fostering the rise of digital-first brands, with cities like Bangalore emerging as prime test markets for D2C herbal shampoo brands. The state's regulatory landscape, shaped by central AYUSH policies and local industrial promotion schemes, is conducive to herbal product manufacturing and export.

In the eastern and northeastern regions, states like West Bengal and Assam are increasingly embracing herbal personal care products, signaling emerging growth opportunities. The region's rich biodiversity offers unique botanical ingredients, yet its supply chain infrastructure lags behind western manufacturing hubs. Consumers here prefer affordable herbal formulations that clearly outshine synthetic alternatives in value. The rise of organized retail and e-commerce is unlocking new distribution channels, bolstered by government initiatives that champion traditional industries and local herbal product development. Furthermore, regional climate variations dictate formulation strategies: humid coastal areas lean towards lighter formulations, while the dry northern plains gravitate towards more moisturizing variants.

Recent Industry Developments

- October 2024: Dabur India completed the acquisition of Sesa Care for USD 38-42 million, expanding its herbal hair care portfolio and strengthening market position in South India. This strategic move eliminates a regional competitor while adding specialized formulations to Dabur's product range, supporting the company's premiumization strategy in herbal personal care.

- February 2024: Herbal Essences launched 11 Newly Formulated Shampoos and Conditioners that are herbal in nature. Every new blend contains pure aloe and camellia oil, certified by The Royal Botanic Gardens, KEW plant specialists.

India Herbal Shampoo Market Report Scope

A herbal shampoo is infused with extracts of herbs and plant ingredients. It is generally free of harsh chemicals and offers long-lasting effects.

The Indian herbal shampoo market is segmented by distribution channel into supermarkets/hypermarkets, convenience stores, specialty stores, online stores, and other distribution channels.

The market sizing has been done in value terms in USD for all the abovementioned segments.

By Category

| Mass |

| Premium |

By End User

| Adults |

| Children/Kids |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Pharmacy and Drug Store |

| Convenience/Traditional Stores |

| Online Retail Stores |

| Other Distribution Channels |

| By Category | Mass |

| Premium | |

| By End User | Adults |

| Children/Kids | |

| By Distribution Channel | Supermarkets/Hypermarkets |

| Pharmacy and Drug Store | |

| Convenience/Traditional Stores | |

| Online Retail Stores | |

| Other Distribution Channels |

Key Questions Answered in the Report

What is the 2026 value of the India herbal shampoo market?

It is valued at USD 360.07 million in 2026.

How fast will the market grow through 2031?

The forecast calls for a 10.03% CAGR, taking value to USD 580.69 million.

Which consumer segment is expanding the quickest?

Premium herbal shampoos are advancing at a 10.58% CAGR, outpacing mass products.

Why are online channels important for herbal shampoo sales?

E-commerce platforms offer ingredient filters, influencer reviews, and same-day delivery, enabling 12.08% CAGR for online sales.

What are the main growth restraints?

Counterfeit claims eroding trust and volatility in certified botanical supply remain key challenges.

Page last updated on: