Milk Replacers Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

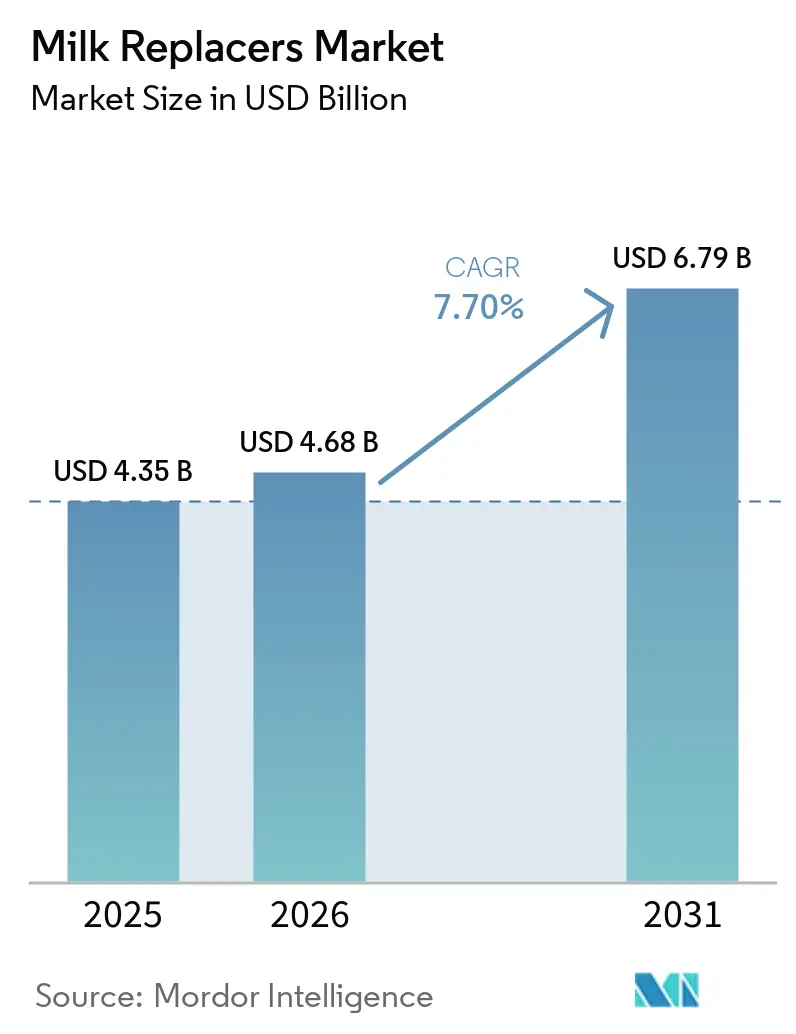

| Market Size (2026) | USD 4.68 Billion |

| Market Size (2031) | USD 6.79 Billion |

| Growth Rate (2026 - 2031) | 7.70% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Milk Replacers Market Analysis by Mordor Intelligence

The milk replacers market size is projected to grow from USD 4.35 billion in 2025 and USD 4.68 billion in 2026 to USD 6.79 billion by 2031, registering a CAGR of 7.7% between 2026 and 2031. Growth is driven by factors such as automated feeding systems that reduce labor requirements, regulatory measures limiting the use of routine antibiotics, and carbon-labeling initiatives promoting low-emission formulations. Technological advancements in membrane filtration enable processors to recover high-value whey fractions, supporting competitive pricing in the milk replacers market. Additionally, e-commerce platforms are increasing access to premium formulations, while precision sensors integrate feeder data with formulation updates, creating a feedback loop that enhances lifetime animal productivity.

Key Report Takeaways

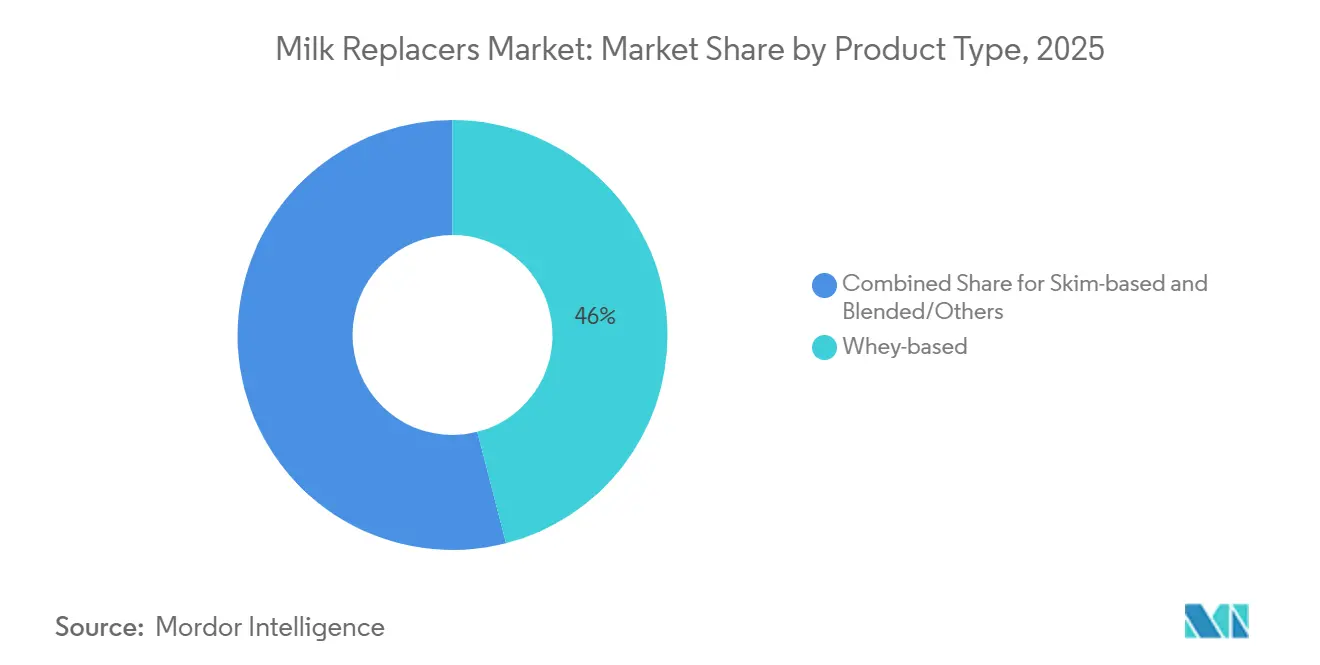

- By product type, whey-based led with the largest 46% of the milk replacers market share in 2025. The blended/others market size is projected to expand at the fastest 8.9% CAGR from 2026 to 2031.

- By livestock, calves held the largest 68% of the milk replacers market share in 2025. Piglets market size is anticipated to advance at the fastest 9.4% CAGR from 2026 to 2031.

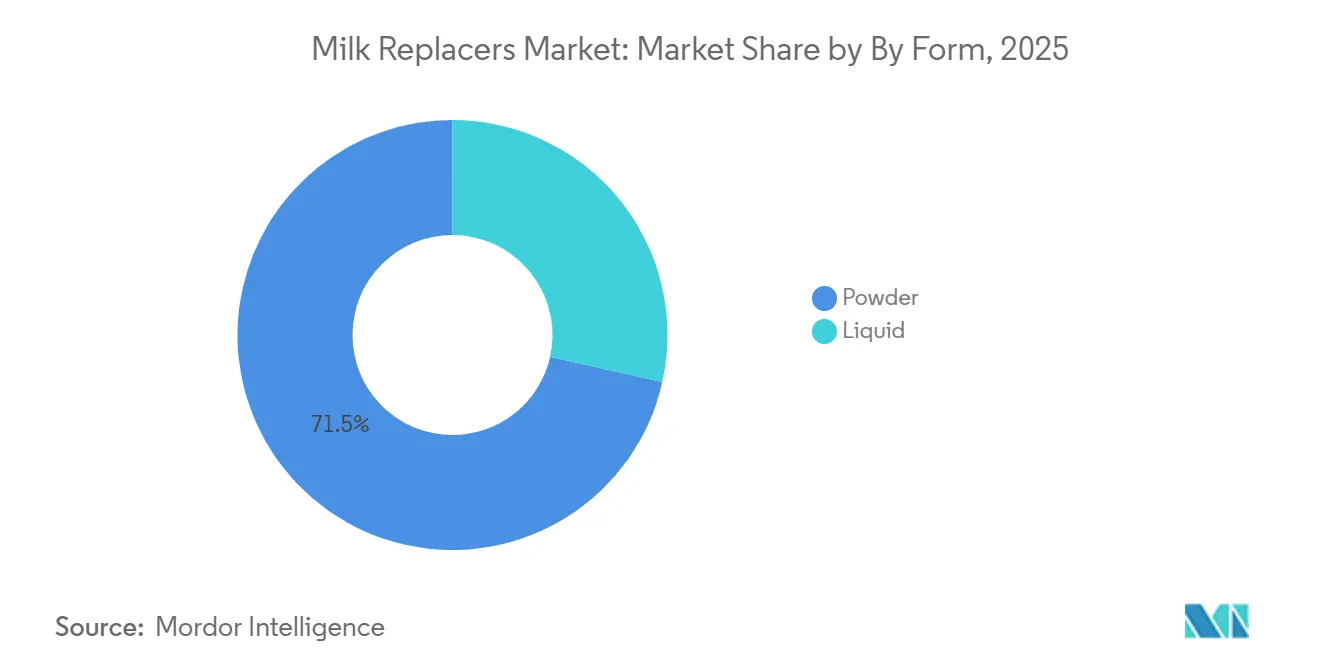

- By form, powder captured the largest 71.5% of the milk replacers market share in 2025. Liquid market size is projected to grow at the fastest 8.1% CAGR from 2026 to 2031.

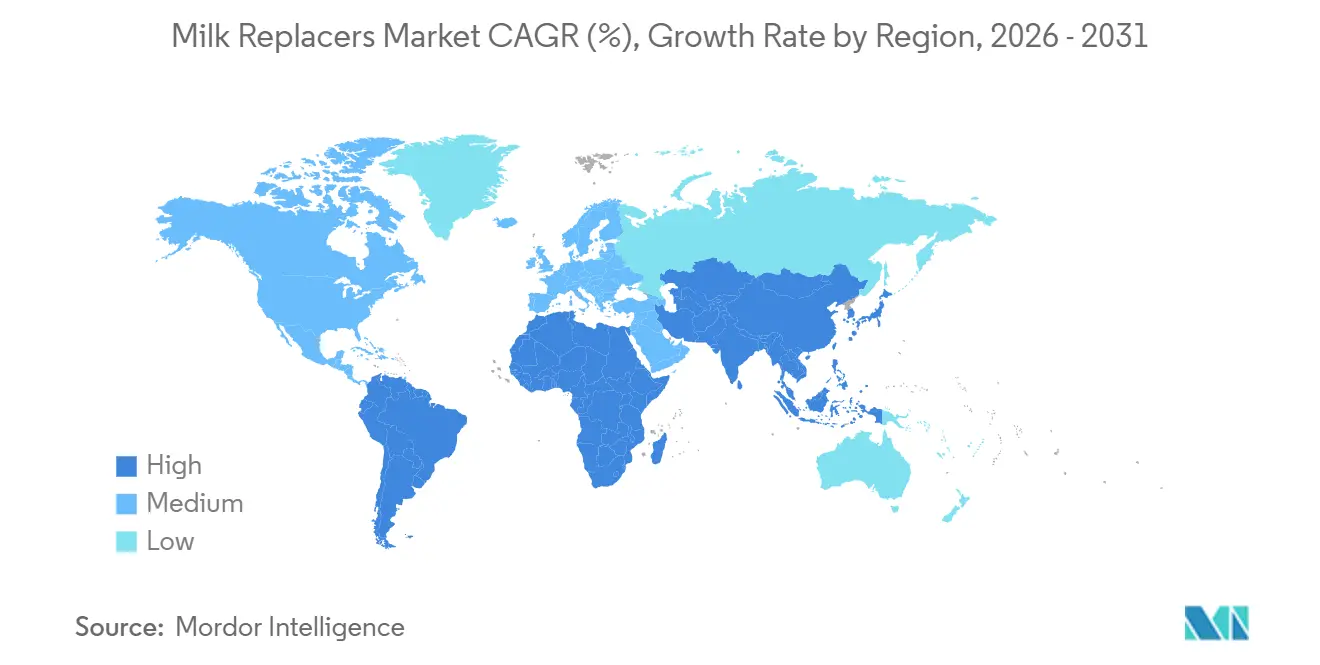

- By geography, Europe dominated with the largest 34% of the milk replacers market share in 2025. Asia-Pacific market size is projected to grow at the fastest 8.7% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Milk Replacers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for early-life nutrition solutions | +1.2% | Global, strongest in Asia-Pacific and Europe | Medium term (2-4 years) |

| Growth of whey-protein technologies improving efficiency | +0.9% | North America and Europe | Long term (≥4 years) |

| Increasing biosecurity concerns and antibiotic mandates | +1.0% | Global, led by North America, European Union, and China | Short term (≤2 years) |

| Expanding e-commerce in farm input procurement | +0.8% | Global, early gains in North America and Europe | Medium term (2-4 years) |

| Precision feeding sensors enabling customization | +0.7% | North America and Europe, spillover to Asia-Pacific | Long term (≥4 years) |

| Carbon-footprint labeling influencing feed choices | +0.5% | Europe and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Early-Life Nutrition Solutions

Early-life nutrition is widely acknowledged as a critical factor in enhancing livestock productivity and ensuring long-term farm profitability, contributing to the growing adoption of milk replacers. Optimized feeding strategies during the pre-weaning phase support improved growth, stronger immunity, and better lifetime performance in calves. According to research from Trouw Nutrition B.V. (Nutreco N.V.), enhanced calf nutrition programs can boost first-lactation milk yield by approximately 400 liters per cow, highlighting significant long-term economic advantages [1]Source: Trouw Nutrition, “A LifeStart Calf Feeding Program Increases First Lactation Milk Yield,” trouwnutrition.com.

Growth of Whey-Protein Technologies Improving Efficiency

Advancements in whey-processing technologies are enhancing the efficiency and nutritional profile of milk replacers, driving their adoption in livestock systems. Processes such as ultrafiltration and enzymatic treatment improve protein digestibility and facilitate the production of customized nutritional fractions for young animals. According to the United States Department of Agriculture National Agricultural Statistics Service, total dry whey production in the United States reached 853 million pounds (USD 1,147 million) in 2024, highlighting its substantial availability for feed and nutrition applications [2]Source: United States Department of Agriculture National Agricultural Statistics Service, “Dairy Products Annual Summary,” nass.usda.gov. This expanding supply base improves cost efficiency and promotes the broader use of whey-based formulations in the milk replacers market.

Increasing Biosecurity Concerns and Antibiotic Mandates

Regulatory pressure on antibiotic use in livestock is driving changes in feeding strategies and increasing the demand for functional milk replacers. The European Commission's Regulation (EU) 2019/6, effective from 28 January 2022, prohibits the use of antibiotics for disease prevention in groups of animals and limits antimicrobial use to justified therapeutic cases. This regulatory change is prompting producers to adopt preventive nutrition solutions, such as milk replacers fortified with probiotics, organic acids, and bioactive compounds, to support calf health. Additionally, the regulation aligns with the EU's goal of reducing antimicrobial sales in farmed animals by 50% by 2030, accelerating the shift toward non-antibiotic health management practices. Consequently, milk replacers are increasingly designed to improve immunity and gut health, meeting stricter biosecurity requirements and promoting sustainable livestock production systems.

Expanding E-Commerce in Farm Input Procurement

The study "Rural Agricultural Development Through E-Commerce Platforms (2024)" explains that digital platforms allow farmers to directly access agricultural products and services while connecting them with a wider network of suppliers. It emphasizes that e-commerce reduces dependence on intermediaries and enhances procurement efficiency through improved price transparency and market access. This transition indirectly supports the milk replacers market by increasing overall procurement efficiency and enabling livestock producers to utilize modern purchasing channels for specialized nutrition products.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in dairy-derived raw-material prices | −0.8% | Global | Short term (≤2 years) |

| Competition from plant-based and fermented alternatives | −0.5% | North America and Europe | Medium term (2-4 years) |

| Regulatory scrutiny on antimicrobial residues | −0.4% | Global, led by European Union and North America | Short term (≤2 years) |

| Cold-chain logistics challenges for liquid formats | −0.3% | Asia-Pacific, Middle East, and Africa | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Volatility in Dairy-Derived Raw-Material Prices

Fluctuations in dairy-derived raw material prices are evident in the official whey price trends, a critical component in milk replacer formulations. According to the United States Department of Agriculture, dry whey prices rose from USD 0.4198 per pound (USD 925.7 per metric ton) in January 2023 to USD 0.6544 per pound (USD 1,442.6 per metric ton) in December 2024, and further increased to USD 0.6955 per pound (USD 1,533.3 per metric ton) in January 2026. These significant price changes highlight instability caused by supply-demand dynamics in dairy markets. As whey represents a substantial portion of milk replacer costs, such volatility directly impacts production expenses, reduces profit margins, and exerts pricing pressure on the milk replacers market.

Competition from Plant-Based and Fermented Alternatives

The growing adoption of plant-based and fermentation-derived protein alternatives is increasing competition in the market. These alternatives are attracting attention due to their cost-effectiveness, sustainability attributes, and improving nutritional profiles. Developments in precision fermentation and plant protein processing are facilitating the creation of formulations that can partially replace traditional dairy-based ingredients. This trend is prompting some producers to consider non-dairy options, especially in cost-sensitive operations. As advancements in alternative proteins progress, traditional manufacturers are under rising pressure to differentiate their products and sustain their market position.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Whey Dominates, Blends Gain Traction

Whey-based milk replacers are projected to account for the largest share, 46%, of the milk replacers market in 2025. Whey remains a preferred ingredient due to its high digestibility and well-established supply chains in major dairy-producing regions, including the Netherlands and New Zealand. Its consistent nutritional profile supports early-life animal growth and immunity, making it a key component in calf nutrition programs. Additionally, the availability of whey as a by-product of cheese production enhances its cost competitiveness, reinforcing its dominance in large-scale dairy operations.

The blended/others market size is anticipated to grow at a robust CAGR of 8.9% from 2026 to 2031, primarily driven by the need to address raw material price fluctuations and enhance formulation flexibility. Manufacturers are increasingly utilizing plant-based proteins and fermentation-derived ingredients to reduce reliance on dairy inputs. These blended formulations facilitate cost optimization while maintaining nutritional efficacy. Developments in enzyme-treated proteins are enhancing amino acid availability, promoting wider adoption. As sustainability and cost efficiency become more critical, blended milk replacers are positioning themselves as a practical option for diversified livestock feeding strategies.

By Livestock: Calves Lead, Piglets Accelerate

Calves held the largest 68% of the milk replacers market share in 2025. This dominance is attributed to dairy farm economics, where using milk replacers allows whole milk to be diverted for commercial sale, thereby improving profitability while ensuring adequate calf nutrition. Calf-specific formulations are widely adopted due to their benefits in enhancing early growth, immunity, and long-term productivity. Large dairy operations increasingly rely on milk replacers to standardize feeding practices and optimize herd management.

The piglets market size is projected to grow at the fastest CAGR of 9.4% from 2026 to 2031. This growth is driven by the recovery in global swine production and a heightened focus on early-weaning practices. Milk replacers play a critical role in reducing stress during transition phases and improving piglet survival rates. The expansion of commercial pig farming, particularly in the Asia-Pacific region, is fueling demand for specialized formulations. Producers are increasingly adopting milk replacers to enhance feed efficiency and maintain herd health under intensive farming conditions, thereby strengthening the role of milk replacers in non-dairy livestock markets.

By Form: Powder Prevails, Liquid Gains Ground

Powdered milk replacers accounted for the largest market share of 71.5% in 2025. This dominance is attributed to their longer shelf life, ease of storage, and lower transportation costs compared to liquid alternatives. These characteristics make powdered formulations particularly suitable for regions with limited cold-chain infrastructure and extensive distribution networks. Farmers favor powdered products due to their flexibility in mixing and dosage control. Additionally, the efficient storage and transportation of powdered milk replacers contribute to their widespread adoption in both developed and emerging agricultural markets.

The liquid milk replacers market size is projected to grow at the fastest CAGR of 8.1% from 2026 to 2031. This growth is driven by the increasing adoption of automated feeding systems and precision livestock farming practices. Liquid formulations offer reduced preparation time and consistent nutrient delivery, enhancing feeding efficiency. Their use is expanding in large-scale dairy operations where labor optimization is a priority. Investments in cold-chain infrastructure and advancements in shelf-stable liquid concentrates are further supporting their adoption. As automation in livestock farming continues to rise, liquid milk replacers are becoming a preferred solution for convenient and efficient feeding.

Geography Analysis

Europe is projected to hold the largest market share of 34% in 2025, driven by intensive dairy farming practices in countries such as the Netherlands, France, and Germany. The region benefits from strong regulatory frameworks that promote sustainable livestock production and efficient feed utilization, encouraging the adoption of specialized nutrition solutions. Additionally, established dairy supply chains and advanced herd management practices contribute to robust regional demand. Producers in Europe prioritize high-quality feeding systems to enhance productivity while adhering to environmental standards. These structural advantages position Europe as a leading region in livestock nutrition and dairy efficiency.

The Asia-Pacific market size is projected to register the fastest CAGR of 8.7% from 2026 to 2031, driven by the growth of livestock populations and the increasing commercialization of dairy and swine farming. According to the Food and Agriculture Organization, Asia accounted for 46% of global milk production in 2023, supported by significant output growth in China and India. This substantial share is attributed to the rapid expansion of dairy herds and improvements in productivity, which have increased the demand for efficient calf nutrition solutions, such as milk replacers, thereby contributing to the region's growth.

Regional dynamics highlight differences in dairy intensity and calf-rearing practices across markets. Developed regions like North America and Europe exhibit higher adoption rates of structured feeding systems, while emerging regions are gradually transitioning toward commercial nutrition solutions. According to the Food and Agriculture Organization, the use of milk replacers instead of whole milk during early calf-rearing stages can reduce liquid milk consumption by up to 50%, improving farm-level milk availability for sale[3]Source: Food and Agriculture Organization of the United Nations, “Rearing Young Ruminants on Milk Replacers and Starter Feeds, FAO Animal Production and Health Manual No. 13,” fao.org. This efficiency advantage is driving adoption in regions focused on enhancing dairy profitability and optimizing resource utilization.

Competitive Landscape

The industry is moderately consolidated, with key players including Cargill, Incorporated, Archer-Daniels-Midland Company, Land O’Lakes, Inc. (Purina Animal Nutrition LLC), FrieslandCampina Ingredients B.V., and Trouw Nutrition B.V. (Nutreco N.V.). These companies leverage vertically integrated supply chains, extensive distribution networks, and advanced research capabilities. For example, in 2024, Trouw Nutrition B.V. (Nutreco N.V.) launched Sprayfo Ultimo, a calf milk replacer aimed at supporting early-life development and enhancing herd productivity.

Competition within the market is increasing as companies focus on product innovation, strategic partnerships, and geographic expansion to strengthen their market position. For instance, in 2024, Volac Milk Replacers Limited introduced a new skim milk-based calf milk replacer to address farmers' demand for this specific dairy protein formulation. The new product, Flourish Calf, features a 23% all-dairy protein and 19% fat composition, with a 50% skim content. It is further enriched with a tested package of calf health ingredients, along with increased levels of vitamins and minerals. This highlights a broader industry trend toward advanced formulations.

Competitive dynamics are also shaped by product performance and nutritional outcomes. Research from the United States Department of Agriculture indicates that calves achieving optimal nutrition programs, including milk replacer feeding, can reach average daily gains above 0.82 kg per day, highlighting the importance of formulation quality in improving growth performance and driving product differentiation across the industry[4]Source: United States Department of Agriculture Animal and Plant Health Inspection Service, “Average Daily Gain in Preweaned Holstein Heifer Calves,” usda.gov. As producers increasingly prioritize performance-based feeding strategies, companies are focusing on high-quality ingredients and functional additives. This emphasis on measurable productivity improvements is intensifying competition and fostering advancements in formulation technologies across the industry.

Milk Replacers Industry Leaders

Cargill, Incorporated

Land O’Lakes, Inc. (Purina Animal Nutrition LLC)

Trouw Nutrition B.V. (Nutreco N.V.)

Archer-Daniels-Midland Company

FrieslandCampina Ingredients B.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Denkavit Futtermittel GmbH intends to launch the joint venture under the name “Denkavit MILCH plus” on 1 June 2026. The venture will oversee nationwide sales of milk replacers and enhance the company's distribution network. This initiative aims to expand market reach and improve the availability of calf milk replacer products in key regions.

- October 2025: De Heus Animal Nutrition established its first dedicated feed mill in India. The facility will produce dairy and young animal nutrition products. This initiative aims to localize production and develop formulations tailored to the needs of regional dairy farmers, enhancing the company's presence in high-growth markets.

- November 2024: Trouw Nutrition B.V. (Nutreco N.V.) launched Sprayfo Ultimo, a calf milk replacer formulated to replicate the fatty acid composition of cow’s milk and support early-life development. The product is designed to improve gut health, enhance resilience, and facilitate earlier breeding performance in calves.

Global Milk Replacers Market Report Scope

Milk replacers are formulated feed products developed to replace whole milk in the early-life nutrition of young animals, including calves and piglets. These products typically consist of a balanced combination of proteins (mainly whey-based), fats, vitamins, and minerals to promote growth, immunity, and digestive development. The milk replacers market report is segmented by product type (whey-based, skim-based, and blended or other product), by livestock (calves, lambs, piglets, and companion animals), by form (powder and liquid), and by geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The forecasts are provided in terms of value (USD).

| Whey-based |

| Skim-based |

| Blended/Others |

| Calves |

| Lambs |

| Piglets |

| Companion Animals |

| Powder |

| Liquid |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Product Type | Whey-based | |

| Skim-based | ||

| Blended/Others | ||

| By Livestock | Calves | |

| Lambs | ||

| Piglets | ||

| Companion Animals | ||

| By Form | Powder | |

| Liquid | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the projected global milk replacers market size in 2031?

The milk replacers market size is forecast to reach USD 6.79 billion by 2031 with a CAGR of 7.7% from 2026 to 2031.

Which format is projected to grow quickest from 2026 to 2031?

Liquid concentrates are set to expand at the fastest 8.1% CAGR from 2026 to 2031.

Which geographic region is forecast to add the most new demand by 2031?

Asia-Pacific market size is projected to grow at the fastest 8.7% CAGR from 2026 to 2031.

What portion of 2025 sales flowed through traditional distributors?

Distributors accounted for the largest 53.0% market share in 2025.

Page last updated on: