Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 3.82 Billion |

| Market Size (2026) | USD 4.01 Billion |

| Market Size (2031) | USD 5.11 Billion |

| Growth Rate (2026 - 2031) | 4.97% CAGR |

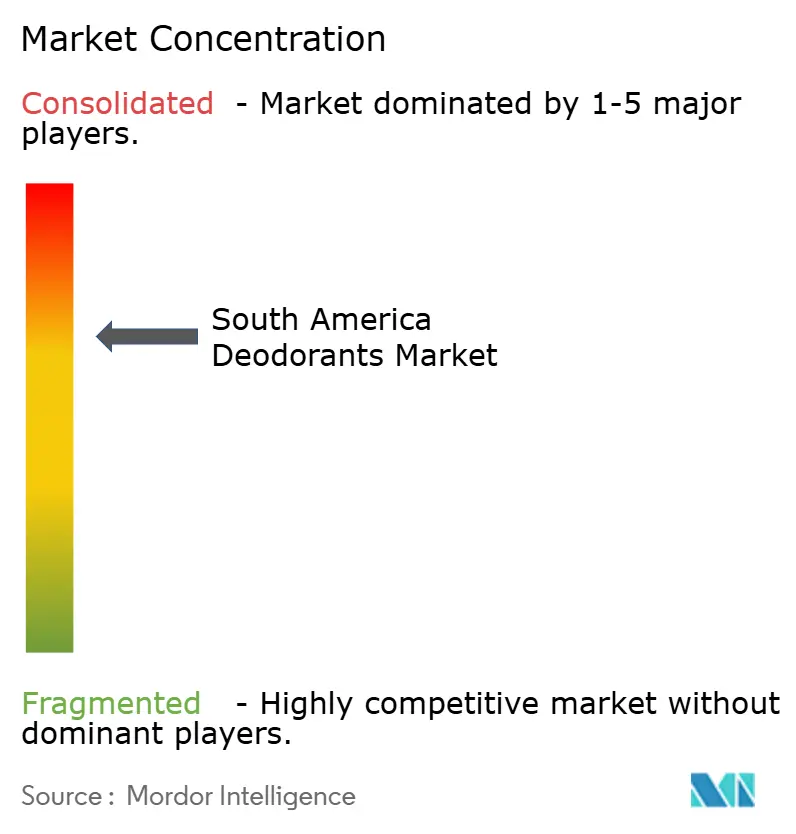

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Deodorants Market Analysis by Mordor Intelligence

The South American deodorants market size was valued at USD 3.82 billion in 2025 and estimated to grow from USD 4.01 billion in 2026 to reach USD 5.11 billion by 2031, at a CAGR of 4.97% during the forecast period (2026-2031). In South America, demand for deodorant is surging, driven by heightened personal hygiene awareness, a burgeoning middle class with rising disposable incomes, and a tropical climate that underscores the need for effective odor control. As consumers become increasingly aware of health concerns tied to ingredients like aluminum compounds and parabens, there's a marked pivot towards natural, organic, and aluminum-free deodorant formulations. While this shift isn't a direct result of government mandates, it's largely fueled by health-conscious consumer behavior and public health campaigns that elevate personal care standards. Moreover, industry associations, including those linked to Brazilian jiu-jitsu, subtly champion hygiene norms, like deodorant use, underscoring a societal shift that values grooming and cleanliness in both public and professional spheres. Reflecting this market evolution, 2024 and 2025 witnessed notable product launches and strategic maneuvers: In January 2025, Unilever debuted its Sure Whole Body Deodorant and Lynx Lower Body Spray lines, catering to the rising consumer demand for multifunctional odor protection. March 2024 saw Native, a brand with a keen focus on health-conscious consumers, introduce its Whole Body Deodorant line, boasting clinically validated 72-hour odor protection with an emphasis on natural ingredients. Further solidifying the trend, Procter & Gamble, in May 2024, bolstered its portfolio in the burgeoning natural segment by acquiring Native, a direct-to-consumer brand known for its natural deodorants. These developments underscore the proactive stance of major brands in addressing the region's evolving consumer preferences, emphasizing efficacy, natural ingredients, and specialized product applications.

Key Report Takeaways

- By product type, sprays retained a 47.98% revenue lead in 2025; roll-ons are projected to advance at a 5.95% CAGR through 2031.

- In 2025, the Mass segment dominated the South American deodorants market, holding a 67.92% share. Meanwhile, the Premium segment is projected to expand at a CAGR of 7.01% by 2031.

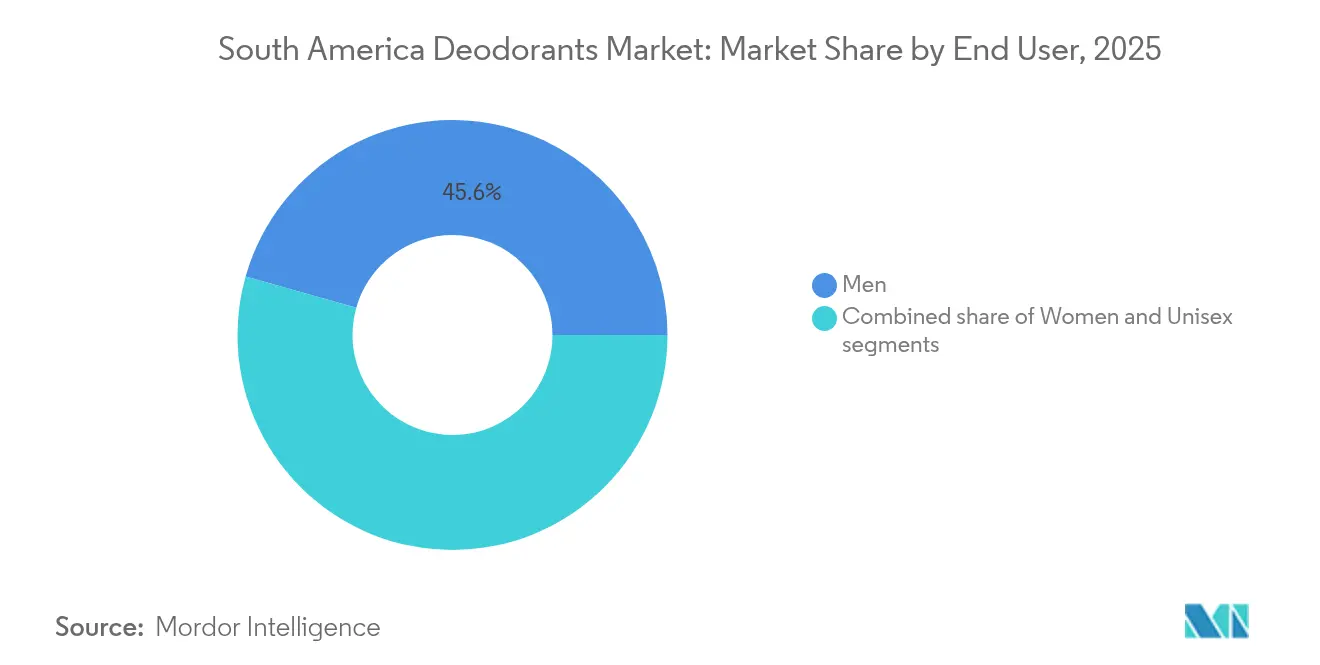

- In 2025, the Men segment accounted for 45.61% of the South American deodorants market. Looking ahead, the Unisex segment is anticipated to witness a growth rate of 7.45% CAGR by 2031.

- By distribution channel, supermarkets and hypermarkets contributed 38.12% of 2025 sales, while online retail is forecast to grow 7.58% annually to 2031.

- In 2025, Brazil accounted for 61.10% of the South American deodorants market. Looking ahead, Colombia is anticipated to witness a growth rate of 5.27% CAGR by 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South America Deodorants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising disposable incomes and trading up to premium formats | +1.2% | Brazil, Colombia, Chile; spillover to Argentina and Peru as inflation stabilizes | Medium term (2-4 years) |

| Health-oriented shift toward aluminum-free and natural formulations | +1.0% | Regional, with the strongest adoption in Brazil's urban centers and the Colombian middle class | Long term (≥ 4 years) |

| Expansion of direct-to-consumer (D2C) digital native brands | +0.8% | Brazil (São Paulo, Rio de Janeiro), Argentina (Buenos Aires), Colombia (Bogotá) | Short term (≤ 2 years) |

| Adoption of refillable packaging to meet ESG mandates | +0.6% | Brazil (ANVISA compliance zones), Chile (Santiago, Valparaíso), Argentina (Buenos Aires) | Medium term (2-4 years) |

| On-device biosensor integration enabling smart deodorants | +0.3% | Brazil Tier-1 cities, early adopters in Colombia and Chile | Long term (≥ 4 years) |

| Effective promotional and marketing strategies | +0.9% | Regional, with digital-first campaigns in Brazil, Argentina, and Colombia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising disposable incomes and trading-up to premium formats

In 2024, Colombia's GDP grew by 1.8%, with a forecasted rise to 2.3% in 2025. Meanwhile, Peru boasted a 3.2% growth in 2024. This economic backdrop has birthed a class of aspirational consumers in both nations, perceiving deodorants not merely as commodities but as symbols of status. In Brazil, the luxury perfumery market witnessed a surge in the first half of 2024. Grupo Boticário's Priveé Légumes collection and Natura's premium line, launched in November 2024, featuring seven eau de parfum fragrances, successfully captured market share from imported brands. This trend of premiumization isn't limited to just fragrance intensity; it encompasses packaging aesthetics and the narrative behind ingredients. Brands are now emphasizing Amazonian botanicals and securing dermatologist endorsements, allowing them to command prices two to three times higher than mass-market offerings. This shift is especially evident among Gen Z and millennials, who are dedicating a larger portion of their discretionary spending to personal care compared to earlier generations. A significant majority of Brazilians not only use deodorants daily but also voice concerns about body odor. In response, retailers are allocating prime shelf space for premium products and setting up in-store fragrance sampling stations. Simultaneously, e-commerce platforms are spotlighting "clean beauty" and "luxury self-care" categories, using algorithms to highlight high-margin SKUs to discerning shoppers.

Health-oriented shift toward aluminum-free and natural formulations

South American shoppers increasingly favor natural ingredients in personal-care products, prompting heightened regulatory scrutiny and more frequent reformulations. Brazil's ANVISA has rolled out RDC 894/2024 to bolster post-market oversight of cosmetics, including antiperspirants. Meanwhile, Argentina's ANMAT is aligning with MERCOSUR standards, mandating clear labeling of aluminum salts like aluminum chlorohydrate, as highlighted by the Brazilian Health Regulatory Agency. Unilever is making waves with its June 2025 debut of the All Body Deo line, featuring brands like Rexona, Dove, and Dove Men+Care. These new offerings boast aluminum-free, alcohol-free formulas with a commendable 72-hour efficacy. Achieving this milestone necessitated a revamp of propellant systems and active-delivery matrices. In December 2024, Natura introduced its Tododia Limão Siciliano roll-on, enriched with prebiotic complexes to bolster skin microbiome health. This move is a strategic nod to dermatology-savvy consumers who often cross-check ingredient lists with online databases. Meanwhile, Natura &Co's Care Natural Beauty, a direct-to-consumer newcomer, derives a significant 80% of its sales from online channels. The brand emphasizes sustainability, using 95% glass or green plastic and offering refill options. Notably, refill purchases alone account for 9% of its revenue. However, the shift to aluminum-free formulations comes with challenges. Formulators grapple with achieving the right balance between efficacy, skin feel, and shelf stability. Moreover, early adopters have noted increased per-unit costs, which can strain margins until economies of scale are realized.

Expansion of direct-to-consumer (D2C) digital native brands

Brazil's e-commerce for care products is witnessing a robust growth trajectory. Direct-to-consumer (D2C) brands are capitalizing on this shift, leveraging customer data to tailor product recommendations and refining formulations through real-time feedback, an agility that traditional consumer packaged goods (CPG) giants struggle to match. Care Natural Beauty, with its 80% direct-sales model, strategically reinvests retail-margin earnings into influencer collaborations and subscription perks. Notably, its 9% share of refill sales underscores that messaging around convenience and sustainability can effectively drive repeat purchases, independent of a physical retail presence. Latin America's digital consumer base is expanding, with retail e-commerce transactions not only growing but also projected to maintain a double-digit growth rate until 2027. Drogaraia.com.br, the top online care retailer in Brazil, raked in USD 779.1 million in 2024. This underscores the rising role of pharmacy-channel aggregators as key discovery platforms for nascent brands. In response, established players are adopting omnichannel approaches. For instance, L'Oréal's pharmacy-channel sales in Brazil reached BRL 3.3 billion (approximately USD 660 million), marking a 5.1% growth. This highlights the transformation of pharmacies into go-to spots for impulse personal-care buys. Furthermore, the D2C surge is nudging established brands to streamline their SKU portfolios, as digital platforms tend to favor high-velocity products with favorable ratings over slower-moving extensions.

Adoption of refillable packaging to meet ESG mandates

In 2024, Natura &Co recovered 14,900 tonnes of post-consumer resin, achieving a 10.9% recycled plastic content across its portfolio. Additionally, 75% of its SKUs now feature sustainable elements, including refillable formats and biodegradable components. Grupo Boticário has established a network of 4,000 Boti Recicla collection points throughout Brazil. This reverse-logistics network not only channels recycled materials back into production but also underscores the company's commitment to environmental sustainability, appealing to ESG-focused institutional buyers. Care Natural Beauty's refill program highlights that consumers are willing to embrace minor inconveniences when brands position refills as both cost-effective and environmentally friendly. Regulatory oversight is intensifying: Brazil's ANVISA, under RDC 907/2024, has unified cosmetics regulations, emphasizing packaging recyclability and extended producer responsibility. Meanwhile, Chile and Argentina are crafting similar regulations in line with OECD's circular-economy principles. Retailers are responding by dedicating premium shelf space to sustainably certified brands. Furthermore, procurement teams at Carrefour and Grupo Éxito are now evaluating suppliers based on packaging circularity metrics. The financial viability of refill programs relies on achieving a scale that can counterbalance reverse-logistics expenses, a milestone reached predominantly by major players and niche D2C brands.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply-chain inflation is pressuring aerosol propellant costs | -0.7% | Regional, with acute pressure in Brazil and Argentina due to currency volatility | Short term (≤ 2 years) |

| Regulatory scrutiny over antiperspirant actives in Brazil and Argentina | -0.4% | Brazil (ANVISA jurisdiction), Argentina (ANMAT jurisdiction), and spillover to the MERCOSUR bloc | Medium term (2-4 years) |

| Fragmented last-mile logistics outside Tier-1 Brazilian cities | -0.5% | Brazil Tier-2 and Tier-3 cities, rural areas in Colombia, Peru, Chile | Long term (≥ 4 years) |

| Proliferation of counterfeit products | -0.6% | Brazil, Argentina, Peru; concentrated in informal retail channels | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Supply-chain inflation pressuring aerosol propellant costs

Aerosol deodorants use liquefied petroleum gas (LPG) or compressed hydrocarbons as propellants. These commodities are vulnerable to fluctuations in energy markets and geopolitical supply disruptions. While data on propellant costs for 2024-2025 is proprietary, broader reports from the FMCG supply chain highlight that inflation in packaging and raw materials has squeezed gross margins in personal care. This has led brands to either reduce pack sizes or reformulate using more affordable active ingredients. Due to Brazil's currency depreciation against the U.S. dollar, import costs for specialty chemicals have surged. This situation compels local manufacturers to either absorb the resulting margin compression or increase prices. However, retailers are hesitant to accept these hikes in a competitive landscape. Unilever's investment of BRL 410 million (USD 82 million) in March 2025, aimed at expanding its Aguaí factory and logistics network, underscores the importance of vertical integration and economies of scale as shields against input-cost fluctuations. In contrast, smaller players, lacking the financial muscle for such maneuvers, find themselves at a disadvantage. This has led to a market divide: established brands enhance their market share through operational efficiency, while niche brands carve out their identity through unique formulations or sustainability efforts, rather than competing on price. If the inflation in aerosol costs continues, there might be a quicker shift towards roll-ons and creams, formats that don't need pressurized propellants. Yet, it's worth noting that in hot and humid regions, where the quick-dry convenience of sprays is paramount, consumer preference for spray formats remains strong, even in the face of rising costs.

Regulatory scrutiny over antiperspirant actives in Brazil and Argentina

Brazil's ANVISA, through RDC 48/2013 and RDC 7/2015, classifies antiperspirants as cosmetics and sets concentration limits for aluminum salts like aluminum chlorohydrate. Meanwhile, RDC 894/2024 bolsters post-market surveillance to identify adverse events[1]Source: Agência Nacional de Vigilância Sanitária, “RDC 894/2024 Cosmetics Surveillance,” gov.br. Argentina's ANMAT, in line with MERCOSUR standards, mandates clear labeling and regular safety assessments. This comes as consumer advocacy groups voice concerns over aluminum absorption and its potential health implications. While outright bans remain absent, the regulatory landscape nudges companies towards aluminum-free formulations. However, this shift poses a technical challenge, necessitating a balance between efficacy, skin feel, and shelf stability. Unilever's June 2025 debut of All Body Deo, boasting aluminum-free formulations with a 72-hour protection claim, underscores the industry's pivot. They're not just adapting; they're investing in next-gen actives, aiming to stay ahead of regulatory curves and appeal to health-conscious consumers. In contrast, smaller brands grapple with elevated research and development costs per unit to match performance, creating a significant entry barrier and consolidating market dominance among financially robust players. A UNCTAD report highlights that 44% of countries lack thorough cosmetics regulations. This hints at a potential harmonization of standards by South American authorities in the coming 3 to 5 years, possibly leading to stricter testing and labeling mandates. Such changes would likely benefit established players with adept regulatory affairs teams.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Roll-Ons Gain Ground on Leak-Proof Innovation

From 2026 to 2031, roll-ons are projected to grow at a rate of 5.95% CAGR, surpassing the market average of 4.97%. This growth comes as brands rectify past packaging issues. Data from ANVISA, Brazil's Health Regulatory Agency, highlighted that 9% to 24% of consumer complaints in personal care were due to leaky bottles. In response, manufacturers revamped ball-and-socket designs and introduced tamper-evident seals. In December 2024, Natura launched its Tododia Limão Siciliano roll-on, boasting a prebiotic formula and 48-hour protection, appealing to consumers who value skin health over the convenience of sprays.

In 2025, sprays held a dominant 47.98% market share, driven by consumer preference for quick-drying applications in hot, humid conditions. However, rising costs of aerosol propellants and challenges in reformulating without aluminum could threaten their margin edge. Meanwhile, creams and other formats cater to niche audiences, like travelers needing TSA-compliant sizes and athletes seeking potent actives, but they lack the scale for broader category growth. Unilever's June 2025 launch of All Body Deo in both aerosol and cream formats indicates a strategic move, allowing incumbents to mitigate format risks and cater to varied consumer occasions. The rise of roll-ons is also tied to their compatibility with natural formulations; water-based gels and prebiotic complexes thrive in roll-on systems, unlike pressurized aerosols that depend on alcohol or synthetic solvents for stability.

By Category: Premium Segment Accelerates on Haute Parfumerie

From 2026 to 2031, premium deodorants are set to expand at a robust 7.01% CAGR, nearly doubling the growth pace of their mass-market counterparts. This shift underscores a growing consumer preference for formulations that seamlessly blend effectiveness with a touch of sensory luxury. In 2025, the mass segment commanded a dominant 67.92% market share, buoyed by value-driven shoppers and their frequent repurchase habits. However, this segment grapples with challenges: intense price competition and the infiltration of counterfeit products are squeezing margins and curtailing innovation budgets. Meanwhile, Brazil's luxury perfumery scene witnessed a notable uptick in early 2024. Notably, Grupo Boticário unveiled its 'Priveé Légumes' collection in September, and Natura rolled out a premium line featuring seven eau de parfum fragrances in November, both targeting the aspirational consumer base.

Premium brands are capitalizing on Amazonian botanicals, securing endorsements from dermatologists, and introducing refillable glass packaging. These strategies allow them to command price points that are two to three times higher than mass-market offerings. Retailers, recognizing this trend, are dedicating prime shelf space and setting up in-store fragrance sampling stations to encourage trials. The trend of premiumization is especially evident among Gen Z and millennial consumers. These younger cohorts are channeling a larger portion of their discretionary spending towards personal care, perceiving deodorants as status symbols rather than mere commodities. In response, mass brands are rolling out "masstige" sub-brands, mid-tier lines that adopt premium characteristics like minimalist packaging and natural ingredient claims. This strategy aims to protect market share without cannibalizing flagship products. However, there's a fine line: if not executed meticulously, it could lead to consumer confusion and potential dilution of brand equity.

By End User: Unisex Formats Collapse Gender Boundaries

From 2026 to 2031, unisex deodorants are set to experience a robust surge at a 7.45% CAGR, outpacing all other segments. This growth underscores brands' recognition that gender-neutral positioning not only broadens their market reach but also streamlines SKU management. In 2025, men accounted for a notable 45.61% market share, buoyed by Natura's launch of the Natura Homem men's line in July and Dove Men+Care's introduction of a whole-body deodorant in May. Meanwhile, women's deodorants, bolstered by fragrance-centric formulations and skin-care benefits like moisturizing and brightening actives, continue to hold the position of the second-largest segment.

Unilever's June 2025 launch of All Body Deo, spanning brands like Rexona, Dove, and Dove Men+Care, underscores the industry's pivot towards unisex offerings. These products, boasting alcohol-free and aluminum-free formulations with an impressive 72-hour protection, cater to consumers across the gender spectrum. This shift not only mirrors societal movements towards gender fluidity but also highlights a growing awareness: traditional masculine and feminine fragrance profiles often alienate non-binary and LGBTQ+ consumers, underscoring the need for inclusive branding. In response, retailers are reconfiguring their shelf displays to spotlight unisex products, while e-commerce platforms leverage algorithms to prominently feature gender-neutral options for all users. However, there's a strategic concern: as more competitors adopt similar unisex formulations and messaging, there's a risk of brand differentiation blurring, potentially leading the category into a price-driven, commoditized race.

By Distribution Channel: Online Retail Rewrites Shelf Economics

From 2026 to 2031, online retail stores are set to grow at a 7.58% CAGR. This growth is largely fueled by Brazil's e-commerce segment for care products, which is projected to jump from USD 2,749.4 million in 2025 to USD 4,030.2 million by 2029, marking a robust 10.0% CAGR. During this period, online penetration in the sector is expected to rise from 18.8% to 26.4%. In 2025, supermarkets and hypermarkets commanded a 38.12% market share, bolstered by high foot traffic and the dynamics of impulse buying. However, these brick-and-mortar retailers are grappling with margin pressures as landlords hike rents and labor costs soar. Drogaraia.com.br, the top online care retailer in Brazil, reported a revenue of USD 779.1 million in 2024, highlighting the growing role of pharmacy-channel aggregators as key platforms for brand discovery.

While convenience stores and specialty shops cater to specific needs, like travelers opting for single-use products or beauty aficionados seeking artisanal brands, they lack the scale necessary to propel category-wide growth. In March 2025, Unilever made a strategic move, investing BRL 410 million (approximately USD 82 million) to bolster its logistics. This expansion, increasing capacity to 280,000 pallet positions across 9 distribution centers, emphasizes the need to cater to both e-commerce fulfillment and the fragmented last-mile delivery networks, especially in areas beyond Tier-1 cities. L'Oréal reported BRL 3.3 billion (USD 660 million) in sales through the pharmacy channel in Brazil, marking a 5.1% growth. This uptick underscores pharmacies' evolving role as convenient stops for impulse personal-care purchases. The online boom is pushing established players to streamline their SKU portfolios. Digital platforms tend to favor high-velocity products with favorable ratings, sidelining slower-moving line extensions. This trend, amplified by algorithms, underscores a winner-takes-most scenario, concentrating sales among top-tier listings.

Geography Analysis

In 2025, Brazil held a dominant 61.10% market share, driven by its population of over 215 million, high deodorant usage rates, and a robust retail network comprising supermarkets, pharmacies, and e-commerce platforms. Unilever's March 2025 investment of BRL 410 million (USD 82 million) to establish a fourth deodorant production line at its Aguaí factory and expand logistics capacity to 280,000 pallet positions across nine distribution centers highlights Brazil's role as a regional profit center, despite challenges like currency volatility and counterfeit products. Natura and Grupo Boticário leverage extensive direct-sales networks, Natura with over 1.5 million consultants and Boticário with more than 4,000 Boti Recicla collection points, to bypass traditional retail channels and gather consumer insights for product innovation. Brazil's stringent cosmetics regulations, enforced by ANVISA under RDC 48/2013, RDC 7/2015, RDC 894/2024, and RDC 907/2024, create a compliance barrier that benefits well-capitalized companies with strong regulatory teams. Additionally, the luxury perfumery segment grew by 15% in the first half of 2024, reflecting the premiumization trend extending beyond deodorants to other fragrance categories.

Colombia is projected to be the fastest-growing market, with a CAGR of 5.27% from 2026 to 2031. This growth is supported by GDP increases of 1.8% in 2024 and a forecasted 2.3% in 2025, alongside middle-class expansion and urbanization that concentrates purchasing power in Bogotá, Medellín, and Cali. INVIMA, Colombia's health-regulatory authority, ensures cosmetics compliance in alignment with Andean Community standards, enabling products approved in Colombia to circulate across Ecuador, Peru, and Bolivia with minimal additional testing. E-commerce adoption is accelerating, with digital-buyer penetration exceeding 50% in urban areas. However, fragmented last-mile logistics outside major cities limit direct-to-consumer brands' ability to achieve nationwide distribution.

Argentina, Peru, and Chile collectively account for the remainder of the regional market. Argentina faces economic challenges, including inflation and currency depreciation, which constrain discretionary spending. In contrast, Peru's GDP is expected to grow by 3.2% in 2024, and Chile's by 2.5%, signaling recovering consumer confidence, according to the International Monetary Fund. Argentina's ANMAT, adhering to MERCOSUR standards, mandates transparent labeling of aluminum salts and periodic safety reviews, encouraging reformulation toward aluminum-free alternatives. Peru and Chile benefit from improved retail infrastructure and rising smartphone penetration, yet counterfeit products remain a significant issue in informal channels where enforcement is inconsistent.

Competitive Landscape

In South America, the deodorants market is moderately concentrated, with key players such as Unilever, Natura & Co, Procter & Gamble, and Grupo Boticário maintaining dominance through multi-brand portfolios, extensive distribution networks, and sustained marketing investments. These companies employ three main strategies: vertical integration, as seen in Unilever's BRL 410 million investment in factory and logistics expansion to mitigate input-cost volatility; omnichannel approaches, exemplified by Natura's combination of 1.5 million consultants and digital platforms to address both physical and online demand; and premiumization, highlighted by Grupo Boticário's Priveé Légumes luxury collection to counteract margin pressures in mass-market segments. Growth opportunities are emerging in aluminum-free whole-body formats, refillable packaging systems achieving 15% to 20% refill-sales share, and biosensor-enabled smart deodorants, which are transforming the category into a platform business model. Direct-to-consumer (D2C) brands like Care Natural Beauty, which channels 80% of its sales through online platforms and achieves a 9% refill-sales share, demonstrate that niche players can profitably cater to sustainability-conscious consumers without competing for traditional shelf space.

New entrants are leveraging regulatory gaps and digital-first strategies to bypass the advantages of established players. Counterfeiting remains a significant challenge, as evidenced by INTERPOL's Operation Crete II, which seized over 11 million illicit personal-care products valued at USD 225 million[3]Source: Interpol, “Operation Crete II Fact Sheet 2025,” interpol.int . Counterfeiters primarily target high-margin SKUs and exploit informal retail channels where enforcement is weak. Meanwhile, technological advancements are reshaping the competitive landscape. For instance, Unilever's June 2025 launch of All Body Deo, offering aluminum-free, 72-hour protection, required complex reformulations in propellant systems and active-delivery matrices. Such innovations demand significant research and development budgets, creating barriers for smaller brands. Additionally, Natura's 75% SKU penetration of sustainable elements and Grupo Boticário's establishment of 4,000 Boti Recicla collection points underscore the growing importance of ESG credentials for institutional buyers and ESG-focused retail chains.

Regulatory developments are also influencing market dynamics. Brazil's ANVISA, through its RDC 907/2024 regulations, has consolidated compliance frameworks for cosmetics, creating entry barriers that favor established players with experienced regulatory teams. Smaller players, however, face challenges due to the capital-intensive nature of navigating these approval processes. This regulatory shift benefits incumbents, enabling them to strengthen their market positions while smaller competitors struggle to meet compliance requirements. As a result, the deodorants market in South America is increasingly shaped by a combination of strategic investments, technological advancements, and evolving regulatory landscapes.

South America Deodorants Industry Leaders

Unilever PLC

Beiersdorf AG

L’Oréal SA

Natura & Co Holding SA

Procter & Gamble Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Unilever launched the All Body Deo category in Brazil, spanning Rexona, Dove, and Dove Men+Care brands, featuring alcohol-free and aluminum-free formulations with 72-hour protection in aerosol and cream formats. This launch represented a strategic pivot toward whole-body application and addresses growing consumer demand for aluminum-free alternatives, positioning Unilever to capture health-conscious segments while defending share against D2C insurgents.

- March 2025: Unilever invested BRL 410 million (USD 82 million) in Brazil, allocating BRL 265 million (USD 53 million) to expand its Aguaí factory with a fourth deodorant production line that increases capacity by over 30%, and BRL 145 million (USD 29 million) to enhance logistics infrastructure, reaching 280,000 pallet positions across 9 distribution centers by year-end. This investment underscores Unilever's commitment to vertical integration and last-mile efficiency in the region's second-largest deodorant market globally.

- December 2024: Natura launched the Tododia Limão Siciliano limited edition, featuring a roll-on deodorant with 48-hour protection and a prebiotic formula designed to support skin microbiome health. The launch reflects Natura's strategy to blend efficacy with dermatology-backed ingredient storytelling, targeting consumers who prioritize skin-health benefits over spray convenience.

South America Deodorants Market Report Scope

The South America deodorants market is available as spray, roll on, sticks and others. By distribution channels, the market is segmented into supermarkets/ hypermarkets, specialty stores, convenience stores, online retail stores, and others.

Product Type

| Sprays |

| Creams |

| Roll-ons |

| Others |

Category

| Mass |

| Premium |

End User

| Men |

| Women |

| Unisex |

By Distribution Channel

| Supermarkets and hypermarkets |

| Convenience stores |

| Specialty stores |

| Online Retail Stores |

| Other Distribution Channels |

Geography

| Brazil |

| Argentina |

| Colombia |

| Peru |

| Chile |

| Rest of South America |

| Product Type | Sprays |

| Creams | |

| Roll-ons | |

| Others | |

| Category | Mass |

| Premium | |

| End User | Men |

| Women | |

| Unisex | |

| By Distribution Channel | Supermarkets and hypermarkets |

| Convenience stores | |

| Specialty stores | |

| Online Retail Stores | |

| Other Distribution Channels | |

| Geography | Brazil |

| Argentina | |

| Colombia | |

| Peru | |

| Chile | |

| Rest of South America |

Key Questions Answered in the Report

How large will deodorant sales be in South America by 2031?

The South America deodorant market size is forecast to reach USD 5.11 billion by 2031, up from USD 4.01 billion in 2026.

Which product formats are growing fastest?

Roll-on deodorants lead with a projected 5.95% CAGR through 2031, outstripping sprays and creams.

What drives premium deodorant demand?

Rising disposable incomes, luxury fragrance launches, and refillable glass packaging are lifting premium segment growth at a 7.01% CAGR.

Why are unisex deodorants gaining momentum?

Inclusive branding and neutral scents appeal to a broader consumer base, pushing unisex formats toward a 7.45% CAGR.

Which countries offer the best expansion prospects beyond Brazil?

Colombia shows the fastest geographic growth at 5.27% CAGR, followed by Peru and Chile as GDP recovery boosts personal-care spending.

How are brands tackling counterfeit risks?

Companies deploy QR-code authentication, holograms, and blockchain provenance while collaborating with agencies on enforcement actions such as INTERPOL’s Operation Crete II.

Page last updated on: