Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 7.08 Billion |

| Market Size (2026) | USD 7.37 Billion |

| Market Size (2031) | USD 9.02 Billion |

| Growth Rate (2026 - 2031) | 4.13% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Deodorants Market Analysis by Mordor Intelligence

The Europe deodorants market size was valued at USD 7.08 billion in 2025 and estimated to grow from USD 7.37 billion in 2026 to reach USD 9.02 billion by 2031, at a CAGR of 4.13% during the forecast period (2026-2031). The growth is driven by increasing awareness of personal hygiene and grooming, the incorporation of fitness and sports into daily routines, and the integration of deodorants into self-care practices. These factors contribute to higher adoption rates among late-adopting demographics and increased usage frequency among existing consumers. Structural trends are also reshaping the market, including a shift toward natural and organic formulations, rising demand for aluminum-free and sensitive-skin products, and the growing emphasis on sustainability. Features such as eco-friendly packaging, refillable formats, and cleaner ingredient profiles are gaining traction, fostering opportunities for premiumization and innovation beyond traditional mass-market sprays and roll-ons.

Key Report Takeaways

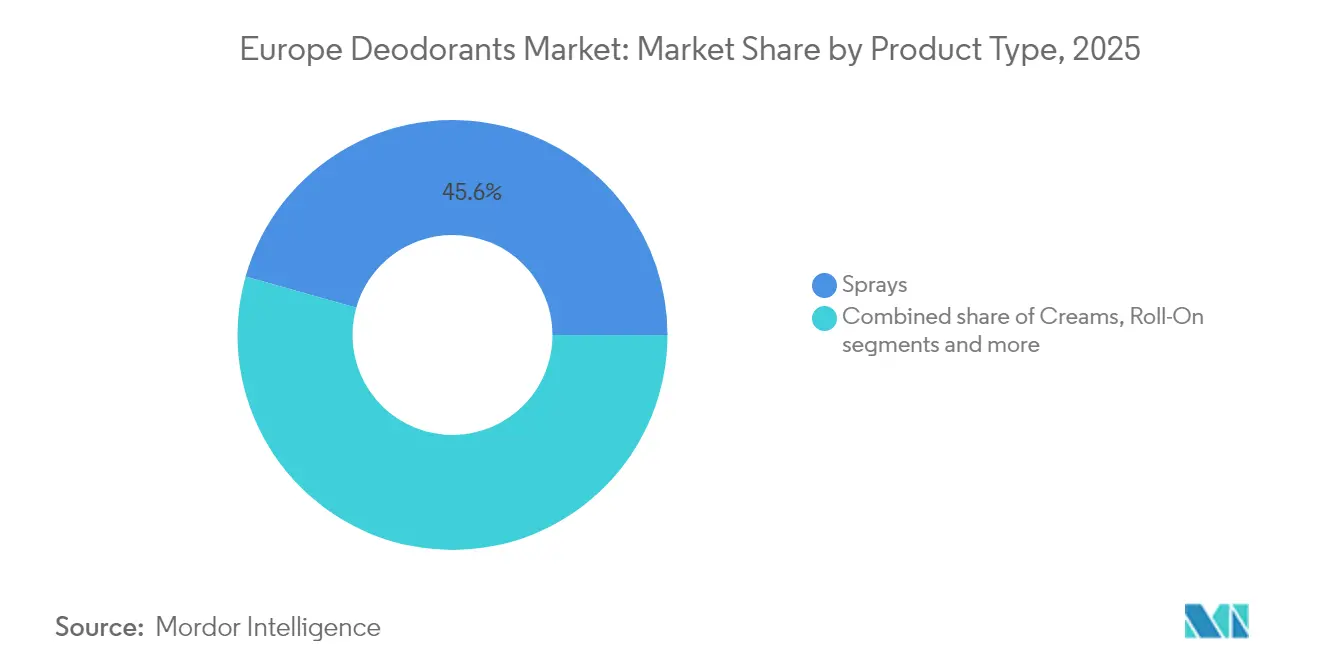

- By product type, sprays led with 45.62% volume share in 2025, while roll-ons are advancing at a 4.53% CAGR to 2031.

- By category, conventional lines captured 86.05% of the Europe deodorants market share in 2025; organic and natural variants are growing at a 5.29% CAGR through 2031.

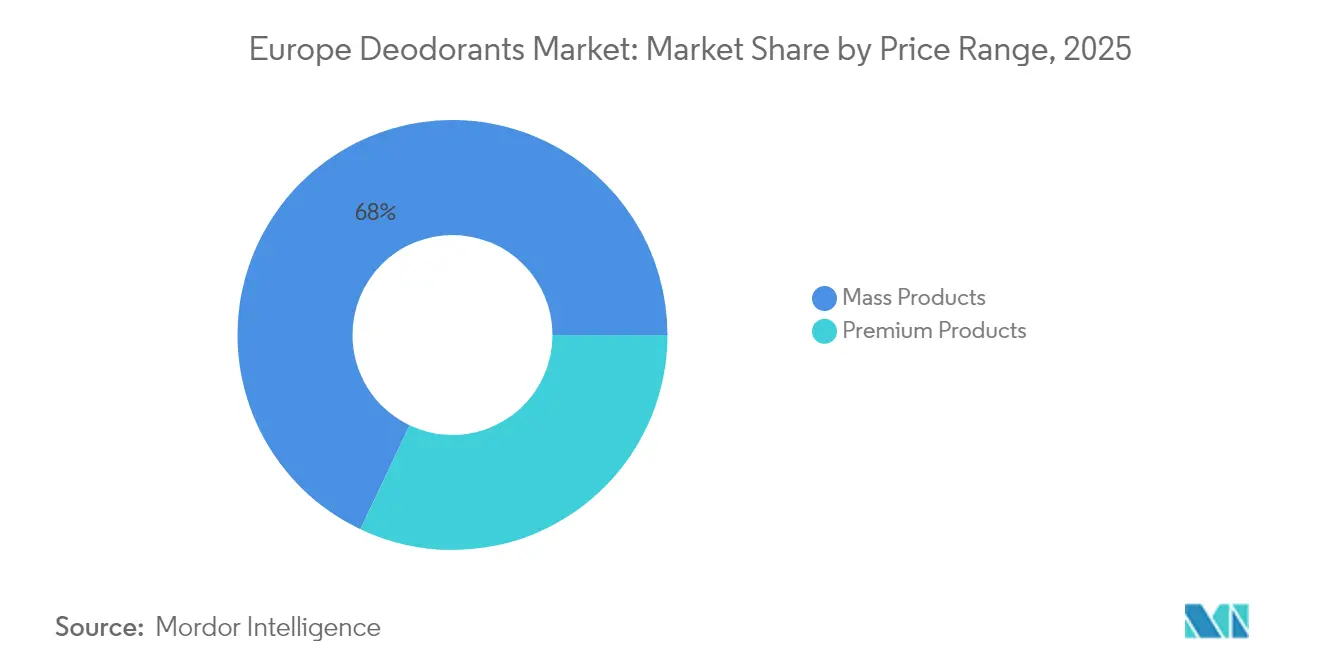

- By price range, mass products held 67.95% share of the Europe deodorants market size in 2025, whereas premium offerings are rising at a 5.5% CAGR.

- By distribution channel, supermarkets and hypermarkets accounted for 40.55% value in 2025, yet online retail is expanding at a 6.28% CAGR to 2031.

- By geography, Germany commanded 21.32% of the Europe deodorants market in 2025; Poland records the highest projected CAGR at 5.2% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Deodorants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing personal hygiene and grooming awareness | +0.7% | Germany, the United Kingdom, the Netherlands, Poland, and accelerating in Spain, Italy post-pandemic | Medium term (2-4 years) |

| Influence of fitness and sports culture | +0.5% | United Kingdom, Germany, Netherlands, Poland; urban centers and younger cohorts | Medium term (2-4 years) |

| Sustainability and eco-packaging | +1.2% | Regional, with highest adoption in Germany, Netherlands, France, Sweden | Medium term (2-4 years) |

| Social media and influencer marketing | +0.6% | The United Kingdom, Germany, Spain, France; younger demographics across all markets | Short term (≤ 2 years) |

| Premiumization and specialization | +0.9% | Germany, the United Kingdom, France, Italy; spillover to Poland, Spain | Long term (≥ 4 years) |

| Product and format innovation | +0.8% | Regional, led by Western Europe (Germany, the United Kingdom, France); Poland rapid adoption | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing personal hygiene and grooming awareness

Rising awareness of personal hygiene and grooming is a key factor driving the Europe deodorants market. Consumers in the region are increasingly prioritizing cleanliness, freshness, and daily self-care routines. This trend is influenced by changing lifestyle standards, greater health consciousness, and a cultural focus on maintaining a well-groomed appearance in both social and professional environments. Younger demographics are adopting deodorants at an earlier age, incorporating them into multi-step grooming routines shaped by social media, wellness trends, and peer influences. Additionally, increased awareness of body odor management, sweat control, and overall hygiene, supported by public health campaigns, workplace expectations, and the growing popularity of fitness and outdoor activities, continues to enhance the market's significance. The demand for innovative deodorant formulations, such as natural, eco-friendly, and long-lasting products, is also rising as consumers seek options that align with their values and preferences, further driving market growth.

Influence of fitness and sports culture

The increasing emphasis on fitness and sports culture is a significant driver for the Europe deodorants market. As consumers adopt more active lifestyles, there is a growing demand for deodorants that offer enhanced odor and sweat protection. The rise in participation in gyms, sports clubs, outdoor activities, and structured fitness programs has made deodorants a vital part of daily routines, providing freshness and confidence before, during, and after physical activity. This trend is particularly noticeable in regions with expanding fitness engagement. For instance, according to Sport England, in 2024, approximately 6.7 million people participated in fitness classes in England, highlighting the substantial and growing need for effective deodorant solutions tailored to high-intensity and frequent workouts [1]Source: Sport England, "Number of people participating in fitness classes in England", sportengland.org. Consumers increasingly prefer deodorants that deliver endurance, long-lasting protection, anti-sweat performance, and quick-drying application.

Sustainability and eco‑packaging

Sustainability and eco-packaging are significant drivers in the Europe deodorants market, as consumers increasingly prioritize environmentally responsible products and brands committed to reducing waste and minimizing ecological impact. With growing awareness of plastic pollution, carbon footprints, and ethical sourcing, European consumers are shifting toward deodorants that feature recyclable, refillable, biodegradable, or reduced-plastic packaging. In response, manufacturers are innovating by developing products such as solid sticks in paper tubes, aluminum-free refills, and packaging made from post-consumer recycled materials to meet the demand for eco-conscious grooming options. For instance, in June 2023, cosmetics brand Respectueuse introduced a deodorant line utilizing Sonoco’s fully recyclable EnviroStick packaging. These products are vegan, 100% natural, and certified organic, aligning with consumer expectations for sustainability and ingredient purity. Such initiatives demonstrate how brands are incorporating environmental responsibility into both product formulation and packaging, fostering consumer trust and driving market growth.

Social media and influencer marketing

Social media and influencer marketing are significant drivers of the Europe deodorants market, shaping consumer preferences, increasing awareness, and enhancing brand engagement across various demographics. Platforms like Instagram, TikTok, and YouTube enable brands to highlight product innovations, emphasize natural or premium formulations, and deliver lifestyle-oriented messages that appeal to younger, digitally active consumers. Influencers and content creators play a vital role in educating audiences about product benefits, demonstrating application techniques, and fostering trust, which directly influences purchase decisions and brand loyalty. The impact of these channels is further strengthened by high social media penetration. For example, according to the World Population Review, 73.61% of people in Russia are expected to be active on social media in 2025, showcasing the extensive reach and influence potential of digital marketing campaigns [2]Source: World Population Review, "Social Media Users by Country 2025", worldpopulationreview.com. By utilizing visually engaging content, tutorials, reviews, and collaborations with fitness, wellness, and lifestyle influencers, deodorant brands can enhance visibility, encourage trials of new formats such as natural or eco-friendly products, and establish emotional connections with consumers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Europe cosmetic regulations | -0.5% | Europe-wide, with strictest enforcement in Germany, France, Netherlands | Long term (≥ 4 years) |

| Allergic reactions and skin sensitivity | -0.4% | Regional, with higher clinical reporting in Germany, the United Kingdom, France, Netherlands | Medium term (2-4 years) |

| Market saturation and intense competition | -0.7% | Germany, the United Kingdom, France, Italy, Spain (mature markets); less impact in Poland, Belgium | Medium term (2-4 years) |

| Proliferation of counterfeit and grey-market products | -0.3% | Spain, Italy, Poland, Belgium; e-commerce platforms across all markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent Europe cosmetic regulations

Stringent cosmetic regulations in Europe significantly restrain the deodorants market, as manufacturers must address complex compliance requirements that can delay product launches, increase costs, and restrict formulation flexibility. The regulatory framework in Europe is highly rigorous, with frequent updates to ingredient safety standards, labeling requirements, and usage restrictions aimed at protecting consumer health. For example, the EU Cosmetics Regulation amendments in 2024 (Regulation 2024/858) introduced stricter controls on the use of nanomaterials, mandating extensive safety testing, documentation, and approval processes before products containing such ingredients can be marketed. These additional compliance demands pose challenges for deodorant brands, particularly those focusing on advanced formulations, natural nano-encapsulated actives, or high-performance odor-control technologies. Smaller and emerging brands are disproportionately impacted, as the associated costs and technical complexities can create significant barriers to market entry.

Allergic reactions and skin sensitivity

Allergic reactions and skin sensitivity represent a significant restraint on the Europe deodorants market. Concerns about irritation, rashes, and allergic responses can hinder consumer adoption and affect brand loyalty. Deodorants often include active ingredients such as aluminum salts, alcohol, synthetic fragrances, preservatives, and essential oils, any of which can cause skin sensitivity in some individuals. These reactions can lead to discomfort, redness, or even more severe dermatological issues, further discouraging usage. Consumers with sensitive skin or dermatological conditions may avoid conventional deodorants entirely or frequently switch products in search of options that do not irritate. This behavior impacts trial and repeat purchases, particularly for mass-market products and high-fragrance formulations, where the perceived risk of adverse reactions is higher. Additionally, the growing awareness of ingredient safety and demand for hypoallergenic products adds pressure on manufacturers to reformulate or innovate, which can increase production costs and affect market dynamics.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Roll-On Precision Drives Format Shift

Spray deodorants accounted for approximately 45.62% of the Europe deodorants market in 2025, maintaining their dominance due to their combination of performance, sensory appeal, and continuous innovation. Sprays offer fast, even coverage and quick drying, catering to busy, urban, and fitness-oriented lifestyles where consumers prioritize immediate freshness without residue on clothing or sticky underarms. This format is strongly associated with effective odor protection and a cooling sensation, making it particularly popular among men and younger consumers. These groups perceive sprays as more effective and less intimate compared to roll-ons or creams, contributing to high usage frequency and strong brand loyalty.

Roll-on deodorants in Europe are expanding at a compound annual growth rate (CAGR) of approximately 4.53% through 2031, serving as a complementary growth driver to sprays. This format addresses emerging consumer needs for control, skin comfort, and a cleaner product positioning. Roll-ons provide precise, close-to-skin application with minimal product wastage, appealing to users seeking targeted protection and those concerned about inhaling aerosols. Additionally, roll-ons are widely perceived as gentler and more moisturizing due to their liquid or gel bases, which often include emollients, soothing agents, and sensitive-skin claims. These attributes make roll-ons particularly appealing to consumers with sensitive or recently shaved skin, as well as in markets where dermatological endorsements and clinical efficacy are key purchasing factors.

By Category: Organic Acceleration Amid Conventional Dominance

Conventional deodorants, which held an 86.05% market share in 2025, continue to dominate the European market due to their established consumer trust, proven efficacy, and widespread availability across major brands. This category benefits from decades of formulation advancements, providing consumers with reliable odor and sweat protection that is often perceived as more effective than emerging natural or alternative options. Conventional deodorants are available in various formats, including sprays, roll-ons, sticks, and creams, offering diverse fragrances and advanced features such as anti-stain properties, long-lasting protection, and dermatologically tested solutions. Over time, these products have seen significant improvements in performance, including time-release odor control, enhanced sweat absorption, alcohol-free formulations, and skin-conditioning ingredients, which enhance their appeal to users seeking both effectiveness and comfort.

Organic and natural deodorant variants in Europe, projected to grow at a CAGR of 5.29% through 2031, are reshaping the market as health- and eco-conscious consumers seek alternatives to aluminum salts, synthetic fragrances, and harsh preservatives found in conventional products. These deodorants typically feature plant-based odor-control ingredients, essential oils or allergen-reduced fragrance systems, and skin-friendly bases, appealing to users with sensitive skin or concerns about long-term chemical exposure. This allows brands to position these products at a premium price while expanding their market penetration. For instance, in March 2024, Eticos launched a refillable deodorant formulated with 100% natural, organic, and safe ingredients designed for effective odor control. The product is positioned as a sustainable option that reduces single-use plastic in daily routines, demonstrating how natural claims are increasingly combined with circular-economy packaging in this rapidly growing segment.

By Price Range: Premium Surge Reshapes Margin Mix

Mass-range deodorants, which accounted for a 67.95% market share in 2025, continue to lead the European market due to their strong value proposition, widespread consumer acceptance, and extensive product variety tailored to everyday personal care needs. These products benefit from established brand familiarity and trust, providing reliable odor and sweat protection at affordable price points without compromising performance. Over time, mass deodorants have incorporated advanced features such as long-lasting freshness, anti-stain technology, sensitive-skin formulations, and a wide range of fragrance options. These enhancements not only enable them to compete effectively with premium and niche alternatives but also reinforce their appeal by addressing diverse consumer preferences and maintaining affordability for the majority of users.

Premium deodorants, projected to grow at a 5.5% CAGR through 2031, are gaining momentum in the European market as consumers increasingly seek enhanced personal-care experiences, superior formulations, and products aligned with their lifestyle and wellness preferences. This segment benefits from a growing demand for high-quality, performance-focused ingredients, including botanical actives, advanced odor-neutralizing complexes, long-wear technologies, and dermatologist-approved formulations. These features appeal to users prioritizing efficacy, skin health, and sophisticated sensory experiences. Premium deodorants also differentiate themselves through refined fragrance profiles inspired by fine perfumery, minimalist or luxury packaging, and inclusive, gender-neutral designs that resonate with contemporary consumer preferences.

By Distribution Channel: E-Commerce Disrupts Shelf Dynamics

Supermarkets and hypermarkets accounted for approximately 40.55% of deodorant distribution in Europe in 2025. These outlets remain the primary distribution channel due to their ability to offer a wide assortment of brands, formats, and price points in one location. They cater to high-traffic shopping trips where personal care items are often purchased alongside groceries and household goods. Large retail chains typically dedicate significant shelf space to deodorants, facilitating strong brand visibility, frequent in-store promotions, and secondary placements near checkout areas or personal care aisles. This approach enhances brand awareness and supports high-volume sales for leading mass-market and mid-priced brands.

Online retail stores, growing at a compound annual growth rate (CAGR) of approximately 6.28% through 2031, are emerging as the fastest-growing distribution channel for deodorants in Europe. This growth is supported by the region's high internet penetration, with about 93% of individuals using the internet in 2024, according to the International Telecommunication Union (ITU) . E-commerce platforms and brand websites provide consumers with access to a broader range of deodorant formats, niche natural and premium products, and specialized fragrances compared to physical stores. Additionally, these platforms enable bulk purchases, dynamic pricing, and subscription-based delivery services, aligning with the convenience-driven lifestyles of digitally active shoppers.

Geography Analysis

Germany accounted for a 21.32% share of the Europe deodorants market in 2025, driven by its large population, high per-capita deodorant usage, and the strong presence of both multinational and domestic personal care manufacturers. The country benefits from a well-established hygiene culture, a diverse range of conventional and increasingly natural deodorant products, and a robust innovation ecosystem. Major brands in Germany often pilot advanced formulations, such as microbiome-friendly and sensitive-skin lines, which later expand across the region. Germany's significant market share also reflects the strength of its leading companies, which ensure efficient local production, frequent product updates, and strong consumer trust in domestic and European brands.

Poland is the fastest-growing deodorants market in Europe, with a projected CAGR of 5.2% through 2031. This growth is fueled by rising urbanization, increasing adoption of personal care products, and the rapid emergence of modern beauty and grooming habits, which are driving deodorant penetration beyond basic usage. The market's expansion is further supported by a relatively young population, growing middle-class aspirations, and the swift adoption of both mainstream and natural deodorant formats. These factors enable Poland to scale both volume and value from a lower base compared to Western Europe. Meanwhile, the United Kingdom, despite being a more mature market, continues to grow steadily. This growth is attributed to consumers trading up to premium, sustainable, and aluminum-free options, as well as experimenting with new formats and fragrances, which sustain positive value growth even in a high-demand market.

The Netherlands, Belgium, and Sweden, though smaller in absolute market size, are notable for their high penetration of private-label deodorants. This trend reflects sophisticated retail structures and consumer willingness to switch from global brands to retailer brands that offer comparable quality at lower prices. The rest of Europe, including markets such as Austria, Switzerland, Portugal, and the broader Nordic region, exhibits diverse market dynamics. Affluent markets tend to favor natural, organic, and eco-designed deodorants, while Southern and some Central/Eastern European markets remain more focused on value-oriented conventional products. However, these regions are rapidly catching up in the adoption of premium and clean-label deodorant options.

Competitive Landscape

The Europe deodorants market exhibits a moderately concentrated competitive environment, dominated by a few global leaders driving category development. Companies such as Unilever, Beiersdorf, Procter & Gamble, L’Oréal, and Henkel collectively hold a significant share of deodorant sales across major European markets. These players leverage extensive brand portfolios that cater to mass, masstige, and premium price segments. Their scale advantages in areas like fragrance development, dermatological testing, and cross-category marketing enable them to maintain shelf space and consumer mindshare against regional brands and independent natural product manufacturers. They also lead in core formats such as sprays and roll-ons.

Market leaders are actively evolving their strategies by incorporating AI-enabled research and development to accelerate formulation cycles, refine fragrance compositions, and predict consumer preferences. Companies are further strengthening their market presence through omnichannel ecosystems that combine traditional retail partnerships with direct-to-consumer platforms, subscription models, and data-driven loyalty programs. A notable example of long-term capacity building and localization efforts occurred in October 2025, when Unilever announced an investment of approximately USD 76 million in a new deodorant manufacturing facility in Hungary. This expansion enhances its European production capabilities, enabling more efficient supply to both Western and Central/Eastern European markets.

White-space opportunities in the market are increasingly focused on functional and territory extensions beyond traditional underarm antiperspirants. Both leading and challenger brands are investing in innovative formulations, such as microbiome-modulating products that aim to support skin flora rather than merely masking odor. Other developments include aluminum-free antiperspirants that offer comparable sweat and odor control without traditional salts, as well as whole-body deodorants targeting areas like feet, intimate regions, and overall body freshness, aligning with broader self-care trends.

Europe Deodorants Industry Leaders

-

Unilever PLC

-

Beiersdorf AG

-

Procter & Gamble Company

-

L’Oréal SA

-

Coty Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Wild introduced a refillable roll-on deodorant with a reusable metal case and a bio-based, compostable refill pack, addressing issues such as messy pour-in refills and inconvenient mechanisms that hinder adoption.

- August 2025: European Wax Center, Inc. unveiled the latest addition to its award-winning EWC TREAT line: the EWC TREAT All Over Deodorant. This gentle yet effective formula is aluminum-free, pH-balanced, and has been tested by dermatologists and gynecologists, ensuring its safety for even the most sensitive areas.

- 2025: Rock Face launched its first refillable deodorant specifically formulated for men in the United Kingdom. The product is designed to provide 48-hour odor protection.

- January 2025: Rexona launched a new campaign to promote its Whole Body Deodorant range. The range is available in three formats: Aerosol Spray, Glide Stick, and Body Cream Lotion.

Europe Deodorants Market Report Scope

Deodorant is applied to the body to prevent or cover odor caused by bacterial breakdown of perspiration in the armpits and genitals.

The European deodorant market is segmented by product type, end-user, distribution channel, and geography. By type, the market is segmented into sprays, roll-on, stick, and other product types. By end-user, the market is segmented into men & women. By distribution channel, the market is segmented into hypermarkets/supermarkets, convenience/grocery stores, online retail stores, and other distribution channels. By geography, the market is segmented into the United Kingdom, Germany, France, Italy, Spain, and the Rest of Europe.

The market sizing has been done in value terms in USD for all the abovementioned segments.

By Product Type

| Sprays |

| Creams |

| Roll-On |

| Other Product Types |

By Category

| Conventional |

| Organic/Natural |

By Price Range

| Mass Products |

| Premium Products |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Specialty Stores |

| Online Retail Stores |

| Other Distribution Channels |

By Geography

| Germany |

| United Kingdom |

| Italy |

| France |

| Spain |

| Netherlands |

| Poland |

| Belgium |

| Sweden |

| Rest of Europe |

| By Product Type | Sprays |

| Creams | |

| Roll-On | |

| Other Product Types | |

| By Category | Conventional |

| Organic/Natural | |

| By Price Range | Mass Products |

| Premium Products | |

| By Distribution Channel | Supermarkets/Hypermarkets |

| Specialty Stores | |

| Online Retail Stores | |

| Other Distribution Channels | |

| By Geography | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe |

Key Questions Answered in the Report

How large is the Europe deodorant market in 2026?

The Europe deodorant market size is USD 7.37 billion in 2026, with a forecast CAGR of 4.13% to 2031.

Which product format is growing fastest across Europe?

Roll-on deodorants lead growth at a 4.53% CAGR thanks to precision applicators that support refill and waste-reduction goals.

Which European country is the fastest growing market for deodorants?

Poland posts the highest projected CAGR at 5.2% through 2031, fueled by rising incomes and strong subscription interest.

How are online channels reshaping deodorant sales?

Direct-to-consumer models and e-commerce subscriptions grow at 6.28% CAGR, cutting acquisition costs and driving repeat purchases.

Page last updated on: