Opioid Use Disorder Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.78 Billion |

| Market Size (2031) | USD 8.04 Billion |

| Growth Rate (2026 - 2031) | 10.97% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

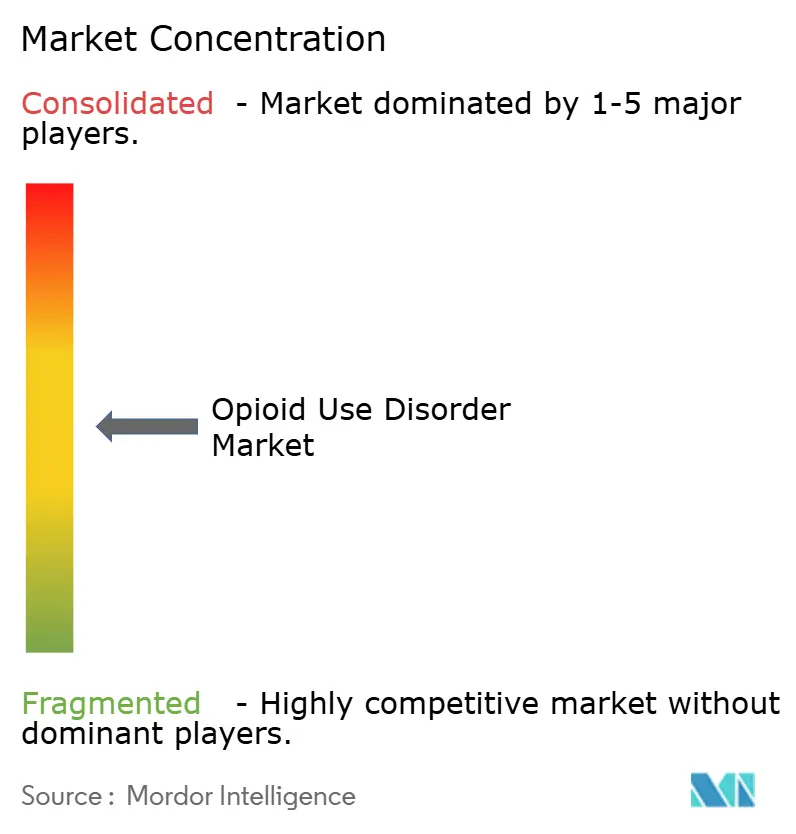

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Opioid Use Disorder Market Analysis by Mordor Intelligence

The Opioid Use Disorder Market size is expected to increase from USD 4.30 billion in 2025 to USD 4.78 billion in 2026 and reach USD 8.04 billion by 2031, growing at a CAGR of 10.97% over 2026-2031.

The treatment landscape is shifting from daily sublingual therapies and clinic-only dispensing to long-acting injectable products and telehealth-supported care models. This transition is driving improved treatment retention, higher revenue per patient, and broader access for individuals previously outside formal care pathways. Opioid-related deaths in the U.S. declined from over 110,000 in 2024 to nearly 75,000 in 2025, yet treatment access for the estimated 4.6 million Americans with opioid use disorder remained limited, maintaining demand pressures.[1]American Medical Association, “Time for Decisive Action on Substance-Use Disorder Treatment,” AMA, ama-assn.org

Key Report Takeaways

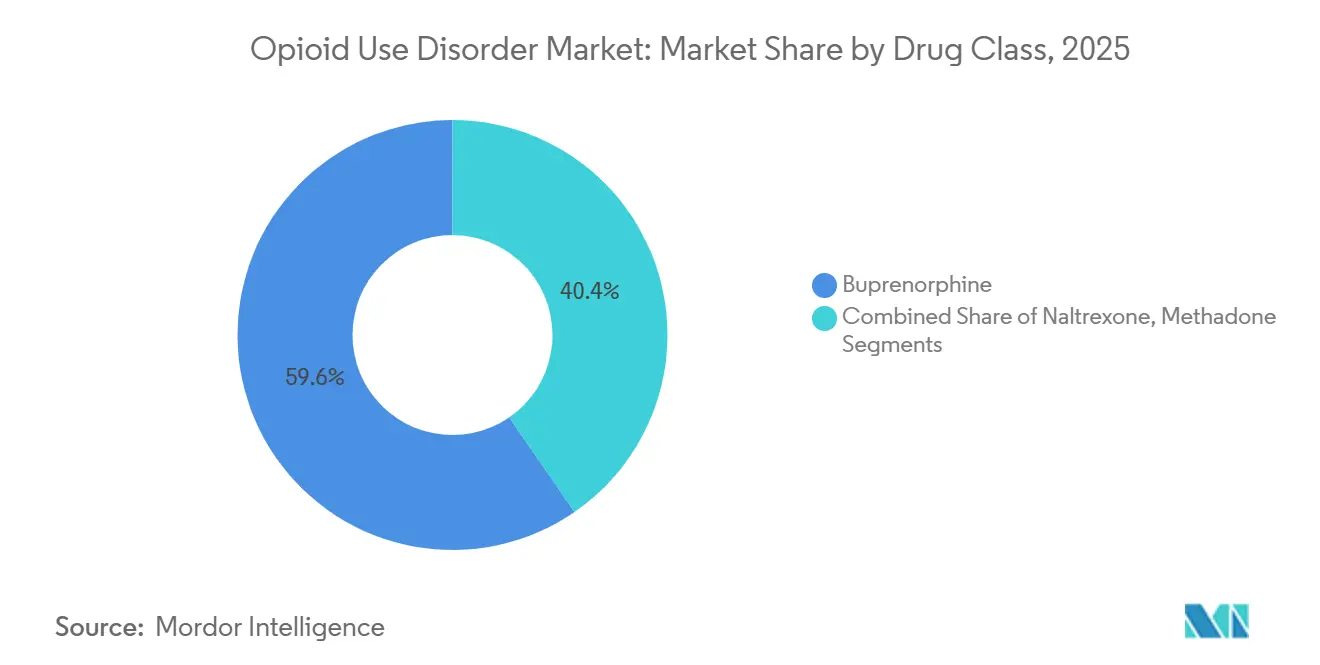

- By drug class, buprenorphine held 59.58% of the opioid use disorder market share in 2025, while naltrexone is projected to grow at the fastest CAGR of 11.45% through 2031.

- By route of administration, injectable formulations accounted for 59.78% of the opioid use disorder market size in 2025, while the oral segment is expected to expand at the fastest CAGR of 12.55% through 2031.

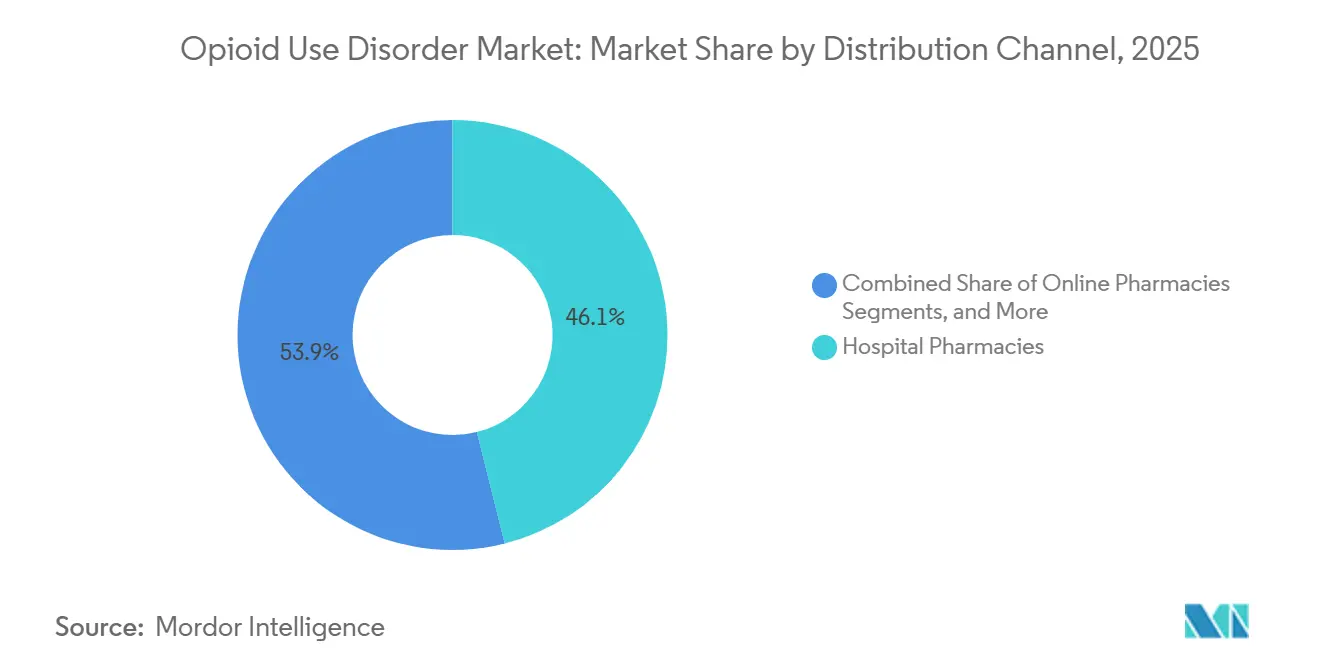

- By distribution channel, hospital pharmacies held a 46.12% share in 2025, while online pharmacies are projected to grow at the fastest CAGR of 11.24% through 2031.

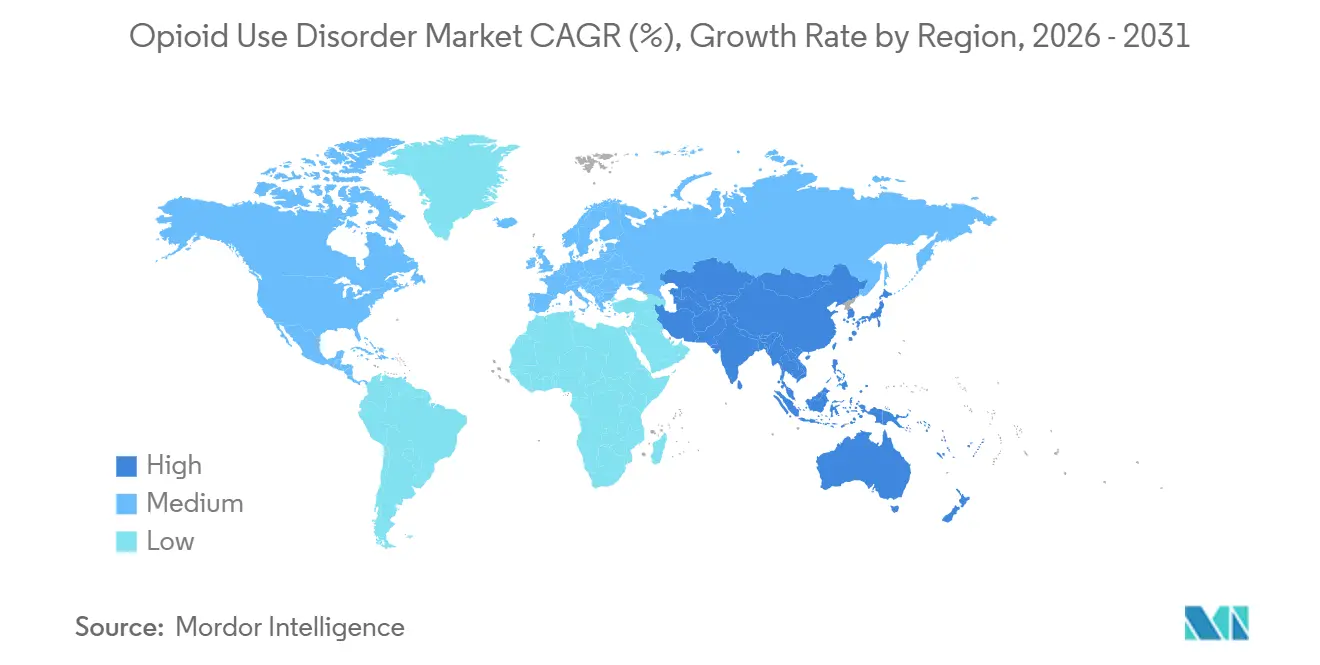

- By geography, North America led with a 39.25% share in 2025, while Asia-Pacific is expected to record the highest CAGR of 11.20% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Opioid Use Disorder Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising opioid dependence and persistent treatment gap | +2.5% | Global, with highest burden in North America and APAC emerging economies | Long term (≥ 4 years) |

| Telemedicine expansion for buprenorphine prescribing | +2.1% | North America and Europe, with early adoption in Australia | Medium term (2-4 years) |

| Long-acting injectable adoption improving adherence and retention | +2.0% | North America, core European markets, and Australia | Medium term (2-4 years) |

| Policy flexibility for opioid treatment programs | +1.3% | North America primary, Europe secondary | Short term (≤ 2 years) |

| Fentanyl-driven demand for higher-dose and sustained-release formulations | +1.7% | North America core, with spillover into Europe | Medium term (2-4 years) |

| Expanded payer coverage for chronic addiction management | +1.5% | North America through Medicaid, Europe through statutory coverage systems | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Opioid Dependence and Untreated Treatment Gap

In 2024, the U.S. recorded over 80,000 overdose deaths. Data from early 2026 indicated that, despite a recent decline in total fatalities, the burden of synthetic opioids remained significantly elevated compared to pre-fentanyl levels. A key demand driver in the opioid use disorder market is the low treatment rate, overshadowing mere prevalence figures. SAMHSA's 2024 estimates revealed that only 25% of individuals with substance use disorders received treatment, highlighting a substantial and persistent care gap.[2]The White House, “National Drug Control Strategy 2026,” The White House, whitehouse.gov The 2026 National Drug Control Strategy emphasized early recognition and treatment access, advocating for broader prescribing opportunities across all approved medication classes.[3]U.S. Drug Enforcement Administration, “DEA Extends Telemedicine Flexibilities to Ensure Continued Access to Care,” DEA, dea.gov In India, government data indicated that 2.06% of the population faces opioid consumption issues, spotlighting a vast, untreated patient demographic in a pivotal growth region for the opioid use disorder market. The treated population lags significantly behind clinical needs, with market expansion driven more by improved access than by incidence growth.

Telemedicine Expansion for Buprenorphine Prescribing

In December 2025, the DEA and HHS extended COVID-19 telemedicine flexibilities, allowing audio-video and audio-only prescriptions of Schedule III-V opioid use disorder medications through December 31, 2026. This move prevented stricter in-person visit mandates for remote treatment patients, safeguarding a significant portion of the prescribing base. Additionally, a rule effective February 18, 2025, permitted practitioners to prescribe a 6-month supply of buprenorphine post an audio-only telehealth session, contingent on meeting PDMP verification standards. A February 2025 study revealed an 82.6% retention rate for patients using home-delivery pharmacy partners over three months, compared to 58.9% for pharmacy pickups. Policy flexibility for telemedicine prescribing continues to support the opioid use disorder market, though state laws and DEA compliance shape its scalability.[4]U.S. Drug Enforcement Administration and Department of Health and Human Services, “Expansion of Buprenorphine Treatment via Telemedicine Encounter, Final Rule,” Regulations.gov, regulations.gov

Long-Acting Injectable Adoption Improves Adherence and Reduces Diversion Risk

In February 2025, the FDA approved label changes for SUBLOCADE, enabling quicker initiation post a single sublingual dose and expanding injection sites to include the thigh, buttock, and upper arm. Long-acting injectables are now integrated earlier in treatment pathways, particularly in cases of weak adherence or high relapse risks. A 2025 study highlighted the safe initiation of long-acting injectable buprenorphine in emergency departments for patients with Clinical Opiate Withdrawal Scale scores of 4 or higher. Commercial uptake is evident, with Camurus reporting a 47% year-over-year increase in Brixadi quarterly royalties, reaching SEK 122 million (USD 23.56 million) in Q4 2025. Federal diversion-control expectations favor non-transferable formulations, while clinical guidance supports extended-release buprenorphine and naltrexone for adherence or relapse concerns, strengthening the injectable segment of the market.

Fentanyl-Driven Demand for Higher-Retention Formulations

The fentanyl crisis has reshaped treatment initiation and maintenance, with many patients requiring daily buprenorphine doses exceeding 24 mg and facing higher risks of precipitated withdrawal under traditional induction methods. This has driven the adoption of low-dose induction techniques and extended-release products, offering greater stability during early treatment. Patients failing on standard-dose sublingual therapy are transitioning to branded injectable alternatives with higher prescription values. The emergence of sedatives like medetomidine in urban U.S. areas has increased the preference for supervised delivery over home-managed dosing. These trends reinforce the dominance of injectable formulations and sustain demand for extended-release products through 2031.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Methadone access limited to certified opioid treatment programs | -1.8% | North America, where 80% of U.S. counties lack an OTP | Long term (≥ 4 years) |

| Stigma, prior authorization, and reimbursement gaps | -1.6% | Global, with the strongest effect in North America and APAC | Medium term (2-4 years) |

| Diversion concerns and controlled-substance compliance burdens | -1.0% | North America and Europe | Medium term (2-4 years) |

| Adverse effects and induction complexity from fentanyl exposure | -0.9% | North America core, with early emergence in Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Methadone Access Limited to Certified Opioid Treatment Programs

Under the Controlled Substances Act, methadone is restricted to federally certified opioid treatment programs, creating a significant barrier to growth in the opioid use disorder market. In 2025, ASAM reported that 80% of U.S. counties lacked an opioid treatment program, with half of these counties being rural, highlighting geographic disparities in access. A 2025 study found that states with stricter OTP regulations had lower methadone maintenance treatment rates per ZIP code, even after accounting for demographic differences. Additional challenges, such as state certificate-of-need laws, zoning regulations, and counseling frequency requirements, increase the cost of establishing or expanding treatment sites, limiting competition and slowing new channel development. Reform proposals, including state-led methadone policy changes and community pharmacy dispensing models, remain under discussion, but the lack of federal support suggests these restrictions will persist during much of the forecast period.

Stigma, Prior Authorization, and Reimbursement Gaps

Stigma continues to hinder treatment adoption, as patients delay care, rural primary care providers hesitate to prescribe, and some institutions restrict medication use despite clear need. A 2025 study highlighted that rural primary care providers face stigma toward patients, prescribers, and buprenorphine itself, reducing their willingness to prescribe. A review in 2025 identified gaps in Medicaid managed care access, with some states lacking documented coverage for extended-release buprenorphine, indicating a disconnect between policy and clinical access. Another study found that banning prior authorization for buprenorphine did not improve retention among privately insured patients, pointing to broader systemic barriers. Additional challenges, such as compliance requirements, diversion control, and fentanyl-related induction complexities, further impede treatment uptake. The American Medical Association has called for removing prior authorization and expanding methadone access to address these barriers effectively.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: Buprenorphine Holds the Lead While Naltrexone Gains Ground

In 2025, Buprenorphine captured 59.58% of the opioid use disorder market share, driven by its partial-agonist profile, superior safety compared to methadone, and availability in various forms such as sublingual and buccal films, tablets, and injectables. Non-OTP prescribers, including primary care and telehealth providers, further boosted its adoption under federal telemedicine regulations. Methadone remained the second-largest drug class, playing a critical role in high-dependency and polysubstance cases, though its reach was limited by OTP access barriers.

Naltrexone is projected to grow at a CAGR of 11.45% through 2031, supported by its opioid-free antagonist mechanism, which appeals to settings and patients favoring full receptor blockade over agonist therapy. Alkermes reported VIVITROL net sales of nearly USD 468 million in FY 2025, with 2026 guidance of USD 460-480 million, indicating sustained demand at premium pricing. The September 2025 authorized generic agreement between Alkermes and Amneal Pharmaceuticals, covering up to 15% of 2024 VIVITROL unit sales, reflects evolving pricing dynamics. Naltrexone’s non-scheduled status under the Controlled Substances Act enhances accessibility for community pharmacies and correctional health systems, reducing compliance burdens compared to buprenorphine.

By Route of Administration: Injectable Leadership Stays Intact While Oral Use Expands Faster

Injectable formulations accounted for 59.78% of the opioid use disorder market in 2025, driven by clinical preference for supervised, long-acting treatments in structured settings. Monthly injectable buprenorphine led this trend, benefiting from improved adherence, reduced diversion risks, and increased provider confidence following label updates. Camurus reported 67,000 patients on Buvidal in Europe and Australia as of September 2025, with a target of over 100,000 patients by 2027. The December 2025 BRIXADI label update and the adoption of prolonged-release injectable buprenorphine in five European countries further support growth in this segment.

The oral segment is expected to grow at a CAGR of 12.55% from 2026 to 2031, aided by telehealth regulations that simplify sublingual buprenorphine initiation and maintenance. A February 2025 federal rule allowing a 6-month supply after an audio-only encounter streamlined treatment entry without requiring in-person visits. Research from Workit Health showed home delivery of oral buprenorphine achieved 82.6% three-month retention compared to 58.9% for standard pharmacy pickup, encouraging providers and payers to support remote dispensing. Generic oral products from Hikma, Teva, and Sun Pharmaceutical remain critical for cost-effective treatment options, while prior authorization requirements for extended-release injectables direct some patients toward oral therapies.

By Distribution Channel: Hospital Pharmacies Lead Today While Online Pharmacies Scale Quickly

Hospital pharmacies held a 46.12% share of the distribution channel segment in 2025, serving as the primary dispensing point for long-acting injectable products requiring clinical administration and monitoring. SUBLOCADE and BRIXADI operate under FDA-mandated REMS frameworks, ensuring compliance through hospital-based outpatient pharmacies and certified OTPs. This structure secures a strong channel position for branded injectables while limiting competition from other channels. Retail pharmacies remain essential for dispensing oral buprenorphine generics and supporting patients transitioning to maintenance therapy.

Online pharmacies are projected to grow at a CAGR of 11.24% through 2031, driven by telehealth-linked buprenorphine treatments. Workit Health data highlighted a nearly 24 percentage point higher six-month retention rate for home delivery patients compared to in-person pickup. The DEA’s extension of telemedicine flexibilities through December 2026 supports digital prescribing models used by providers like Ophelia, DoneRx, and Bicycle Health. However, scaling remains constrained by PDMP verification requirements, as practitioners must document state-level monitoring before issuing controlled-substance prescriptions initiated via telehealth.

Geography Analysis

In 2025, North America held 39.25% of the opioid use disorder market share, making it the largest region by value and treatment volume. This dominance stems from a high disease burden, a mature opioid treatment program infrastructure, and significant public-payer involvement in treatment financing. While Canada is advancing injectable treatments in urban centers, Mexico faces limited opportunities due to inadequate OTP infrastructure and low addiction-care spending. Medicaid expansion states in the U.S. saw only a 17% decline in buprenorphine prescriptions during restrictive policy periods, compared to a 47.6% decline in non-expansion states, highlighting the impact of payer structures on demand resilience.

Europe remained the second-largest region in the opioid use disorder market, with Germany and France leading as key national contributors. Their buprenorphine and methadone treatment systems address most opioid agonist therapy needs, providing a strong treatment base. The European Drug Report 2025 indicated that 35% of opioid agonist therapy clients in Europe use buprenorphine, while methadone accounts for 55%, with buprenorphine being the primary option in nine member states.

Asia-Pacific is projected to grow at the fastest CAGR of 11.20% through 2031, making it a key expansion region for the opioid use disorder market. India’s 2.06% opioid problem prevalence highlights a large untreated population, even as formal treatment systems are still scaling. China is progressing with early-stage public investments and pilot programs. Mature treatment settings in Australia, South Korea, and Japan, along with Buvidal’s traction in Australia, demonstrate the potential for long-acting injectable models to gain market share outside North America. South America, the Middle East, and Africa remain smaller markets, with Brazil and GCC countries offering near-term opportunities, while fragmented regulations and criminalization policies in parts of Southeast Asia limit demand and increase entry costs for global suppliers.

Competitive Landscape

The opioid use disorder market remains moderately concentrated in branded specialty treatments, despite the broader treatment space including a significant layer of generic oral solutions. Camurus and Braeburn are key challengers in long-acting injectable therapies, with Camurus reporting Brixadi as the strongest launch in its category and Buvidal achieving six consecutive years of double-digit sales growth across Europe, Australia, and MENA. Alkermes maintains a unique position with VIVITROL, the only extended-release injectable naltrexone product, and its 2025 authorized generic agreement with Amneal Pharmaceuticals reflects a strategic approach to pricing pressures. The generic segment, including Hikma, Teva, Sun Pharmaceutical, and Dr. Reddy’s Laboratories, competes primarily on price and formulary access, exerting the most pressure on branded oral products rather than injectable franchises.

Opportunities for differentiation exist in digital support tools, methadone access expansion, and correctional health delivery. Orexo AB, through its work with ZUBSOLV, is advancing prescription digital therapeutics to enhance patient engagement and treatment persistence. Indivior’s Phase III development efforts and investments in proprietary manufacturing platforms demonstrate its commitment to maintaining leadership beyond its current portfolio. FDA-mandated REMS structures for BRIXADI and SUBLOCADE create significant barriers for generic injectable competitors due to strict distribution and site certification controls.

The opioid use disorder market is defined by a dual structure, with branded injectable suppliers dominating high-value treatment segments and generic oral suppliers driving access through cost-effective volume. Companies that integrate payer access, compliant distribution, and simplified initiation pathways hold a competitive edge over those relying solely on brand presence. Recent developments, such as Indivior’s SUBLOCADE label update, Camurus’s geographic expansion of Buvidal, and Alkermes’s controlled authorized generic strategy, indicate that leading players are preparing for a larger yet more segmented treatment landscape. Competitive intensity is expected to rise through 2031, but profitability will likely depend on compliance capabilities, payer positioning, and product differentiation rather than pricing alone.

Opioid Use Disorder Industry Leaders

Alkermes plc

Indivior PLC

Camurus AB

Orexo AB

Teva Pharmaceutical Industries Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: cliexaAI's Opioid Use Disorder Solution was recognized as a qualified solution on the Mayo Clinic Platform. This achievement highlights the company's eight-year effort to develop clinically validated and explainable AI tools for the healthcare industry.

- December 2025: The DEA and HHS issued the Fourth Temporary Extension of COVID-19 Telemedicine Flexibilities, extending them through December 31, 2026. This extension ensures the continuation of audio-video and audio-only prescribing for Schedule III-V opioid use disorder medications, supporting telehealth-based treatment continuity.

- December 2025: BRIXADI's prescribing information was updated to include revised Dosage and Administration guidelines and enhanced Warnings and Precautions. These updates expand administration guidance and reinforce safety protocols, particularly for use with overdose reversal agents.

- May 2025: Camurus launched Buvidal in Portugal, offering weekly and monthly formulations for opioid dependence treatment. This expansion increased coverage to over 20 countries and raised the estimated patient base to approximately 65,000 across Europe and Australia by mid-2025.

Global Opioid Use Disorder Market Report Scope

As per the scope of the report, opioid use disorder (OUD) is defined as the chronic use of opioids that causes clinically significant distress or impairment. Symptoms of this disease include an overpowering desire to use opioids, increased opioid tolerance, and withdrawal syndrome when opioids are discontinued.

The opioid use disorder market is segmented by drug class, route of administration, distribution channel, and geography. By drug class, the market includes buprenorphine, methadone, and naltrexone. By route of administration, the market is segmented into oral and injectable. By distribution channel, the market is categorized into hospital pharmacies, retail pharmacies, and online pharmacies. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Buprenorphine |

| Methadone |

| Naltrexone |

| Oral |

| Injectable |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Drug Class | Buprenorphine | |

| Methadone | ||

| Naltrexone | ||

| By Route Of Administration | Oral | |

| Injectable | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the opioid use disorder market?

The opioid use disorder market was valued at USD 4.78 billion in 2026 and is forecast to reach USD 8.04 billion by 2031, at a CAGR of 10.97%.

Which region leads opioid use disorder treatment demand?

North America led in 2025 with a 39.25% share, supported by established OTP infrastructure and Medicaid's role in treatment financing.

Which drug class holds the largest share in opioid use disorder treatment?

Buprenorphine led the drug class segment with a 59.58% share in 2025, helped by broad formulation availability and telehealth prescribing flexibility.

Which route of administration is growing the fastest?

The oral segment is projected to grow at a 12.55% CAGR through 2031, supported by telehealth initiation and strong retention in home-delivery models.

Why are long-acting injectables gaining traction in opioid dependence care?

They improve adherence, reduce diversion risk, and are becoming easier to initiate after the 2025 SUBLOCADE label changes and ongoing BRIXADI rollout.

Which distribution channel is expanding the fastest for opioid dependence medications?

Online pharmacies are projected to grow at an 11.24% CAGR through 2031 as telehealth prescribing and home delivery become more common.

Page last updated on: