Opioid Induced Constipation Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.26 Billion |

| Market Size (2031) | USD 4.49 Billion |

| Growth Rate (2026 - 2031) | 6.61% CAGR |

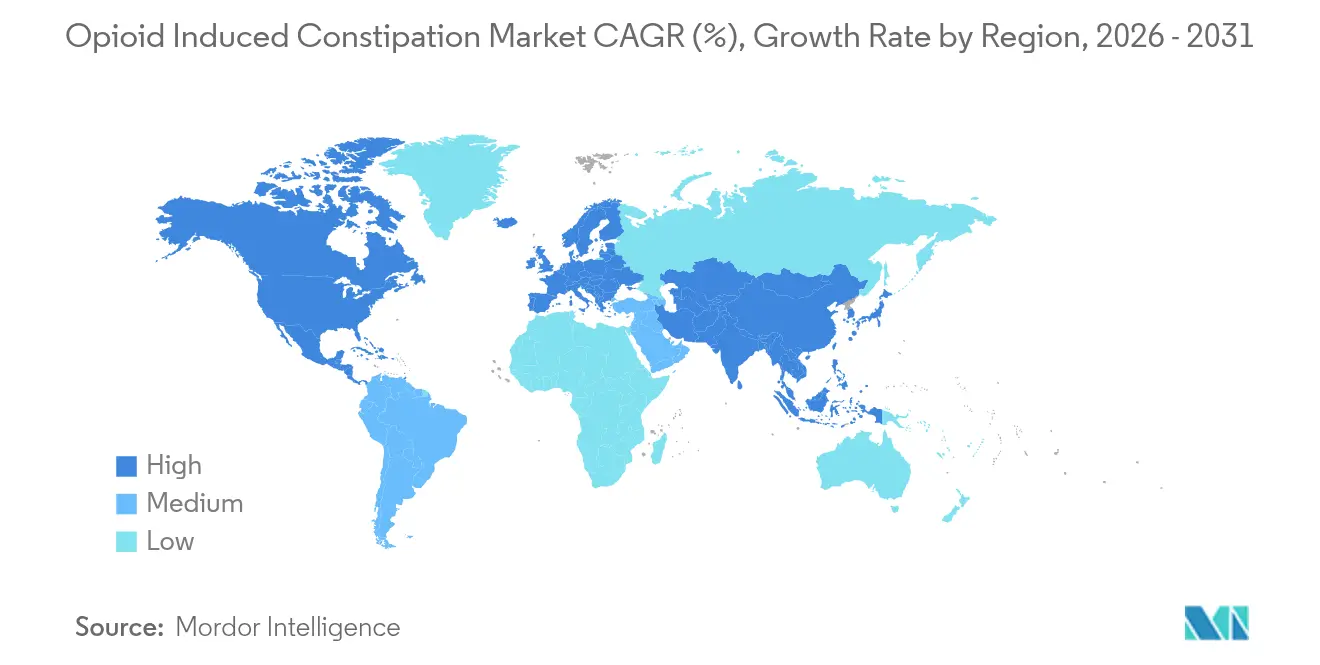

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

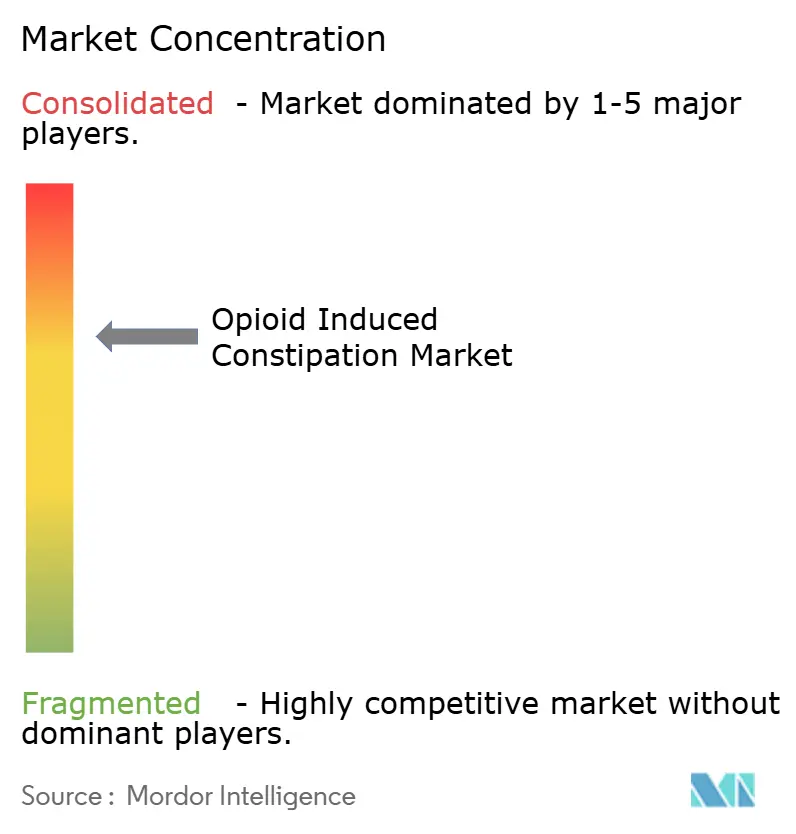

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Opioid Induced Constipation Market Analysis by Mordor Intelligence

The opioid induced constipation market size was valued at USD 3.06 billion in 2025 and estimated to grow from USD 3.26 billion in 2026 to reach USD 4.49 billion by 2031, at a CAGR of 6.61% during the forecast period (2026-2031). The sustained growth reflects the need to manage constipation in 40–80% of patients who rely on opioids for chronic or cancer-related pain. Rising opioid prescriptions, regulatory approvals for novel peripherally acting µ-opioid receptor antagonists (PAMORAs), and growing adoption of digital adherence tools are core demand drivers. North America dominates due to high opioid consumption, yet Asia Pacific records the fastest expansion as Japan, China, and India harmonize guidelines and broaden access to proven therapies. Label extensions into pediatric populations and hospital stewardship mandates institutionalize prophylactic bowel regimens, while pipeline products with improved safety profiles strengthen the opioid induced constipation market’s long-term outlook.

Key Report Takeaways

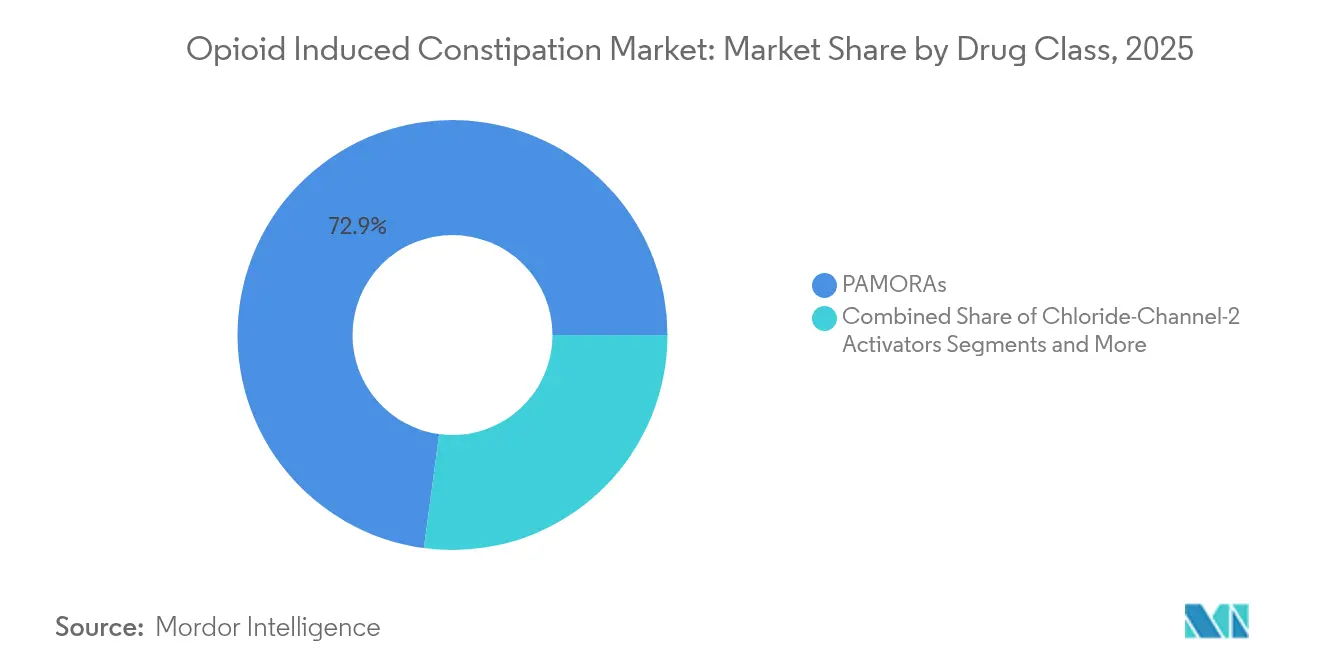

- By drug class, PAMORAs led with 72.88% revenue share in 2025; guanylate cyclase-C agonists are forecast to expand at an 11.02% CAGR through 2031.

- By prescription type, prescription medications held 90.80% of the opioid induced constipation market share in 2025, while OTC products are projected to grow at an 7.95% CAGR to 2031.

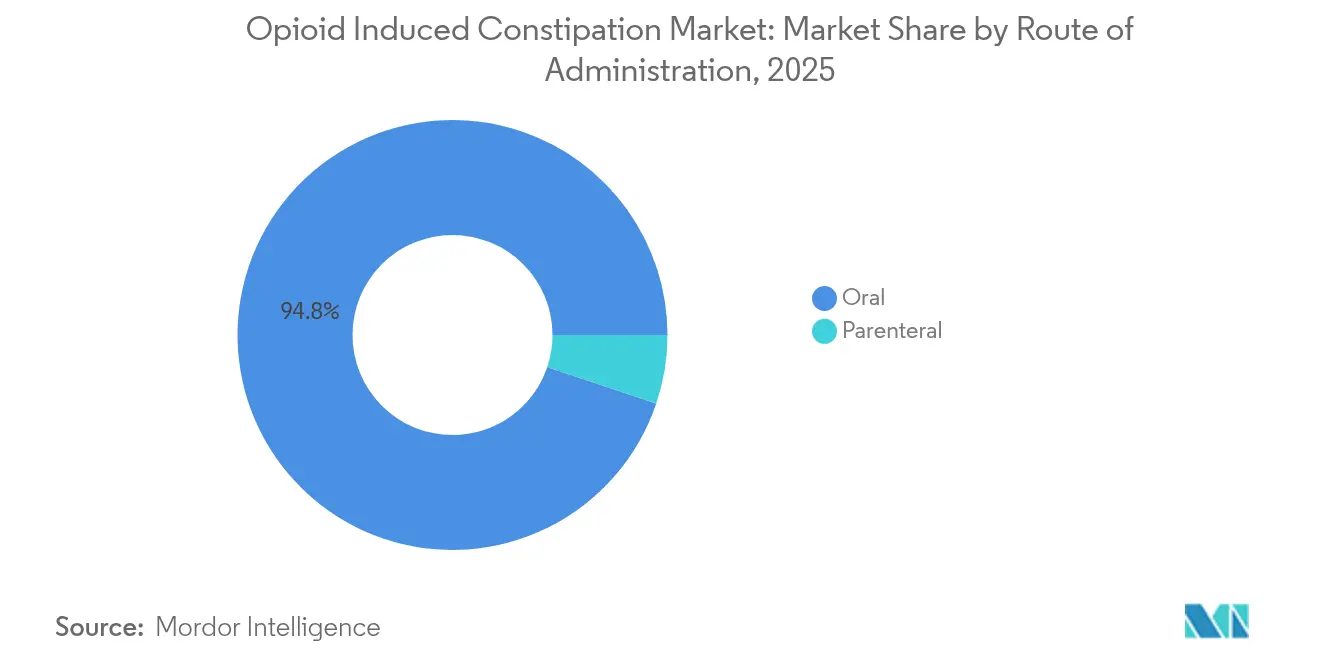

- By route, oral formulations accounted for 94.83% share of the opioid induced constipation market size in 2025 and parenteral products are set to advance at a 7.32% CAGR through 2031.

- By patient group, non-cancer chronic-pain patients captured 68.55% of the opioid induced constipation market share in 2025; the cancer segment is expected to grow at a 9.12% CAGR between 2026-2031.

- By distribution channel, hospital pharmacies represented 44.90% of revenue in 2025, while online pharmacies are forecast to post a 10.15% CAGR during the same period.

- By geography, North America contributed 44.10% revenue in 2025; Asia Pacific is projected to witness the highest 7.28% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Opioid Induced Constipation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Opioid Prescriptions For Chronic Pain Management | +1.80% | Global, concentrated in North America | Long term (≥ 4 years) |

| Label Expansions & Launches Of Novel PAMORAs | +1.20% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| High Prevalence Of Chronic Non-Cancer & Cancer Pain | +1.50% | Global | Long term (≥ 4 years) |

| Digital-Therapeutic Co-Prescription Boosting Adherence | +0.70% | North America & EU core, spill-over to APAC | Medium term (2-4 years) |

| Pipeline Combo Opioid-PAMORA Formulations | +0.90% | Global | Long term (≥ 4 years) |

| Hospital Opioid-Stewardship Mandates For Bowel Regimens | +0.60% | North America & EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Opioid Prescriptions for Chronic Pain Management

Steady reliance on opioids for legitimate pain control sustains product demand despite broader efforts to curb misuse. A 2025 Japanese cohort study found 30% opioid-induced constipation (OIC) incidence among non-cancer patients using weak opioids, climbing to 49.2% by day 14 of therapy.[1]NCBI, “Opioid-Induced Constipation Review,” ncbi.nlm.nih.govCancer cohorts reported 56% cumulative incidence within two weeks of opioid initiation, underlining the inevitability of bowel dysfunction when analgesia is opioid-based. Many U.S. hospitals now require prophylactic laxatives within 24 hours of the first opioid dose, formalizing treatment as a default component of pain care.

Label Expansions & Launches of Novel PAMORAs

Regulators are broadening indications to underserved populations. FDA clearance of linaclotide for children aged 6–17 in May 2024 established the first U.S. pediatric option.[2]Rika Ohta et al., “Incidence of Opioid-Induced Constipation in Japanese Non-Cancer Pain,” nature.com The European Medicines Agency accepted AstraZeneca’s naloxegol dossier in June 2024, signaling alignment with U.S. standards.[3]FDA, “Linaclotide Pediatric Approval,” gi.org Conversely, the FDA withdrew ENTEREG (alvimopan) in August 2024, highlighting close scrutiny. Pipeline assets such as PF614-MPAR, which combines opioid analgesia with built-in overdose protection, widen the competitive field.

High Prevalence of Chronic Non-Cancer & Cancer Pain

Non-cancer conditions—chiefly osteoarthritis and neuropathic pain—constituted 69.0% of 2024 prescriptions, yet cancer patients generate the fastest demand growth owing to longer survival and higher dosing. A 2024 meta-analysis of 24 randomized trials (9,586 participants) showed opioids increased constipation risk 3.57-fold in osteoarthritis management. Clinical protocols increasingly embed proactive bowel regimens to prevent therapy interruptions.

Digital-Therapeutic Co-Prescription Boosting Adherence

Permanent German reimbursement for Cara Care IBS in June 2024 validated payers’ willingness to cover gastrointestinal digital therapeutics. Evidence indicates that coupling PAMORAs with smartphone-based symptom tracking improves adherence and accelerates dose titration. U.S. centers leverage real-time dashboards to trigger nurse interventions if no stool is logged within 24 hours, lowering unplanned readmissions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Next-Generation Non-Opioid Analgesics | -1.40% | Global, early adoption in North America | Medium term (2-4 years) |

| Patient Reluctance Due To Adverse-Event Awareness | -0.80% | Global | Short term (≤ 2 years) |

| European Reimbursement Claw-Backs On PAMORA Pricing | -0.60% | Europe | Short term (≤ 2 years) |

| Medical-Cannabis Substitution Lowering Opioid Doses | -0.50% | North America, selective EU markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Next-Generation Non-Opioid Analgesics

The FDA approved suzetrigine in January 2025. It offers strong acute analgesia with no opioid receptor action, removing the risk of constipation. Although priced at USD 15.50 per pill, hospital formularies may adopt it for postsurgical pain, trimming future OIC cases. Academic teams are also advancing gut-selective oxytocin mimetics that calm visceral pain without systemic absorption.

Patient Reluctance Due to Adverse-Event Awareness

Real-world data link naldemedine to 27.5% diarrhea versus 5.3% on placebo, prompting some patients to forego therapy. The FDA’s adverse-event database lists rare ischemic colitis with lubiprostone, sparking online caution communities. Clinicians spend more time counseling, and some switch to step-wise osmotic laxatives, temporarily delaying PAMORA initiation

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: Diverse Mechanisms Deepen the Therapeutic Toolbox

PAMORAs contributed USD 2.23 billion in 2025, equal to 72.88% of the opioid induced constipation market size, as their gut-restricted receptor blockade preserves central analgesia. The class retains physician confidence despite the FDA withdrawal of alvimopan because alternatives such as naldemedine yield 81–90% spontaneous bowel movement response in Japanese trials. Looking ahead, guanylate cyclase-C agonists are forecast to post the highest 11.02% CAGR, underpinned by pediatric label extensions. Sustained investment in combination opioid-PAMORA pills promises to defend the opioid induced constipation market share of peripherally acting agents amid mounting class competition.

Manufacturers hedge risk by diversifying their mode of action. 5-HT4 receptor agonists with improved cardiac safety, hemp-derived motility enhancers, and gut-selective peptides are now in Phase II. These entrants could capture niche cohorts intolerant of diarrhea or abdominal cramping. Nonetheless, prescribers may prefer well-established PAMORAs until head-to-head outcomes trials confirm equivalence, ensuring the opioid induced constipation market remains dominated by incumbents through most of the outlook period.

By Prescription Type: Evolving Regulation Shapes Consumer Access

Prescription products represented 90.80% of 2025 revenue, confirming clinician oversight remains essential when manipulating µ-opioid receptors. The opioid induced constipation market size for OTC formulations was modest but is predicted to grow as consumer familiarity rises. Regulatory bodies continue to debate switching select PAMORAs to pharmacist-guided status once post-marketing surveillance demonstrates low misuse risk.

Advocates believe successful Rx-to-OTC switches could reduce emergency visits caused by chronic laxative misuse. Yet the mechanistic complexity of opioid antagonism and potential for precipitated withdrawal keep most molecules in prescription channels for now. Digital prescription platforms may blur lines: validated bowel-tracking apps bundled with drug coupons offer semi-automated follow-up, gradually shifting portions of the opioid induced constipation industry toward a self-management paradigm.

By Route of Administration: Oral Dominance with Targeted Parenteral Use

Oral agents controlled 94.83% of 2025 volumes, favored for convenience and lower administration cost. Institutional protocols, however, rely on injectable methylnaltrexone when patients cannot tolerate oral intake, contributing to a 7.32% CAGR for parenteral options. Product developers seek oral formulations with minimal food effect to improve adherence; revised naloxegol formulations under clinical review allow dosing without regard to meals, which could further reinforce oral predominance within the opioid induced constipation market.

Hospitals nonetheless value rapid-acting injectables for postoperative and palliative care. Novel delivery vectors such as buccal films and transdermal patches are in early studies, targeting populations with impaired swallowing. Should these platforms gain approval, they may incrementally erode the oral share, especially in specialized oncology settings where predictable onset outweighs tablet convenience.

By Patient Group: Divergent Care Pathways Shape Demand

Non-cancer chronic-pain patients accounted for 68.55% of the opioid induced constipation market size in 2025, buoyed by long-term osteoarthritis management in aging populations. Cancer patients, although only 31.45% of total users, underpin premium pricing strategies: high-dose opioid regimens elevate constipation severity, and willingness to pay for rapid relief supports formulary inclusion of newer PAMORAs.

Evidence-based guidelines from oncology societies now advocate prophylactic bowel regimens from day 1 of opioid therapy, driving earlier and often higher-dose intervention. In contrast, primary-care settings for back pain or neuropathy typically exhaust bulk-forming and osmotic laxatives before escalating to prescription PAMORAs, explaining slower unit growth despite large absolute volumes within the opioid induced constipation market.

By Distribution Channel: Digital Dispensing Gains Traction

Hospital pharmacies generated 44.90% of 2025 sales, reflecting inpatient stewardship mandates. Telehealth growth stabilised digital opioid prescribing at 8.4% of total scripts in 2022, creating fertile ground for online pharmacies to process refill orders with integrated video counselling. As a result, the online channel is projected to expand at a 10.15% CAGR.

Retail outlets refine their value proposition by offering on-site pharmacists certified in opioid risk mitigation and bowel regimen education. Meanwhile, manufacturers form exclusive e-pharmacy partnerships for high-priced launches such as suzetrigine, ensuring tight supply control and real-time patient data collection. This hybrid landscape reinforces the opioid induced constipation industry’s need to balance broad access with controlled substance safeguards.

Geography Analysis

North America contributed 44.10% of global revenue in 2025, anchored by the United States, which consumes nearly 80% of worldwide opioid volumes. Widespread payer coverage, entrenched pain management guidelines, and FDA leadership in approving innovative classes keep the region at the forefront. Hospital networks, from Cedars-Sinai to Mayo Clinic, have embedded digital stool monitors that trigger immediate laxative escalation when no bowel movement is recorded within 24 hours, underscoring an institutional commitment to proactive care. Canada mirrors U.S. dynamics ,though on a smaller scale, with national opioid stewardship frameworks adopting fixed bowel regimen bundles in tertiary hospitals. Policy reforms aimed at curbing opioid misuse steadily reduce new opioid starts, yet high chronic-user prevalence maintains a sizeable patient pool requiring constipation therapies. Consequently, the opioid induced constipation market retains robust, if maturing, growth prospects in North America.

Asia Pacific exhibits the highest 7.28% CAGR through 2031. Japan's rapid uptake of naldemedine, validated in Phase III trials reporting 81–90% response despite 88-90% adverse-event incidence, showcases clinical confidence. China's inclusion of PAMORAs in provincial reimbursement lists improves affordability, while a 2024 osteoarthritis meta-analysis confirming a 3.57-fold constipation risk with opioids informs policymakers considering broader adoption. India's burgeoning generic manufacturing base positions domestic firms to launch cost-effective entrants once international patents lapse, enhancing treatment penetration across lower-income populations.

Europe maintains steady uptake amid payer scrutiny. The EMA's June 2024 acceptance of naloxegol and Germany's permanent reimbursement for a gastrointestinal digital therapeutic illustrate balanced innovation and cost containment. National health technology assessment bodies evaluate not just drug price but total cost of care, encouraging manufacturers to package PAMORAs with adherence-support platforms. Reimbursement claw-backs in markets such as France temper list prices, yet volume remains resilient due to aging demographics and oncologic opioid use. The opioid induced constipation market therefore shows moderate but reliable expansion across the continent.

Competitive Landscape

The opioid induced constipation market is moderately consolidated. Grünenthal strengthened its position by purchasing global rights to Movantik for USD 250 million in July 2024, supplementing an existing pain portfolio. In March 2025, Mallinckrodt and Endo agreed to a USD 6.7 billion merger, combining legacy opioid franchises to secure scale efficiencies while navigating litigation liabilities. Such deals raise combined market power but still leave room for mid-cap innovators focusing on complementary mechanisms.

Pipeline differentiation is intense. Ensysce Biosciences won USD 5.3 million NIH funding to progress PF614-MPAR, a tamper-resistant opioid paired with an on-board PAMORA that aims to abolish OIC while mitigating overdose. Vertex entered the space tangentially with suzetrigine, leveraging non-opioid pain relief to bypass constipation entirely. Digital-health specialists, including Mahana Therapeutics, partner with drug firms to supply FDA-cleared apps that document stool frequency and trigger dosing reminders, an emerging battleground for user loyalty.

Regulatory actions shape competition. The FDA’s withdrawal of alvimopan removed a perioperative PAMORA option, consolidating share among naloxegol, naldemedine, and methylnaltrexone. Conversely, pediatric clearance for linaclotide opened a white-space segment that incumbent Aperion now races to serve. Overall, firms concentrate on demonstrating value through health-economic studies rather than price alone, recognizing that payers demand evidence of reduced hospitalization and improved quality of life before granting premium reimbursement tiers.

Opioid Induced Constipation Industry Leaders

AstraZeneca plc

Merck & Co Inc

Shionogi & Co Ltd

Mallinckrodt Pharmaceuticals

Bausch Health ( Salix Pharmaceutical Inc.)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Mallinckrodt and Endo announced a USD 6.7 billion merger aimed at integrating opioid portfolios and resolving legal liabilities.

- January 2025: FDA approved Journavx (suzetrigine), the first new non-opioid pain therapy in decades, eliminating OIC risk for acute pain patients.

- January 2025: FDA cleared ANI Pharmaceuticals’ first generic of prucalopride with 180-day exclusivity.

- July 2024: FDA approved Zurnai, the inaugural nalmefene autoinjector for opioid overdose reversal.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the opioid-induced constipation (OIC) market as every branded or generic prescription and over-the-counter drug that is expressly labeled to ease constipation caused by short- or long-term opioid therapy. Covered classes include peripherally acting µ-opioid receptor antagonists (PAMORAs), chloride-channel activators, guanylate cyclase-C agonists, plus stimulant or osmotic laxatives carrying an OIC claim. Values reflect manufacturer revenue across seventeen countries that issue more than ninety-five percent of global opioid prescriptions.

Scope exclusion: Devices, fiber supplements, and general-use laxatives without an OIC claim are left outside our work.

Segmentation Overview

- By Drug Class

- PAMORAs

- Chloride-Channel-2 Activators

- Guanylate Cyclase-C Agonists

- Others

- By Prescription Type

- Prescription

- Over-the-Counter (OTC)

- By Route of Administration

- Oral

- Parenteral

- By Patient Group

- Cancer-Pain Patients

- Non-Cancer Chronic-Pain Patients

- By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts spoke with gastroenterologists, pain doctors, hospital pharmacists, and payor managers across North America, Europe, and Asia-Pacific. Their views on therapy mix, net prices, and adherence refined assumptions and validated desk findings.

Desk Research

We pulled opioid-prescription totals from the CDC, NHS Digital, and Japan's MHLW, then matched them with UN Comtrade shipment codes. Launch timelines and label updates were mapped from US FDA, EMA, and PMDA notices. Price curves and channel splits came from IQVIA MIDAS snapshots, while D&B Hoovers and Dow Jones Factiva helped us isolate pure OIC revenue inside diversified firms. This list is illustrative; many other public and paid sources informed the evidence base.

Market-Sizing & Forecasting

A top-down prevalence-to-treated-pool model converts national opioid-user counts into an addressable OIC base, multiplies therapy days by weighted average selling price, and is cross-checked through supplier roll-ups and channel calls. Core drivers, opioid-prescription growth, PAMORA uptake, therapy duration, patent expiries, and reimbursement shifts feed a multivariate regression that builds the 2025-2030 view, while selective bottom-up tests keep totals realistic.

Data Validation & Update Cycle

Outputs face peer review, anomaly flags, and variance checks versus quarterly sales prints. Full refreshes come each year, with interim updates after major approvals or policy shocks.

Why Mordor's Opioid Induced Constipation Market Baseline Commands Reliability

Published figures diverge because firms pick narrower drug baskets, apply list rather than net prices, or freeze models for years.

We blend broader scope with discounted prices and annual reviews, giving buyers a dependable starting point.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.06 B (2025) | Mordor Intelligence | - |

| USD 2.10 B (2023) | Global Consultancy A | Prescription drugs only, 27-country scope |

| USD 2.87 B (2024) | Industry Association B | Uses wholesale list prices, no channel discounts |

| USD 1.11 B (2021) | Trade Journal C | Excludes OTC products; outdated base year |

Together, these contrasts show how Mordor's transparent scope, realistic price work, and disciplined refresh cadence give decision-makers a balanced baseline they can trace and reproduce with confidence.

Key Questions Answered in the Report

What is the current size of the opioid induced constipation market?

The market stands at USD 3.26 billion in 2026 and is projected to grow to USD 4.49 billion by 2031 at a 6.61% CAGR.

Which drug class leads the opioid induced constipation market?

PAMORAs dominate with 72.88% revenue share in 2025 due to their ability to relieve constipation without reducing analgesic efficacy.

Why is Asia Pacific the fastest-growing region?

Regulatory harmonization, expanding pain-care infrastructure, and rapid adoption of naldemedine in Japan are driving a 7.28% regional CAGR through 2031.

How are digital therapeutics influencing market growth?

Reimbursed apps that monitor bowel function improve adherence and provide real-time data, increasing treatment effectiveness and creating new revenue streams.

What impact will non-opioid analgesics have on the market?

New agents like suzetrigine remove constipation risk entirely, potentially reducing future demand, yet cost and limited chronic-pain data suggest only gradual uptake.

Which distribution channel is growing fastest?

Online pharmacies are forecast to register a 10.15% CAGR as telehealth stabilizes and patients seek convenient refill options.

Page last updated on: