Disruptive Behavior Disorder Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

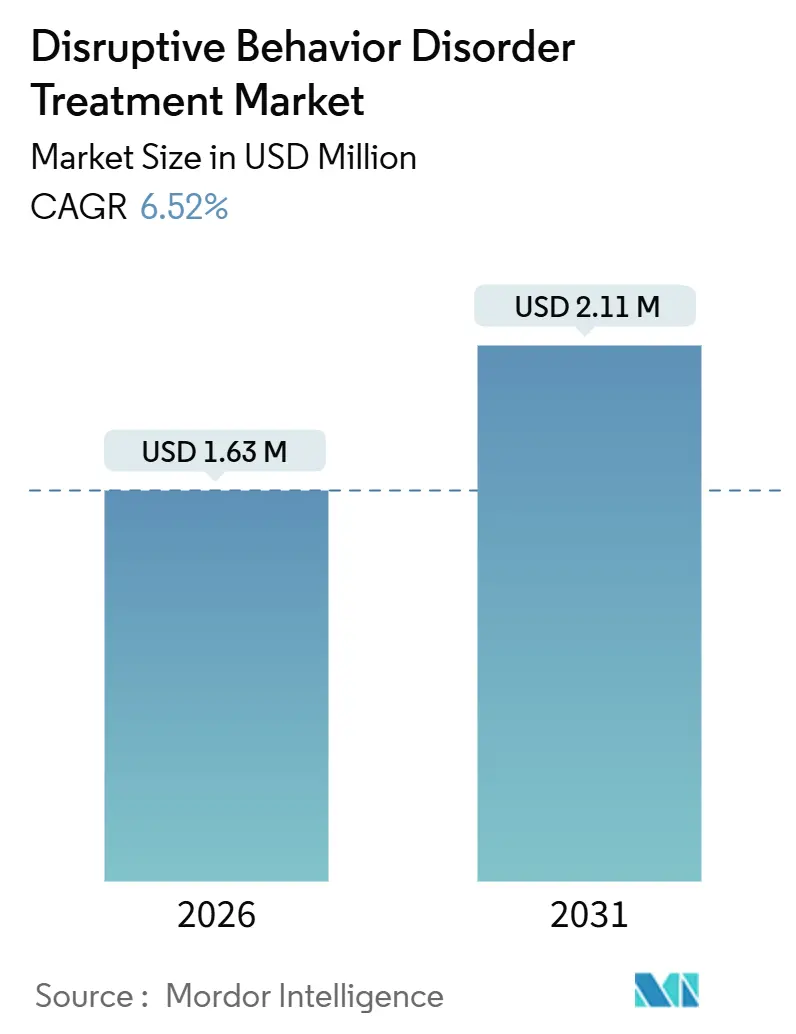

| Market Size (2026) | USD 1.63 Million |

| Market Size (2031) | USD 2.11 Million |

| Growth Rate (2026 - 2031) | 6.52% CAGR |

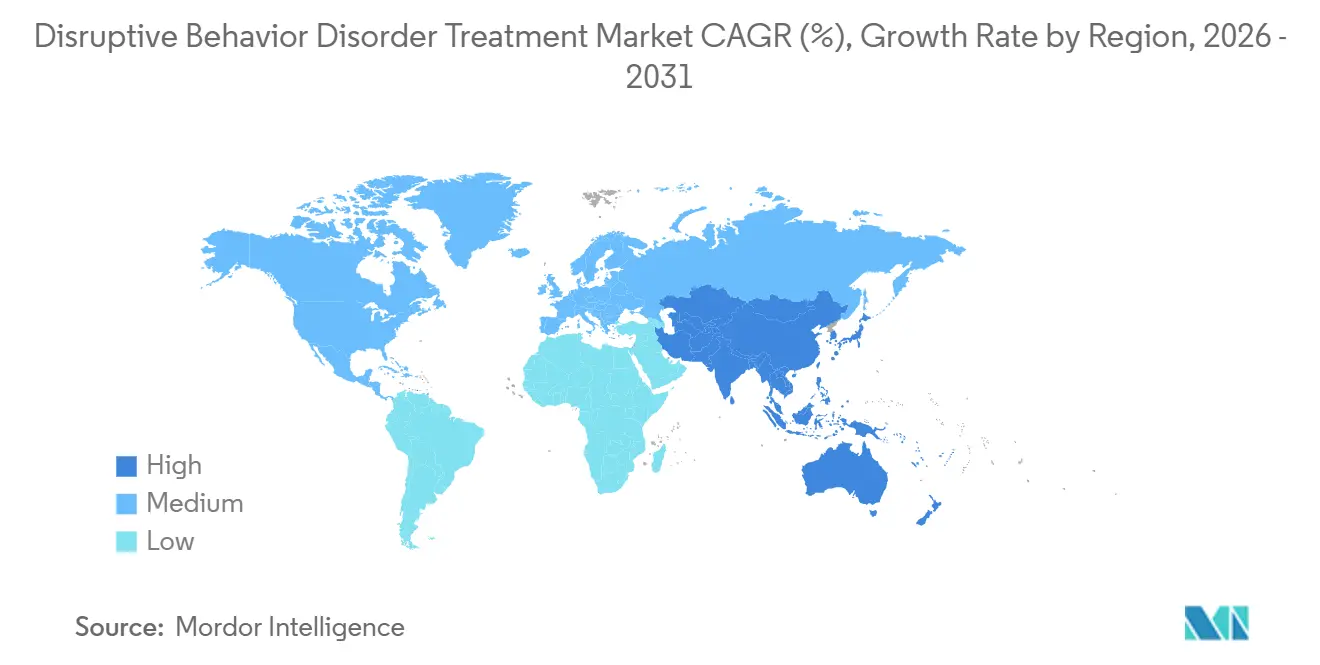

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

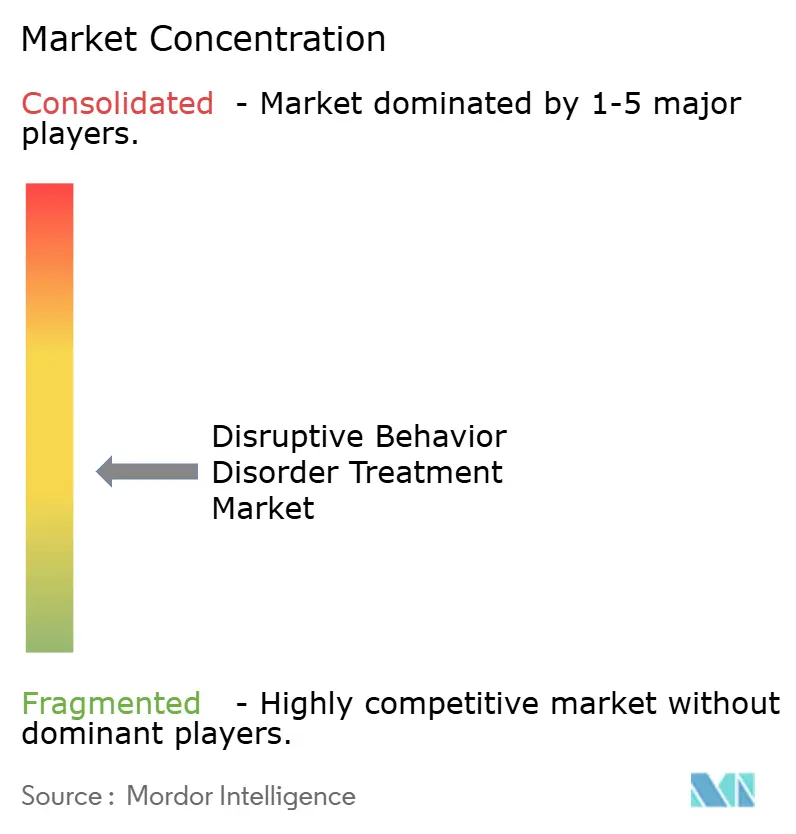

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Disruptive Behavior Disorder Treatment Market Analysis by Mordor Intelligence

The Disruptive Behavior Disorder Treatment Market size is estimated at USD 1.63 million in 2026, and is expected to reach USD 2.11 million by 2031, at a CAGR of 6.52% during the forecast period (2026-2031).

A confluence of early-intervention policy reforms, workforce innovations, and the integration of digital therapeutics is expanding the addressable patient pool. Health systems are leveraging collaborative-care models that embed child psychiatrists into primary-care practices, while schools implement evidence-based programs that normalize therapy within daily routines. Pharmaceutical pipelines continue to diversify beyond stimulant-based agents, targeting serotonergic and dopaminergic pathways linked to episodic aggression, and regulators are clearing prescription digital therapies that augment scarce clinical capacity. Meanwhile, venture investors are consolidating community providers, signaling confidence in hybrid treatment paradigms that combine medication, coaching apps, and family-based therapy. Together, these factors reinforce steady demand growth, even though absolute revenues remain modest compared with broader pediatric mental health segments.

Key Report Takeaways

- By disorder type, oppositional defiant disorder led with 44.56% of the disruptive behavior disorder treatment market share in 2025; intermittent explosive disorder is advancing at an 8.54% CAGR to 2031.

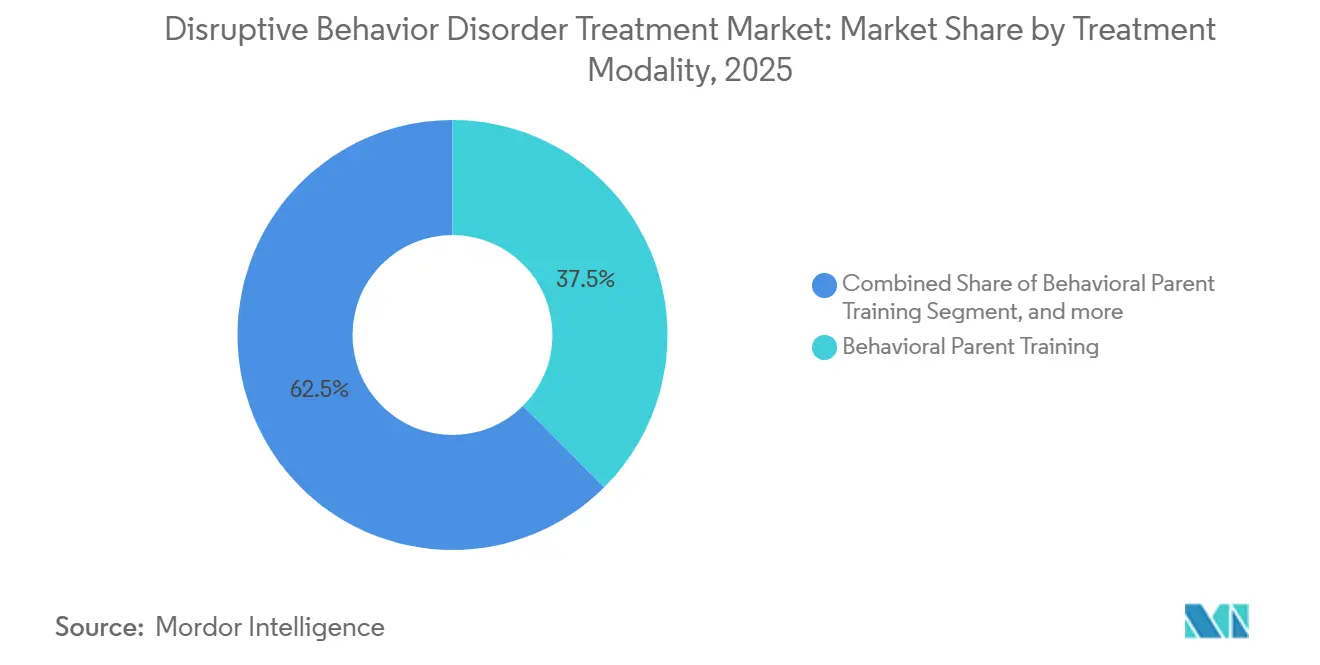

- By treatment modality, behavioral parent training accounted for 37.53% of the disruptive behavior disorder treatment market in 2025, while medication management is forecast to expand at an 8.99% CAGR through 2031.

- By geography, North America captured 42.76% of the disruptive behavior disorder treatment market share in 2025; Asia-Pacific is on track for a 7.54% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Disruptive Behavior Disorder Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Global Burden of Pediatric Mental Health Disorders | +1.8% | Global, with acute pressure in North America and Asia-Pacific | Medium term (2-4 years) |

| Policy Momentum Toward Mental-Health Parity and Early Intervention | +1.5% | North America and Europe, spillover to APAC | Short term (≤ 2 years) |

| Technological Advancements in Digital Therapeutics and Telepsychiatry | +1.2% | North America, Western Europe, urban APAC | Medium term (2-4 years) |

| Increasing Investments in Novel Non-Stimulant Pharmacotherapies | +0.9% | Global, led by North America and Europe | Long term (≥ 4 years) |

| Integration of Behavioral Health Services Within Primary Care Settings | +1.1% | North America, with early adoption in Canada and select EU markets | Short term (≤ 2 years) |

| Rising Adoption of Evidence-Based School and Community Treatment Models | +0.8% | Global, with strongest uptake in North America and Oceania | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating Global Burden of Pediatric Mental-Health Disorders

UNICEF’s 2024 report showed 1 in 7 boys and 1 in 9 girls aged 10-19 in East Asia and the Pacific living with mental-health conditions, compelling governments to widen screening programs. Conduct disorder ranked as a top cause of disability-adjusted life years for children under 15 in multiple Asian countries, thereby highlighting the economic payoff of early treatment. Nepal’s 2025 national survey found that 5.2% of adolescents exhibited behavioral difficulties, spurring school-based pilots that shorten referral pathways. Malaysia’s 2024 data echoed this trend, with 15.9% of children screening positive but facing care gaps due to workforce shortages. Collectively, these findings are expanding the disruptive behavior disorder treatment market by increasing diagnosis rates and prompting donor-funded capacity ramps.

Policy Momentum Toward Mental-Health Parity and Early Intervention

The U.S. EARLY Minds Act (2025) broadens Medicaid reimbursement for infant mental-health screenings, compressing the window between symptom onset and therapy initiation. HHS parity rules finalized in 2024 compel insurers to remove non-quantitative treatment limits, curbing prior-authorization delays for multimodal care. Illinois’ 2024 legislation mandates social-emotional curricula and formal referral pathways, stimulating demand for school-based parent-training programs. HRSA, however, projects a 30% deficit of child psychiatrists by 2030, meaning utilization gains will intensify pressure on already constrained provider networks[1]HRSA, “Pediatric Mental Health Care Access Program 2024 Report,” hrsa.gov. Europe follows a similar arc, with the EU funding school health initiatives that dovetail with existing universal coverage systems.

Technological Advancements in Digital Therapeutics and Telepsychiatry

FDA’s June 2024 510(k) clearance for an over-the-counter digital ADHD treatment signaled regulator openness to software-as-therapy models. A September 2024 device-classification rule then carved a pathway for prescription digital therapies, prompting developers to pursue disruptive-behavior indications under analogous codes. American Academy of Pediatrics data show that 40% of pediatric behavioral visits remained virtual in 2024, reflecting durable post-pandemic telehealth adoption. SAMHSA guidance endorses integration of measurement-based apps into community mental-health centers, helping providers track aggression and parent-child interaction metrics remotely. Nonetheless, interstate licensing and uneven reimbursement continue to temper telepsychiatry scale.

Increasing Investments in Novel Non-Stimulant Pharmacotherapies

Viloxazine extended-release posted favorable two-year data in August 2025, reinforcing confidence in non-stimulant pathways that also modulate impulsive aggression. WHO’s proposal to add methylphenidate to the Essential Medicines List for ages 6-17 is poised to lower procurement costs in low-income markets, indirectly boosting multimodal-therapy uptake. NIMH’s September 2025 call for adult ADHD non-stimulant trials widens the evidence base for agents with crossover utility in intermittent explosive disorder. Yet black-box warnings on atypical antipsychotics sustain physician caution, especially in primary-care settings where metabolic monitoring is limited. Venture funding is therefore steering toward agents with benign side-effect profiles and once-daily dosing.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic Shortage of Specialized Child Mental-Health Workforce | -1.3% | Global, most acute in North America & rural regions | Medium term (2-4 years) |

| High Cost and Limited Reimbursement for Long-Term Multimodal Care | -1.0% | North America & Europe, spillover to emerging markets | Short term (≤ 2 years) |

| Safety and Efficacy Concerns Surrounding Off-Label Pharmacologic Use | -0.9% | North America & Europe, rising scrutiny in Asia-Pacific | Medium term (2-4 years) |

| Persistent Social Stigma and Low Awareness in Emerging Economies | -0.8% | Asia-Pacific, Latin America, Middle East & Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Chronic Shortage of Specialized Child Mental-Health Workforce

HRSA forecasts a 30% shortfall of U.S. child psychiatrists by 2030, lengthening waitlists to 6-12 months in many regions. Only 7% of licensed psychologists concentrate on pediatric populations, according to 2024 APA data, creating geographic deserts without specialist access[2]APA, “2024 Psychology Workforce Report,” apa.org. Certification for Parent-Child Interaction Therapy demands 40-80 hours of supervision, and PCIT International reports multi-year waitlists that constrict program scale. Telepsychiatry bridges distance but cannot replace in-person coaching that requires observation of parent-child dynamics. These deficits collectively suppress throughput, tempering disruptive behavior disorder treatment market expansion despite strong latent demand.

High Cost and Limited Reimbursement for Long-Term Multimodal Care

Comprehensive protocols exceed USD 10,000 annually per child, a figure unattainable for families lacking robust insurance[3]CMS, “Collaborative Care Billing Codes Fact Sheet 2024,” cms.gov. While CMS broadened collaborative-care codes in 2024, many private insurers still impose session caps and stringent utilization management, fracturing continuity. Educationally classified parent-training programs often fall outside medical-billing frameworks, pushing families toward out-of-pocket or grant-funded slots that cannot meet demand. Parity rules adopted in 2024 require carrier compliance audits, yet enforcement lags, leaving persistent gaps in coverage. Consequently, cost barriers continue to restrain patient uptake in lower-income and under-insured populations across both developed and emerging markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Disorder Type: Diagnostic Refinement Fuels Intermittent Explosive Disorder Upswing

Intermittent explosive disorder therapies are projected to expand 8.54% annually through 2031, the fastest-growing slice of the disruptive behavior disorder treatment market, as improved screening separates episodic aggression from generalized defiance. Oppositional defiant disorder controlled 44.56% of the disruptive behavior disorder treatment market share in 2025, owing to earlier preschool-age diagnoses when tantrums disrupt home and classroom routines. Conduct disorder occupies a smaller share yet garners public-health focus because untreated cases escalate into antisocial trajectories that burden justice systems.

Growth for intermittent explosive disorder hinges on serotonergic and dopaminergic agents now progressing through Phase II pipelines, alongside cognitive-control training protocols embedded in mobile games. Oppositional defiant disorder management remains anchored in parent-training curricula, which, despite workforce bottlenecks, deliver durable gains in emotion regulation. Conduct disorder programs increasingly employ multisystemic therapy, blending family counseling with peer-group restructuring to curb recidivism into adult criminality. Collectively, these developments diversify therapeutic options but also spotlight the need for finely tuned reimbursement to match disorder severity.

By Treatment Modality: Medication Management Grabs Momentum

Behavioral parent training retained 37.53% of disruptive behavior disorder treatment market size in 2025, affirming its status as first-line care. Yet medication management is surging at an 8.99% CAGR to 2031, propelled by long-term viloxazine data and broader physician comfort with non-stimulant profiles. Family therapy, group sessions, and SEL-based skills programs fill psychosocial niches but struggle with reimbursement and therapist supply.

The medication upswing also mirrors payer appetites for scalable, protocolized treatments that fit within 15-minute consults, contrasting with labor-intensive parent-coaching series. Digital therapeutics now bundle coaching nudges with pharmacotherapy, forming hybrid models that compress clinician touchpoints. Insurers still cap behavioral-session counts, but value-based contracts pegged to reduced emergency-department visits indicate a nascent shift toward longer-term coverage of multimodal regimens. Workforce realities ensure that medication plus app-mediated support will remain a practical compromise in many settings.

Geography Analysis

North America commanded 42.76% of disruptive behavior disorder treatment market share in 2025, buoyed by HRSA grants that embed psychiatrists into 8,880 primary-care practices and serve 27,000 youths. Federal legislation, including the EARLY Minds Act, strengthens Medicaid reimbursement for infant screenings, while private philanthropy funds specialty inpatient beds, such as Boston Children’s 2025 Brighton campus. Canada pilots integrated-youth hubs that co-locate counseling, primary care, and substance-use services, mitigating fragmentation. Mexico expands school-screening rollouts through multilateral collaborations, though therapist shortages persist in rural states.

Asia-Pacific is forecast to rise at a 7.54% CAGR from 2026-2031, the fastest regional clip, driven by WHO’s Special Initiative that reached 72.3 million people by 2024 and funded community-treatment pilots across Nepal, Malaysia, and Indonesia. China and Japan bankroll AI-enabled telepsychiatry to offset urban-rural disparities, while Australia’s state health services integrate digital-coaching apps into juvenile-justice diversion programs. Regulatory frameworks for prescription software remain formative, yet market players anticipate analogs to U.S. FDA guidance within five years, setting the stage for rapid scale once policies crystallize.

Europe emphasizes psychosocial over pharmacologic care, with the U.K.’s NHS prioritizing parent-training curricula delivered in school or community settings. Germany and Italy expand SEL lessons via EU social-fund grants, boosting early identification. The Middle East and Africa confront more acute workforce gaps, but Gulf Cooperation Council states invest in tertiary pediatric psychiatry wings staffed by expatriate clinicians. South America leverages national telehealth portals; Argentina’s 24/7 hotline launched in 2024 now funnels callers into regional CBT or family-therapy cohorts, though reimbursement parity is still emerging.

Competitive Landscape

The disruptive behavior disorder treatment market remains fragmented, with no single actor exceeding 5% global revenue. Academic hospitals such as Boston Children’s, Seattle Children’s, and NYU Langone undertake capacity expansions, using philanthropy and state capital to underwrite 100+ new beds since 2024. Pharmaceutical majors—including Eli Lilly, Pfizer, and Johnson & Johnson—continue repurposing ADHD and antipsychotic assets but encounter off-label safety scrutiny that curtails pediatric uptake. Digital-therapeutics firms like Akili Interactive pivot from ADHD into intermittent explosive disorder, leveraging FDA’s device-classification rule to expedite 510(k) pathways.

Investor appetite remains robust; Q1 2024 saw 42 private-equity deals worth USD 350 million targeting pediatric behavioral-health roll-ups. These aggregators aim to stitch together outpatient clinics, telepsychiatry units, and school-based contractors into regional networks that are attractive to Medicaid managed-care plans. Meanwhile, midsize entrants such as Triplemoon test AI-driven parent-coaching platforms that personalize modules based on real-time emotion-recognition data. Hospitals partner with tech vendors to deploy such tools; Texas Children’s 2024 alliance with The Menninger Clinic exemplifies integrated units that embed digital monitoring from admission onward. Overall, competitive intensity centers on securing payer contracts that reward measurable functional gains rather than fee-for-service volumes.

Disruptive Behavior Disorder Treatment Industry Leaders

Eli Lilly & Co.

Pfizer Inc.

Johnson & Johnson Services Inc.

Boston Children’s Hospital

Neuphoria Therapeutics Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Johnson & Johnson submitted a supplemental New Drug Application (sNDA) to the U.S. Food and Drug Administration (FDA) based upon long-term data evaluating the safety and efficacy of CAPLYTA (lumateperone) for the prevention of relapse in schizophrenia. CAPLYTA is the newest addition to Johnson & Johnson’s portfolio of schizophrenia therapies, which now offers the broadest range of oral and long-acting injectable treatment options to support each patient’s individual treatment journey.

- June 2024: FDA granted 510(k) clearance to EndeavorOTC, the first OTC digital ADHD therapy, setting precedent for similar digital tools

Global Disruptive Behavior Disorder Treatment Market Report Scope

As per scope of the report, disruptive behavior disorder treatment involves therapeutic strategies to manage and reduce challenging behaviors such as aggression, defiance, and temper outbursts in children and adolescents. It typically includes behavioral therapy, parent training, and sometimes medication. The goal is to improve social functioning and emotional regulation.

The Disruptive Behavior Disorder Treatment Market Report is Segmented by Disorder Type (Oppositional Defiant Disorder, Conduct Disorder, and Intermittent Explosive Disorder), Treatment Modality (Medication Management, Behavioral Parent Training, Family Therapy, Group Therapy, Individual CBT, and Social & Emotional Skills Training), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Oppositional Defiant Disorder |

| Conduct Disorder |

| Intermittent Explosive Disorder |

| Medication Management |

| Behavioral Parent Training |

| Family Therapy |

| Group Therapy |

| Individual CBT |

| Social & Emotional Skills Training |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest Of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest Of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest Of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest Of South America |

| By Disorder Type | Oppositional Defiant Disorder | |

| Conduct Disorder | ||

| Intermittent Explosive Disorder | ||

| By Treatment Modality | Medication Management | |

| Behavioral Parent Training | ||

| Family Therapy | ||

| Group Therapy | ||

| Individual CBT | ||

| Social & Emotional Skills Training | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest Of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest Of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest Of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest Of South America | ||

Key Questions Answered in the Report

How large will the disruptive behavior disorder treatment market become by 2031?

Forecasts point to USD 2.11 million in global revenues, reflecting a 6.52% compound annual growth rate.

Which disorder subtype shows the strongest growth momentum?

Intermittent explosive disorder therapies are projected to expand 8.54% annually through 2031, outpacing oppositional defiant and conduct disorders.

What are the main factors fueling demand?

Early-intervention legislation, digital?therapeutics adoption, and expanding non-stimulant drug pipelines are simultaneously widening diagnosis rates and easing care access.

Which geographic region is expanding the quickest?

Asia-Pacific is set to grow at a 7.54% CAGR from 2026Ð2031, driven by school-based screening programs and multilateral public-health initiatives.

Why are medication-based interventions gaining share?

Long-term viloxazine data and therapist shortages are steering clinicians toward pharmacotherapy blended with parent-coaching apps and brief telehealth check-ins, lifting medication management to an 8.99% CAGR.

How fragmented is the provider landscape?

The top five hospital and digital-therapy operators control roughly 12% of global revenue, indicating a low market concentration score of 4 and ample room for new entrants.

Page last updated on: