Bleeding Disorder Testing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

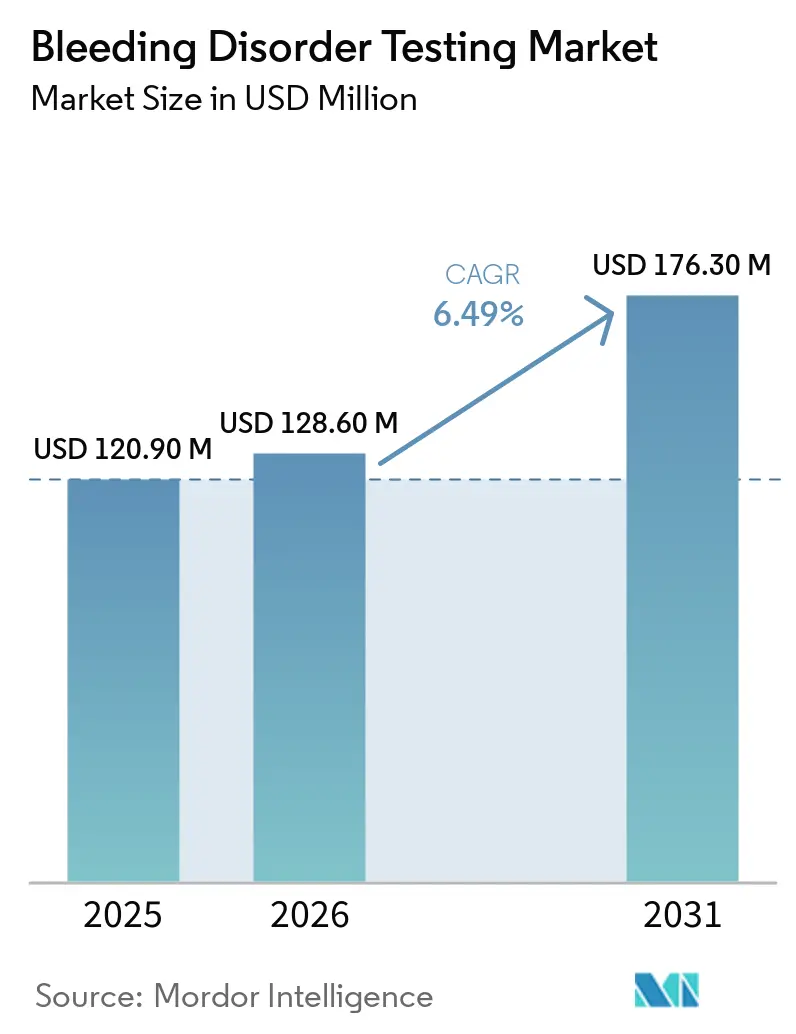

| Market Size (2026) | USD 128.60 Million |

| Market Size (2031) | USD 176.30 Million |

| Growth Rate (2026 - 2031) | 6.49% CAGR |

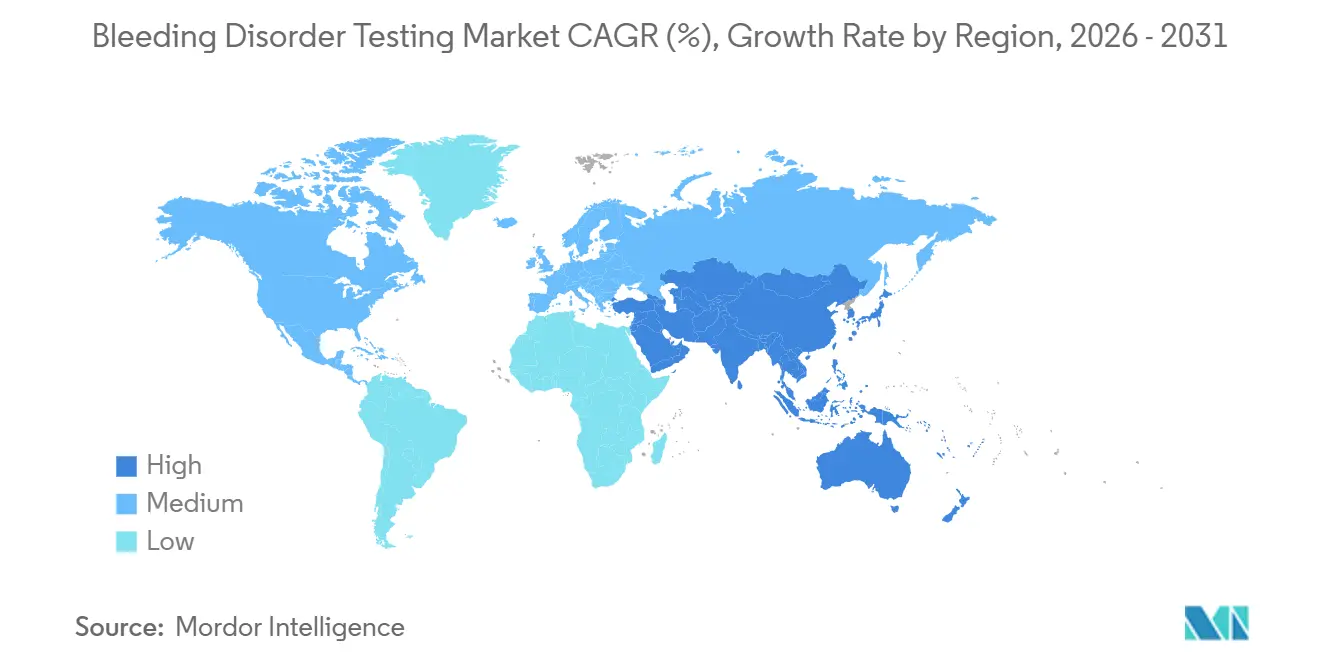

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bleeding Disorder Testing Market Analysis by Mordor Intelligence

The Bleeding Disorder Testing Market size is expected to increase from USD 120.90 million in 2025 to USD 128.60 million in 2026 and reach USD 176.30 million by 2031, growing at a CAGR of 6.49% over 2026-2031.

Steady test-volume growth stems from guideline-mandated quality programs, rapid automation, and continued uptake of emicizumab-compatible chromogenic Factor VIII assays, each of which drives reagent refresh cycles. Asia-Pacific laboratories are expanding installed bases to diagnose the 75% of hemophilia cases that remain undocumented, pushing equipment demand beyond simple replacement in mature regions. Molecular panels that deliver 74% diagnostic yields in three weeks shorten the diagnostic odyssey and stimulate earlier prophylaxis, while single-use cartridges mitigate cross-contamination in high-throughput sites. Vendors embed pre-analytical integrity checks to curb the 46%–68.2% error rate linked to citrate underfilling, hemolysis, and temperature excursions.

Key Report Takeaways

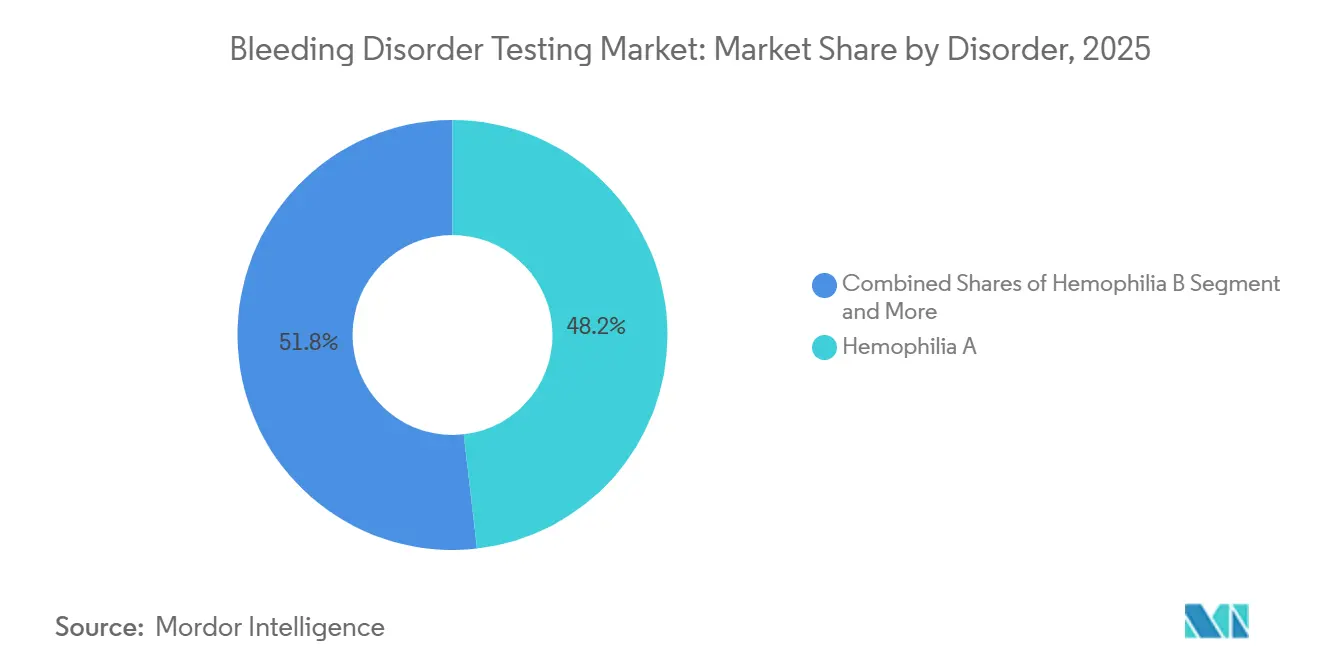

- By disorder, Hemophilia A held 48.19% of the bleeding disorder testing market share in 2025, while Von Willebrand Disease is advancing at a 7.98% CAGR through 2031.

- By technology, coagulation assays accounted for 42.16% of revenue in 2025; molecular diagnostics is poised to expand at an 8.35% CAGR to 2031.

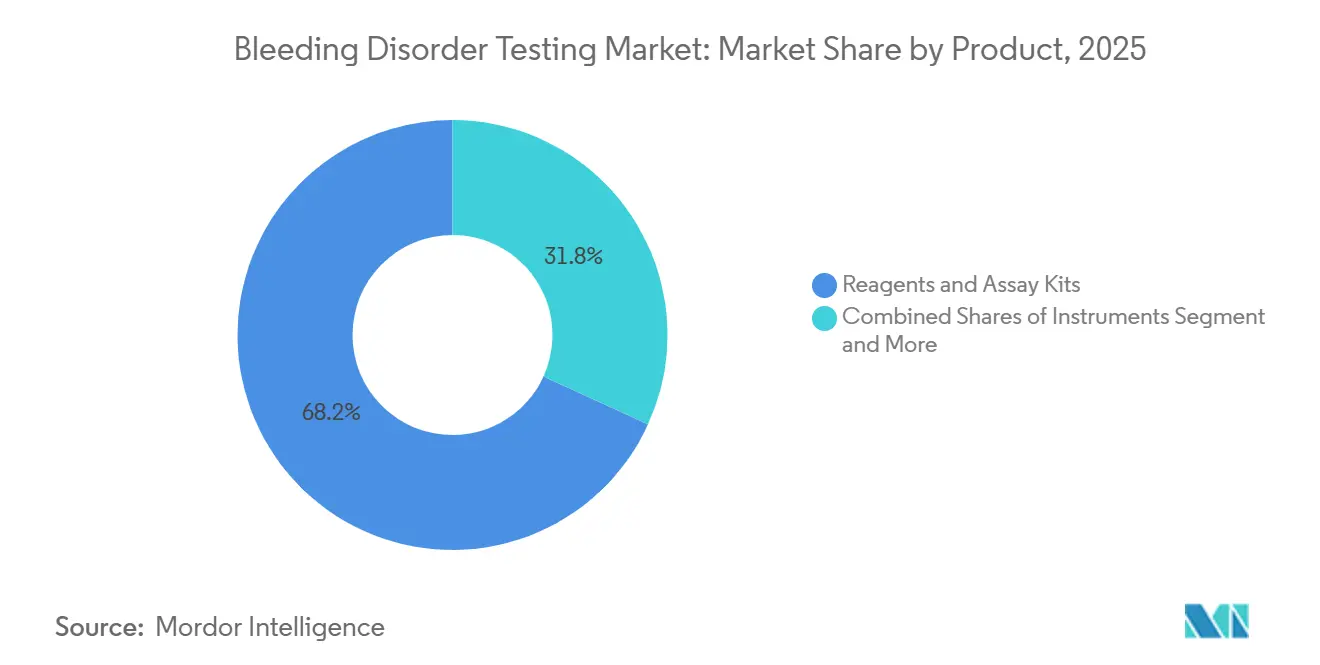

- By product, reagents and assay kits captured 68.19% of the bleeding disorder testing market size in 2025 and continue as the fastest segment at an 8.43% CAGR.

- By end user, hospitals commanded 43.18% of revenue in 2025, whereas hemophilia treatment centers recorded the highest projected 8.68% CAGR to 2031.

- By geography, North America led with 39.17% share in 2025, but Asia-Pacific is forecast to climb at an 8.33% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Bleeding Disorder Testing Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Guideline-mandated testing and QA programs | +1.2% | Global, strongest in North America & EU | Medium term (2–4 years) |

| Shift to automation and integrated platforms | +1.5% | North America, EU, APAC tier-1 cities | Short term (≤ 2 years) |

| Point-of-care PT/INR and near-patient tests | +0.9% | North America, EU, APAC urban centers | Medium term (2–4 years) |

| Asia-Pacific diagnostic capacity build-out | +1.8% | Core APAC with MEA spill-over | Long term (≥ 4 years) |

| Emicizumab-driven shift to chromogenic FVIII | +0.7% | Global, initial focus on North America & the EU | Short term (≤ 2 years) |

| GPIb-based modernization of VWD testing | +0.4% | North America, EU, selected APAC markets | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Guideline-Mandated Testing Adoption and Quality Assurance Programs

Global societies updated laboratory manuals in 2025, requiring chromogenic assays for emicizumab-treated patients and standardized inhibitor screening intervals[1]World Federation of Hemophilia, “Laboratory Diagnosis Manual, 3rd Edition,” wfh.org. European laboratories responded to the British Society for Hematology’s 2024 Von Willebrand guidance by switching to GPIbM or GPIbR assays, triggering reagent reformulation. Laboratories enrolling in external quality schemes now link compliance directly to reimbursement eligibility, pushing adoption of traceable calibration and ISO 15189 accreditation. Embedded pre-analytical checks lower repeat collection by 40% and shrink medicolegal exposure in gene-therapy monitoring. As harmonized protocols spread, inter-laboratory result portability improves, easing multicenter trial logistics.

Shift to Automation and Integrated Coagulation Platforms

High-volume sites deploy workcells that integrate barcode verification, centrifugation, and data management, cutting manual touchpoints by 70% and enabling overnight lights-out runs[2]Diagnostica Stago, “STA Workcell Max,” stago.com. Newly launched analyzers consolidate hemostasis, chemistry, and immunoassay results on one dashboard, trimming emergency-department turnaround times by 30%. RFID reagent tracking eliminates transcription errors and reduces expired inventory. Return on investment arrives within 18 months for labs processing more than 200 hemostasis samples daily, largely through labor savings and decreased waste. Automation also standardizes specimen handling and boosts proficiency-test performance.

Expansion of Point-of-Care PT/INR Self-Testing and Near-Patient Hemostasis

Connected handheld meters send INR data by Bluetooth to clinics, shrinking time-in-therapeutic-range variability by 15% against monthly central-lab visits. Whole-blood cartridges deliver 3-minute PT/INR results at bedside, expediting warfarin adjustments after cardiac surgery. Low-cost inhibitor and emicizumab kits priced under USD 2 widen rural access in India. Although U.S. reimbursement favors facility-based over home testing, European payers already reimburse self-testing at parity, supporting broader uptake.

Asia-Pacific Diagnostic Capacity Build-Out and Installed-Base Expansion

Prevalence data show hemophilia recognition rising across Asia as registries mature, signaling latent diagnostic demand. Foundation grants are outfitting 40 new Indian district hemophilia centers with analyzers and skilled technologists, cutting patient travel time by 60%. China’s 2025 guidelines mandate inhibitor surveillance, unveiling a 6,000-patient testing gap equaling nearly USD 3 million in reagent sales. Lower-priced domestic analyzers capture tier-2 hospital demand, and humanitarian factor donations create ongoing quarterly monitoring needs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Inter-lab assay variability and lack of harmony | −0.8% | Global, acute in North America & EU | Medium term (2–4 years) |

| Pre-analytical errors in specimen handling | −0.5% | Global, higher in APAC & MEA | Short term (≤ 2 years) |

| Limited FDA clearance for GPIb VWD assays | −0.3% | North America | Medium term (2–4 years) |

| High costs and reimbursement friction | −0.6% | North America, EU, select APAC markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Inter-Lab Assay Variability and Lack of Harmonization Across Methods

Proficiency testing in 2024 showed Factor VIII results swinging by ≥30% among labs using identical plasma because of reagent lot drift and differing optical paths[3]European Federation of Clinical Chemistry and Laboratory Medicine, “Pre-Analytical Errors Study,” degruyter.com. Such noise can force unnecessary dose escalations, adding USD 50,000 per patient annually. Von Willebrand testing is even more discordant; mixed methodologies delay diagnosis an extra 14 months in 18% of Type 2 cases. Central-lab mandates in clinical trials add up to USD 0.5 million in cold-chain logistics, prompting vendors to develop locked-cartridge systems that raise reagent costs by 30% but cap calibration variance.

Pre-Analytical Errors and Specimen Handling Constraints

Nearly two-thirds of laboratory mistakes arise before analysis, predominantly from incorrect citrate ratios and delayed centrifugation. A 10% citrate deviation alters partial thromboplastin time by 15%, leading to false-positive lupus anticoagulant findings. Room-temperature delays degrade Factor VIII and VWF by 20% in four hours, yet 35% of Indian district samples exceeded this window in a 2024 audit. Hemolysis in 8% of emergency samples masks bleeding disorders until sentinel events occur. Upgraded analyzers flag compromised tubes automatically, but added capital costs slow deployment in price-sensitive regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Disorder: Emicizumab Reshapes Hemophilia A Testing

Hemophilia A generated 48.19% of 2025 revenue as the bleeding disorder testing market transitioned from niche inhibitor monitoring to broad prophylaxis surveillance, swelling the testable population to 40,000 patients worldwide. Von Willebrand Disease represents the fastest-growing disorder, advancing at a 7.98% CAGR as GPIb activity assays expose underdiagnosed Type 2 variants. The bleeding disorder testing market size for Hemophilia B rises with RNA-interference therapy approvals that mandate quarterly Factor IX and antithrombin checks. Molecular panels now identify causal mutations in 74% of rare factor deficiencies, shifting diagnosis from phenotype to genotype.

Gene-therapy adoption alters lifetime testing cadence: monthly Factor VIII/IX levels for three months, then quarterly, replacing episodic inhibitor screens. Intensified monitoring underpins the projected growth of hemophilia treatment centers, which deliver rapid turnaround and clinical oversight that decentralized labs struggle to match. Widening newborn screening further lifts baseline volumes.

By Technology: Chromogenic Substrates Displace One-Stage Clotting

Coagulation assays held 42.16% of 2025 revenue, anchored by activated partial thromboplastin time and prothrombin time screens. Yet chromogenic Factor VIII methods are overtaking one-stage tests as emicizumab adoption spreads. Molecular diagnostics is the fastest technology segment, climbing 8.35% annually as next-generation sequencing panels shrink turnaround from eight weeks to three. Point-of-care coagulometers capture a modest share by enabling bedside dose titration, though reimbursement gaps limit U.S. uptake.

Head-to-head trials show comparable precision between premium analyzers, with incremental gains tied to visual defect sensors that flag hemolysis earlier. The bleeding disorder testing market size for molecular platforms is forecast to widen as nationwide genomic initiatives subsidize hereditary-disease panels. Closed-system reagent cartridges reinforce manufacturer lock-in, elevating consumable-to-instrument revenue ratios.

By Product: Single-Use Cartridges Drive Reagent Growth

Reagents and assay kits supplied 68.19% of 2025 revenue and will keep leading at an 8.43% CAGR as single-use chromogenic cartridges dominate. These sealed vials eliminate contamination risk and extend shelf life to 60 days, reducing wastage in low-volume centers. Instruments make up a notable share of spend, with lifecycles stretching to 10 years thanks to modular middleware upgrades. Software and connectivity held a modest portion of sales, becoming mandatory for registry participation and remote QC.

RFID tracking cuts reagent loss in reference labs, while cloud dashboards merge hemostasis, chemistry, and immunoassay results, shaving off emergency turnaround. The bleeding disorder testing market share of reagents will stay elevated as gene-therapy pathways require high-frequency chromogenic monitoring.

By End User: Gene Therapy Propels HTC Growth

Hospitals accounted for 43.18% of 2025 revenue through perioperative and emergency testing. Independent laboratories captured a significant share, leveraging scale to lower unit costs, but face competition from three-minute point-of-care devices. Hemophilia treatment centers are set to register the quickest 8.68% CAGR because gene-therapy protocols demand specialized oversight and same-day Factor assays.

India’s district-level HTC expansion, funded through 2026, shows how decentralized care cuts travel times and boosts compliance. Outsourcing trends shift routine screens away from hospital cores, allowing facilities to focus on stat orders. The bleeding disorder testing market size, as realized by point-of-care and home monitoring, will rise steadily but remains constrained by reimbursement differentials.

Geography Analysis

Asia-Pacific is the fastest region, projected at an 8.33% CAGR, as the prevalence recognition of hemophilia shifts from 2.57 per 100,000 in 2023 toward 3.12 by 2030, revealing a diagnostic backlog. Government guidelines mandating inhibitor screens, plus affordable domestic analyzers, accelerate market penetration in China and India. Humanitarian factor donations translate into recurring quarterly Factor VIII/IX trough tests, deepening consumable demand.

North America commanded 39.17% revenue in 2025, buoyed by USD 45 Medicare reimbursement per VWF activity assay and a high density of gene-therapy trials that require chromogenic monitoring. Nonetheless, prior authorizations delay testing up to 10 days and elongate dose-adjustment cycles. Europe held a significant share, guided by 2024 VWF recommendations that spurred GPIb reagent adoption, although Brexit extended supply lead times to six weeks and forced 90-day inventory buffers.

Middle East & Africa and South America represented notable shares, with growth clustered in urban HTCs that partner with global training hubs in Japan and Australia. The bleeding disorder testing market share across emerging regions will climb as newborn screening and registry reporting become routine public-health mandates.

Competitive Landscape

The bleeding disorder testing market features moderate fragmentation. Siemens Healthineers, Sysmex, Werfen, and Diagnostica Stago lead the instrument tier, while regional specialists dominate reagents and point-of-care niches. Sysmex booked USD 550 million in hemostasis sales for fiscal 2025 after shifting to direct distribution in Europe and the Americas, lifting margins. Werfen’s EUR 2.2 billion 2024 revenue included the ACL TOP 70 launch and the acquisition of Omixon for transplant diagnostics diversification. Diagnostica Stago, newly acquired by ARCHIMED for an estimated USD 1.3 billion, will channel funds into STA Workcell Max rollouts across Asia-Pacific.

Decentralized testing is the prime white space. Mindray and HORIBA supply analyzers priced below Western units, winning a notable portion of China’s tier-2 installations in 2025 by promising same-day service and native interfaces. Competitive differentiation is shifting to middleware; Siemens’ Atellica Data Manager unifies multispecialty results, cutting emergency turnaround and raising clinician satisfaction. Roche secured a 20-year U.S. patent on a Bluetooth-enabled INR meter with dose-recommendation algorithms, hardening its moat in connected self-testing.

Bleeding Disorder Testing Industry Leaders

Siemens Healthineers

Sysmex Corporation

WerfenLife, SA

Shenzhen Mindray Bio-Medical Electronics Co., Ltd.

Diagnostica Stago

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: AddLife acquired CoaChrom Diagnostica for EUR 10 million, adding chromogenic substrates and 200 reference-lab customers.

- April 2026: ARCHIMED Diagnostics acquired a majority stake in Stago Group, a global player in blood coagulation analysis. Stago continues operating under its current brand and management, utilizing the investment to accelerate growth in the hemostasis sector.

- February 2026: FDA cleared ConcizuTrace ELISA as a companion diagnostic for concizumab therapy.

Global Bleeding Disorder Testing Market Report Scope

As per the scope of the report, bleeding disorder testing refers to a series of laboratory tests conducted to evaluate the blood's ability to clot properly. These tests help identify underlying bleeding disorders, such as hemophilia, von Willebrand disease, or platelet function disorders.

The bleeding disorder testing market is segmented by disorder, technology, product, end user, and geography. Based on disorder, the market is segmented into Hemophilia A, Hemophilia B, Von Willebrand disease (Type 1/2A/2B/2M/2N/3), and other bleeding disorders. By technology, the market is segmented into coagulation assays, molecular diagnostics, point-of-care coagulometers, and others. By product, the market is reagents & assay kits, instruments, and software & connectivity. By end users, the market is segmented into Hospitals, independent/clinical laboratories, hemophilia treatment centers, point-of-care/home monitoring, and research & academia. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Hemophilia A |

| Hemophilia B |

| Von Willebrand Disease (Type 1/2A/2B/2M/2N/3) |

| Other Bleeding Disorders |

| Coagulation Assays |

| Molecular Diagnostics |

| Point-of-care Coagulometers |

| Others |

| Reagents & assay kits |

| Instruments |

| Software & connectivity |

| Hospitals |

| Independent/clinical laboratories |

| Hemophilia treatment centers |

| Point-of-care/home monitoring |

| Research & academia |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Disorder (Indication) | Hemophilia A | |

| Hemophilia B | ||

| Von Willebrand Disease (Type 1/2A/2B/2M/2N/3) | ||

| Other Bleeding Disorders | ||

| By Technology | Coagulation Assays | |

| Molecular Diagnostics | ||

| Point-of-care Coagulometers | ||

| Others | ||

| By Product | Reagents & assay kits | |

| Instruments | ||

| Software & connectivity | ||

| By End User | Hospitals | |

| Independent/clinical laboratories | ||

| Hemophilia treatment centers | ||

| Point-of-care/home monitoring | ||

| Research & academia | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the bleeding disorder testing market in 2026?

The bleeding disorder testing market size at USD 128.6 million in 2026, on track for USD 176.3 million by 2031 at a 6.49% CAGR.

Which segment grows fastest between 2026 and 2031?

Molecular diagnostics leads technology growth at an 8.35% CAGR through 2031 as next-generation sequencing panels accelerate etiologic confirmation.

What region is expanding most rapidly?

Asia-Pacific posts the quickest 8.33% CAGR through 2031, driven by new hemophilia guidelines and expanded district-level treatment centers.

Why are hemophilia treatment centers outpacing hospitals in revenue growth?

Gene-therapy monitoring protocols require monthly then quarterly Factor VIII/IX checks, boosting test volumes at specialized centers to an 8.68% CAGR through 2031.

Page last updated on: