Attention Deficit Hyperactivity Disorder Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

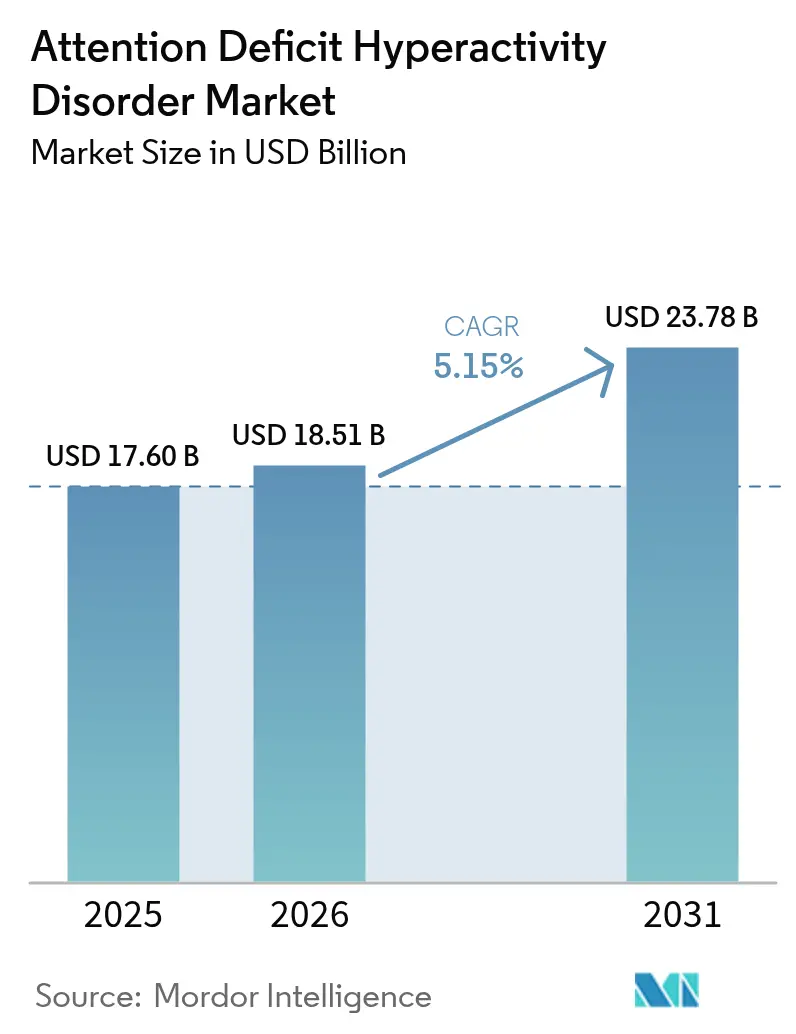

| Market Size (2026) | USD 18.51 Billion |

| Market Size (2031) | USD 23.78 Billion |

| Growth Rate (2026 - 2031) | 5.15% CAGR |

| Fastest Growing Market | North America |

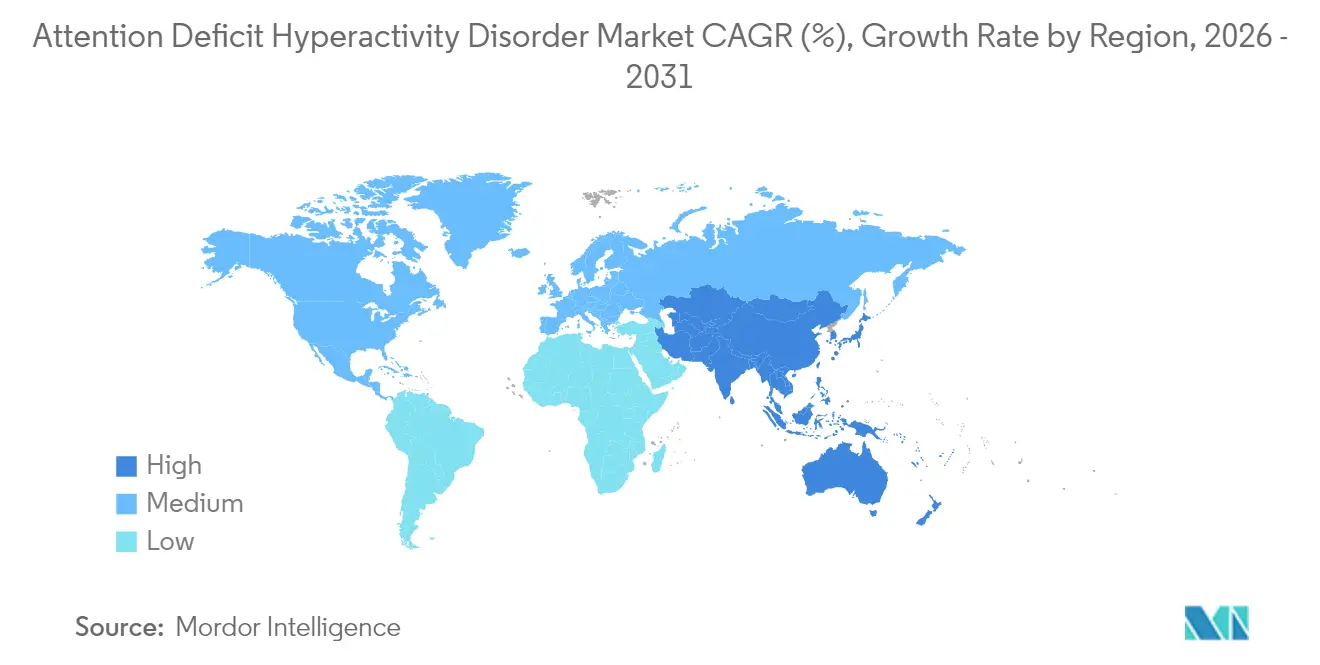

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Attention Deficit Hyperactivity Disorder Market Analysis by Mordor Intelligence

The attention deficit hyperactivity disorder market size was valued at USD 17.60 billion in 2025 and estimated to grow from USD 18.51 billion in 2026 to reach USD 23.78 billion by 2031, at a CAGR of 5.15% during the forecast period (2026-2031). Higher diagnostic vigilance, broader adult recognition, and steady innovation in both stimulant and non-stimulant regimens are expanding treatment volumes. Stimulants still anchor most prescriptions, yet non-stimulants gain momentum as physicians seek options with lower abuse potential. Telehealth services now link specialists to underserved communities, compressing wait times for evaluation and prescription fulfilment. North America holds a 42.45% revenue lead thanks to mature reimbursement systems, whereas Asia-Pacific posts the quickest regional climb at 6.54% CAGR, reflecting rising awareness and policy reform.

Key Report Takeaways

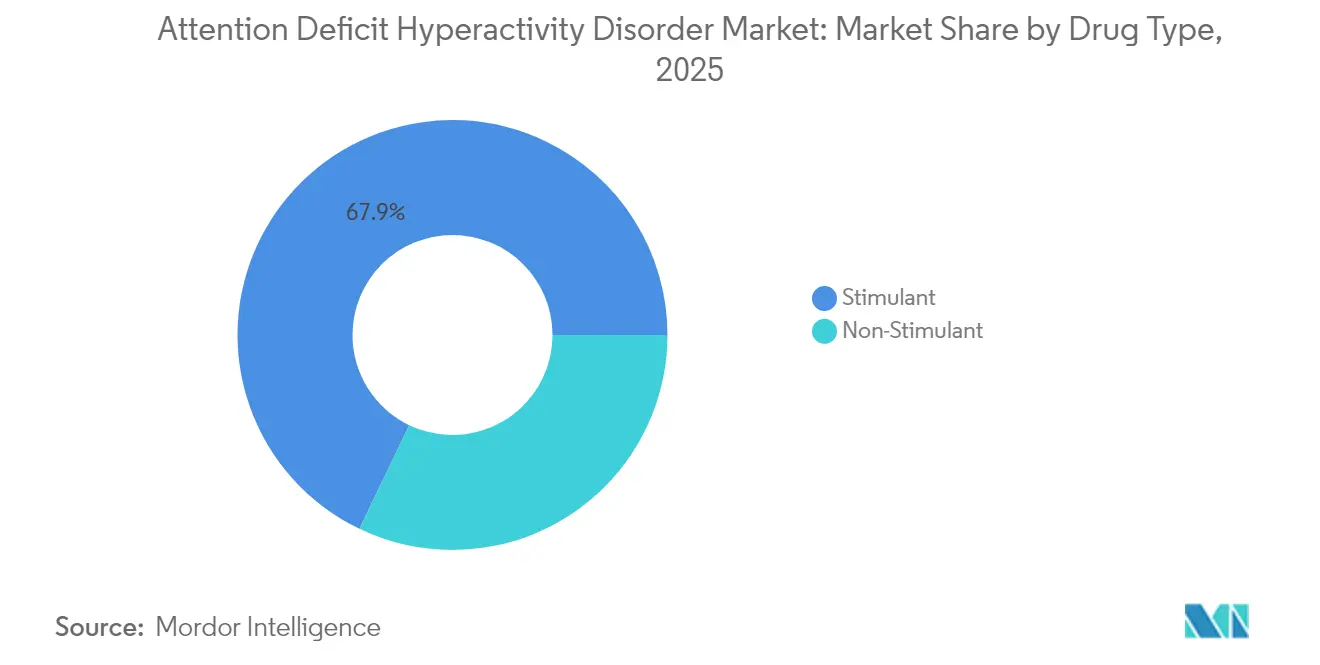

- By drug type, stimulants led with 67.88% of Attention Deficit Hyperactivity Disorder market share in 2025, while non-stimulants are projected to register a 7.32% CAGR to 2031.

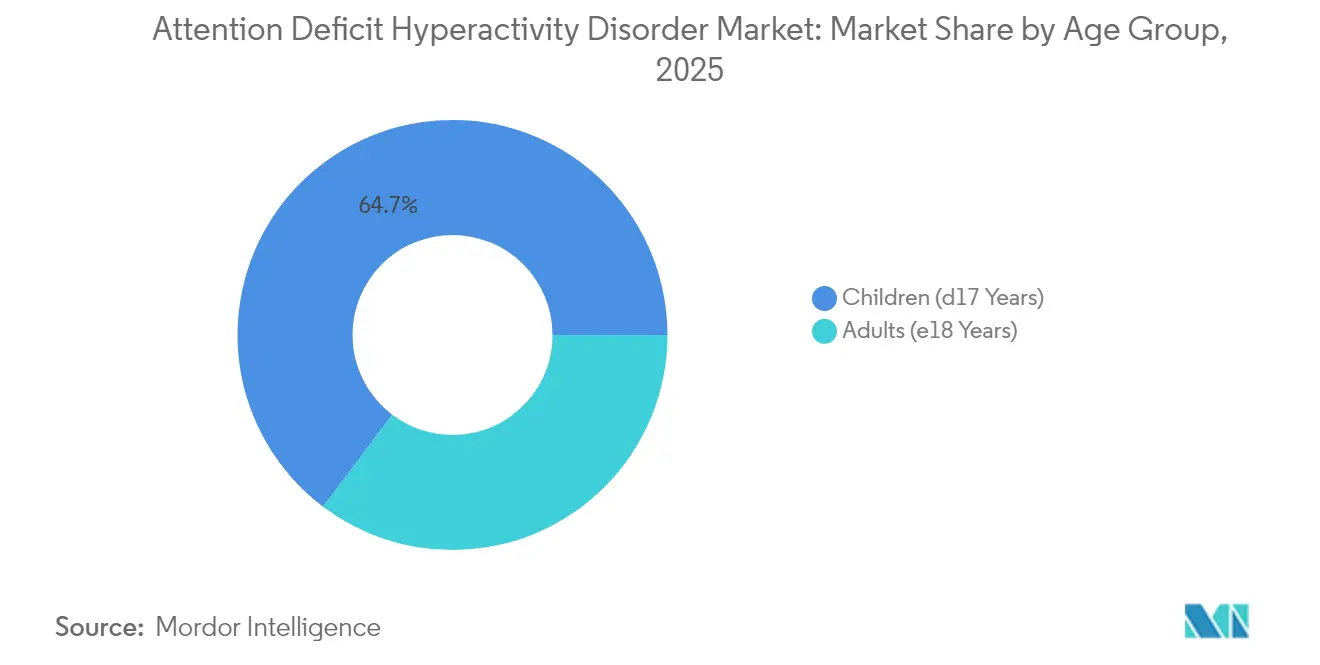

- By age group, the pediatric cohort captured 64.72% revenue in 2025; the adult segment is set to expand at an 8.09% CAGR through 2031.

- By distribution channel, retail pharmacies held 54.12% of the Attention Deficit Hyperactivity Disorder market size in 2025; online pharmacies are forecast to grow at an 8.48% CAGR to 2031.

- By region, North America accounted for 42.02% of 2025 revenue; Asia-Pacific is poised for the fastest 6.42% CAGR by 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Attention Deficit Hyperactivity Disorder Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising ADHD Prevalence Worldwide | +1.2% | Global, with highest impact in North America & Europe | Medium term (2-4 years) |

| Growing Awareness And Screening Initiatives | +0.8% | Global, particularly strong in Asia-Pacific | Short term (≤ 2 years) |

| Advancements In Pharmacotherapy And Formulations | +1.0% | North America & EU, expanding to APAC | Long term (≥ 4 years) |

| Supportive Reimbursement And Coverage Policies | +0.7% | North America & Europe | Medium term (2-4 years) |

| Expanding Adult Patient Segment Via Telehealth | +0.9% | Global, led by North America | Short term (≤ 2 years) |

| Integration Of Digital Therapeutics With Medication | +0.6% | North America & EU, early adoption in Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising ADHD Prevalence Worldwide

Global prevalence continues climbing: 12.0% of U.S. children aged 3-17 had an ADHD diagnosis in 2023, an uptick that stems from refined diagnostic criteria rather than sudden pathological change[1]Centers for Disease Control and Prevention, “ADHD Data and Statistics,” cdc.gov. Adult diagnoses pass 15.5 million in the United States, half confirmed after age 18, underscoring long-standing underrecognition. China’s school-age prevalence reached 6.4%, with modelling indicating a peak caseload in 2029, signalling sizeable latent demand in emerging economies. Climbing prevalence syncs with prescription volumes; U.S. stimulant scripts rose 57.9% from 2012-2022, sustaining demand across therapeutic classes.

Growing Awareness and Screening Initiatives

Primary-care clinicians increasingly deploy validated screeners, trimming referral delays. The American Professional Society for ADHD and Related Disorders is finalising the first U.S. adult guideline, closing a long-standing gap in standardised assessment pathways. Telehealth broadens access: 46% of diagnosed adults used virtual consultations in 2024 and 30.5% secured prescriptions online. Canadian claims data show a 20% jump in ADHD medication reimbursements during 2024, an indicator of accelerated recognition.

Advancements in Pharmacotherapy and Formulations

Innovation centres on adherence and safety. Tris Pharma earned FDA clearance for Onyda XR, the first liquid non-stimulant enabling bedtime dosing through LiquiXR technology. Cingulate’s CTx-1301 employs timed-release micro-beads to smooth coverage without afternoon boosters, with Phase 3 data supporting once-daily efficacy. Digital therapeutics mature in parallel; EndeavorRx achieved FDA approval for paediatric cognitive training, offering a non-pharmacologic option that sidesteps diversion risk. Axsome’s solriamfetol hit Phase 3 endpoints as the first dopamine-norepinephrine reuptake inhibitor tailored for ADHD.

Expanding Adult Patient Segment via Telehealth

Deferred diagnosis in adults now fuels incremental demand. Professional commitments and stigma formerly limited specialty visits, but synchronous video consults remove geographic and scheduling barriers. Adult women present the fastest-growing sub-segment after historical under-diagnosis, aided by guideline updates that recognise inattentive phenotypes. Tele-prescribing extensions through December 2025 allow controlled substance scripts without initial in-person visits, preserving treatment continuity while rules are finalised. Elevated adult volumes pressure payers to broaden coverage for combined pharmacologic-behavioural programs that mitigate workplace productivity loss.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Diagnostic Challenges And Underrecognition | -0.9% | Global, particularly acute in developing markets | Medium term (2-4 years) |

| High Abuse Liability And Safety Concerns Of Stimulants | -1.1% | Global, strongest impact in North America | Short term (≤ 2 years) |

| Strict Regulatory Controls On Controlled Substances | -0.8% | Global, most restrictive in North America & Europe | Medium term (2-4 years) |

| Cost Containment Pressures From Healthcare Payers | -0.7% | North America & Europe, emerging in APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Diagnostic Challenges and Underrecognition

Subjective symptom scoring and overlap with anxiety or mood disorders complicate clear-cut diagnosis. Absence of a biomarker forces clinicians to rely on multi-informant scales, generating both false negatives and false positives. Research on circulating micro-RNAs such as miR-140-3p advances but is years from routine use. Primary-care providers, especially in resource-limited settings, report low confidence in adult assessment, perpetuating unmet need. Cultural stigma further depresses help-seeking in Asia-Pacific, slowing attention deficit hyperactivity disorder market penetration despite public awareness drives.

High Abuse Liability and Safety Concerns of Stimulants

Federal quotas constrain output of amphetamine and methylphenidate products. DEA 2025 caps increased only marginally despite rising legitimate demand, perpetuating shortages[2]Source: U.S. Federal Register, “Controlled Substances Quotas for 2025,” federalregister.gov. Research from the University of Michigan associates tele-initiated stimulant therapy with higher incident substance-use disorder, intensifying scrutiny. Monthly visit mandates, PDMP checks, and exhaustive documentation erect hurdles that some clinicians avoid. The 2024-2025 Adderall shortfall forced millions into therapeutic switches, spotlighting vulnerabilities in a stimulant-dependent treatment paradigm.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Type: Non-Stimulants Gain Momentum Despite Stimulant Dominance

Stimulant products generated 67.88% of 2025 revenue, illustrating entrenched efficacy and prescriber familiarity. Yet non-stimulants logged a 7.32% CAGR, exceeding total attention deficit hyperactivity disorder market growth as safety-minded clinicians search for lower diversion risk. Lisdexamfetamine’s patent expiry in 2024 unlocked generic competition; Granules India and Lupin secured FDA approvals, supplying cost-sensitive buyers. DEA production caps pressured amphetamine supply, nudging prescribers toward alternatives such as viloxazine and guanfacine.

Supernus Pharmaceuticals reported Qelbree sales of USD 241.3 million in 2024, a 72% jump year-on-year, signalling robust uptake of novel non-stimulant mechanisms. Atomoxetine use remained steady despite batch recalls elsewhere, underlining persistent need for once-daily options. Liquid clonidine (Onyda XR) now offers paediatric caregivers a nocturnal regimen that circumvents school-time dosing hurdles. Consequently, the attention deficit hyperactivity disorder market size for non-stimulants is forecast to expand faster than any subcategory through 2031.

By Age Group: Adult Recognition Drives Expansion

Paediatric patients accounted for 64.72% of diagnoses in 2025, but adult cases are rising at an 8.09% CAGR. Many adults long mislabelled as “underachieving” now secure formal evaluations, buoyed by professional society guidelines and workplace accommodation policies. Japanese cohort work revealed mood-disorder comorbidity in 60.9% of affected adults, necessitating integrated care. Telehealth proves pivotal: 67.2% of virtual users procured ADHD medications online in 2024, an access vector especially valuable for rural communities.

The attention deficit hyperactivity disorder market size attributable to adult therapies is projected to eclipse USD 10.2 billion by 2031, propelled by format innovations such as CTx-1301 that address eight-hour workdays without midday boosters. Paediatric care is evolving too: behaviour first for under-6s, pharmacotherapy for school-age children when educational performance falters. The CDC counted 2 million untreated U.S. children with ADHD in 2022, highlighting residual opportunity. Holistic family-centred programs now pair parent training with medication, reinforcing adherence and academic gains.

By Distribution Channel: Digital Transformation Accelerates Online Growth

Retail chains remained the prime outlet with 54.12% market share, backed by insurance integration and pharmacist counselling. Still, online pharmacies post the quickest 8.48% CAGR, spurred by same-day delivery and easier shop-around during shortages. Integrated e-prescription systems now auto-route telehealth orders to mail-order fulfilment, shrinking friction. Hospital pharmacies uphold initiation for complex comorbid cases but hold a stable share given outpatient dominance of ADHD treatment.

Specialty pharmacies carve a niche for high-cost or liquid formulations requiring temperature control and adherence coaching. DEA proposals for in-person exams before remote refills loom as a wildcard that could temper online traction. Retail players retaliate by embedding screeners and nurse-led consults in-store, forging a hybrid model. Consequently, the attention deficit hyperactivity disorder market is likely to see blurred channel boundaries rather than a zero-sum shift.

Geography Analysis

North America, with 42.02% 2025 revenue, remains the anchoring geography. In 2023, U.S. pharmacies dispensed 45 million stimulant prescriptions, up from 35.5 million in 2019, indicating pervasive clinical adoption. Canada’s claim volumes climbed 20% in 2024 after provinces widened coverage, reinforcing access. Regional innovation depth is notable: most first-in-class approvals—Onyda XR, solriamfetol, CTx-1301—originated or were trialled here, underscoring a pipeline advantage.

Europe offers a structurally mature but controlled environment. Post-pandemic, prescription volumes ran 16.4% above pre-COVID forecasts by 2022, signalling greater societal comfort with pharmacologic care. The EMA’s green lights for Paxneury and Tuzulby added guanfacine and extended-release methylphenidate choices to paediatric algorithms. Germany spearheads digital therapeutics; EndeavorRx secured CE marking and a reimbursement code, accelerating adoption pathways.

Asia-Pacific delivers the fastest 6.42% CAGR, lifted by policy liberalisation and urbanising populations. Japan’s government-backed biotech incentives catalyse neuroscience start-ups, widening clinical trial capacity. China’s 6.4% paediatric prevalence equates to tens of millions of potential patients as screening scales nationally. India’s manufacturers leverage FDA approvals—such as generic Vyvanse—to supply lower-priced options globally, reinforcing regional affordability. Remaining hurdles include rural service gaps and persisting stigma, but rising digital literacy mitigates some obstacles, suggesting the attention deficit hyperactivity disorder market will experience steady diffusion across megacities first, then into secondary centres.

Competitive Landscape

Consolidation meets disruption. Takeda’s Vyvanse patent lapse prompted a USD 900 million restructuring after profit slid 57%, illustrating post-exclusivity pressure. Collegium’s USD 525 million buyout of Ironshore Therapeutics gave it Jornay PM, signalling diversification beyond pain franchises. Supernus’s viloxazine success proves that differentiated non-stimulants can flourish even in a stimulant-heavy arena.

Digital entrants reshape therapeutic hierarchies. EndeavorRx, cleared for paediatric use, obviates controlled-substance protocols and is now reimbursed by multiple U.S. payers. Cingulate’s timed-release approach targets adherence pain points unaddressed by incumbents. Supply volatility also creates openings; companies with robust manufacturing capacity or alternative mechanisms can capture prescriptions when quota-bound competitors run short. Net effect: the attention deficit hyperactivity disorder market exhibits moderate concentration, with roughly 60% of revenue held by the five leading firms, yet ongoing innovation keeps competitive intensity high.

Attention Deficit Hyperactivity Disorder Industry Leaders

Takeda Pharmaceutical Co.

Novartis AG

Johnson & Johnson (Janssen)

Eli Lilly & Co.

Pfizer Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Cingulate completed Phase 3 safety testing for CTx-1301 and scheduled an NDA submission for mid-2025.

- March 2025: Axsome Therapeutics’ solriamfetol met Phase 3 endpoints in adult ADHD, achieving a 45% mean symptom reduction.

- February 2025: Supernus Pharmaceuticals confirmed 72% Qelbree sales growth to USD 241.3 million for 2024, aided by a label update highlighting low breast-milk transfer.

- January 2025: Johnson & Johnson announced a USD 14.6 billion agreement to acquire Intra-Cellular Therapies, adding CAPLYTA to its neuroscience stable with future ADHD indications possible.

- January 2025: Granules India gained FDA clearance for generic lisdexamfetamine dimesylate, expanding its ADHD product range.

Global Attention Deficit Hyperactivity Disorder Market Report Scope

As per the scope of the report, Attention deficit hyperactivity disorder (ADHD) is one of the most common neurodevelopmental disorders that primarily affects children. ADHD is often diagnosed in childhood and persists into adulthood. Children with ADHD may daydream excessively, forget or lose things, have difficulty resisting temptation, have trouble taking turns, have difficulty getting along with others, be overly active, and have difficulty paying attention. The attention deficit hyperactivity disorder market is segmented by drug type (stimulant, non-stimulant), age (adult (aged 18 and above), children), distribution (retail pharmacy, hospital pharmacy), and geography (North America, Europe, Asia-Pacific, Middle-East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Stimulant | Amphetamine |

| Methylphenidate | |

| Dextroamphetamine | |

| Dexmethylphenidate | |

| Lisdexamfetamine Dimesylate | |

| Non-Stimulant | Atomoxetine |

| Bupropion | |

| Guanfacine | |

| Clonidine |

| Children (<17 Years) |

| Adults (>18 Years) |

| Retail Pharmacy |

| Hospital Pharmacy |

| Online Pharmacy |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Drug Type | Stimulant | Amphetamine |

| Methylphenidate | ||

| Dextroamphetamine | ||

| Dexmethylphenidate | ||

| Lisdexamfetamine Dimesylate | ||

| Non-Stimulant | Atomoxetine | |

| Bupropion | ||

| Guanfacine | ||

| Clonidine | ||

| By Age Group | Children (<17 Years) | |

| Adults (>18 Years) | ||

| By Distribution Channel | Retail Pharmacy | |

| Hospital Pharmacy | ||

| Online Pharmacy | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected size of the Attention Deficit Hyperactivity Disorder market by 2031?

The Attention Deficit Hyperactivity Disorder market is expected to reach USD 23.78 billion by 2031, expanding at a 5.15% CAGR.

Which drug class dominates current sales?

Stimulant medications held 67.88% of the Attention Deficit Hyperactivity Disorder market share in 2025, supported by long-standing efficacy data.

Why are non-stimulants gaining popularity?

Prescribers and patients seek alternatives with lower abuse risk, and new agents like viloxazine show strong efficacy and growth, posting a 7.32% CAGR forecast.

How fast is the adult segment growing?

Adult diagnoses are rising at an 8.09% CAGR as telehealth makes specialist evaluation more accessible and guidelines formalise adult screening.

Which region offers the highest growth potential?

Asia-Pacific leads with a 6.42% forecast CAGR thanks to improving awareness, favourable policy shifts, and expanding healthcare infrastructure.

How are digital therapeutics impacting treatment?

FDA-cleared platforms such as EndeavorRx provide non-pharmacologic options, alleviating supply constraints and safety concerns tied to controlled stimulants.

Page last updated on: