On Call Scheduling Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

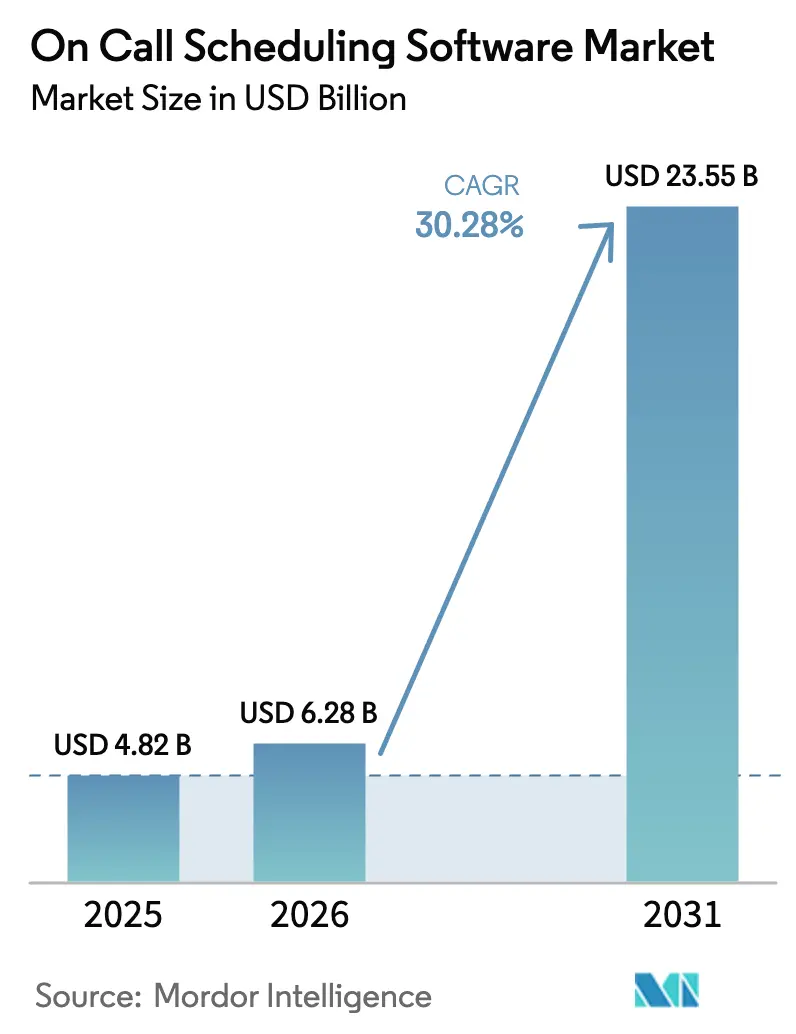

| Market Size (2026) | USD 6.28 Billion |

| Market Size (2031) | USD 23.55 Billion |

| Growth Rate (2026 - 2031) | 30.28% CAGR |

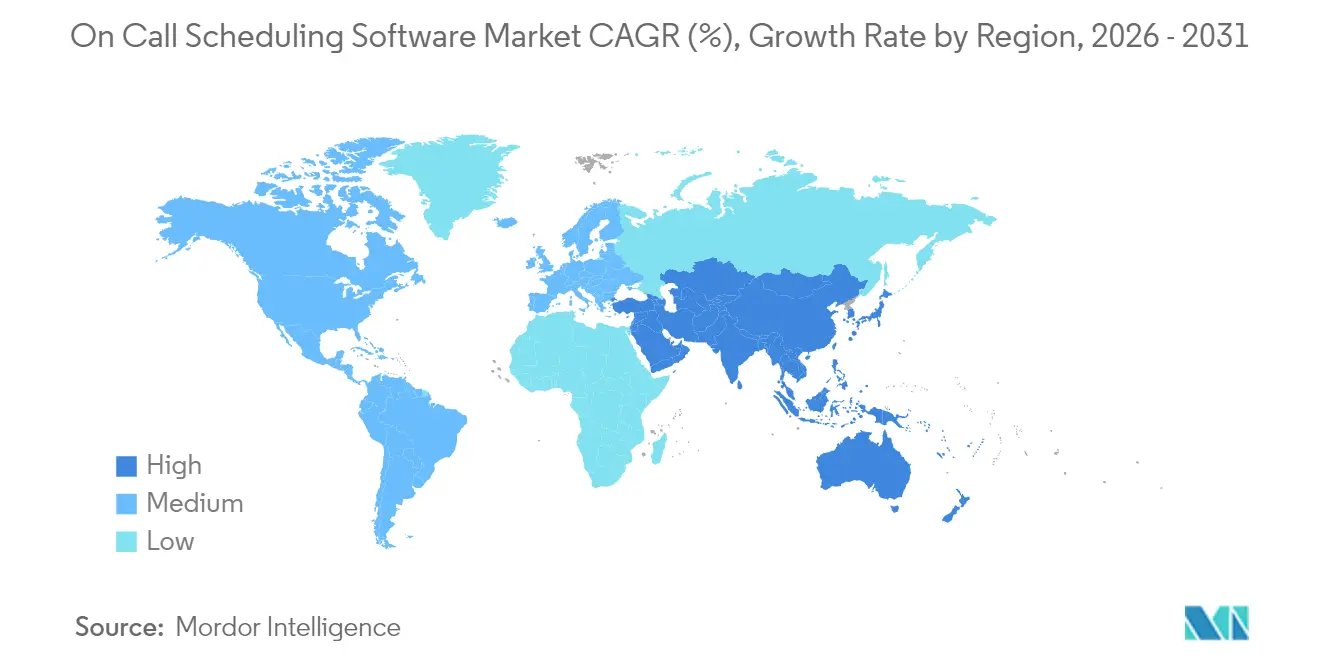

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

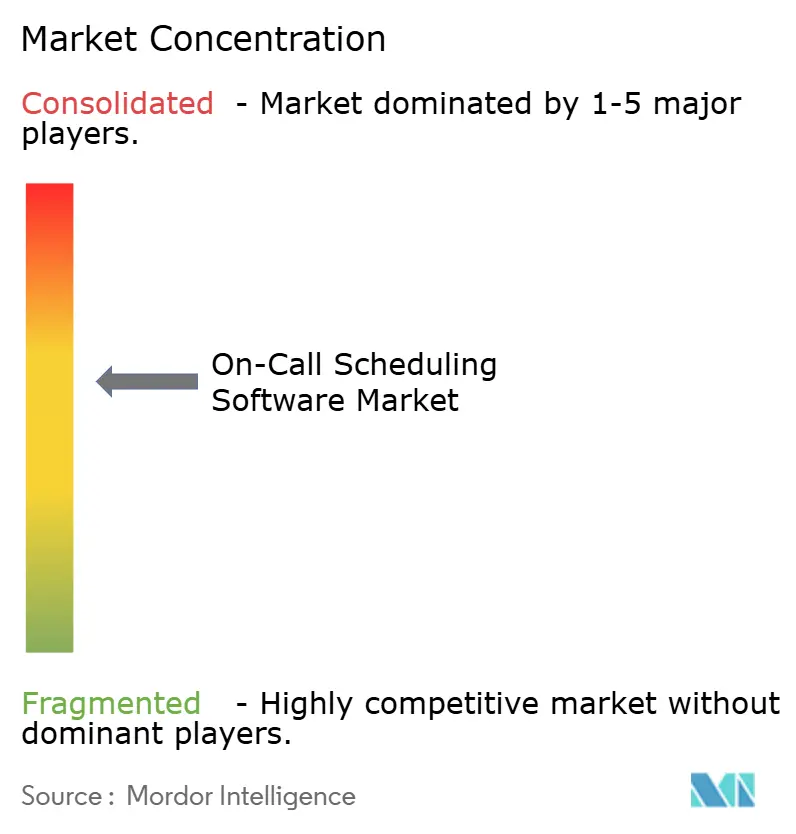

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

On Call Scheduling Software Market Analysis by Mordor Intelligence

On-call scheduling software market size in 2026 is estimated at USD 6.28 billion, growing from 2025 value of USD 4.82 billion with 2031 projections showing USD 23.55 billion, growing at 30.28% CAGR over 2026-2031. Cloud-based deployment models already hold a dominant position, and hybrid options are closing the gap as regulated industries balance data sovereignty needs with modern functionality. Rapid expansion is fueled by DevOps maturity, distributed cloud-native architectures, and stricter compliance rules that penalize slow response times. Vendors that embed AI to anticipate incidents and tailor escalations are winning deals because they help enterprises reduce mean time to resolution and lower revenue loss from outages. Consolidation is intensifying, as illustrated by ServiceNow’s 2024 acquisition of Moveworks, where platforms are fusing conversational AI with incident workflows to eliminate manual handoffs.

Key Report Takeaways

- By deployment type, cloud-based models held 69.12% of the on-call scheduling software market share in 2025, whereas hybrid deployments are projected to expand at a 31.20% CAGR through 2031.

- By organization size, large enterprises accounted for a 61.74% share of the on-call scheduling software market size in 2025, while small and medium-sized enterprises are expected to advance at a 30.85% CAGR to 2031.

- By end-use industry, information technology and telecommunications led with a 36.40% revenue share in 2025; healthcare is forecast to post the fastest growth at a 31.75% CAGR through 2031.

- By application, incident response management captured 43.10% of the revenue in 2025, while DevOps and continuous delivery are set to grow at a 30.60% CAGR between 2026 and 2031.

- By geography, North America dominated with a 39.15% share in 2025, whereas the Asia Pacific is positioned to log a 31.90% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global On Call Scheduling Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of DevOps and Site Reliability Engineering Practices | +8.2% | Global, led by North America and Europe | Medium term (2-4 years) |

| Rising Incidence of Digital Service Outages and Need for Rapid Response | +7.8% | Global, most acute in cloud-dependent regions | Short term (≤ 2 years) |

| Growing Adoption of Cloud-Native Microservices Architectures | +6.9% | Asia-Pacific core, spill-over to North America and Europe | Medium term (2-4 years) |

| Expansion of Remote and Hybrid Workforces Requiring 24-7 Coverage | +5.4% | Global, skewed toward developed economies | Short term (≤ 2 years) |

| Increasing Regulatory Scrutiny on Response Times in Critical Industries | +4.1% | North America and EU, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Integration of AI-Powered Alerting and Predictive Escalation Features | +3.7% | Global early adopters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Proliferation of DevOps and Site Reliability Engineering Practices

A critical mass of enterprises now runs DevOps pipelines, and 78% link those workflows directly into on-call scheduling solutions.[1]PagerDuty, “State of Digital Operations Report 2024,” pagerduty.com Continuous integration shortens release cycles, so incident teams must respond in lockstep with deployment velocity. Sophisticated rotation engines that map expertise to service ownership have become the standard, and demand for automated incident correlation continues to rise. Organizations emphasize mean time to resolution as a board-level metric, pushing vendors to embed analytics that surface skill gaps and optimize handoffs. As site reliability engineering gains adoption beyond technology companies, even traditional sectors now require advanced queueing logic and bidirectional links to observability stacks.

Rising Incidence of Digital Service Outages and Need for Rapid Response

Outages remain costly: 80% of firms experienced at least one major disruption in 2024, averaging more than USD 1 million per incident.[2]Uptime Institute, “Global Data Center Survey 2024,” uptimeinstitute.com Boards view downtime as brand erosion and revenue leakage, so the ability to orchestrate rapid multi-channel alerts escalates in importance. Automated routing, role-based paging, and fallback mechanisms help reduce human latency. Real-time dashboards that unify monitoring data with on-call status shorten diagnosis cycles. These capabilities shift buying criteria from simply scheduling personnel to guaranteeing service continuity under stringent service-level agreements.

Growing Adoption of Cloud-Native Microservices Architectures

Enterprises transitioning from monoliths to microservices create many more points of failure, resulting in 3.2 times more specialized incidents per month.[3]Alibaba Cloud, “Microservices Architecture Best Practices,” alibabacloud.com New tools must understand service meshes, container orchestration, and dependency graphs to pinpoint the right responder. Scheduling engines now pull run-time context from Kubernetes and serverless environments, matching failures with engineers familiar with each microservice. Vendors also deliver API hooks for service discovery, so that incident data can enrich architectural maps. As cloud-native footprints grow, integration depth with continuous delivery pipelines and infrastructure-as-code repositories becomes a key differentiator.

Expansion of Remote and Hybrid Workforces Requiring 24-7 Coverage

A distributed workforce complicates handoffs across time zones; 67% of enterprises report coverage gaps in hybrid models. Mobile-first interfaces enable responders to acknowledge alerts without needing a laptop. Geo-based rotations reduce burnout by aligning schedules with local hours, and self-service swap requests maintain fairness. Integrations with collaboration suites keep stakeholders informed in a single channel, minimizing context switching. Analytics modules track off-hour burden to refine staffing plans, easing compliance with regional labor codes. The shift toward flexible work, therefore, raises baseline functionality that buyers expect from modern platforms.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Switching Costs from Legacy Paging Systems | -4.3% | Global, pronounced in long-established enterprises | Medium term (2-4 years) |

| Data Security and Compliance Concerns with Cloud Deployments | -3.8% | EU and regulated verticals worldwide | Short term (≤ 2 years) |

| Alert Fatigue Leading to User Resistance | -2.9% | Global, high-volume incident environments | Short term (≤ 2 years) |

| Budget Constraints in Small and Medium-Sized Enterprises | -2.1% | Global, cost-sensitive markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Switching Costs from Legacy Paging Systems

Decades-old pagers remain entrenched in hospitals, utilities, and emergency services. Replacing them requires training, network upgrades, and dual-running periods that introduce operational risk. Many organizations preserve legacy paging for redundancy, which limits the immediate payback on full migrations. Integrations that bridge pager gateways with modern alerts help reduce disruption but also postpone full platform adoption. Vendors must therefore build coexistence pathways and demonstrate unambiguous ROI before boards approve budget reallocations.

Data Security and Compliance Concerns with Cloud Deployments

The EU’s Digital Operational Resilience Act enforces strict logging, audit readiness, and data residency mandates. Financial services, healthcare, and critical infrastructure operators scrutinize whether incident data can remain in-region and encrypted at rest. Cloud platforms must be certified against ISO 27001 and sector-specific standards, while also offering private networking and customer-managed keys. Some buyers default to hybrid or on-premises modes, dampening near-term SaaS penetration until providers satisfy governance checklists.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Type: Cloud Dominance Drives Hybrid Innovation

Cloud installations generated 69.12% of revenue in 2025 as users prioritized fast onboarding and seamless upgrades, underscoring the scale advantage of the on-call scheduling software market. Many enterprises favor SaaS because it offloads infrastructure tasks and provides instant access to AI modules released on a rolling cadence. Yet regulatory mandates encourage dual-stack strategies, propelling hybrid models to a forecast 31.20% CAGR. Vendors such as PagerDuty introduced split-plane architecture in 2024 to meet this requirement.

Hybrid deployments enable firms to store sensitive logs on-premises while deriving predictive insights from cloud analytics. The arrangement suits cross-border businesses subject to data localization laws. Meanwhile, on-premises deployments persist among defense agencies and industrial operators that prohibit outbound connections. As multicloud adoption rises, scheduling engines must orchestrate incidents across Kubernetes clusters, serverless endpoints, and legacy bare-metal assets in a single unified console, positioning the hybrid tier for significant growth.

By Organization Size: Enterprise Leadership Meets SME Acceleration

Large enterprises controlled 61.74% of 2025 spending, indicating the significant purchasing power of Fortune 1000 technology, banking, and telecom firms. Their complex tech stacks demand granular rota rules, skill-based routing, and integration with dozens of DevOps and IT service management tools. These buyers also utilize advanced capacity models that reveal labor gaps months in advance, thereby ensuring uptime for mission-critical digital services.

The small and medium-sized cohort, however, is scaling quickly at 30.85% CAGR as subscription pricing lowers entry barriers. The Australian Cyber Security Centre emphasized incident preparedness in its updated 2024 continuity guidance, influencing budget allocation among resource-constrained firms. Vendors respond with drag-and-drop policy builders, chat-based onboarding, and pay-as-you-grow tiers that fit lean staff structures. Over time, multi-tenant SaaS backbones reduce the cost of ownership, reinforcing an adoption flywheel within the SME user base.

By End Use Industry: IT Leadership Yields to Healthcare Growth

The information technology and telecommunications segment held 36.40% of 2025 demand, reflecting its early adoption of continuous delivery and microservices architectures that turn every release into an implicit reliability test. Operators in this vertical monitor feature flags, rolling canaries, and traffic splits, all of which benefit from tight webhook loops into incident queues.

Healthcare, though smaller today, shows the steepest 31.75% CAGR as electronic health records, telemedicine, and connected devices expand the blast radius of downtime. Oregon’s HB4089 requires facilities to document on-call coverage and meet prescribed response times, spurring hospital procurement. Scheduling platforms must interoperate with clinical paging and comply with HIPAA logging mandates. As remote surgery and wearable sensors proliferate, uptime has a direct impact on patient safety, thereby elevating the urgency of this vertical.

By Application: Incident Response Dominance Faces DevOps Disruption

Incident response management produced 43.10% of 2025 revenue, underscoring the historical core of the on-call scheduling software market. Standard functions include multi-channel alerting, escalation loops, and post-incident reporting. Yet, DevOps and continuous delivery workflows are advancing at a 30.60% CAGR as engineering teams embed rotation triggers directly into deployment pipelines.

Integrations with CI/CD tools automatically tag commits, allocate hotfix owners, and trigger rollbacks when error budgets are depleted. Field service management is an emerging adjacency where mobile crews coordinate physical repairs with digital triage data; SAP’s 2024 launch of a combined suite validates this convergence. Forward-looking buyers seek single consoles that orchestrate both software and hardware incidents, broadening total addressable use cases.

Geography Analysis

North America retained a 39.15% revenue share in 2025, driven by widespread DevOps maturity, deep cloud penetration, and stringent service-level requirements in technology, finance, and healthcare. United States enterprises deploy multi-cloud topologies that boost incident counts yet allocate larger budgets to manage them. Canada follows closely, pushed by banking and provincial e-health mandates that prioritize uptime documentation. Mexico’s software-as-a-service boom generates new demand from fintechs and retailers expanding their digital storefronts.

The Asia Pacific, the fastest-growing region with a 31.90% CAGR, benefits from smartphone ubiquity, hyperscale cloud expansion, and government tech stimulus. Boston Consulting Group measured a regional AI adoption rate of 78% in 2024, outpacing the global average and intensifying interest in predictive escalation engines. China’s city-level smart-service targets, India’s booming IT outsourcing sector, and Japan’s Quality-of-Service culture all create tailwinds. Hybrid cloud edges remain important where national data policies limit outbound telemetry, encouraging the implementation of localized failsafes within global chains.

Europe posts steady growth as DORA takes effect, compelling financial institutions to audit incident workflows and maintain immutable logs. Germany’s Industry 4.0 initiative promotes reliability across cyber-physical factories, while the United Kingdom embeds operational resilience into its post-Brexit regulatory framework. France advocates digital sovereignty, so vendors offering hosted solutions inside domestic borders gain an advantage. The Middle East and Africa, as well as South America, are later adopters, yet they benefit from cloud region launches and e-government projects that raise citizen expectations for 24/7 availability.

Competitive Landscape

The on-call scheduling software market remains moderately fragmented, with a blend of broad ITSM suites and focused best-of-breed challengers. PagerDuty defends its early-mover status by releasing AI modules that cluster alerts and recommend responders, curbing fatigue. ServiceNow capitalized on its Moveworks purchase to weave conversational interfaces into workflow automation, allowing employees to triage incidents in plain language. Atlassian deepened integrations between Jira Service Management and leading observability vendors, streamlining ticket genesis from performance anomalies.

Differentiation centers on predictive analytics, mobile usability, and sector-specific compliance. Healthcare buyers favor HIPAA-ready messaging channels with granular audit trails, prompting entrants like OnPage to enhance encryption and logging capabilities. Energy utilities prioritize SCADA tie-ins and air-gapped deployment flavors to safeguard grid operations. Meanwhile, SME-oriented upstarts provide quick-start templates that slash onboarding from weeks to hours. Price competition intensifies in the mid-market as annual subscriptions fall into the low-five-figure USD range, but large-scale enterprise deals still reward platform breadth.

Mergers and large-ticket acquisitions hint at tightening competition. The 2024 ServiceNow-Moveworks deal, valued at USD 2.85 billion, eclipsed previous transactions in the space, signaling that conversational AI will soon become a table-stakes requirement. Private-equity interest is also rising, seen in minority stakes taken in regional vendors specializing in public safety. Over the forecast period, expect convergence between incident response, AIOps, and workflow orchestration as buyers consolidate tooling to minimize integration overhead.

On Call Scheduling Software Industry Leaders

PagerDuty, Inc.

Atlassian Corporation Plc

Everbridge, Inc.

Splunk Inc.

ServiceNow, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Splunk expanded Splunk On-Call with an edge-deployment option that keeps incident data inside customer-controlled environments to meet stringent EMEA data-residency requirements.

- May 2025: Atlassian introduced Jira On-Call, a streamlined SaaS add-on within Jira Service Management designed for small and medium-sized enterprises seeking rapid rota setup and integrated alerting.

- March 2025: PagerDuty announced the USD 450 million acquisition of FireHydrant, adding automated post-incident analysis and runbook generation to its on-call scheduling portfolio.

- January 2025: ServiceNow released a proactive incident-prevention module for the Now Platform that combines real-time telemetry with generative AI to divert potential outages before alerts are triggered.

Global On Call Scheduling Software Market Report Scope

| Cloud-Based |

| On-Premises |

| Hybrid |

| Small and Medium-Sized Enterprises |

| Large Enterprises |

| Healthcare |

| Information Technology and Telecommunications |

| Public Safety and Emergency Services |

| Energy and Utilities |

| Financial Services |

| Other End Use Industries |

| Incident Response Management |

| Employee Scheduling |

| Shift Planning and Rostering |

| Field Service Management |

| DevOps and Continuous Delivery |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Deployment Type | Cloud-Based | ||

| On-Premises | |||

| Hybrid | |||

| By Organization Size | Small and Medium-Sized Enterprises | ||

| Large Enterprises | |||

| By End Use Industry | Healthcare | ||

| Information Technology and Telecommunications | |||

| Public Safety and Emergency Services | |||

| Energy and Utilities | |||

| Financial Services | |||

| Other End Use Industries | |||

| By Application | Incident Response Management | ||

| Employee Scheduling | |||

| Shift Planning and Rostering | |||

| Field Service Management | |||

| DevOps and Continuous Delivery | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the projected value of the on-call scheduling software market by 2031?

The market is expected to reach USD 23.55 billion by 2031, reflecting a 30.28% CAGR from 2026.

Which deployment model is expanding the fastest within the on-call scheduling software space?

Hybrid deployments are forecast to grow at a 31.20% CAGR as enterprises blend cloud analytics with on-premises control.

Why are healthcare organizations increasing spending on on-call scheduling tools?

New regulations such as Oregon’s HB4089 mandate documented coverage and rapid response, driving healthcare’s 31.75% forecast CAGR.

How does AI enhance on-call scheduling performance?

AI modules cluster related alerts, predict incident probability, and auto-assign responders, cutting mean time to resolution and reducing alert fatigue.

Which region is poised for the strongest growth in on-call scheduling software adoption?

Asia Pacific is projected to post a 31.90% CAGR through 2031 due to aggressive digital transformation and high AI adoption rates.

What is the main barrier to replacing legacy paging systems?

High switching costs, including training, risk of disruption, and dual operations during migration, delay full adoption of modern platforms.

Page last updated on: