Predictive Dialer Software Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

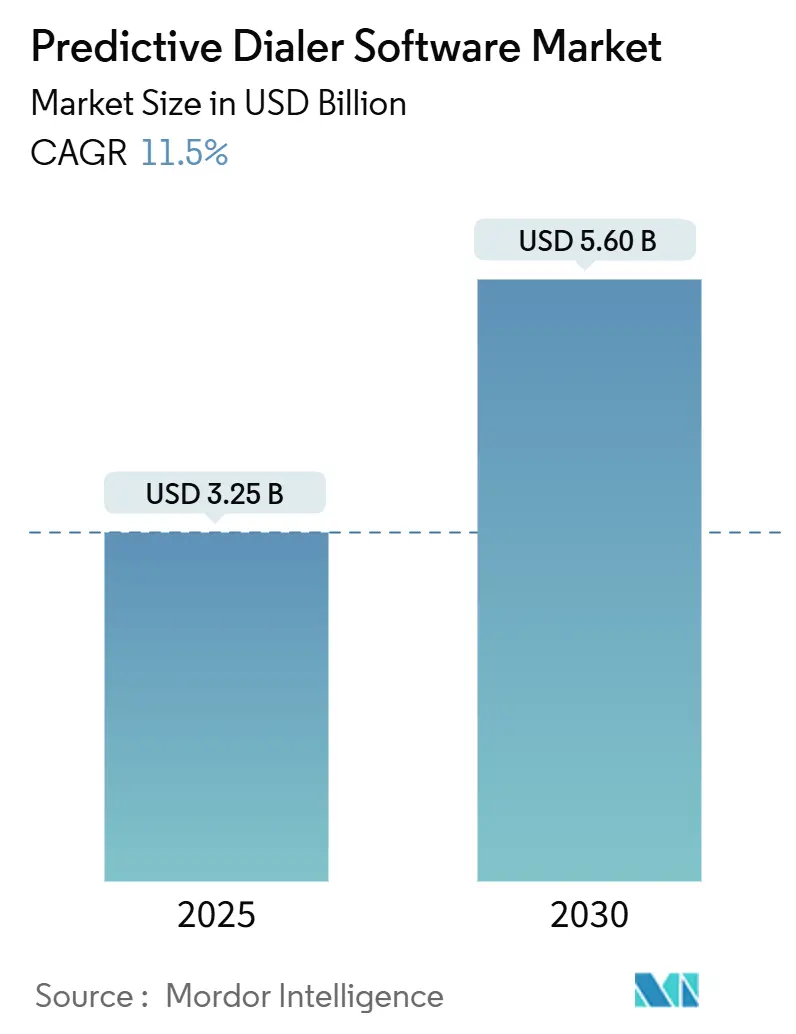

| Market Size (2025) | USD 3.25 Billion |

| Market Size (2030) | USD 5.60 Billion |

| Growth Rate (2025 - 2030) | 11.50% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Predictive Dialer Software Market Analysis by Mordor Intelligence

The predictive dialer software market size stands at USD 3.25 billion in 2025 and is projected to reach USD 5.6 billion by 2030, reflecting an 11.5% CAGR over the forecast period. Heightened investments in cloud-native contact center platforms, expanding artificial intelligence integration, and growing regulatory compliance requirements collectively underpin this robust trajectory. Vendors that embed real-time analytics within dialing workflows differentiate by lifting contact rates, while enterprises adopting proactive customer-outreach programs translate call efficiency into measurable revenue gains. North America retains scale leadership through stringent consent rules that accelerate technology upgrades, whereas Asia Pacific supplies outsized incremental volume as enterprises in banking, telecommunications, and healthcare modernize customer-engagement infrastructure.

Key Report Takeaways

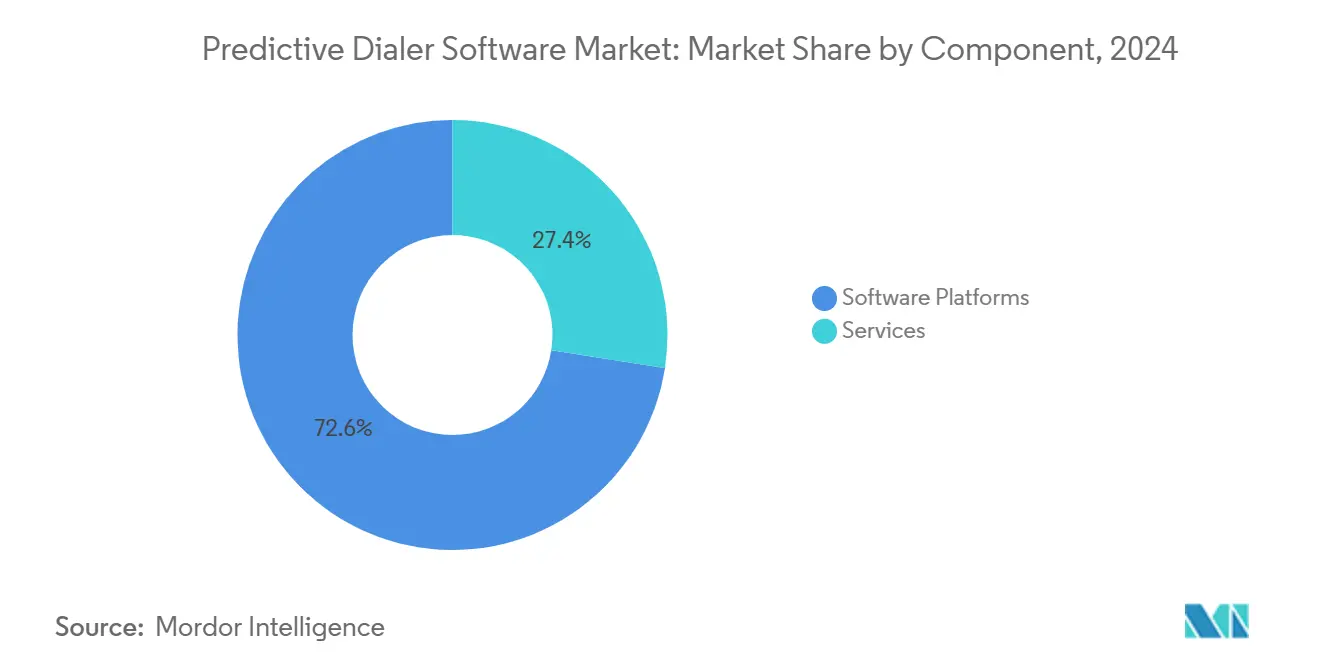

- By component, software platforms captured 72.55% of the predictive dialer software market share in 2024, while services are advancing at the fastest 13.57% CAGR to 2030.

- By deployment mode, cloud deployments accounted for 85.52% of the predictive dialer software market size in 2024 and are on course to expand at a 14.44% CAGR through 2030.

- By dialer type, the predictive dialer segment led with a 57.44% share of the predictive dialer software market in 2024; AI-enhanced variants are projected to post the highest 12.52% CAGR from 2024 to 2030.

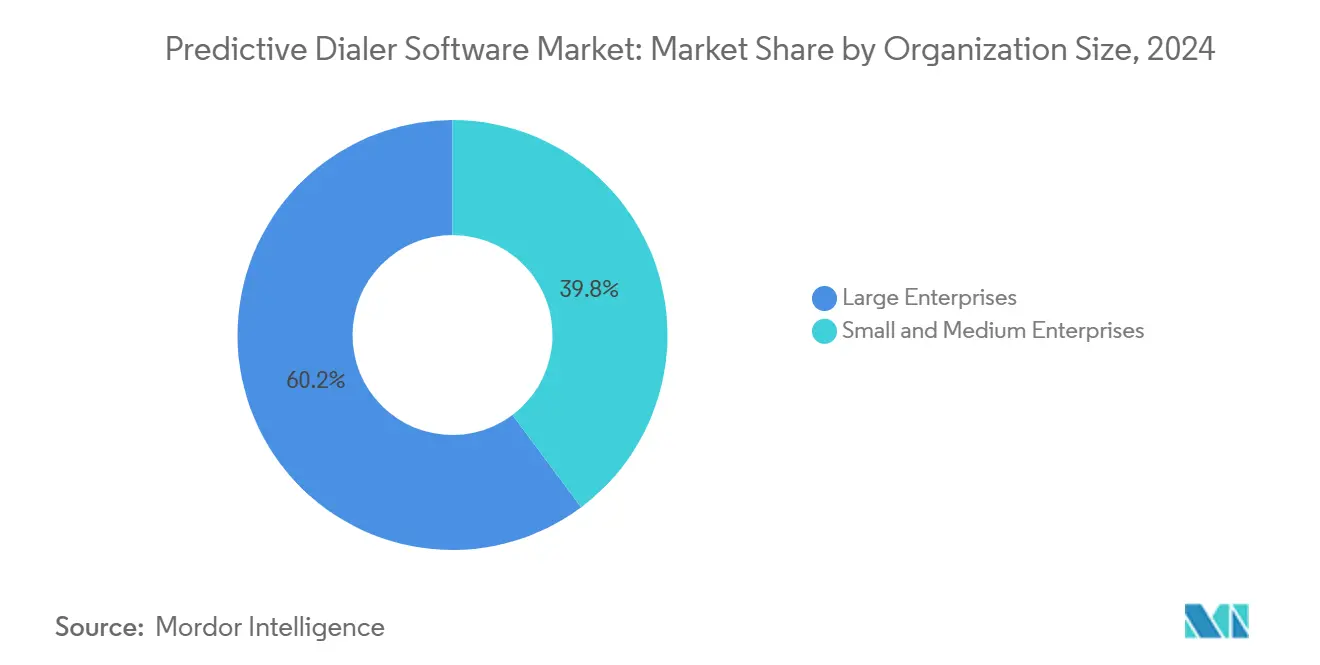

- By organization size, large enterprises held a 60.22% revenue share of the predictive dialer software market in 2024, while small and medium-sized enterprises registered the fastest growth at a 14.89% CAGR from 2024 to 2030.

- By end-use industry, telecommunications accounted for a 26.11% share of the predictive dialer software market size in 2024, as debt-collection operations are projected to grow at a 12.24% CAGR through 2030.

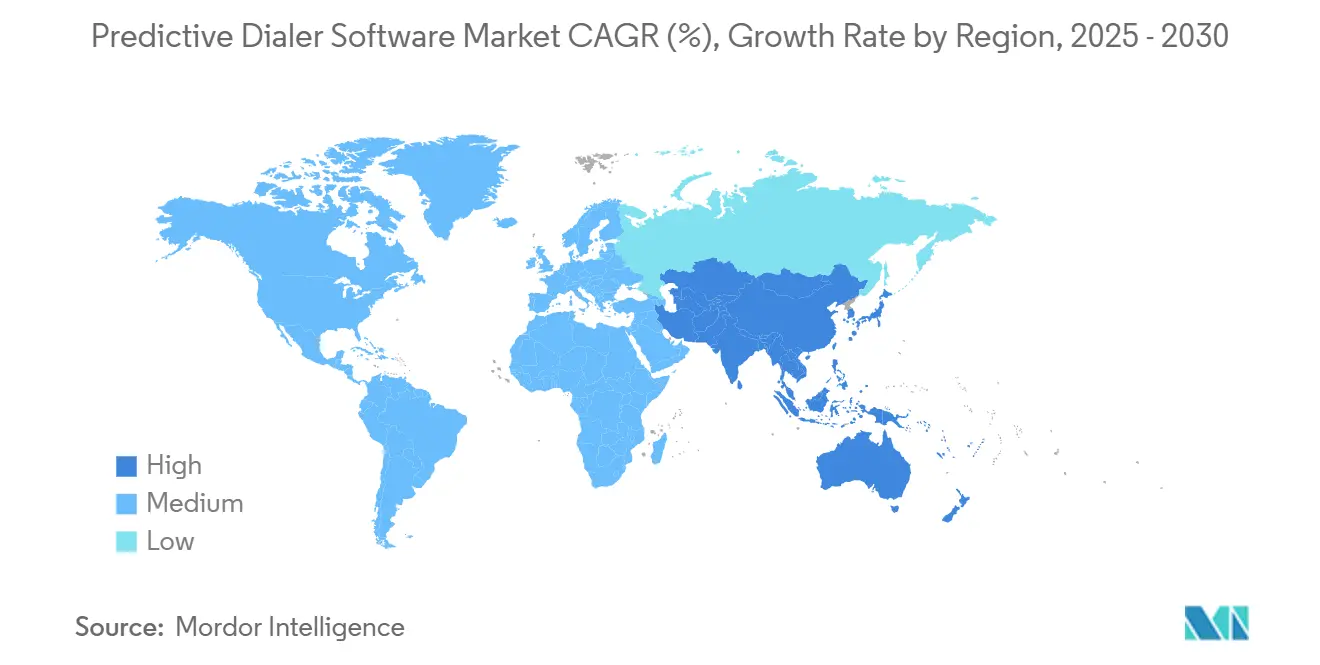

- By geography, North America maintained a 41.55% market share of the predictive dialer software market in 2024, and the Asia Pacific emerged as the fastest-growing region, with a 13.82% CAGR through 2030.

Global Predictive Dialer Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated Adoption of Cloud-Based Contact Centers | +2.1% | Global, with North America and Europe leading | Medium term (2-4 years) |

| Growing Demand for Proactive Customer Outreach | +1.6% | Global, strongest in APAC and North America | Short term (≤ 2 years) |

| Integration of Predictive Dialing with CRM and AI Analytics | +1.0% | North America, Europe, developed APAC markets | Medium term (2-4 years) |

| Rise of Remote and Hybrid Work Models | +1.8% | Global, particularly North America and Europe | Short term (≤ 2 years) |

| AI-Powered Right-Party Contact Optimization | +1.5% | Global, early adoption in North America | Long term (≥ 4 years) |

| Carrier-Level STIR/SHAKEN Authentication Boosting Answer Rates | +0.9% | North America primarily, expanding to other regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerated Adoption of Cloud-Based Contact Centers

Enterprises shifting from on-premises PBX hardware to cloud contact-center-as-a-service models unlock on-demand scalability, unified API frameworks, and subscription-based pricing that eliminate substantial capital expenditure barriers. Centralized cloud environments simplify multi-tenant consent management, a capability vital under tightened telemarketing rules, and shorten solution deployment cycles from months to days. Providers boasting SOC 2 Type II, PCI DSS Level 1, and region-specific data-residency assurances increasingly win competitive bids among regulated verticals. This migration democratizes sophisticated dialing algorithms, enabling midsized businesses to harness capabilities formerly reserved for Fortune 500 operators. Vendor roadmaps show accelerated release cadences for conversation intelligence, predictive list management, and automated workflow orchestration functions that are only feasible on elastic cloud infrastructures.

Growing Demand for Proactive Customer Outreach

Organizations now embed outbound campaigns across retention, collections, appointment management, and fraud alert journeys instead of limiting calls to pure sales.[1]Five9 Healthcare Solutions Team, “AI Creates Exceptional Experiences in Healthcare,” five9.com Healthcare systems report double-digit reductions in missed appointments when predictive dialers trigger automated reminders, and financial institutions cite measurable declines in late-payment delinquency after right-time payment-reminder cadences replace generic batch calls. This value migration reframes dialing as a revenue-protection discipline rather than a cost center, permitting larger budget allocations and executive-level sponsorship of outbound modernization projects. Consequently, vendors broaden native integration blueprints to electronic health record, billing, and loan-management platforms, thereby lowering the total cost of ownership for cross-functional deployments. Outcome-based key performance indicators, including conversion rate uplift, hold periods avoided, and net promoter score improvements, dominate procurement scorecards and reinforce continued spending momentum.

Integration with CRM and AI Analytics

Tight coupling between predictive dialer engines and customer relationship management systems unifies historical contact data, customer-lifecycle events, and third-party intent signals to support intelligent call-list prioritization. Machine-learning models analyze answer likelihood, purchasing propensity, and abandonment behavior to adjust pacing algorithms in real time, delivering 3× agent productivity gains relative to legacy statistical dialers. On-screen agent aids draw from sentiment analysis and knowledge-base suggestions to reduce average handle time while lifting first-call resolution. Vendors investing in proprietary AI frameworks erect competitive moats as training-data volume directly correlates with algorithm precision. Enterprises increasingly evaluate platform choices based on breadth of pre-built CRM and marketing-automation connectors, thereby reinforcing ecosystem lock-in around top vendors that command premium recurring revenue multiples.

Rise of Remote and Hybrid Work Models

Telework adoption, cemented during 2024, imposes new architectural, security, and compliance demands on outbound programs. Contact-center leaders must furnish distributed agents with low-latency voice connectivity, while supervisors require granular oversight regardless of agent location. Cloud-native dialers embed voice-over-internet-protocol optimizers that adapt to broadband variability, plus real-time screen monitoring to maintain quality-assurance standards previously achieved on-premises. Equally important, encrypted call recordings, multifactor authentication, and secure number-masking preserve data confidentiality in home offices. The expanded talent pool available to remote-enabled employers drives seat-count growth even in mature markets, underscoring why location-agnostic dialing platforms represent a structural growth catalyst for the predictive dialer software market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Global Telemarketing Regulations (e.g., TCPA, GDPR) | -1.2% | Global, with varying intensity by region | Long term (≥ 4 years) |

| Growing Consumer Adoption of Call Blocking and Labeling Apps | -0.7% | Global, strongest in developed markets | Medium term (2-4 years) |

| Cost Burden of Carrier Call Authentication and Verification | -0.6% | North America primarily, expanding globally | Medium term (2-4 years) |

| Data Scarcity for Training AI Models in Small Enterprises | -0.4% | Global, particularly affecting SME segment | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Global Telemarketing Regulations

Expanded enforcement of the United States Telephone Consumer Protection Act, the European Union’s General Data Protection Regulation, and region-specific opt-in mandates compels outbound organizations to prove explicit consent, track dialing frequency, and honor do-not-call requests.[2]Federal Communications Commission, “FCC Adopts New Rules to Combat Illegal Robocalls and Texts,” fcc.gov These provisions raise implementation complexity, lengthen campaign-setup cycles, and impose non-compliance penalties that can exceed annual technology budgets. Unified consent repositories, automated record-keeping, and dynamic suppression algorithms become mandatory feature sets, raising total ownership costs for entry-level buyers. Where regulators introduce regional data-localization clauses, vendors must negotiate additional hosting contracts or form sovereign-cloud alliances, slowing cross-border expansion.

Growing Consumer Adoption of Call Blocking and Labeling Apps

Smartphone operating systems and carrier-level analytics now label or automatically silence suspected spam calls, curtailing answer rates for even fully compliant enterprises. Legitimate businesses must therefore register numbers with authentication frameworks such as STIR/SHAKEN to avoid misclassification, invest in branded caller ID certificates, and rotate outbound numbers to preserve dialing reputation. Contact centers without dedicated telephony engineers struggle to keep pace with evolving carrier scoring algorithms, which undercut outreach conversion metrics. The result is an upward cost spiral as organizations purchase additional inventory, implement analytic dashboards to track call-authentication health, and retrain agents to manage verification workflows.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Deepen Post-Deployment Value Creation

Software platforms held 72.55% predictive dialer software market share in 2024 as core dialing engines, user consoles, and pacing algorithms remained foundational procurement priorities. Rapid cloud adoption, however, elevates services demand, pushing that revenue stream toward a 13.57% CAGR and widening the overall predictive dialer software market size. Enterprises pursuing multi-region rollouts purchase implementation consulting to configure consent management rules, integrate CRM triggers, and calibrate AI models against bespoke outcome metrics. Managed services teams subsequently oversee campaign orchestration, deliver weekly performance dashboards, and optimize call-list segmentation based on real-time customer-journey feedback. Regulatory audits further propel growth in compliance-focused advisory engagements, as clients request expert validation of opt-in verbiage, data-storage residency, and call-record retention settings. Vendors responding with tiered service portfolios spanning design workshops, run-operate managed models, and outcome-based optimization retainers cement longer contract tenures and raise average revenue per user.

The acceleration of artificial intelligence adoption intensifies the need for ongoing data-science support. Model-retraining services align predictive pacing parameters with seasonal customer-behavior shifts such as holiday purchasing surges or tax-season collections spikes. Simultaneously, enterprises entrust vendor experts to monitor answer-rate fluctuations caused by carrier reputation scoring, update call-authentication tokens, and liaise with telecom partners to promptly resolve flagging incidents. These post-deployment dependencies signify why the services segment, although currently smaller, absorbs a disproportionate share of incremental spend as the predictive dialer software market matures.

By Deployment Mode: Cloud Dominance Becomes Irreversible

Cloud solutions controlled an 85.52% slice of the predictive dialer software market in 2024, and their double-digit 14.44% CAGR underscores an irreversible shift toward consumption-based delivery. Subscription pricing aligns operating expenses with seat utilization, while automated feature updates allow rapid adoption of AI analytics, omnichannel orchestration, and workflow bots without disruptive version upgrades. The resulting turbulence in on-premises demand compresses hardware refresh cycles, erodes maintenance revenue for legacy vendors, and prompts accelerated vendor consolidation across the predictive dialer software industry.

Hybrid configurations persist where data-sovereignty mandates constrain full cloud migrations or where latency-sensitive voice recordings require local storage. Even in those contexts, cloud control planes oversee on-premises media gateways, proving the ascendancy of centralized management regardless of edge topology. Platform leaders invest in regionally distributed microservices to maintain sub-200-millisecond audio latency, thereby dislodging residual objections about call quality. In parallel, cloud ecosystems streamline application-programming-interface integrations with workforce-management, sentiment-analysis, and payments-processing providers, enabling one-click marketplace installs that amplify the predictive dialer software market size. Collectively, these factors raise the switching costs of reverting to legacy environments, locking in the cloud share trajectory across the forecast horizon.

By Dialer Type: AI-Enhanced Predictive Dialers Redefine Category Boundaries

Traditional predictive dialers accounted for 57.44% of revenue in 2024, yet the infusion of artificial intelligence blurs historical distinctions among predictive, progressive, and preview dialing modes. AI-enhanced engines dynamically shift pacing strategies based on instantaneous answer rate trends, agent availability, and customer sentiment gleaned from speech analytics, thereby boosting list penetration without violating regulatory call-attempt ceilings. This functional convergence elevates AI-enhanced variants to the forecast-leading 12.52% CAGR, broadening the predictive dialer software market size as enterprises justify premium licenses for adaptive engagement capabilities.

Progressive and preview approaches retain relevance in high-value consultative sales and medical outreach where contact-center managers prioritize personalization over maximum call throughput. Vendors therefore bundle configuration toggles that permit campaign-level selection among dialing modes, allowing agents to pivot between volume and quality targets intra-shift. The coexistence of modes within single platforms stimulates expansion of unified analytics dashboards that benchmark productivity across strategy mixes, further entrenching suppliers that deliver holistic dialer portfolios across the predictive dialer software market.

By Organization Size: SMEs Democratize Advanced Outbound Capabilities

Large enterprises maintained 60.22% revenue dominance in 2024 owing to extensive agent headcounts and intricate integration topologies that favor enterprise-grade platforms. Nonetheless, cloud affordability has unleashed a wave of small and medium enterprise adoption, translating into the predictive dialer software market’s fastest 14.89% CAGR cohort. Entry-level subscription tiers, drag-and-drop campaign builders, and pre-configured compliance templates lower total implementation costs below USD 10,000 annually, making predictive dialing attainable for companies that historically relied on manual call lists. This democratization of technology inflates the total addressable market, accelerating predictive dialer software market size expansion even where large-enterprise seat counts plateau.

SME buyers prioritize rapid time-to-value, compelling vendors to invest in guided onboarding wizards, video tutorials, and turnkey CRM connectors. Vendors that right-price feature bundles offering essentials such as STIR/SHAKEN authentication, dynamic caller ID rotation, and real-time dashboards avoid margin dilution while securing durable growth within this long-tail segment. The feeding back of anonymized performance benchmarks from the SME customer base enriches vendor AI models, reinforcing platform intelligence and creating virtuous data scale unique to the predictive dialer software market.

By End-Use Industry: Vertical Playbooks Deepen Market Penetration

Telecommunications providers deployed predictive dialers to manage churn-prevention outreach, plan upgrades, and network-maintenance notifications, thereby capturing 26.11% predictive dialer software market share in 2024. Collections operations emerge as the ascendant vertical, showing a 12.24% CAGR as lenders, utilities, and retail credit issuers adopt algorithmic right-party-contact timing to curb default rates. Banking, financial services, and insurance entities commit to long-term licenses because predictive dialers tie fraud-alert efficiency directly to risk mitigation savings, ensuring a continued share of wallet within the predictive dialer software market.

Healthcare adoption scales across appointment-reminder, post-discharge follow-up, and medication-adherence programs after hospital systems verified tangible reductions in no-show and readmission rates. Meanwhile, retail and e-commerce operators integrate predictive dialers with shipment-tracking and customer-feedback loops to lift net promoter scores, thereby reinforcing omnichannel loyalty strategies. Vendors co-create industry-specific compliance packs—HIPAA voice-record encryption, PCI voice-payment redaction, and financial-services audit trails—to hasten deployment cycles and command premium pricing for specialized assurance layers. These tailored playbooks expand the predictive dialer software market size by converting industry regulations from adoption barriers into technology catalysts.

Geography Analysis

North America contributed 41.55% revenue in 2024, underpinned by sophisticated contact-center ecosystems and the most stringent enforcement of consent regulations. TCPA compliance necessities, coupled with mandated STIR/SHAKEN call authentication, ensure sustained platform renewals as enterprises upgrade to integrated consent-record and branded-caller-ID capabilities. Vendors headquartered in the United States accelerate feature enhancements around real-time AI coaching and speech analytics, leveraging domestic labor scarcity to position technology as a productivity multiplier. Canadian buyers mirror U.S. usage patterns after aligning their anti-spam frameworks with cross-border partners, further consolidating regional share within the predictive dialer software market.

Asia Pacific delivers the fastest 13.82% CAGR thanks to rapid digitization across India, Southeast Asia, and China. National service providers modernize legacy outbound centers to compete for international business-process-outsourcing contracts, raising seat counts and pushing international compliance capabilities such as Timezone-Aware Dialing into mainstream procurements. Government-sponsored AI adoption programs and 5G network rollouts reduce latency barriers, allowing cloud vendors to host instances within emerging digital hubs like Indonesia and Vietnam. The pandemic-driven rise of remote agents across the Philippines stimulates demand for browser-based dialing consoles, propelling further expansion of the predictive dialer software market.

Europe’s multifaceted privacy landscape complicates volume-focused outreach, yet steady cloud adoption persists as enterprises embrace consent-centric personalization. Vendors localize user interfaces and data-retention rules to meet country-specific guidelines in Germany, France, and the Nordics, while United Kingdom financial institutions deploy advanced recording-redaction to align with Financial Conduct Authority directives. Expansion in Southern and Eastern Europe lags due to lower cloud readiness but exhibits upside potential as European Union post-COVID recovery funds channel digital-transformation subsidies toward small business contact centers. Latin America, the Middle East and Africa remain emerging contributors; however, rising smartphone penetration and fintech-led outbound models foreshadow double-digit expansion beyond 2027, collectively lifting the predictive dialer software market size at the tail of the forecast horizon.

Competitive Landscape

Market concentration is moderate as diversified contact-center-as-a-service platforms pursue vertical integration and niche AI innovators carve specialized footholds. Five9’s acquisition of Acqueon broadened omnichannel outbound orchestration, embedding journey mapping and real-time analytics to surpass pure dialing efficiency.[3]No Jitter Editorial, “Five9 to Acquire Acqueon to Expand Proactive Engagement Offerings,” nojitter.com Genesys channels over USD 400 million annually into research and development to bundle predictive dialers with experience orchestration, workforce engagement, and digital bots, thereby cross-selling six-figure annual recurring revenue packages to global banks. NICE entrenches share by fusing voice analytics with dialing engines to deliver real-time compliance automation, differentiating within regulated verticals.

Specialist vendors focus on remote-agent quality monitoring, branded-caller-ID management, or mid-market CRM integration, often packaging solutions through marketplace partnerships with cloud telephony providers. These alliances accelerate reach yet expose niche suppliers to acquisition by platform leaders seeking incremental functionality. Competitive barriers increasingly revolve around proprietary AI training data sets, depth of consent-management workflows, and global telecom carrier relationships, rather than classical dialing-algorithm performance. Customers evaluate multiyear roadmaps for AI-driven conversation intelligence, predictive contact scheduling, and omnichannel orchestration to future-proof investments, reinforcing advantages for capital-rich incumbents within the predictive dialer software market.

Pricing competition remains rational as compliance complexities elevate switching costs and heighten penalties for downtime. Vendors therefore emphasize unified service-level agreements, 99.999% uptime guarantees, and enterprise-grade security certifications. Open-API ecosystems, low-code integration builders, and marketplace extension modules further embed platforms within customer technology stacks, shrinking addressable share for emerging challengers that do not cultivate complementary partner communities.

Predictive Dialer Software Industry Leaders

Genesys Cloud Services Inc.

Five9 Inc.

NICE Ltd.

Alvaria Inc.

Talkdesk Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Exotel launched Enterprise Contact Center on Microsoft Marketplace, adding AI-first omnichannel capabilities with Dialer Plus intelligence designed for deployments of up to 20,000 users.

- March 2025: Yunlian Qimo deployed an intelligent conversational system for a Chinese healthcare group, achieving a 60% IVR deflection rate and a 50% reduction in manual outbound costs by running more than 3,000 automated patient-engagement calls per day.

- July 2025: PropStream revealed the purchase of Batch Leads and Batch Dialer (AI-driven lead generation and dialing platforms) to strengthen their real estate data and communication ecosystem.

- May 2025: MightyCall revealed enhanced manual control features for their predictive dialer, facilitating campaign efforts.

Global Predictive Dialer Software Market Report Scope

| Software Platforms |

| Services |

| Cloud |

| On-Premises |

| Predictive Dialer |

| Progressive Dialer |

| Preview Dialer |

| Small and Medium Enterprises |

| Large Enterprises |

| Banking, Financial Services and Insurance |

| Telecommunications |

| Healthcare |

| Debt Collection and Accounts Receivable |

| Retail and E-Commerce |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Southeast Asia | |

| Rest of Asia Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Kenya | |

| Rest of Africa |

| By Component | Software Platforms | |

| Services | ||

| By Deployment Mode | Cloud | |

| On-Premises | ||

| By Dialer Type | Predictive Dialer | |

| Progressive Dialer | ||

| Preview Dialer | ||

| By Organization Size | Small and Medium Enterprises | |

| Large Enterprises | ||

| By End-Use Industry | Banking, Financial Services and Insurance | |

| Telecommunications | ||

| Healthcare | ||

| Debt Collection and Accounts Receivable | ||

| Retail and E-Commerce | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Southeast Asia | ||

| Rest of Asia Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What revenue figure does the predictive dialer software market reach by 2030?

The market is projected to hit USD 5.6 billion by 2030, expanding from USD 3.25 billion in 2025 on an 11.5% CAGR.

Which deployment model is growing fastest in predictive dialing solutions?

Cloud deployments are expanding at a 14.44% CAGR as organizations favor subscription pricing and rapid scalability.

Why are services outpacing software in growth within this space?

Rising implementation complexity, AI model training, and regulatory consulting demand push services toward a 13.57% CAGR.

Which region is the quickest-growing adopter of predictive dialing platforms?

Asia Pacific leads with a 13.82% CAGR, driven by rapid digital transformation across telecom and finance.

How do regulations impact outbound calling strategies?

Rules like TCPA and GDPR necessitate stringent consent tracking and call authentication, increasing technology investment needs but restricting non-compliant dialing.

What distinguishes AI-enhanced predictive dialers from legacy systems?

AI-driven platforms adjust pacing in real time, use speech analytics for agent guidance, and optimize call timing based on dynamic conversion-probability scoring.

Page last updated on: