Broadcast Scheduling Software Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

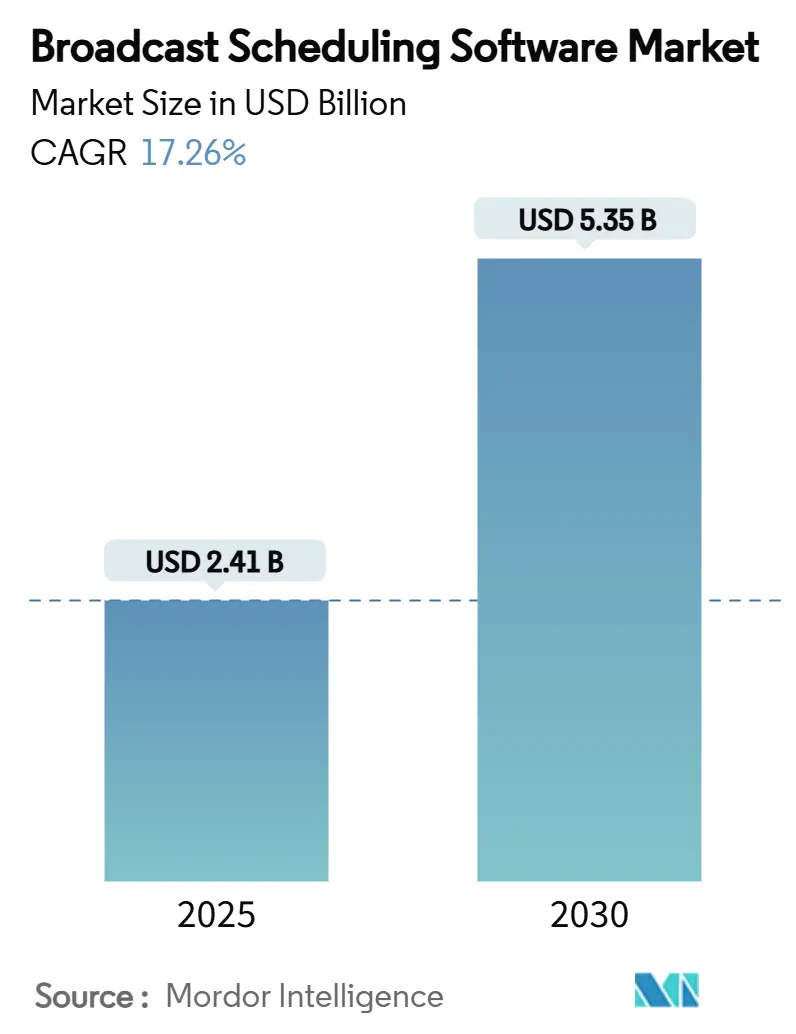

| Market Size (2025) | USD 2.41 Billion |

| Market Size (2030) | USD 5.35 Billion |

| Growth Rate (2025 - 2030) | 17.26% CAGR |

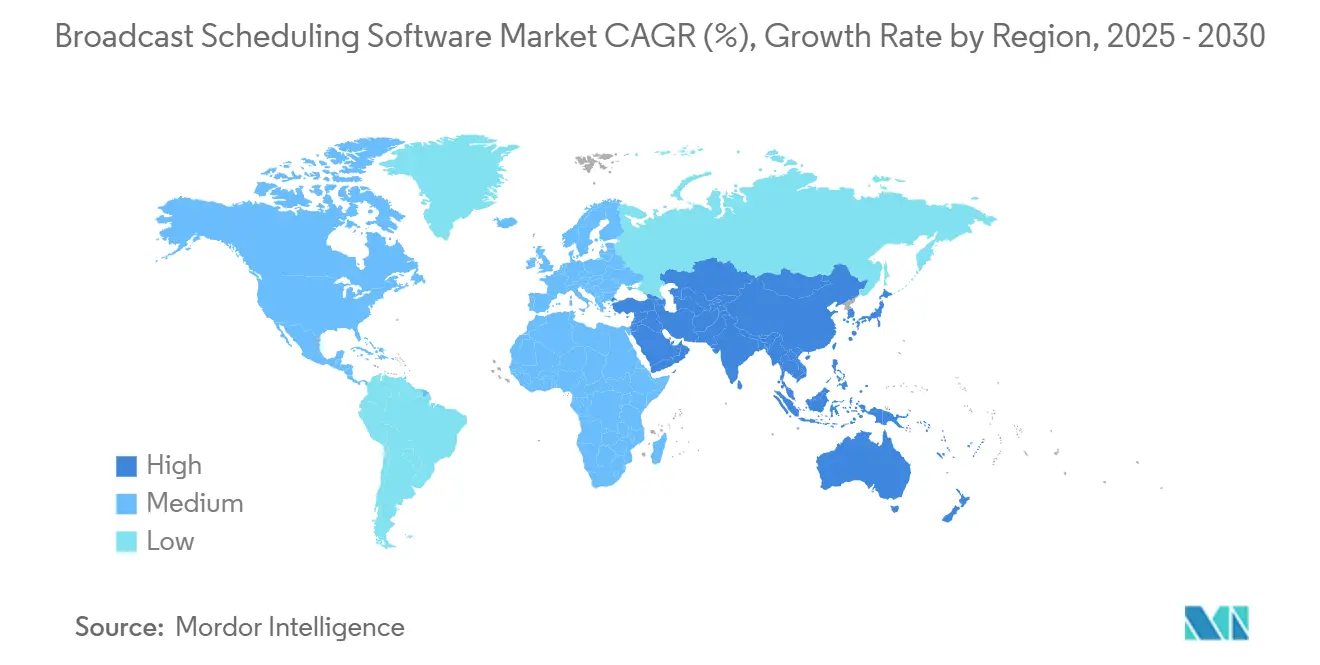

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Broadcast Scheduling Software Market Analysis by Mordor Intelligence

The broadcast scheduling software market registered a current value of USD 2.41 billion in 2025 and is forecast to climb to USD 5.35 billion by 2030, reflecting a 17.26% CAGR. This broadcast scheduling software market size expansion is being propelled by cloud-native adoption, AI-driven automation, and converging linear-to-streaming workflows. Heightened regulatory focus on accessibility, the rising complexity of multi-platform content orchestration, and the need to monetize ad inventory in real time further reinforce demand for agile scheduling suites. Vendors that can unify traffic, playout, and ad-tech into a single pane of glass are increasingly favored, while operators are shifting capital budgets toward SaaS contracts that promise faster feature velocity and lower maintenance overheads.

Key Report Takeaways

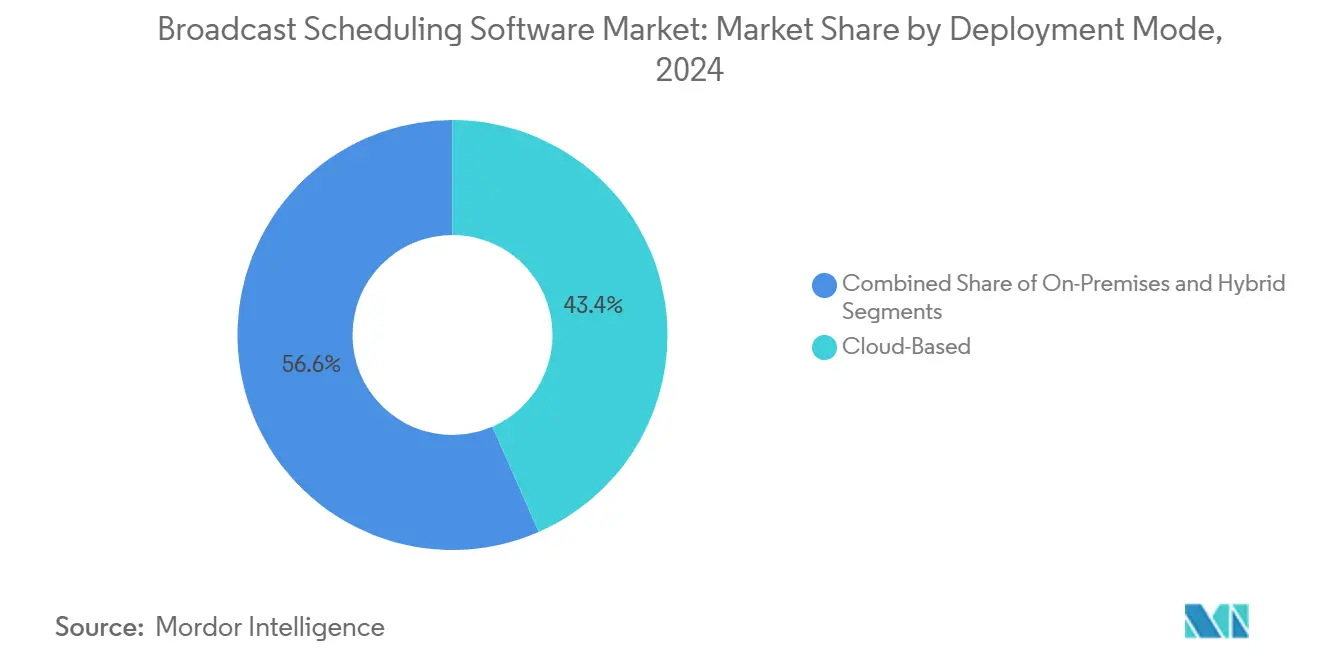

- By deployment mode, cloud-based solutions captured 43.44% share of the broadcast scheduling software market in 2024.

- By application, the broadcast scheduling software market for OTT and streaming channels is projected to capture an 18.53% CAGR between 2025 to 2030.

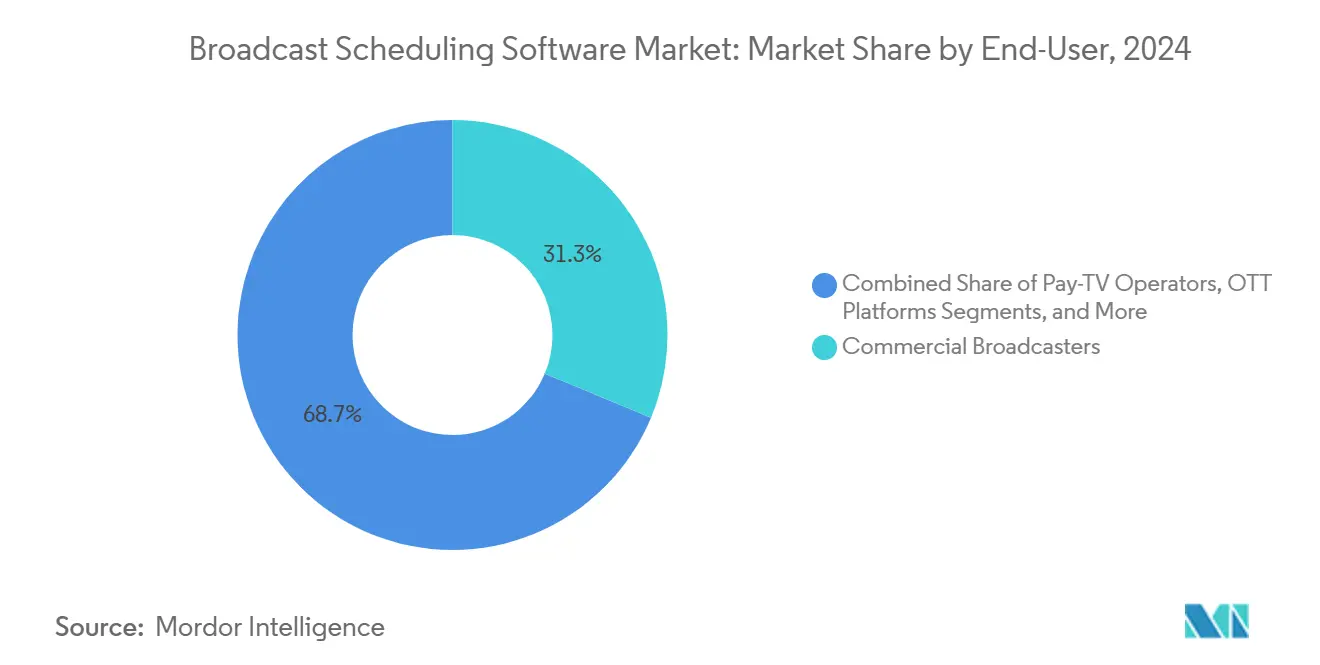

- By end-user, commercial broadcasters captured a 31.28% share of the Broadcast Scheduling Software market in 2024.

- By geography, the broadcast scheduling software market in Asia-Pacific is projected to capture an 18.50% CAGR between 2025 to 2030.

Global Broadcast Scheduling Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Migration to cloud-based SaaS platforms | +3.2% | North America, EU, global rollout | Medium term (2-4 years) |

| Proliferation of OTT / streaming channels | +4.1% | Global, APAC leading | Short term (≤2 years) |

| Ad-revenue optimisation and dynamic ad insertion | +2.8% | North America and EU core, APAC emerging | Medium term (2-4 years) |

| AI-driven predictive scheduling | +2.3% | North America and EU early adopters | Long term (≥4 years) |

| Convergence of linear and FAST channels | +1.9% | Global, pace varies | Medium term (2-4 years) |

| Accessibility compliance mandates | +1.4% | North America and EU regulators | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Migration to Cloud-Based SaaS Platforms

Broadcasters are pivoting from capex-heavy on-premise systems toward elastic SaaS models that reduce upgrade cycles and enable geo-redundancy at lower cost. Netflix directed more than USD 1.2 billion in 2024 toward cloud-native operations to underpin global scheduling agility. Azure media workload revenue jumped 29% the same year, underscoring hyperscaler traction. Integrated disaster-recovery, pay-as-you-scale pricing, and continuous deployment of new scheduling algorithms are now baseline expectations rather than stretch goals.

Proliferation of OTT / Streaming Channels

Streaming services must reconcile personalized recommendations with traditional time-slot logic, creating intricate rule sets that legacy schedulers cannot handle. Disney’s direct-to-consumer revenue reached USD 5.8 billion in 2024, necessitating sophisticated cross-platform orchestration for Disney+, Hulu, and ESPN+. FAST channels intensify pressure to serve linear-like streams with on-demand flexibility, boosting uptake of scheduling engines that ingest viewer analytics and automate placement decisions.

Ad-Revenue Optimisation and Dynamic Ad Insertion

Programmatic ad buys require frame-accurate coordination between content and ad servers. Cumulus Media attributed part of its 4% 2024 revenue uplift to digital monetization enabled by tighter scheduling-ad-tech integration. European Broadcasting Union guidelines recommend direct API bridges between schedulers and demand-side platforms to guard against mid-roll mistimings. Broadcasters that execute real-time insertion report advertising yield gains of 15–25%.[1]European Broadcasting Union, “Cybersecurity for Media Vendor Systems,” ebu.ch

AI-Driven Predictive Scheduling Adoption

Machine-learning models mine historical ratings, social chatter, and external events to predict optimal slotting. Public service newsrooms deploying AI recommendation engines saw audience retention rise between 8-12% in pilot studies. Netflix processes more than 1 billion viewing actions daily to refine release times across 190+ markets, proving the scalability of data-driven scheduling logic.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy on-premise lock-in and switching cost | -2.1% | Global, acute in mature markets | Long term (≥4 years) |

| Cyber-security and data-sovereignty concerns | -1.8% | Global, policy-driven | Medium term (2-4 years) |

| Skills gap in broadcast-IT talent | -1.3% | APAC and emerging regions | Long term (≥4 years) |

| Integration complexity across traffic / ad-tech stacks | -0.9% | North America and EU heavy users | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Legacy On-Premise Lock-In and Switching Cost

Many mid-market stations amortised legacy schedulers over a decade ago and face USD 500,000–2 million capex for wholesale replacement. Audacy’s 2024 filings spotlight maintenance of ageing stacks that siphon capital from innovation. Deep integrations with traffic, billing, and automation tools deter abrupt changeovers, stretching cloud roadmaps beyond initial timelines.

Cyber-Security and Data-Sovereignty Concerns

Scheduling platforms dictate real-time content flow, making them prime ransomware targets. EBU’s 2024 security guidelines mandate zero-trust architectures and in-country data residency options. Public broadcasters often opt for private-cloud or hybrid deployments until SaaS vendors obtain required certifications, slowing blanket cloud adoption.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Mode: Cloud Preference Deepens

Cloud solutions captured 43.44% share of the broadcast scheduling software market in 2024 and are tracking an 18.92% CAGR through 2030. Operators cite elastic scaling, geographic redundancy, and subscription-based pricing as decisive advantages over fixed on-prem architectures. The broadcast scheduling software market size attributed to cloud deployments is expected to exceed USD 3.2 billion by 2030, nearly doubling on-premise spend. On-site installations persist where sovereignty or latency mandates apply, especially in defence or public-service environments. Hybrid rollouts act as stepping-stones, coupling centralised SaaS engines with local edge caches to safeguard live feeds during connectivity outages. Azure’s media workload surge and Netflix’s cloud commitment underscore that the growth arc is irreversible.[2]Microsoft Corporation, “Microsoft 2023 Annual Report,” msft.com

The vendor battlefield now revolves around containerised microservices, infrastructure-as-code templates, and native integration with hyperscaler AI toolchains. SaaS-based schedulers push incremental feature updates weekly, contrasting with the multi-year upgrade cadence common in traditional license models. Broadcasters report 30–40% cuts in maintenance labour after retiring legacy hardware, redirecting savings into data analytics and audience engagement features. Still, some CTOs are cautious about ceding mission-critical functions to third-party clouds until regulatory audit frameworks mature.

By Application: Streaming Complexity Catalyses Innovation

Television broadcasting kept pole position with 32.15% of the broadcast scheduling software market in 2024. Yet the OTT and streaming cohort will swell fastest at an 18.53% CAGR, mirroring consumer migration to mobile and connected-TV viewing. For streamers, playlist logic must embrace binge behaviour, personalised rails, and real-time A/B testing capabilities beyond many legacy linear tools. The broadcast scheduling software market share tied to OTT workflows is projected to cross 25% by 2030 as direct-to-consumer brands escalate catalogue volumes and localise feeds.

Traditional radio and cable segments exhibit single-digit growth but still invest in schedulers that integrate podcast inserts, addressable advertising, and hybrid-radio data services. Digital-signage networks in transport hubs and retail spaces form a niche yet rising sub-segment, needing second-accurate rotation control and proof-of-play audits. Ultimately, unified software that spans live, VOD, and dynamic ad placement is emerging as the default procurement spec, compelling vendors to modularise codebases for cross-format flexibility.

By End-User: OTT Platforms Reshape the Buyer Mix

Commercial broadcasters retained a 31.28% share in 2024, leveraging entrenched advertising alliances. Yet OTT platforms will clock a 19.37% CAGR through 2030, becoming the largest buyer cluster by decade-end as they chase global scale and ad-supported tiers. Public-service entities adopt cloud suites to capex-light budgets while fulfilling mandates for accessibility and local content. Pay-TV incumbents fight cord-cutting by overlaying IP streaming and predictive metadata onto linear grids, fuelling moderate demand.

Studios and sports networks value schedulers that juggle rights windows, blackout restrictions, and real-time score-based break timing. Netflix’s 260 million-plus membership base shows the volume of decisions an algorithmic engine must take daily. Vendors offering granular entitlements management, multi-territory rights tracking, and automated compliance reporting are winning competitive tenders.

Geography Analysis

North America’s 41.70% share in 2024 stems from mature infrastructure, early cloud uptake, and FCC accessibility mandates that trigger steady upgrade cycles. Broadcasters must dual-stack ATSC 1.0 and ATSC 3.0 as the NAB transition roadmap advances, reinforcing software refresh plans.[3]National Association of Broadcasters, “Petition for Next Gen TV Transition Plan,” nab.org Consolidation among station groups like Cumulus Media, which operates 404 radio properties, amplifies demand for enterprise schedulers that pool metadata across holdings. US and Canadian operators also pilot dynamic ad insertion at scale, pushing vendors to embed programmatic connectors natively.

Asia-Pacific is on track for the fastest 18.50% CAGR through 2030, propelled by rising smartphone penetration, spectrum liberalisation, and aggressive OTT expansion. Chinese streamers localise content across dialects and time zones, complicating scheduling matrices. India’s multilingual landscape likewise necessitates robust rules engines and cloud elasticity as broadband accessibility widens. Japan and South Korea are early adopters of AI-assisted grids, while Southeast Asian telcos bundle video apps to monetise 5G, spurring new scheduler procurements.

Europe maintains healthy growth anchored by EBU standardisation efforts around security, middleware, and AI ethics. Public-service broadcasters modernise ageing tech stacks to fulfil multilingual access and sustainability objectives. Brexit-driven divergence adds compliance overhead for pan-European networks, intensifying interest in SaaS platforms that can pivot reporting templates by jurisdiction. Accessibility directives and impending Digital Services Act enforcement keep workflow re-engineering high on board agendas.

Competitive Landscape

The broadcast scheduling software market is moderately fragmented yet tightening as buyers seek single-vendor coverage from traffic through ad-tech. Legacy specialists such as WideOrbit, Mediagenix, and Imagine Communications leverage decades-deep domain know-how, entrenched workflows, and global support desks. Cloud-native challengers tout microservice agility, per-use pricing, and AI scheduling cores, appealing to OTT pure-plays and digital-first broadcasters. Hyperscalers like Microsoft and Amazon are bundling scheduling modules within wider media toolkits, foreshadowing potential commoditization and margin pressure on incumbents.

Strategic differentiation hinges on API breadth, rights-aware metadata handling, and zero-downtime release pipelines. Vendors are launching self-service dashboards that expose predictive metrics, ad yield forecasts, and compliance alerts to non-technical staff. M&A activity rose in 2024 as mid-tier providers sought scale or niche capabilities such as sports rundowns and accessibility automation. Intellectual-property filings around secure content access hint at future disruption from in-house studio tech. Overall, bargaining power is shifting toward buyers able to negotiate multi-year, multi-platform deals that consolidate playout, traffic, and digital ad insertion under unified SLAs.

Broadcast Scheduling Software Industry Leaders

WideOrbit Inc.

Mediagenix NV

Imagine Communications Corp.

Marketron Broadcast Solutions, LLC

Operative Media, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Netflix posted 16% revenue growth to USD 43.5 billion for 2024, channeling new funds into live programming and global ad-tier scheduling optimization.

- December 2024: Disney finalized its Entertainment and Sports reorganization, triggering fresh scheduler integrations across Disney+, Hulu, ESPN+, and linear outlets.

- November 2024: Disney recorded USD 23.2 billion Q3 2024 revenue after Disney+ sign-ups surged on the ‘Inside Out 2’ release, spotlighting the importance of coordinated release calendars.

- September 2024: FCC enforced updated accessibility rules mandating user-friendly caption settings, accelerating scheduler compliance projects .

- March 2024: EBU refreshed cybersecurity requirements for SaaS broadcast tools, raising the bar on vendor certifications.

Global Broadcast Scheduling Software Market Report Scope

| Cloud-Based |

| On-Premises |

| Hybrid |

| Television Broadcasting |

| Radio Broadcasting |

| OTT / Streaming Channels |

| Cable and Satellite Channels |

| IPTV |

| Digital Signage and OOH |

| Public Service Broadcasters |

| Commercial Broadcasters |

| Pay-TV Operators |

| OTT Platforms |

| Production Houses and Studios |

| Sports and Live-Events Networks |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Australia and New Zealand | |

| Rest of Asia Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Deployment Mode | Cloud-Based | |

| On-Premises | ||

| Hybrid | ||

| By Application | Television Broadcasting | |

| Radio Broadcasting | ||

| OTT / Streaming Channels | ||

| Cable and Satellite Channels | ||

| IPTV | ||

| Digital Signage and OOH | ||

| By End-User | Public Service Broadcasters | |

| Commercial Broadcasters | ||

| Pay-TV Operators | ||

| OTT Platforms | ||

| Production Houses and Studios | ||

| Sports and Live-Events Networks | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia and New Zealand | ||

| Rest of Asia Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the forecast value of the broadcast scheduling software market by 2030?

The market is projected to reach USD 5.35 billion by 2030, growing at a 17.26% CAGR.

Which deployment mode is expanding fastest?

Cloud-based SaaS solutions are forecast to grow at an 18.92% CAGR through 2030.

Which region shows the highest growth momentum?

Asia-Pacific is anticipated to post an 18.50% CAGR, outpacing all other regions.

Why are OTT platforms accelerating software demand?

OTT services need sophisticated scheduling to manage personalized feeds, multi-territory rights, and dynamic ad insertion simultaneously.

How do new FCC accessibility rules affect scheduling solutions?

Platforms must integrate captioning, audio descriptions, and automated compliance logs, prompting widespread software upgrades.

What is the main hurdle to replacing legacy on-prem schedulers?

High switching costs and deep integrations with existing traffic and billing systems slow migration to modern cloud alternatives.

Page last updated on: