Panama Management Consulting Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

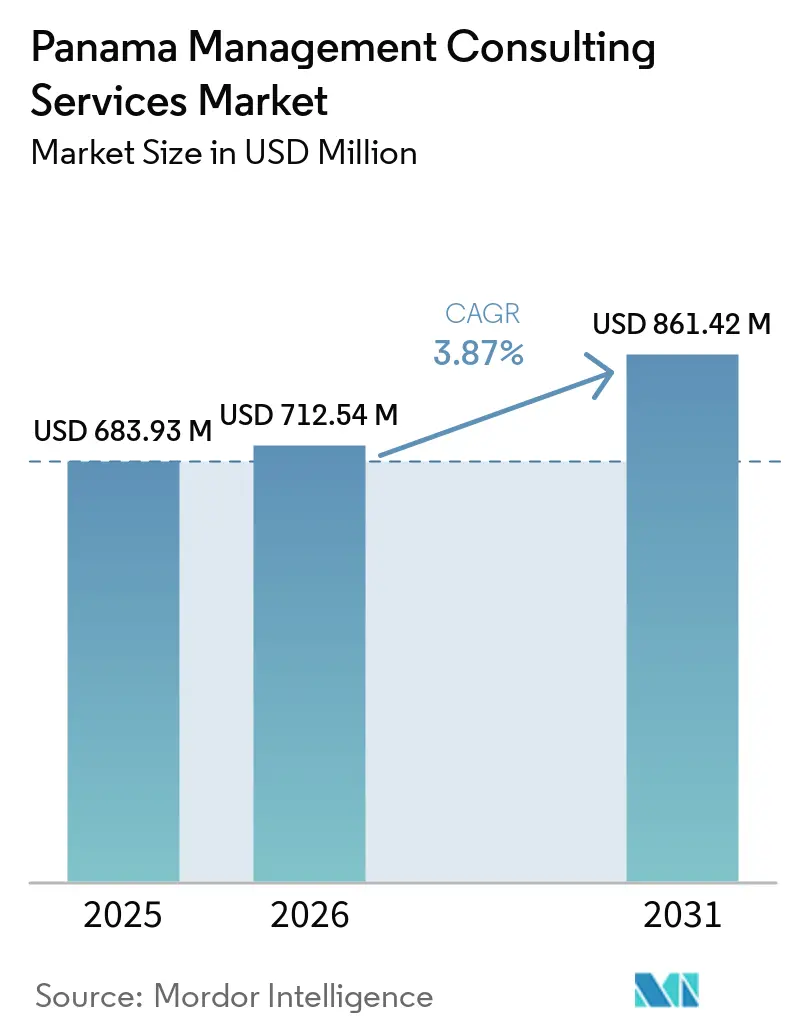

| Base Year Market Size (2025) | USD 683.93 Million |

| Market Size (2026) | USD 712.54 Million |

| Market Size (2031) | USD 861.42 Million |

| Growth Rate (2026 - 2031) | 3.87% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Panama Management Consulting Services Market Analysis by Mordor Intelligence

The Panama Management Consulting Services market size is projected to be USD 683.93 million in 2025, USD 712.54 million in 2026, and reach USD 861.42 million by 2031, growing at a CAGR of 3.87% from 2026 to 2031. The Panama Management Consulting Services market continues to benefit from the country’s role as a regional service hub, strong foreign direct investment in logistics and banking, and the government’s multi-billion-dollar digital transformation agenda. Demand is also reinforced by nearshoring of shared-service centers from North America, which values Panama’s dollarized economy and time-zone alignment. At the same time, public-sector fiscal tightening and SME budget constraints temper overall spending growth, encouraging firms to pursue hybrid delivery models that stretch consulting budgets. Competitive intensity remains moderate because global firms and regional boutiques coexist, each differentiating through either sector specialization or Spanish-language delivery, which sustains price discipline in the Panama Management Consulting Services market.

Key Report Takeaways

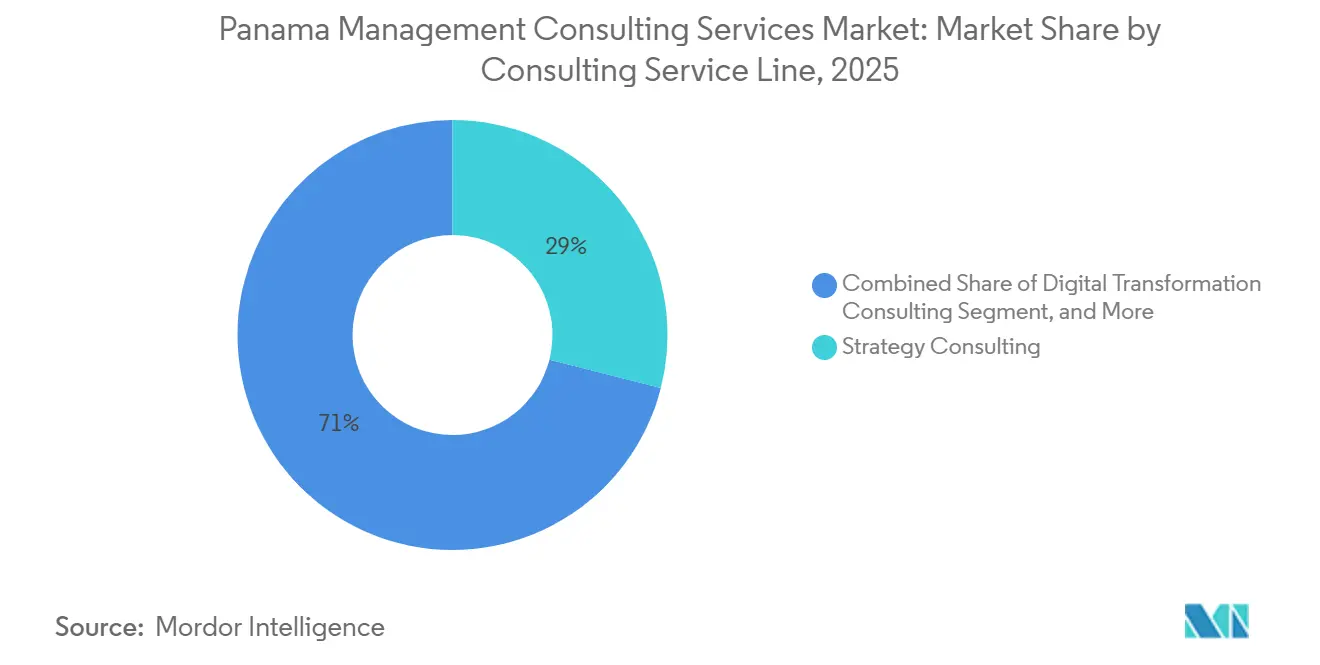

- By consulting service line, Strategy Consulting led with 28.97% revenue share in 2025, while Digital Transformation Consulting is forecast to expand at a 4.11% CAGR through 2031, reflecting clients’ accelerating shift toward cloud migration, automation, and analytics.

- By organization size, Large Enterprises held 60.89% of the Panama Management Consulting Services market share in 2025, whereas Small and Medium-Sized Enterprises are projected to grow at a 3.92% CAGR to 2031 as guarantee funds and fintech sandbox programs lower advisory entry barriers.

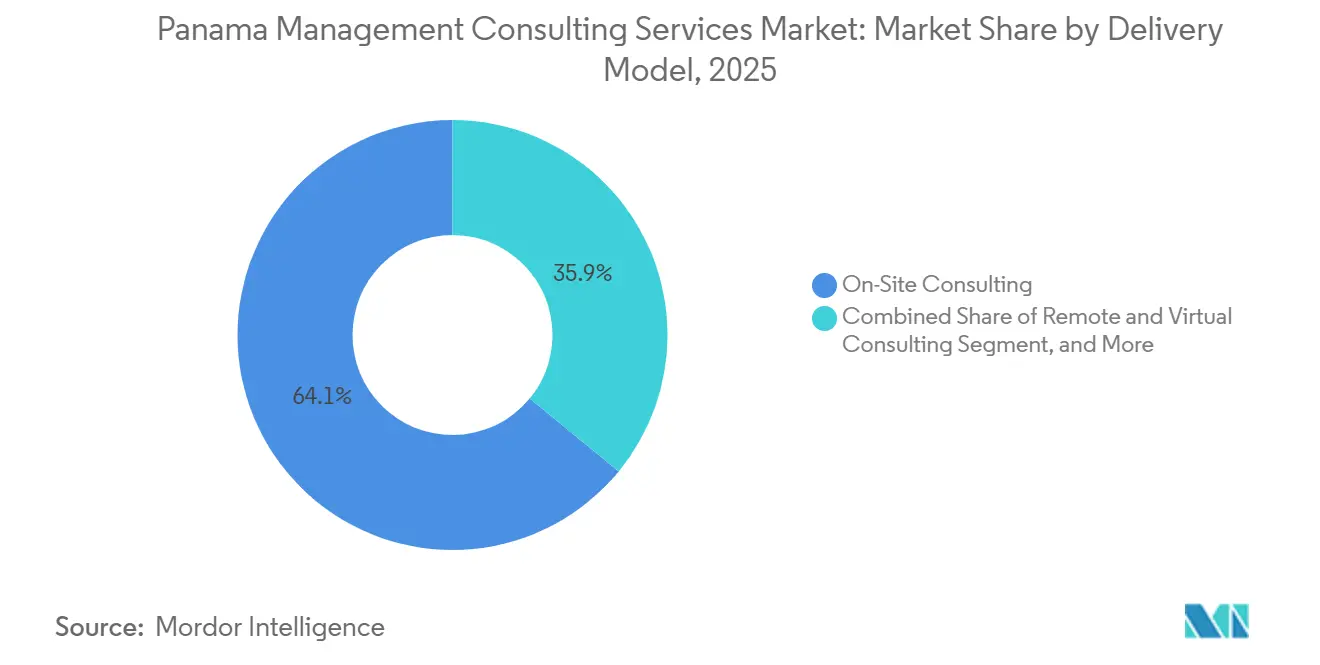

- By delivery model, On-Site Consulting accounted for 64.06% of the Panama Management Consulting Services market size in 2025, yet Hybrid Consulting is advancing at a 4.03% CAGR to 2031 because higher internet penetration supports mixed virtual and in-person engagement structures.

- By end user industry, Banking and Insurance commanded 22.14% of consulting revenue in 2025, while Healthcare is forecast to post the fastest 3.98% CAGR through 2031 due to the National Digital Health Strategy’s requirement for telemedicine and AI-enabled diagnostics.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Panama Management Consulting Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital Transformation Push Among Panama Enterprises | +1.2% | National, concentrated in Panama City, Colón Free Zone, Panama Pacifico | Medium term (2-4 years) |

| Growing FDI in Panama's Services Sector | +0.9% | National, spillover to Colón and Panama Pacifico special economic zones | Medium term (2-4 years) |

| Increasing Regulatory Complexity Post-OECD Grey-List Monitoring | +0.8% | National, especially financial services and multinational HQs | Long term (≥ 4 years) |

| Nearshoring of Shared-Service Centers from North America to Panama | +0.7% | Panama City, Panama Pacifico, Colón Free Zone | Medium term (2-4 years) |

| Rise of Sustainable-Finance Consulting Linked to Canal Decarbonization Goals | +0.5% | National, maritime and logistics corridors | Long term (≥ 4 years) |

| Surge in Panama's Fintech Sandbox Initiatives | +0.6% | National, centered in Panama City financial district | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Digital Transformation Push among Panama Enterprises

Inter-American Development Bank financing of USD 60 million in 2025 accelerated cloud adoption and process automation across ministries, creating multiyear pipelines for implementation, change management, and cybersecurity assignments. A 2025 KPMG survey showed 70% of regional executives prioritizing technology spending, a trend mirrored in banking and telecom clients that now request integrated cyber-risk and transformation roadmaps. The Ministry of Health mandate for interoperable electronic health records further widens opportunities for health-IT specialists.[1]Ministry of Health Panama, “National Digital Health Strategy 2025-2030,” Minsa.gob.pa Despite these positives, limited 5G coverage outside Panama City caps demand for edge-computing advisory, keeping most work concentrated in the capital.

Growing FDI in Panama’s Services Sector

Services exports hit PAB 14.8 billion (USD 14.8 billion) during the first nine months of 2025, attracting headquarters that rely on tax structuring, transfer pricing, and organizational design consulting.[2]National Institute of Statistics and Census Panama, “Services Export Data 2025,” Inec.gob.pa Incentives under the SEM and EMMA regimes, which apply 5% income tax and dividend exemptions, have positioned Panama as an alternative to Miami for regional command centers. Companies such as Prodapt expanded nearshore delivery operations in 2025, generating spin-off projects in talent sourcing, vendor management, and IT integration. Perceived corruption, however, forces consultancies to allocate additional hours to enhanced due diligence, lifting project costs.

Increasing Regulatory Complexity Post-OECD Grey-List Monitoring

Panama’s OECD accession committee, launched in 2026, commenced reviews of tax transparency and beneficial-ownership rules that drive demand for compliance gap assessments and process re-engineering. Agreement 1-2026 obliges banks to enhance anti-money-laundering protocols, spurring system upgrades and staff training led by consulting teams.[3]Superintendency of Banks of Panama, “Agreement 1-2026,” Superbancos.gob.pa Fintech draft bills under legislative debate have made advisory on crypto and digital-wallet compliance a growth area for early movers.

Nearshoring of Shared-Service Centers From North America to Panama

Prodapt’s enlarged Panama hub illustrates how shared-service relocations convert into market-entry studies, site selection, and workforce planning assignments. Panama Pacifico offers tax and customs incentives but still requires consultancies to navigate labor laws and vendor ecosystems for incoming multinationals\. New free-zone announcements keep advisory pipelines active even as final project timelines hinge on public-infrastructure delivery.[4]Government of Panama, “DINAMICA II Program,” Gob.pa

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Availability of Skilled Consultants in Niche Domains | -0.6% | National, acute in cybersecurity, sustainable finance, analytics | Medium term (2-4 years) |

| Budget Constraints Among SMEs Amid Economic Slowdowns | -0.5% | National, stronger outside Panama City | Short term (≤ 2 years) |

| Cultural Preference for In-House Decision-Making in Family Conglomerates | -0.3% | National | Long term (≥ 4 years) |

| Fragmented Procurement Processes Within Public Sector | -0.4% | National, all ministries | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited Availability of Skilled Consultants in Niche Domains

Cybersecurity and sustainable-finance expertise remain scarce, forcing firms to import talent from Colombia and Mexico at premium rates, which inflates project budgets and elongates sales cycles. The NetZero Slot program has created immediate demand for maritime decarbonization skills, yet fewer than a dozen local practitioners cover this domain.[5]Panama Canal Authority, “NetZero Slot Incentive,” Pancanal.com

Budget Constraints Among SMEs Amid Economic Slowdowns

SMEs represent 97% of businesses but only 17% of GDP, and limited collateral narrows credit lines, compressing consulting spend, even after the IDB’s USD 150 million guarantee fund became available in 2025.[6]Inter-American Development Bank, “IDB Approves USD 60 Million to Strengthen Digital Government in Panama,” IADB.org Uptake of the DINAMICA II digital support fund remains modest because application complexity discourages smaller firms.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Consulting Service Line: Digital Transformation Accelerates

Digital Transformation Consulting contributed the fastest expansion within the Panama Management Consulting Services market, and its 4.11% projected CAGR is set to reshape revenue mix. The Panama Management Consulting Services market size linked to this segment aligns with health-IT rollouts mandated by the National Digital Health Strategy, which alone covers telemedicine, AI diagnostics, and interoperable records. Clients increasingly bundle change management, cybersecurity, and data governance into single statements of work, nudging traditional strategy houses to deepen technical capacity.

At the same time, Strategy Consulting still maintains the largest 28.97% slice of Panama Management Consulting Services market share because M and A due diligence and regional expansion moves remain board-level priorities. Financial Advisory activity tied to Davivienda’s USD 60 billion regional integration shows that valuation, synergy mapping, and regulatory alignment cannot be commoditized quickly. Operations and HR practices stay relevant in free-zones where lean manufacturing, incentive compliance, and bilingual talent acquisition keep demand positive.

By Organization Size: SME Momentum Builds

Large Enterprises dominated spending, yet the Panama Management Consulting Services market size attributable to SMEs is forecast to expand steadily owing to public guarantee schemes and sandbox programs that lower advisory entry barriers. Fintech pilots involving reg-tech and customer-experience redesign often tap boutique consultancies that can deliver short, cost-effective sprints. Hybrid engagement models, which blend virtual analytics with two-to-three in-person workshops, resonate with SME cash-flow realities.

Budget sensitivity persists, but the DINAMICA II seed capital program and multilateral technical-assistance grants gradually unlock higher-value scopes, such as digital storefront enablement and inventory optimization. Global firms pursue a land-and-expand strategy by offering pro-bono diagnostics that convert into paid follow-up work once financing closes, indirectly lifting SME penetration in the Panama Management Consulting Services market.

By Delivery Model: Hybrid Engagement Rises

On-Site Consulting remains the dominant method because executive workshops and sensitive strategy sessions still require physical presence. The Panama Management Consulting Services market size attached to this model, however, is losing share to hybrid approaches as clients embrace video conferencing and cloud collaboration for documentation and analytics. Higher broadband coverage, 78% in 2025, plus digital nomad visa policies give both clients and consultants flexibility.

Hybrid projects typically start with a kick-off week held in client offices, move to remote data work, and close with an on-site sprint to finalize implementation, cutting lodging and travel outlays by up to 25%. Remote-only delivery stabilizes as a niche option for compliance training and post-go-live support. Big Four firms promote proprietary portals that allow clients to track milestones in real time, while boutiques differentiate through Spanish-language, evening-hour availability for U.S. clients.

By End User Industry: Healthcare Gains Velocity

Banking and Insurance is the single largest consumer of advisory services due to anti-money-laundering upgrades and platform modernization, but the Ministry of Health’s digital roadmap gives Healthcare the momentum to be the fastest climber. The Panama Management Consulting Services market share for Healthcare is set to expand as hospitals and clinics outsource systems integration, change management, and vendor selection.

Telecommunications operators sustain spending on spectrum strategy, 5G rollouts, and cyber-resilience, while manufacturing entities in Colón and Panama Pacifico request supply-chain and lean assessments to preserve margins amid energy-price volatility. Renewable-energy developers engage consultants for project finance packaging and grid-compatibility assessments, benefiting from the Industrial Promotion Certificate tax credit that requires technical validation documentation.

Geography Analysis

Panama City anchors most engagements because it houses ministries, banks, and multinational headquarters that demand continuous advisory. The capital’s bilingual talent pool and fiber connectivity permit large project teams to work in agile sprints, compressing cycle times. Secondary hubs such as the Colón Free Zone and Panama Pacifico grow faster, driven by logistics trade and shared-service relocations that need regulatory, human-capital, and operational guidance.

The Colón Free Zone’s 3,000-plus firms fuel continuous supply-chain optimization mandates, especially as e-commerce exporters demand customs-compliance reviews and inventory analytics. Panama Pacifico’s incentives attract call centers and light manufacturers, spurring demand for labor-law audits and ERP rollouts. Emerging free-zone projects promise future pipelines, although historical delays in public infrastructure could defer engagement timing.

Beyond these corridors, provinces like Chiriquí and Veraguas see sporadic consulting linked to agribusiness modernization and renewable-energy feasibility studies. Utility-tariff consultations open specialized modeling work, yet travel logistics and smaller fee pools restrict the number of firms willing to bid. Corruption-perception risk and weaker contract enforcement still inflate due-diligence hours outside the capital, slowing deal velocity but not eliminating growth prospects.

Competitive Landscape

The Panama Management Consulting Services market hosts Big Four powerhouses, Deloitte, PwC, EY, and KPMG, alongside regional boutiques such as Sintec Consulting, Indra Business Consulting, and Panama Consulting Group. Global firms leverage international playbooks and sector depth, targeting bank digitization and cross-border tax structuring, while boutiques win mid-market work through flexible pricing and Spanish-language delivery. Capability expansion in digital transformation and ESG reporting is the strategic theme across tiers, exemplified by BDO Panama’s integration of analytics firm iThink and its 2026 IFRS sustainability role.

Technology adoption varies: leading firms deploy AI-enabled risk analytics and cloud-based portals that cut project turnaround, whereas smaller consultancies still depend on PowerPoint led project artifacts. Alliances are common; Versata Capital’s tie-in with M and A Worldwide opens cross-border deal flow that challenges Big Four transaction teams.

Regulation shapes demand patterns: Agreement 1-2026 and OECD accession steps push banks and multinational HQs to sign multiyear compliance retainers. Talent shortages in cybersecurity, sustainable finance, and advanced analytics allow niche experts to command premium rates, which partially offset price competition in commoditized offerings like basic tax compliance. MergersCorp’s 2026 pivot into corporate finance advisory underscores how new entrants merge investment banking skills with classic management consulting, blurring competitive lines.

Panama Management Consulting Services Industry Leaders

Deloitte Consulting

PwC Advisory Services

Ernst and Young (EY) Advisory

KPMG Advisory

Accenture Strategy

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: MergersCorp M and A International expanded into full-scale corporate advisory and investment banking services, targeting middle-market businesses with 30 multidisciplinary offerings.

- March 2026: Panama established an OECD accession committee to coordinate alignment with global standards, creating a sustained pipeline for risk and compliance engagements.

- January 2026: Calibore launched a partner-led M and A advisory practice with offices in New York, London, Vienna, and Panama, focusing on cross-border transactions for family-owned entities.

- December 2025: Davivienda completed the USD 60 billion integration of Scotiabank operations across Colombia, Costa Rica, and Panama, sparking post-merger consulting around technology consolidation.

Panama Management Consulting Services Market Report Scope

The Panama Management Consulting Services Market Report is Segmented by Consulting Service Line (Strategy Consulting, Operations Consulting, HR Consulting, Financial Advisory Consulting, Digital Transformation Consulting, Risk and Compliance Consulting, and Other Consulting Service Lines), Organization Size (Large Enterprises, and Small and Medium-Sized Enterprises), Delivery Model (On-Site Consulting, Remote and Virtual Consulting, and Hybrid Consulting), End User Industry (IT and Telecommunications, Manufacturing, Energy and Resources, Public Sector, Healthcare, Banking and Insurance, and Other End User Industries), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Strategy Consulting |

| Operations Consulting |

| HR Consulting |

| Financial Advisory Consulting |

| Digital Transformation Consulting |

| Risk and Compliance Consulting |

| Other Consulting Service Lines |

| Large Enterprises |

| Small and Medium-Sized Enterprises |

| On-Site Consulting |

| Remote and Virtual Consulting |

| Hybrid Consulting |

| IT and Telecommunications |

| Manufacturing |

| Energy and Resources |

| Public Sector |

| Healthcare |

| Banking and Insurance |

| Other End User Industries |

| By Consulting Service Line | Strategy Consulting |

| Operations Consulting | |

| HR Consulting | |

| Financial Advisory Consulting | |

| Digital Transformation Consulting | |

| Risk and Compliance Consulting | |

| Other Consulting Service Lines | |

| By Organization Size | Large Enterprises |

| Small and Medium-Sized Enterprises | |

| By Delivery Model | On-Site Consulting |

| Remote and Virtual Consulting | |

| Hybrid Consulting | |

| By End User Industry | IT and Telecommunications |

| Manufacturing | |

| Energy and Resources | |

| Public Sector | |

| Healthcare | |

| Banking and Insurance | |

| Other End User Industries |

Key Questions Answered in the Report

What is the current Panama Management Consulting Services market size and its projected value by 2031?

The Panama Management Consulting Services market size stands at USD 683.93 million in 2025, is set to reach USD 712.54 million in 2026, and is forecast to climb to USD 861.42 million by 2031.

Which consulting service line is expected to grow fastest in Panama through 2031?

Digital Transformation Consulting is projected to record the quickest rise, expanding at a 4.11% CAGR as organizations prioritize cloud, automation, and analytics projects.

Why are SMEs becoming a more attractive client segment for consultancies operating in Panama?

Government-backed guarantee funds and fintech sandbox initiatives lower financing and regulatory barriers, enabling more SMEs to engage advisory firms for digital and compliance needs.

How is the shift toward hybrid consulting changing project delivery in Panama?

Higher internet penetration allows consultants to mix on-site workshops with remote analytics sessions, reducing travel costs and widening access to expert talent.

What factors are driving demand for compliance and risk advisory services?

Panama's OECD accession process and new anti-money-laundering regulations compel banks and multinational headquarters to upgrade governance frameworks, fueling multiyear compliance engagements.

Which end-user industry outside finance is showing the strongest consulting growth potential?

Healthcare is set for the fastest expansion, driven by the Ministry of Health's 2025-2030 digital strategy that mandates telemedicine and AI-enabled diagnostic systems.

Page last updated on: