Oman Cybersecurity Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

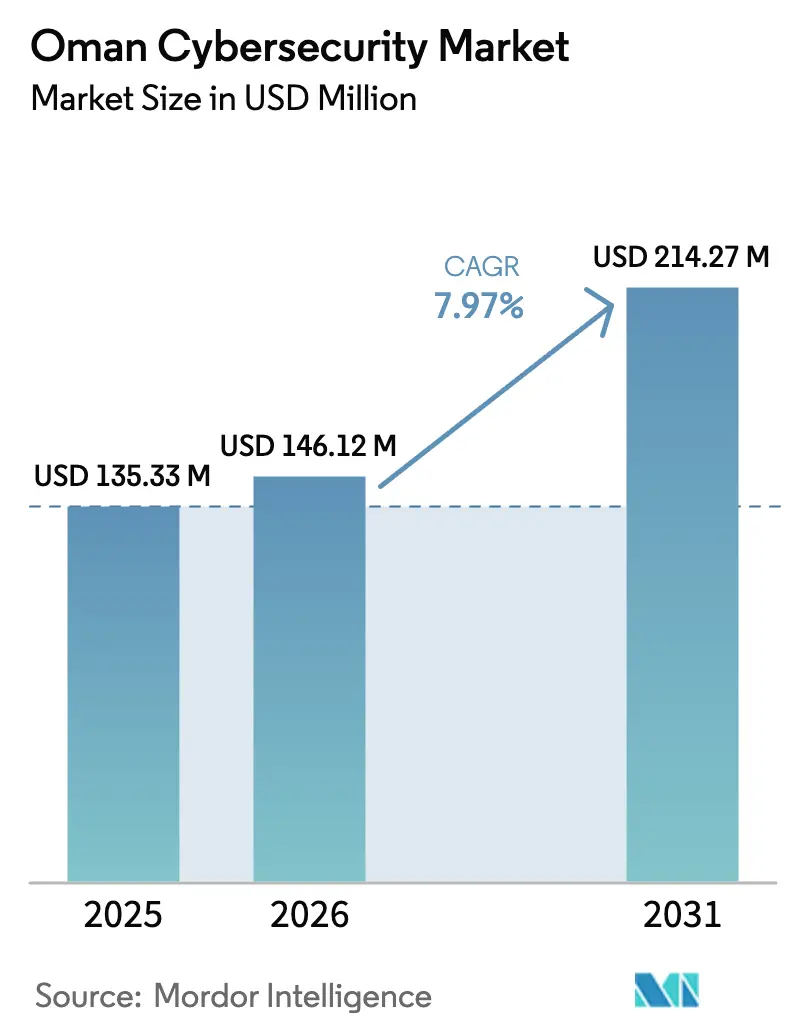

| Base Year Market Size (2025) | USD 135.33 Million |

| Market Size (2026) | USD 146.12 Million |

| Market Size (2031) | USD 214.27 Million |

| Growth Rate (2026 - 2031) | 7.97% CAGR |

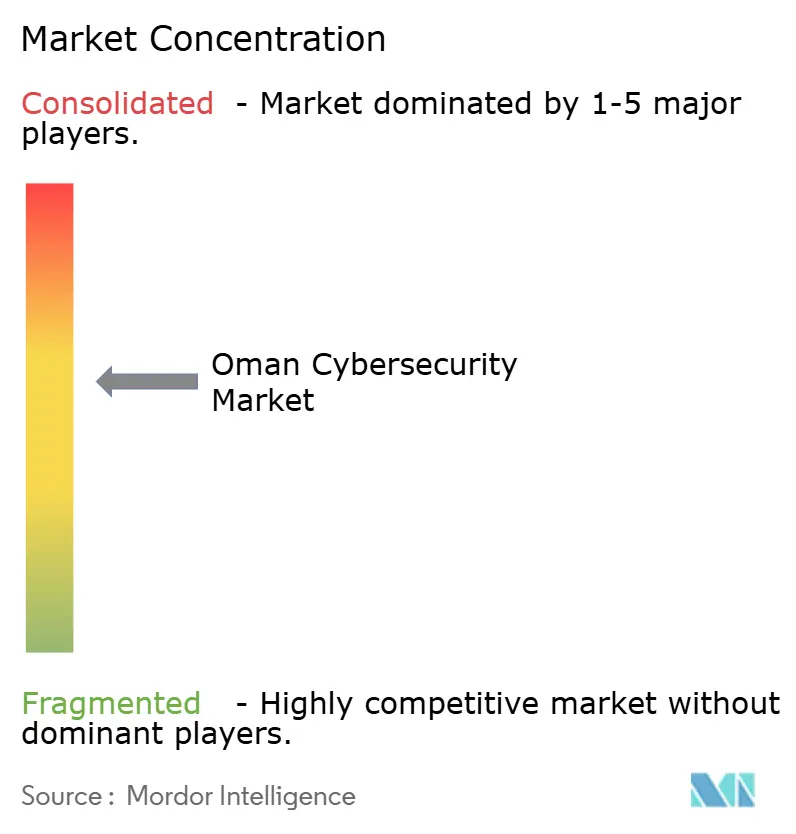

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Oman Cybersecurity Market Analysis by Mordor Intelligence

The Oman cybersecurity market size is expected to grow from USD 135.33 million in 2025 to USD 146.12 million in 2026 and is forecast to reach USD 214.27 million by 2031 at 7.97% CAGR over 2026-2031. Adoption is accelerating as Vision 2040 programs mandate “security by design” for every new public-sector workload, while enterprises digitize supply chains and customer channels. Mandatory data-residency rules channel fresh capital toward domestic data centers and sovereign cloud zones, stimulating vendor partnerships and managed security uptake. Rapid port automation, open-banking APIs, and green-hydrogen investments expand the threat surface, prompting sector-specific spending that now spans perimeter controls, identity governance, and OT-security platforms. Combined with Oman's second-place ranking for cybersecurity readiness in the Arab world, these factors anchor a demand curve that moves from tactical contracts to multi-year frameworks.

Key Report Takeaways

- By offering, services led with 67.92% of the Oman cybersecurity market share in 2025; managed security services are advancing at a 13.78% CAGR through 2031.

- By deployment mode, on-premise held 59.68% of the Oman cybersecurity market size in 2025, while cloud security is projected to expand at 17.16% CAGR.

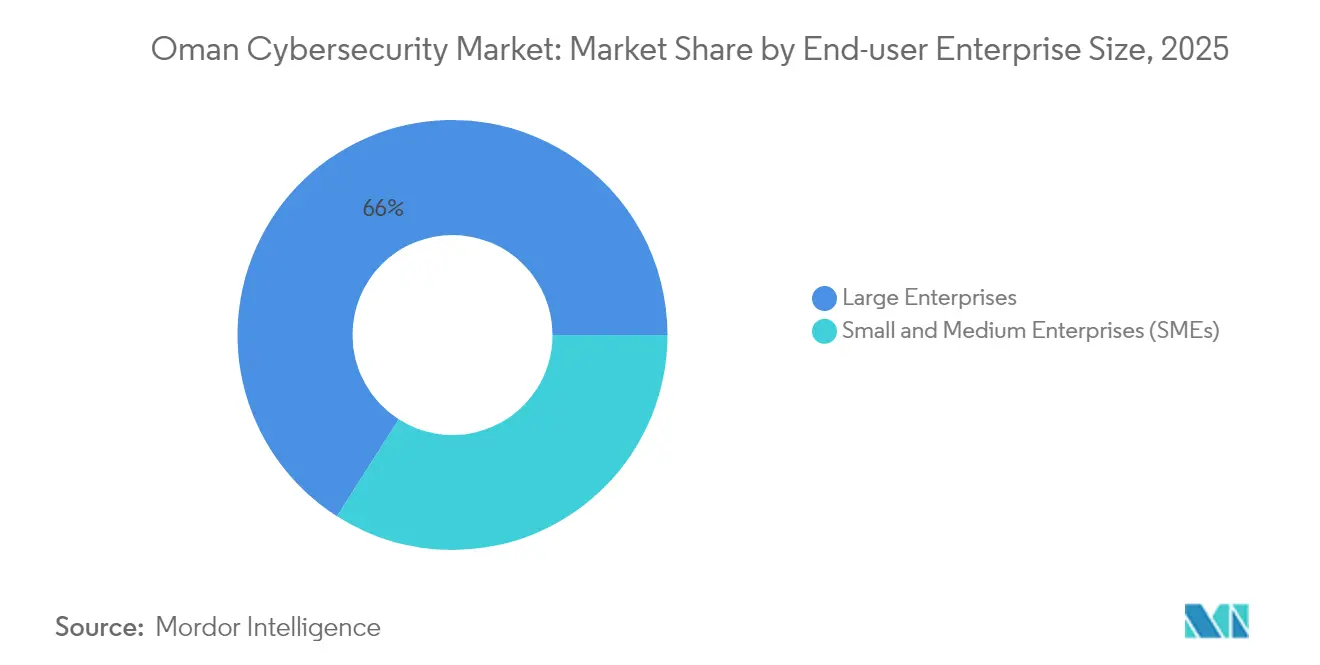

- By end-user enterprise size, large enterprises captured 65.97% of the Oman cybersecurity market share in 2025; SMEs post the highest 18.05% CAGR to 2031.

- By end user, BFSI commanded 29.45% of revenue in 2025; healthcare is set to grow fastest at a 18.74% CAGR through 2031.

- Microsoft, Cisco, Fortinet, Oman Data Park, and National Security Services Group collectively held about 48.52% of 2024 revenue.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Oman Cybersecurity Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Oman Vision 2040 digital-government projects | +2.1% | National, Muscat focus | Medium term (2-4 years) |

| Mandatory data-residency rules | +1.8% | National | Short term (≤ 2 years) |

| Accelerated IIoT roll-outs at Sohar and Duqm ports | +1.2% | Sohar, Duqm | Medium term (2-4 years) |

| Surging mobile-money and open-banking APIs | +1.0% | National, urban hubs | Short term (≤ 2 years) |

| Green-hydrogen assets designated as critical infrastructure | +0.9% | Industrial zones | Long term (≥ 4 years) |

| National cyber-drill program | +0.4% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Oman Vision 2040 Digital-Government Projects

The Ministry of Transport, Communications and Information Technology is migrating hundreds of workloads to a sovereign government cloud, including a recent shift of 2 000 users at four agencies onto Microsoft 365 with advanced threat-protection features.[1]International Telecommunication Union, “Global Cybersecurity Index 2024,” itu.int Each migration requires vulnerability assessment, identity federation, and 24×7 monitoring, which expands contract scopes for local integrators. Cloud-native security budget lines are now embedded in every public-sector digital tender, ensuring predictable demand. Joint working groups coordinate baseline controls, reducing duplicated effort and speeding approvals. The predictable rollout cadence allows vendors to align capacity with project milestones, smoothing quarterly revenue.

Mandatory Data-Residency Rules

The Personal Data Protection Law obliges critical data to remain physically inside Oman, steering investments toward in-country racks and domestic Security Operations Centers. Omantel’s partnership with AWS to build a sovereign cloud region illustrates how telecom providers and hyperscalers localize compute while satisfying regulators.[2]Noventiq, “Noventiq Migrates Four Omani Government Entities to Microsoft 365,” noventiq.com Enterprises cite lower legal risk, latency benefits, and simplified audits as reasons for preferring local hosting, which amplifies hardware refresh cycles. Providers offering tier-III facilities and Arabic-language SOC dashboards report higher win ratios, as compliance officers rank residency guarantees alongside price. This environment raises entry barriers for offshore-only vendors, indirectly consolidating market share around players with Omani real estate.

Accelerated IIoT Roll-outs at Sohar and Duqm Ports

Smart cranes, sensors, and predictive-maintenance agents proliferate across the two gateway ports, linking OT traffic to corporate IT networks. More than 70% of deployed IoT devices ship without native encryption, exposing command packets to interception.[3]Muscat Daily, “Omantel, AWS to Establish Sovereign Cloud Region in Oman,” muscatdaily.comOperators respond by installing whitelisting-based intrusion systems such as StationGuard that secure IEC-61850 and Modbus frames without large learning windows.[4]OMICRON, “StationGuard for Utility Automation Security,” omicron.energyInsurance underwriters now request OT-segmentation evidence before covering cargo-handling downtime, translating cyber-architecture into financial leverage. As port authorities add hydrogen export terminals, new safety interlocks arrive bundled with embedded security modules, elevating unit-price averages.

Surging Mobile-Money and Open-Banking APIs

Banks account for 25% of the Oman cybersecurity market, and ISO 27001 certification is mandatory for all licensed institutions. Open-API initiatives facilitate instant payments but widen the attack surface, a trend confirmed by Kaspersky research that found 58% of Omani consumers encountered fraud attempts. Financial service providers layer tokenization, dynamic risk scoring, and secure API gateways to contain threats. Behavioral-biometric pilots cut false positives in real-time by tracking swipe cadence and device tilt. Vendor roadmaps increasingly bundle CIAM modules with anti-fraud analytics, lifting total contract value.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cyber-talent shortfall | –1.5% | National | Short term (≤ 2 years) |

| Fragmented government procurement | –1.0% | National, government sector | Medium term (2-4 years) |

| Global OEM supply-chain concerns | –0.8% | National | Medium term (2-4 years) |

| Low cyber-insurance penetration | –0.5% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cyber-Talent Shortfall

The Advanced Cybersecurity Academy, established with Thales, graduates 150 professionals each year, yet vacancy postings in Muscat alone exceed 400 roles. Salary premiums reach 25% above regional averages, stretching IT budgets. Organisations offset gaps by outsourcing tier-one monitoring to managed security services, but complex investigations still require in-house expertise, creating bottlenecks. Delays in tuning SIEM rules extend compliance timelines, particularly for new ISO audits. Vendors embed low-code orchestration to trim manual triage hours, partially easing the constraint.

Fragmented Government Procurement

Over 70 ministries and agencies hold individual tenders that rarely share technical templates, forcing suppliers to re-enter due-diligence data for each bid. Contract finalisation can slip by six months, deferring cash flow and raising bid-management costs. A pilot framework agreement covering Microsoft 365 migrations shows early success, yet broader standardisation progresses slowly. Inconsistent baseline controls also create integration overhead once inter-agency data exchange goes live. Integrators with presales teams fluent in public-sector compliance score higher on shortlists, but overall transaction friction still suppresses volume.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Services Gain Momentum Amid Talent Scarcity

Services revenue in the Oman cybersecurity market is rising at 13.78% CAGR, underpinned by demand for managed detection and response that compensates for staffing shortages. Oman Data Park bundles Fortinet Secure SD-WAN and SOC monitoring into fixed-fee packages, simplifying procurement for mid-market buyers. Network firewalls and cloud posture-management tools remain the largest solution categories, but identity governance and data-centric security grow fastest as zero-trust policies spread. Professional services maintain double-digit expansion because compliance audits and red-team exercises require certified expertise. Managed services convert once-off projects into recurring revenue streams, boosting lifetime value.

The solutions slice, while slower, still commands 32.08% of 2025 revenue. Buyers modernise perimeter stacks with deep-packet inspection and web-application firewalls that recognise Arabic script. Endpoint platforms shift toward AI-driven behavioural detection, fitting remote-work priorities. As sovereign clouds proliferate, customers favour toolsets that deploy identically across virtual machines and physical racks, reducing learning curves and configuration drift. Operator feedback suggests that solution refresh cycles now align with three-year OPEX budgets rather than five-year CAPEX timelines, accelerating churn in legacy appliances.

By Deployment Mode: Hybrid Architectures Dominate Roadmaps

On-premise assets accounted for 59.68% of the Oman cybersecurity market size in 2025, supported by compliance obligations in government and critical infrastructure. Nonetheless, cloud security revenue is forecast to climb 17.16% CAGR as sovereign regions remove data-location barriers. The launch of Oman Data Park’s Amazon Outposts service allows regulated entities to maintain workload sovereignty while accessing cloud elasticity. Early adopters consolidate logging into cloud-native SIEMs that deliver instant correlation without hardware constraints.

Hybrid scenarios prevail; operators keep SCADA workloads behind air-gaps yet run analytics and DevOps pipelines in sovereign zones. Investors cite lower upfront costs and quicker procurement as drivers for this hybrid shift. Tool vendors respond with licensing models that track workload units rather than CPU sockets, smoothing audits. Buyers judge success on time-to-patch metrics and cross-domain policy enforcement rather than historical gadget counts, reflecting maturing security operations.

By End-user Enterprise Size: SMEs Accelerate, Enterprises Sustain Bulk Spend

Large enterprises held 65.97% of the Oman cybersecurity market share in 2025, anchored by banks, oil-and-gas majors, and telecom incumbents. These groups execute multi-year roadmaps covering threat hunting, OT-security, and cyber-range simulation. Their procurement cycles favour platform providers offering integrated dashboards, thereby raising switching costs. Enterprise pilots of generative-AI detection engines influence vendor roadmaps, with trickle-down features scheduled for small business editions within two release cycles.

SMEs expand at 18.05% CAGR because Vision 2040 incentives push digitisation of invoicing and customer portals across retail, hospitality, and logistics. The Oman Technology Fund issues seed grants that include compulsory cybersecurity budgets, embedding spend early in start-up journeys. Lightweight frameworks that map onto ISO 27001 but skip lengthy reporting attract owners who lack dedicated CISOs. Managed service bundles popular with SMEs include endpoint defence, secure email, and 24×7 hotline support, priced predictably to reduce cash-flow uncertainty.

By End User: BFSI Leads, Healthcare Surges

The BFSI sector retains the largest expenditure, accounting for 29.45% of the Oman cybersecurity market in 2025. Central Bank regulations enforce strong encryption, real-time fraud monitoring, and disaster-recovery audits, ensuring continuous refresh. Open-banking experiments spur deployment of API gateways with integrated runtime shielding and zero trust identity hooks. Banks also expand bug-bounty programs, rewarding external researchers for responsibly reporting vulnerabilities.

Healthcare clocks the fastest 18.74% CAGR through 2031 as hospitals digitise records and roll out telemedicine platforms. OQ’s partnership with Trend Micro demonstrates how energy-domain standards influence hospital OT-security design. Medical administrators invest in micro-segmentation to quarantine diagnostic devices, curbing lateral movement in the event of ransomware. Regional insurers pilot policy riders covering patient safety impacts, making documented cyber-controls a prerequisite for premium discounts.

Geography Analysis

Muscat remains the epicenter for the Oman cybersecurity market because ministries, the ITU Regional Cybersecurity Centre, and major banks co-locate there, concentrating expertise and budgets. Centralised decision making accelerates pilots, and vendor customer-success teams position near Knowledge Oasis offices to ensure rapid response. Capital-region universities funnel fresh graduates into SOC analyst roles, partly easing the talent crunch.

Sohar port is emerging as a security technology showcase, where industrial operators demand protocol-aware firewalls and sensor-level anomaly detection. The cyber-insurance community anchors premium tables to validated OT controls, integrating security engineering with financial planning. Vendor footprints in Sohar often include on-site spares depots to meet strict mean-time-to-repair clauses.

Duqm follows a similar trajectory as green-hydrogen and petrochemical hubs break ground. Each new production line embeds secure-by-default PLC templates, pushing orders for ruggedised network taps and passive-monitoring plates. Local colleges collaborate with manufacturers to tailor cybersecurity curricula around IEC-62443 standards, seeding a pipeline of OT-focused analysts. Over time, secondary cities copy these models, gradually flattening regional spending disparities.

Competitive Landscape

Global heavyweights such as Microsoft, Cisco, and Fortinet deliver broad portfolios that span perimeter, cloud, and analytics, giving them a combined 32% share of the Oman cybersecurity market in 2024. They localise threat-intelligence feeds to include Arabic language artefacts and open training hubs in Muscat to accelerate skill transfer. Compliance teams appreciate vendor roadmaps that align with ISO and NIST updates, fostering brand stickiness.

Local leaders Oman Data Park and National Security Services Group capture 16% share by pairing sovereign-cloud capacity with Arabic-language SOC dashboards. Their proximity to regulators trims project-approval cycles and positions them for advisory engagements when new mandates appear. Oman Data Park’s USD 450 million expansion into the Kemet Data Center extends cross-border redundancy that benefits Omani tenants pursuing multi-cloud resilience.

Boutique specialists including PureSquare and Potech carve out niches in privacy VPNs and AI risk assessment respectively, catering to organisations that prefer focused expertise. Strategic alliances remain the preferred growth lever; recent examples include Oman Data Park partnering with Seclore for data-centric protection and Omantel with AWS for sovereign cloud. MandA activity is poised to accelerate as Gulf conglomerates replicate the G42-CPX model to build end-to-end AI and security stacks, pointing to gradual consolidation over the decade.

Oman Cybersecurity Industry Leaders

Dell Technologies Inc.

IBM Corporation

Cisco Systems Inc.

Fortinet Inc.

Check Point Software Technologies Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Oman Data Park and ITHCA Group launched the Sultanate’s largest cloud system.

- February 2025: G42 acquired CPX to integrate cybersecurity into its AI value chain.

- January 2025: PureSquare opened offices in Saudi Arabia and the UAE to serve Gulf clients.

- October 2024: Oman Data Park signed a USD 450 million MoU with INTRO Technology for the Kemet Data Center.

Oman Cybersecurity Market Report Scope

The cybersecurity market's scope encompasses the revenues derived from solutions and services utilized across end-user industries. The analysis draws from a blend of secondary research and primary sources, providing a comprehensive view of the market. The market also delves into the key drivers and restraints shaping its growth trajectory.

The Oman cybersecurity market is segmented by offerings (solutions [application security, cloud security, data security, identity access management, infrastructure protection, integrated risk management, network security, end-point security, and other solution types] and services [professional services and managed services]), by deployment (On-premise, and cloud), by organization size (SMEs, large enterprises), by end-user vertical (BFSI, healthcare, IT and telecom, industrial and defense, retail, energy and utilities, manufacturing, and other end-user industries). The market sizes and forecasts are provided in terms of value in (USD) for all the above segments.

| Solutions | Application Security |

| Cloud Security | |

| Data Security | |

| Identity and Access Management | |

| Infrastructure Protection | |

| Integrated Risk Management | |

| Network Security | |

| End-point Security | |

| Services | Professional Services |

| Managed Services |

| Cloud |

| On-Premise |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| BFSI |

| Healthcare |

| IT and Telecom |

| Industrial and Defense |

| Retail and E-commerce |

| Energy and Utilities |

| Manufacturing |

| Others |

| By Offering | Solutions | Application Security |

| Cloud Security | ||

| Data Security | ||

| Identity and Access Management | ||

| Infrastructure Protection | ||

| Integrated Risk Management | ||

| Network Security | ||

| End-point Security | ||

| Services | Professional Services | |

| Managed Services | ||

| By Deployment Mode | Cloud | |

| On-Premise | ||

| By End-user Enterprise Size | Large Enterprises | |

| Small and Medium Enterprises (SMEs) | ||

| By End-user Industry | BFSI | |

| Healthcare | ||

| IT and Telecom | ||

| Industrial and Defense | ||

| Retail and E-commerce | ||

| Energy and Utilities | ||

| Manufacturing | ||

| Others | ||

Key Questions Answered in the Report

What is the projected value of the Oman cybersecurity market by 2031?

The market is expected to reach USD 214.27 million by 2031.

Which deployment mode is growing fastest?

Cloud-based security solutions are forecast to expand at a 17.16% CAGR between 2026 and 2031 as sovereign cloud regions mature.

Why are managed security services in high demand?

They offset the national shortage of certified professionals and provide 24×7 monitoring that many organisations cannot staff internally.

Which vertical posts the highest growth rate?

Healthcare leads with a 18.74% CAGR, driven by electronic records, telemedicine, and stringent patient-data regulations.

Page last updated on: