Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

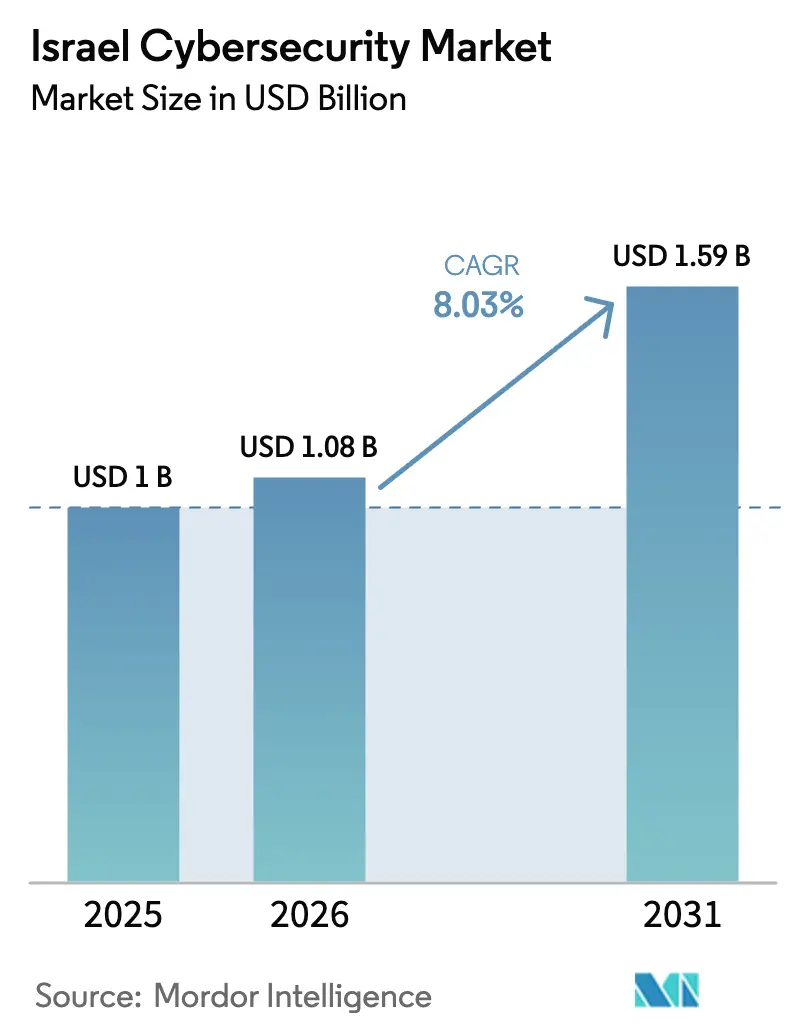

| Base Year Market Size (2025) | USD 1.0 Billion |

| Market Size (2026) | USD 1.08 Billion |

| Market Size (2031) | USD 1.59 Billion |

| Growth Rate (2026 - 2031) | 8.03% CAGR |

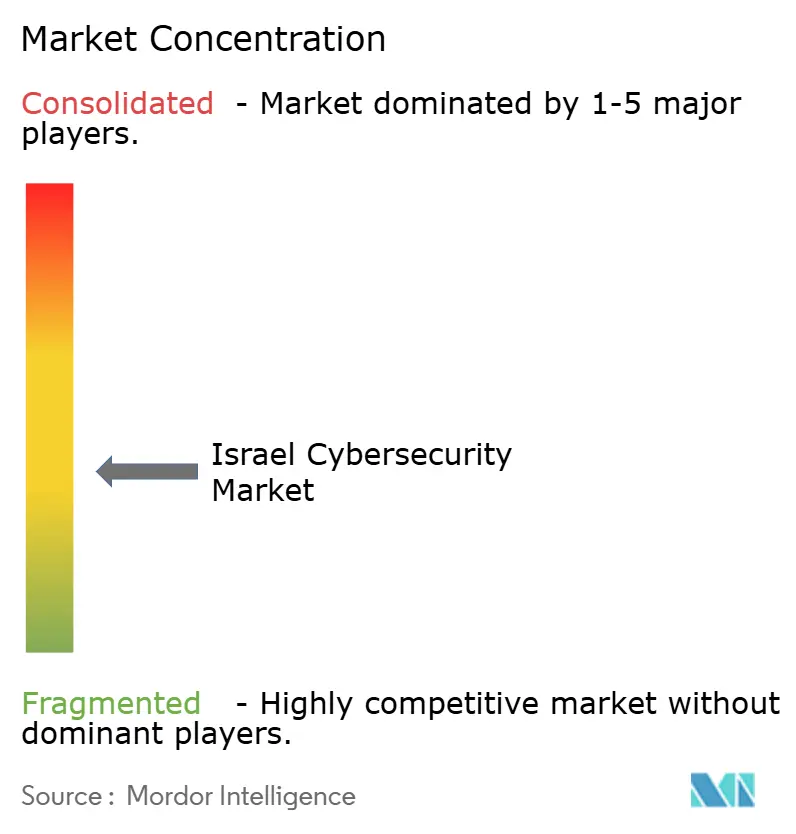

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Israel Cybersecurity Market Analysis by Mordor Intelligence

The Israel cybersecurity market size is expected to grow from USD 1.0 billion in 2025 to USD 1.08 billion in 2026 and is forecast to reach USD 1.59 billion by 2031 at 8.03% CAGR over 2026-2031. The national ecosystem maintains momentum by fusing elite military talent, substantial venture funding, and strict regulatory mandates that consistently translate battlefield-grade innovations into commercial products. Nearly 38% of total Israeli tech investment flowed into cybersecurity during 2024, underscoring the sector’s role as an economic safety net when macro headwinds curtail other verticals. Mandatory compliance programs led by the National Cyber Directorate, rapid cloud adoption, and a surge of AI-driven analytics ensure sustained enterprise purchasing even as budgets tighten elsewhere. Escalating regional conflict further drives real-time threat-detection demand, while government R&D incentives accelerate translation of academic research into industrial platforms. Collectively, these forces keep the Israel cybersecurity market on a steeper growth trajectory than the broader local digital economy.

Key Report Takeaways

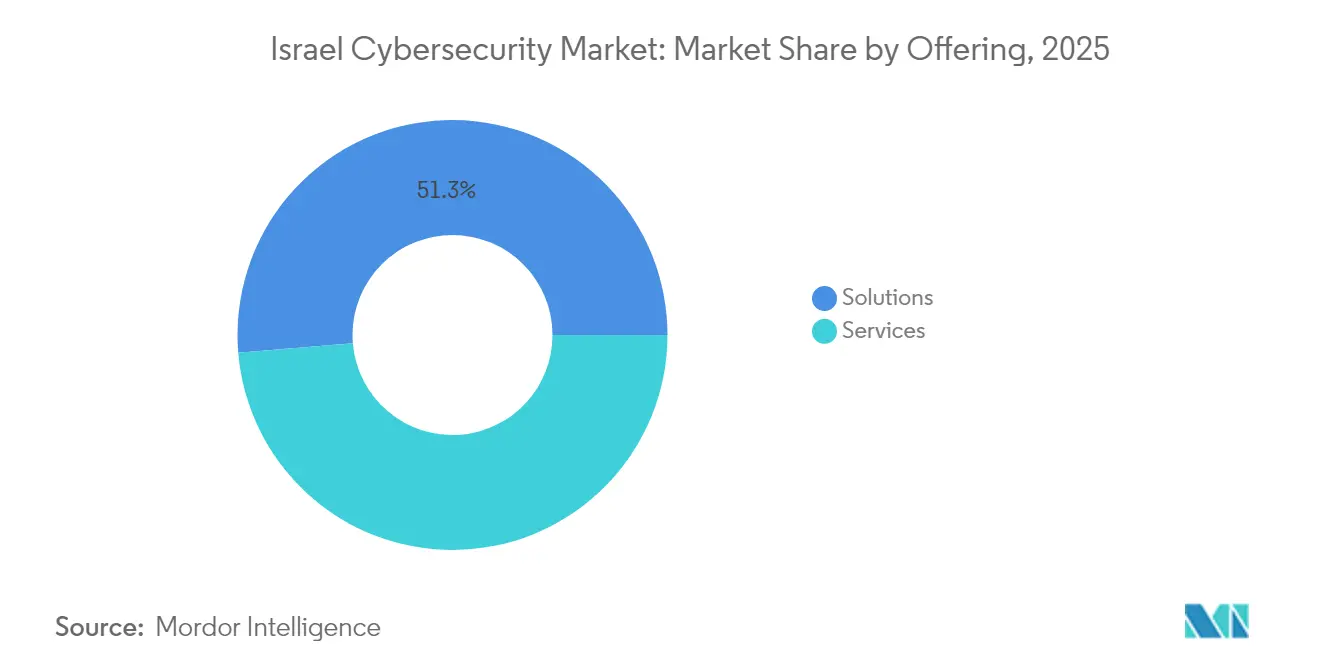

- By offering, solutions led with 51.32% revenue share of the Israel cybersecurity market in 2025, whereas services are forecast to grow at an 11.23% CAGR through 2031.

- By deployment mode, on-premise accounted for 60.45% of the Israel cybersecurity market share in 2025, yet cloud is advancing at a 14.62% CAGR to 2031.

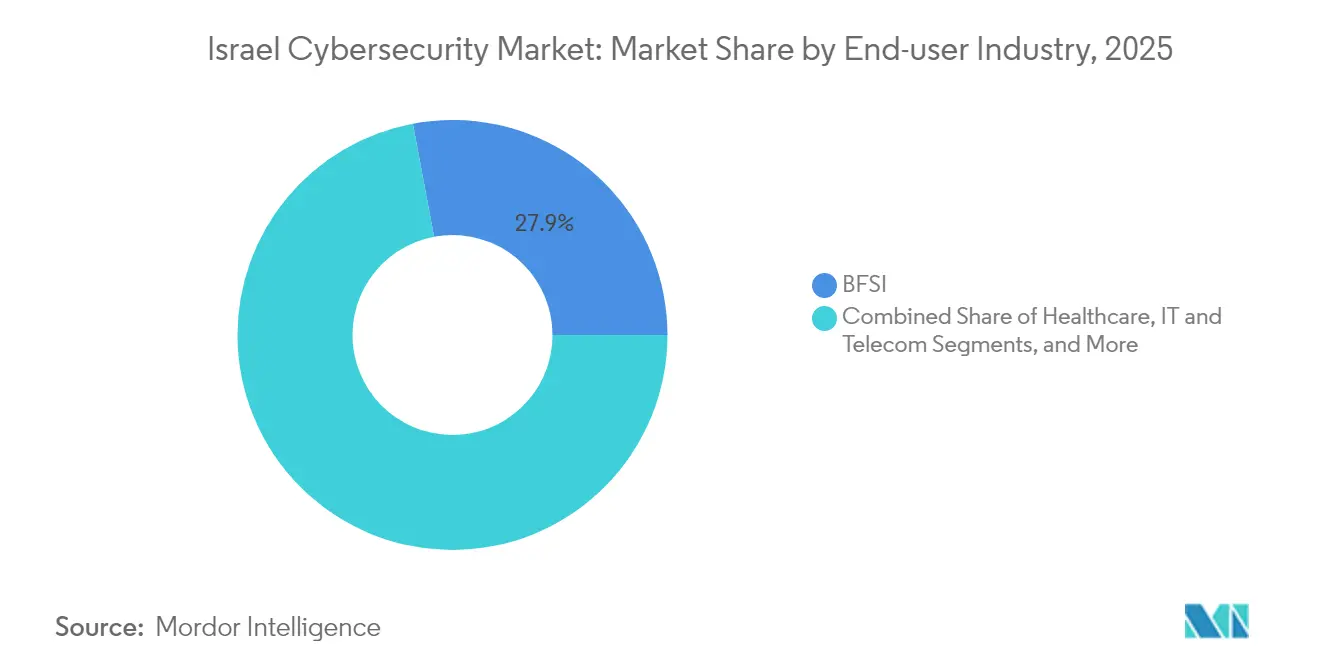

- By end-user industry, BFSI occupied 27.95% of 2025 revenue, whereas healthcare is poised to expand at an 8.14% CAGR through 2031.

- By end-user enterprise size, large enterprises held a dominant 70.55% share of the Israel cybersecurity market size in 2025 while SMEs represent the fastest-growing cohort at a 10.36% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Israel Cybersecurity Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| National Cyber Directorate compliance mandates | +1.9 | Nationwide (all critical-infrastructure sites) | Short term (≤ 2 years) |

| Vibrant start-up and venture funding | +1.6 | Tel Aviv–Herzliya start-up corridor | Medium term (2-4 years) |

| Rapid Enterprise Adoption of Cloud and IoT Platforms | +1.3 | Central District enterprise campuses | Medium term (2-4 years) |

| Geopolitical Tensions Driving Advanced Threat Activity | +1.0 | Northern and Southern border regions | Short term (≤ 2 years) |

| Export-Oriented Tech Sector’s Compliance Requirements | +0.8 | Greater Tel Aviv export hubs | Medium term (2-4 years) |

| Government R&D Incentives for Cyber Innovation | +0.7 | Beersheba CyberSpark and Jerusalem academic centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

National Cyber Directorate Compliance Mandates

The National Cyber Directorate introduced sector-wide rules that require real-time threat sharing, standardized incident reporting, and continuous monitoring across government, BFSI, and critical-infrastructure operators, forcing organizations to modernize SIEM, SOAR, and identity platforms in compressed timeframes. Since October 2023, coordinated defenses have neutralized roughly 800 major attacks, validating the centrally managed “cyber dome” strategy and anchoring near-term spending surges.

Vibrant start-up and venture funding environment

Cybersecurity startups raised USD 4 billion in 2024 across 75 deals, more than doubling 2023 totals and equal to 38% of overall tech funding, with headline rounds for Wiz and Cyera. Serial entrepreneurs recycle know-how into fresh ventures, compressing go-to-market cycles and spawning niche products in CNAPP, API security, and industrial IoT defense.

Rapid Enterprise Adoption of Cloud and IoT Platforms

Cloud deployments already account for over half of national security spend and are climbing at double-digit CAGR as enterprises pivot toward SaaS, edge computing, and connected-device ecosystems. Check Point’s Infinity platform posted double-digit growth in these domains, reflecting an appetite for elastic, centrally managed defenses.

Geopolitical Tensions Driving Advanced Threat Activity

Regional conflict elevates Israel to a front-line laboratory where sophisticated, state-linked threat actors stress-test local defenses. Check Point recorded a 44% YoY jump in global attacks during 2024, and many vectors specifically targeted Israeli government and commercial assets [1]Grace McDougal, “Check Point Announces New CEO & Reports Strong Q2 2024,” checkpoint.com. This accelerates customer interest in automated response, air-gapped OT protections, and AI-driven anomaly detection.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Severe cyber-talent shortage and wage inflation | −1.3 | Tel Aviv metropolitan labor pool | Medium term (2-4 years) |

| Tool sprawl and integration complexity | −0.7 | Nationwide enterprise SOCs | Short term (≤ 2 years) |

| SME budget constraints amid capital tightening | −0.4 | Peripheral cities and industrial parks | Short term (≤ 2 years) |

| Shekel volatility inflating imported hardware | −0.3 | Haifa tech-manufacturing corridor | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Severe cyber-talent shortage and wage inflation

Roughly 15% of local cybersecurity positions remain open; premium salaries run two-three times national tech averages, pressuring start-ups to expand offshore engineering hubs in Eastern Europe and Latin America. Distributed teams prolong release cycles and elevate operational risk, dampening sector growth prospects.

Tool sprawl and integration complexity

The average Israeli enterprise now manages more than 75 distinct security tools, complicating policy management and widening attack-surface blind spots. Vendors are pursuing acquisitions and platform roll-ups to streamline controls, but migration projects add near-term friction.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Solutions Hold Lead, Services Accelerate

Solutions captured 51.32% of 2025 revenue, as enterprises continued refreshing firewalls, endpoint detection, and data-protection suites. Spending emphasizes zero-trust network access, CNAPP, and advanced EDR where Israeli code heritage shines. Services, however, are projected to outpace solutions with an 11.23% CAGR through 2031, reflecting rising demand for managed detection, incident response, and continuous compliance monitoring.

Platform vendors now embed advisory and implementation services directly within subscription bundles, pushing hybrid revenue models. Incident-response retainer uptake increased sharply after the October 2023 attacks, as boards accepted the inevitability of compromise. Israeli consultancies leverage proximity to elite military units to offer red-team and threat-hunting engagements that global corporations seek for adversary simulation. This mix ensures services will gradually erode solution-only dominance while preserving vendor stickiness across the Israel cybersecurity market.

By Deployment Mode: Cloud Momentum Builds

On-premise deployment retained 60.45% share in 2025, driven by defense, energy, and payments workloads requiring deterministic latency and sovereignty controls. Yet cloud environments clock a 14.62% CAGR, adding the most absolute dollars through 2031. Large enterprises are increasingly adopting secure access service edge (SASE) and micro-segmentation to extend policy enforcement across multicloud estates.

Check Point’s CloudGuard Network Security reports 58% of its deployments among Fortune 1000 clients seeking consistent posture across AWS, Azure, and GCP. For Israeli SMEs, cloud-first security enables enterprise-grade defenses without hardware procurement, making OPEX-driven models attractive amid funding constraints. Consequently, hybrid orchestration layers—capable of toggling controls between data center and public cloud—have become a primary evaluation metric within vendor shortlists throughout the Israel cybersecurity market.

By End-user Industry: BFSI Leads, Healthcare Emerges

BFSI held 27.95% of 2025 revenue, retaining top spot due to stringent Bank-of-Israel guidance and evolving PSD2-style regulations. Fraud analytics, transaction monitoring, and machine-identity governance remain hot procurement areas. Healthcare, growing at an 8.14% CAGR, benefits from telemedicine adoption and new data-privacy obligations that compel encryption, asset-management, and PACS-security investments.

Industrial firms that manage critical infrastructure have also accelerated spending as the National Cyber Directorate enforces OT hardening standards. Vendors like Claroty leverage Israeli ICS research heritage to penetrate energy and water utilities. This sectoral diversification, underpinned by mandatory compliance and threat realism, sustains broad-based demand across the Israel cybersecurity market.

By End-user Enterprise Size: Large Enterprises Dominate, SMEs Gain Velocity

Large enterprises command 70.55% of 2025 spend, reflecting complex attack surfaces, regulatory audits, and budgetary heft. These organizations orchestrate multi-platform architectures spanning SIEM, SOAR, EDR, and threat-intel feeds, and increasingly pilot AI-assisted SOC automation. Yet SMEs record a 10.36% CAGR thanks to subscription bundles that disguise advanced detection under predictable monthly fees.

Israeli start-ups target this cohort with lightweight agents, automated policy templates, and outcome-based service-level agreements. For example, identity-security vendor CyberArk’s SaaS tier packages privileged session recording into an OpEx-friendly bundle, lowering entry barriers for mid-market finance and healthcare operators . This democratization broadens the customer base and supports long-term scale across the Israel cybersecurity market.

Geography Analysis

Tel Aviv continues to anchor roughly 70% of cybersecurity companies, benefitting from dense venture-capital networks, shared workspaces, and immediate adjacency to global banks’ innovation arms. The clustering enables rapid talent circulation and fosters informal knowledge exchange, propelling accelerated proof-of-concept cycles. Many multinationals locate regional R&D centers here, further enriching the talent pool and providing domestic start-ups with high-value acquisition pathways.

Beersheba, home to the CyberSpark campus, has become Israel’s industrial-cyber nexus. Military intelligence relocation to the Negev city seeded a crossover community where academic researchers, industrial-control vendors, and elite Unit 8200 veterans collaborate on OT anomaly detection. The government incentivizes southern expansion through tax breaks and grants, distributing economic activity and enhancing national resilience against concentrated physical attacks.

Jerusalem and Herzliya act as complementary micro-clusters. Jerusalem hosts encryption and quantum-security labs linked to Hebrew University, while Herzliya houses many early-stage SaaS start-ups targeting API and supply-chain security. Combined, these nodes create a geographically diversified innovation lattice that underwrites sustained export growth; Israeli vendors now direct more than 70% of revenue overseas, primarily to North America and Europe where regulatory similarity accelerates market entry.

Competitive Landscape

The Israel cybersecurity market houses a layered mix of incumbents and insurgents. CyberArk leads identity security after integrating Venafi’s machine-identity controls into its privileged-access platform, positioning it to address both human and non-human credentials. Check Point maintains end-to-end coverage from network to cloud, forecasting AI-enabled revenue boosts for 2025 after beating Q4 2024 analyst expectations.

Start-ups such as Wiz, valued at USD 23 billion in discussions with Google, typify Israel’s ability to scale cloud-native platforms rapidly [3]Rohan Goswami, “Google in Talks to Acquire Wiz for USD 23 Billion,” cnbc.com. Their appetite for hyper-growth pushes incumbents toward acquisition sprees; Tenable’s USD 150 million Vulcan Cyber purchase and Bitsight’s USD 115 million Cybersixgill buy illustrate portfolio-gap filling aimed at retaining enterprise relevance. Smaller specialists like Radware (DDoS), Claroty (OT), and Cybereason (EDR) target defensible niches where unique telemetry or patented heuristics confer durable advantage.

Market dynamics favor consolidation as customers demand integrated dashboards and unified policy engines. Nevertheless, low entry barriers for software innovation sustain continuous churn, with roughly 30 new cybersecurity start-ups launching annually. As a result, the competitive landscape balances moderate concentration with high velocity, keeping vendor roadmaps in perpetual motion and encouraging global players to tap Israel’s R&D ecosystem for inorganic growth.

Israel Cybersecurity Industry Leaders

CyberArk Software Ltd.

Cisco Systems, Inc.

Fortinet, Inc.

Radware Ltd.

IBM Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Cyberstarts, an Israeli venture capital fund, has unveiled a USD 300 million fund to assist its portfolio companies in attracting and retaining cybersecurity talent.

- July 2025: Germany and Israel are set to launch a joint initiative to bolster their defense collaboration with the establishment of a "Cyber Dome."

- January 2025: Tenable acquired Israeli exposure-management firm Vulcan Cyber for USD 150 million, adding remediation orchestration to its platform.

- November 2024: Silverfort bought Rezonate to extend cloud-identity protection across multi-cloud estates.

Israel Cybersecurity Market Report Scope

Cybersecurity refers to securing the services, products, and systems connected intra- and internet within or outside an organization. These services facilitate the end-to-end secure transfer of data and sensitive information, safeguarding the customers' interests from any potential cyber attack or threat. These include several solutions the companies offer for on-premise and cloud deployment of security products and services.

The Israel cybersecurity market is segmented by offerings (solutions [application security, cloud security, data security, identity access management, infrastructure protection, integrated risk management, network security, end-point security, and other solution types] and services [professional services and managed services]), by deployment (On-premise, and cloud), by organization size (SMEs, large enterprises), by end-user vertical (BFSI, healthcare, IT and telecom, industrial and defense, retail, energy and utilities, manufacturing, and other end-user industries). The market sizes and forecasts are provided in terms of value in (USD) for all the above segments.

By Offering

| Solutions | Application Security |

| Cloud Security | |

| Data Security | |

| Identity and Access Management | |

| Infrastructure Protection | |

| Integrated Risk Management | |

| Network Security | |

| End-point Security | |

| Services | Professional Services |

| Managed Services |

By Deployment Mode

| Cloud |

| On-Premise |

By End-user Industry

| BFSI |

| Healthcare |

| IT and Telecom |

| Industrial and Defense |

| Retail and E-commerce |

| Energy and Utilities |

| Manufacturing |

| Others |

By End-user Enterprise Size

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| By Offering | Solutions | Application Security |

| Cloud Security | ||

| Data Security | ||

| Identity and Access Management | ||

| Infrastructure Protection | ||

| Integrated Risk Management | ||

| Network Security | ||

| End-point Security | ||

| Services | Professional Services | |

| Managed Services | ||

| By Deployment Mode | Cloud | |

| On-Premise | ||

| By End-user Industry | BFSI | |

| Healthcare | ||

| IT and Telecom | ||

| Industrial and Defense | ||

| Retail and E-commerce | ||

| Energy and Utilities | ||

| Manufacturing | ||

| Others | ||

| By End-user Enterprise Size | Large Enterprises | |

| Small and Medium Enterprises (SMEs) | ||

Key Questions Answered in the Report

How large is the Israel cybersecurity market in 2026?

The Israel cybersecurity market size stands at USD 1.08 billion in 2026 and is projected to reach USD 1.59 billion by 2031 at an 8.03% CAGR.

Which segment grows fastest between 2026 and 2031?

Cloud deployment leads growth with a 14.62% CAGR as enterprises migrate workloads to multicloud and edge platforms.

Why is venture capital so concentrated in Israeli cybersecurity?

National defense expertise, repeat founders, and demonstrated export success attracted USD 4 billion in 2024 alone—38% of all Israeli tech funding.

What role does the National Cyber Directorate play?

The Directorate enforces real-time threat-sharing rules and standardized security controls across critical sectors, spurring immediate upgrades in SIEM, SOAR, and analytics platforms.

Page last updated on: