Qatar Cybersecurity Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

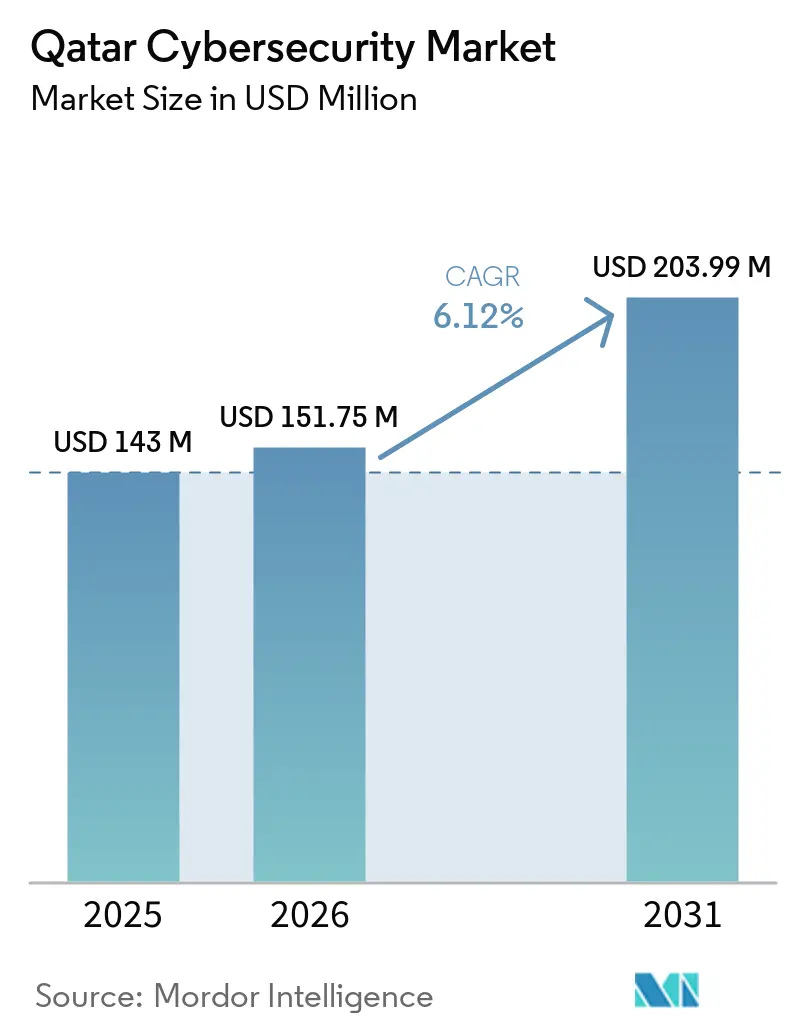

| Base Year Market Size (2025) | USD 143 Million |

| Market Size (2026) | USD 151.75 Million |

| Market Size (2031) | USD 203.99 Million |

| Growth Rate (2026 - 2031) | 6.12% CAGR |

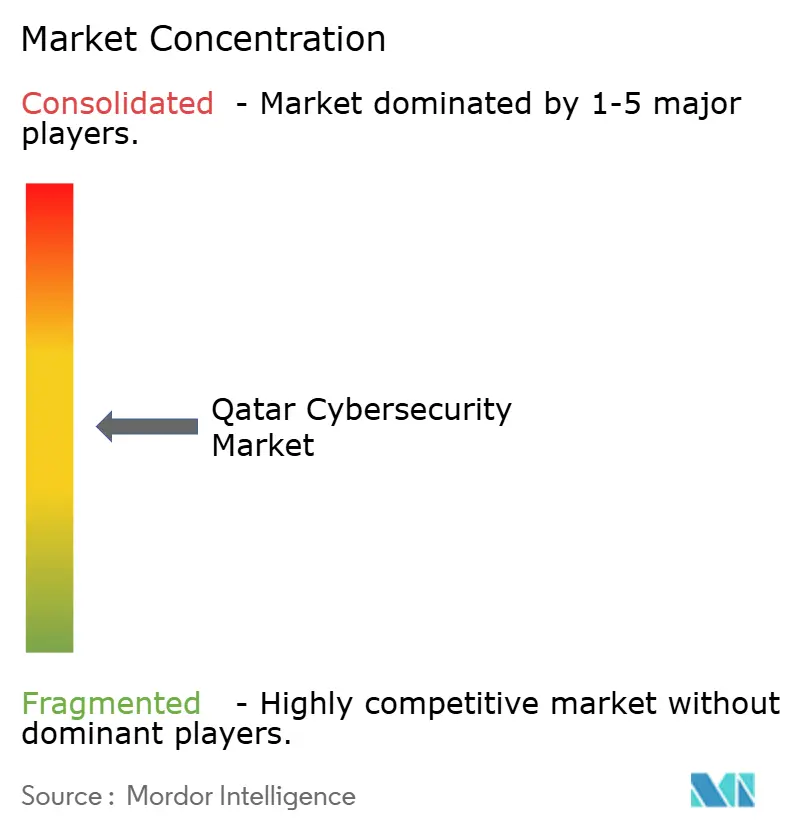

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Qatar Cybersecurity Market Analysis by Mordor Intelligence

The Qatar cybersecurity market size is projected to expand from USD 143 million in 2025 and USD 151.75 million in 2026 to USD 203.99 million by 2031, registering a CAGR of 6.12% over 2026-2031. The Qatar cybersecurity market is being shaped by state policy that treats cyber resilience as part of national governance, which ties spending to compliance and risk management. This direction is especially important in a market where government entities, sovereign enterprises, and regulated sectors set much of the purchasing pace. The Qatar cybersecurity market is also benefiting from broader digitization, driven by cloud-led public programs, smart infrastructure, and financial-sector modernization, which are expanding the number of systems that require protection. At the same time, the market remains exposed to industrial security pressure because energy assets and connected operational environments require specialized controls and managed oversight. Competition in the Qatar cybersecurity market, therefore, centers on vendors that can combine platform breadth, local delivery capability, and regulatory alignment, even as the shortage of specialized talent continues to raise service costs and stretch project timelines.

Key Report Takeaways

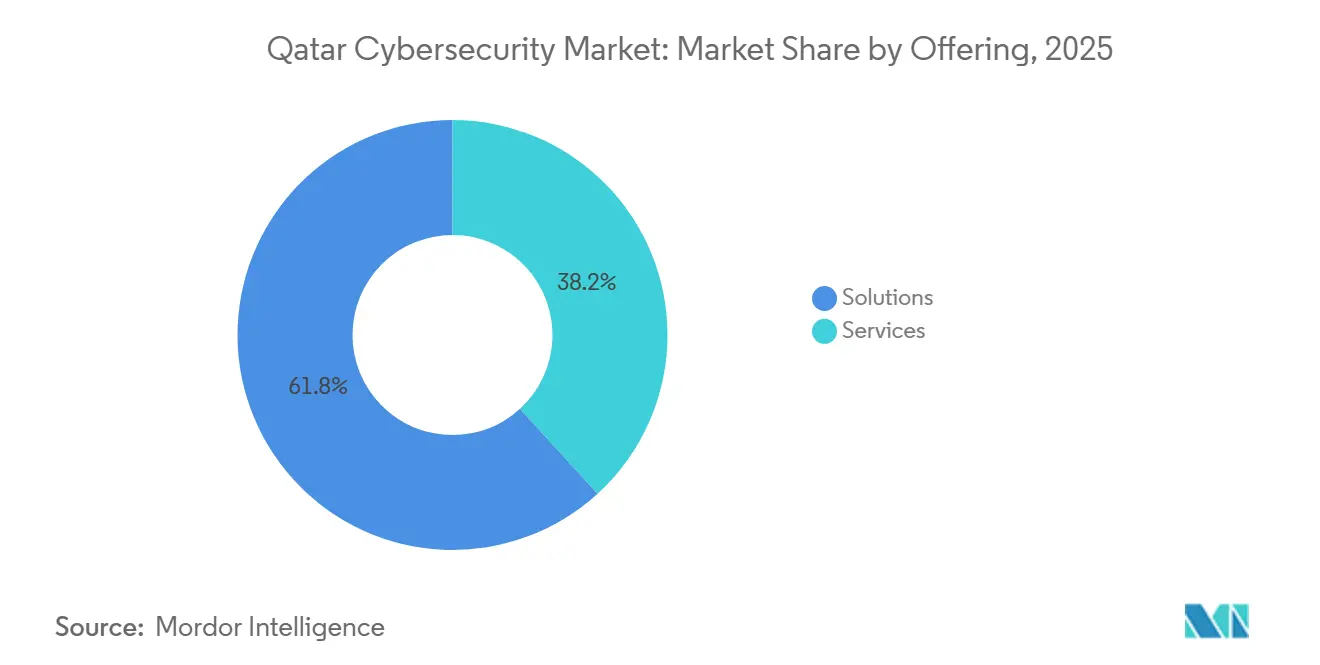

- By offering solutions, it held 61.79% of the Qatar cybersecurity market in 2025, while services are forecast to expand at a 7.92% CAGR through 2031.

- By deployment mode, on-premise accounted for 61.21% of the Qatar cybersecurity market in 2025, while cloud is projected to grow at a 6.52% CAGR through 2031.

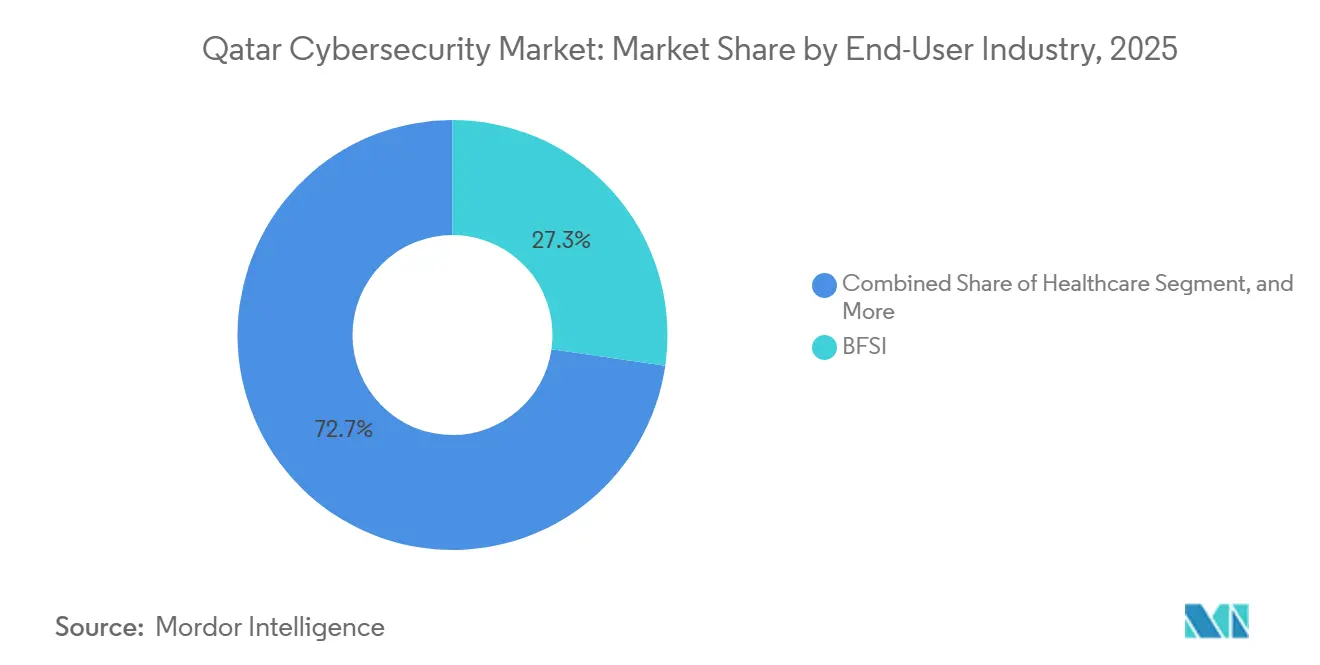

- By end-user industry, BFSI accounted for 27.28% of the Qatar cybersecurity market in 2025, while healthcare is expected to record the highest CAGR of 7.82% through 2031.

- By end-user enterprise size, large enterprises represented 67.83% of the Qatar cybersecurity market in 2025, while SMEs are projected to expand at a 6.47% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Qatar Cybersecurity Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| State-Mandated Critical Infrastructure Protection Law Boosts Compliance Spending | +1.8% | Qatar-wide, with concentrated effect in Doha government and energy clusters | Long term (≥ 4 years) |

| Surge In OT Attacks On LNG Facilities Driving ICS And SCADA Security Demand | +1.5% | Primarily Ras Laffan Industrial City and offshore LNG platforms | Medium term (2-4 years) |

| FIFA 2022 Legacy Smart-City Assets Require Robust Cyber Safeguards | +0.9% | Doha city core, Lusail, and stadium districts | Short term (≤ 2 years) |

| TASMU Cloud-First Program Accelerating Cloud-Native Security Adoption | +0.7% | Qatar-wide, led by MCIT-governed entities and digital service operators | Medium term (2-4 years) |

| Fintech And Open-Banking Rules Expanding IAM And Payment Security Budgets | +0.6% | Financial district, QFC-registered firms, and fintech hubs | Medium term (2-4 years) |

| Mandatory Personal Data Law Raising Encryption And DLP Uptake | +0.4% | National, with early compliance gains among healthcare and public-sector data processors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

State-Mandated Critical Infrastructure Protection Law Boosts Compliance Spending

Qatar's Cabinet adopted the National Cybersecurity Strategy 2024-2030 in February 2024 and set out five pillars such as critical infrastructure resilience, legislation and law enforcement, the data-driven economy, workforce development, and international cooperation. This policy direction keeps the Qatar cybersecurity market closely linked to public-sector governance rather than discretionary IT upgrades.[1]International Trade Administration, “Qatar's New Cybersecurity Strategy 2024-2030,” trade.gov The National Cyber Security Agency also has a formal assurance role, including issuing, auditing, and revoking compliance certificates within its governance and assurance functions. That framework gives cybersecurity investment direct commercial weight because compliance affects eligibility for government-facing work and critical infrastructure operations. The result is a Qatar cybersecurity market in which ministries, state-linked enterprises, and private contractors continue to fund controls aligned with national standards rather than treating security as a narrow IT expense.

Surge In OT Attacks On LNG Facilities Driving ICS And SCADA Security Demand

Industrial protection remains a core growth theme in the Qatar cybersecurity market because the country's energy system is part of the national critical infrastructure agenda. QatarEnergy's recruitment for a Senior Industrial Control Systems Security Engineer role shows that dedicated OT security capability is now embedded in operating requirements, not treated as an occasional specialist need. The role's emphasis on industrial control systems and recognized certifications points to steady demand for ICS and SCADA security inside the Qatar cybersecurity market. As industrial sites become more connected, operators need segmentation, asset visibility, and incident response processes that fit production environments rather than standard office networks. That pattern supports continued procurement in Ras Laffan and related facilities, where operational continuity remains the main buying priority in the Qatar cybersecurity market.

FIFA 2022 Legacy Smart-City Assets Require Robust Cyber Safeguards

The Qatar cybersecurity market continues to absorb the long-tail security needs of connected infrastructure that remained in place after the FIFA 2022 buildout. Palo Alto Networks' work with the Supreme Committee for Delivery and Legacy showed that large, connected public systems in Qatar already required zero-trust design and AI-led endpoint protection at scale. That installed base now operates as part of everyday urban life, which means protection has shifted from event readiness to continuous operational resilience. The Qatar cybersecurity market, therefore, sees durable demand from smart-city environments that combine transport systems, connected facilities, public networks, and city services. This keeps smart infrastructure security relevant because public systems still need identity control, monitoring, and recovery capability long after the tournament period ended.

TASMU Cloud-First Program Accelerating Cloud-Native Security Adoption

TASMU remains one of the clearest structural drivers in the Qatar cybersecurity market because it extends digital services across transport, healthcare, logistics, and environmental use cases through a cloud-based model. The TASMU platform also operates under a formal security policy that defines baseline, enhanced, and critical controls for data and IoT environments, ensuring cybersecurity is built into digital service design. In parallel, the Qatar Central Bank introduced Cloud Computing Regulations in April 2024, which added binding security obligations for regulated financial institutions using cloud services. Palo Alto Networks also launched local cloud infrastructure in Qatar in January 2024, strengthening in-country support for log processing, analytics, and the delivery of its security platform. Together, these factors expand the addressable market for cloud-native controls in Qatar while keeping data residency and local presence central to vendor selection.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Scarcity Of Arabic-Speaking Cyber Talent Inflates MSSP Costs | -1.5% | Qatar-wide, most acute in government and BFSI segments requiring bilingual compliance officers | Long term (≥ 4 years) |

| Legacy OT Assets In Gas Terminals Complicate Security Integration | -1.2% | Ras Laffan Industrial City and onshore gas processing infrastructure | Medium term (2-4 years) |

| Fragmented Procurement Across Semi-Government Firms Slows Project Cycles | -0.6% | Qatar-wide, concentrated in state-linked holding companies and sovereign entities | Medium term (2-4 years) |

| Data Sovereignty Concerns Over Foreign Cloud SOC Hosting | -0.4% | National, with highest sensitivity in defense, intelligence-adjacent, and financial-sector entities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Scarcity Of Arabic-Speaking Cyber Talent Inflates MSSP Costs

The Qatar cybersecurity market continues to face a shortage of Arabic-speaking specialists in roles that combine technical depth with regulatory reporting and public-sector engagement. The launch of a Cybersecurity Manual for SMEs by Qatar Development Bank and the National Cyber Security Agency in August 2024 showed that authorities still see capacity building as a live need across the business base. The Communications Regulatory Authority also partnered with RIPE NCC, Cisco, and Huawei in June 2025 to expand training and digital awareness in cybersecurity, IoT security, IPv6 routing security, and 5G topics. Even with these efforts, many buyers still rely on managed security providers for round-the-clock monitoring, local delivery, and bilingual documentation. That dependence keeps the service pricing firm in the Qatar cybersecurity market and can slow project execution when clients need local staffing, local presence, and Arabic-language assurance support.

Legacy OT Assets In Gas Terminals Complicate Security Integration

Legacy control environments remain a restraint on the Qatar cybersecurity market because industrial protection in gas facilities cannot be rolled out as quickly as standard enterprise security programs. These sites depend on long-lived operational technology, strict uptime requirements, and vendor-specific systems, which makes retrofit work more difficult than security deployment in office or cloud environments. QatarEnergy's continued recruitment of senior ICS security engineering talent underscores the specialized expertise required to secure these assets on an ongoing basis.[2]QatarEnergy Careers, “SR. Industrial Control SYS Security ENGR,” careerportal.qatarenergy.qa Since energy is one of the most important demand centers in the Qatar cybersecurity market, delays in OT integration can hold back implementation even when strategic intent is strong. This pushes buyers toward phased deployment of visibility, segmentation, and monitoring tools rather than rapid full-site modernization.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Solutions Retain Majority Share As Managed Services Scale

Solutions held 61.79% of the Qatar cybersecurity market in 2025, keeping them in the lead. Network security, cloud security, identity and access management, and endpoint security remain the main solution areas because they closely align with national assurance requirements, sector regulations, and public digital programs.[3]National Cyber Security Agency, “National Cyber Governance and Assurance Affairs,” assurance.ncsa.gov.qa Application security is also rising in the Qatar cybersecurity market as financial institutions strengthen governance across digital channels and regulated software environments. This leaves the Qatar cybersecurity industry tilted toward platforms that can protect identity, network traffic, data, workloads, and user endpoints within a more unified control structure.

Services are projected to grow at a 7.92% CAGR from 2026 to 2031, making them the fastest-growing segment at the top level of the Qatar cybersecurity market. MEEZA expanded its managed offering through a June 2024 partnership with Darktrace, adding AI-powered detection, investigation, and autonomous response from its Doha security operations capability. IBM, Cisco, and Palo Alto Networks have also deepened their local footprint through government agreements and local infrastructure, which supports more advisory, integration, and managed security work inside the Qatar cybersecurity market. Buyers are increasingly using these services to support lean internal teams and to manage compliance across mixed on-premise and cloud environments. That trend keeps managed detection, incident support, and advisory work growing faster than product deployment alone in the Qatar cybersecurity industry.

By Deployment Mode: On-Premise Dominance Gradually Yields To Cloud Economics

On-premises deployment accounted for 61.21% of the Qatar cybersecurity market in 2025, reflecting the current operating model of the largest regulated buyers. The Qatar Central Bank's Cloud Computing Regulations require financial institutions to process personally identifiable information and financial data within Qatar and to obtain approval before engaging cloud service providers for regulated workloads. Government entities operating under national assurance requirements also remain cautious where sensitive functions and national systems are involved. This keeps locally controlled environments important in finance, government, and industrial operations across the Qatar cybersecurity market.

Cloud deployment is forecast to grow at a 6.52% CAGR from 2026 to 2031, making it the fastest-growing deployment model in the Qatar cybersecurity market. TASMU's cloud-first design continues to expand digital services across multiple sectors, which directly raises demand for cloud-native security controls. Palo Alto Networks launched local cloud infrastructure in Qatar in January 2024 to support country-specific log processing, analytics, and platform delivery, reducing compliance friction for regulated users. The Qatar cybersecurity market is therefore shifting toward cloud security in a measured way rather than through a full replacement of on-premise models. That pace will likely continue, as cloud growth remains strong, but local requirements still shape where and how security workloads are hosted.

By End-User Enterprise Size: Large Enterprises Drive Volume While SMEs Lead Growth

Large enterprises accounted for 67.83% of Qatar's cybersecurity market share in 2025, keeping them at the center of the market. Ministries, sovereign energy groups, banks, and state-linked conglomerates face layered compliance obligations under national assurance functions and sector regulations, which support larger and more complex security budgets. IBM signed a letter of intent with the Ministry of Interior in May 2025, and Cisco signed a separate agreement in the same month, showing that major buyers are working with large platform vendors on long-horizon transformation and security agendas. This buying pattern favors integrated platforms and multi-year service relationships over small standalone tools in the Qatar cybersecurity market.

SMEs are forecast to grow at a 6.47% CAGR from 2026 to 2031, making them the fastest-growing buyer cohort in the Qatar cybersecurity market. Qatar Development Bank and the National Cyber Security Agency launched a Cybersecurity Manual for SMEs in August 2024 to provide guidance on cyber risk, cloud use, basic controls, and incident response. The Qatar Development Bank also supports SME digital transformation financing, which lowers the barriers to adopting formal security for smaller companies. This model fits the Qatar cybersecurity industry because many SMEs can adopt subscription-based services without funding dedicated in-house infrastructure. It also broadens the reach of the Qatar cybersecurity market beyond the largest government, finance, and energy accounts.

Geography Analysis

Qatar represented a single-country demand environment in 2025, but the Qatar cybersecurity market was shaped by three clear operating clusters, Doha, Ras Laffan Industrial City, and the connected districts tied to Lusail and QSTP. Doha remained the administrative core of the Qatar cybersecurity market because ministries, regulators, banks, and state-linked enterprises are concentrated there. The National Cybersecurity Strategy 2024-2030 and the National Cyber Security Agency's assurance role give this cluster outsized importance because policy, compliance, and procurement are set there. That concentration means policy changes in Doha move quickly across the rest of the Qatar cybersecurity market.

Ras Laffan Industrial City is the highest-consequence node in the Qatar cybersecurity market because it anchors LNG and related industrial operations. QatarEnergy's continued recruitment for senior industrial control systems security roles shows that OT security is now a sustained operating requirement in this geography. In Ras Laffan, buyers focus less on generic enterprise tools and more on visibility, segmentation, and response controls that address industrial uptime requirements. The same pressure supports demand in environments where local operators and international partners must align on security practices and assurance expectations. As a result, spending in this part of the Qatar cybersecurity market tends to be deliberate, specialized, and closely tied to continuity risk.

Lusail, QSTP, and the wider free-zone ecosystem represent the most digitally experimental side of the Qatar cybersecurity market. TASMU and related public digital programs continue to increase the number of cloud-connected, data-intensive workloads in these areas.[4]Ministry of Communications and Information Technology, “TASMU Smart Qatar - Driving Qatar's Digital Transformation and Smart Economy,” mcit.gov.qa The Qatar Financial Center's January 2024 memorandum with MEEZA showed that data center, cloud, managed IT, and cybersecurity services are becoming part of the support structure for firms operating in modern business zones. This mix of regulated finance in Doha, industrial risk in Ras Laffan, and cloud-led services in Lusail and the free zones gives the Qatar cybersecurity market a concentrated but varied geographic demand profile.

Competitive Landscape

The Qatar cybersecurity market is moderately fragmented, with the largest accounts usually served by global platform vendors and a smaller set of local delivery partners. IBM, Cisco, Palo Alto Networks, Fortinet, and Check Point remain central to competition because they can combine network security, cloud controls, analytics, and service ecosystems across the Qatar cybersecurity market. The Qatar cybersecurity market also leaves room for domestic players when clients need local hosting, local service relationships, or closer alignment with national compliance expectations. This balance keeps competition active rather than locked into a sole-vendor structure.

IBM strengthened its position in May 2025 by signing a letter of intent with the Ministry of Interior to support digital transformation, smart infrastructure, and information security services in Qatar. Cisco reinforced its standing in the same month through a separate agreement with the Ministry of Interior focused on technology, AI, digital infrastructure development, and cybersecurity cooperation. Palo Alto Networks added a different competitive advantage in January 2024 by launching local cloud infrastructure in Qatar for Prisma Access, Cortex XSIAM, Cortex XDR, and Cortex Data Lake.[5]Palo Alto Networks, “Palo Alto Networks Invests in New Local Cloud Infrastructure in Qatar to Deliver Best-in-Class Cybersecurity Platforms,” paloaltonetworks.ca Fortinet also pointed to a Doha cloud point of presence in its March 2026 investor materials, which shows how local data handling has become a competitive lever. Together, these moves show that platform breadth, long-term public relationships, and in-country presence matter as much as product depth in the Qatar cybersecurity market.

MEEZA plays a distinct role in the Qatar cybersecurity market by combining domestic ownership, local infrastructure, and managed security capabilities. Its January 2024 memorandum with QFC expanded access to data center, cloud, managed IT, and cybersecurity services for QFC firms, which strengthened its position in regulated commercial accounts. Its June 2024 partnership with Darktrace further improved its managed security proposition through AI-powered detection and response services. Competitive outcomes in the Qatar cybersecurity market, therefore, depend on who can combine compliance credibility, local delivery, and integrated platform coverage most effectively.

Qatar Cybersecurity Industry Leaders

IBM Corporation

Cisco Systems, Inc.

Palo Alto Networks, Inc.

Fortinet, Inc.

MEEZA QSTP-LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: The National Cyber Security Agency granted Atos Qatar a consulting services accreditation certificate, qualifying the company to deliver government-facing cybersecurity advisory engagements under NCSA's accreditation framework. This formalized Atos's role in Qatar's critical infrastructure protection programs.

- February 2026: QNB disclosed an AI-integrated cybersecurity framework aligned with NIST standards, ISO certifications, and PCI DSS, covering cloud security controls, phishing simulation programs, and mandatory staff training. The bank outlined a 5-year AI security roadmap focused on advanced threat detection algorithms and next-generation AI security controls.

- November 2025: QNB launched a USD 10+ million modernization of its physical and digital surveillance infrastructure across 40 branches, 11 corporate buildings, and 420 ATMs in partnership with Ooredoo Qatar, specifically to comply with Ministry of Interior regulatory security standards.

- June 2025: The Communications Regulatory Authority partnered with RIPE NCC, Cisco, and Huawei on a joint capacity-building initiative to deliver online training and webinars on cybersecurity, IoT security, IPv6 routing security, and 5G across Qatar's student, professional, and technology enthusiast communities.

Qatar Cybersecurity Market Report Scope

The Qatar Cybersecurity Market refers to the ecosystem of technologies, services, and solutions designed to protect organizations in Qatar from cyber threats, data breaches, and digital infrastructure vulnerabilities across public and private sectors. It encompasses security tools and services that safeguard networks, endpoints, applications, cloud environments, and critical industrial systems, particularly as digital transformation, cloud adoption, and smart infrastructure initiatives expand nationwide.

The Qatar Cybersecurity Market Report is Segmented by Offering (Solutions, and Services), Deployment Mode (Cloud, and On-Premise), End-User Industry (BFSI, Healthcare, IT and Telecom, Industrial and Defense, Retail and E-Commerce, Energy and Utilities, Manufacturing, Other End-User Industries), End-User Enterprise Size (Large Enterprises, and Small and Medium Enterprises). The Market Forecasts are Provided in Terms of Value (USD).

| Solutions | Application Security |

| Cloud Security | |

| Data Security | |

| Identity and Access Management | |

| Infrastructure Protection | |

| Integrated Risk Management | |

| Network Security | |

| End-Point Security | |

| Services | Professional Services |

| Managed Services |

| Cloud |

| On-Premise |

| BFSI |

| Healthcare |

| IT and Telecom |

| Industrial and Defense |

| Retail and E-Commerce |

| Energy and Utilities |

| Manufacturing |

| Other End-User Industries |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| By Offering | Solutions | Application Security |

| Cloud Security | ||

| Data Security | ||

| Identity and Access Management | ||

| Infrastructure Protection | ||

| Integrated Risk Management | ||

| Network Security | ||

| End-Point Security | ||

| Services | Professional Services | |

| Managed Services | ||

| By Deployment Mode | Cloud | |

| On-Premise | ||

| By End-User Industry | BFSI | |

| Healthcare | ||

| IT and Telecom | ||

| Industrial and Defense | ||

| Retail and E-Commerce | ||

| Energy and Utilities | ||

| Manufacturing | ||

| Other End-User Industries | ||

| By End-User Enterprise Size | Large Enterprises | |

| Small and Medium Enterprises (SMEs) | ||

Key Questions Answered in the Report

What is the current size and forecast of the Qatar cybersecurity market?

The Qatar cybersecurity market was valued at USD 143 million in 2025, is projected at USD 151.75 million in 2026, and is forecast to reach USD 203.99 million by 2031 at a 6.12% CAGR.

Which offering is growing fastest in Qatar cybersecurity?

Services are the fastest-growing offering, with a projected 7.92% CAGR from 2026 to 2031, as more organizations rely on managed detection, response, and advisory support.

Which deployment model currently leads in Qatar?

On-premise led with 61.21% share in 2025 because regulated sectors and government entities still prioritize local control and data residency.

Which end-user segment drives the most spending in Qatar?

BFSI led with 27.28% share in 2025 due to strong regulatory oversight from the Qatar Central Bank and continued investment by major banks.

Which end-user segment is expanding fastest in Qatar?

Healthcare is expected to grow at a 7.82% CAGR through 2031 as digital health systems, connected services, and operational continuity requirements increase security spending.

Why are SMEs becoming more important buyers in Qatar?

SMEs are projected to grow at a 6.47% CAGR through 2031 because cloud-delivered security services and QDB-NCSA support programs lower the entry barrier for adoption.

Page last updated on: