Kuwait Cybersecurity Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

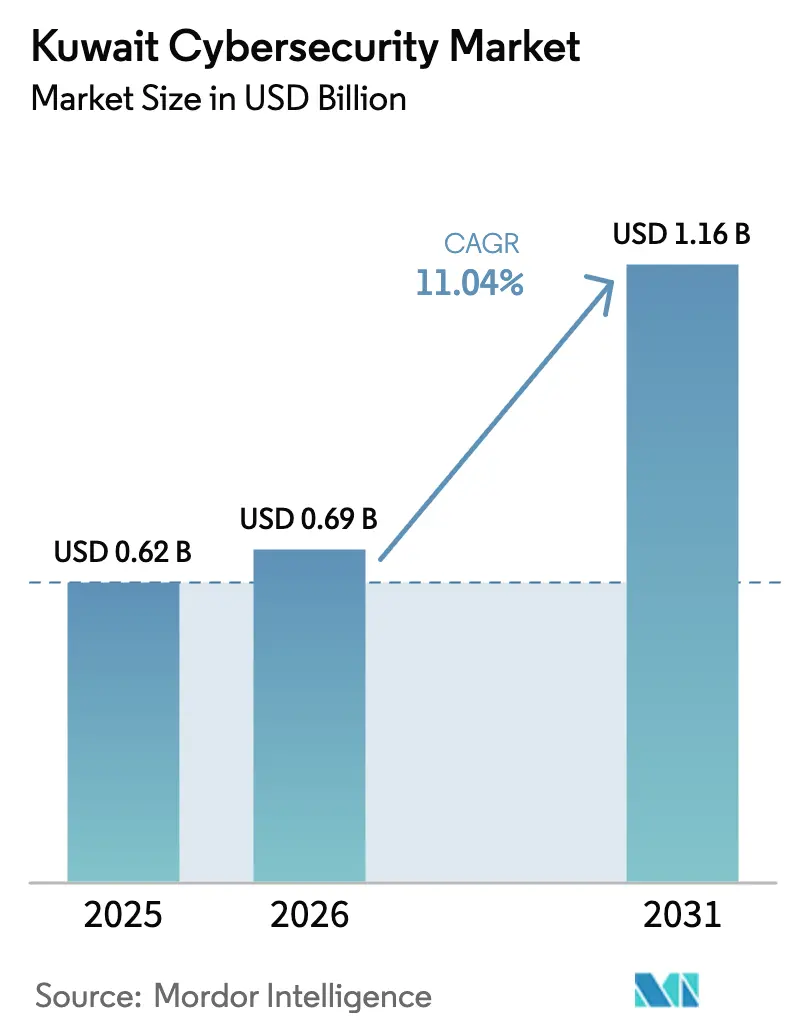

| Base Year Market Size (2025) | USD 0.62 Billion |

| Market Size (2026) | USD 0.69 Billion |

| Market Size (2031) | USD 1.16 Billion |

| Growth Rate (2026 - 2031) | 11.04% CAGR |

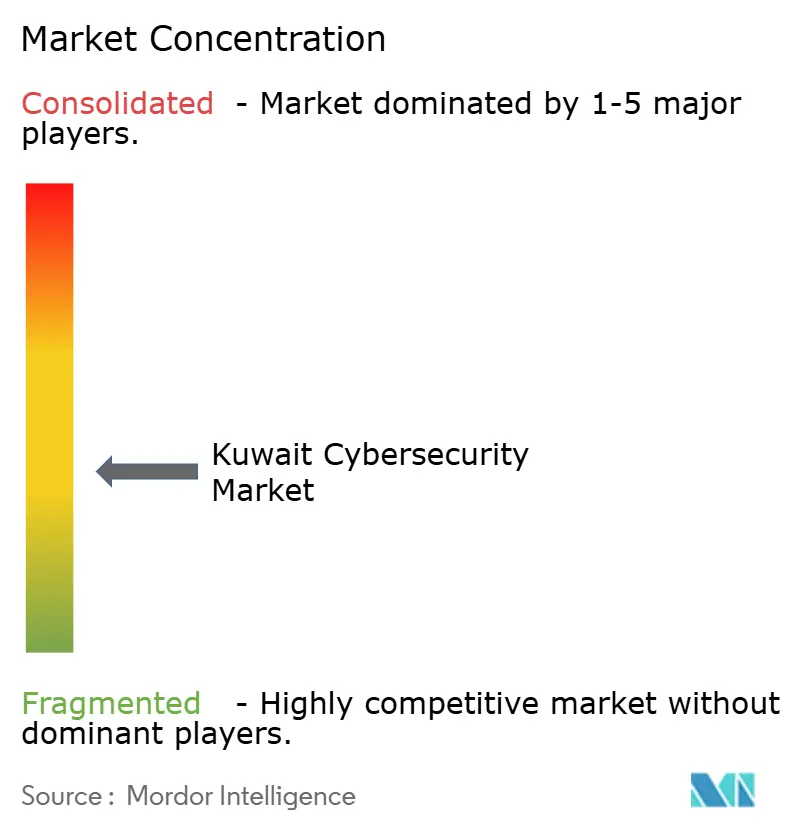

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Kuwait Cybersecurity Market Analysis by Mordor Intelligence

The Kuwait Cybersecurity Market size is expected to grow from USD 0.62 billion in 2025 to USD 0.69 billion in 2026 and is forecast to reach USD 1.16 billion by 2031 at 11.04% CAGR over 2026-2031. Digital sovereignty policies, accelerated cloud adoption, 5G rollouts, and sustained capital spending under the National Cybersecurity Strategy 2023-27 shape this expansion path. Large enterprises anchor spending, yet the fast-growing SME base amplifies incremental demand as mandatory data-privacy compliance closes historic protection gaps. Security-as-a-service models gain prominence because they substitute scarce in-house expertise with round-the-clock local SOC capabilities. Competitive intensity rises around managed security services and cloud-native controls as global vendors localize operations and partner with domestic integrators. Legacy OT convergence costs and a shortage of cybersecurity professionals temper growth but do not derail the upward trajectory of the Kuwait cybersecurity market.[1]Communication & Information Technology Regulatory Authority, “Cybersecurity and Emergency Response,” citra.gov.kw

Key Report Takeaways

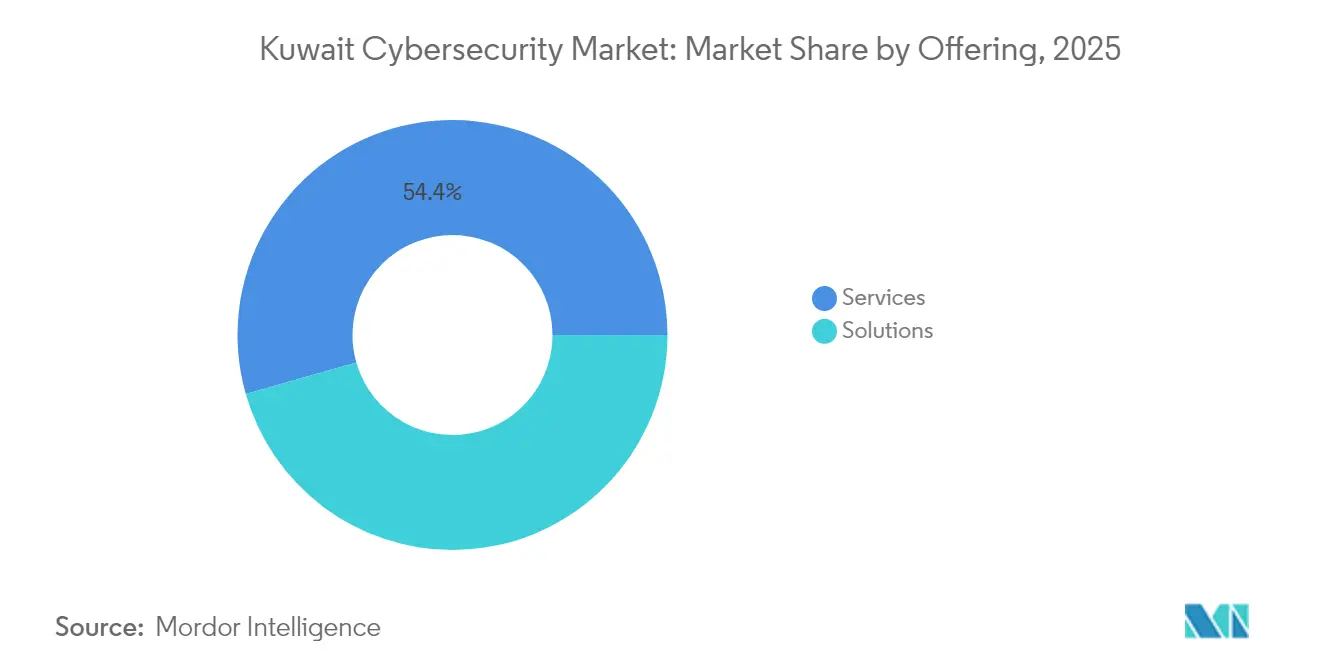

- By offering, Services commanded 54.43% of Kuwait cybersecurity market share in 2025 while solutions expand at a 16.98% CAGR through 2031.

- By deployment mode, cloud captured 66.21% revenue share of the Kuwait cybersecurity market size in 2025 and is projected to grow at 16.55% CAGR to 2031.

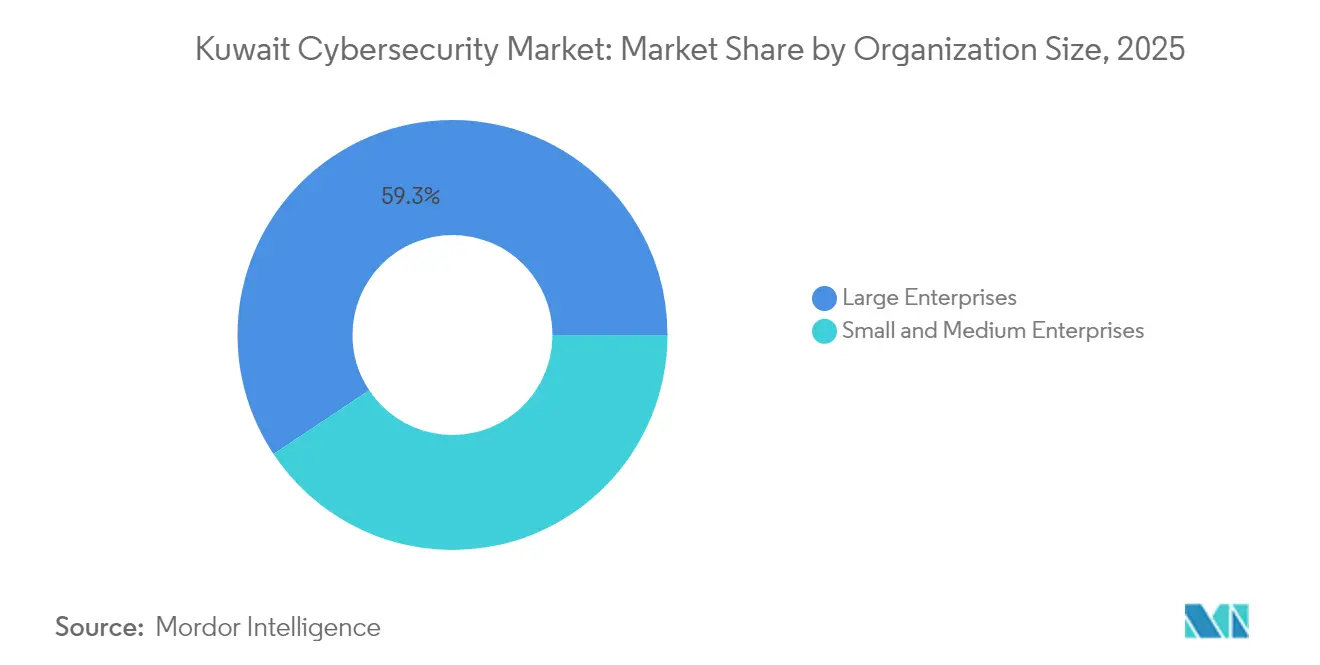

- By organization size, large enterprises held 59.34% of Kuwait cybersecurity market share in 2025; SMEs post the highest 14.92% CAGR through 2031 under Regulation 26/2024 compliance.

- By end-user vertical, BFSI led with 28.47% share of the Kuwait cybersecurity market size in 2025 while healthcare advances at 17.06% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Kuwait Cybersecurity Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-sovereignty rules drive local SOC & MSS demand | +2.8% | National, concentrated in Al Asimah and Hawalli | Medium term (2–4 years) |

| Smart-city and OT security spending for mega-projects | +2.1% | Jahra and Ahmadi governorates | Long term (≥4 years) |

| National Cybersecurity Strategy 2023–27 spending | +1.9% | Nationwide with government-sector focus | Short term (≤2 years) |

| 5G & IoT rollout expands threat surface | +1.7% | National coverage, urban concentration | Medium term (2–4 years) |

| Digital banking and open-API rules accelerate IAM | +1.4% | Al Asimah financial district | Short term (≤2 years) |

| AI-driven threat hunting in oil & gas sector | +1.3% | Ahmadi and other industrial zones | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Data-sovereignty rules boosting in-country SOC & MSS demand

Resolution 26/2024 enforces local data residency and 24-hour breach notification, compelling organizations to build or subscribe to Kuwaiti security operations centers. Enterprises pivot toward managed security services that deliver continuous monitoring, localized threat intelligence, and dual-language compliance reporting. The National Cybersecurity Center’s information-sharing platform increases collective defense effectiveness and further elevates demand for domestic SOC capacity. Financial institutions already invest a higher share of IT budgets in localized security, a pattern that is spreading across the Kuwait cybersecurity market.

Smart-city and OT security spend for Silk City and other mega-projects

Kuwait’s USD 4 billion Saad Al-Abdullah smart-city program integrates energy, water, and transport systems, making OT security a budget priority. Industrial control networks that once operated in isolation now connect to cloud platforms, multiplying attack vectors. Security vendors with deep OT expertise win contracts for anomaly detection, secure gateways, and identity management that protect tens of thousands of sensors and control points. Early deployment rounds indicate security spending per connected device exceeds traditional infrastructure outlays, underscoring the strategic weight of OT security in the Kuwait cybersecurity market.[2]Wilson Center, “The Rise of Gulf Smart Cities,” wilsoncenter.org

National Cybersecurity Strategy 2023-27 capex outlays

The strategy mandates every government entity allocate 8-12% of its IT spend to cybersecurity. Funds target network segmentation, Zero Trust adoption, and local skill development through university partnerships and vendor academies. Public-sector projects create reference architectures for private organizations, catalyzing new demand across verticals. The predictable budget cycle stabilizes procurement planning and further entrenches the Kuwait cybersecurity market as a core pillar of Vision 2035.

5G and IoT roll-out expanding threat surface

Nationwide 5G coverage connects millions of devices across smart homes, telemedicine, and industrial automation. Network slicing and edge computing improve performance but add policy-management complexity. Telecommunications operators collaborate with security vendors to embed threat detection at the edge and enforce micro-segmentation. These developments stimulate continuous product innovation and drive incremental revenue across the Kuwait cybersecurity market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High OT-IT convergence upgrade costs | -1.8% | Industrial zones in Ahmadi and Farwaniya | Medium term (2–4 years) |

| Cyber-skills shortage and expat turnover | -1.5% | National, strongest in Al Asimah | Short term (≤2 years) |

| SME security budgets linked to oil price cycles | -1.2% | National SME sector | Medium term (2–4 years) |

| Fragmented sectoral regulations | -0.9% | Cross-sector coordination challenges | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Legacy OT and IT convergence upgrade costs

Industrial facilities deploy proprietary protocols and dated hardware that lack modern authentication features. Upgrading control systems while maintaining production uptime raises costs to as much as triple those of comparable IT projects. Limited vendor choices in OT security keep pricing power high, elongating the payback period and slowing investment cycles in parts of the Kuwait cybersecurity market.[3]TradeArabia, “KNPC Upgrades Data Centre Infrastructure,” tradearabia.com

Acute cyber-skills shortage and expatriate turnover

Demand for cloud, AI, and Zero Trust expertise outstrips supply as expatriate specialists rotate abroad and local training programs mature slowly. Organizations compensate by outsourcing, yet excessive reliance on managed services can hinder internal knowledge accumulation. Salary inflation elevates operating costs and adds friction to large-scale rollouts within the Kuwait cybersecurity industry

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Services Drive Market Maturation

Services contributed 54.43% revenue in 2025, reflecting enterprises’ preference for outsourced 24/7 protection amid talent constraints. Managed detection and response dominates contract awards while advisory engagements spike post-Regulation 26/2024. Solutions advance at 16.98% CAGR because hybrid workloads demand consistent policy enforcement. These patterns reinforce the central role of services in the Kuwait cybersecurity market, which relies on localized SOC deployment for compliance verification.

Solutions covering network, application, and data layers continue to evolve. Identity and access management gains traction in banking and government identity programs. Next-generation firewalls, secure web gateways, and data-loss prevention suites accompany 5G backhaul upgrades. The interplay of solutions and services cements end-to-end value propositions across the Kuwait cybersecurity market.

By Deployment Mode: Cloud Transformation Accelerates

Cloud secured 66.21% share during 2025 as ministries and banks adopted a cloud-first mandate tied to new in-country hyperscale regions. Hybrid architectures blend on-premise vault systems with public-cloud analytics, balancing sovereignty with elasticity. The resulting 16.55% CAGR positions cloud controls as the primary expansion lever for the Kuwait cybersecurity market size between 2026 and 2031.

On-premise security persists in critical infrastructure where air-gapped segments underpin safety and process integrity. Unified security consoles now cover cloud, edge, and data-center assets, allowing administrators to enforce uniform baselines. This convergence fosters incremental platform bookings and locks in long-term subscription revenue streams for vendors active in the Kuwait cybersecurity market.

By Organization Size: SME Adoption Surges

Large enterprises held 59.34% revenue in 2025 driven by extensive compliance obligations and multi-layered risk-management frameworks. Oil majors and telecoms lead early adoption of AI-assisted threat hunting and Zero Trust segmentation. Their reference projects validate blueprints later replicated across mid-market accounts, preserving scale economics inside the Kuwait cybersecurity market.

SMEs record the fastest 14.92% CAGR because the data-privacy law applies extraterritorially and fines scale with breach severity. Cloud delivered security bundles, virtual firewalls, and pay-as-you-go SOC seats lower cost barriers. Government training vouchers and assessment subsidies further shrink adoption frictions, accelerating SME penetration throughout the Kuwait cybersecurity market.

By End-User Vertical: BFSI Leadership and Healthcare Surge

BFSI sector led with 28.47% of Kuwait cybersecurity market share in 2025 as open-API banking and digital wallets multiplied transaction surfaces. Institutions fortified real-time fraud analytics, strong customer authentication, and secure DevOps pipelines to sustain customer trust. Regulatory scrutiny drives continued above-average security spend, anchoring steady contract flow for vendors.

Healthcare expands at 17.06% CAGR to 2031 powered by electronic health records, tele-ICU platforms, and connected diagnostic devices. Confidential patient data requires encryption in motion and at rest, while medical device firmware must withstand remote exploits. Similar security modernization ripples across telecom, manufacturing, and defense, each adding tailored demand layers to the Kuwait cybersecurity market.

Geography Analysis

Al Asimah remains the strategic command center for national cybersecurity initiatives. The governorate hosts the National Cybersecurity Center, ministerial data centers, and financial SOCs that shape standards later mirrored nationwide. Public-sector allocations and continuous policy updates translate into predictable multi-year demand, allowing vendors to calibrate long-range investment in localized R&D and Arabic language support. Resulting flagship deployments reinforce Al Asimah’s role as a testing ground for next-gen security solutions within the Kuwait cybersecurity market.

Jahra’s double-digit CAGR stems from mega-projects such as Silk City that blend smart energy grids, IoT-enabled utilities, and AI-controlled mobility corridors. Industrial tenants adopt secure gateways, protocol translators, and incident-response playbooks tailored to OT environments. Collaboration between municipal planners and the private sector fosters integrated security blueprints that scale efficiently, ensuring Jahra becomes a pivotal growth corridor for the Kuwait cybersecurity market.

Ahmadi capitalizes on its hydrocarbon infrastructure by procuring bespoke intrusion-detection sensors, encryption for pipeline telemetry, and sandboxing for refinery process controllers. Hawalli and Farwaniya add mid-market contracts linked to retail digitization and small-office cloud migration. Mubarak Al-Kabeer’s new commercial zones opt for secure-by-design architectures from inception, reducing future retrofit costs while enlarging the total contract base of the Kuwait cybersecurity market.

Competitive Landscape

The Kuwait cybersecurity market hosts a balanced mix of global platform vendors, regional telecom-affiliated providers, and niche local specialists. Multinationals such as Microsoft, Cisco, and Palo Alto Networks leverage strategic alliances with domestic integrators to ensure compliance with data-localization and Arabic interface requirements. Their cloud marketplaces supply AI-driven analytics, Secure Access Service Edge, and Zero Trust frameworks optimized for high-bandwidth 5G environments. [4]SAMENA Council, “Kuwait’s Vision 2035 Drives Digital Transformation,” samenacouncil.org

Regional operators like stc Kuwait’s sirar division and Mobile Telecommunications Company deliver managed detection services grounded in existing network footprints. Local firms offer penetration testing, digital-forensics, and Arabic threat-intel that resonate strongly with public-sector buyers. Competitive positioning coalesces around platform breadth, localized support, and bundled training that mitigates the talent deficit affecting the Kuwait cybersecurity industry.

Strategic activity centers on AI acquisition, localized cloud region launches, and OT-security portfolio build-outs. G42’s purchase of CPX expands AI-secured services across Gulf markets, while National Bank of Kuwait’s Tech Academy cultivates domestic skill pipelines that vendors tap for future growth. Joint projects between hyperscalers and ministries to deploy confidential computing and national secure clouds further anchor the Kuwait cybersecurity market’s medium-term dynamism.

Kuwait Cybersecurity Industry Leaders

Microsoft Corporation

Dell Technologies Inc.

IBM Corporation

Cisco Systems Inc.

Fortinet Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: G42 acquired CPX, adding 400 specialists to secure the AI value chain across Gulf projects.

- February 2025: National Bank of Kuwait launched the six-month NBK Tech Academy to build local cybersecurity talent.

- February 2025: Zain became strategic partner of the Kuwait CyberChamps competition to nurture cybersecurity skills among students.

- January 2025: Kuwait University reported a data breach involving national ID cards, heightening awareness of academic cybersecurity.

Kuwait Cybersecurity Market Report Scope

The cybersecurity market's scope includes revenues from solutions and services used across various industries. The analysis combines secondary research with primary sources, offering a thorough market view of the market. The market analysis explores the primary drivers and constraints influencing the market's growth.

The Kuwait cybersecurity market is segmented by offerings (solutions [application security, cloud security, data security, identity access management, infrastructure protection, integrated risk management, network security, end-point security, and other solution types] and services [professional services and managed services]), by deployment (On-premise, and cloud), by organization size (SMEs, large enterprises), by end-user vertical (BFSI, healthcare, IT and telecom, industrial and defense, retail, energy and utilities, manufacturing, and other end-user industries). The market sizes and forecasts are provided in terms of value in (USD) for all the above segments.

| Solutions | Application Security |

| Cloud Security | |

| Data Security | |

| Identity and Access Mgmt | |

| Infrastructure Protection | |

| Integrated Risk Mgmt | |

| Network Security Equipment | |

| Endpoint Security | |

| Other Solutions | |

| Services | Professional Services |

| Managed Services |

| Cloud |

| On-Premise |

| Small and Medium Enterprises |

| Large Enterprises |

| BFSI |

| Healthcare |

| IT and Telecom |

| Industrial and Defense |

| Retail |

| Energy and Utilities |

| Manufacturing |

| Others |

| By Offering | Solutions | Application Security |

| Cloud Security | ||

| Data Security | ||

| Identity and Access Mgmt | ||

| Infrastructure Protection | ||

| Integrated Risk Mgmt | ||

| Network Security Equipment | ||

| Endpoint Security | ||

| Other Solutions | ||

| Services | Professional Services | |

| Managed Services | ||

| By Deployment Mode | Cloud | |

| On-Premise | ||

| By Organization Size | Small and Medium Enterprises | |

| Large Enterprises | ||

| By End-User Vertical | BFSI | |

| Healthcare | ||

| IT and Telecom | ||

| Industrial and Defense | ||

| Retail | ||

| Energy and Utilities | ||

| Manufacturing | ||

| Others | ||

Key Questions Answered in the Report

What is the current value of the Kuwait cybersecurity market?

The market is valued at USD 0.69 billion in 2026 and is projected to reach USD 1.16 billion by 2031.

Which segment generates the largest revenue in Kuwait’s cybersecurity sector?

Security services lead with 54.43% of revenue due to high demand for managed detection and response.

Why is cloud security growing so quickly in Kuwait?

Government cloud-first mandates and new local hyperscale regions allow compliant data residency, propelling a 16.55% CAGR for cloud-deployed controls.

Which governorate offers the fastest growth opportunity?

Jahra records a 12.96% CAGR through 2031 owing to Silk City’s smart-infrastructure projects and expanding industrial base.

How is Kuwait addressing its cybersecurity skills gap?

Initiatives such as the NBK Tech Academy and student competitions like CyberChamps aim to train local talent and reduce reliance on expatriate professionals.

What factors restrain faster market growth?

High costs of upgrading legacy OT systems and an acute shortage of skilled cybersecurity workers limit short-term adoption speed.

Page last updated on: