Peptide Synthesis Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

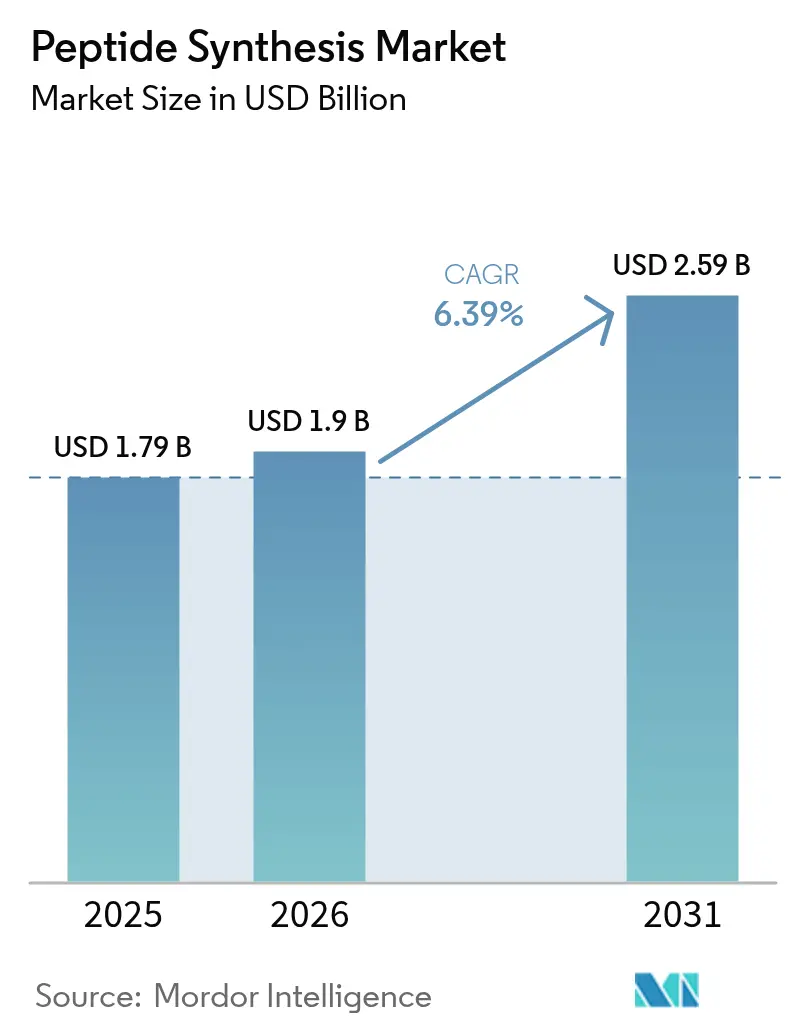

| Market Size (2026) | USD 1.9 Billion |

| Market Size (2031) | USD 2.59 Billion |

| Growth Rate (2026 - 2031) | 6.39% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Peptide Synthesis Market Analysis by Mordor Intelligence

The Peptide Synthesis Market size was valued at USD 1.79 billion in 2025 and is estimated to grow from USD 1.9 billion in 2026 to reach USD 2.59 billion by 2031, at a CAGR of 6.39% during the forecast period (2026-2031).

Regulatory approvals for peptide therapeutics remain steady, R&D investments in chronic disease drugs are on the rise, and there's a consistent shift towards green-chemistry synthesis routes. In 2025 alone, four peptide or oligonucleotide drugs received U.S. approval, bolstering the confidence of venture investors. These investors had previously backed AI-driven design platforms like Peptone and Insilico Medicine. While solid-phase technologies led revenue streams in 2025, enzymatic and cell-free alternatives are carving out a larger market share. This shift comes as EU REACH restrictions on dimethylformamide push sponsors towards cleaner processes, resulting in up to 95% reduction in solvent waste. Discovery activities remain anchored in North America. However, capacity expansions by WuXi AppTec, GenScript, and SK pharmteco in the Asia-Pacific hint at a significant eastward shift in large-scale manufacturing. Additionally, catalogue-grade cosmetic and diagnostic peptides, now priced below USD 500 per gram, are attracting a broader clientele, extending beyond the traditional pharmaceutical sector.

Key Report Takeaways

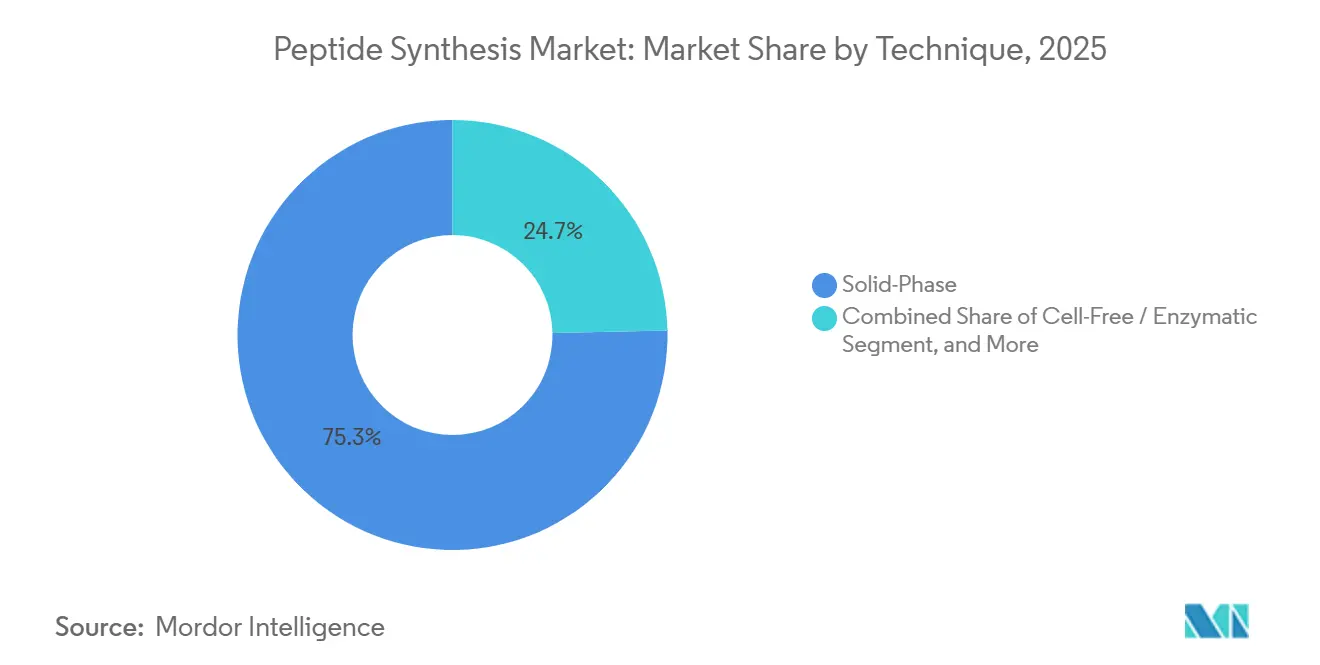

- By technique, solid-phase synthesis led with 75.36% revenue share in 2025; cell-free and enzymatic methods are on course for a 6.43% CAGR through 2031.

- By product type, reagents and consumables accounted for 51.25% of the peptide synthesis market size in 2025, while services are projected to expand at a 6.06% CAGR through 2031.

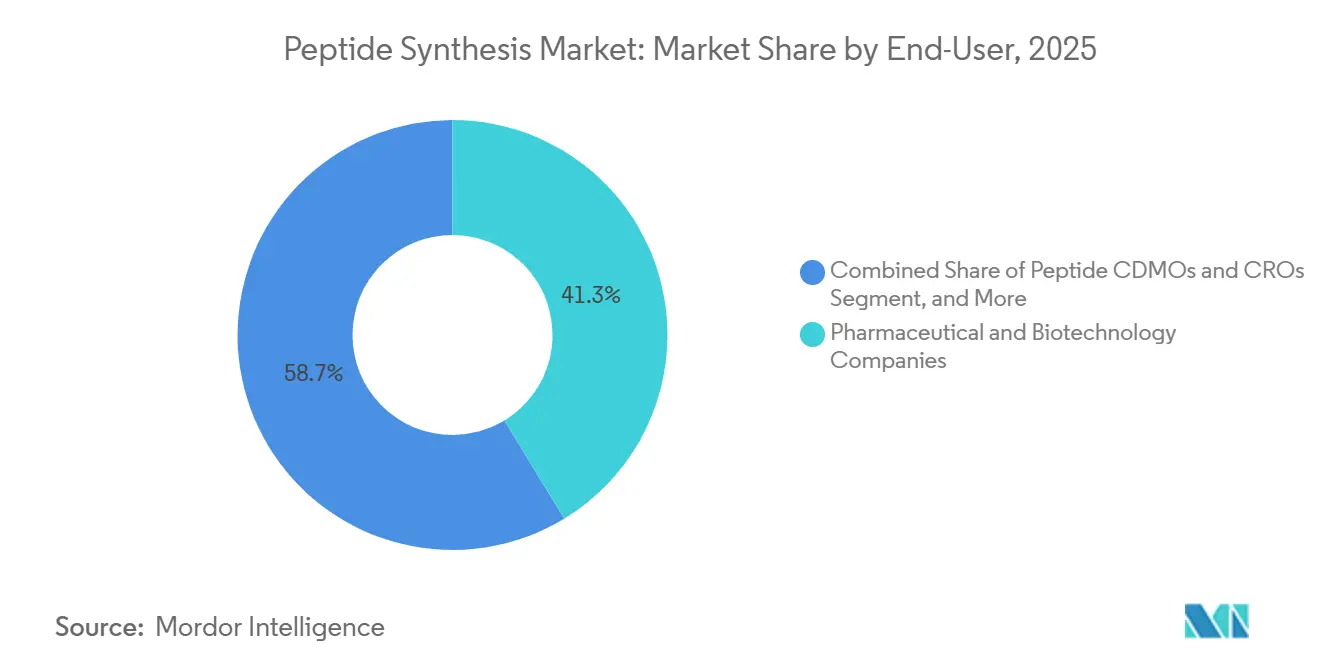

- By end user, pharmaceutical and biotechnology companies held 41.31% of the peptide synthesis market size in 2025; peptide CDMOs and CROs are advancing at a 7.32% CAGR through 2031.

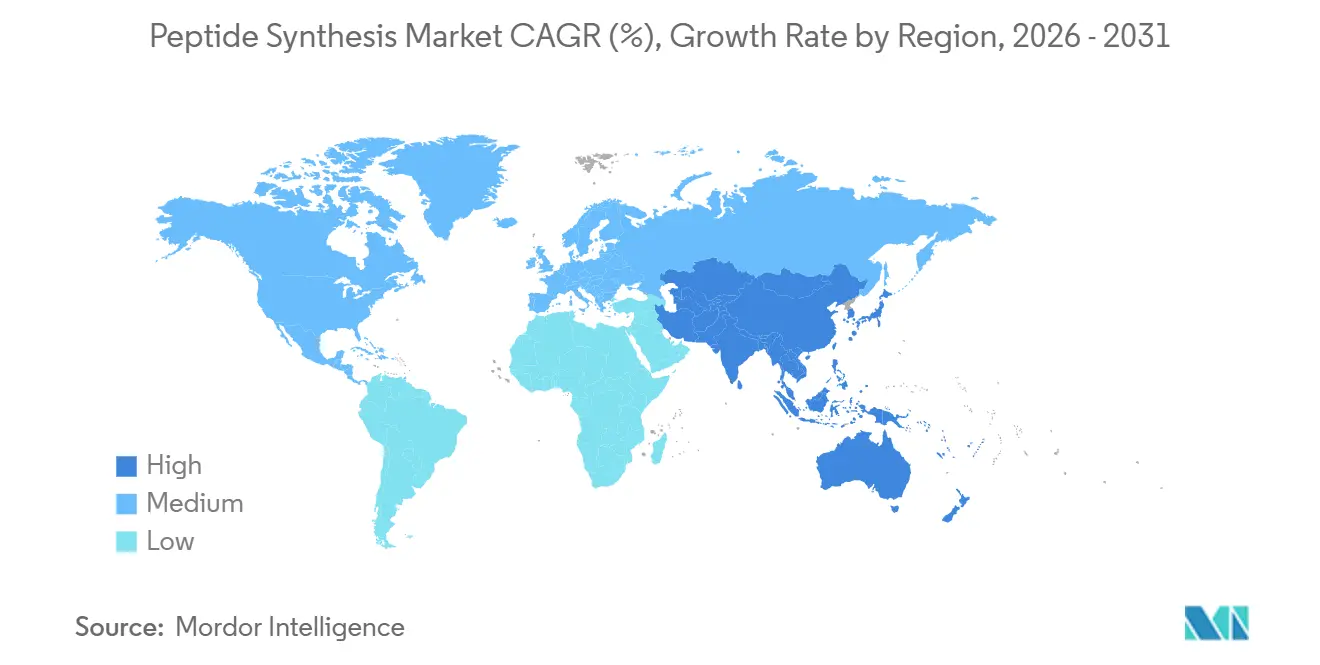

- By geography, North America commanded a 41.71% share of the peptide synthesis market size in 2025, whereas Asia-Pacific is rising at a 6.53% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Peptide Synthesis Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Increasing acceptance of peptide-based therapeutics | +1.8% | Global, strongest in North America and Europe | Medium term (2–4 years) |

| Growing prevalence of chronic diseases | +1.5% | Worldwide, most acute in Asia-Pacific | Long term (≥4 years) |

| Advancements in solid-phase & automated technologies | +1.2% | North America and Europe first movers | Short term (≤2 years) |

| Expansion of CDMO services | +1.0% | Global, capacity centered in Asia-Pacific & Europe | Medium term (2–4 years) |

| Green-chemistry mandates boosting enzymatic & cell-free synthesis | +0.5% | Europe origin, spreading to North America | Long term (≥4 years) |

| AI-driven in-silico design compressing R&D timelines | +0.3% | North America venture clusters, Europe academia | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Increasing Acceptance of Peptide-Based Therapeutics

Regulators have endorsed peptides with over 110 approvals globally as of 2024, validating their clinical value and propelling the peptide synthesis market. The U.S. FDA cleared four new peptide drugs in 2024, including imetelstat and olezarsen, signaling confidence in the modality. Blockbuster GLP-1 receptor agonists, including semaglutide and tirzepatide, have sparked more than USD 1 billion in CDMO capacity additions across Europe and North America. Oncology is following suit; 177Lu-DOTATATE exemplifies how peptide-drug conjugates deliver targeted radiotherapeutics with fewer off-target effects. Fast-track designations and the EMA’s synthetic peptide guidance shorten approval cycles, stimulating R&D pipelines. Collectively, these factors add an estimated +2.1% to the forecast CAGR.

Growing Prevalence of Chronic Diseases

By 2030, the International Diabetes Federation forecasts that 643 million adults will grapple with type 2 diabetes, driving heightened demand for GLP-1 agonists produced at a multi-kilogram scale.[1]International Diabetes Federation, “IDF Diabetes Atlas 2024,” IDF, idf.org

In 2024, the World Health Organization recognized obesity as a chronic disease. Meanwhile, supply constraints for semaglutide and tirzepatide persisted into mid-2025, prompting Novo Nordisk and Eli Lilly to urgently expand capacity. With cancer cases projected to reach 30 million annually by 2040, the strategic value of peptide-drug conjugates like 177Lu-PSMA-617 becomes evident, especially as it has blossomed into a USD 1 billion franchise for Novartis.

Advancements in Solid-Phase and Automated Synthesis Technologies

Microwave-assisted SPPS slashes coupling cycles from hours to minutes, raising crude purity above 90% and compressing lead times to days.[2]Insilico Medicine, “INS018 Clinical Trial Announcement,” Insilico, insilico.com CEM’s Liberty PRIME platform employs headspace gas flushing, eliminating volatile deprotection bases and lifting final purity by up to 25% compared with legacy equipment. GenScript’s PepPower system delivers ≥95% sequence fidelity for peptides as long as 200 amino acids in as little as five days. Machine-learning algorithms now predict aggregation hotspots in real time, trimming synthesis failures and waste.

Expansion of Contract Development and Manufacturing Services

PolyPeptide Group grew H2 2023 revenue by 43% and aims to double 2023 turnover by 2028, exemplifying surging outsource demand. Asia-Pacific CDMOs are expanding fastest; BioDuro opened a Shanghai site with kilogram-scale capacity, while SK pharmteco is investing USD 260 million in South Korea. Chinese suppliers filed more peptide drug master files with the FDA than U.S. or European peers in 2024, reflecting maturing quality systems. End-to-end service bundles, from discovery through commercial fill-finish, reduce sponsor timelines and capital outlay.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High production costs & scalability challenges | -0.9% | Global, more acute in North America & Europe | Medium term (2–4 years) |

| Stringent regulatory & quality requirements | -0.6% | Worldwide, led by EMA & FDA benchmarks | Long term (≥4 years) |

| Fragile supply chains for specialty reagents & resins | -0.4% | Risk concentrated in China-sourced inputs | Short term (≤2 years) |

| Shortage of skilled peptide chemists | -0.3% | North America & Europe, emerging in Asia-Pacific | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

High Production Costs and Scalability Challenges

SPPS generates roughly 13,000 kg of waste per kilogram of peptide, compared with 168-308 kg for small-molecule APIs, inflating solvent disposal bills and environmental footprints. Raw materials account for 60-70% of the cost of goods, as specialized amino acids and coupling reagents remain expensive and prone to supply disruptions. Purification can triple overall production time; preparative HPLC cycles consume large volumes of solvent, though emerging multicolumn gradient technologies promise 50% solvent savings. Scale-up headaches intensify beyond 30 amino acids, where incomplete couplings and deletion sequences become more prevalent. Capital expenditures for dedicated kilo labs often exceed USD 50 million, stretching break-even timelines for smaller firms.

Stringent Regulatory and Quality Requirements

The FDA now mandates immunogenicity risk assessments and detailed impurity profiling for synthetic peptides, elevating analytical burdens. EMA guidelines require full disclosure of process-related impurities, forcing manufacturers to validate cleaning and cross-contamination controls to microgram levels.[3]European Peptide Society, “Industry Cost Survey 2024,” European Peptide Society, europeanpeptidesociety.org Global bans on peptide compounds of uncertain safety, such as the FDA’s 2024 prohibition of BPC-157 in compounding pharmacies, illustrate heightened surveillance. Compliance costs rise as firms add real-time release testing and data-integrity platforms, consuming 15-20% of annual manufacturing budgets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technique: Microwave Innovation Drives Synthesis Evolution

Solid-phase synthesis retained 75.36% of the peptide synthesis market share in 2025 due to mature process chemistry and broad reagent availability. The peptide synthesis market size for SPPS is projected to advance at 6.43% CAGR through 2031 as manufacturers retrofit older instruments with microwave reactors that lift coupling efficiencies and slash solvent volumes. Automated SPPS lines now achieve 95% stepwise yields for sequences up to 200 residues, enabling kilogram-scale batches under cGMP. Liquid-phase synthesis remains viable for short peptides that demand low cost of goods, yet its share is stable rather than expanding. Continuous-flow adaptations of SPPS are entering commercial trials, promising even higher volumetric productivity and solvent recovery rates approaching 80%.

Cell-free and enzymatic synthesis, though starting from a smaller base, is the fastest-growing technique at an 5.91% CAGR as green-chemistry mandates gain traction. Protein-engineering firms have scaled cell-free platforms that bypass fermentation, trimming lead times by 30% and shrinking water consumption by 70%. Enzymatic ligation offers near-perfect stereoselectivity under ambient conditions, yielding fewer byproducts and easing downstream purification. Hybrid chemo-enzymatic routes have produced stable lasso peptides with improved oral bioavailability, stimulating pharma interest in novel scaffolds. ISO 14001 credentials are becoming contract prerequisites, positioning eco-friendly methods to capture new outsourcing contracts. The convergence of digital design, flow technology, and biocatalysis is expected to erode SPPS dominance beyond 2030.

By Product Type: Services Outpace Equipment on CDMO Outsourcing Wave

Reagents and consumables contributed 51.25% of the peptide synthesis market size in 2025, dominated by Fmoc-protected amino acids and polystyrene or PEG resins from suppliers such as Bachem and Merck KGaA. Yet service revenue is positioned for a 7.71% CAGR to 2031, reflecting a marked shift by innovator firms toward asset-light models. Equipment growth lags at 4.5% as CDMOs sweat existing assets rather than purchasing additional HPLC lines. Post-translational modification services, such as phosphorylation, glycosylation, and PEGylation, are offered by fewer than 15 vendors worldwide and command premiums given their enzyme-intensive workflows.

Looking ahead, the service category will also benefit from the chronic chemist shortage. Sponsors unable to hire in-house experts outsource both development and GMP supply, locking in multi-year master-service agreements that stabilize CDMO order books. Meanwhile, reagent margins remain under pressure because China-sourced amino acids account for more than 70% of global volume and remain subject to price swings tied to upstream petrochemicals and environmental audits.

By End User: CDMOs Capture Pharma Outsourcing Surge

Pharmaceutical and biotech firms absorbed 41.31% of peptide synthesis market size in 2025 but increasingly rely on external partners for GMP output. Academic laboratories remain price-sensitive, negotiating rates below USD 200 per g for standard catalog sequences. Diagnostic radiopharmacies, while niche, generate high-margin demand for ready-to-label peptides such as 68Ga-PSMA-11. Nutraceutical and cosmetic players favor short bioactive sequences like GHK-Cu, and price erosion to less than USD 500 kg-1 for high-volume chains has normalized peptide inclusion in mass-market formulations.

Contract development and manufacturing organizations themselves are a distinct, fast-growing customer set as they sub-contract specialized steps such as large-scale lyophilization or in-line quality-control testing. CDMOs’ combined share of the peptide synthesis market is on track to widen because innovators want single-source responsibility from route scouting through release analytics an offering only integrated providers can match.

Geography Analysis

North America accounted for 41.71% of the peptide synthesis market in 2025, anchored by the United States’ deep pharmaceutical ecosystem and a regulatory stance that favors expedited review of complex biologics. More than USD 200 billion in drug R&D spending flowed through the region in 2025, with a growing share earmarked for peptide modalities. The FDA’s guidance on synthetic peptides has shortened review queues, encouraging small innovators to file first-in-class applications. Capacity expansions, such as CordenPharma’s Colorado upgrade and Merck’s USD 493 million oral peptide licensing deal with Cyprumed, spotlight strategic bets on formulation innovation. Federal tax credits for advanced manufacturing further bolster domestic capital spending.

Asia-Pacific is the fastest-growing geography, charting a 6.78% CAGR through 2031 on the back of cost-competitive CDMOs, expanding talent pools, and supportive industrial policies. China’s peptide CDMO share is projected to rise from 5% in 2020 to 9% by 2025 as firms such as BioDuro and Asymchem scale kilogram capacities and file increasing numbers of FDA drug master files. South Korea is deploying USD 260 million for a new SK pharmteco facility slated to open in 2026, underpinning regional surge in GLP-1 and oncology capacity. Japan maintains a leadership position in discovery platforms, as exemplified by PeptiDream’s expanded pact with Novartis. Rising domestic incidence of obesity and cancer also fuels regional demand for metabolic and radiolabeled peptides.

Europe maintains robust volume behind Switzerland, Germany, and the United Kingdom, benefiting from the EMA’s detailed peptide guidance that harmonizes quality expectations. Switzerland alone attracted CHF 2.7 billion of biotech investment in 2024, with Bachem and CordenPharma both announcing large-scale greenfield projects near Basel. The region relies on strong university–industry linkages that feed early-stage innovation into CDMO pipelines. EU Green Deal policies accelerate the adoption of enzymatic synthesis and solvent-recovery technologies, providing grants for low-emission equipment upgrades. Supply-chain resilience initiatives encourage dual sourcing across EU and North American plants, smoothing cross-border peptide flows despite variant GMP codes.

Competitive Landscape

The peptide synthesis market is moderately consolidated, with the top five suppliers accounting for an estimated 55-60% of global revenues. Bachem, PolyPeptide Group, and CordenPharma leverage decades of process know-how, large reactor fleets, and international quality certifications to anchor high-margin custom manufacturing contracts. Their competitive edge rests on end-to-end service bundles covering discovery libraries, process development, GMP production, and fill-finish. Mid-tier players in Asia are climbing the value chain by investing in high-throughput purification trains and real-time release analytics, narrowing historical quality gaps.

Capacity expansion is the dominant strategic theme. CordenPharma’s EUR 900 million outlay adds twin peptide mega-plants in Switzerland and the United States, boosting annual capacity for GLP-1 analogs by roughly 2 metric tons. PolyPeptide’s multi-site debottlenecking program lifts purification output and adds NADES-based green solvents that cut waste by 15%. Asian entrants such as Zhejiang Xianju and Chengdu Nuoer are investing in automated SPPS lines with 150-liter reactors capable of multikilogram batches, positioning for global supply agreements.

Technology differentiation remains pivotal. Leaders deploy AI-guided route scouting to cap raw-material cost variance and predictive maintenance on synthesizers to raise uptime beyond 95%. The adoption of flow chemistry for short peptides and enzyme-mediated ligation for more extended sequences is creating new white-space opportunities. Sustainable manufacturing closed-loop solvent recovery, recyclable resins, and renewable-energy sourcing has evolved from a compliance necessity to a commercial differentiator, winning environmentally focused sponsor contracts. Partnerships between instrument vendors and CDMOs are accelerating tech rollout, with revenue-sharing models that align incentives with efficiency gains.

Peptide Synthesis Industry Leaders

Merck KGaA

Thermo Fisher Scientific Inc.

GenScript

Bachem Holding AG

Biotage AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Ellara completed the build-out of a small-scale peptide facility in Russia’s Vladimir Region, aiming for a Q1 2026 start-up.

- October 2025: SK pharmteco invested USD 6.1 million to add SPPS labs and a CGMP kilo suite at its Rancho Cordova, California site.

- April 2025: Sai Life Sciences inaugurated a dedicated Peptide Research Center at its Hyderabad R&D campus.

- March 2025: CordenPharma broke ground on a EUR 500 million greenfield peptide plant in Basel featuring 5,000 L reactors.

- January 2025: BioDuro opened a kilogram-scale SPPS plant in Shanghai’s Zhangjiang tech cluster.

Global Peptide Synthesis Market Report Scope

Peptides are a unique class of highly active and specific pharmaceutical compounds, molecularly poised between small molecules and proteins, yet biochemically and therapeutically diverse from both. The advantages of peptides, such as relative ease of synthesis, ready availability, and low toxicity, have increased their applications in the pharmaceutical, nutritional, and cosmetic industries, resulting in high demand for rapid advancements in the technologies to enhance their synthesis.

The peptide synthesis market is segmented by technology, product, end user, and geography. By technology, the market is segmented into solid-phase, liquid-phase, hybrid, and recombinant. By product, the market is segmented into equipment, reagents and consumables, and services. The reagents and consumables are further segmented into enzymes and others. By end user, the market is segmented into pharmaceutical and biotechnology companies, contract development and manufacturing organizations (CDMO), and academic and research institutes. By geography, the market is segmented into North America, Europe, Asia-Pacific, Latin America, and the Middle East and Africa. The report also covers the market sizes and forecasts in 17 countries across major regions. For each segment, market sizing and projections were based on revenue (USD).

| Solid-Phase | Manual SPPS |

| Automated SPPS | |

| Microwave-Assisted SPPS | |

| Liquid-Phase | Batch LPPS |

| Continuous-Flow LPPS | |

| Hybrid & Recombinant | |

| Cell-Free/Enzymatic |

| Equipment | Peptide Synthesizers |

| Cleavage & Deprotection Systems | |

| Purification (Prep-HPLC) | |

| Lyophilizers | |

| Reagents & Consumables | Amino-Acid Building Blocks |

| Resins | |

| Coupling Reagents & Activators | |

| Solvents | |

| Enzymes | |

| Other Reagents & Consumables | |

| Services | Custom/Catalog Peptide Synthesis |

| GMP Peptide Manufacturing | |

| Peptide Library Design | |

| Post-translational Modification Services |

| Pharmaceutical & Biotechnology Companies |

| Peptide CDMOs & CROs |

| Academic & Research Institutes |

| Diagnostic Laboratories |

| Food & Nutraceutical Producers |

| Cosmetic Manufacturers |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | GCC | |

| Rest of South America | Turkey | |

| By Technique | Solid-Phase | Manual SPPS | |

| Automated SPPS | |||

| Microwave-Assisted SPPS | |||

| Liquid-Phase | Batch LPPS | ||

| Continuous-Flow LPPS | |||

| Hybrid & Recombinant | |||

| Cell-Free/Enzymatic | |||

| By Product Type | Equipment | Peptide Synthesizers | |

| Cleavage & Deprotection Systems | |||

| Purification (Prep-HPLC) | |||

| Lyophilizers | |||

| Reagents & Consumables | Amino-Acid Building Blocks | ||

| Resins | |||

| Coupling Reagents & Activators | |||

| Solvents | |||

| Enzymes | |||

| Other Reagents & Consumables | |||

| Services | Custom/Catalog Peptide Synthesis | ||

| GMP Peptide Manufacturing | |||

| Peptide Library Design | |||

| Post-translational Modification Services | |||

| By End-User | Pharmaceutical & Biotechnology Companies | ||

| Peptide CDMOs & CROs | |||

| Academic & Research Institutes | |||

| Diagnostic Laboratories | |||

| Food & Nutraceutical Producers | |||

| Cosmetic Manufacturers | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| Australia | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | GCC | ||

| South Africa | |||

| Rest of Middle East and Africa | |||

| South America | Brazil | ||

| Argentina | GCC | ||

| Rest of South America | Turkey | ||

Key Questions Answered in the Report

What is the current value of the peptide synthesis market?

The peptide synthesis market stands at USD 1.90 billion in 2026 and is forecast to reach USD 2.59 billion by 2031.

Which technique dominates global peptide production?

Solid-phase synthesis leads with 75.36% market share in 2025 thanks to decades of process optimization and wide reagent availability.

Why are CDMOs growing faster than in-house manufacturing?

Biopharma firms prefer asset-light models, so they outsource complex, capital-intensive peptide production to CDMOs that offer end-to-end, GMP-compliant services.

Which region is expanding most rapidly?

Asia-Pacific is projected to post a 6.78% CAGR through 2031, driven by Chinese and South Korean capacity additions and cost-competitive services.

What is the biggest hurdle to large-scale peptide manufacturing?

High process-mass intensity and stringent impurity controls make peptides costly to produce and scale, adding pressure to adopt greener, more efficient technologies.

Page last updated on: