Open Compute Project (OCP) Servers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

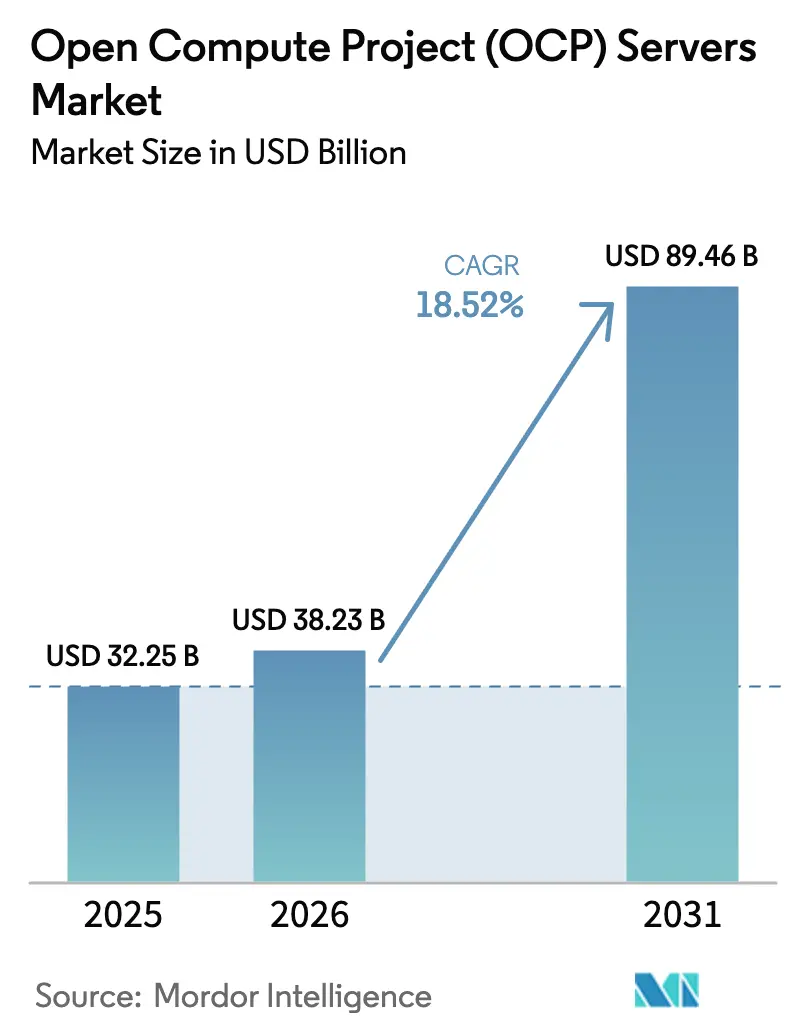

| Market Size (2026) | USD 38.23 Billion |

| Market Size (2031) | USD 89.46 Billion |

| Growth Rate (2026 - 2031) | 18.52% CAGR |

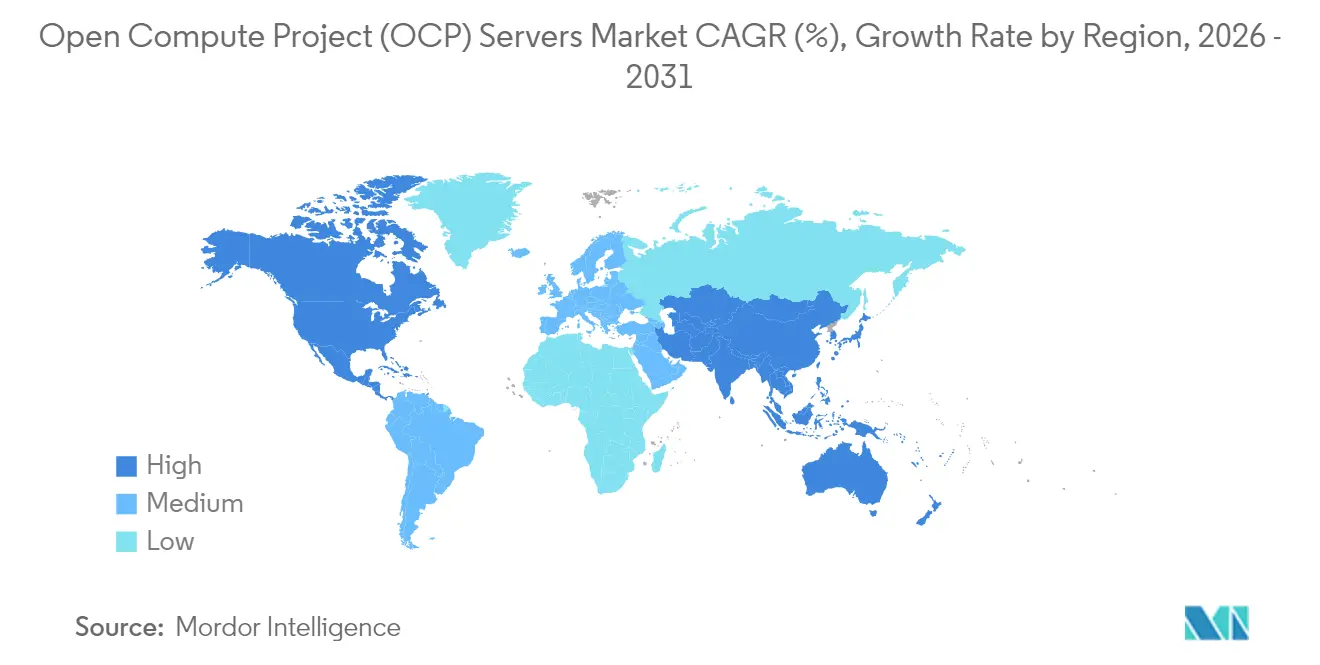

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Open Compute Project (OCP) Servers Market Analysis by Mordor Intelligence

The Open Compute Project (OCP) Servers Market size in 2026 is estimated at USD 38.23 billion, growing from 2025 value of USD 32.25 billion with 2031 projections showing USD 89.46 billion, growing at 18.52% CAGR over 2026-2031. Steady momentum stems from hyperscalers that bypass legacy OEM catalogs to purchase disaggregated hardware directly from original design manufacturers, reducing the total cost of ownership by 20-30% through standardized 48-volt power, liquid-cooling-ready chassis, and rack-level integration. Generative-AI clusters that break past 100 kW per rack, sovereign-cloud mandates in Asia-Pacific and the Middle East, and Europe’s circular-economy incentives together amplify adoption, while the arrival of liquid cooling and 800G Ethernet reshapes component priorities. ODM lead times of 30-60 days, versus the 90-day industry norm, alongside published field data showing power-usage-effectiveness levels near 1.08, underscore the financial and sustainability advantages that drive the Open Compute Project servers market to expand at a pace that surpasses mainstream enterprise server refresh cycles.

Key Report Takeaways

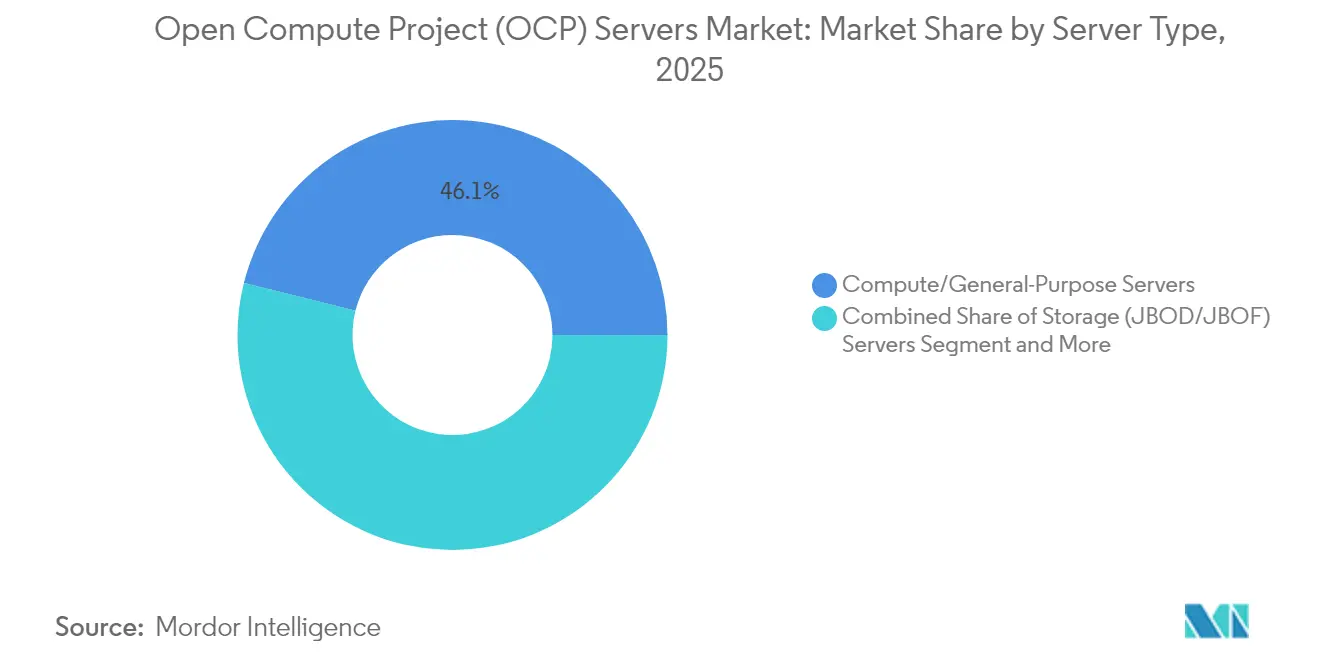

- By server type, compute/general-purpose servers retained 46.12% of the Open Compute Project (OCP) server market in 2025; however, accelerator/GPU servers are forecast to compound at a 20.62% CAGR through 2031.

- By component, compute nodes led the Open Compute Project (OCP) server market with 41.92% in 2025, while networking switches are forecast to compound at a 22.38% CAGR through 2031.

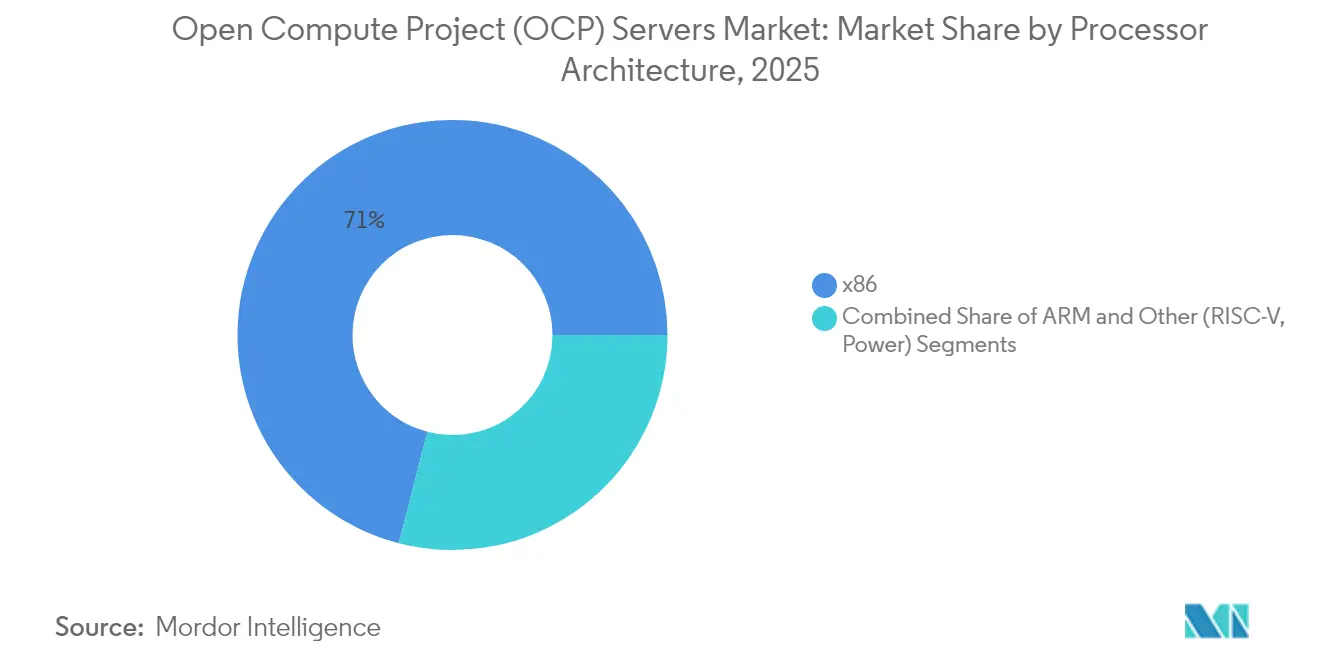

- By processor architecture, x86 devices held a 70.98% share in 2025, whereas ARM-based chips are expected to register the strongest 19.63% CAGR to 2031.

- By end-user type, service providers captured 63.74% of 2025 spend; enterprises are poised for a 22.06% CAGR through 2031.

- By geography, North America retained 38.12% of the Open Compute Project (OCP) server market in 2025; however, Asia-Pacific is forecast to compound at a 21.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Open Compute Project (OCP) Servers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost Reduction and Power Efficiency | +3.2% | Global, highest in North America and Asia-Pacific | Medium term (2-4 years) |

| High Degree of Customization and Flexibility | +2.8% | North America and Europe | Medium term (2-4 years) |

| Hyperscale Data Center Expansion | +4.5% | Global, led by North America then Asia-Pacific and Middle East | Short term (≤ 2 years) |

| Rapid AI/ML Workload Deployment Cycles | +4.1% | North America and Asia-Pacific, spillover to Europe and Middle East | Short term (≤ 2 years) |

| Circular-Economy Incentives for Refurbished OCP Gear | +1.9% | Europe rising, early North America | Long term (≥ 4 years) |

| Telco Edge Adoption for Private-5G Micro-Sites | +2.4% | Asia-Pacific and North America, early Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Hyperscale Data Center Expansion

Annual capex commitments from Microsoft, Amazon, and emerging sovereign clouds extend multi-gigawatt roadmaps that favor disaggregated racks over proprietary frames. Microsoft and OpenAI’s USD 100 billion Stargate initiative aims for 5 GW of AI capacity by 2028 and is standardizing on 48-volt, liquid-cooled ORv3 racks for GB200 NVL72 clusters. [1]Financial Times, “Microsoft and OpenAI Announce $100bn Stargate AI Project,” ft.com Meta’s Catalina rollout shows 30-fold inference speed gains and 25-fold energy savings per token when paired with 140 kW high-performance racks. [2]Meta, “Building Meta’s GenAI Infrastructure,” engineering.fb.com Liquid-cooling envelopes of 480 kW per rack in Dell’s IR7000 underscore density leaps unreachable with air-cooled OEM chassis. [3]Dell Technologies, “IR7000 Spec Sheet,” delltechnologies.com Public-investment-fund projects in Saudi Arabia replicate the U.S. hyperscale blueprint and lock in OCP specifications for regional digital-sovereignty targets.

Rapid AI/ML Workload Deployment Cycles

NVIDIA’s annual cadence, from Hopper to Blackwell to the expected Rubin, compresses hardware refresh windows to 12-18 months, rewarding modular sleds that allow operators to swap GPUs without touching the rack backbone. ODMs, such as Wiwynn and Quanta, ship pre-certified systems within 30-60 days, halving validation times compared to OEMs and propelling the adoption of accelerator racks. Dell forecasts that AI will account for 50% of total processing by 2026, intensifying demand for NVMe-oF storage servers that feed dense GPU fabrics. Microsoft’s single order for 1,400-1,500 NVL72 racks in 2024 exemplifies the scale of immediate deployments.

Cost Reduction and Power Efficiency

Open Rack v3 mandates 48-volt distribution, reducing conversion losses to 7% and saving USD 50,000 per MW annually at a power tariff of 0.10 USD/kWh. Meta reports a 1.08 PUE, which is well below the legacy data center averages, and AWS demonstrates 99% hardware reuse rates, extending server life from five to six years. These gains translate into 20-30% lower total cost of ownership, the core economic lure that accelerates enterprise pilots despite service-support concerns.

Telco Edge Adoption for Private-5G Micro-Sites

Telecom operators are pivoting to OCP gear for Open RAN and private 5G rollouts that demand commodity economics and sub-10 ms latency. Dish’s nationwide U.S. deployment reports site capex down 30% when substituting proprietary radio gear with 21-inch edge servers. Rakuten Symphony offers a turnkey Open RAN stack globally, integrating white-box switches and OCP servers to meet the stringent latency requirements of industrial IoT applications.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lack of Vendor Support and After-Sales Service | -1.8% | Europe and emerging markets | Medium term (2-4 years) |

| Integration Complexity with Legacy Infrastructure | -2.3% | Europe and North America | Short term (≤ 2 years) |

| Enterprise Reliability and Liability Concerns | -1.9% | Regulated verticals worldwide | Medium term (2-4 years) |

| Patent-Litigation Risk for Open Hardware IP | -1.2% | North America and Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Integration Complexity with Legacy Infrastructure

Most enterprise data halls still utilize 19-inch racks and 12-volt rails, so integrating 21-inch, 48-volt OCP frames necessitates new distribution, raised-floor layouts, and sometimes the installation of chilled-water loops. A 2024 Uptime Institute survey found that only 14% of European enterprises had any OCP footprint, compared to a 42% penetration among North American hyperscalers. Integration timelines can triple when storage fabrics and backup regimes must interoperate with open-hardware management stacks. Auto makers adopting hybrid topologies now budget 15-20% more upfront capex to reconcile proprietary storage arrays with OCP GPU racks.

Enterprise Reliability and Liability Concerns

OEMs promise four-hour on-site support and indemnity clauses; ODM warranties often limit coverage to depot repairs that can take up to 10 days, prompting insurers to raise premiums by up to 15% for facilities that rely chiefly on open hardware. Ongoing 48-volt power-module patent suits filed by Vicor against Delta, Foxconn, and Quanta add perceived legal risk that can stall procurement, particularly in healthcare and government bids. Traditional vendors responded by launching OCP-compliant systems such as Dell’s IR7000 and Lenovo ThinkSystem SR lines, bundling open design with familiar service contracts to reduce liability hesitations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Server Type: GPU Racks Reshape Hyperscale Buildouts

Accelerator platforms are tracking a 20.62% CAGR and will eclipse historic compute spend as AI training standardizes on 72-GPU NVL72 and MI325X enclosures consuming up to 140 kW. Compute and general-purpose units retained a 46.12% market share of 2025 Open Compute Project servers, but their expansion slowed to the mid-teens as hyperscalers redirected budgets toward AI-focused nodes.

Meta’s Catalina deployment validated 30-fold inference gains while Microsoft’s 1,400-plus rack commitment illustrates fleet-wide transitions already underway. Storage sleds, powered by EDSFF drives, are expected to grow at a 17.94% CAGR to alleviate bottlenecks between petascale datasets and GPU memory. Edge and micro-data-center units, key to Open RAN and 5G, are advancing at a 19.12% CAGR and anchoring new Open Compute Project server market opportunities among telcos seeking commodity cost curves.

By Component: Networking Switches Surge on 800G Adoption

Compute nodes held a 41.92% component share in 2025; however, networking switches led growth at a 22.38% CAGR, as operators deploy 800-gigabit Ethernet for GPU-to-GPU interconnects and adopt distributed switching fabrics embedded in OCP racks. Meta and Microsoft deployed 800-gigabit Ethernet in 2024 to support NVIDIA GB200 NVL72 clusters, which require 3.6 terabits per second of bisection bandwidth, while traditional top-of-rack switches are being replaced by single-chip designs that reduce latency by 40%.

The shift to 48-volt power distribution, standardized in the Open Rack v3 specification, reduces conversion losses from 12% to 7%, resulting in an annual savings of USD 50,000 per megawatt at an electricity rate of USD 0.10 per kilowatt-hour. Vicor's patent litigation against Delta Electronics, Foxconn, and Quanta over 48-volt power modules introduces supply-chain risk, as potential injunctions could halt shipments to hyperscalers. Dell's IR7000 integrates liquid-cooling manifolds that support up to 480 kilowatts per rack, targeting enterprises deploying private AI clusters.

By Processor Architecture: ARM Gains on Cloud-Native Workloads

ARM-based systems grow at a 19.63% clip, steadily nibbling at x86’s 70.98% 2025 stronghold. AWS Graviton4, Microsoft Cobalt 100, and Ampere Altra Max all tout 40% better performance per watt for containerized workloads, a metric that resonates as operators strive for lower energy density and licensing fees.

RISC-V evaluation boards remain in pre-production, leaving the near-term contest essentially between ARM and x86. Intel Xeon 6 and AMD EPYC 5th Gen chiplet designs maintain x86 performance leadership in legacy and transactional back-office applications. However, a growing mix-and-match rack strategy, sanctioned under DC-MHS v2, allows both architectures to coexist side by side, reinforcing hardware agility within the Open Compute Project servers market.

By End-User Type: Enterprises Accelerate Private AI Deployments

Service providers, including hyperscalers and telcos, accounted for 63.74% of 2025 shipments, while enterprise adoption shows a sharper trajectory, expanding at a rate of 22.06% per year. Automotive firms lead, training autonomous-vehicle models on in-house GPU farms to sidestep cloud fees while safeguarding IP.

Healthcare and financial services players are chasing similar control with imaging and fraud-detection clusters, respectively, confirming a broadening appeal beyond tech natives. Tier-2 clouds leverage ODM pricing to compete against hyperscale incumbents, and telcos rely on 21-inch edge servers for Open RAN to reduce site TCO by 30%, collectively sustaining a diverse demand mix that underpins long-term durability for the Open Compute Project servers market.

Geography Analysis

North America retained a 38.12% share in 2025, driven by concentrated hyperscale footprints in Northern Virginia, Oregon, and Texas. Market maturity, land scarcity, and grid pressure taper the CAGR to 17.46%, yet orders, such as Microsoft’s Stargate racks, still elevate overall revenue pools. Dell’s IR7000 and AMD’s ZT Systems purchase illustrate expanded vertical integration and OEM counter-offensives designed for domestic enterprises worried about open-hardware support gaps.

The Asia-Pacific region is expected to show the highest 21.12% CAGR through 2031. Taiwan’s Foxconn, Wiwynn, Quanta, and Inventec collectively generate 60% of the worldwide OCP server output, feeding the growing hyperscalers in India, Indonesia, and Vietnam. Regional data-sovereignty edicts that prioritize local assembly accelerate deployments, while Rakuten Symphony’s Open RAN success story sparks orders for sub-10 ms industrial IoT services throughout the region.

The European region is also growing due to limited reference wins and supply-chain fragmentation. Delegated Regulation 2024/1364 requires data halls exceeding 500 kW to disclose PUE, WUE, and renewable energy fractions as of September 2024, encouraging operators to adopt OCP rack modularity, which facilitates audit compliance. The South American region is also accelerating as Brazil and Argentina expand their cloud footprints, while the Middle East, driven by Saudi Arabia’s USD 6 billion data center fund, and Africa are developing geothermal-powered edge zones, such as G42’s Azure region in Kenya.

Competitive Landscape

Roughly 60% of 2024 capex is concentrated in the top ten players, positioning the Open Compute Project servers market in a moderately consolidated yet fiercely contested arena. Foxconn is on course to become the world’s largest server vendor in 2024 on record GB200 allocations, whereas Super Micro’s USD 3.85 billion fiscal-Q3 revenue reflects triple-digit year-over-year growth and a 30-day lead-time promise that undercuts traditional schedules.

AMD’s USD 4.9 billion deal for ZT Systems marks the chip-maker's ambition to own design while maintaining contract-manufacturing neutrality, hinting at future competition between vertically integrated silicon houses and incumbent ODMs. Dell, HPE, and Lenovo unveil hybrid strategies, including the IR7000, Cray EX, and ThinkSystem SR lines, that bridge OCP openness with full-service contracts, enticing enterprises deterred by multi-vendor support gaps.

Circular-economy niches are gaining traction as AWS reports 23.5 million reused components and a 99% reuse rate within its fleet, sparking a 25% annual growth for refurbishment marketplaces. Patent battles such as Vicor’s 48-volt module suit threaten supply continuity but also motivate innovation in power-conversion designs that sidestep contested IP. White-box networking specialist Edgecore claims a 15% share of hyperscale Ethernet ports at 40% lower average selling prices, highlighting ongoing price pressure across hardware layers.

Open Compute Project (OCP) Servers Industry Leaders

Quanta Cloud Technology (QCT)

Wiwynn Corporation

Inspur Information

Foxconn (Hon Hai Precision)

Inventec Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Microsoft and OpenAI announced the USD 100 billion Stargate project targeting 5 GW of AI capacity by 2028 with OCP-compliant GPU racks and liquid cooling.

- October 2024: Dell Technologies introduced the PowerEdge XR7000 (IR7000), an OCP-compliant system that supports 480 kW of liquid cooling and modular GPU trays, designed for enterprise AI clusters.

Global Open Compute Project (OCP) Servers Market Report Scope

The Global Open Compute Project Servers Market Report is Segmented by Server Type (Compute/General-Purpose Servers, Storage (JBOD/JBOF) Servers, Accelerator/GPU Servers, Edge/Micro Data-Center Servers), Component (Compute Nodes, Storage Nodes, Networking Switches, Power Shelves and Cooling), Processor Architecture (x86, ARM, Other RISC-V/Power), End-User Type (Service Providers [Hyperscale, Telco, Tier-2 CSP], Enterprises [Manufacturing, Healthcare, Government, Financial Services, Automotive/Industrial, Other Industry Verticals]), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Compute/General-Purpose Servers |

| Storage (JBOD/JBOF) Servers |

| Accelerator/GPU Servers |

| Edge/Micro Data-Center Servers |

| Compute Nodes |

| Storage Nodes |

| Networking Switches |

| Power Shelves and Cooling |

| x86 |

| ARM |

| Other (RISC-V, Power) |

| Service Providers | Hyperscale |

| Telco | |

| Tier-2 CSP | |

| Enterprises | Manufacturing |

| Healthcare | |

| Government | |

| Financial Services | |

| Automotive/Industrial | |

| Other Industry Verticals |

| North America |

| South America |

| Europe |

| Asia-Pacific |

| Middle East |

| Africa |

| By Server Type | Compute/General-Purpose Servers | |

| Storage (JBOD/JBOF) Servers | ||

| Accelerator/GPU Servers | ||

| Edge/Micro Data-Center Servers | ||

| By Component | Compute Nodes | |

| Storage Nodes | ||

| Networking Switches | ||

| Power Shelves and Cooling | ||

| By Processor Architecture | x86 | |

| ARM | ||

| Other (RISC-V, Power) | ||

| By End-User Type | Service Providers | Hyperscale |

| Telco | ||

| Tier-2 CSP | ||

| Enterprises | Manufacturing | |

| Healthcare | ||

| Government | ||

| Financial Services | ||

| Automotive/Industrial | ||

| Other Industry Verticals | ||

| By Geography | North America | |

| South America | ||

| Europe | ||

| Asia-Pacific | ||

| Middle East | ||

| Africa | ||

Key Questions Answered in the Report

How large is the Open Compute Project servers market in 2026?

It is valued at USD 38.23 billion and is forecast to expand to USD 89.46 billion by 2031.

Which server type is growing the fastest?

Accelerator and GPU racks are advancing at 20.62% CAGR through 2031, outpacing all other categories.

What drives the shift toward 48-volt power rails?

The Open Rack v3 design trims power-conversion loss to 7% and can save USD 50,000 per MW each year at typical electricity prices.

Why are enterprises embracing OCP hardware now?

Lower total cost, avoidance of vendor lock-in, and modular upgrades for AI workloads push enterprise CAGR to 22.06% through 2031.

Which region will post the highest growth?

Asia-Pacific leads with a 21.12% CAGR, fueled by Taiwan ODM production and rising sovereign-cloud spend in India and Southeast Asia.

How are OEMs responding to ODM competition?

Vendors such as Dell, HPE, and Lenovo now ship OCP-compliant lines that pair open hardware with familiar 4-hour on-site service contracts.

Page last updated on: