Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

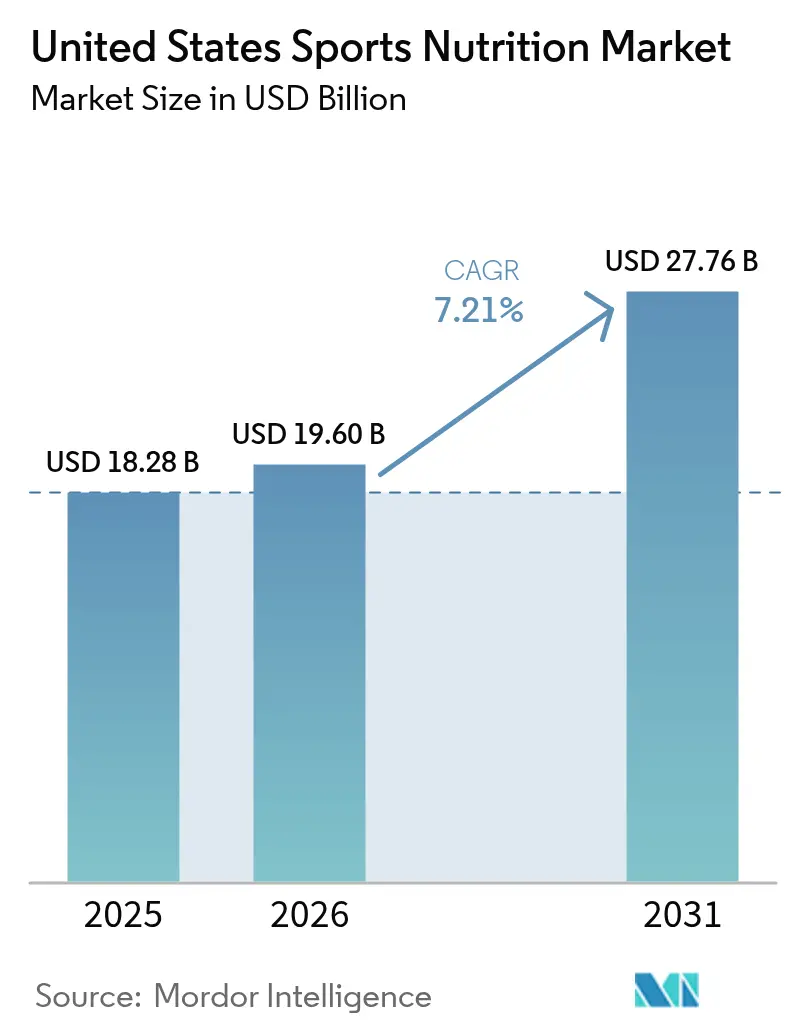

| Base Year Market Size (2025) | USD 18.28 Billion |

| Market Size (2026) | USD 19.6 Billion |

| Market Size (2031) | USD 27.76 Billion |

| Growth Rate (2026 - 2031) | 7.21% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

United States Sports Nutrition Market Analysis by Mordor Intelligence

The United States sports nutrition market size was valued at USD 18.28 billion in 2025 and estimated to grow from USD 19.6 billion in 2026 to reach USD 27.76 billion by 2031, at a CAGR of 7.21% during the forecast period (2026-2031). While athletes and bodybuilders remain core consumers, the market has expanded significantly to include recreational users, weekend warriors, and lifestyle enthusiasts, driven by increased health awareness and rising disposable income. This evolution from a niche athletic segment to a mainstream wellness category is supported by the democratization of fitness culture, digital health integration, and regulatory modernization across key markets. The growth is further amplified by the increasing number of health and fitness centers that actively promote sports nutrition products to their members. The market's transformation reflects a broader shift in consumer preferences toward sustainable nutrition, indicating that traditional users alone cannot sustain the market's growth trajectory. As the industry continues to evolve, manufacturers must adapt their product offerings and marketing strategies to meet the diverse needs of this expanding consumer base while maintaining high quality and safety standards.

Key Report Takeaways

- By product type, protein products led with 83.05% of the United States sports nutrition market share in 2025, whereas non-protein products are projected to register an 8.35% CAGR to 2031.

- By source, animal-based ingredients accounted for 60.72% share of the United States sports nutrition market size in 2025, while plant-based sources are forecast to expand at 9.78% CAGR between 2026-2031.

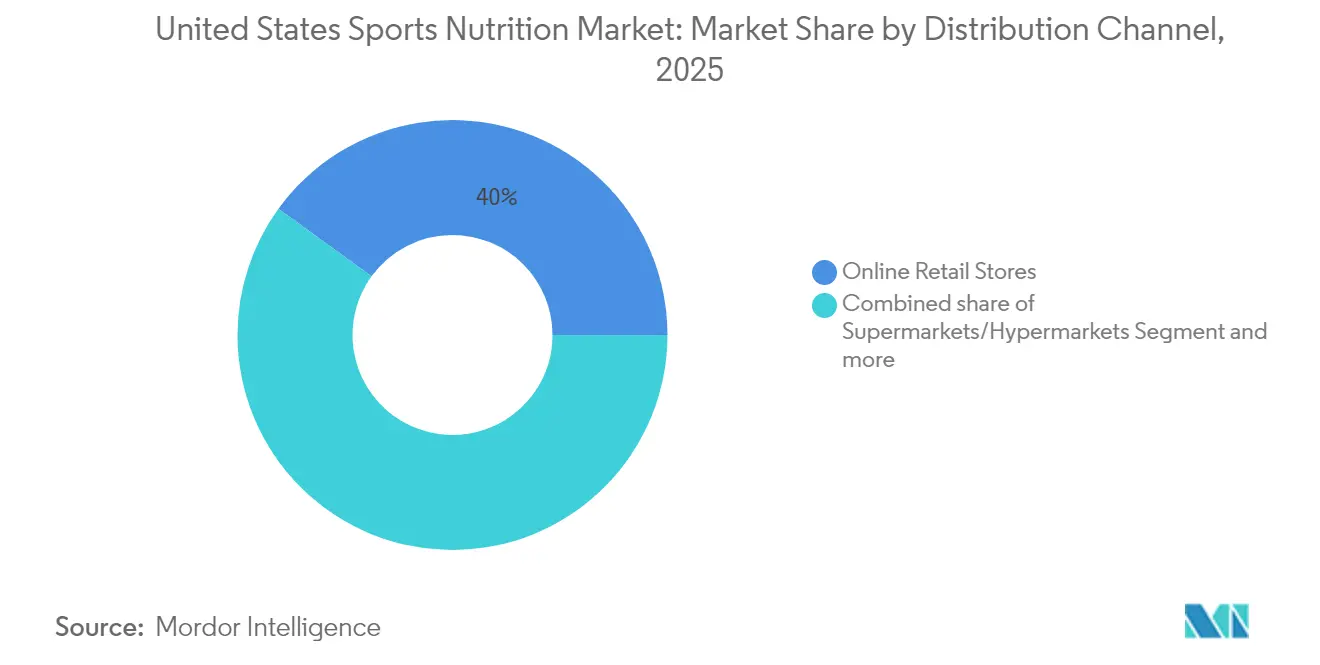

- By distribution channel, online retail stores captured 40.02% of the United States sports nutrition market size in 2025 and are poised to grow at a 10.74% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Sports Nutrition Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Spike in outdoor fitness activities | +1.8% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| University athletics programs | +1.2% | North America and Europe, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Availability of functional combination products | +1.5% | Global | Short term (≤ 2 years) |

| Rise in plant based sports nutrition products | +2.1% | North America and Europe core, spill-over to Asia-Pacific | Medium term (2-4 years) |

| Growing influence of social media and fitness influencers | +1.7% | Global, strongest in North America and Asia-Pacific | Short term (≤ 2 years) |

| Rising demand for personalized nutrition solutions | +1.4% | North America and Europe, early adoption in urban Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Spike in outdoor fitness activities

The post-pandemic period witnessed a significant shift in sports nutrition demand patterns, driven by increased outdoor fitness participation. According to the Sports and Fitness Industry Association [1]Source: Sports and Fitness Industry Association, "2024 Sports, Fitness, and Leisure Activities Topline Participation Report,” sfia.org, 242 million Americans (78.8% of the population) engaged in physical activities in 2023, marking a 2.2% increase from the previous year. This trend, which has shown consistent growth for ten consecutive years with 5 million new participants in 2023, has influenced product development in the sports nutrition market. Manufacturers are now focusing on portable, weather-resistant formulations, particularly energy gels and ready-to-drink protein beverages, to support extended outdoor activities. The emphasis on outdoor fitness has also increased demand for hydration and electrolyte replacement products. In response, companies are developing specialized formulations incorporating natural preservatives and temperature-stable ingredients to maintain product efficacy across various environmental conditions. This ongoing evolution in consumer preferences and product development is expected to continue shaping the sports nutrition market, driving innovation and growth in outdoor-focused nutritional solutions.

University athletics programs

University athletics programs drive the sports nutrition market in the United States through their comprehensive nutrition and supplementation programs for student-athletes. These programs create demand for protein powders, energy drinks, and recovery supplements to support athletic performance and recovery. The expanding student-athlete population and increased nutrition awareness contribute to market growth. The sports nutrition market in the United States benefits from a well-established distribution network of specialty retailers, online platforms, and university partnerships. Professional sports teams and training facilities across the country have also adopted similar nutrition protocols, creating a trickle-down effect that influences amateur athletes and fitness enthusiasts. The National Collegiate Athletic Association's (NCAA) [2]Source: National Collegiate Athletic Association, "Driving Change for Today's Student Athletes", ncaa.org mandatory nutrition education requirement, effective August 2024, further strengthens the demand for sports nutrition supplements among collegiate athletes. The market continues to evolve with innovations in personalized nutrition solutions and clean-label products that cater to specific athletic performance requirements.

Availability of functional combination products

The convergence of multiple nutritional benefits into single-serving formats addresses consumer demand for convenience while maximizing bioactive compound synergies, particularly in pre-workout and recovery formulations. Companies are developing sophisticated combination products that merge protein, electrolytes, vitamins, and adaptogens to support multiple physiological pathways simultaneously. This trend extends beyond traditional categories, as demonstrated by Caribe Juice's May 2024 launch of WTRMLN ADE, an electrolyte-rich hydration beverage available in three flavors, indicating a significant market opportunity for recovery-focused combination products. The integration of multiple functional ingredients in a single product reduces the need for consumers to purchase and consume multiple supplements separately, thereby improving adherence to supplementation regimens. The growing awareness among athletes and fitness enthusiasts about the importance of comprehensive nutrition support has prompted manufacturers to invest in research and development of these multi-functional formulations. Additionally, the success of combination products in the market has encouraged retailers to allocate more shelf space to these innovative offerings, further accelerating their adoption among consumers.

Rise in plant-based sports nutrition products

Plant-based protein adoption is accelerating beyond environmental considerations, driven by digestibility advantages and amino acid profile innovations that challenge traditional whey protein dominance. According to Glanbia Nutritionals, [3]Source: Glanbia Nutritionals, "5 Plant-Based Protein Trends for 2025," glanbianutritionals.com 25% of US consumers identify as flexitarian. This trend is evident in new product launches, such as Plezi Nutrition's sports drink introduction in March 2025. The beverage, available in Lemon Lime, Tropical Punch, and Orange Mango Twist flavors, features naturally gluten-free and plant-based ingredients, reflecting the market's shift toward plant-based alternatives in sports nutrition. The increasing consumer awareness about plant-based protein benefits has prompted established sports nutrition companies to expand their product portfolios with vegan options. Additionally, improvements in taste and texture of plant-based formulations have addressed previous barriers to adoption among athletes and fitness enthusiasts. The integration of diverse protein sources, including pea, hemp, and rice proteins, has also enabled manufacturers to create complete amino acid profiles that match the nutritional benefits of animal-based proteins.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent regulatory standards by FDA and FTC | -1.3% | North America, with spillover effects globally | Medium term (2-4 years) |

| Prevalence of counterfeit or adulterated products | -0.9% | National, concentrated in emerging markets | Short term (≤ 2 years) |

| Limited consumer awareness in certain demographic segments | -0.7% | Emerging markets and rural areas | Long term (≥ 4 years) |

| High product costs limiting adoption among price-sensitive consumers | -0.8% | National, particularly in price-sensitive markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent regulatory standards by FDA and FTC

Regulatory requirements in the United States sports nutrition market operate within a complex framework established by the Food and Drug Administration (FDA) and Federal Trade Commission (FTC). The FDA mandates manufacturers to follow Good Manufacturing Practices and provide accurate product labels containing ingredients, nutritional information, and allergen warnings. New dietary ingredients require pre-market FDA approval, involving extensive time and financial resources. Companies that fail to meet these regulatory standards risk substantial financial penalties and product recalls, which increase operational risks and costs. Product development timelines extend, and production costs increase due to required documentation, testing procedures, and certification processes. These comprehensive regulatory measures, while ensuring product safety and consumer protection, significantly impact market dynamics and operational strategies in the U.S. sports nutrition industry.

Prevalence of counterfeit or adulterated products

The prevalence of adulterated products in the sports nutrition market, particularly in supplements and performance enhancers, presents significant challenges to market growth. These counterfeit products not only pose severe health risks to consumers but also result in substantial revenue losses for legitimate manufacturers and retailers. The FDA has documented numerous cases of supplements containing undeclared ingredients, banned substances, and incorrect labeling, leading to increased regulatory scrutiny and enforcement actions across the supply chain. In February 2025, One Source Nutrition, Inc. issued a voluntary nationwide recall of Vitality Capsules due to the presence of undeclared Sildenafil and Tadalafil [4]Source: U.S. Food & Drug Administration, "Recalls Market Withdrawals Safety Alerts", fda.gov according to FDA. The rise in adulteration cases has prompted regulatory bodies to implement stricter quality control measures and testing protocols for sports nutrition products. Consumer trust has been negatively impacted by these incidents, resulting in heightened skepticism toward supplement manufacturers and their products. The increasing costs associated with quality assurance and compliance measures have forced many smaller manufacturers to exit the market. These challenges collectively hamper the growth potential of the United States sports nutrition market, necessitating industry-wide efforts to maintain product integrity and rebuild consumer confidence.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Protein Products Dominate Despite Non-Protein Acceleration

Sports protein products maintain market leadership with an 83.05% share in 2025, reflecting protein's essential role in muscle synthesis and recovery across athletic performance levels. Sports non-protein products represent the fastest-growing segment with an 8.35% CAGR through 2031, driven by advanced pre-workout formulations and specialized recovery compounds that address specific physiological needs beyond protein supplementation. The dominance of protein products is further reinforced by increasing awareness among recreational athletes and fitness enthusiasts about the importance of protein timing and dosage for optimal results.

Within protein products, powder formulations remain dominant due to cost efficiency and customization flexibility, while ready-to-drink formats gain market share through convenience benefits. Energy gels and BCAA powders in the non-protein segment show growth as consumers become more knowledgeable about targeted supplementation approaches and their specific performance benefits. The market also witnesses increased demand for multi-component protein blends that offer varied absorption rates and amino acid profiles to support different training phases.

By Source: Plant-Based Disruption Accelerates Animal-Based Dominance

Animal-based protein sources hold a 60.72% market share in 2025, primarily due to whey protein's complete amino acid profile and strong reputation among performance-focused athletes. Plant-based alternatives are projected to grow at a 9.78% CAGR through 2031, supported by better digestibility, environmental sustainability benefits, and improved protein isolation technologies that enhance taste and solubility. The dominance of animal-based proteins is further reinforced by their established supply chains and widespread consumer acceptance in traditional sports nutrition markets.

The plant-based segment continues to expand beyond traditional pea and soy proteins, incorporating hemp, pumpkin seed, and fermentation-derived proteins with distinct nutritional benefits. The rise of flexitarian consumers has increased demand for hybrid products that combine plant and animal proteins to balance performance and sustainability. While the segment faces higher production costs compared to whey protein, ongoing technological advancements and increased production scale are reducing this gap. New fermentation methods and agricultural technologies enable the development of plant proteins with amino acid compositions comparable to animal proteins. Market research indicates that consumer education about plant protein benefits and increased retail availability are key factors driving adoption across diverse demographic groups.

By Distribution Channel: Online Retail Achieves Dual Leadership

Online retail stores hold 40.02% market share in 2025 and are projected to grow at 10.74% CAGR through 2031. This growth stems from the channel's ability to provide product education, subscription options, and direct consumer engagement. The trend indicates a shift in purchasing patterns, especially among younger consumers who value convenience, user reviews, and personalized product suggestions. The expansion of mobile shopping applications and secure payment gateways further strengthens the dominance of online retail in the United States Sports Nutrition market.

Traditional retail channels, including supermarkets, pharmacies, and specialty stores, retain substantial market presence but experience increasing competition from online platforms that offer wider product selection and competitive prices. The integration of social commerce through Instagram and TikTok creates additional sales opportunities, particularly in reaching Gen Z consumers. Online channel growth is supported by improved logistics networks, lower delivery costs, and enhanced product verification systems that address consumer concerns about supplement quality. Despite these challenges, physical stores maintain their relevance through expert staff consultation and immediate product availability, which remain valuable to certain consumer segments.

Geography Analysis

The United States market benefits from high disposable income levels and an advanced distribution infrastructure across specialty retailers and mainstream supermarkets. The Dietary Supplement Health and Education Act (DSHEA) regulatory framework provides manufacturers with operational clarity while enabling product innovation. However, increased FDA oversight creates compliance requirements that benefit larger companies with substantial resources. The market's robust e-commerce infrastructure further enhances accessibility and consumer reach across the country.

The region's consumer base has expanded beyond traditional bodybuilders to include fitness enthusiasts, aging populations, and health-conscious individuals. This demographic shift drives demand for convenient, multi-functional formulations. Social media significantly influences purchasing decisions, particularly among younger consumers. Market research indicates that personalized nutrition and targeted supplementation continue to gain traction among these diverse consumer segments.

The adoption of GLP-1 medications for weight management presents growth opportunities as consumers seek nutrition products to maintain muscle mass during weight loss. Companies are developing specialized formulations for this market segment. In June 2024, Pure Protein launched an all-in-one protein powder for GLP-1 users, offering an accessible solution to address nutrient deficiency side effects associated with these medications. Industry analysts project this specialized segment to experience substantial growth as GLP-1 adoption increases across the United States.

Competitive Landscape

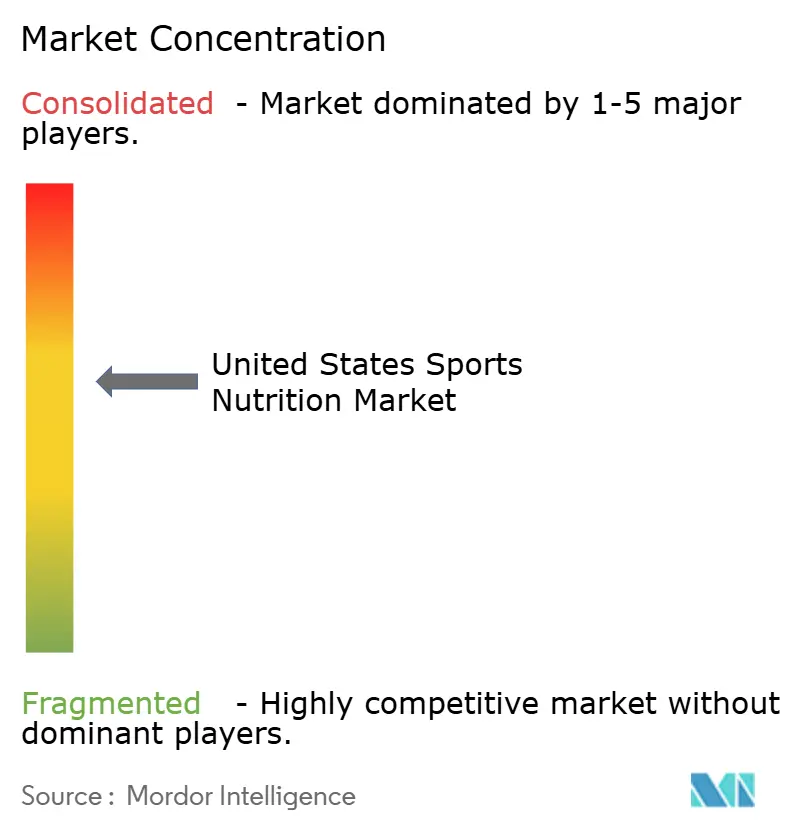

The United States sports nutrition market exhibits moderate fragmentation with established multinational corporations competing alongside specialized direct-to-consumer brands that leverage digital marketing and niche positioning strategies. Market leaders including Glanbia, Abbott, and PepsiCo maintain competitive advantages through scale economies, distribution reach, and Research and Development capabilities, while emerging players disrupt traditional categories through innovative formulations and targeted demographic focus. The market's competitive dynamics continue to evolve as companies adapt to changing consumer preferences and technological advancements.

Companies are pursuing vertical integration strategies by investing in ingredient sourcing, manufacturing capabilities, and direct-to-consumer channels to improve profit margins. Success in the market depends on regulatory compliance, supply chain transparency, and sustainability practices while maintaining product effectiveness and competitive pricing. These strategic initiatives enable companies to better control quality standards and respond quickly to market demands.

Companies are forming strategic partnerships to increase their market presence. In September 2024, C4 partnered with The Hershey Company to launch confectionery-inspired products across multiple categories. The collaboration introduced new Energy Drinks, Pre-Workout supplements, and a Protein Powder line featuring three candy-inspired variants, marking the first protein powder products for both companies. This partnership demonstrates the industry's trend toward innovative flavor profiles and cross-category expansion to attract new consumer segments.

United States Sports Nutrition Industry Leaders

-

Glanbia PLC

-

Now Foods

-

The Coca Cola Company

-

Abbott Laboratories Inc.

-

PepsiCo Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Edible Garden launched Kick Sports Nutrition on Amazon through a partnership with Pirawna, an e-commerce growth agency managing over USD 500 million in Amazon revenue. The collaboration aims to strengthen the brand's entry into the sports nutrition market.

- January 2025: Cizzle Brands launched Spoken Nutrition, an NSF Certified for Sport nutraceutical product line designed for athletes. The sports nutrition company introduced this premium performance supplement range to expand its health and wellness portfolio.

- October 2024: Reebok formed a partnership with Generation Joy to distribute Reebok-branded sports nutrition products in the United States and Canada. The product line includes protein and collagen supplements, vitamins, pre-workout and post-workout supplements, and hydration products.

- January 2024: Abbott has introduced the PROTALITY brand, offering nutritional support for adults managing their weight. The product line features a high-protein nutrition shake that combines fast- and slow-digesting proteins, designed to provide sustained muscle nourishment for up to seven hours.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the United States sports nutrition market as value sales of sports-targeted protein powders, ready-to-drink (RTD) protein, energy or recovery bars, amino-acid blends, creatine, and similar non-protein formulas that are marketed to improve athletic performance, muscle recovery, or body composition. The consumer base runs from professional athletes to lifestyle exercisers who use these products to complement regular training routines.

Scope exclusion: Conventional hydration beverages and energy drinks positioned primarily for casual refreshment are not counted.

Segmentation Overview

-

By Product Type

-

Sports Protein Products

-

Powder

- Whey And Casein Powder

- Plant based Protein Powder

- Other Sports Protein Powder

- Protein Ready to Drink

- Protein /Energy Bars

-

Powder

-

Sports Non Protein Products

- Energy Gels

- BCAA Powder

- Creatine Powder

- Other Sports Non Protein Products

-

Sports Protein Products

-

By Source

- Animal-based

- Plant-based

-

By Distribution Channel

- Supermarkets/Hypermarkets

- Pharmacy/Health Stores

- Online Retail Stores

- Other Distribution Channels

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed formulators, contract manufacturers, specialty retailers, collegiate athletic trainers, and e-commerce category buyers across all four U.S. census regions. These conversations confirmed channel mix shifts, typical plant-based ASP premiums, and allowable inclusion rates for ingredients such as beta-alanine, letting us fine-tune assumptions born from desk work.

Desk Research

We began with public datasets such as USDA FoodData Central, FDA 483 inspection records, and Physical Activity Council participation surveys, which clarify product definitions, labeling constraints, and consumption cohorts. Trade bodies including the Council for Responsible Nutrition and Sports & Fitness Industry Association supplied shipment tonnage, club memberships, and athlete demographics that anchor demand pools. Company 10-K filings, investor decks, and press releases added average selling price (ASP) direction. Proprietary collections like D&B Hoovers for company revenue splits and Dow Jones Factiva for launch counts filled further gaps. The sources named illustrate the breadth consulted; many additional public and subscription outlets were reviewed to validate figures.

Market-Sizing & Forecasting

A top-down demand pool model starts with U.S. adult and youth exercise participation, layers average use incidence and standard servings per active user, and multiplies by verified ASPs. Supplier roll-ups of whey processors and selected online store checks act as a bottom-up reasonableness test, and mismatches beyond five percent trigger re-work. Key variables include gym membership penetration, plant-based share progression, Amazon supplement best-seller rank velocity, collegiate sports scholarships, and ingredient cost indices. Forecasts employ multivariate regression blended with scenario analysis, where coefficients are stress-tested with primary experts for sensitivity before finalizing the 2025-2030 outlook.

Data Validation & Update Cycle

Outputs pass anomaly checks, cross-tab variance reviews, and senior analyst sign-off. Reports refresh every twelve months; interim updates are issued if regulation, major recalls, or M&A events materially shift model drivers.

Why Mordor's United States Sports Nutrition Baseline Commands Credibility

Published estimates often differ because publishers vary product baskets, channel inclusion, currency conversions, and update cadence.

Key gap drivers here include whether mainstream sports drinks are bundled, how online discounting is captured in ASPs, and if forecast models apply constant or sliding participation rates. Mordor's scope excludes hydration drinks, applies monthly ASP tracking from specialty retailers, and refreshes annually, which together deliver a balanced midpoint between optimistic channel-stuffing numbers and conservative retail-only views.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 18.28 B (2025) | Mordor Intelligence | - |

| USD 15.70 B (2024) | Global Consultancy A | Includes mainstream sports drinks and uses fixed 2020 ASP benchmarks |

| USD 10.23 B (2023) | Trade Journal B | Excludes online DTC sales and applies constant athlete cohort only |

| USD 15.63 B (2023) | Industry Analyst C | Combines sports and weight-management supplements, inflating total |

In summary, the disciplined scoping, live ASP monitoring, and dual-check modelling adopted by Mordor Intelligence give decision-makers a dependable, transparent baseline they can retrace and update with ease.

Key Questions Answered in the Report

What is the projected value of the sports nutrition supplements market by 2031?

The market is forecast to reach USD 27.76 billion in 2031 on a 7.21% CAGR trajectory.

Which product segment currently commands the largest revenue share?

Protein-based products held 83.05% share in 2025, reflecting their entrenched role in muscle recovery routines.

How fast is the plant-based source segment growing?

Plant-based ingredients are set to expand at 9.78% CAGR between 2026-2031, the highest rate among source categories.

Why is online retail outperforming other channels?

Subscription models, influencer-driven education, and expedited last-mile logistics help online retail advance at 10.74% CAGR through 2031.

Page last updated on: