Mints Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

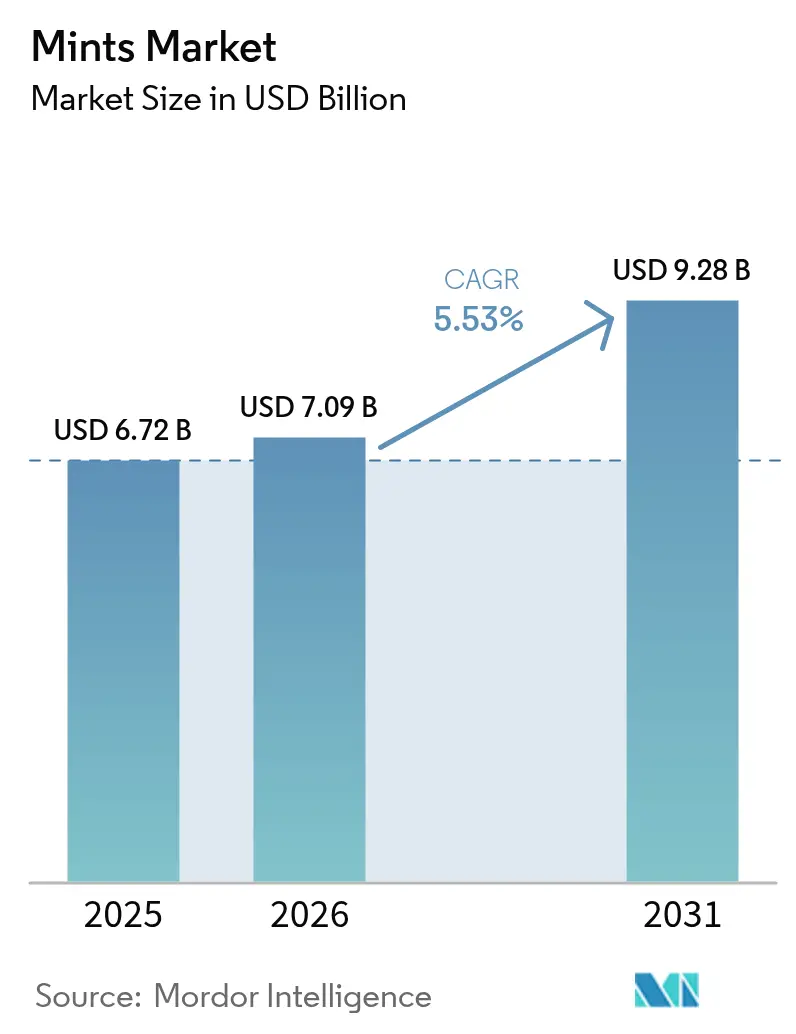

| Market Size (2026) | USD 7.09 Billion |

| Market Size (2031) | USD 9.28 Billion |

| Growth Rate (2026 - 2031) | 5.53% CAGR |

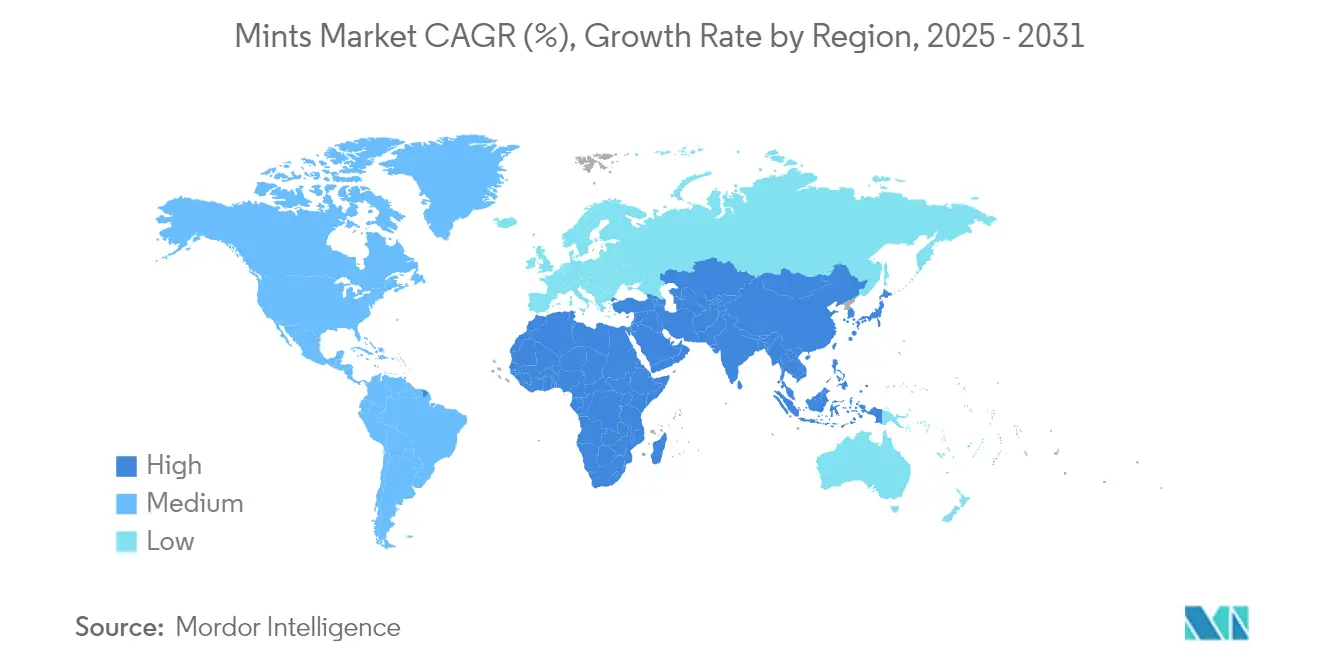

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Mints Market Analysis by Mordor Intelligence

Mint market size in 2026 is estimated at USD 7.09 billion, growing from 2025 value of USD 6.72 billion with 2031 projections showing USD 9.28 billion, growing at 5.53% CAGR over 2026-2031. The market's growth trajectory is bolstered by a robust demand for breath-freshening products, an increasing inclination towards functional confectionery, and their heightened availability via online platforms. Distinct value propositions emerge from premium positioning, sugar-free reformulations, and eco-friendly packaging, appealing to a diverse consumer base. While shoppers in mature economies gravitate towards gourmet and organic choices, emerging markets witness volume growth driven by rising disposable incomes and a burgeoning middle class. This moderate fragmentation in the market enables both global giants and nimble regional players to seize new consumption opportunities, intensifying competition and driving relentless innovation in flavors and formats.

Key Report Takeaways

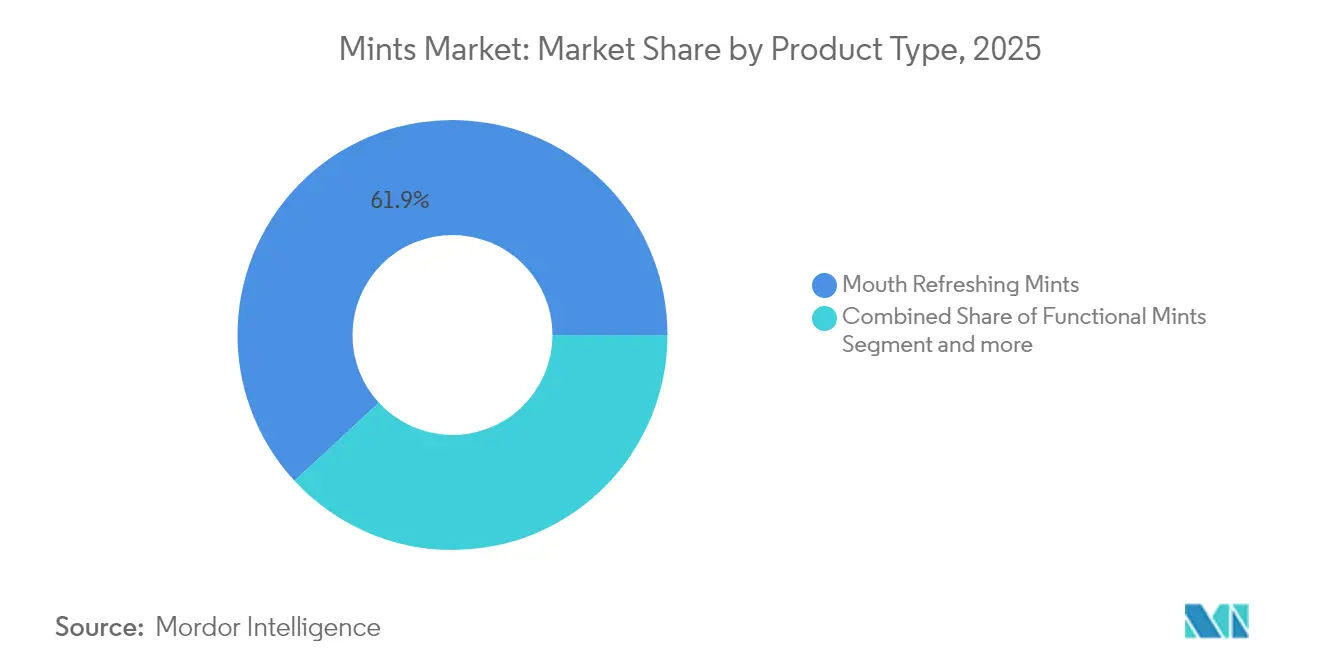

- By product type, Mouth Refreshing Mints held 61.86% of Mint market share in 2025, while Functional Mints are projected to expand at a 5.98% CAGR to 2031.

- By sugar content, Sugar Mints accounted for 64.41% share of the Mint market size in 2025, whereas Sugar-Free Mints are set to advance at a 5.61% CAGR through 2031.

- By flavor, Traditional Mint Flavor controlled 72.62% revenue share in 2025, and Fruity Flavors are expected to post a 5.92% CAGR to 2031.

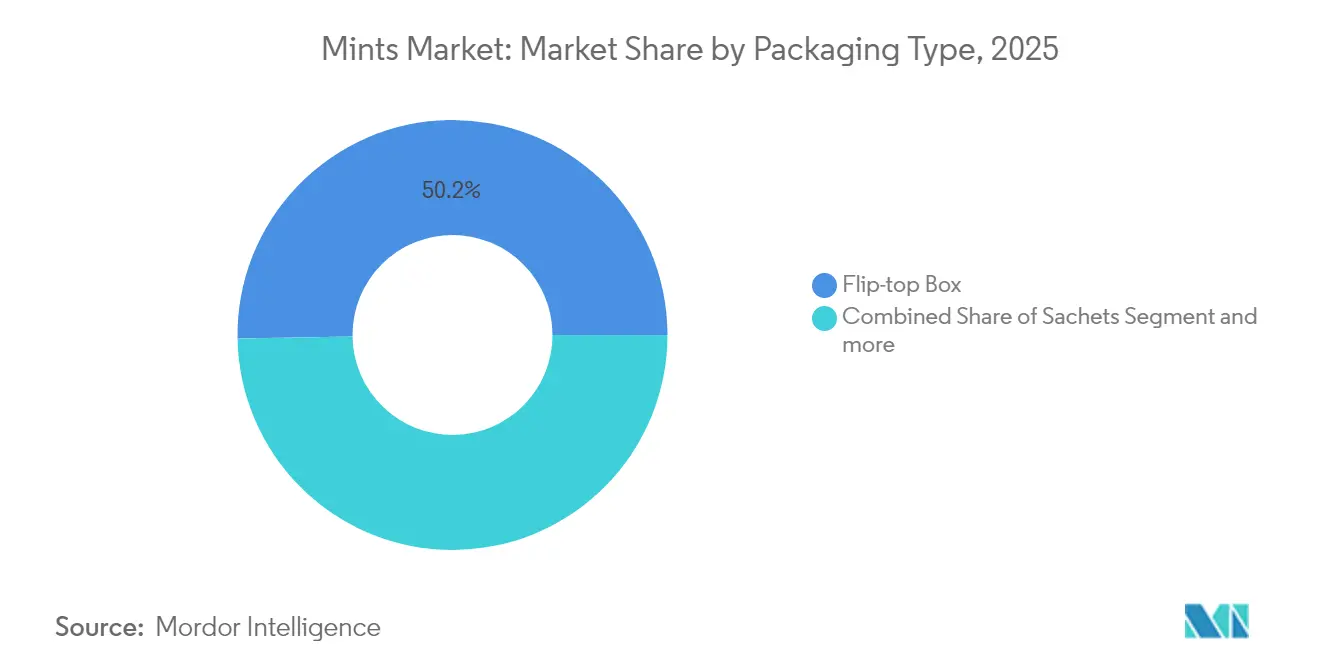

- By packaging, Flip-top Boxes led with 50.25% revenue share in 2025; Sachets are forecast to record a 5.54% CAGR between 2026 and 2031.

- By distribution channel, Supermarkets/Hypermarkets captured 45.27% revenue share in 2025, while Online Retail Stores are projected to grow at an 7.88% CAGR over the forecast period.

- By geography, North America commanded 34.86% revenue share in 2025, whereas Asia-Pacific is anticipated to rise at a 6.76% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Mints Market*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for breath-freshening products is boosting mint confectionery sales. | +1.8% | Global, with higher impact in Asia-Pacific and North America | Medium term (2-4 years) |

| Expansion of online retail enhances accessibility and visibility of mint candies. | +1.2% | Global, particularly strong in developed markets | Short term (≤ 2 years) |

| Innovative flavors and textures are attracting younger and experimental consumers. | +0.9% | North America & EU, expanding to urban Asia-Pacific | Medium term (2-4 years) |

| Premiumization trends fuel interest in gourmet and artisanal mint confections. | +0.7% | North America & EU, selective urban centers in emerging markets | Long term (≥ 4 years) |

| Compact and portable packaging supports on-the-go consumption of mints. | +0.6% | Global, with emphasis on urban centers | Short term (≤ 2 years) |

| Cultural and social habits sustain regular use of mints for oral freshness. | +1.1% | Global, with regional variations in consumption patterns | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing demand for breath-freshening products is boosting mint confectionery sales.

The growing demand for breath-freshening products continues to drive the expansion of the mint confectionery market. Consumers, particularly busy professionals, smokers, and individuals who consume alcohol, increasingly rely on mints as a convenient solution to mask odors or as a quick alternative to traditional oral hygiene when time is constrained. Additionally, the rising awareness of health and wellness is pushing buyers toward sugar-free and natural mint options, which are widely regarded as beneficial for dental health and overall well-being. Product innovation plays a pivotal role in sustaining market growth. Manufacturers are introducing new flavors and hybrid mints enriched with functional ingredients such as caffeine or herbal extracts, catering to diverse consumer preferences and enhancing product appeal. The impulse-driven nature of mint purchases, coupled with visually appealing packaging and extensive availability across retail channels, further encourages frequent buying and experimentation with new offerings. These evolving consumer behaviors and preferences are expected to support the steady growth of the global mint confectionery market throughout the forecast period. The market's ability to adapt to changing demands, such as the preference for healthier and multifunctional products, positions it for sustained expansion over the next decade.

Expansion of online retail enhances accessibility and visibility of mint candies.

Food e-commerce has emerged as a significant driver of online sales, accounting for 30% of total online sales in key markets like South Korea. According to the USDA, this segment is witnessing a strong 12% year-on-year growth, reflecting the rapid transformation in consumer purchasing behaviors[1]United States Department of Agriculture, "South Korea Food Ecommerce Market", apps.fas.usda.gov. The digital commerce landscape is reshaping how consumers discover and purchase mint products by offering capabilities that traditional retail channels cannot match. Features such as subscription models and bulk purchasing options address the increasing demand for convenience and cost-effectiveness. Additionally, advanced algorithm-driven recommendations are broadening consumer access to a diverse range of premium and functional mint variants, many of which are unavailable in physical stores. This digital shift is particularly advantageous for smaller, innovative brands that often encounter challenges in traditional retail distribution. By leveraging direct-to-consumer channels, these brands can overcome conventional barriers, gain quicker market entry, and utilize real-time consumer feedback to refine and accelerate their product innovation cycles. This transformation is fostering a more competitive and dynamic market environment, driving sustained growth and innovation across the sector. As digital commerce continues to evolve, it is expected to play a pivotal role in shaping the future of the food e-commerce market.

Innovative flavors and textures are attracting younger and experimental consumers.

Manufacturers are broadening flavor innovations beyond the conventional mint profiles, infusing exotic botanicals and functional ingredients. This strategy aims to captivate younger demographics in search of distinctive sensory experiences. Such a pivot resonates with the rising consumer appetite for diverse and refined taste options, where an array of choices signals product quality and brand ingenuity. Notably, Millennials and Generation Z are steering this trend, emphasizing experiential consumption. They gravitate towards brands showcasing innovative flavors, often sidelining those anchored in traditional brand loyalty. Data from the US Census Bureau highlights the significance of this demographic shift: in 2024, Millennials emerged as the predominant generation in the U.S., constituting roughly 21.81% of the population[2]United States Census Bureau, "Population and Housing Unit Estimates", www.census.gov. Furthermore, the adoption of natural sweeteners like monk fruit and stevia not only bolsters flavor experimentation but also underscores a health-centric approach, aligning with the rising demand for healthier yet flavorful alternatives.

Premiumization trends fuel interest in gourmet and artisanal mint confections.

Mint products are transitioning from basic confections to premium lifestyle accessories, driven by changing consumer preferences. Shoppers are increasingly willing to pay higher prices for attributes such as organic certification, artisanal production techniques, and sustainable packaging solutions. The USDA's organic flavor certification program, which now includes over 14,000 certified organic flavor products, including mint, highlights the growing emphasis on transparency and quality assurance in flavor sourcing[3]United States Department of Agriculture, "United States Department of Agriculture Agricultural Marketing Service | National Organic Program Document Cover Sheet", www.ams.usda.gov. This trend of premiumization is particularly prominent in developed markets, where higher disposable incomes enable consumers to invest in premium, functional products. In contrast, emerging markets are experiencing selective adoption, primarily in urban areas. Here, premium positioning not only reflects social status but also aligns with a rising focus on health and wellness among urban consumers.

Restraints Impact Analysis of Mints Market*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing concerns over sugar intake are limiting traditional mint candy consumption. | -1.4% | Global, particularly acute in developed markets with health awareness | Medium term (2-4 years) |

| Regulatory pressure on food labeling and health claims complicates marketing. | -0.8% | EU & North America primarily, expanding globally | Short term (≤ 2 years) |

| Strong presence of substitute products like chewing gum reduces mint consumption. | -1.1% | Global, with regional preferences varying | Long term (≥ 4 years) |

| Rising environmental concerns discourage use of plastic-heavy mint packaging. | -0.5% | EU & North America leading, Asia-Pacific following | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing concerns over sugar intake are limiting traditional mint candy consumption.

Growing health consciousness is significantly impacting the consumption of traditional sugar-based mints, as consumers increasingly scrutinize ingredient labels and prioritize products that align with their wellness objectives. The Center for Science in the Public Interest's 2024 report sheds light on regulatory gaps in flavor safety evaluations, emphasizing how the GRAS (Generally Recognized as Safe) loophole enables the inclusion of thousands of flavor chemicals in food products without formal FDA oversight. This lack of stringent regulation, combined with rising awareness of diabetes and obesity, is accelerating the shift toward sugar-free alternatives[4]Center For Science In The Public Interest, "Hidden Ingredients What are 'Flavors' and 'Spices,' and are they Safe?", www.cspinet.org. Consequently, traditional mint manufacturers face mounting pressure to reformulate their offerings with natural sweeteners to meet evolving consumer preferences. Failure to adapt could result in a significant loss of market share to competitors who are strategically positioning themselves with health-focused product innovations.

Strong presence of substitute products like chewing gum reduces mint consumption.

Chewing gum manufacturers are increasingly launching sugar-free formulations that not only offer extended flavor release but also provide added functional benefits, such as oral health support. This strategic shift is intensifying competition with adjacent oral care categories. As the gum market approaches maturity, innovation is pivoting towards sugar-free mints, a segment experiencing significant growth, particularly in Asia. The rapid expansion in this region highlights the rising consumer preference for healthier and more convenient alternatives. However, the threat of substitution extends beyond direct competitors within the mint category. Products such as breath sprays, oral strips, and probiotic lozenges, which deliver similar functional benefits while offering unique consumption experiences, are gaining traction. This diversification is fragmenting the traditional mint market share, distributing it across a broader range of product categories. In response to these challenges, mint manufacturers are shifting their strategies. They are focusing on creating distinct value propositions to differentiate their offerings, rather than relying solely on their historical dominance within the category. This approach aims to address evolving consumer demands and maintain competitiveness in an increasingly crowded market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Mints Market Segment Analysis

By Product Type:

Mouth Refreshing Mints Dominates and Functional Mints AcceleratesIn 2025, Mouth Refreshing Mints hold a dominant 61.86% market share, highlighting their pivotal role in traditional oral hygiene practices and their appeal as an impulse purchase across global markets. This segment's leadership is rooted in consumer trust, driven by its proven ability to provide immediate breath-freshening solutions. These mints are particularly valued in social and professional settings, where maintaining oral hygiene confidence is essential. Furthermore, the segment benefits from well-established distribution networks and strategic point-of-sale placements, which effectively capture consumer attention and drive impulse purchases in retail environments.

Functional Mints set to grow with a projected CAGR of 5.98% through 2031. This growth is propelled by increasing consumer demand for products that offer health benefits beyond basic breath freshening. The segment leverages scientific research supporting the therapeutic properties of mint, particularly peppermint oil, which has demonstrated efficacy in managing irritable bowel syndrome symptoms and its antimicrobial effects on oral microbiomes. These effects include reducing harmful bacteria such as Prevotella, Streptococcus, and Neisseria species. The rise of functional mints aligns with broader health and wellness trends, as consumers increasingly seek products that combine multiple benefits within familiar formats. This positions functional mints as a hybrid offering, bridging the gap between traditional confectionery products and nutraceutical solutions.

By Sugar Content:

Sugar Mints Dominates where Sugar-Free Mints AcceleratesIn 2025, Sugar Mints hold a dominant 64.41% market share, highlighting the sustained popularity of traditional formulations despite increasing health concerns over sugar consumption. This segment's leadership is driven by ingrained consumer taste preferences, affordability, and habitual purchasing patterns, which collectively hinder the rapid adoption of reformulated alternatives. The segment remains particularly robust in emerging markets, where cost considerations often outweigh health-focused positioning, and in traditional retail channels, where impulse purchases tend to favor well-known and trusted products.

Sugar-Free Mints, on the other hand, are propelling category growth with a projected CAGR of 5.61% through 2031, reflecting a gradual but noticeable shift in consumer preferences toward healthier options. This trend is especially evident among diabetic consumers and health-conscious demographics seeking indulgent yet guilt-free alternatives. The growth of sugar-free formulations is supported by advancements in sweetener technologies, such as the use of natural alternatives like monk fruit, which preserve flavor profiles while eliminating caloric content. Furthermore, certifications from organizations like Toothfriendly International, endorsing products such as Vita Pharmed's NotSore range, provide credible third-party validation. These certifications play a crucial role in enhancing consumer confidence and driving the adoption of sugar-free alternatives.

By Flavor:

Mint Flavor Dominates and Fruity Flavor AcceleratesIn 2025, the mint flavor holds a commanding 72.62% market share, reflecting its strong alignment with consumer preferences and strategic brand positioning centered on delivering authentic mint experiences with reliable breath-freshening efficacy. This segment's dominance is attributed to deeply ingrained consumer associations between mint and oral hygiene benefits, reinforced by decades of targeted marketing and widespread cultural acceptance across global markets. Furthermore, the production of traditional mint flavoring remains cost-effective, supported by robust and well-established supply chain networks, which further solidify its market leadership.

Fruity flavors are projected to grow at a 5.92% CAGR through 2031, driven by increasing demand from younger demographics seeking diverse and innovative taste experiences that go beyond traditional mint profiles. This growth aligns with a broader trend in the confectionery market, where offering a variety of flavors is perceived as a marker of product sophistication and brand creativity. Advances in sweetener and flavor technologies, such as rubusoside and steviol glycosides, have enabled manufacturers to develop complex and appealing flavor profiles without compromising health-conscious positioning. This shift toward flavor diversification resonates strongly with millennials and Generation Z, who prioritize unique and experiential consumption over conventional brand loyalty, further fueling the segment's expansion.

By Packaging:

Flip-top Box Dominates and Sachets AcceleratesIn 2025, Flip-top Box packaging holds a commanding 50.25% market share, driven by its ability to combine consumer convenience with robust product protection. This packaging format plays a pivotal role in supporting premium product positioning and fostering repeat purchase behavior. Its dominance is attributed to features such as maintaining product freshness, enabling precise portion control, and creating a distinctive shelf presence that enhances brand differentiation. The flip-top format is particularly appealing to consumers who value convenient access while ensuring the product's integrity across multiple consumption occasions, making it a preferred choice in the market.

Sachets are positioned as the fastest-growing packaging format, with a projected CAGR of 5.54% through 2031. This growth is propelled by increasing consumer preferences for portion control and a heightened focus on environmental sustainability. The rising demand for sachets reflects a shift in consumer priorities, where reducing packaging waste significantly influences purchasing decisions, especially among environmentally conscious demographics. Additionally, the evolution of sachet packaging aligns with global regulatory trends aimed at minimizing plastic usage. Over 45 countries are actively implementing or drafting new packaging standards, including bans on single-use plastics and mandates for minimum recycled content, further driving the adoption of sustainable packaging solutions.

By Distribution Channel:

Supermarkets/Hypermarkets Dominates and Online Retail Stores AcceleratesIn 2025, Supermarkets and Hypermarkets maintain a dominant 45.27% market share, driven by their ability to integrate impulse buying seamlessly with routine shopping patterns. These channels benefit from established relationships with traditional retailers, strategic product placements near checkout counters, and consumer familiarity with store layouts, particularly for mint products. Additionally, cross-merchandising strategies and targeted promotional campaigns significantly contribute to incremental sales growth. By aligning these factors strategically, Supermarkets and Hypermarkets continue to reinforce their leadership position in the market, offering a comprehensive shopping experience that caters to diverse consumer needs.

Online Retail Stores are projected to grow at a robust CAGR of 7.88% through 2031, reflecting the transformative influence of digital commerce on consumer purchasing behaviors. The pandemic has accelerated the adoption of online grocery shopping, with convenience, personalized subscription models, and enhanced accessibility reshaping consumption patterns. This channel is particularly well-suited for premium and functional mint products, which often require detailed product information and consumer education. Unlike traditional retail, online platforms provide an opportunity to engage consumers with tailored content, fostering informed purchasing decisions and driving growth in these specialized segments.

Geography Analysis

North America Mints Market

In 2025, North America commands a 34.86% share of the global mint market, underscoring its consumers' long-standing commitment to oral hygiene and a retail landscape adept at promoting premium products. This regional leadership is bolstered by high disposable incomes, a pronounced health consciousness, and a cultural inclination towards functional foods that offer wellness advantages beyond mere nutrition. While traditional mint consumption persists, there's a notable shift towards organic and natural products, a trend validated by USDA organic certifications ensuring quality and transparency in sourcing. Moreover, the region's intricate regulatory landscape offers clear guidelines for product development and marketing claims, fostering innovation within set boundaries.

APAC Mints Market

Asia-Pacific is on track to be the fastest-growing region, boasting a projected CAGR of 6.76% through 2031. This growth is fueled by a burgeoning middle class, heightened awareness of oral hygiene, and the cultural embedding of mint in daily practices. Urban centers, in particular, are witnessing a surge in demand for convenient oral care products, spurred by an accelerated adoption of Western lifestyles. Companies like Asahi Group Holdings are capitalizing on this trend, with offerings such as MINTIA mint tablets, showcasing their adeptness at merging global mint concepts with local tastes and distribution methods.

EMEA and South America Mints Market

Europe, South America, and the Middle East & Africa stand as notable players in the mint market, albeit with a more tempered growth trajectory. These regions present a dual-edged sword for mint manufacturers: a tapestry of diverse cultural preferences and a maze of regulatory intricacies. European markets, for instance, place a premium on sustainability and organic certifications. The EU's stringent spice market regulations, emphasizing food safety, traceability, and labeling, significantly shape mint product development and marketing approaches. While there's a discernible uptick in the adoption of premium and functional mint products across these regions, growth remains subdued. This is largely attributed to entrenched local preferences and a price sensitivity that curtails the reach of premium products beyond urban locales.

Regulatory Landscape

Regulation affecting mints is primarily driven by horizontal food rules on labeling, claims, import controls, and facility registration. In July 2026, the FAO/WHO Codex Alimentarius Commission (CAC49) adopted new guidance on precautionary allergen labeling (PAL) to be annexed to the General Standard for the Labelling of Pre-packaged Foods (CXS 1-1985), strengthening an international reference point for how manufacturers use and justify \"may contain\" statements on packaged confectionery.\n\nCross-border compliance requirements have tightened for brands sourcing flavors and ingredients globally. In the EU, Commission Implementing Regulation (EU) 2026/194 (January 2026) and 2026/1206 (June 2026) updated how official controls are applied to certain imported high-risk food and feed, raising the importance of robust supplier documentation and testing workflows for importers and co-manufacturers. In China, GACC issued guidance under Decree 280 (effective 1 June 2026) for overseas food facility registration, adding operational steps for exporters of packaged foods into the China market; in the UK, amendments to official controls for high-risk food and feed of non-animal origin came into force on 1 January 2026, reinforcing import compliance obligations for selected ingredient streams used in confectionery.

Competitive Landscape

The global mint market is moderately consolidated, characterized by a few dominant players holding significant market shares alongside numerous regional and niche brands. Leading companies such as Ferrero International S.A., Mondelez International, Mars, Incorporated, Perfetti Van Melle Holding B.V., and Nestlé S.A. have leveraged their extensive global distribution networks and strong brand equity to maintain a competitive edge, particularly in the sugar-free and functional mint segments. However, the growing consumer demand for clean-label, organic products, and innovative formats—such as functional mints enriched with probiotics or vitamins—has created opportunities for emerging players to carve out market space.

Despite the dominance of key players, the market remains competitive due to factors like product diversification, the expansion of private labels, and varying regional preferences. This balance between market concentration and fragmentation reinforces its moderately consolidated structure. Competition is particularly intense in areas such as functional ingredients and sustainable packaging, where smaller, agile players often lead innovation. Larger companies frequently adopt these successful concepts through acquisitions or internal development, further driving market evolution.

Strategic initiatives in the market increasingly focus on vertical integration and direct-to-consumer models, enabling companies to enhance quality control, reduce operational costs, and gather valuable consumer data to inform product development. Innovation remains a priority, as evidenced by patent activity in sweetener and flavor compositions. Advances in rubusoside and steviol glycosides have facilitated the creation of sugar-free formulations that retain taste appeal, addressing consumer preferences for healthier options. Additionally, significant growth opportunities exist in the functional mint segment, particularly in emerging markets. Rising disposable incomes and increasing health consciousness in these regions are accelerating the adoption of premium products, especially those positioned to deliver oral health benefits alongside broader wellness advantages.

Mints Industry Leaders

-

Ferrero International S.A.

-

Mondelez International

-

Mars, Incorporated

-

Perfetti Van Melle Holding B.V.

-

Nestlé SA

- *Disclaimer: Major Players sorted in no particular order

Mints Market Companies Covered in this Report

- Mondelez International Inc.

- Mars, Incorporated (Wrigley)

- Nestle SA

- Perfetti Van Melle Holding B.V.

- Ferrero International S.A.

- Ricola Ltd

- Cloetta AB

- Lotte Corporation

- Grupo Arcor S.A.

- Asahi Group Holdings, Ltd. (Mintia)

- The Hershey Company

- The Procter and Gamble Company

- Ferndale Foods Australia

- Annabelle Candy Company

- Hint Mint Inc.

- Lofthouse of Fleetwood Ltd.

- VerMints Inc.

- Simply Gum

- Midas Care

- Herbion Naturals

Market Opportunities and Future Outlook

Premiumization and reformulation provide whitespace where mint brands can pair recognizable formats (tablets, flip-top boxes, rolls, and sachets) with sugar-free positioning and functional cues, while staying inside tightening rules on labeling and claims. The Codex Commission's July 2026 adoption of guidance on precautionary allergen labeling adds a practical anchor for multinational brands to standardize PAL approaches across SKUs and geographies, reducing label redesign churn and improving confidence in export readiness for products that use complex flavor systems.\n\nOnline discovery and direct-to-consumer mechanics continue to favor differentiated and education-led propositions (functional and sugar-free variants), where digital product pages can explain ingredients, sweeteners, and usage occasions better than shelf tags. Separately, large food and beverage companies are investing in more automated, data-driven manufacturing and distribution footprints in Asia, illustrated by Nestle's July 2026 announcement of a CHF 563 million AI-enabled Nescafe hub in Thailand (170,000 metric tons annual capacity, opening late 2028). While outside mints specifically, this scale of investment reinforces a broader pathway for confectionery supply chains operating in Asia-Pacific to pursue higher traceability, efficiency, and compliance readiness that supports faster SKU rotation and packaging changes across modern trade and e-commerce.

Recent Industry Developments in Mints Market

- April 2026: Ferrero began production of Nutella Peanut at its Franklin Park, Illinois site, supported by a USD 75 million investment that included a new production line. The added US-based capacity and new variant highlight how major confectionery groups keep expanding localized manufacturing footprints to support innovation and reduce supply-chain friction in core markets.

- July 2026: Nestle announced a CHF 563 million AI-enabled Nescafe hub in Thailand, with 170,000 metric tons annual capacity and planned opening in 2028, signaling a major shift in regional manufacturing capacity and advanced automation across beverage and confectionery supply chains.

- January 2024: IMPACT MINTS launched in Australia with Kakao Friends-themed collectible packaging alongside Slim Slide IMPACT MINTS. The launch underscores licensing and pop-culture packaging strategies to differentiate mint formats.

Mints Market Report Scope and Research Methodology

Market Definition and Coverage

This market covers the retail and wholesale value of packaged mints sold for breath freshening and light confectionery consumption, across offline and online channels, and counted at the point where the product is sold into the market.

Scope exclusions: We exclude chewing gum, raw mint ingredients and oils, and mint-flavored candies that are not positioned or sold as mints.

Segments Covered in This Report

-

By Product Type

- Functional Mints

- Mouth Refreshing Mints

- Others

-

By Sugar Content

- Sugar Mints

- Sugar -Free Mints

-

By Flavor

- Mint Flavor

- Fruity Flavors

- Others

-

By Packaging

- Flip-top box

- Rolls/tubes

- Sachets

- Others

-

By Distribution Channel

- Supermarkets /Hypermarkets

- Convenience/Grocery Stores

- Online Retail Stores

- Other Distribution Channels

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- Indonesia

- South Korea

- Thailand

- Singapore

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

-

Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts with compiling a clean fact base for consumption and trade, then mapping how mints are typically sold by channel and region. For this, we use public sources such as UN Comtrade trade statistics, national customs and tariff schedules, the US Census Bureau and Bureau of Labor Statistics for retail and price indicators, Eurostat for consumer and trade series, and FAO datasets that help sanity-check mint-related supply context.

We also review company annual reports, investor presentations, earnings call transcripts, retailer and distributor announcements, and reputable press coverage to understand product positioning and pricing changes. When available, we use paid subscriptions focused on company financials and news, plus import and export shipment-level data and patent databases, to cross-check claims and close gaps without over-assuming. The desk sources listed here are illustrative and not exhaustive, since we used many other public references for data collection and clarification.

Primary Interviews and Surveys

Primary interviews and survey inputs are used to confirm what is counted as mints in each region, and to test price bands and channel splits that are not consistently visible in public datasets. We speak with manufacturers, distributors, and retail category stakeholders, and we also include packaging and ingredient-side viewpoints to validate volume direction and mix shifts across APAC, EMEA, and the Americas.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 14% | APAC: 42% |

| Mid tier: 50% | Functional/Unit leaders: 29% | EMEA: 31% |

| Smaller Players: 22% | Managers: 57% | Americas: 27% |

Market-Sizing & Forecasting

Sizing is built using a top-down approach where confectionery demand pools are reconstructed from consumer spending signals, category share references, and trade and production direction, then filtered to mints based on how the category is sold in each geography. The totals are corroborated using selective bottom-up checks in sampled markets, including supplier and distributor roll-ups, channel checks for key retail formats, and sampled price per pack multiplied by estimated unit movement, which helps us adjust for outliers.

Key inputs that shape the model include regional confectionery spending growth, average selling price movement for small-pack confectionery, sugar-free penetration within mints, pharmacy and convenience store share shifts, and online availability trends that affect reach and assortment. Where a country has limited visibility, we bridge gaps using proxy indicators such as similar market channel structures and trade intensity, followed by re-testing with interview feedback. Forecasting uses scenario analysis supported by short-series trend smoothing, with assumptions on pricing, sugar-free mix, and channel expansion stress-tested before the final path is set.

Data Validation & Update Cycle

Outputs are validated by comparing implied per capita consumption and price points against independent indicators, then reviewing variances by region and channel so the final numbers remain realistic. If a market shows an unusual jump, we re-check the input series, revisit interview notes, and re-contact sources when the change cannot be explained by pricing, distribution, or trade.

Before sign-off, the model is reviewed in multiple steps, first at the analyst level and then through an internal cross-check against related confectionery categories. Reports are refreshed annually, and interim updates are made when material events occur, such as sharp commodity cost shifts or major channel disruptions. Prior to delivery, a final pass is completed so clients receive the latest updated view.

Mordor Intelligence's Mints Market Size Measured Against Other Published Estimates

Published mints market values can look far apart because each publisher makes its own choices on what products qualify as mints, how sugar-free and functional claims are treated, and whether chewing gum or adjacent mint-flavored confectionery is blended into the same total. Differences also show up when one study uses retail sales value and another leans on shipment value, or when exchange rates and inflation timing are handled in different ways.

Some external estimates use a broader definition that blends mints with mint-related formats like gum and other breath care items. Mordor Intelligence counts only packaged mints sold as mints across the listed channels, and it keeps the model anchored to channel mix and price progression checks that were validated through primary discussions.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 7.09 B (2026) | |

| Industry Publisher A | USD 6.10 B (2022) | Uses an older base year and the definition appears broader across end-use mentions, which can mix in mint-related products beyond packaged mints. The time period and price inflation handling are also not aligned to a 2026 current-year view. |

| Global Research Group B | USD 4.21 B (2024) | Employs a narrower 2024 base with different product-form coverage and may net out parts of the category through form splits and consumer targeting filters. The lower total is consistent with tighter inclusion rules and a slower price progression assumption. |

The spread mainly comes from year selection and product coverage choices, followed by how pricing and channel mix are carried forward into the forecast. By keeping the scope tied to packaged mints and then checking the implied price and consumption logic against multiple signals, we end up with a number that is easier to trace back to clear steps and inputs.

Key Questions Answered in the Report

What is the current size of the global mint market?

The market stands at USD 7.09 billion in 2026.

How fast is the global mint market expected to grow?

It is projected to expand at a 5.53% CAGR and reach USD 9.28 billion by 2031.

Which product segment is growing the quickest?

Functional mints lead growth with a forecast 5.98% CAGR through 2031, fueled by added health benefits.

Which region shows the highest growth potential?

Asia-Pacific is the fastest-growing region, projected to register a 6.76% CAGR to 2031, driven by expanding middle-class populations and strong online retail uptake.

Page last updated on: