Nuts And Seeds Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 2.62 Billion |

| Market Size (2031) | USD 3.64 Billion |

| Growth Rate (2026 - 2031) | 6.81% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Nuts And Seeds Market Analysis by Mordor Intelligence

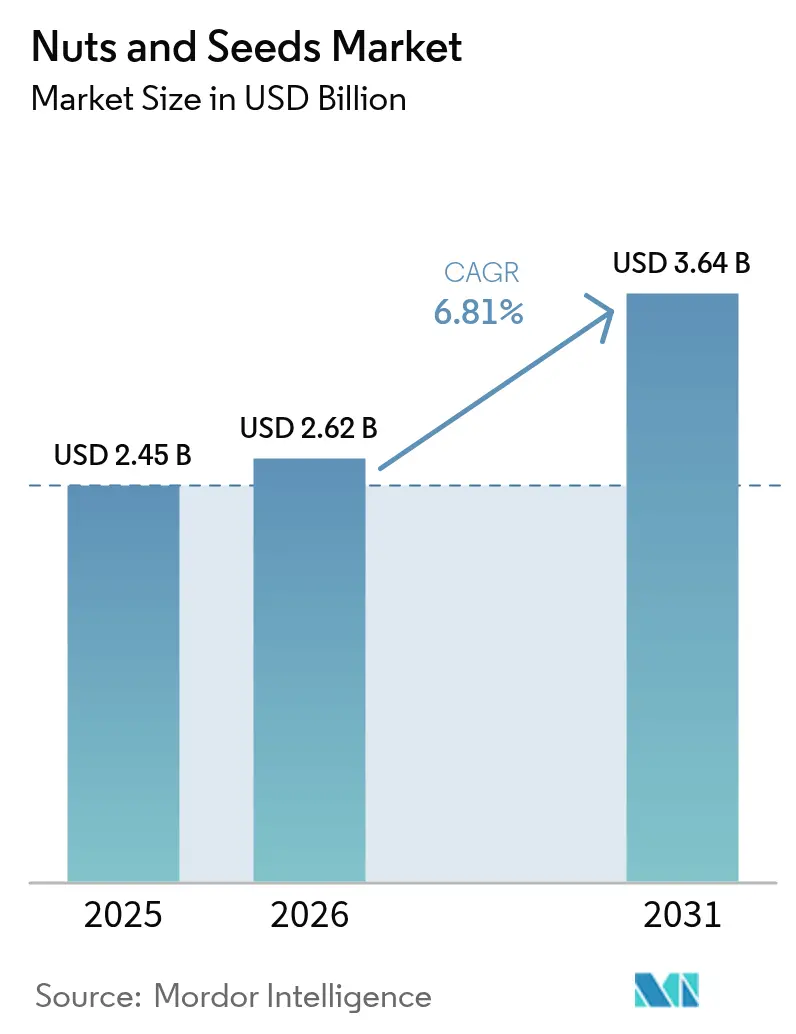

The nuts and seeds market size is expected to grow from USD 2.45 billion in 2025 to USD 2.62 billion in 2026 and is forecast to reach USD 3.64 billion by 2031 at 6.81% CAGR over 2026-2031. This growth stems from consumers incorporating almonds, walnuts, chia, flax, and pumpkin seeds into their daily diets rather than treating them as occasional snacks. Health-conscious consumers are particularly drawn to these products for their high protein content, essential fatty acids, and micronutrients. The market expansion is further driven by diverse industrial applications, with these ingredients being used in cosmetics for their moisturizing properties, nutraceutical powders for protein supplementation, and specialty cold-pressed oils for both culinary and therapeutic purposes. Additional demand comes from bakery, confectionery, and cereal manufacturers incorporating visible nut and seed ingredients to enhance texture and nutritional value. These manufacturers are responding to consumer preferences for clean-label products and natural ingredients, while also capitalizing on the premium positioning that nuts and seeds provide to their finished products.

Key Report Takeaways

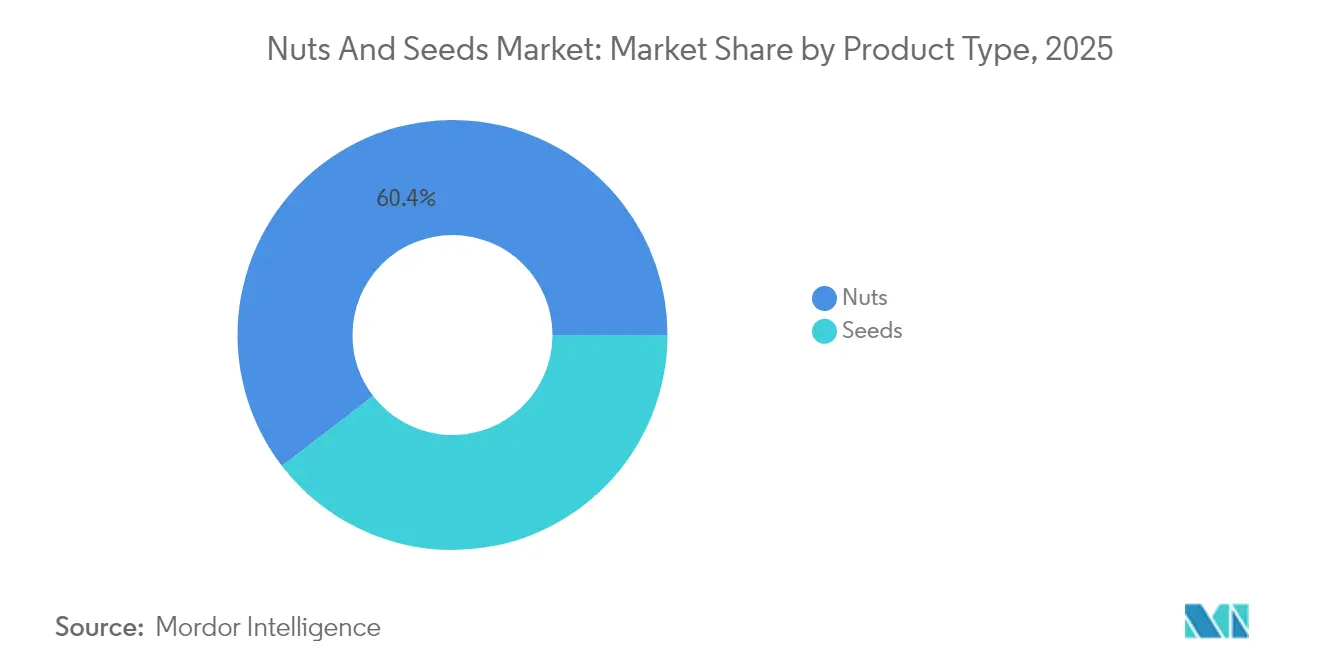

- By product type, nuts led with 60.42% of the nuts and seeds market share in 2025, whereas seeds are forecast to post a 6.88% CAGR between 2026-2031.

- By form, whole kernels captured 41.92% of the nuts and seeds market size in 2025; oils are poised to expand at a 7.28% CAGR through 2031.

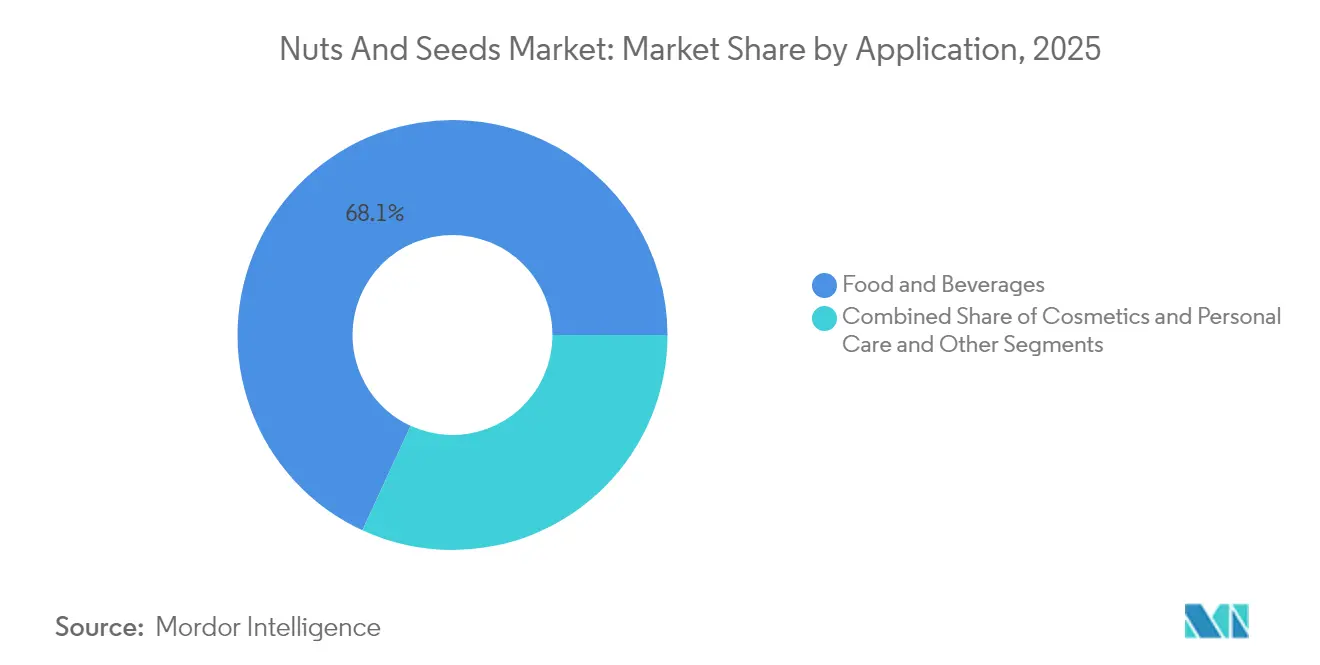

- By application, food and beverages contributed 68.12% revenue in 2025, while cosmetics and personal care is on track for an 8.22% CAGR to 2031.

- By geography, Asia-Pacific held 35.02% revenue share in 2025, yet the Middle East and Africa region will accelerate at an 8.66% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Nuts And Seeds Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing adoption in bakery and confectionery sector fuels demand | +1.5% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Rising demand from snack and cereal manufacturers | +0.8% | Global, led by Asia-Pacific and North America | Short term (≤ 2 years) |

| Expanding food processing industry boosts bulk ingredient purchases | +1.2% | Asia-Pacific core, spill-over to Middle East and Africa | Medium term (2-4 years) |

| Global sourcing networks enhance raw material availability and reliability | +0.9% | Global, with emphasis on supply chain optimization | Long term (≥ 4 years) |

| Surge in superfood popularity fuels demand for seeds as ingredients in food and beverages sector | +0.7% | North America and Europe, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Growing vegan and plant-based diet trends support its usage in various applications | +0.6% | North America and Europe, emerging in urban Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing adoption in bakery and confectionery sector fuels demand

Nuts and seeds have become premium staples in the bakery and confectionery sector, signaling a shift towards enhancing texture and boosting nutrition in processed foods. This trend is especially evident in high-end bakery products, where nuts and seeds not only elevate flavor but also align with clean-label demands. For instance, according to International Nut and Dried Fruit Council, the global production of tree nuts reached accounted to over 5.69 million metric tons in 2023/24 [1]Source: International Nut and Dried Fruit, "Nuts and Dried Fruits Statistics Yearbook-December 2024", inc.nutfruit.org, reflecting a growing supply to meet rising demand. As manufacturers increasingly turn to bulk purchases, they're reshaping supply chain dynamics, often opting for long-term contracts to ensure consistent quality and pricing. Meanwhile, economic pressures are spurring innovation, with companies delving into cost-effective blends of nuts and seeds that don't compromise on sensory appeal. This integration of nuts and seeds into mainstream bakery offerings isn't just a fleeting trend; it's a lasting evolution, driven by rising consumer demands for nutritional value even in indulgent treats.

Rising demand from snack and cereal manufacturers

Snack and cereal manufacturers are incorporating nuts and seeds as primary ingredients instead of premium additions, responding to consumer preferences for protein-rich, convenient nutrition options. This change reflects the increasing role of nuts and seeds in food manufacturing, especially in snacks and cereals. These ingredients provide essential nutritional benefits, including omega-3 fatty acids, plant-based proteins, fiber, vitamin E, magnesium, and zinc. The versatility of nuts and seeds allows manufacturers to create diverse product offerings, from granola bars and breakfast cereals to trail mixes and protein-enriched snacks. Additionally, their natural, wholesome appeal aligns with clean-label trends and health-conscious consumer preferences. The texture and flavor profiles of different nuts and seeds enable manufacturers to develop unique product variations while maintaining nutritional value.

Expanding food processing industry boosts bulk ingredient purchases

The food processing industry's structural expansion in Asia-Pacific markets is fundamentally altering nuts and seeds procurement patterns, with manufacturers increasingly viewing these ingredients as essential rather than optional components. China's food processing sector expansion has created heightened demand for tree nuts, with the USDA noting increased consumer preference for healthier and premium foods driving industry growth [2]Source: Foreign Agriculture Services, U.S. Department of Agriculture, "China: Food Processing Ingredients Annual," fas.usda.gov. This trend extends beyond traditional applications into functional food development, where nuts and seeds serve as natural sources of omega-3 fatty acids, protein, and micronutrients. The industry's shift toward bulk purchasing reflects supply chain optimization efforts, with processors seeking to reduce per-unit costs through volume commitments while ensuring traceability and quality consistency. Processing technology advancements are enabling more efficient extraction and utilization of nut and seed components, creating new revenue streams from previously discarded by-products. The integration of nuts and seeds into processed food formulations is becoming more sophisticated, with manufacturers developing proprietary blends that deliver specific nutritional profiles while maintaining cost competitiveness.

Surge in superfood popularity fuels demand for seeds as ingredients in food and beverages sector

The superfood trend has elevated seeds from niche health food ingredients to mainstream functional components, with chia seeds exemplifying this transformation through their integration into European markets where Germany serves as the largest consumer.This popularity surge is driven by documented nutritional benefits and social media amplification of health-conscious eating patterns, creating sustained demand beyond initial trend cycles. The seeds segment's 6.93% CAGR (2025-2030) reflects this structural shift, with manufacturers incorporating diverse seed varieties into products ranging from beverages to baked goods. Supply chain volatility remains a challenge, with chia seed markets experiencing price fluctuations due to concentrated South American production, prompting exploration of African cultivation sources. The trend is expanding beyond traditional health food channels into mainstream retail, with major food manufacturers developing seed-enhanced product lines. Consumer education about nutritional benefits continues to drive adoption, with seeds increasingly positioned as accessible superfoods that deliver measurable health benefits without requiring significant dietary changes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising allergen management requirements drive complex production line adaptations | -0.4% | Global, with stricter enforcement in North America and Europe | Short term (≤ 2 years) |

| Food safety concerns require extensive quality control testing | -0.6% | Global, with emphasis on import-dependent regions | Medium term (2-4 years) |

| Supply chain disruptions increase logistics and warehousing costs | -0.8% | Global, with higher impact in import-dependent markets | Short term (≤ 2 years) |

| Seasonal harvest cycles limit year-round product availability | -0.5% | Global, with regional variations in harvest timing | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising allergen management requirements drive complex production line adaptations

Allergen management requirements are creating significant operational complexities for food manufacturers seeking to incorporate nuts and seeds into existing production lines, with the FDA's comprehensive allergen labeling guidance requiring clear identification of tree nuts as major allergens [3]Source: U.S. Food and Drug Administration, "Food Allergies-March 2025", fda.com. These regulations mandate dedicated production lines or extensive cleaning protocols between allergen and non-allergen products, substantially increasing capital expenditure requirements for manufacturers. The complexity extends beyond labeling to include supply chain traceability, with companies required to document allergen presence throughout the entire production process. Cross-contamination prevention measures are driving investment in specialized equipment and facility modifications, creating barriers to entry for smaller manufacturers. The regulatory landscape continues to evolve, with sesame recently added to major allergen lists, indicating potential future expansion that could affect nuts and seeds processing. Training requirements for production staff and quality control personnel add ongoing operational costs that particularly impact smaller-scale operations seeking to enter the nuts and seeds processing market.

Supply chain disruptions increase logistics and warehousing costs

Supply chain disruptions have fundamentally altered the cost structure of nuts and seeds distribution, with climate change impacts on temperate fruit and nut production creating additional volatility in supply planning. The concentration of production in specific geographic regions makes the market vulnerable to weather events, trade policy changes, and transportation disruptions that can rapidly affect global availability. Warehousing costs have increased significantly due to requirements for climate-controlled storage and extended inventory holding periods to buffer against supply interruptions. The complexity of managing multiple origin sources while maintaining quality consistency has led to increased logistics coordination costs and longer lead times. Transportation cost volatility, particularly for international shipments, is forcing companies to reassess their supply chain strategies and consider regional sourcing alternatives. The need for enhanced traceability and quality documentation throughout the supply chain is adding administrative costs that ultimately impact end-user pricing and market accessibility.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Seeds Segment Accelerates Despite Nuts Dominance

In 2025, nuts dominated the market, capturing a 60.42% revenue share. This dominance can be attributed to several factors, including the widespread popularity of nuts as a convenient and healthy snacking option, their rich nutritional profile, and their versatility in various culinary applications. Nuts are a staple in many diets due to their high content of protein, healthy fats, vitamins, and minerals, which appeal to health-conscious consumers. Furthermore, the presence of a well-established processing infrastructure has enabled large-scale production, efficient distribution, and the development of value-added products such as flavored nuts, nut butters, and snack mixes. These factors collectively reinforce the strong position of nuts in the market.

While seeds may lag in tonnage, they're projected to expand at a robust 6.88% CAGR, driven by the consumer shift towards functional superfoods. Chia seeds have made their mark with mainstream European retailers, and pumpkin seeds are lauded for their zinc and magnesium content. Flax seeds, particularly in North America, have capitalized on omega-3 messaging, buoyed by heart-health claims that bolster sales. Sesame seeds, despite facing new allergen-labeling costs, benefit from heightened awareness. Moreover, innovations like micro-milled seed flours and sprouted seed powders underscore the technological advancements broadening seeds' applications. This blend of nutritional benefits, versatility, and processing innovations fuels the growing prominence of seeds in the nuts and seeds market.

By Form: Oils Segment Emerges as Processing Innovation Driver

In 2025, whole kernels accounted for 41.92% of the nuts and seeds market, packaged in transparent pouches, bulk snack bins, and as toppings in bakeries, emphasizing their unprocessed authenticity. Whole kernels are widely preferred due to their versatility and nutritional benefits, making them a popular choice among consumers seeking healthy snacking options and natural ingredients for cooking and baking. The demand for whole kernels is further driven by the growing trend of clean-label products, as consumers increasingly prioritize minimally processed and natural food items. Additionally, the rise in plant-based diets and the incorporation of nuts and seeds into various cuisines have bolstered the consumption of whole kernels.

Nut and seed oils are expected to register the highest growth rate with a CAGR of 7.28%. The increasing demand for plant-based oils, driven by their health benefits and applications in various industries such as food, cosmetics, and pharmaceuticals, is a significant factor contributing to this growth. These oils are gaining traction due to their rich nutrient profile, including essential fatty acids, antioxidants, and vitamins, which appeal to health-conscious consumers. Furthermore, the expanding use of nut and seed oils in premium skincare and haircare products, owing to their moisturizing and nourishing properties, is expected to further propel their market growth during the forecast period.

By Application: Cosmetics Segment Drives Premium Value Creation

In 2025, the food and beverages segment within the nuts and seeds market commanded a dominant 68.12% share of the revenue. This was primarily driven by substantial tonnage absorption in everyday snacking, cereals, and bakery categories, where nuts and seeds are widely used as key ingredients due to their nutritional benefits and versatility. The increasing consumer preference for healthy snacking options has further bolstered the demand for nuts and seeds in this segment. Nuts and seeds are increasingly incorporated into granola bars, trail mixes, and breakfast cereals, catering to the growing demand for convenient and nutritious food products. Additionally, the bakery industry has witnessed a surge in the use of nuts and seeds as toppings and ingredients in bread, cakes, and pastries, enhancing both flavor and nutritional value.

Furthermore, the cosmetics and personal care sector, which utilizes nuts and seeds for their natural oils and extracts, is poised for an annual growth rate of 8.22%. This growth is attributed to the rising consumer inclination toward natural and organic personal care products, where nuts and seeds play a significant role in formulations. Products such as almond oil and argan oil, derived from nuts and seeds, are increasingly being used in skincare and haircare products due to their moisturizing and nourishing properties. The demand for such products is further driven by the growing awareness of the harmful effects of synthetic chemicals, prompting consumers to opt for plant-based and sustainable alternatives. The dual application of nuts and seeds across food and non-food sectors highlights their versatility and underscores their critical role in driving market growth.

Geography Analysis

Asia-Pacific holds a 35.02% market share in 2025, driven by its large consumer base, expanding middle class, and increasing health consciousness, which stimulates demand for premium food ingredients. China's expanding food processing industry maintains a steady demand for tree nuts, supported by urbanization and higher disposable incomes. Japan's consistent consumption patterns and high quality requirements create opportunities for premium suppliers who meet these standards. Southeast Asian markets show increased adoption of Western snacking habits, particularly nuts and seeds, influenced by lifestyle changes, global food trends, and demand for convenient, nutritious snacks.

The Middle East and Africa region is projected to grow at 8.66% CAGR during 2026-2031. High per-capita income and the traditional use of nuts in regional cuisine drive market growth, while limited agricultural land maintains import dependency. South Africa's expanding tree nut production, supported by higher returns compared to other crops, indicates growing regional supply capabilities. The GCC countries show strong market potential due to their young demographic profile and increasing health awareness. The development of modern retail infrastructure creates enhanced distribution networks. Turkey's market demonstrates regional complexity, as it maintains significant almond and walnut imports despite its domestic production capacity.

North America and Europe represent mature markets with established consumption patterns and sophisticated supply chains that emphasize quality, traceability, and sustainability credentials. The U.S. maintains its position as the world's leading tree nut exporter demonstrating the region's production efficiency and global market integration. European markets show particular strength in organic and specialty varieties, with Germany serving as the largest consumer market for chia seeds and the Netherlands functioning as a key trading hub South America's role as a key production region for certain seeds, particularly chia from countries like Argentina and Bolivia, creates opportunities for vertical integration and supply chain optimization that could enhance regional market positions.

Regulatory Landscape

Regulation for nuts and seeds is being shaped by tighter import controls, evolving maximum limits for contaminants (notably mycotoxins and pesticide residues), and broader traceability expectations across major consuming markets. In June 2026, the European Commission issued Implementing Regulation (EU) 2026/1206 amending Regulation (EU) 2019/1793, increasing official controls on certain non-animal origin imports where risks such as mycotoxins and pesticide residues were flagged in late 2025. This raises compliance and testing burdens for exporters and import-dependent regions.

In Asia, China notified a revised draft National Food Safety Standard for Nut and Seed Foods to the WTO in May 2026 (G/SPS/N/CHN/1363), signaling moves toward more explicit safety requirements, including mold-related limits for roasted products. In the United States, the FDA Food Traceability Rule (FSMA Section 204) remains a key reference for downstream recordkeeping expectations, while FY2026 appropriations language has been cited as prohibiting FDA from using funds for administration or enforcement before July 20, 2028. That timing gives supply chain operators additional time to align data capture systems without near-term enforcement pressure.

Value Chain Analysis

The nuts and seeds value chain runs from farm production (orchards and field crops) through aggregation by traders and cooperatives, primary processing (shelling, cleaning, sorting, roasting), and secondary processing (pieces, powders, pastes, and cold-pressed oils). Ingredients then move into industrial channels such as bakery, confectionery, cereals, and snack and nutrition bars, along with non-food uses in cosmetics and personal care. Large global processors and traders such as Archer Daniels Midland Company and Olam Group (ofi) typically combine origin sourcing with cleaning, grading, and ingredient processing, while branded players and specialist processors such as The Wonderful Company LLC and Blue Diamond Growers focus more on consumer-facing kernels and value-added snack formats.

Quality and compliance are recurring friction points, especially allergen controls and mycotoxin testing, alongside storage and logistics needs like climate-controlled warehousing. Origin concentration also heightens exposure to disruption, as seen in 2026 reports of shipping disruptions through the Strait of Hormuz that added costs and created bottlenecks for tree nut exports. Commentary in 2025 on Brazil nut shortages and Iran pistachio constraints further highlighted volatility in particular origins. At the buyer level, upstream farm programs and verification are expanding, including the April 2026 Argentina Peanuts Project (SAI Platform with Ferrero, Importaco, Intersnack, Lorenz, Mars, and others) and KINDs regenerative sourcing milestone and related collaborations, which place more weight on farm practices, traceability, and ingredient procurement.

Competitive Landscape

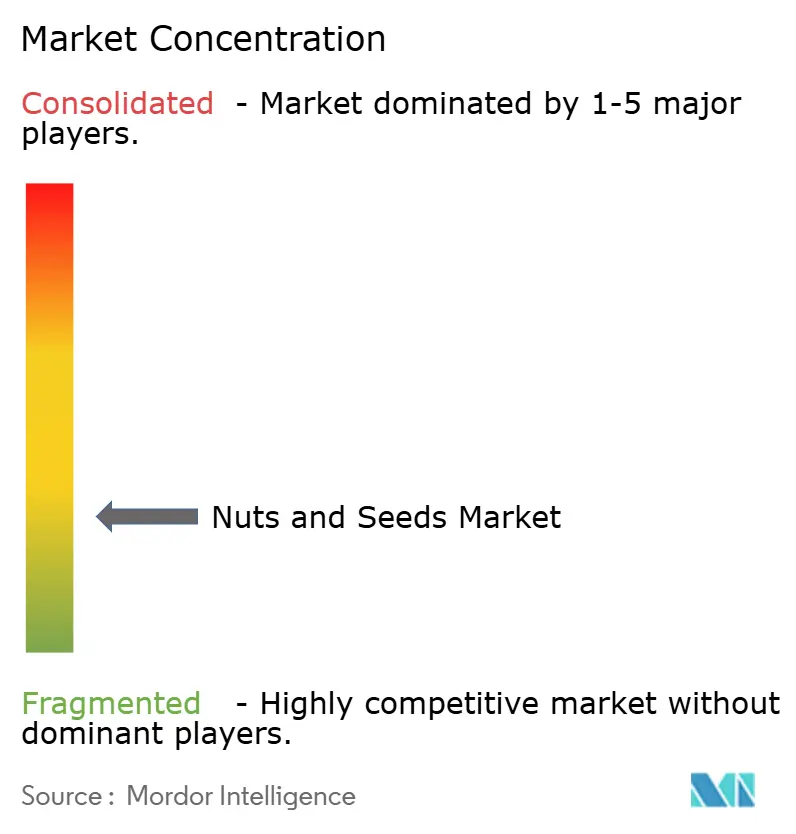

The nuts and seeds market exhibits low concentration with a 3 out of 10 rating, indicating a fragmented competitive environment where numerous regional processors, agricultural cooperatives, and specialized suppliers compete alongside established multinational corporations. By focusing on product innovation, adopting sustainable sourcing practices, and implementing targeted geographic expansion strategies, players can effectively capture market share. Industry leaders like Archer Daniels Midland Company and Olam Group leverage their extensive global supply chains and processing capabilities to meet the demands of large-scale food manufacturers. In contrast, specialized companies such as Blue Diamond Growers and The Wonderful Company emphasize premium consumer brands and value-added products, catering to a more niche audience.

Strategic trends in the market highlight the growing importance of innovation in processing technologies, sustainable sourcing certifications, and expansion into high-growth applications such as cosmetics and functional foods. Companies are increasingly investing in advanced infrastructure, including climate-controlled storage facilities, state-of-the-art sorting technologies, and traceability systems, to meet evolving quality standards and regulatory requirements. These investments not only enhance operational efficiency but also enable companies to address consumer demands for transparency and sustainability. The focus on sustainability and innovation is becoming a critical differentiator, allowing companies to strengthen their competitive positioning in the market.

Regulatory developments, particularly the FDA's comprehensive allergen management requirements, are reshaping the competitive landscape. Smaller processors, often constrained by limited resources, face challenges in meeting these stringent compliance standards, leading to increased consolidation within the market. As the market evolves, the interplay between regulatory pressures, technological advancements, and strategic investments will continue to shape the competitive dynamics of the nuts and seeds market.

Nuts And Seeds Industry Leaders

-

Archer Daniels Midland Company

-

Olam Group

-

HBS Foods Ltd.

-

Kanegrade Ltd.

-

The Wonderful Company LLC

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Processing-led diversification is creating whitespace beyond whole kernels, especially in powders, flours, and other functional formats that fit bakery, snack, and nutrition formulations. A clear example is the February 2026 commissioning of Plenty Foods high-protein, de-fatted nut powder processing capability in Queensland, Australia, which points to continued investment in local value addition and new ingredient formats that help food manufacturers deliver higher protein density and easier incorporation than whole nuts.

Commercial pathways are also strengthening around traceability, sustainability verification, and circular processing in collaboration with large buyers and premium channels. ofi has been expanding farm mapping and traceability work in cashew origins (Cote dIvoire, Ghana, Nigeria) using GPS and polygon monitoring under its AtSource approach, and it commissioned a solar power plant at its Kerabury Orchard in New South Wales in early 2025, linking energy transition actions to nut supply chains. In parallel, industry attention is shifting toward lower-impact decontamination and yield improvement methods, supported by peer-reviewed work such as the 2025 validation of IVDV processing for chickpeas and sesame seeds, which aligns with clean-label positioning while addressing microbial control needs.

Recent Industry Developments

- May 2026: Archer Daniels Midland Company introduced eight new protein ingredient solutions across North America and Europe, expanding its plant-based formulation toolkit. The additions broaden options for snack, bakery, and nutrition manufacturers that use nut and seed-derived ingredients alongside other plant proteins to hit texture and protein targets.

- December 2025: Archer Daniels Midland Company reached an agreement with Planters Cotton Oil Mill to form a cottonseed processing joint venture tied to the Pine Bluff, Arkansas crush plant and Memphis, Tennessee facilities. The move strengthens access to cottonseed-derived ingredients and oils, reinforcing scale advantages for processors serving food and industrial customers.

- April 2024: Pecan Nation and South Georgia Pecan Company initiated a collaboration to expand nut production and strengthen quality standards across the supply chain. By focusing on enhanced processing capabilities and quality control, the partnership supports more consistent pecan supply for ingredient buyers and branded nut programs.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the nuts and seeds market is defined as the value generated from commercially sold edible nuts and edible seeds across retail packs and ingredient uses, covering whole, processed pieces, and oils used in end products.

Scope exclusions: Homegrown and informal direct barter sales, along with non-edible planting seeds meant only for crop propagation, are not counted.

Segmentation Overview

-

By Product Type

-

Nuts

- Almonds

- Peanuts

- Walnuts

- Cashews

- Pistachios

- Others

-

Seeds

- Sunflower

- Pumpkin

- Chia

- Flax

- Sesame

- Others

-

Nuts

-

By Form

- Whole

- Pieces and Powdered

- Oils

- Other Forms

-

By Application

-

Food and Beverages

- Bakery and Confectionery

- Dairy and Dairy Alternatives

- Snack Bars and Trail Mixes

- Others

- Cosmetics and Personal Care

- Other Applications

-

Food and Beverages

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Rest of South America

-

Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by mapping which nut and seed items are traded and consumed, and how they typically move from origin to processors and then to brands and retailers. We rely on public data points that help anchor volumes and trade flows, such as FAOSTAT for crop production, UN Comtrade and national customs portals for import export patterns, USDA and other agriculture ministry statistics for category trends, and Codex or food regulator guidance for product definitions and labeling.

To make the model usable in dollar terms, price direction is checked using public commodity and food price series (where available), and we also review company filings, investor presentations, and reputable press for capacity additions and product mix cues. Patent databases are used selectively to understand where processing and oil extraction are gaining attention, which helps explain form shifts over time. This list is illustrative only, and many other public sources were also reviewed for data collection, cross-checking, and clarification.

Primary Interviews and Surveys

Primary work is used to sanity check the desk assumptions that most often move the numbers, especially conversion from raw to processed forms, channel splits between retail packs and ingredient demand, and typical price realization by geography. We spoke with a mix of processors, branded product teams, distributors, and large buyers, and inputs were balanced across APAC, EMEA, and the Americas so regional consumption habits and trade reliance were not averaged out.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 19% | APAC: 45% |

| Mid tier: 51% | Functional/Unit leaders: 30% | EMEA: 31% |

| Smaller Players: 21% | Managers: 51% | Americas: 24% |

Market-Sizing & Forecasting

Sizing is built using a top-down structure where crop production and trade data reconstruct the available supply pool, which is then adjusted for typical processing yields and the share that goes into edible retail packs, ingredients, and oils. Once the demand pool is shaped, average price levels are applied by form and region, and then the totals are summed into the market value.

To keep the result realistic, selective bottom-up approximations are used as a check, such as rolling up a sample of supplier and channel revenue signals and comparing implied volumes against trade and production totals. Key inputs that usually matter in this market include nut and seed production volumes, import dependency by region, processing yield factors for oils and powders, retail packaged mix versus ingredient usage, and average selling price direction tied to harvest cycles and freight costs. For forecasting, we use scenario analysis supported by simple trend models, where variables like production outlook, price normalization, and health-led snacking demand are stress tested with expert inputs. When bottom-up views do not cover smaller countries or fragmented channels, gaps are filled using trade proxies and per-capita consumption cues before the final reconciliation.

Data Validation & Update Cycle

Validation is done through multiple passes so the model does not rely on one data stream. We compare computed market values against independent signals like production plus net trade balance, visible price trends, and known shifts in retail versus ingredient demand, and then outliers are flagged for re-check.

Before sign-off, assumptions are reviewed by another analyst, and large variances trigger a re-contact with selected interviewees to confirm what changed (for example, a poor harvest, a sudden import policy shift, or a price spike). The report is refreshed annually, and interim updates are made when material events can move volumes or prices. Right before delivery, we perform a final scan so clients receive the most current view available.

Mordor Intelligence's Nuts and Seeds Market Size Measured Against Other Published Estimates

Published market numbers for nuts and seeds can look far apart because the product definition sounds simple, but the counting rules often are not. Differences usually come from whether the estimate tracks edible raw and processed forms only, or also adds downstream packaged snack sales, prepared foods, and broader grocery revenue pools.

Some external studies appear to use a broad food retail lens that inflates totals by pulling in packaged snack and ready-to-eat value. Packaged snack mixes, coated nuts, and ready-to-eat items are frequently added as finished-goods revenue, then Mordor Intelligence counts nuts and seeds as products and forms (whole, pieces and powdered, and oils) across retail and ingredient use so those finished items are not stacked on top of the underlying nut and seed value.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.62 B (2026) | |

| Global Consultancy A | USD 2.85 B (2026) | Uses a wider application mapping and may apply higher price realization across bakery, cereals, and processed dairy uses, which can lift the blended ASP when form-level prices are not separated. |

| Industry Publisher B | USD 30.14 B (2024) | Likely includes a much broader packaged and prepared foods revenue pool, which can stack final product value on top of underlying nut and seed inputs and results in a materially larger headline number. |

The table shows that the spread is mainly a scope and counting issue rather than a disagreement about growth direction. By tying volumes to production and net trade, and then applying form-specific pricing with interview checks, our estimate stays traceable to repeatable inputs that can be explained and updated as supply and pricing change.

Key Questions Answered in the Report

What is the current size of the nuts and seeds market?

The nuts and seeds market is valued at USD 2.62 billion in 2026 and is forecast to reach USD 3.64 billion by 2031.

Which region holds the largest share of the nuts and seeds market?

Asia-Pacific leads with 35.02% revenue share, supported by rising incomes and growing health awareness.

Which segment is growing fastest within the nuts and seeds market?

Seeds are projected to grow at a 6.88% CAGR, driven by demand for functional superfoods like chia and flax.

Why are nut and seed oils gaining popularity?

Cold-pressed oils command premium prices in culinary and skincare applications and are forecast to grow at a 7.28% CAGR through 2031.

Page last updated on: