Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

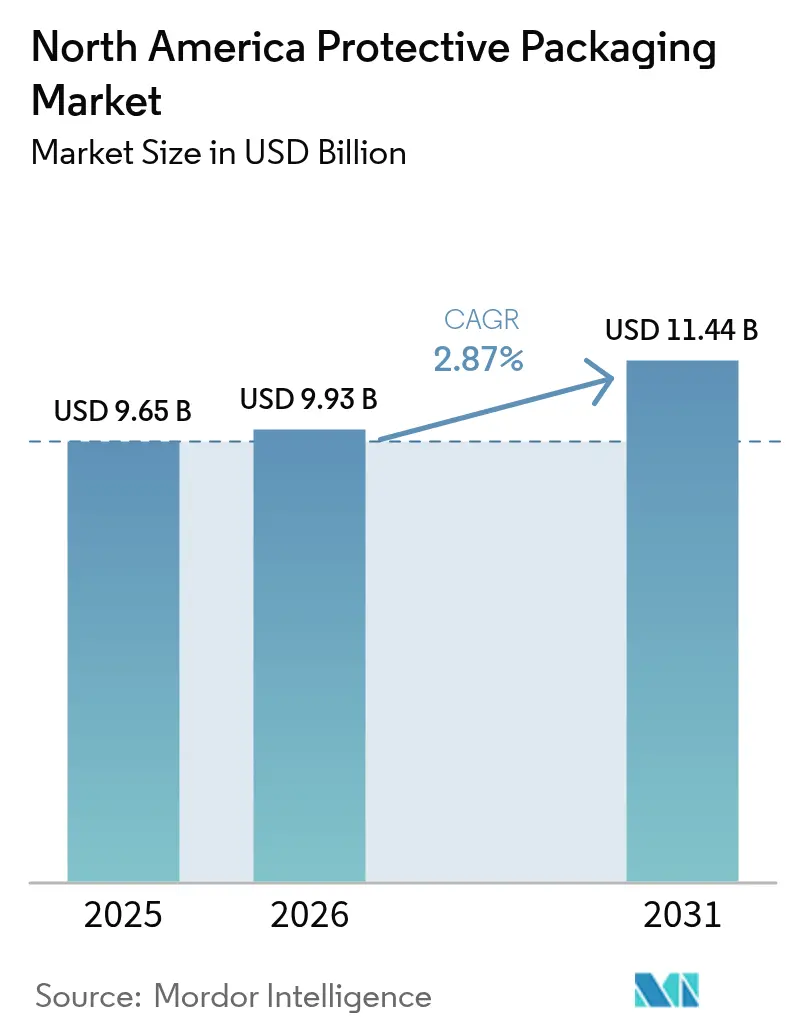

| Base Year Market Size (2025) | USD 9.65 Billion |

| Market Size (2026) | USD 9.93 Billion |

| Market Size (2031) | USD 11.44 Billion |

| Growth Rate (2026 - 2031) | 2.87% CAGR |

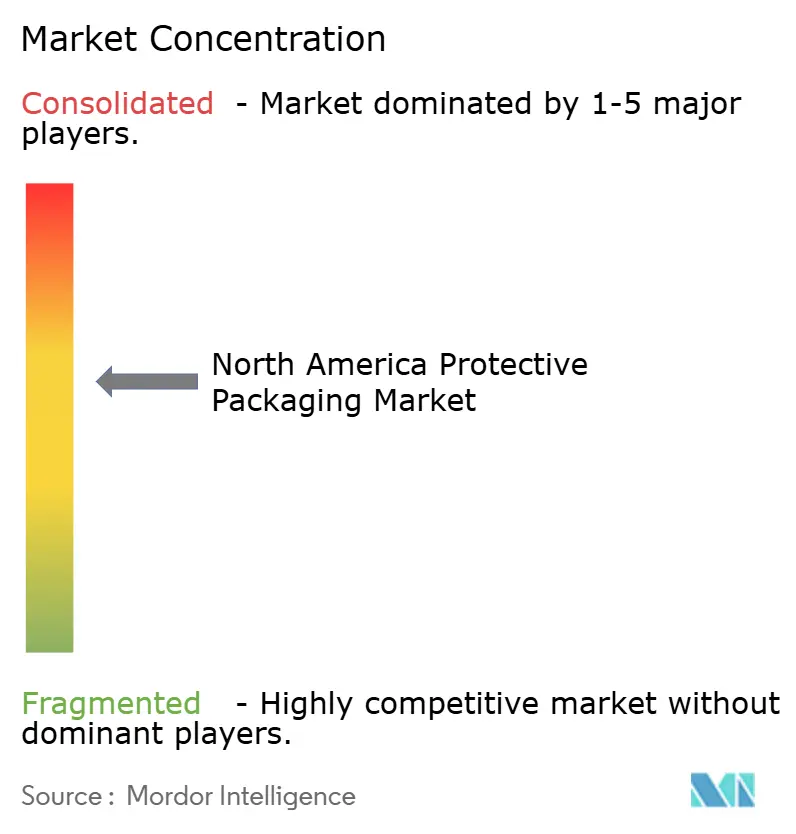

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Protective Packaging Market Analysis by Mordor Intelligence

The North America protective packaging market size is expected to grow from USD 9.65 billion in 2025 to USD 9.93 billion in 2026 and is forecast to reach USD 11.44 billion by 2031 at 2.87% CAGR over 2026-2031. This trajectory reflects a landscape where dimensional-weight freight rules, e-commerce fulfillment automation, and sustainability mandates each pull demand in different directions. Flexible formats gain favor as carriers price by volume and parcel hubs automate cube optimization, while cold-chain expansion in food and pharmaceuticals unlocks premium opportunities for insulated and foam solutions. At the same time, volatile resin prices and stringent single-use plastics bans temper growth, forcing suppliers to recalibrate material portfolios and pricing strategies. M&A activity continues as scale proves critical for absorbing cost spikes, funding R&D in bio-based substrates, and meeting retailer requirements for end-to-end packaging automation.

Key Report Takeaways

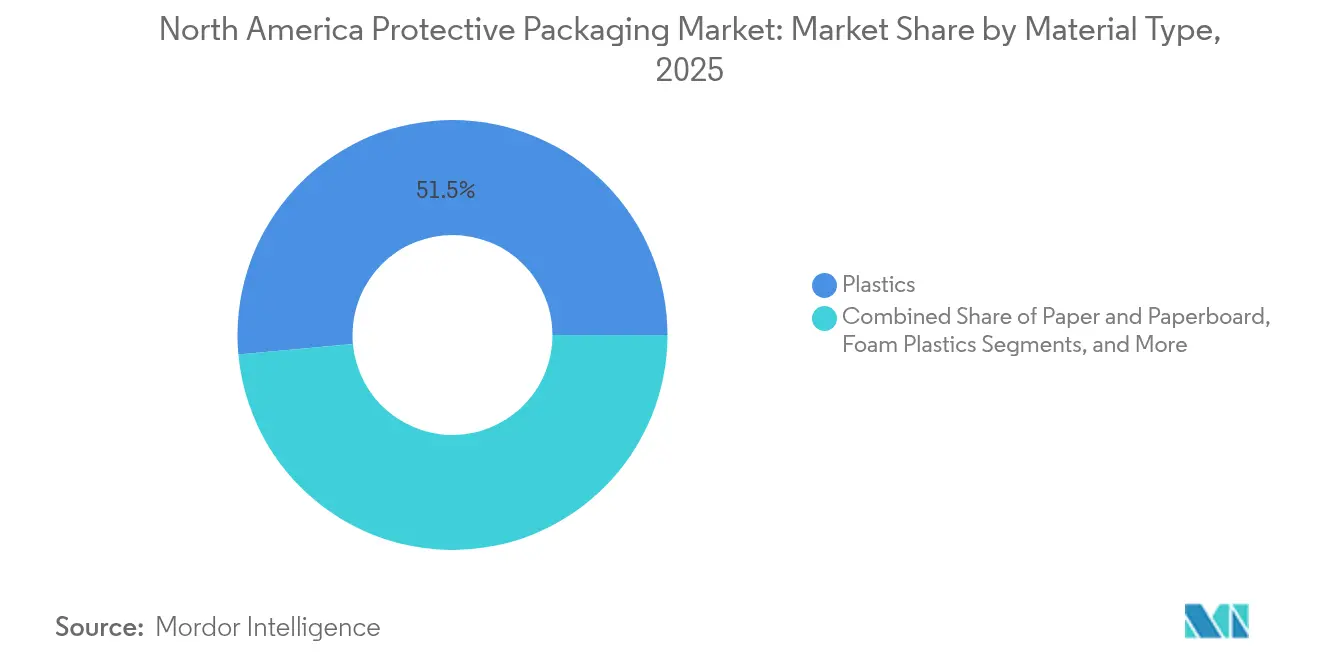

- By material type, plastics led with 51.45% of the North America protective packaging market share in 2025, while bio-based and compostable materials are projected to grow at a 5.49% CAGR through 2031.

- By product type, flexible formats held 46.12% of the North America protective packaging market size in 2025; foam products are set to expand at a 4.38% CAGR to 2031.

- By functionality, cushioning commanded 39.25% share of the North America protective packaging market size in 2025, and insulation is advancing at a 4.79% CAGR through 2031.

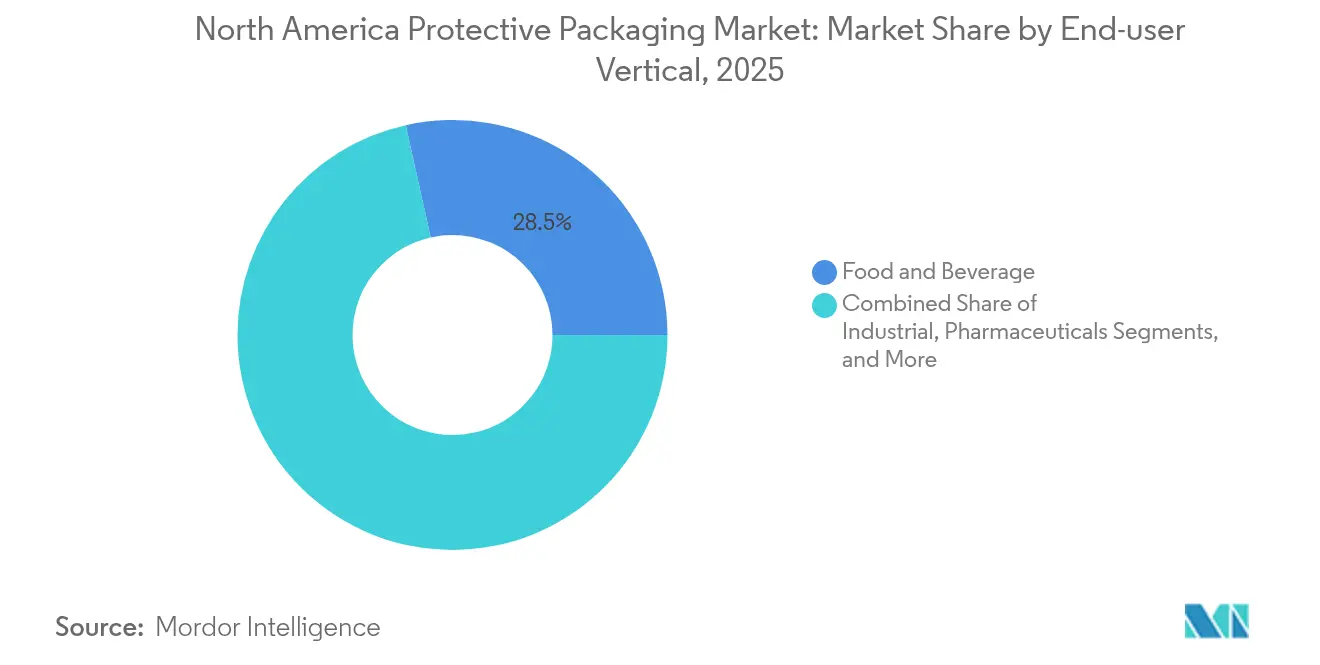

- By end-user vertical, pharmaceuticals are on track to record the fastest CAGR of 4.86% during 2026-2031, whereas food and beverage remained the largest revenue contributor with 28.49% share in 2025.

- By country, the United States retained a 71.65% share of the North America protective packaging market size in 2025, while Mexico is forecast to post a 4.97% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Protective Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce boom and parcel-volume growth | +1.2% | Global, concentrated in U.S. urban centers | Short term (≤ 2 years) |

| Shift toward sustainable and recycled materials | +0.8% | North America regulatory zones, Canada federal mandate | Medium term (2-4 years) |

| Cold-chain expansion in food and pharma | +0.6% | U.S. pharmaceutical corridors, Mexico food processing | Medium term (2-4 years) |

| Dim-weight freight rules favoring light flexible formats | +0.4% | U.S. and Canada freight networks | Short term (≤ 2 years) |

| Reverse-logistics uptick demanding reusable protection | +0.3% | E-commerce dense regions in U.S. | Long term (≥ 4 years) |

| On-site AI-driven packaging automation at fulfillment hubs | +0.2% | Major U.S. distribution centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

E-commerce boom and parcel-volume growth

Surging parcel volumes continue to redefine protective packaging market requirements. Automated fulfillment centers rely on pre-formed mailers and air pillows that cut packing time by up to 40%, keeping pace with same-day delivery promises. Sealed Air reported robust e-commerce sales in 2024, attributing growth to automation-ready solutions that integrate seamlessly with high-speed lines.[1]Sealed Air Corporation, “2024 Annual Report,” sealedair.com Retailers, however, increasingly deploy cube-optimization software that trims excess void, reducing material intensity even as shipment counts climb. This duality sustains volume growth for automation-compatible formats while capping runaway tonnage gains for traditional void-fill.

Shift toward sustainable and recycled materials

Sustainability commitments from multinationals accelerate the adoption of fiber-based and compostable solutions despite cost premiums. Nestlé earmarked EUR 1.5 billion (USD 1.6 billion) for sustainable packaging through 2025, funneling funds toward bio-based cushioning and molded-pulp inserts. Health Canada’s single-use plastics prohibition, effective December 2024, eliminates several fossil-based formats, prompting rapid material substitution across North American supply chains. Despite 20–25% cost premiums, brand-owner ESG targets and consumer preference shifts underpin a steady pipeline of plant-derived films, starch loose-fill, and mycelium cushioning.

Cold-chain expansion in food and pharma

Personalized medicines, biologics, and meal-kit delivery are widening the protective packaging market for insulated shippers. Pfizer invested USD 2 billion in cold-chain infrastructure during 2024 to safeguard mRNA vaccines, driving demand for phase-change panels, EPS molded containers, and data-logging liners. Moderna’s ultra-low-temperature requirements (-70 °C) further stretch insulation performance thresholds. Food processors echo this trajectory as fresh-produce exports and omnichannel grocery expand, requiring thermal packaging that maintains quality through last-mile delivery.

Dim-weight freight rules favoring light flexible formats

FedEx and UPS dimensional-weight formulas charge by volume as much as mass, rewarding shippers that minimize cubic footprint. This pricing logic propels inflatable air pillows, paper void-fill, and film-based mailers that collapse to reduce volumetric penalties. Shippers report 10–15% freight savings after switching from molded foam to lightweight flexibles, supporting continued penetration of air-cell cushioning and honeycomb paperboard that deliver comparable protection at lower cube.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent regulations on single-use plastics and degradability | -0.7% | Canada federal regulations, U.S. state initiatives | Medium term (2-4 years) |

| Volatile resin and fiber prices | -0.5% | Global supply chains, petrochemical regions | Short term (≤ 2 years) |

| Warehouse cube-optimization reducing void-fill volumes | -0.4% | U.S. e-commerce fulfillment networks | Short term (≤ 2 years) |

| High CAPEX for smart-packaging machinery | -0.3% | Manufacturing facilities needing automation upgrades | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent regulations on single-use plastics and degradability

Health Canada’s prohibition eliminates checkout bags, cutlery, and defined packaging types, forcing rapid reformulation and significant R&D outlays for converters. Simultaneously, the U.S. EPA proposed limits on PFAS in food-contact coatings, removing conventional fluoropolymer barriers from the protective packaging toolbox. Compliance spending already absorbs 8–12% of development budgets, and uncertainty over enforcement timelines postpones investment in alternative chemistries.

Volatile resin and fiber prices

Dow reported polyethylene price swings of 20–25% in 2024 tied to feedstock disruptions, while International Paper cited 12–15% kraft cost hikes as mill outages collided with e-commerce demand. These gyrations squeeze converter margins, especially for small and mid-sized firms lacking long-term feedstock contracts or financial hedges. List-price adjustments trail raw-material spikes, pressuring cash flows and slowing capex plans.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Bio-based innovation accelerates despite plastic dominance

Plastics secured 51.45% of 2025 revenue and remain indispensable for moisture and puncture barriers in the protective packaging market. However, the bio-based segment advances at a 5.49% CAGR, reflecting regulatory pressure and corporate ESG targets. The protective packaging industry logged a 35% rise in USPTO patent filings for PHA films and mycelium foams, signaling R&D momentum. Producers channel capex toward scalable compostable resins even as price premiums persist.

Paper and molded-fiber alternatives benefit from recyclability perceptions, though fiber price volatility narrows cost advantages. Foam plastics face scrutiny for disposal challenges yet retain irreplaceable insulation properties for fragile or temperature-sensitive loads. The protective packaging market is increasingly split into high-performance polymer applications and sustainability-driven fiber or compostable niches, with converters like Sealed Air earmarking USD 150 million for circular-material development.

By Product Type: Flexible formats lead amid foam resurgence

Flexible mailers, bubble wrap, and air pillows captured 46.12% of 2025 revenue as e-commerce shippers chase lightweight, automation-friendly options. Dim-weight freight economics amplify this edge, reinforcing demand for low-cube solutions. Foam regained momentum through pharmaceutical cold-chain expansion, registering the highest 4.38% CAGR outlook to 2031. Pfizer’s USD 2 billion cold-chain push underscores durable insulation demand for biologics.

Rigid corrugated inserts persist in industrial supply chains, while molded pulp gains share in electronics as OEMs swap EPS for fiber to meet recycling mandates. The protective packaging market sees discretionary upgrades toward smart variants embedding temperature sensors, QR tracking, and tamper evidence, enabling converters to upsell performance without proportionate material increases.

By Functionality: Cushioning dominates while insulation surges

Cushioning held 39.25% of 2025 spending, anchored by high-frequency outbound parcels in electronics and consumer goods. Yet, insulation is forecast to log a 4.79% CAGR as biologics, meal kits, and fresh grocery sales in North America. Moderna’s -70 °C distribution tests performance boundaries, elevating demand for vacuum-insulated panels and phase-change materials.

Void-fill experiences downward pressure from cube-optimization software, nudging suppliers toward higher-density, multi-use solutions that justify their footprint. Blocking and bracing remains resilient in heavy industrial shipments where the welfare costs of damage exceed marginal packaging savings. Overall, the protective packaging market balances cost-per-ship with risk tolerance and regulatory oversight, particularly where temperature excursions trigger write-offs.

By End-user Vertical: Food leads while pharma accelerates

Food and beverage retained 28.49% of 2025 revenue, supported by omnichannel grocery and export-grade fresh produce. Nestlé’s EUR 1.5 billion (USD 1.76 billion) commitment to sustainable packaging channels volume toward recyclable paper sleeves and compostable cushioning. Pharmaceuticals register the strongest 4.86% CAGR through 2031, driven by cell therapies and mRNA platforms requiring validated, temperature-controlled shippers.

Industrial manufacturing holds steady demand for blocking, bracing, and heavy-duty wraps, while consumer electronics favor low-static, high-clarity protective films to minimize returns. E-commerce acts as a horizontal force, influencing packaging design requirements across every vertical in the protective packaging market.

By Packaging Technology: Inflatable systems lead innovation wave

Inflatable formats commanded 32.78% revenue in 2025, reflecting their synergies with automated fulfillment and ease of storage. Insulated shipping containers deliver the fastest 4.31% CAGR as cold-chain intensifies across healthcare and perishables. Pregis’ pharma-grade inflatable with integrated temp monitoring highlights convergence between cushioning and analytics.

Molded pulp and honeycomb paperboard earn traction where single-use plastics restrictions tighten. Suspension and retention solutions cater to high-value electronics, securing lenses and glass panels during long-haul transit. Smart integration-RFID, NFC, or printed circuitry-emerges as a differentiator, letting shippers verify integrity without opening containers.

Geography Analysis

The United States generated 71.65% of 2025 revenue, anchored by a vast e-commerce engine and sophisticated fulfillment infrastructure. Sealed Air’s USD 5.5 billion sales underscore the protective packaging market heft available to suppliers that align with automation platforms and cold-chain standards. Advanced cartonization algorithms now trim void space, moderating material tonnage even as parcel volumes climb. Consolidation, such as Smurfit WestRock’s EUR 22.2 billion revenue scale, further concentrates bargaining power and fuels investments in bio-based R&D.

Canada represents a regulatory pressure cooker driving sustainable adoption. Health Canada’s plastics ban forces rapid material shifts, elevating fiber-based and compostable options along with reusable tote pilots. The pharmaceutical cold-chain remains a pocket of premium growth given climatic extremes and remote communities that heighten spoilage risk. Forest-products supply chains underpin steady demand for heavy-duty industrial protection despite pulp price swings.

Mexico posts a 4.97% CAGR through 2031 as nearshoring relocates electronics and automotive assembly southward. USMCA provisions streamline cross-border flows, yet tropical climate and infrastructure gaps demand robust thermal and moisture barriers. Investments in regional distribution hubs create fresh orders for fit-to-size equipment and recyclable cushioning as OEMs export finished goods back to U.S. consumers. Local converters partner with multinationals to certify plants under GFSI and ISO-9001, aligning quality benchmarks with North American retail expectations.

Competitive Landscape

North America’s protective packaging market shows moderate consolidation. The top five suppliers control roughly 55-60% of revenue, led by Sealed Air at USD 5.5 billion and Smurfit WestRock at USD 24.0 billion in 2024. Scale lets these firms hedge resin volatility, fund smart-factory upgrades, and win multi-year contracts with big-box retailers. Patent data reveal a 35% uptick in filings during 2024, signifying an arms race in bio-based materials and sensor-enabled packaging.

Strategic moves include Sealed Air’s USD 150 million sustainability investment and International Paper’s launch of automation-friendly kraft grades tailored to fit-to-size erectors.[3] International Paper Company, “Investor Presentation 2024,” internationalpaper.com Pregis and Ranpak intensify focus on paper-based inflatables and void-fill systems to capitalize on plastics bans, while Amcor spends USD 75 million to add North American capacity for pharmaceutical liners. Smaller specialists carve niches in reusable totes or ultra-low-temperature shippers, leveraging domain expertise to sidestep scale disadvantages.

Technology defines competitive advantage: vendors offering IoT-ready inserts, RFID-embedded mailers, or AI-compatible substrates gain pricing power. Sustainability credentials also influence bid awards as retailers publish supplier scorecards on recyclability, CO₂ footprint, and chemical safety. As M&A persists, integration of digital tools with material science will likely separate market leaders from commodity suppliers.

North America Protective Packaging Industry Leaders

Sealed Air Corporation

Pregis LLC

Sonoco Products Company

Intertape Polymer Group Inc.

Smurfit WestRock

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Sealed Air Corporation announced a USD 150 million investment in sustainable material development, focusing on bio-based protective packaging solutions for e-commerce applications.

- February 2025: Smurfit WestRock reported EUR 22.2 billion (USD 24.0 billion) in annual revenue for 2024, with protective segments driving growth through automation-compatible solutions.

- January 2025: International Paper Company launched new kraft grades optimized for protective packaging, targeting automated lines.

- December 2024: Health Canada implemented the Single-use Plastics Prohibition Regulations, spurring fiber-based alternatives across North America.

North America Protective Packaging Market Report Scope

Protective packaging is made of materials that protect and provide a barrier to a product from potential harm, damage, or destruction during shipping or warehousing. Protective packaging can be used as primary or secondary packaging material, depending on the end-user application of the packaged product.

The studied market is segmented by rigid (molded pulp, paperboard-based protectors, and insulated shipping containers), flexible (mailers, bubble wraps, paper full, and air pillows), and foam-based packaging.

The study also covers the end-user verticals for protective packagings, such as the food and beverage, pharmaceutical, and consumer electronics industries, across the region. The impact of COVID-19 has also been considered for current market estimations and growth projections.

By Material Type

| Paper and Paperboard |

| Plastics |

| Foam Plastics |

| Bio-based and Compostable Materials |

By Product Type

| Rigid | Corrugated Paperboard Protectors |

| Molded Pulp | |

| Insulated Shipping Containers | |

| Flexible | Protective Mailers |

| Bubble Wraps | |

| Air Pillows/Air Bags | |

| Paper Fill | |

| Foam | Molded Foam |

| Foam-in-Place (FIP) | |

| Loose Fill | |

| Foam Rolls/Sheets |

By Functionality

| Cushioning |

| Blocking and Bracing |

| Void Fill |

| Insulation |

| Wrapping and Surface Protection |

| Other Functionalities |

By End-user Vertical

| Food and Beverage |

| Industrial |

| Pharmaceuticals |

| Consumer Electronics |

| Cosmetics and Home Care |

| E-commerce and Logistics |

| Other End-user Verticals |

By Packaging Technology

| Inflatable Packaging Systems |

| Molded Pulp and Fiber-based Systems |

| Suspension and Retention Packaging |

| Insulated Shipping Containers |

| Dunnage and Layer Pads |

| Honeycomb Paper Solutions |

By Country

| United States |

| Canada |

| Mexico |

| By Material Type | Paper and Paperboard | |

| Plastics | ||

| Foam Plastics | ||

| Bio-based and Compostable Materials | ||

| By Product Type | Rigid | Corrugated Paperboard Protectors |

| Molded Pulp | ||

| Insulated Shipping Containers | ||

| Flexible | Protective Mailers | |

| Bubble Wraps | ||

| Air Pillows/Air Bags | ||

| Paper Fill | ||

| Foam | Molded Foam | |

| Foam-in-Place (FIP) | ||

| Loose Fill | ||

| Foam Rolls/Sheets | ||

| By Functionality | Cushioning | |

| Blocking and Bracing | ||

| Void Fill | ||

| Insulation | ||

| Wrapping and Surface Protection | ||

| Other Functionalities | ||

| By End-user Vertical | Food and Beverage | |

| Industrial | ||

| Pharmaceuticals | ||

| Consumer Electronics | ||

| Cosmetics and Home Care | ||

| E-commerce and Logistics | ||

| Other End-user Verticals | ||

| By Packaging Technology | Inflatable Packaging Systems | |

| Molded Pulp and Fiber-based Systems | ||

| Suspension and Retention Packaging | ||

| Insulated Shipping Containers | ||

| Dunnage and Layer Pads | ||

| Honeycomb Paper Solutions | ||

| By Country | United States | |

| Canada | ||

| Mexico | ||

Key Questions Answered in the Report

What is the forecast value of the North American protective packaging market by 2031?

The market is expected to reach USD 11.44 billion by 2031.

Which material segment is growing fastest in protective packaging?

Bio-based and compostable materials are projected to grow at a 5.49% CAGR through 2031.

How are dimensional-weight freight rules influencing packaging choices?

They incentivize lightweight, flexible formats that reduce cubic volume, leading to freight savings of up to 15%.

Which end-user vertical is set to record the highest CAGR?

Pharmaceuticals are forecast to expand at a 4.86% CAGR during 2026-2031 due to cold-chain needs.

Why is Mexico’s protective packaging demand accelerating?

Nearshoring of manufacturing and investment in regional distribution hubs push market growth to a 4.97% CAGR.

How are suppliers addressing resin price volatility?

Larger players leverage long-term contracts, hedging, and R&D into alternative materials to cushion margin impact.

Page last updated on: