North America Residential Ductwork Design Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

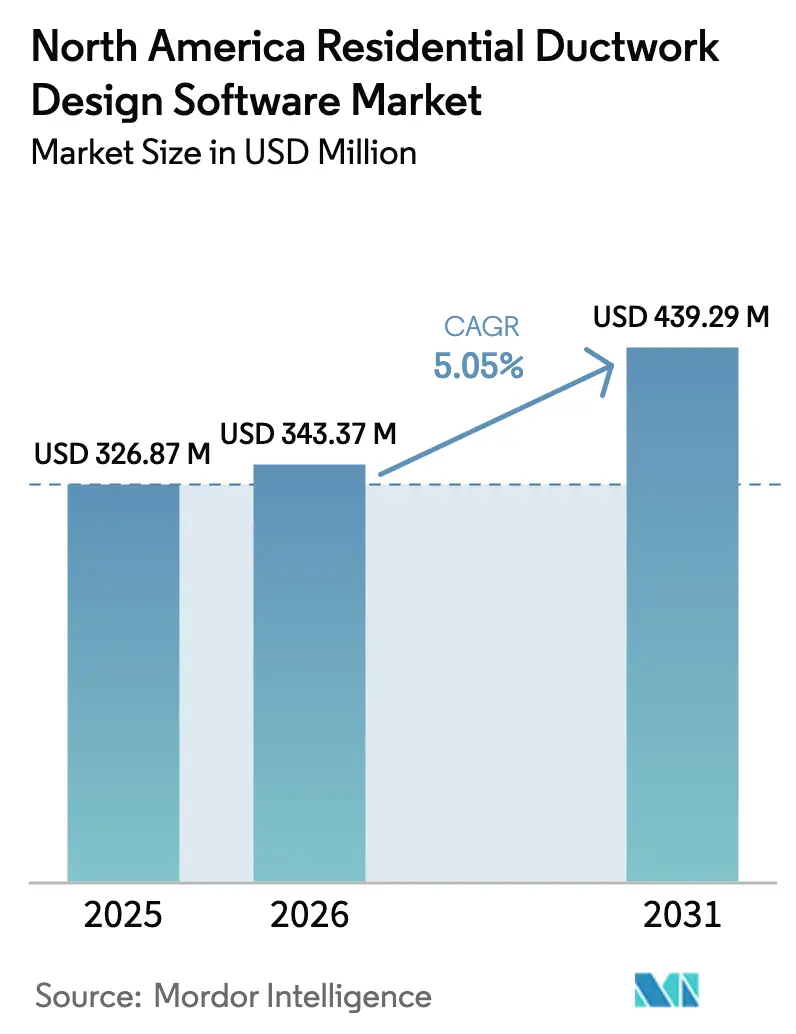

| Base Year Market Size (2025) | USD 326.87 Million |

| Market Size (2026) | USD 343.37 Million |

| Market Size (2031) | USD 439.29 Million |

| Growth Rate (2026 - 2031) | 5.05% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Residential Ductwork Design Software Market Analysis by Mordor Intelligence

The North America residential ductwork design software market size is expected to grow from USD 326.87 million in 2025 to USD 343.37 million in 2026 and is forecast to reach USD 439.29 million by 2031 at 5.05% CAGR over 2026-2031. The rising digitalization of HVAC design, aggressive building energy codes, and record residential retrofit spending are combining to drive software adoption. Contractors are increasingly favoring cloud-based platforms that reduce coordination time, automate compliance checks, and integrate seamlessly with BIM workflows. Electrification policies that accelerate heat-pump installations continue to drive full-house duct redesigns, pushing demand for simulation and CFD modules that validate airflow performance. Regional growth remains anchored in the United States, yet Mexico’s fast-moving construction sector is boosting overall momentum. Competitive rivalry is moderate, with large multi-discipline CAD providers working alongside specialty MEP vendors to build open ecosystems rather than closed architectures.

Key Report Takeaways

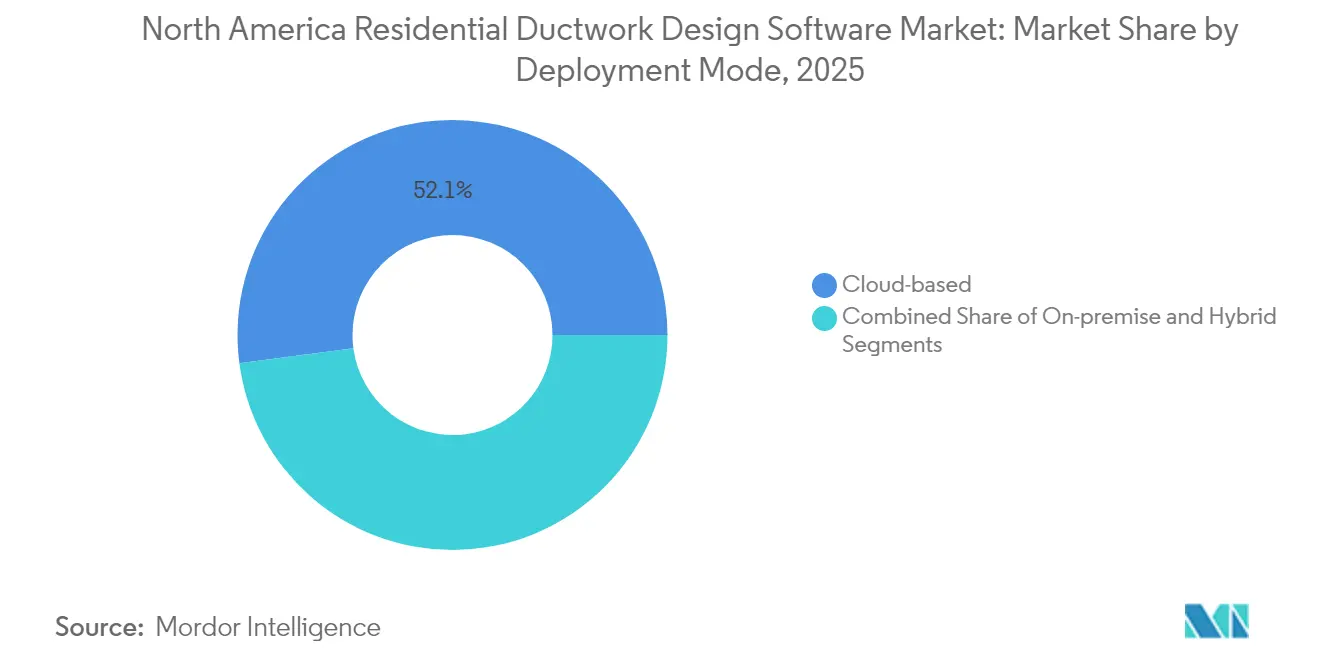

- By deployment mode, cloud-based solutions led the North America residential ductwork design software market with a 52.10% revenue share in 2025 and are projected to grow at a 6.37% CAGR through 2031.

- By end user, HVAC contractors commanded a 40.15% share of the North America residential ductwork design software market in 2025, whereas retrofit specialists were projected to post the highest CAGR at 6.82% through 2031.

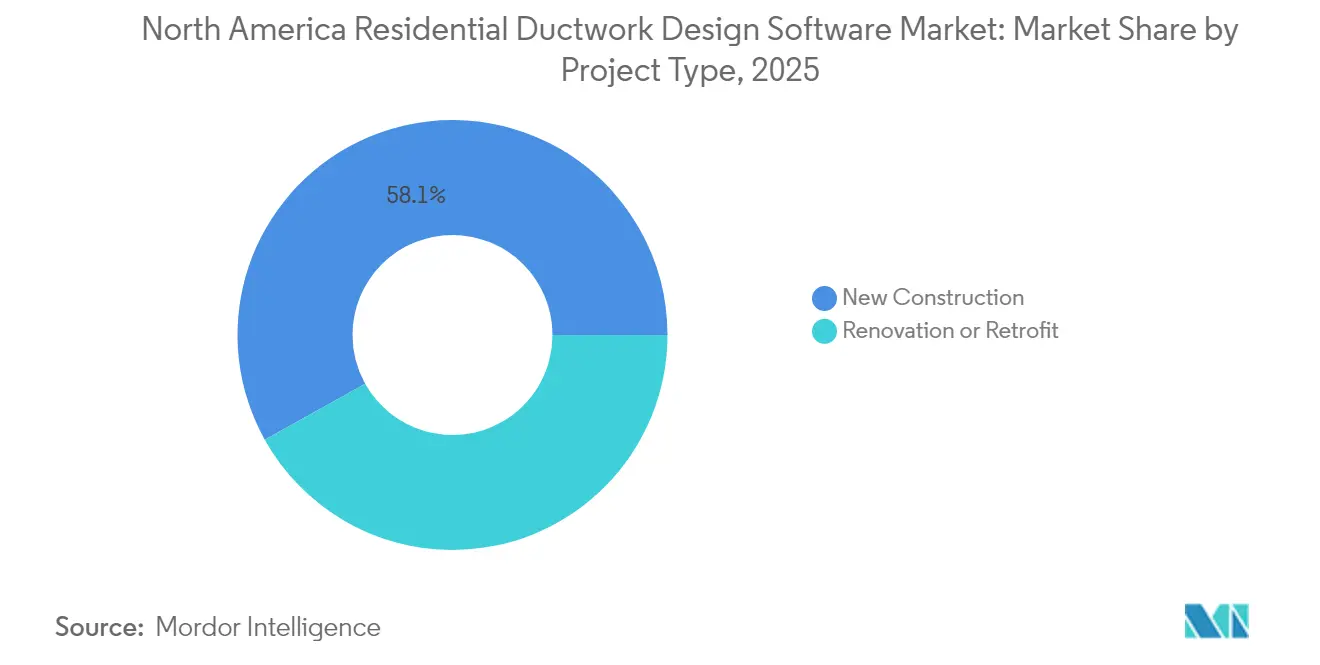

- By project type, new-construction projects accounted for 58.10% of the North America residential ductwork design software market size in 2025, while renovation and retrofit projects are expected to advance at a 5.82% CAGR through 2031.

- By functionality, the Design and Drafting modules captured a 47.55% share of the North America residential ductwork design software market in 2025; the Simulation and CFD modules are set to expand at a 7.05% CAGR through 2031.

- By geography, the United States held an 79.85% share of the North America residential ductwork design software market size in 2025, whereas Mexico showed the quickest growth at a 6.21% CAGR during the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Residential Ductwork Design Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in residential HVAC retrofit spending | +1.2% | United States, Canada | Medium term (2-4 years) |

| Stringent North American building energy codes | +0.9% | United States, Canada, Mexico | Long term (≥ 4 years) |

| Growing adoption of BIM workflows among HVAC contractors | +0.8% | United States, Canada | Medium term (2-4 years) |

| Rising use of AI-assisted duct sizing algorithms | +0.6% | United States, Canada | Long term (≥ 4 years) |

| Homeowner demand for IAQ-centric duct layouts | +0.5% | North America | Short term (≤ 2 years) |

| Incentive grants for heat-pump installations driving duct redesign | +0.7% | United States, Canada | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in Residential HVAC Retrofit Spending

Residential retrofit outlays climbed sharply, with the U.S. retrofit market reaching USD 16.43 billion in 2023 and progressing toward USD 19.88 billion by 2029, a 3.23% CAGR.[1]Sheet Metal and Air Conditioning Contractors' National Association, “The Residential HVAC Market Is Heating Up,” SMACNA, smacna.org Ductwork reuse strategies that leverage advanced modeling can reduce installed costs by up to 48%, prompting widespread adoption of software.[2]Emily Jenkins, “Reducing the Cost of Home Energy Upgrades in the U.S.: An Industry Survey,” Journal of Building Engineering, sciencedirect.com Heat-pump units now account for roughly 40% of HVAC shipments; however, they often require airflow adjustments that can only be accurately simulated with sophisticated design tools. State-level electrification incentives, such as New York’s Clean Heat Initiative, which offers USD 5,000 per full replacement, further stimulate demand for platforms that evaluate the feasibility of existing ducts. The North America residential ductwork design software market gains steady tailwinds as contractors use digital workflows to compress project timelines and safeguard retrofit economics.

Stringent North American Building Energy Codes

The 2024 International Energy Conservation Code introduced new leakage thresholds tied to conditioned floor area and equipment configuration, while exempting ventilation ducts from testing.[3]Residential Energy Services Network, “What to Expect in the 2024 IECC,” resnet.us California’s 2025 Energy Code mandates heat-pump systems in most new single-family homes and tightens ventilation budgets, adding climate-zone complexity that software must translate into compliant layouts. Proposed updates to the International Mechanical Code introduce new ventilation equations and permit reductions for balanced systems. These evolving regulations necessitate real-time rule sets, automated documentation, and rapid what-if analyses, underscoring the need for robust design platforms.

Growing Adoption of BIM Workflows Among HVAC Contractors

The usage of digital tools among HVAC contractors increased from 40% in 2020 to 65% in 2022, and industry surveys anticipate 80% penetration by 2024.[4]Autodesk, “Can Better MEP Solve Construction's Skilled Labor Shortage?,” autodesk.com Productivity gains are notable, as firms report that material utilization improves from 50% to more than 90% once on-site BIM coordination is eliminated. Interoperability pacts, such as the April 2024 agreement between Autodesk and Nemetschek, enable bidirectional data flow, allowing duct models created in Revit to be transferred seamlessly into ArchiCAD and Vectorworks. Cloud-connected platforms also provide field teams with version-controlled drawings, which reduces schedule slips. Adoption barriers, primarily learning curves, are receding as training resources expand, fueling the continuous growth of the North America residential ductwork design software market.

Rising Use of AI-Assisted Duct Sizing Algorithms

Machine-learning engines have begun to generate complete duct networks directly from room geometry and load data. Autodesk’s March 2025 Duct and Sheet Metal Generator exemplifies this advance by automatically selecting trunk and branch dimensions that balance velocity and pressure drop. AI modules also fine-tune layouts for optimal energy use, freeing designers to focus on client consultation rather than manual calculations. As skilled labor shortages intensify, contractors view AI tools as a force multiplier that democratizes expert-level outputs. Continuous algorithm training on thousands of completed projects promises improvements in both accuracy and speed, sustaining long-term uplift for the North America residential ductwork design software market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High initial license and training costs | -0.8% | North America | Short term (≤ 2 years) |

| Shortage of skilled BIM technicians | -1.1% | United States, Canada | Medium term (2-4 years) |

| Hesitancy of small contractors toward cloud SaaS due to data ownership concerns | -0.4% | North America | Short term (≤ 2 years) |

| Fragmented interoperability standards among ductwork add-ons | -0.3% | North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Initial License and Training Costs

Professional-grade platforms range from USD 495 for entry-level load-calculation packages to approximately USD 2,400 per year for full BIM authoring suites. Additional expenses for workstations, plug-ins, and 40-80 hours of structured training significantly impact small contractors. Although subscription pricing spreads costs over the project pipeline, some rural or low-volume firms still view the outlay as prohibitive. As cloud delivery matures, vendors are expected to roll out scaled tiers that match feature depth to company size, but near-term adoption may slow in price-sensitive segments of the North America residential ductwork design software market.

Shortage of Skilled BIM Technicians

The demand for technicians who can merge mechanical knowledge with digital workflows outstrips the supply. Trade-school cohorts are small, and graduates often require additional upskilling before they can effectively navigate multidisciplinary coordination tasks. The talent gap exacerbates wage pressure, increasing project costs and sometimes forcing firms to delay software deployment until staff can be adequately trained. Industry associations are expanding certification tracks, yet the pipeline will take years to normalize, holding back optimal growth for the North America residential ductwork design software market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Mode: Cloud Migration Accelerates

Cloud platforms captured 52.10% of the North America residential ductwork design software market in 2025, and this share is projected to grow at a 6.37% CAGR through 2031. Subscription access removes heavy upfront infrastructure costs, while browser-based interfaces support distributed design teams. Contractors report 15-20% workflow efficiency gains once real-time collaboration replaces file-based exchanges. Yet, certain rural projects experience latency challenges that encourage hybrid strategies, utilizing local compute for CFD runs and cloud storage for documentation. Ongoing improvements in edge processing and bandwidth availability are expected to overcome residual performance concerns.

On-premise deployments continue to serve firms with strict data-sovereignty rules or limited internet access. Hybrid options appeal to national contractors that maintain centralized servers for large simulations but employ cloud dashboards for project tracking. As vendor roadmaps increasingly prioritize API consistency, even cautious adopters are forecast to transition workloads to the cloud, reinforcing long-term expansion of the North America residential ductwork design software market.

By End User: Retrofit Specialists Drive Innovation

HVAC contractors accounted for 40.15% of 2025 revenue, thanks to project volume and established client relationships. Retrofit specialists, however, deliver the fastest growth, at a 6.82% CAGR, as electrification retrofits surge across the aging housing stock. These firms invest heavily in simulation and CFD features that predict airflow under modified duct paths, allowing them to guarantee post-install comfort and efficiency. Mechanical engineers remain important buyers for complex custom homes that demand meticulous load calculations. Home builders are increasingly incorporating design software into their production workflows to accelerate schedule adherence and minimize change orders.

The retrofit boom rewards platforms that combine laser-scan import, existing duct condition assessment, and performance gap analytics. As regulatory pressure drives deeper energy upgrades, specialized firms will wield advanced tools as competitive leverage, expanding their share of the North America residential ductwork design software market.

By Project Type: Renovation Gains Momentum

New-construction projects still held 58.10% share in 2025, yet renovation and retrofit work is climbing at 5.82% CAGR. Code updates and incentive programs significantly expand the scope of required upgrades, extending beyond equipment swaps to encompass precise modeling of constrained spaces and legacy systems. Since older homes often feature atypical duct geometries, renovation workflows depend on 3D capture and flexible routing algorithms not always needed in greenfield designs. Software vendors now package dedicated retrofit toolkits that overlay new proposals on point-cloud scans, thereby reducing site visits and rework.

Builders in seismic or high-wind zones value these capabilities because structural retrofits frequently coincide with mechanical overhauls. Integration of duct models with structural reinforcement drawings helps limit field clashes and expedite permit approvals. As housing stock ages, renovation-centric features will continue to lift the North America residential ductwork design software market.

By Functionality: Simulation Capabilities Surge

The Design and Drafting modules commanded a 47.55% share in 2025, reflecting their role as the core authoring environment for construction documents. Load Calculations remain indispensable for right-sizing equipment, and Estimation modules accelerate bid turnaround. The Simulation and CFD category, however, is charting the fastest trajectory, with a 7.05% CAGR. Contractors credit CFD visualizations with reducing post-installation balancing calls, while code officials increasingly request performance proofs before issuing occupancy certificates.

AI-integrated solvers now iterate multiple duct configurations in minutes, presenting cost-performance tradeoffs that once required hours of manual adjustment. As heat-pump airflow requirements differ from legacy furnaces, simulation helps teams validate comfort under lower supply-air temperatures. The resulting reduction in callbacks and warranty claims supports rising investment in advanced modules, solidifying the competitive edge of vendors offering high-fidelity solvers within the North America residential ductwork design software market.

Geography Analysis

The United States continues to anchor the region with a 79.85% share, underpinned by stringent codes and a mature BIM culture. The United States dominates due to the nationwide adoption of the 2024 IECC, which is layered with state codes that tighten leakage limits and encourage heat-pump solutions. BIM reliance is well established among large mechanical contractors, and cloud collaboration aligns with geographically dispersed project teams. Localized climate zones, from humid southeast to cold northeast, require varied duct strategies that benefit from flexible design platforms.

Canada upholds high standards for mechanical ventilation and envelope tightness, prompting installers to use software that certifies airflow and energy metrics. Provincial rebate programs for deep energy retrofits stimulate additional demand. Cross-border design firms share workflows between U.S. and Canadian offices, favoring interoperable solutions that dynamically apply code libraries.

Mexico, with 6.21% CAGR through 2031, leads growth as residential construction expands and HVAC adoption deepens. Mexico’s urbanizing corridors around Monterrey, Guadalajara, and Mexico City are witnessing the rapid rollout of heat-pump and split-ducted systems in new mid-rise housing. Emerging regulations require documented design calculations, prompting contractors to transition from 2D drafting to comprehensive duct modeling suites. As domestic HVAC manufacturing expands, local distributors partner with software vendors to bundle design licenses with equipment sales, thereby accelerating the uptake of these solutions across the country.

Competitive Landscape

Market concentration is moderate, with Autodesk, Trimble, and Bentley leveraging broad CAD platforms, while MagiCAD and Design Master compete through their specialized depth in MEP. Strategic alliances shape the landscape; the Autodesk-Trane integration embeds load-calculation expertise directly into BIM authoring, while API agreements between major vendors reduce data-silo friction. Consolidation within the broader HVAC equipment sector can influence software direction, as OEMs seek design environments that showcase proprietary performance advantages.

Innovation centers on AI-driven layout engines, real-time code compliance dashboards, and cost-performance analytics. Vendors emphasize open API ecosystems to attract third-party plug-ins that extend niche capabilities. Pricing strategies range from entry-level SaaS tiers designed for small firms to enterprise bundles that integrate model data with field execution and commissioning. The combined share of the top five providers approaches 65%, positioning the sector at a moderate level of consolidation that still allows nimble newcomers to carve out specialty niches within the North America residential ductwork design software market.

North America Residential Ductwork Design Software Industry Leaders

Autodesk, Inc.

Trimble Inc.

Dassault Systèmes SE

Graphisoft SE

Design Master Software, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Autodesk has released the Duct and Sheet Metal Generator plug-in, featuring machine-learning layout automation.

- November 2024: Trane Technologies partnered with Autodesk to link TRACE 3D Plus with Revit for seamless thermal modeling.

- September 2024: Nemetschek Group updated Allplan 2025, Vectorworks 2025, and Archicad 28 with AI-enhanced collaboration functions.

- August 2024: EPA released Indoor AirPlus Version 2, which strengthens duct-sealing and testing requirements.

North America Residential Ductwork Design Software Market Report Scope

| Cloud-based |

| On-premise |

| Hybrid |

| HVAC Contractors |

| Mechanical Engineers |

| Home Builders |

| Retrofit Specialists |

| New Construction |

| Renovation or Retrofit |

| Design and Drafting |

| Load Calculation |

| Simulation or CFD |

| Estimation and Costing |

| United States |

| Canada |

| Mexico |

| By Deployment Mode | Cloud-based |

| On-premise | |

| Hybrid | |

| By End User | HVAC Contractors |

| Mechanical Engineers | |

| Home Builders | |

| Retrofit Specialists | |

| By Project Type | New Construction |

| Renovation or Retrofit | |

| By Functionality or Module | Design and Drafting |

| Load Calculation | |

| Simulation or CFD | |

| Estimation and Costing | |

| By Country | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

What is the current value of the North America residential ductwork design software market?

The market stands at USD 343.37 million in 2026.

How fast is the market expected to grow?

It is forecast to expand at a 5.05% CAGR and reach USD 439.29 million by 2031.

Which deployment mode shows the quickest growth?

Cloud-based platforms lead, advancing at a 6.37% CAGR through 2031.

Which user segment is expanding the fastest?

Retrofit specialists record the highest growth outlook at 6.82% CAGR.

Which country in the region is seeing the quickest adoption?

Mexico posts the fastest growth at a 6.21% CAGR through 2031.

Page last updated on: