Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

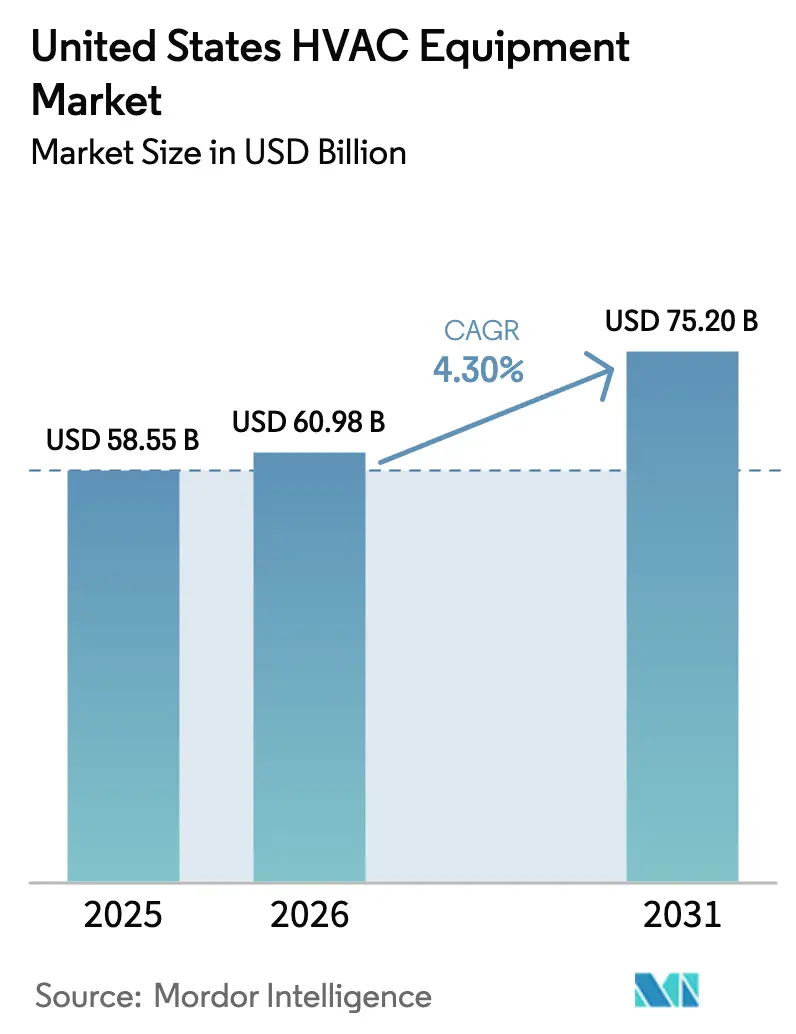

| Base Year Market Size (2025) | USD 58.55 Billion |

| Market Size (2026) | USD 60.98 Billion |

| Market Size (2031) | USD 75.20 Billion |

| Growth Rate (2026 - 2031) | 4.30% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States HVAC Equipment Market Analysis by Mordor Intelligence

The United States HVAC Equipment Market size was valued at USD 58.55 billion in 2025 and is estimated to grow from USD 60.98 billion in 2026 to reach USD 75.20 billion by 2031, at a CAGR of 4.30% during the forecast period (2026-2031).

Strong federal electrification policies, the rapid aging of installed systems, and the mainstreaming of building automation are converging to lift demand in both residential and commercial settings. Heat-pump incentives created by the Inflation Reduction Act (IRA) have begun to redirect sales away from gas furnaces in regions once dominated by fossil-fuel heating.[1]U.S. Department of Energy, “Heat Pump Technologies,” energy.gov Simultaneously, the national refrigerant phase-down is accelerating equipment obsolescence and bringing high-efficiency, low-GWP platforms to the front of manufacturers’ roadmaps. Grid-interactive controls, predictive maintenance software, and utility rebates continue to reinforce premiumization trends, while the skilled-labour shortage imposes a natural ceiling on the annual conversion rate of the installed base.

Key Report Takeaways

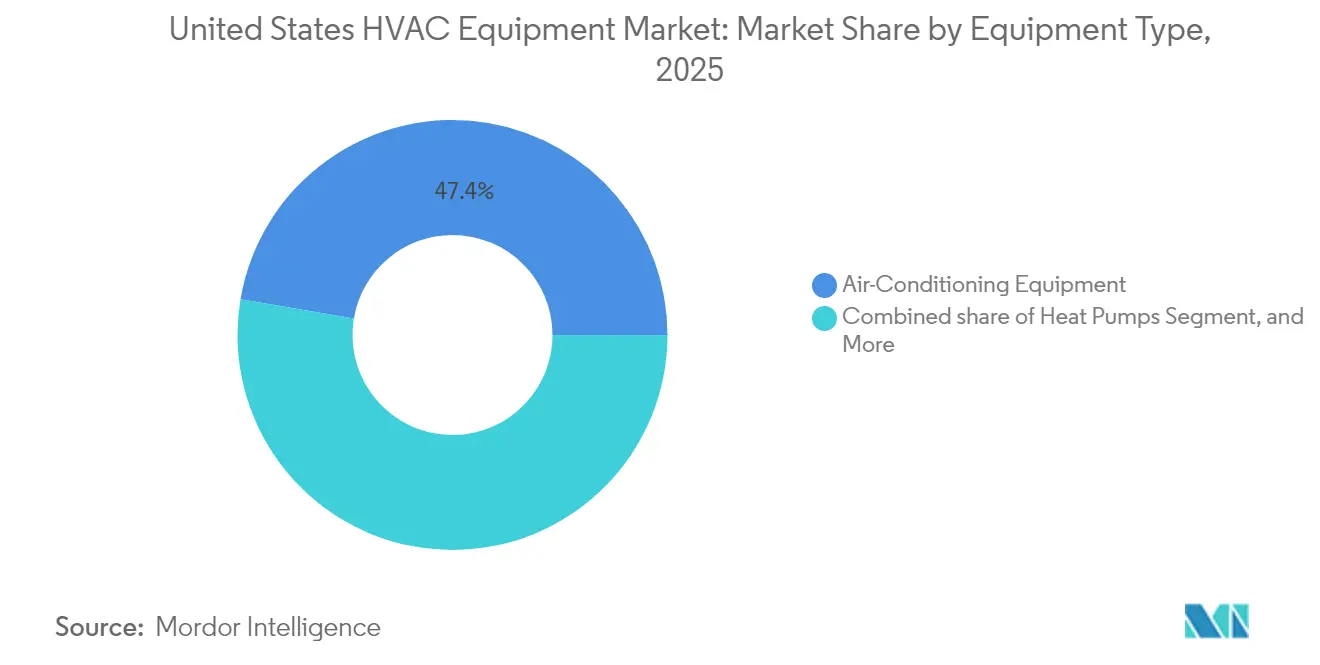

- By equipment type, air-conditioning devices captured 47.35% of the United States HVAC equipment market share in 2025; heat pumps are projected to expand at a 6.21% CAGR through 2031.

- By end user, the residential segment held 45.68% of the United States HVAC equipment market size in 2025, while commercial applications are advancing at a 5.84% CAGR to 2031.

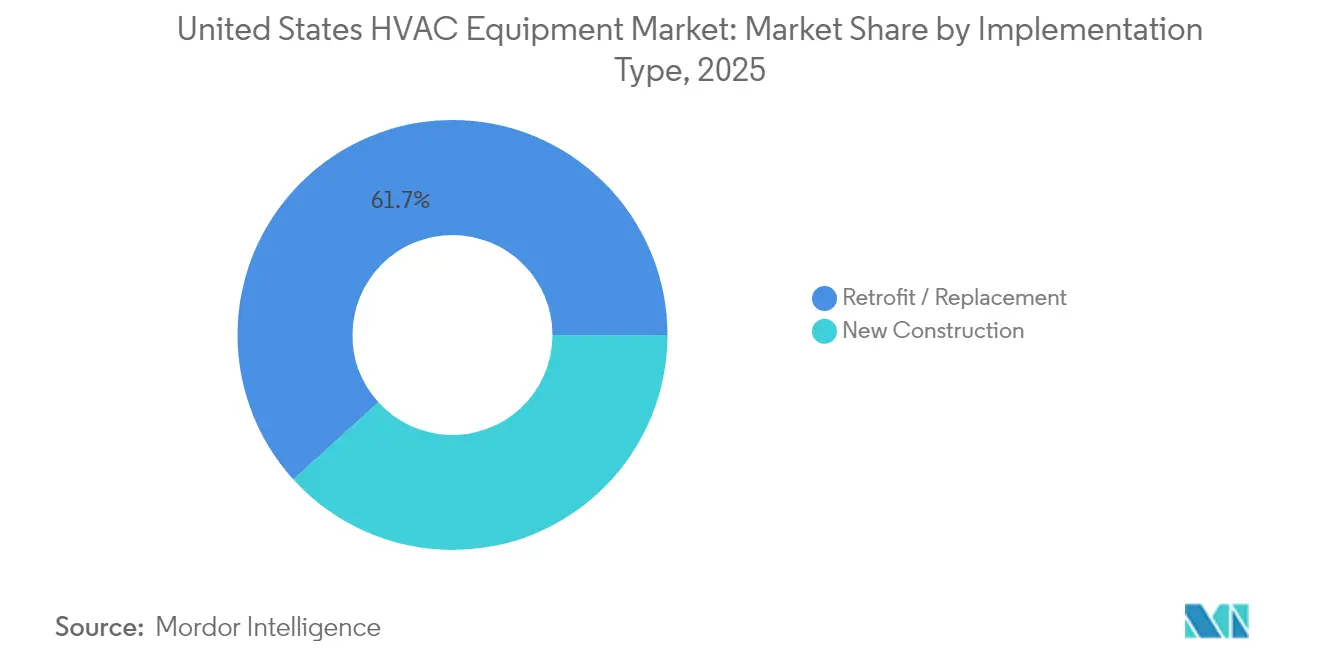

- By implementation type, retrofit and replacement projects commanded 61.74% of the United States HVAC equipment market size in 2025 and are growing at a 6.78% CAGR through 2031.

- By efficiency rating, low-efficiency products maintained a 66.12% share of the United States HVAC equipment market size in 2025; the high-efficiency tier is accelerating at a 7.02% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States HVAC Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing adoption of home and building automation systems | +0.80% | National, with early gains in California, New York, Texas | Medium term (2-4 years) |

| Increasing demand for energy-efficient HVAC equipment | +1.20% | National, strongest in Northeast and West Coast | Long term (≥ 4 years) |

| Stringent federal and state energy-efficiency regulations | +0.90% | National, with state variations in California, New York | Long term (≥ 4 years) |

| Accelerated equipment replacement cycles in aging building stock | +1.10% | National, concentrated in Northeast and Midwest | Short term (≤ 2 years) |

| IRA-driven heat-pump electrification incentives | +0.70% | National, highest impact in cold climate zones | Medium term (2-4 years) |

| Micro-fulfillment centre boom boosting compact HVAC demand | +0.30% | Urban centers, e-commerce distribution hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Adoption of Home and Building Automation Systems

Commercial developers and large homeowners now evaluate new units by their native connectivity as much as by efficiency. Systems with open APIs integrate seamlessly with facility management platforms, enabling schedule optimization and predictive maintenance that trim energy use by 15-20%. IoT-ready thermostats and zoning kits are becoming base-spec items, shortening replacement cycles because legacy units cannot communicate with modern software. Corporations chasing ESG targets view connected HVAC as low-hanging fruit for measurable carbon cuts, driving bulk procurement during capital-planning cycles. Integrators profit from long-tail software subscriptions, a model that reshapes how revenue is earned throughout the equipment life cycle.

Increasing Demand for Energy-Efficient HVAC Equipment

Title 24 updates, minimum SEER uplifts, and smart-grid interoperability rules have triggered field-level specification shifts toward premium gear. While high-efficiency units carry a 15-25% price premium, rising electricity tariffs and time-of-use billing tilt life-cycle economics in their favour. Utilities now pair demand-response payments with equipment rebates, nudging owners toward variable-speed compressors and cold-climate heat pumps. As electrification marches forward, peak-demand fees become pronounced, sharpening attention on kilowatt-level performance during design. Manufacturers, in response, phase variable refrigerant flow (VRF) features into mainstream product lines to satisfy code and financial metrics simultaneously.

Stringent Federal and State Energy-Efficiency Regulations

The HFC phase-down requires an 85% production cut in R-410A by 2036, compelling OEMs to redesign every high-volume chiller, rooftop, and split system around R-32, R-454B, or equivalent blends.[2]Environmental Protection Agency, “Phasing Down Hydrofluorocarbons,” epa.gov States overlay these federal rules with independent timelines New York’s Climate Leadership and Community Protection Act mandates electrification for buildings above 25,000 ft², pulling forward capital spending.[3]Climate Leadership and Community Protection Act, climate.ny.gov Compliance adds 10-15% to equipment cost, incentivizing scale and potentially choking smaller brands unable to fund dual-refrigerant portfolios. For owners, regulatory certainty clarifies the cost of procrastination, reinforcing near-term replacement decisions.

Accelerated Equipment Replacement Cycles in Aging Building Stock

Roughly 40% of commercial floor space dates back more than four decades, meaning the original chillers, boilers, and air handlers are simultaneously reaching end-of-life. Bulk failures have pushed lead times on large units to 16-24 weeks, well above historical norms. Because owners want connectivity and high efficiency in their next systems, simple component swaps no longer suffice. Instead, entire system overhauls are specified, creating a step-change in both ticket size and technological complexity. Contractors face project queues that extend quarterly, elongating revenue recognition but compressing the delivery schedule once products arrive.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront cost of advanced HVAC systems | -0.90% | National, strongest impact in price-sensitive residential segment | Medium term (2-4 years) |

| Skilled labour shortages for installation and service | -1.10% | National, acute in rural and secondary markets | Long term (≥ 4 years) |

| Electrical-grid capacity constraints for all-electric retrofits | -0.60% | Urban centers, aging grid infrastructure regions | Medium term (2-4 years) |

| Uncertain compliance costs from refrigerant phase-down | -0.40% | National, highest impact on commercial segment | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost of Advanced HVAC Systems

Connected, high-SEER heat pumps cost 30-50% more than legacy furnaces, and adding networked controls lifts project budgets by another 15-20%. For single-family homeowners, the absence of subsidized financing keeps payback periods outside a three-year psychological threshold. Commercial real-estate operators have shortened ROI requirements to five years or less, excluding many cutting-edge offerings. While rebates alleviate some pain, funding caps inject uncertainty into long-term planning. Consequently, many buyers stage upgrades, holding on to sub-optimal solutions for another season.

Skilled Labour Shortages for Installation and Service

A forecast deficit of 115,000 HVAC technicians by 2030 threatens to limit the annual conversion rate that the United States HVAC equipment market can sustain. Smart-system commissioning now demands cybersecurity know-how alongside refrigerant-handling certification, widening the skills gap. Install-backlogs add 4-6 weeks to residential cycles and double that for complex commercial jobs, forcing property owners to run inefficient units through another peak season. Workforce training programs lag behind technology evolution, keeping labour capacity structurally tight even as demand grows.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Heat Pumps Drive Electrification Shift

The United States HVAC equipment market size for air-conditioning products stood highest in 2025, when they delivered 47.35% of total value. Cooling remains the core need across U.S. climates, especially in rapidly growing Sun Belt states. Yet heat pumps, aided by federal credits, are forecast to register a 6.21% CAGR through 2031, the fastest among all categories. As cold-climate performance improves, these units take share from both gas furnaces and straight-cool splits.

Regulatory refrigerant bans will accelerate chiller replacements, and vendors that offer R-32 or R-454B compatibility are set to gain volume early in the cycle. Meanwhile, ventilation equipment rises in priority as air-quality norms evolve, and UV-C or MERV-13 filtration is increasingly embedded in packaged units for hospitality and health-care projects. The holistic turn toward indoor environmental quality keeps demand resilient even when new construction slows, supporting the long-run trajectory of the United States HVAC equipment market.

By End User: Residential Segment Leads Smart Technology Adoption

Residential buyers retained a 45.68% slice of the United States HVAC equipment market share in 2025 and are embracing smart controls at an exceptional pace. More than one-third of new single-family homes shipped with connected thermostats that link seamlessly to heat pumps eligible for up to USD 8,000 in IRA credits. While upfront cost sensitivity remains, low-interest utility loans improve the affordability of premium gear.

Commercial demand centers on building automation, occupancy-based ventilation, and ESG-aligned energy reporting. Offices and retail stores pivot toward adaptive operation strategies that cut idle energy draw. Industrial users require tighter temperature and humidity windows for production consistency, reinforcing demand for specialized, high-capacity designs. Though decision cycles lengthen, each transaction is larger, injecting stability into the overall revenue profile of the United States HVAC equipment market.

By Implementation Type: Retrofit Market Dominates Equipment Demand

Retrofit and replacement undertakings generated 61.74% of market value in 2025, far outpacing the capex tied to new construction. With 1990s-era equipment failing end masse, owners prefer whole-system swaps to ensure futureproof connectivity and compliance with low-GWP rules. The IRA sweetens economics, pushing the segment to a 6.78% CAGR to 2031.

New construction, representing the remaining 38.26%, contends with high interest rates and skilled labour scarcity. Yet every ground-breaking today specifies advanced controls and higher SEER baselines, guaranteeing a richer bill of materials per square foot. Modular system designs gain favour where project schedules are compressed, reducing on-site work and installation risk.

By Efficiency Rating: High-Efficiency Tier Accelerates Market Premiumization

Standard-efficiency units still occupy 66.12% of United States HVAC equipment market size in 2025, a reflection of contractor habit and price considerations. However, the high-efficiency cohort, growing at 7.02% CAGR, is steadily eroding that base. ENERGY STAR labelling and variable-speed technology migrate down the price curve, aided by mandatory SEER-2 thresholds that remove the lowest-tier products from the catalogue.

Cold-climate heat-pump breakthroughs further tilt the calculus toward efficient electrification in northern states. Commercial specifiers, under pressure to publish Scope-2 carbon data, increasingly pick high-efficiency VRF or dedicated outdoor-air systems with energy-recovery modules that satisfy both ventilation and energy codes in one shot.

Geography Analysis

Climatic diversity and regulatory heterogeneity shape local demand profiles across the United States HVAC equipment market. The Northeast leads high-efficiency adoption as elevated electricity rates and stringent state laws make premium equipment financially sensible. Massachusetts and New York impose building performance standards that implicitly favour inverter-driven heat pumps and advanced controls. Cold-climate breakthroughs now allow electrified heating to replace fossil systems without comfort compromises, catalysing a wave of oil-to-heat-pump conversions.

The Southeast captures significant cooling-centric growth. Florida and Texas absorb migration inflows and commercial expansions, putting air-conditioning equipment at the heart of mechanical plans. Humidity challenges spur demand for units capable of latent-load control, and mold-prevention features are routinely specified in hospitality and multifamily builds. Time-of-use tariffs across Southern utilities encourage adoption of demand-response-ready thermostats in both residential and light-commercial markets, anchoring smart-grid traction in the region.

On the West Coast, California sets the regulatory pace under its Title 24 code, a template that other states often copy. High rebate levels covering up to 60% of heat-pump installs make electrification cost-competitive with gas, even before lifecycle savings are considered. The technology sector’s dense footprint fuels specialized cooling demand for data centers, propelling sales of precision environmental control systems. Water-scarcity concerns shift preference toward air-cooled chillers, cementing a long-term equipment mix different from that in other climate zones.

Competitive Landscape

The United States HVAC equipment market features moderate concentration. Tier-one brands Carrier Global Corporation, Trane Technologies, and Daikin Industries leverage scale to spread R-D expenses tied to refrigerant shifts and IoT integration. Carrier alone commits roughly USD 200 million per year to future platforms and has earmarked additional capex to ramp heat-pump capacity at its Indiana plant. Trane’s full consolidation of its Mitsubishi Electric Trane HVAC US venture hands its direct control over VRF technology that is central to commercial electrification agendas.

While incumbents reinforce moats with dense dealer networks and nationwide after-sales operations, software-centric startups disrupt value capture. Firms such as Nest Labs and Ecobee monetize analytics and demand-response aggregation rather than hardware margins, forcing OEMs to embrace open-API philosophies. Patent filings on predictive-maintenance algorithms signal a pivot toward service-driven recurring revenue models, a notable shift from historically product-centric competition.

Niche opportunities emerge where conventional designs fall short micro-fulfilment centers require compact, high-BTU-per-cubic-foot units, and edge-data-center operators seek liquid-cooling hybrids. Mid-sized manufacturers deploy agile engineering teams to tailor solutions quickly, trading breadth for depth. As a result, the United States HVAC equipment market maintains a balanced rivalry: scale advantages endure, yet innovation opportunities remain open.[4]Carrier Global Corporation, “Corporate Responsibility and Innovation,” corporate.carrier.com

United States HVAC Equipment Industry Leaders

Daikin Industries Ltd

Lennox International Inc.

Rheem Manufacturing Company

Trane Inc. (Trane Technologies PLC)

Mitsubishi Electric Hydronics & IT Cooling Systems (Mitsubishi Electric Corporation)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2024: Carrier Global Corporation announced a USD 300 million investment to expand heat-pump manufacturing capacity at its Indiana facility, targeting a 50% production lift by 2026.

- August 2024: Trane Technologies completed the USD 870 million acquisition of Mitsubishi Electric Trane HVAC US, gaining full control of VRF and heat-pump portfolios.

- July 2024: Johnson Controls launched the OpenBlue Enterprise Manager platform, promising 20-30% energy savings through AI-based HVAC optimization.

- June 2024: Daikin Industries unveiled a USD 150 million R-D program for next-generation refrigerants and heat-pump systems aimed at 2026 launches.

United States HVAC Equipment Market Report Scope

HVAC equipment ensures thermal comfort and maintains acceptable indoor air quality in indoor and vehicular environments. This technology plays a crucial role in various settings, including residential structures like single-family homes, apartment complexes, hotels, and senior living facilities. In addition, it is vital for medium-to-large industrial and office buildings, such as hospitals, where conditions like temperature and humidity are meticulously regulated using fresh outdoor air to ensure safety and health.

The market is defined by the revenue accrued from the sales of HVAC equipment of different types by major market players in the United States. The study also tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports the market estimations and growth rates over the forecast period.

The US HVAC equipment market is segmented by type of equipment (air conditioning equipment [unitary air conditioners, room air conditioners, packaged terminal air conditioners, and chillers], heating equipment [warm air furnace [gas and oil], boilers, room & zone heating equipment, heat pumps [air-sourced and geothermal], and ventilation equipment [air handling units, fan coil units, building humidifiers, and dehumidifiers]), end user (residential, commercial, and industrial), region (West, South, Midwest, and Northeast). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Equipment Type

| Air-Conditioning Equipment | Unitary Air Conditioners |

| Room Air Conditioners | |

| Packaged Terminal Air Conditioners | |

| Chillers | |

| Heating Equipment | Warm-Air Furnaces (Gas and Oil) |

| Boilers | |

| Room and Zone Heating Equipment | |

| Heat Pumps (Air-Source and Geo-thermal) | |

| Ventilation Equipment | Air Handling Units |

| Fan Coil Units | |

| Building Humidifiers and Dehumidifiers |

By End User

| Residential |

| Commercial |

| Industrial |

By Implementation Type

| New Construction |

| Retrofit / Replacement |

By Efficiency Rating

| Low-Efficiency Tier |

| High-Efficiency Tier |

| By Equipment Type | Air-Conditioning Equipment | Unitary Air Conditioners |

| Room Air Conditioners | ||

| Packaged Terminal Air Conditioners | ||

| Chillers | ||

| Heating Equipment | Warm-Air Furnaces (Gas and Oil) | |

| Boilers | ||

| Room and Zone Heating Equipment | ||

| Heat Pumps (Air-Source and Geo-thermal) | ||

| Ventilation Equipment | Air Handling Units | |

| Fan Coil Units | ||

| Building Humidifiers and Dehumidifiers | ||

| By End User | Residential | |

| Commercial | ||

| Industrial | ||

| By Implementation Type | New Construction | |

| Retrofit / Replacement | ||

| By Efficiency Rating | Low-Efficiency Tier | |

| High-Efficiency Tier | ||

Key Questions Answered in the Report

How large is the United States HVAC equipment market in 2026?

It is valued at USD 60.98 billion in 2026 and is forecast to reach USD 75.20 billion by 2031.

What CAGR is expected for heat pumps through 2031?

Heat pumps are projected to post a 6.21% CAGR, the fastest among all equipment categories.

Which segment commands the greatest share of replacement demand?

Retrofit and replacement projects account for 61.74% of market value in 2025 and maintain a 6.78% CAGR outlook.

How do federal incentives influence residential adoption?

IRA tax credits of up to USD 8,000 make heat pumps cost-competitive, accelerating residential uptake.

Which regions are adopting high-efficiency systems the quickest?

The Northeast leads, driven by stringent state codes and higher electricity prices that favor premium equipment.

Why is the skilled-labor shortage a critical restraint?

A projected deficit of 115,000 technicians by 2030 extends installation lead times and caps the annual replacement rate.

Page last updated on: