Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

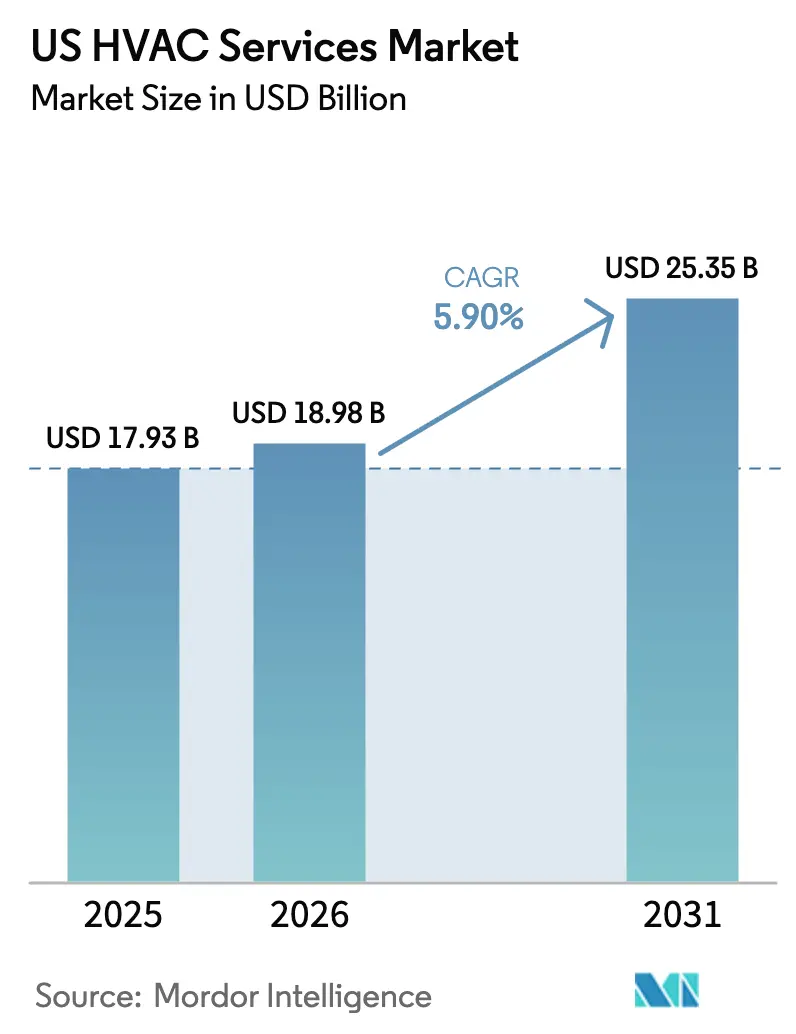

| Base Year Market Size (2025) | USD 17.93 Billion |

| Market Size (2026) | USD 18.98 Billion |

| Market Size (2031) | USD 25.35 Billion |

| Growth Rate (2026 - 2031) | 5.90% CAGR |

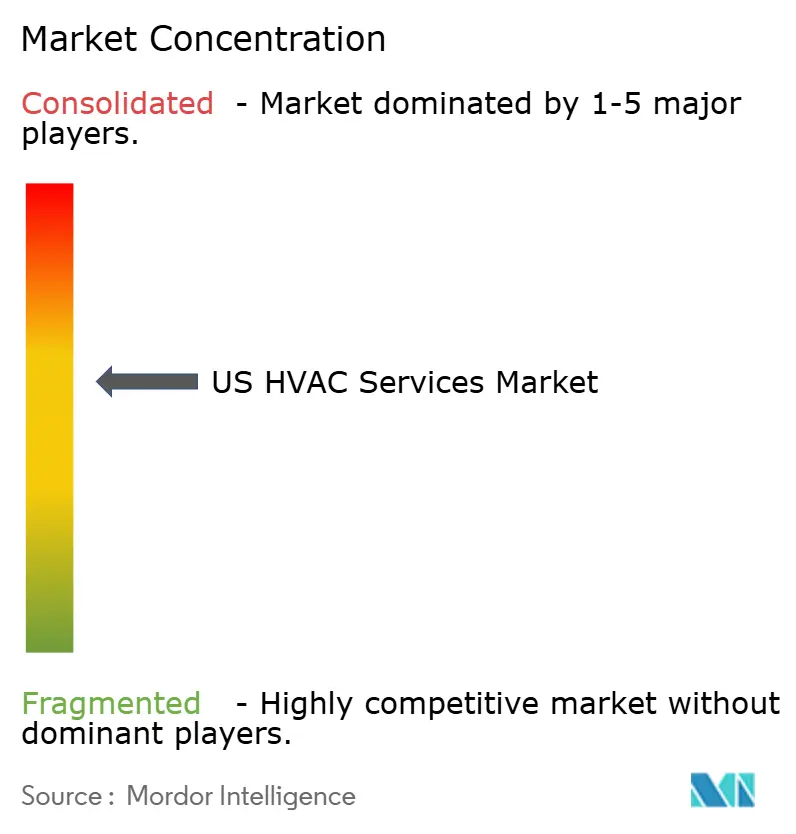

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

US HVAC Services Market Analysis by Mordor Intelligence

The US HVAC Services Market size was valued at USD 17.93 billion in 2025 and is estimated to grow from USD 18.98 billion in 2026 to reach USD 25.35 billion by 2031, at a CAGR of 5.90% during the forecast period (2026-2031).

The expansion reflects persistent demand for replacement of aging equipment, a robust construction pipeline, and sustained policy incentives that lower the cost of energy-efficient upgrades. Construction starts rose 9.9% month-over-month in April 2025, reinforcing a solid flow of installation contracts across commercial, residential, and industrial projects. Federal rebates under the Inflation Reduction Act, paired with state-level incentives, continue to stimulate homeowner retrofits and heat-pump adoption. Parallel shifts toward smart building controls and lower-GWP refrigerants are creating compliance-driven service opportunities that lift the recurring revenue mix. At the same time, a persistent shortage of skilled technicians tightens labor supply, lifts wages, and pressures small contractors, a dynamic that supports consolidation plays by capital-rich operators.

Key Report Takeaways

- By end user: The residential segment held 52% of the US HVAC services market share in 2025, while the industrial segment is forecast to expand at a 7.9% CAGR through 2031.

- By service category: Preventive maintenance contracts captured 39% revenue in 2025; energy-management services are projected to post the fastest growth at an 8.2% CAGR through 2031.

- By system type: Cooling/air-conditioning services accounted for 41% of the US HVAC services market size in 2025; building-management and automation services are set to increase at a 9.1% CAGR to 2031.

- By contract model: Recurring service agreements commanded 55% revenue in 2025 and are anticipated to grow at an 8.3% CAGR, underscoring the shift toward predictable OPEX budgeting.

- By region: The South region led with 38% share of the US HVAC services market size in 2025 and is advancing at a 7.2% CAGR through 2031, supported by population growth and rising cooling-degree days.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

US HVAC Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging Building Stock in OECD Markets Requiring Upgrades | +1.2% | United States, concentrated in Northeast and Midwest legacy metros | Medium term (2-4 years) |

| Mandatory Refrigerant Phase-Downs Driving Retrofit Demand | +1.5% | United States, with accelerated compliance in California and Northeast states | Short term (≤ 2 years) |

| Expansion of Hyperscale Data-Center Build-Outs | +1.3% | United States, clustered in Virginia, Texas, Arizona, and Oregon | Medium term (2-4 years) |

| HVAC-as-a-Service Contracts Unlocking Annuity Revenues | +0.8% | United States, early adoption in commercial real estate and healthcare | Long term (≥ 4 years) |

| Prefabricated Modular Retrofit Solutions Accelerating Project Timelines | +0.6% | United States, gaining traction in urban high-rise and institutional sectors | Medium term (2-4 years) |

| Utility-Backed Predictive-Maintenance Subscriptions Boosting Service Revenues | +0.5% | United States, pilot programs in California, New York, and Massachusetts | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Aging Building Stock in OECD Markets Requiring Upgrades

The median commercial building in the United States was 44 years old in 2025, and many structures erected before 1980 still rely on single-stage rooftop units that lack variable-speed drives, economizers, or modern controls.[1]U.S. Energy Information Administration, “Commercial Buildings Energy Consumption Survey,” eia.gov Energy use by those legacy units runs 30%-40% above code-minimum systems, which pressures landlords in cities with disclosure mandates to commit capital to HVAC retrofits. Institutional investors now price carbon intensity into property valuations, so ESG compliance is another trigger. The Infrastructure Investment and Jobs Act allocated USD 3.5 billion for public-sector upgrades that often serve as templates for private owners.[2]U.S. Department of Energy, “DOE Announces USD 3.5 Billion to Make Federal Buildings More Energy Efficient,” energy.gov Retrofit urgency is highest in the Northeast and Midwest where heating loads dominate, though Sun Belt buildings also pursue upgrades to manage peak cooling demand.

Mandatory Refrigerant Phase-Downs Driving Retrofit Demand

The American Innovation and Manufacturing Act targets an 85% cut in hydrofluorocarbon production by 2036, propelling the transition from R-410A toward lower-GWP A2L blends such as R-32 and R-454B. Because A2L refrigerants require sensors, ventilation, and spark-safe components, most existing equipment cannot simply be recharged, so owners face a retrofit or replacement decision well ahead of normal life cycles. ASHRAE Standard 15 drives up installation cost by USD 2,000-USD 5,000 for detection gear.[3]ASHRAE, “Standards and Guidelines,” ashrae.org California and several Northeastern states front-loaded compliance deadlines to 2028, compressing project schedules and crowding service pipelines.

Expansion of Hyperscale Data-Center Build-Outs

United States hyperscale operators earmarked USD 200 billion for new capacity in 2025 with AI workloads pushing rack densities beyond 50 kW, a regime that traditional air-cooled CRAC units cannot economically manage. Liquid cooling makes inroads, yet precision air handling still serves most colocation halls and demands 24/7 service coverage. Technicians in Virginia’s Loudoun County, Texas’s Dallas-Fort Worth, and Arizona’s Phoenix area command premiums of 15%-20% over residential counterparts because downtime penalties trigger heavy liabilities. Cybersecurity vetting now factors into vendor selection as attacks on building-automation networks could trigger thermal events.

HVAC-as-a-Service Contracts Unlocking Annuity Revenues

Outcome-based contracts bundle equipment, installation, energy, and maintenance into a predictable monthly fee, moving HVAC spending from CapEx to OpEx. Johnson Controls indicated that 18% of 2025 North American bookings fell under this model, up from 11% two years earlier. Federal agencies received 2025 guidance endorsing energy-savings performance contracts, teeing up a wave of public-sector opportunities. The model’s success hinges on IoT sensors streaming data that fuels predictive analytics, letting providers dispatch crews before failures unfold.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance |

|---|---|---|

| Skilled-labor shortages and escalating wage bills | -0.9% | United States, acute in Sun Belt growth markets and rural areas |

| Volatile HVAC component supply and material inflation | -0.7% | United States, with spillover from global semiconductor shortages |

| Cyber-Security Risks in Connected Building Systems | -0.4% | United States, concentrated in high-value commercial and government facilities |

| Rising Urban Permitting Barriers for A2L Refrigerant Storage | -0.3% | United States, primarily in dense urban jurisdictions with strict fire codes |

| Source: Mordor Intelligence | ||

Skilled-Labor Shortages and Escalating Wage Bills

HVAC employment is projected to add 23,000 roles from 2024-2034, but attrition will create 35,000 openings annually, leaving a sizable gap.[4]U.S. Bureau of Labor Statistics, “Heating, Air Conditioning, and Refrigeration Mechanics and Installers,” bls.gov Median hourly wages climbed to USD 28.50 in 2025, while A2L-certified master technicians topped USD 40. Labor now exceeds 55% of total project cost, up from 48% in 2020. Apprenticeships expand, yet four-year training requirements delay relief. Contractors deploy augmented-reality guidance and remote diagnostics to boost productivity, but wage inflation still squeezes margins, especially for smaller firms.

Volatile HVAC Component Supply and Material Inflation

Semiconductor shortages doubled lead times for variable-frequency drives and electronic expansion valves to 16 weeks in early 2025. Copper prices jumped 22% the same year, inflating the cost of refrigerant piping and coils. A Thailand factory fire sidelined one of the three dominant global scroll-compressor suppliers, exposing single-point-of-failure risk. Distributors enlarged inventories, but higher carrying costs ultimately flowed to customers as elevated service fees.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

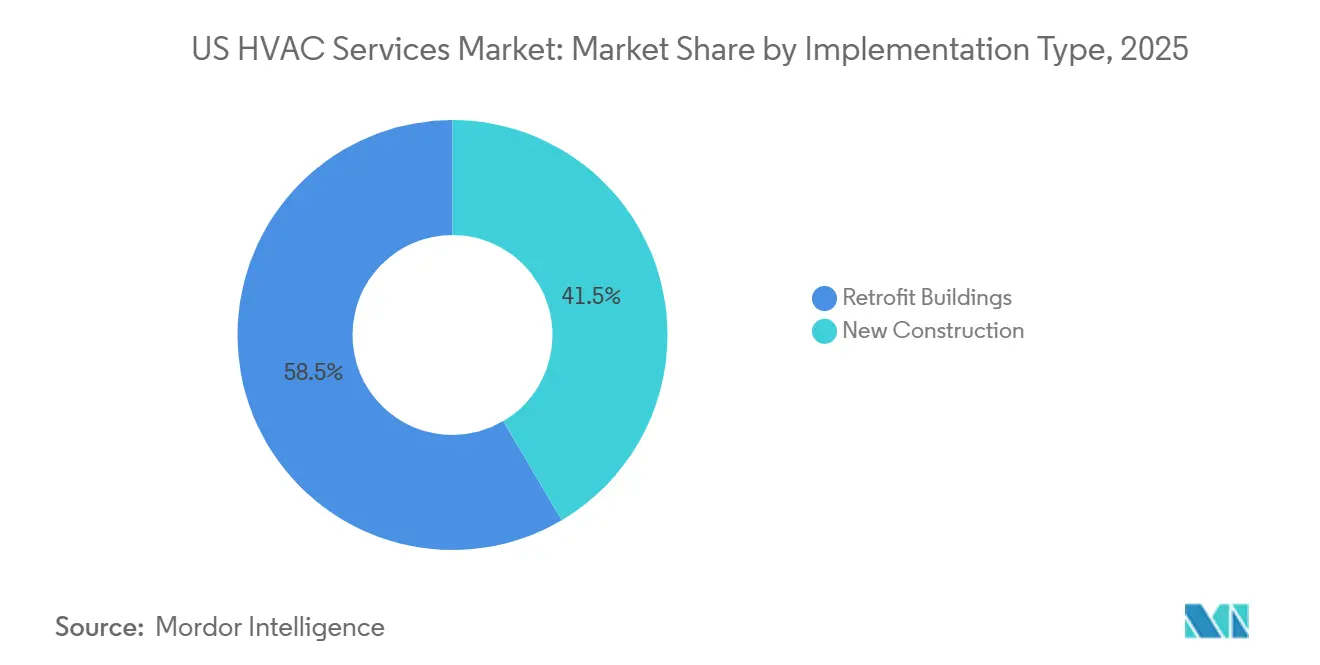

By Implementation Type – Retrofit Buildings Capture Sustained Upgrade Cycles

Retrofit buildings contributed 58.49% of 2025 revenue and are forecast to rise at 6.23% through 2031, reinforcing their role as the growth engine of the US HVAC services market. The US HVAC services market size for retrofit projects is expanding as owners race to replace R-410A systems ahead of the EPA phase-down calendar, creating a retrofit wave that overlaps with normal end-of-life milestones. ESG mandates tie asset values to operational carbon, so capital partners increasingly insist on variable-speed compressors and smart controls that lower kWh per square foot. Prefabricated modular kits, craned into place in a single day, slash disruption and let contractors deliver more jobs per crew per month.

New construction trails at a 5.40% CAGR yet still benefits from stronger design-build coordination. Developers in growth metros specify heat-recovery VRF systems that improve tenant comfort and differentiate Class A properties. Federal funding for public buildings steers toward retrofits, but ground-up healthcare and industrial facilities keep new-build pipelines active in Sun Belt states.

By Service Type – Energy-Efficiency Retrofits Outpace Break-Fix Work

Maintenance and repair retained the largest share at 46.15% in 2025, yet the highest momentum sits with energy-efficiency and retrofit services, advancing 7.03%. The US HVAC services market size for optimization projects benefits from utility rebates that buy down payback to three years or less. Controls upgrades climb 6.50% as buildings migrate from stand-alone thermostats to IP-connected platforms. Installation services face commoditization in residential split-system changeouts, motivating contractors to pivot toward bundled commercial scopes that fold in commissioning and multi-year service.

Consulting and other advisory work accelerates as owners seek third-party audits before allocating capital. Energy-savings performance contracts, now endorsed for federal facilities, enable providers to front the cost and recover investments from verified kWh reductions, reshaping revenue recognition.

By System Type – Ventilation and IAQ Services Gain Post-Pandemic Momentum

Cooling still dominated with 42.58% of 2025 revenue, but ventilation and IAQ lead in growth at 6.76%. Revised ASHRAE Standard 62.1 elevates outdoor air rates by 30% for high-density spaces, encouraging demand-controlled ventilation retrofits that balance air quality with energy spend. Healthcare clients specify MERV 13 and HEPA filters, creating annuity contracts for quarterly replacements. Heating services move gradually toward air-source heat pumps in cold climates where incentives close the cost gap with gas furnaces.

Integrated building-management services rise 6.20% as portfolios bundle HVAC with lighting, elevating cyber-risk profiles that drive service providers to add network segmentation to routine maintenance.

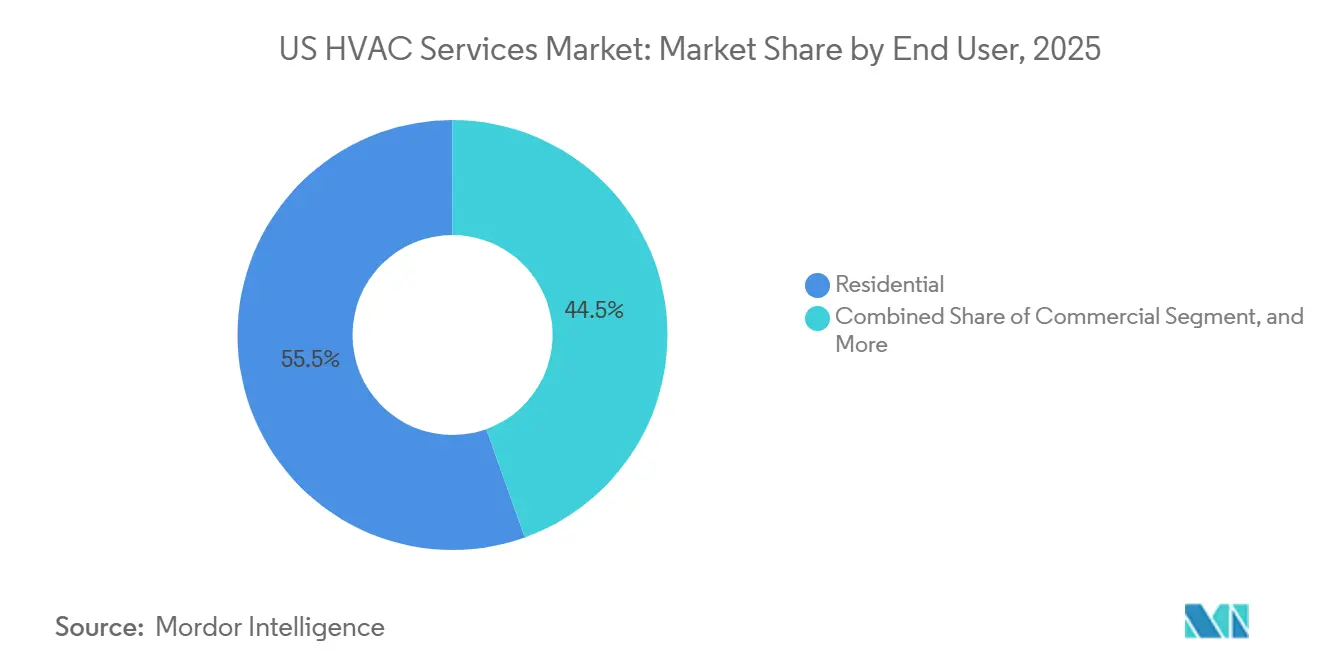

By End User: Industrial Facilities Accelerate Amid Reshoring

Residential accounted for 55.48% of 2025 demand, fueled by a vast installed base of single-family homes, yet industrial is the fastest at 6.88%. The US HVAC services market share held by industrial clients is growing due to biotech, semiconductor, and e-commerce warehouses that require precise thermal control. Pharmaceutical plants mandate ±1 °F tolerance zones, and logistics centers run HVAC year-round to protect automated picking systems.

Commercial tenants in office and hospitality properties continue to outsource maintenance to landlords under triple-net leases, producing fragmented, lower-ticket contracts. Residential growth steadies at 5.50% as smart thermostats and filter-delivery subscriptions deepen lifetime value per home.

By Application Vertical – Data Centers Lead as AI Workloads Surge

Data centers captured 23.71% of 2025 revenue and race ahead at 6.92%. The US HVAC services market size inside data halls benefits from racks above 50 kW that force specialized cooling topologies. Service contracts guarantee sub-hour response times and embed cybersecurity audits. Liquid cooling is still emergent, so precision air systems with redundant CRAH units dominate near-term demand.

Healthcare follows at 6.50% as hospitals retrofit isolation rooms and upgrade filtration. Education rises 6.20% on bond-funded upgrades to aging campuses, while hospitality prioritizes VRF systems that align with guest comfort metrics. Retail defers large upgrades, but preventive maintenance keeps doors open without capital outlays.

Geography Analysis

In North America, the US HVAC services market stands out, largely due to national building codes, licensing, and refrigerant regulations that bolster the competitive edge of domestic providers. These regulations create a structured environment that favors local companies, ensuring compliance and consistency across the market. States in the Sun Belt, particularly Texas, Arizona, Florida, and Georgia, experience a surge in cooling demands, with contractors in these regions managing 20%-25% more summer service calls than the national average. The high temperatures in these states drive the need for frequent maintenance and repair services, making them critical markets for HVAC service providers. As demand intensifies with the heat, wage premiums emerge: technicians in the Dallas-Fort Worth area command salaries 15% higher than their counterparts in cooler regions. This wage disparity reflects the increased workload and the specialized skills required to address the unique challenges posed by extreme heat.

In California, a looming 2028 ban on high-GWP equipment sales propels urgency in retrofitting, prompting owners to expedite changeouts to avoid potential supply bottlenecks. This regulatory shift is expected to significantly impact the market, as businesses and homeowners rush to comply with the new standards, creating opportunities for HVAC service providers to capitalize on the growing demand for retrofitting and equipment upgrades.

Meanwhile, in the Northeast and Midwest, the focus shifts to heating systems, with an emphasis on modernizing boilers to meet winter demands. These regions experience harsh winters, making efficient and reliable heating systems a necessity. The adoption of heat pumps is on the rise, bolstered by incentives that cover 25%-35% of installation costs, effectively shortening payback periods. These financial incentives make heat pumps a more attractive option for consumers, driving their adoption and contributing to the growth of the HVAC services market in these areas. In Loudoun County, Virginia, the concentration of hyperscale campuses exacerbates labor shortages, leading service vendors to offer signing bonuses to attract top-tier technicians. The high density of these campuses creates a unique demand for skilled HVAC professionals, as maintaining optimal environmental conditions is critical for the operation of data centers and other facilities. This labor shortage highlights the importance of workforce development and competitive compensation strategies in sustaining the growth of the HVAC services market.

Regulatory Landscape

The US HVAC services market is shaped by tightening federal requirements for refrigerant and energy-efficiency performance, which influence retrofit and replacement scopes. Under the American Innovation and Manufacturing (AIM) Act, the EPA Technology Transitions program is driving the shift away from high-GWP refrigerants used in many installed systems. A May 2026 EPA final rule, effective July 27, 2026, amended Technology Transitions requirements and added provisions intended to reduce stranded-inventory risk, including permission to install certain residential and light commercial systems manufactured or imported prior to January 1, 2025.

For equipment performance, the US Department of Energy (DOE) continues to regulate central air conditioners and heat pumps under 10 CFR 431.97 using SEER2 and HSPF2 metrics, with additional enforcement-related requirements under 10 CFR 429.134(k)(4) applying as of July 7, 2026. Beyond environmental and efficiency rules, trade policy also affects replacement economics: a June 1, 2026 Presidential proclamation lowered Section 232 tariffs on select residential HVAC systems and components (from 25% to 15%) through December 31, 2027, and reduced the domestic content threshold for a lower tariff tier from 95% to 85%. These changes affect sourcing strategies and installed-cost dynamics that service providers manage in bids and long-term agreements.

Competitive Landscape

The US HVAC services market remains moderately fragmented. The top five players - Johnson Controls, Carrier, Trane Technologies, Comfort Systems USA, and EMCOR Group - collectively control nearly 35% of 2025 revenue. OEMs lean on IoT-enabled diagnostics to upsell predictive-maintenance contracts, locking customers into proprietary parts and data platforms. Johnson Controls disclosed that outcome-based contracts rose to 18% of North American bookings in 2025, underscoring the pivot to recurring revenue.

Regional independents defend share with modular retrofit kits that slash project timelines and avoid single-vendor dependencies. Technology platforms such as on-demand technician marketplaces give smaller firms national reach, but quality assurance remains a hurdle. Cybersecurity credentials differentiate providers in data-center and government segments, responding to CISA advisories that insurers now reference in policy language.

M&A activity intensified: Carrier bought Viessmann Climate Solutions for EUR 12 billion (USD 13.1 billion) in December 2025, adding an 8,000-technician footprint and heat-pump expertise. Trane Technologies earmarked USD 150 million for twelve new hubs and 500 field techs in January 2026, illustrating capacity investments to chase hyperscale data-center contracts. White-space remains in buildings under 50,000 square feet, where owner fragmentation deters national chains and opens lanes for agile local contractors.

US HVAC Services Industry Leaders

Carrier Global Corporatio

Johnson Controls International PLC

Trane Technologies plc

Lennox International Inc.

Daikin Industries Ltd

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Near-term opportunity is concentrated in compliance-led retrofits that bundle refrigerant transition work with controls, safety, and commissioning services. The EPA Technology Transitions actions under the AIM Act, including the May 2026 final rule updates effective July 27, 2026, keep contractors active in equipment changeouts and system modifications beyond routine maintenance, especially where A2L adoption requires sensors, ventilation considerations, and code-aligned installation practices. DOE energy test and enforcement updates, including requirements applying from July 7, 2026 under 10 CFR 429.134(k)(4), further reinforce demand for verification, documentation, and performance-based service programs across commercial portfolios and higher-spec residential replacements.

A second expansion lane is mission-critical cooling and digitized service delivery for customers with uptime and audit requirements. Trane Technologies earmarked USD 150 million in January 2026 for new hubs and additional field technicians aimed at data-center and healthcare corridors, and Carrier expanded investment in ZutaCore in April 2026 to scale liquid-cooling capabilities for AI data centers. Together, these steps support broader service scope around 24/7 uptime coverage, thermal management integration, and cybersecurity-aware building automation maintenance, leaving room for contractors to combine BAS expertise, predictive maintenance tooling, and specialized technician training into recurring service agreements.

Recent Industry Developments

- July 2026: Carrier completed the sale of its Riello business to Ariston Group for about USD 440 million. The divestment sharpened Carrier’s portfolio focus and freed capital and management capacity for higher-priority segments, including energy-efficient and data-center-adjacent thermal management offerings.

- May 2026: Johnson Controls completed the acquisition of Alloy Enterprises, adding thermal management platforms relevant to data centers and industrial applications. The transaction strengthens Johnson Controls ability to deliver integrated, higher-value service and retrofit scopes where uptime and advanced cooling architectures support multi-year agreements.

- September 2025: The US Department of Energy published final rules updating certification, labeling, and enforcement provisions for multiple HVAC product classes, including VRF systems (under 65,000 Btu/h), compressors, and portable air conditioners. The changes raise the bar for compliance documentation and performance verification, increasing demand for contractor capabilities in commissioning, testing, and standards-aligned service delivery.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the revenue earned in the United States from providing HVAC-related services for buildings, including planning, installation labor, retrofit work, preventive maintenance, and repair work tied to heating, ventilation, air conditioning, refrigeration, and connected controls.

Scope exclusions: This sizing excludes sales of brand-new HVAC equipment, over-the-counter parts sales, and purely do-it-yourself labor.

Segmentation Overview

- By Implementation Type

- New Construction

- Retrofit Buildings

- By Service Type

- Installation and Replacement Services

- Maintenance and Repair Services

- Energy-Efficiency and Retrofit Services

- HVAC Controls Upgrade and Integration

- Consulting and Other Services

- By System Type

- Heating Services

- Cooling Services

- Ventilation and IAQ Services

- Integrated Building-Management Services

- By End User

- Residential

- Commercial

- Industrial

- By Application

- Data Centers

- Healthcare Facilities

- Educational Institutions

- Hospitality and Leisure

- Retail Spaces

- Government and Public Buildings

- Other Applications

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Mexico

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Benelux

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Rest of Asia Pacific

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research is used to define the basic market boundaries, the demand drivers, and initial values for key inputs before any forecasting is attempted. We leaned on public sources such as US Census Bureau construction spending and building permits, Bureau of Labor Statistics wage and employment series for HVAC mechanics and installers, EIA data on heating fuels and electricity use, EPA materials on refrigerants and compliance direction, and DOE efficiency standards and program updates.

To tighten assumptions, we also reviewed company filings and investor presentations of major service networks, trade association publications, and reputable press coverage of pricing, labor availability, and replacement cycles. Select paid database subscriptions supported checks on company financials and on shipment-level import and export signals for HVAC components, which helped validate activity levels across the service ecosystem. These examples are not exhaustive, and many other public and paid sources were also referenced for data collection, validation, and clarification during the research process.

Primary Interviews and Surveys

Primary work was completed through expert interviews and structured surveys with contractors, facility managers, building owners, distributors with service arms, and technical specialists who track installation and service demand. We used these discussions to confirm typical ticket sizes, the mix of maintenance versus emergency work, seasonal patterns, and how regulation and efficiency upgrades affect replacement and retrofit activity across the United States.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 16% | |

| Mid tier: 51% | Functional/Unit leaders: 27% | |

| Smaller Players: 22% | Managers: 57% |

Market-Sizing & Forecasting

Sizing is built using a top-down approach where construction and building activity signals are converted into a service demand pool, then realistic service attach rates and price points are applied to the work performed. The outputs are then pressure-tested with selective bottom-up approximations, such as rolling up sampled contractor revenues, using channel checks on service call volumes, and validating implied spend per building cohort, before final totals are locked.

Key inputs that shape the model include housing starts and commercial floor space additions, the aging installed base of HVAC systems and expected replacement cycles, seasonal cooling and heating degree days, technician wage inflation and labor availability, and the share of work shifting toward energy-efficiency retrofits and connected controls (which often increases service content). Forecasts were derived using scenario analysis supported by expert expectations on construction momentum, pricing progression, and regulatory compliance pacing, and then converted into annual values in USD. Where local bottom-up signals were thin, gaps were handled by using state-level building stock proxies and normalized service intensity, followed by interview-based adjustment to avoid overfitting.

Data Validation & Update Cycle

Findings are checked through triangulation across independent signals, including construction spending trends, workforce and wage series, and implied service intensity versus the installed equipment base. When an outlier shows up, assumptions are re-checked, and targeted follow-up calls are triggered to confirm whether the change is real or tied to data timing.

Before publication, the model goes through multi-step analyst review with variance checks across historical years, unit economics, and regional reasonableness, and then a final sign-off pass is completed. Reports are refreshed annually, and interim updates are made when material events occur, such as policy changes impacting refrigerants, sharp labor cost shifts, or meaningful construction cycle turns. Right before delivery, a fresh review is completed so clients receive the latest updated view.

Mordor Intelligence's United States Hvac Services Market Size Compared With Other Published Estimates

Published market sizes for US HVAC services can look far apart, even when they are describing the same general activity, because firms make different calls on what counts as services revenue and how fast pricing and volumes move year to year.

The benchmark table shows a wide spread, and in Mordor Intelligence's model the value reflects service revenue earned inside the United States for design, installation labor, retrofit, preventive maintenance, and emergency repair, while excluding brand-new equipment sales and over-the-counter parts, which some estimates appear to blend into a broader total.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 17.93 B (2025) | |

| Industry Research Publisher A | USD 28.20 B (2025) | Often presented with wider service definitions, and may capture equipment-plus-service bundles or broader contract categories that lift the counted revenue pool versus a services-only boundary. |

| Market Analytics Firm B | USD 25.60 B (2024) | Uses a different base year and can apply faster early-year growth assumptions, and the public scope notes do not clearly state exclusions for new equipment and parts, which can inflate the measured total. |

Overall, the differences mostly come down to scope edges, the base year chosen, and how price progression is applied to installation and maintenance work. By tying inputs to observable building activity, workforce cost signals, and interview-validated service intensity, our estimate stays traceable to clear demand drivers and repeatable calculation steps.

Key Questions Answered in the Report

How large is the US HVAC services market today?

The market stood at USD 18.98 billion in 2026 and is on track to reach USD 25.35 billion by 2031.

What CAGR is expected for US HVAC services through 2031?

The forecast CAGR is 5.90% over the 2026-2031 period.

Which segment of US HVAC services is growing fastest?

Energy-efficiency and retrofit services lead with a 7.03% CAGR as owners prioritize performance optimization.

Why are data centers important for HVAC service demand?

AI workloads drive rack densities above 50 kW, requiring precision cooling and multi-year service contracts with strict uptime clauses.

What is the main challenge facing HVAC service providers?

A skilled-labor shortage that lifts technician wages and squeezes margins is the most immediate hurdle.

How concentrated is the competitive landscape?

The top five firms account for about 35% of revenue, indicating moderate concentration with ample room for regional specialists.

Page last updated on: