North America LED Module Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.96 Billion |

| Market Size (2026) | USD 2.22 Billion |

| Market Size (2031) | USD 4.69 Billion |

| Growth Rate (2026 - 2031) | 16.09% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America LED Module Market Analysis by Mordor Intelligence

The North America LED module market size is projected to expand from USD 1.96 billion in 2025 and USD 2.22 billion in 2026 to USD 4.69 billion by 2031, registering a CAGR of 16.09% between 2026 to 2031. Rapid utility rebate realignments, stricter energy-code thresholds, and semiconductor tariff escalations are reshaping procurement priorities across commercial lighting, automotive platforms, and specialty verticals. Hardware innovation is shifting toward integrated controls, spectral tuning, and data telemetry, features that raise average selling prices while compressing replacement cycles. Vertically integrated suppliers with North American manufacturing footprints are benefiting from geopolitical substrate pricing swings and DesignLights Consortium (DLC) performance floors, whereas import-dependent assemblers face longer lead-time volatility and margin pressure. Automotive adoption of adaptive driving beam headlamps and mini-LED backlight architectures in premium televisions is widening the addressable opportunity for high-power and flexible modules.

Key Report Takeaways

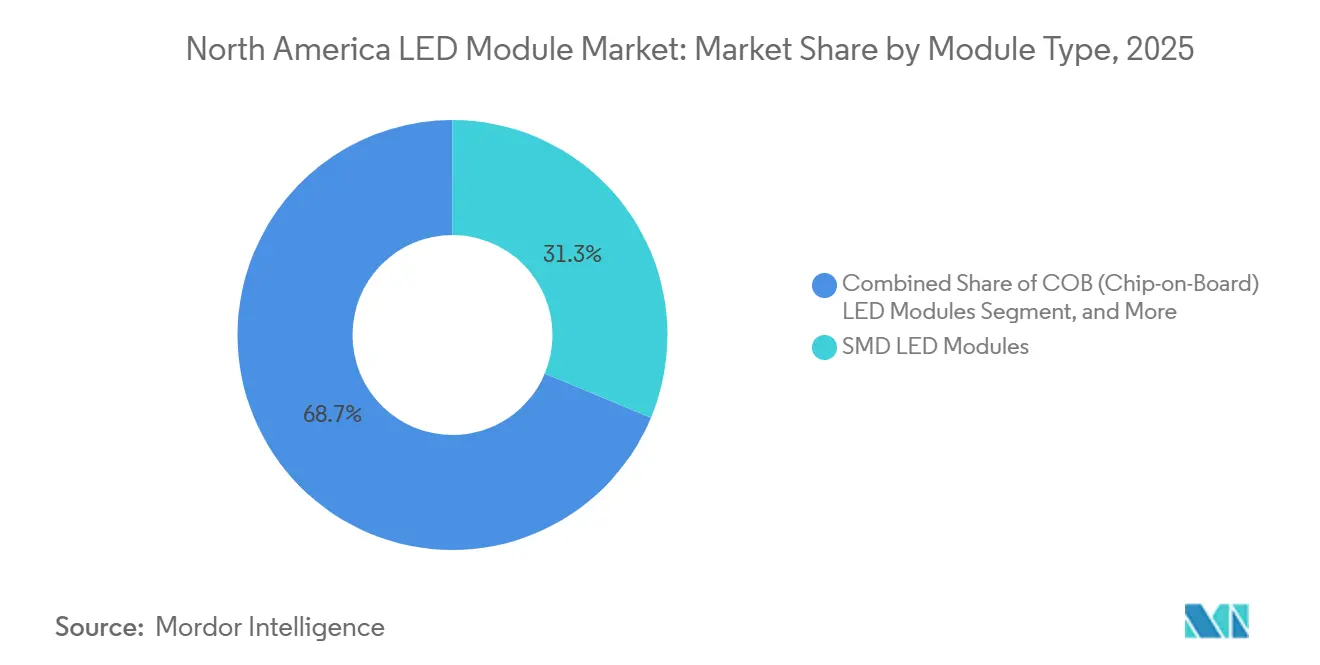

- By module type, SMD LED modules led with 31.29% of the North America LED module market share in 2025, while LED backlight modules are forecast to grow at a 16.57% CAGR through 2031.

- By application, general lighting captured 44.68% of the North America LED module market size in 2025, and display and backlighting are projected to expand at a 16.78% CAGR to 2031.

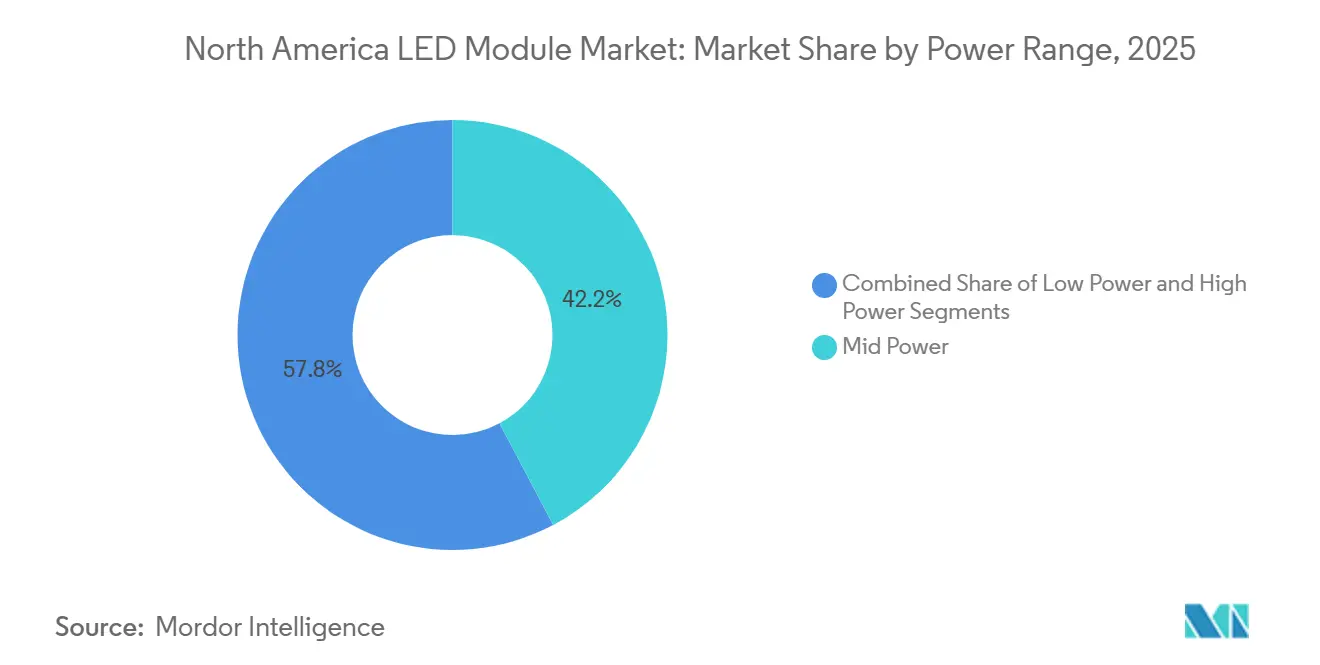

- By power range, the mid-power segment held 42.23% of the North America LED module market share in 2025, whereas high-power modules are advancing at a 16.96% CAGR over 2026-2031.

- By form factor, rigid modules accounted for 82.18% of revenue in 2025, and flexible modules are on track for a 16.73% CAGR through the forecast window.

- By geography, the United States commanded 87.47% of 2025 regional sales, while Canada is the fastest-growing market at a 16.91% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America LED Module Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Expanding Utility Rebates Accelerating LED Retrofit Projects | +3.2% | United States and Canada, concentrated in California, New York, Oregon, Ontario | Short term (≤ 2 years) |

| Surge in Ultraviolet-C LED Modules for Disinfection Systems | +2.8% | United States with secondary uptake in Canadian healthcare and water facilities | Medium term (2-4 years) |

| Automaker Shift to LED Headlamps Across Mid-range Vehicle Lines | +2.5% | United States and Mexico, led by Detroit Three and transplant OEMs | Medium term (2-4 years) |

| IoT-Enabled Smart-Building Codes Mandating Connected Luminaires | +2.3% | United States, especially California Title 24 and New York City codes | Medium term (2-4 years) |

| Rapid Growth of Indoor Vertical-Farming Driving Horticulture Lighting | +1.9% | Urban centers across United States and Canada | Long term (≥ 4 years) |

| Next-Gen Mini- and Micro-LED Backlights in Consumer Displays | +2.1% | Region-wide demand from premium television and automotive OEMs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in Ultraviolet-C LED Modules for Disinfection Systems

The U.S. Environmental Protection Agency’s 2024 guidance recognized UV-C LEDs for 4-log virus inactivation in water treatment, removing a longstanding regulatory hurdle. As a result, municipalities in Arizona, Florida, and British Columbia issued tenders in 2025 that specify mercury-free UV-C arrays, displacing low-pressure mercury lamps in new installations. LG Innotek and Seoul Viosys each launched 100 milliwatt single-chip emitters capable of 10,000-hour L70 performance, enabling compact point-of-use purifiers. Although radiant-flux efficacy remains below 5%, rapid ASP declines and form-factor flexibility have attracted venture funding into U.S. start-ups focusing on HVAC airstream sanitization. Suppliers with verified LM-80 test data and NSF-61 listings command price premiums above visible-spectrum products, lifting overall margin mix for the North America LED module market.[1]U.S. Environmental Protection Agency, “Ultraviolet Disinfection Guidance Manual,” epa.gov

Automaker Shift to LED Headlamps Across Mid-range Vehicle Lines

National Highway Traffic Safety Administration approval of adaptive driving beams in 2024 unlocked LED matrix headlamp deployments across mid-priced sedans and crossovers. Magna’s FlecsForm mini-LED module, introduced in 2025, reduces package height by 15 millimeters, enabling automakers to restyle front fascias without compromising pedestrian-impact compliance. Concurrently, Tianma and Innolux showcased mini-LED head-up displays hitting 12,000 nits, a performance level requiring high-power backlight boards with micro-optics for glare control. The migration downstream from luxury trims expands annual unit demand for automotive-grade modules rated to survive 125 °C junction temperatures and AEC-Q102 shock standards. Flexible interior ambient strips using RGBW arrays are now specified in pickup trucks retailing below USD 40,000, further widening volume opportunities.[2]National Highway Traffic Safety Administration, “Final Rule on Adaptive Driving Beams,” nhtsa.dot.gov

IoT-Enabled Smart-Building Codes Mandating Connected Luminaires

California Title 24 Part 6, effective January 2025, and New York City’s 2025 Energy Conservation Code require networked controls, automatic daylight dimming, and demand-response readiness. DLC V6.0 aligns rebate eligibility with the Connectivity Standards Alliance’s Matter protocol categories, effectively making connectivity a baseline feature. Module makers are embedding Bluetooth mesh or DALI-2 drivers and shipping Zhaga Book 20 receptacles so building owners can hot-swap sensors without rewiring. The codes elevate controls-ready luminaires from premium to standard specification in new construction, and retrofit rebate tiers demand continuous dimming for existing facilities. Vendors that can certify multi-protocol interoperability are capturing higher attach rates and longer service contracts.[3]California Energy Commission, “Title 24 Part 6 2025 Standards,” cec.ca.gov

Expanding Utility Rebates Accelerating LED Retrofit Projects

Utility programs are shifting from first-cycle incandescent conversions toward LED-to-LED upgrades that bundle networked controls and higher efficacy benchmarks. California investor-owned utilities introduced tiered incentives in 2025 that reimburse USD 25-75 per fixture for modules exceeding 130 lumens per watt, a move mirrored by Ontario’s Save on Energy framework. Rebates now hinge on DLC V6.0 Premium listing, compelling suppliers to integrate continuous dimming and spectral files. The higher payout rates shorten payback periods to fewer than 18 months for many commercial retrofits, driving a second replacement wave across offices and warehouses. Manufacturers that can ship field-upgradeable drivers and Zhaga-book interfaces are winning design specifications over lowest-cost commodity boards.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Price Volatility of GaN and Sapphire Substrates | -1.8% | Region-wide exposure to Asia-Pacific wafer supply chains | Short term (≤ 2 years) |

| Thermal Management Challenges in High-Power Modules | -1.3% | United States and Canada outdoor and industrial luminaires | Medium term (2-4 years) |

| Supply-Chain Concentration in Asia-Pacific Creating Lead-Time Risks | -1.1% | Dependence on Taiwanese, South Korean, and Chinese chip fabs | Medium term (2-4 years) |

| Complexity of North American UL and DLC Certification Pathways | -0.9% | Barriers for new entrants seeking U.S. and Canadian access | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Thermal Management Challenges in High-Power Modules

Outdoor area lighting and industrial high-bays now exceed 30 watts per board, intensifying junction temperatures beyond 115 °C under summer peak loads. DLC V6.0 demands L70 to 50,000 hours and, for the Premium tier, L90 to 36,000 hours, forcing suppliers to adopt liquid-cooling plates or phase-change housings. Getian’s 2025 liquid-cooled modules dissipate 100-watt loads yet raise fixture BOM by 30%. Passive alternatives like CooliBlade phase-change fins lower junctions but enlarge luminaire envelopes, clashing with slim-line architectural aesthetics. Without robust thermal models and on-board sensors, warranty claims escalate, eroding brand equity.

Price Volatility of GaN and Sapphire Substrates

China’s 2024 export licensing on gallium and germanium, combined with the United States tariff hikes from 25% to 50% on semiconductor imports in 2025, pushed 6-inch GaN-on-sapphire wafer prices to USD 400 by late 2025. The North America LED module market sources more than 80% of epi-ready wafers from Asia, leaving assemblers exposed to currency swings and shipping delays. Several second-tier suppliers explored GaN-on-silicon, yet lower internal quantum efficiency jeopardized DLC Premium listing. Firms with long-term contracts or equity stakes in domestic crystal growers buffered cost spikes, but smaller players faced 6-week quote validity, disrupting bid accuracy for utility-rebated projects.[4]CooliBlade, “AURORA Passive-Cooling LED Solution,” cooliblade.com

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Module Type: SMD Modules Anchor Volume, Backlight Boards Accelerate

SMD boards captured 31.29% of the North America LED module market share in 2025, supported by mass-manufactured troffers, downlights, and strip fixtures. SMD’s low profile and reflow-solder economy align with contract manufacturing across Mexico and the southern United States. In contrast, LED backlight modules are forecast to post a 16.57% CAGR, fueled by mini-LED and micro-LED panels that pack more than 200,000 dimming zones. The North America LED module market size tied to premium television backlights is expanding as panel makers localize assembly to sidestep semiconductor tariffs. Two hundred square-inch automotive displays, each requiring upwards of 5,000 mini-LEDs, are pulling specialty suppliers into long-term vehicle platforms.

Contention between COB and advanced SMD continues: COB downlights reach 155 lumens per watt, but high-density SMD arrays now pass 181 lumens per watt, leveraging flip-chip packages. Flexible strips built on copper-polyimide laminates occupy a niche for curved dashboards and retail accent lighting, commanding ASPs 2-3 times those of rigid FR-4 boards. DLC listing pathways for modular products make it easier for luminaire brands to qualify families built around common SMD engines, reinforcing SMD’s incumbent momentum while specialty backlight boards deliver the highest growth delta.

By Application: General Lighting Dominates, Display and Backlighting Surges

General lighting maintained 44.68% of 2025 revenue, reflecting decades-deep retrofit activity and code compliance in offices, warehouses, and streetscapes. The segment benefits from standardized utility incentives and bundled sensor packages that streamline payback modeling. Yet display and backlighting is projected to expand at 16.78% CAGR, a pace nearly 2 percentage points above the overall North America LED module market. Television OEMs are upgrading 65-inch and larger sets to mini-LED, boosting individual panel demand to 10,000-plus emitters. Automotive cockpits adopt curved mini-LED HUDs rated at 12,000 nits, tightening tolerances on chromaticity and uniformity.

Horticulture, UV, and automotive adaptive systems round out smaller, high-margin slices. Hospitals specify UV-C downlights for occupied-room disinfection cycles, while vertical farmers invest in red-blue-far-red spectra tuned to lettuce and micro-greens. These specialized modules deliver gross margins north of 35%, double those of commodity troffer engines, a dynamic that helps offset pricing erosion in the general lighting core.

By Power Range: Mid-Power Holds Share, High-Power Gains Pace

Mid-power boards between 5 watts and 30 watts retained 42.23% North America LED module market share in 2025, serving A-lamps, retrofit kits, and recessed cans. ASP pressure intensified as low-cost imports undercut domestic assembly by 15%, prompting regional players to bundle smart sensors to sustain gross margin. High-power modules above 30 watts are forecast to scale at a 16.96% CAGR to 2031, propelled by sports lighting projects and roadway conversions seeking 150-plus lumens per watt. Demand for high voltage, step-down drivers, and active monitoring circuits differentiates suppliers with deep power-electronics stacks.

Low-power accents below 5 watts occupy decorative niches but generate brand-building halo effects through full-RGB or tunable white customization. The upshot is a bifurcated value chain: mid-power commoditizes around cost benchmarks, while high-power and smart-low-power tiers maintain defensible pricing through performance or control sophistication.

By Form Factor: Rigid Boards Prevail, Flexible Strips Advance

Rigid modules commanded 82.18% of 2025 spend, an outcome of mature FR-4 process control, stiffeners that double as heat spreaders, and large-volume contract manufacturing lines. Certification familiarity with UL 8750 and DLC standard categories accelerates time-to-market for rigid-based luminaires. Conversely, flexible modules are set for a 16.73% CAGR on the back of curved architectural coves, automotive interior splash lighting, and conformable retail signage.

Adoption hurdles include higher solder-joint fatigue risk and limited automation for pick-and-place on flex substrates, factors that currently inflate cost. Nonetheless, Magna’s curved mini-LED headlamp substrate and hospitality demand for ribbon-style RGBW strips are validating scale economics. As connectivity ecosystems migrate toward distributed DC or Power-over-Ethernet, thin flexible engines with onboard DC-DC regulation may eclipse rigid retrofit boards in future generations.

Geography Analysis

The United States held 87.47% of the North America LED module market share during 2025, powered by USD 200 million in commercial lighting incentives from California utilities and aggressive Title 24 compliance enforcement. Federal infrastructure spending is replacing 500,000 high-intensity discharge streetlights across Midwestern and Southeastern municipalities, embedding wireless controls and driving field-replaceable module demand. Semiconductor tariffs sparked reshoring moves, with multiple tier-one luminaire brands qualifying U.S. and Mexican contract manufacturers to hedge import duties.

Canada, although smaller in absolute dollars, is pacing the regional growth leaderboard with a 16.91% CAGR forecast through 2031. Provincial frameworks such as Ontario’s Green Button mandate real-time energy data access, encouraging building owners to invest in connected luminaires. Signify’s 2025 acquisition of Calgary-based Nemalux expanded hazardous-location portfolios aimed at Canadian oil, gas, and mining operators that require explosion-proof ratings down to −50 °C ambient.

Mexico remains the smallest slice but is strategically significant for automotive OEM nearshoring. LED headlamp and infotainment display module lines are expanding in Guanajuato and Nuevo León to feed North American vehicle assembly, shortening logistics chains and circumventing tariff layers. Northbound module flows enjoy United States-Mexico-Canada Agreement duty waivers, positioning Mexican fabs as cost-competitive alternates to Asian imports.

Competitive Landscape

Market concentration skews toward established fixture brands yet remains below oligopoly levels. Acuity Brands, Signify, and Eaton leverage DLC-qualified portfolios and distribution through electrical wholesalers, capturing large project specifications. Asian chip specialists, Samsung, LG Innotek, Nichia, Seoul Semiconductor, compete on die-level efficacy and cost, often partnering with North American board assemblers to co-list products under DLC.

Acuity’s May 2025 purchase of M3 Innovation bolstered its sports-lighting and high-power module IP, while Signify’s Canadian acquisition signals a strategic pivot toward harsh-environment verticals. Cree Lighting’s February 2026 contract manufacturing pact illustrated capacity constraints among mid-tier suppliers and a shift toward asset-light engineering models.

Disruptors are entering with Power-over-Ethernet boards that eliminate AC-DC drivers and with spectral-tuning engines for horticulture and circadian health. DLC V6.0’s alternate-component clauses may accelerate commoditization, but premium pathways tied to 100,000-hour driver life and connected-controls categories protect margin in the upper tiers. Suppliers must choose between high-volume, low-margin general-lighting boards and differentiated specialty modules that command price premiums but require deeper R&D and multi-protocol certifications.

North America LED Module Industry Leaders

Signify N.V.

Cree, Inc.

Lumileds Holding B.V.

Samsung Electronics Co., Ltd.

Osram GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Lumentum acquired a 240,000 square-foot Greensboro, North Carolina, plant from Qorvo to build indium-phosphide laser devices for AI data centers, with a mid-2028 production ramp.

- February 2026: Cree Lighting signed a long-term manufacturing agreement with a U.S. specialist in harsh-environment fixtures, aiming to clear order backlogs in the next quarter.

- February 2026: Cree LED launched OptiLamp LEDs, embedding sensors and adaptive dimming for industrial and commercial sites.

- February 2026: Omnilight relocated to a 20,000 square-foot Niles, Illinois facility, tripling capacity and upgrading fabrication lines.

North America LED Module Market Report Scope

An LED Module is a pre-assembled, integrated lighting component consisting of one or more light-emitting diodes (LEDs) mounted on a printed circuit board or substrate, along with essential electrical and thermal management elements such as current-limiting circuitry and heat-dissipation structures, designed to operate as a functional light source when incorporated into a luminaire and powered by an appropriate electrical supply.

The North America LED Module Market Report is Segmented by Module Type (COB, SMD, Linear, Backlight, High-Power, and Other Module Types), Application (General Lighting, Automotive, Display and Backlighting, Signage, and Other Applications), Power Range (Low, Mid, and High), and Form Factor (Rigid, and Flexible). The Market Forecasts are Provided in Terms of Value (USD).

| COB LED Modules |

| SMD LED Modules |

| Linear LED Modules |

| LED Backlight Modules |

| High-Power LED Modules |

| Others, Module Type (Flexible Modules, Mini Modules, Custom Assemblies) |

| General Lighting | Residential |

| Commercial | |

| Industrial | |

| Automotive Lighting | |

| Display and Backlighting | |

| Signage and Advertising | |

| Others, Application (Architectural, Horticulture, UV, Specialty Lighting) |

| Low Power (less than or equal to 5 W) |

| Mid Power (greater than 5 W to less than or equal to 30 W) |

| High Power (greater than 30 W) |

| Rigid LED Modules |

| Flexible LED Modules |

| United States |

| Canada |

| Mexico |

| By Module Type | COB LED Modules | |

| SMD LED Modules | ||

| Linear LED Modules | ||

| LED Backlight Modules | ||

| High-Power LED Modules | ||

| Others, Module Type (Flexible Modules, Mini Modules, Custom Assemblies) | ||

| By Application | General Lighting | Residential |

| Commercial | ||

| Industrial | ||

| Automotive Lighting | ||

| Display and Backlighting | ||

| Signage and Advertising | ||

| Others, Application (Architectural, Horticulture, UV, Specialty Lighting) | ||

| By Power Range | Low Power (less than or equal to 5 W) | |

| Mid Power (greater than 5 W to less than or equal to 30 W) | ||

| High Power (greater than 30 W) | ||

| By Form Factor | Rigid LED Modules | |

| Flexible LED Modules | ||

| By Geography | United States | |

| Canada | ||

| Mexico | ||

Key Questions Answered in the Report

How large will North America LED module revenue be by 2031?

It is forecast to reach USD 4.69 billion, expanding at a 16.09% CAGR from 2026 to 2031.

Which application is growing the fastest?

Display and backlighting boards, led by mini-LED and micro-LED adoption, are projected to grow at 16.78% CAGR.

Why are flexible LED modules gaining traction?

Curved automotive interiors, architectural coves, and conformable retail signage require bendable substrates that rigid PCBs cannot support.

How are tariffs affecting suppliers?

Semiconductor duties rising to 50% in 2025 incentivized local assembly and raised wafer costs, pressuring import-reliant manufacturers.

Page last updated on: