COB LED Module Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.85 Billion |

| Market Size (2031) | USD 4.02 Billion |

| Growth Rate (2026 - 2031) | 16.79% CAGR |

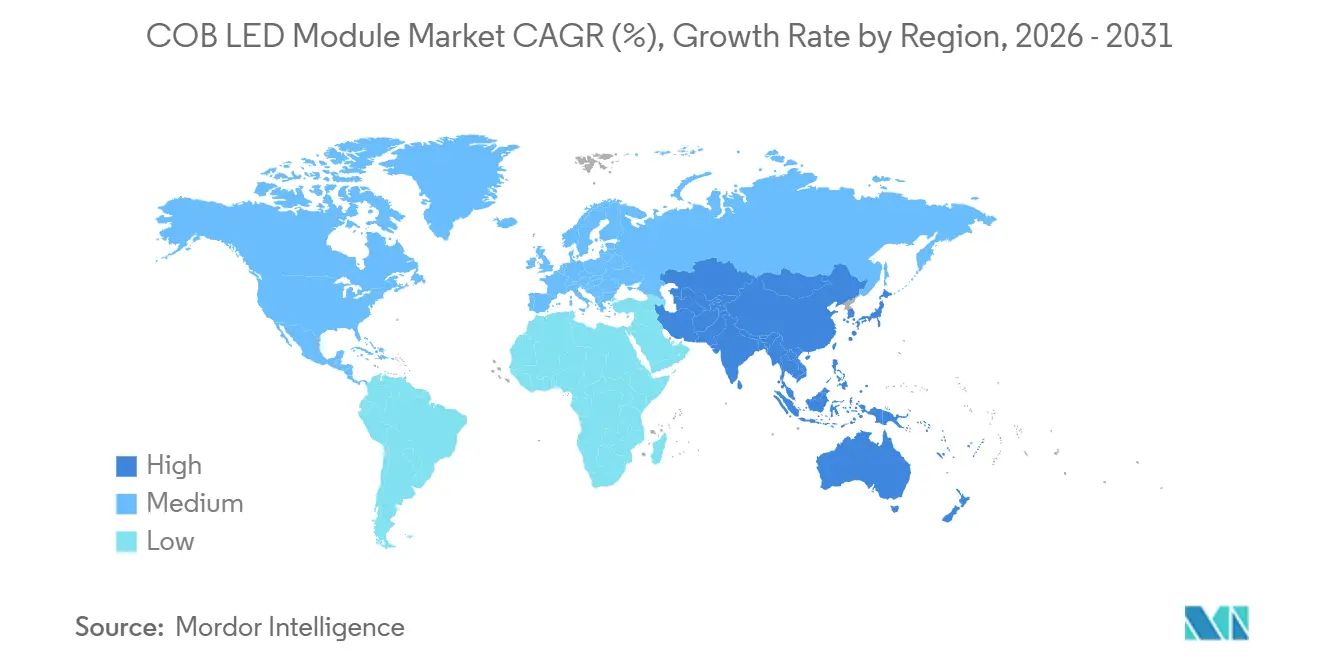

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

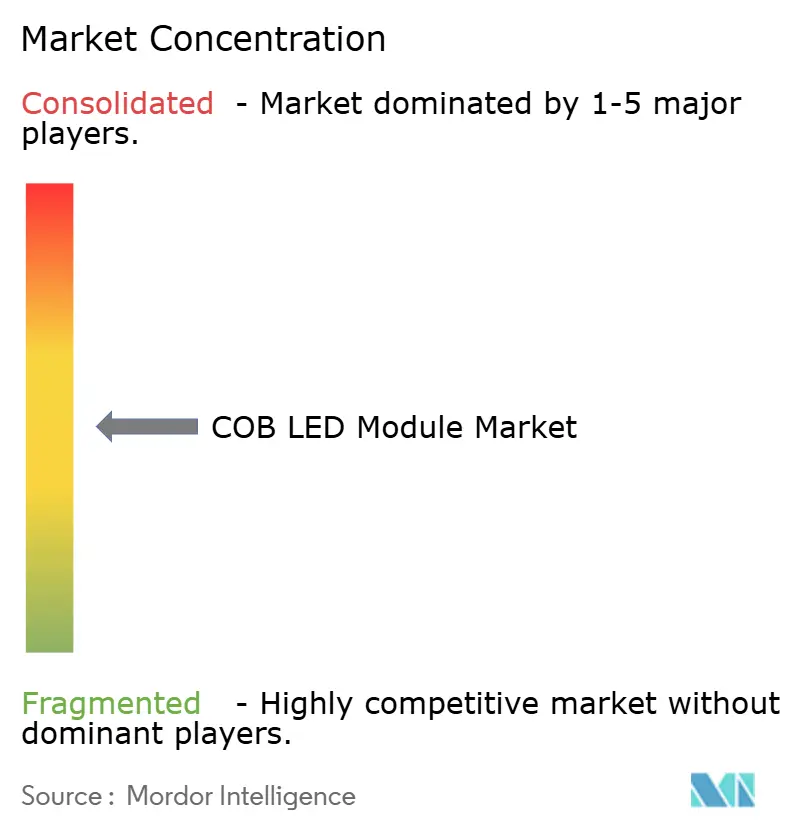

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

COB LED Module Market Analysis by Mordor Intelligence

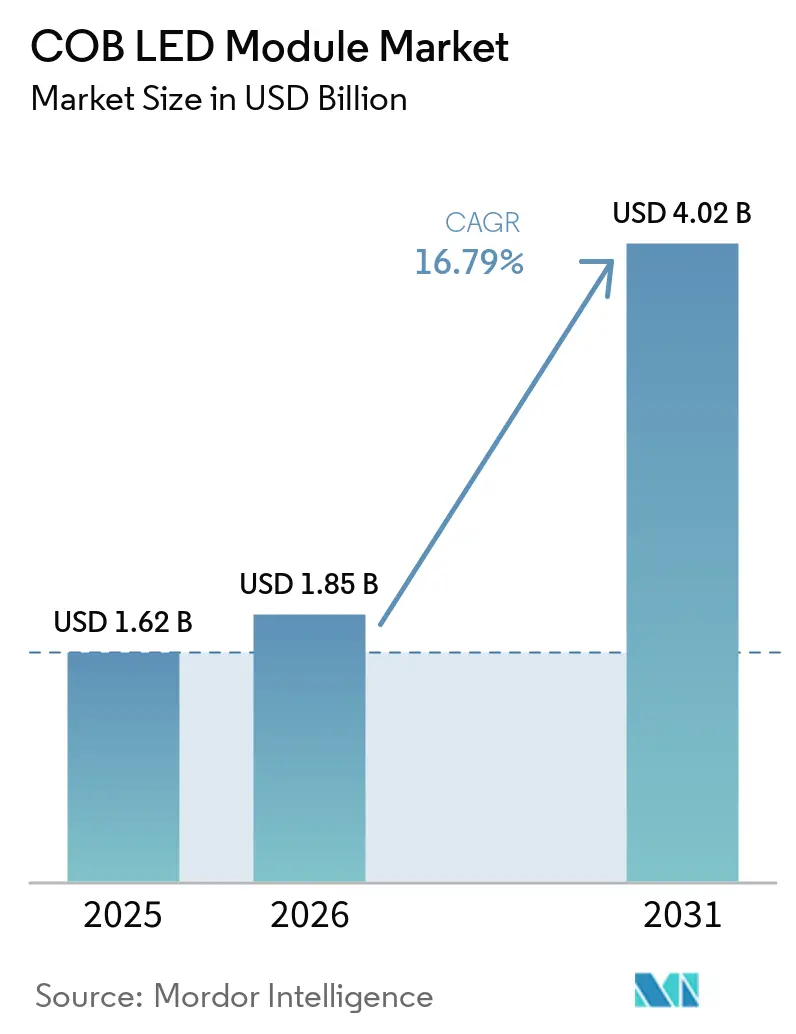

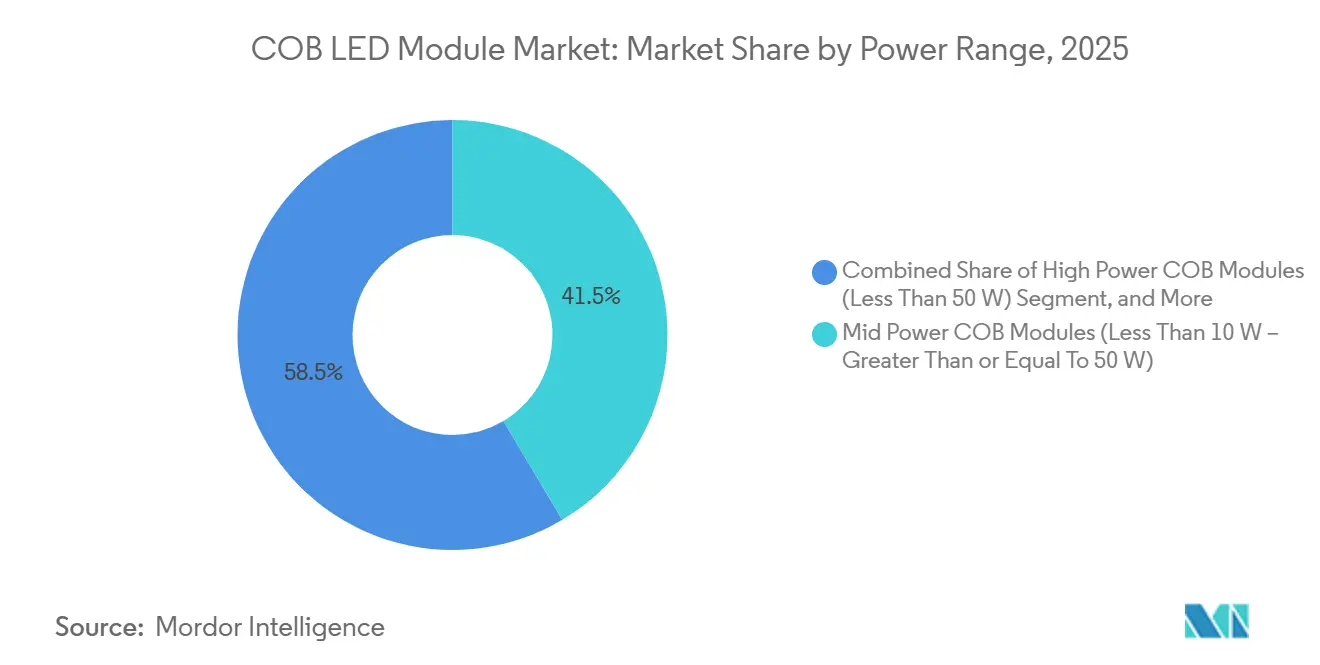

The COB LED module market size is projected to be USD 1.62 billion in 2025, USD 1.85 billion in 2026, and reach USD 4.02 billion by 2031, growing at a CAGR of 16.79% from 2026 to 2031. Continued regulatory pressure for higher efficacy, the electrification of passenger vehicles, and the shift to mini-LED backlighting keep demand on an upward trajectory, while integrated, high-density packaging cements the value proposition over discrete alternatives. Mid-power modules between 10 W and 50 W commanded a 41.47% COB LED module market share in 2025, but high-power devices above 50 W will expand faster because modern stadium retrofits and EV headlamp platforms require sustained luminance beyond 2,000 nits with controlled thermal droop. Asia-Pacific, already home to a significant share of global revenue in 2025, benefits from localized supply chains that reduce lead times and costs, although persistent price erosion caps margins.

Key Report Takeaways

- By power range, mid-power devices held 41.47% of the COB LED module market share in 2025. High-power modules above 50 W are forecast to grow at a 17.73% CAGR through 2031, the fastest among power ranges.

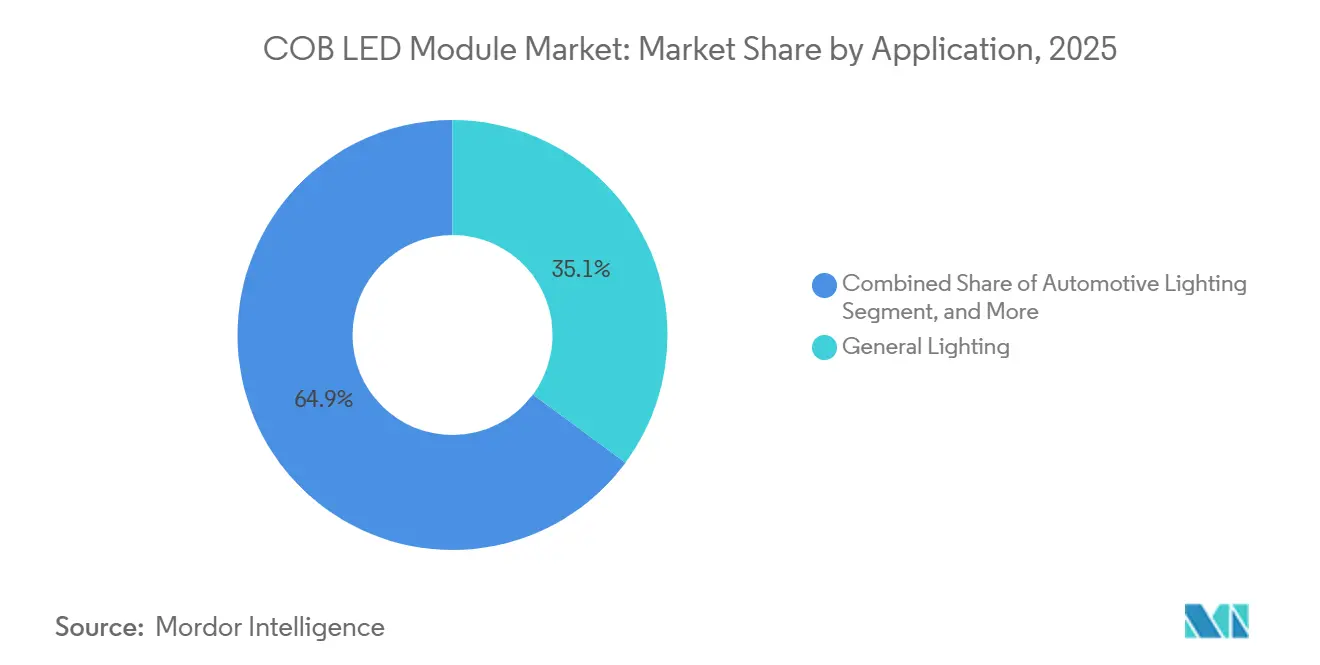

- By application, general lighting held 35.12% of the COB LED module market share in 2025. Architectural and outdoor are forecast to grow at a 17.73% CAGR through 2031, the fastest among the application segments.

- Asia-Pacific captured 66.73% of revenue in 2025 and is projected to remain the largest geography, with a 17.95% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global COB LED Module Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Stringent Energy-Efficiency Regulations Worldwide | +3.2% | Global, strongest in Europe and North America | Medium term (2-4 years) |

| Rapid Decline in USD/Lumen for Mid-Power Modules | +2.8% | Asia-Pacific core, spillover to Middle East and Africa | Short term (≤ 2 years) |

| Mass Adoption of Smart, Connected Lighting Ecosystems | +2.5% | North America and Europe lead, Asia-Pacific accelerating | Medium term (2-4 years) |

| OEM Shift Toward Integrated Headlamp Architectures in EVs | +2.1% | China, Europe, North America | Long term (≥ 4 years) |

| Mini-LED Backlighting Boom in Premium Displays | +1.9% | Asia-Pacific manufacturing, global demand | Short term (≤ 2 years) |

| Urban Stadium and Arena Renovations Demanding High-Power COB | +1.4% | North America and Europe, emerging Middle East | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Energy-Efficiency Regulations Worldwide

Regulatory tightening in the EU under Ecodesign Regulation 2019/2020 and parallel rules in the United States pushes suppliers to raise module efficacy, extend lumen maintenance, and curb flicker. COB products classified as light sources must secure EPREL registration before entering European channels, a requirement that adds compliance costs but also limits the entry of smaller, unaccredited fabricators. From December 2026, the Ecodesign for Sustainable Products Regulation adds circularity mandates that reward socketable, serviceable designs aligned with Zhaga Book 12 holders. The burden of third-party testing, IEC 62031 conformity, and photobiological safety accelerates consolidation among manufacturers with accredited labs capable of issuing declarations of conformity.[1]European Commission, “Regulation (EU) 2019/2020 Laying Down Ecodesign Requirements,” europa.eu

Rapid Decline in USD/Lumen for Mid-Power Modules

Between 2022 and 2025, prices for mid-power COB LED modules dropped significantly. This price drop was largely driven by Chinese suppliers, who capitalized on their domestic MOCVD capacity. However, this deflationary trend led to a significant halving of packaging houses' gross margins. By early 2026, in response to surging precious-metal prices, over 50 companies spanning the value chain implemented price increases to recoup lost margins. This price rebound has shifted the competitive landscape, moving the focus from mere pricing to differentiation. Key differentiators now include color stability, high-CRI phosphors, and integrated driver-on-board features, all of which justify elevated average selling prices. Suppliers from the West and Japan, armed with proprietary phosphor mixes, stand to gain the most from this evolving landscape, as their offerings emphasize value beyond just raw lumens.

OEM Shift Toward Integrated Headlamp Architectures in EVs

Battery-electric vehicles favor compact, multifunction headlamp modules that consolidate daytime running, turn indicator, and high-beam functions in a single optical surface. Forvia Hella’s headlamps on the LUXEED R7 combine position and turn functions via dual-focus COB emitters, reducing parts and wiring while delivering beam widths above 30 m. Field data from 7,086 BEV headlamps confirm lower thermal stress than in internal-combustion vehicles, enabling smaller heatsinks and denser layouts that increase demand for high-flux COB arrays.[2]Forvia Hella, “Next-Generation Integrated Headlamp Launched on LUXEED R7,” hella.com

Mass Adoption of Smart, Connected Lighting Ecosystems

Lighting now acts as a sensor node within commercial buildings, leveraging Matter and Bluetooth mesh to orchestrate daylight harvesting, occupancy sensing, and circadian tuning. Bridgelux’s DriveLux engines embed COB LEDs with on-board drivers and optional wireless control, enabling plug-and-play upgrades that curtail wiring labor. Protocols such as ISELED, which can address more than 4,000 RGB LEDs on a single differential pair, underline how firmware and analytics create new value around the luminaire. COB suppliers that provide firmware hooks, diagnostic data, and secure update paths stand to gain preferred status with fixture OEMs.[3]Bridgelux, “DriveLux Integrated Light Engines,” bridgelux.com

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Price Erosion from Chinese Low-Cost Capacity | -2.1% | Global, sharpest in Asia-Pacific commodity tiers | Short term (≤ 2 years) |

| High Thermal-Management Cost for Less Than 50 W Modules | -1.6% | Industrial and outdoor high-power projects worldwide | Medium term (2-4 years) |

| Competition from Chip-Scale and Flip-Chip Packages | -1.3% | Automotive and display hubs in Asia-Pacific, North America | Medium term (2-4 years) |

| Supply-Chain Volatility in Phosphor and Substrate Materials | -1.1% | Global, supply clustered in China and Japan | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Price Erosion from Chinese Low-Cost Capacity

Chinese chipmakers and packagers are ramping up capacity, outpacing domestic demand growth. This imbalance has led to a consistent supply surplus, pushing mid-power average selling prices (ASPs) downward. Mainstream Chip-on-Board (COB) prices declined significantly, prompting some marginal producers in Taiwan and Southeast Asia to either shut down production lines or pivot to niche applications. The average gross margin for publicly listed Chinese LED companies dipped, prompting the first wave of coordinated price increase notifications. While efforts to restore value are underway, the market for commodity luminaires in the Middle East and Africa remains price-sensitive. As a result, many foreign brands find themselves relegated to premium sub-segments, where differentiation is more pronounced.

High Thermal-Management Cost for Less Than 50 W Modules

To maintain the L70 lifetime, junction temperatures for modules exceeding 50 W must remain below 85 °C. However, standard passive aluminum heat sinks often fall short. Ceramic substrates such as aluminum nitride and direct-bond copper offer superior thermal conductivity, but they can significantly increase module costs. Vapor chambers and liquid micro-jets can withstand industrial stress tests; however, their use increases the form factor and introduces moving parts. This addition can undermine the ruggedness advantage typically associated with Chip-on-Board (COB) solutions. Furthermore, the bill of materials, which typically accounts for a significant portion of the total module cost, can deter adoption in budget-conscious street-lighting tenders. As a result, some buyers are leaning towards distributed arrays of low-power LEDs, which can dissipate heat over larger surfaces.[4]H.Wang et al., “Thermal Performance of Micro-Jet Cooling for High-Power LEDs,” Applied Thermal Engineering, journals.elsevier.com

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Power Range: Momentum Shifts to High-Power Devices

High-power modules above 50 W are on track to expand at 17.73% CAGR during 2026-2031, outstripping the broader COB LED module market. Single-source packages delivering more than 5,000 lm streamline optics and wiring in stadium floodlights, industrial high bays, and outdoor area fixtures. Bridgelux’s Generation 2 F90 family illustrates the trend, offering 8,000 lm from a 40 W emitter while preserving Δu'v' color shift below 0.004 across a 60 °C temperature swing. Meanwhile, the COB LED module market for mid-power products remains large, accounting for 41.47% of the market in 2025 across commercial downlights and architectural accents. Low-power modules under 10 W cluster into display backlighting, cove lighting, and decorative strips, but face rising pressure from chip-scale packages that achieve equivalent flux in slimmer footprints.

The purchasing calculus diverges along this power axis. Buyers of high-power emitters prize lifetime and thermal headroom, tolerating premium ceramic substrates and copper coins to avoid premature lumen depreciation. Utilities and stadium owners view the higher acquisition cost as justified by reduced fixture counts and minimal maintenance over 50,000 h duty cycles. Conversely, the mid-power tier competes on dollars per lumen, with Chinese suppliers undercutting global brands by 10-25%. Here, Western and Japanese incumbents defend territory by offering better phosphor blends that lock in color point and qualify for DLC Premium rebates, especially in CRI 90 hospitality spaces.

By Application: Architectural And Outdoor Lighting Accelerates

Architectural and outdoor lighting applications for COB LEDs are projected to advance at a 17.55% CAGR between 2026 and 2031, making them the fastest-growing slice of the COB LED module market. City authorities are replacing high-intensity discharge lamps with smart COB streetlights, stadium operators are upgrading to broadcast-ready floodlights, and real estate developers are adopting color-tunable façade systems that synchronize with building management platforms. This momentum is reinforced by smart-city mandates that favor fixtures delivering at least 150 lm/W efficacy and instant dimming for traffic or security scenarios. General lighting retained a 35.12% COB LED module market share in 2025, yet its growth is tapering as offices, retail stores, and homes in North America and Europe near full LED penetration and buyers gravitate toward lower-cost chip-scale packages. Automotive demand adds another growth engine: integrated headlamp assemblies in battery electric vehicles now bundle daytime running, turn, and adaptive high-beam functions around compact COB cores, cutting wiring weight while preserving beam precision in slim housings.

Specialty niches are emerging as margin-rich frontiers that help suppliers escape commodity price pressure. Entertainment venues and stage productions favor COB modules for their uniform, shadow-free beams and smooth dimming to zero, while industrial users value IP65-plus sealing, −40°C to 70°C operating ranges, and compliance with UL ECOLOGO and IEC 61347-2-13. Collectively, these specialized verticals bolster the COB LED module market size by rewarding suppliers that can deliver tailored spectra, rigorous certification support, and long-term supply commitments.

Geography Analysis

Asia-Pacific accounted for 66.73% of global revenue in 2025 and will remain the epicenter of the COB LED module market through 2031, with a forecast 17.95% CAGR. China dominates with end-to-end LED clusters in Guangdong and Jiangsu, plus state incentives that defray capex for chip fabs and packaging lines. Mini-LED backlight adoption in televisions, notebooks, and monitors keeps domestic demand robust, while export aggressiveness fuels commodity supply across Southeast Asia. Japan and South Korea pursue smaller but lucrative niches in automotive, display, and medical equipment, leveraging ceramics, AlGaN epitaxy, and rigorous reliability tests to fetch premiums.

North America and Europe together accounted for roughly one-quarter of revenue in 2025. Retrofit programs driven by utility rebates, DLC Premium tiers, and EU Ecodesign rules accelerate replacement of fluorescent troffers and HID floodlights with COB fixtures exceeding 150 lm/W and CRI 90. Stadium renovations connected to the 2026 FIFA World Cup and the 2028 Los Angeles Olympics create headline projects that call for high-power modules capable of delivering flicker-free 8K broadcast levels. Circular-economy policies in Europe prefer socketable, repairable COB modules with digital product passports, rewarding suppliers that align mechanical footprints with Zhaga Book 12.

South America, the Middle East, and Africa are smaller but growing markets for COB LED modules. Brazil and Mexico deploy industrial LED high bays in food processing and logistics parks, while the Gulf Cooperation Council members invest in smart-city corridors that demand IP69K-rated COB floodlights to withstand sand and saline fog. Africa shows early traction for off-grid solar lanterns that integrate low-power COB engines for extended battery life, though price sensitivity limits the adoption of higher-tier products.

Competitive Landscape

The COB LED module market is moderately concentrated, with the top five suppliers accounting for a significant share. ams Osram, Nichia, Samsung Electronics, Lumileds, and Seoul Semiconductor differentiate through proprietary phosphors, wide binning maps, and vertically integrated chip-to-module lines. Bridgelux’s F90 and DriveLux launches exemplify a pivot from bare emitters toward driver-on-board light engines that shorten customers’ design cycles. Zhaga’s conversion of Book 12 into IEC 63356-2 stimulates interoperability, lowering the friction for fixture OEMs to dual-source emitters, and thereby heightening price rivalry.

Chinese challengers such as Refond and Cedar Electronics undercut mainstream SKUs by leveraging local wafer capacity and government subsidies to keep overhead low. Yet their penetration into automotive and industrial safety-critical segments lags because AEC-Q102 qualification, functional-safety documentation, and long-term supply commitments create high entry barriers.

Western, Japanese, and Korean incumbents continue to invest in color-stability formulations, red-enhanced KSF phosphors, and low-thermal-resistance substrates to widen the technical gap. Mergers or technology-licensing pacts remain likely as companies seek scale or unique intellectual property to defend margins amid a structural shift toward smart-lighting ecosystems.

COB LED Module Industry Leaders

ams OSRAM AG

Samsung Electronics Co., Ltd.

Nichia Corporation

Lumileds Holding B.V.

Seoul Semiconductor Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Bridgelux introduced Generation 2 F90 COB modules achieving Δu'v' greater than or equal to 0.004 from 25 °C to 85 °C and typical 185-200 lm/W at CRI 90.

- August 2025: Forvia Hella launched integrated headlamps for the LUXEED R7 that merge position and indicator lighting via dual-focus COB emitters.

- March 2025: Bridgelux unveiled DriveLux light engines with on-board drivers and tunable-white or RGBW mixing options.

- March 2025: Luminus Devices has unveiled its Generation 2 Warm Dimming COB (Chip on Board) LEDs, designed to replicate the cozy, welcoming radiance of classic incandescent and halogen lights, while harnessing the efficiency and dependability of modern LED technology.

Global COB LED Module Market Report Scope

The COB LED Module Market Report is Segmented by Power Range (Low Power COB Modules [Greater Than or Equal To 10 W], Mid Power COB Modules [Less Than 10 W – Greater Than or Equal To 50 W], High Power COB Modules [Less Than 50 W]), Application (General Lighting, Automotive Lighting, Industrial Lighting, Architectural and Outdoor Lighting, and Other Applications), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Low Power COB Modules (Greater Than or Equal To 10 W) |

| Mid Power COB Modules (Less Than 10 W – Greater Than or Equal To 50 W) |

| High Power COB Modules (Less Than 50 W) |

| General Lighting |

| Automotive Lighting |

| Industrial Lighting |

| Architectural and Outdoor Lighting |

| Other Applications (Horticulture, UV, Specialty) |

| North America |

| Europe |

| Asia-Pacific |

| Middle East and Africa |

| South America |

| By Power Range | Low Power COB Modules (Greater Than or Equal To 10 W) |

| Mid Power COB Modules (Less Than 10 W – Greater Than or Equal To 50 W) | |

| High Power COB Modules (Less Than 50 W) | |

| By Application | General Lighting |

| Automotive Lighting | |

| Industrial Lighting | |

| Architectural and Outdoor Lighting | |

| Other Applications (Horticulture, UV, Specialty) | |

| By Geography | North America |

| Europe | |

| Asia-Pacific | |

| Middle East and Africa | |

| South America |

Key Questions Answered in the Report

What is the projected value of the COB LED module market in 2031?

The COB LED module market is forecast to reach USD 4.02 billion by 2031.

How fast will high-power COB modules grow?

High-power modules above 50 W are set to post a 17.73% CAGR between 2026 and 2031, outpacing the total market.

Which region dominates sales today?

Asia-Pacific held 66.73% of global revenue in 2025 and will remain the largest region through 2031.

Why are stadium projects choosing COB technology?

A single COB emitter can deliver more than 5,000 lm, meeting broadcast flicker criteria while reducing fixture counts and maintenance.

How do new EU regulations affect module design?

From December 2026, modules sold in Europe must meet circularity and EPREL documentation rules, favoring socketable, serviceable COB designs.

Page last updated on: