Europe LED Module Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

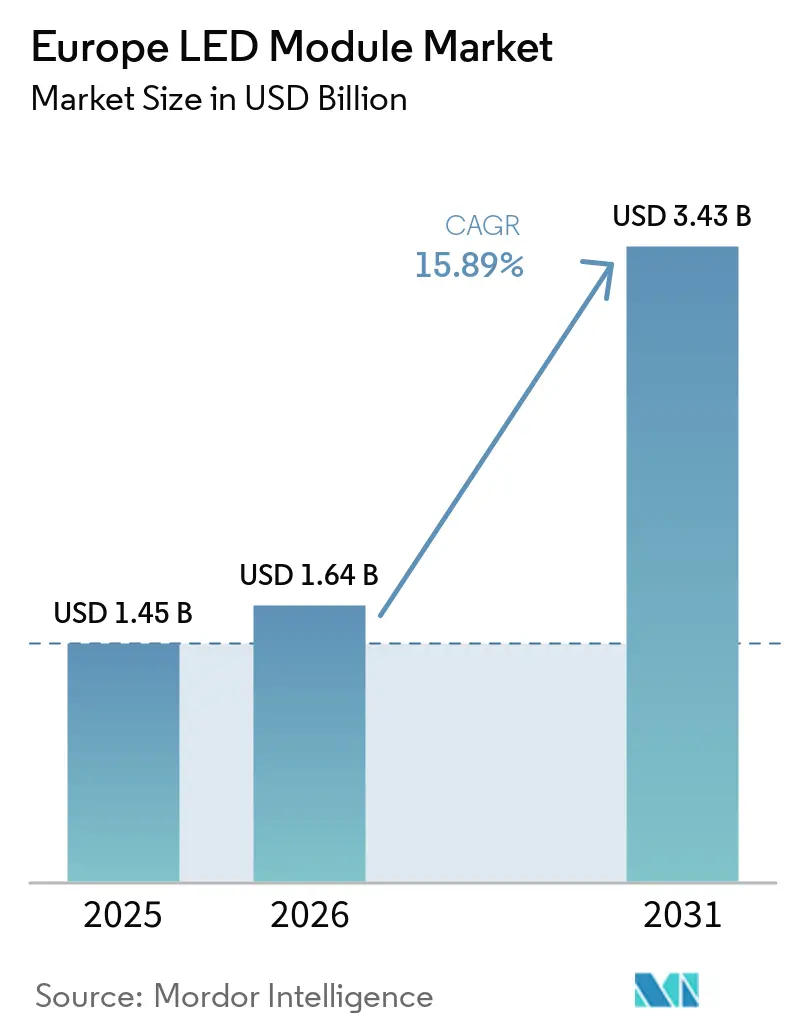

| Base Year Market Size (2025) | USD 1.45 Billion |

| Market Size (2026) | USD 1.64 Billion |

| Market Size (2031) | USD 3.43 Billion |

| Growth Rate (2026 - 2031) | 15.89% CAGR |

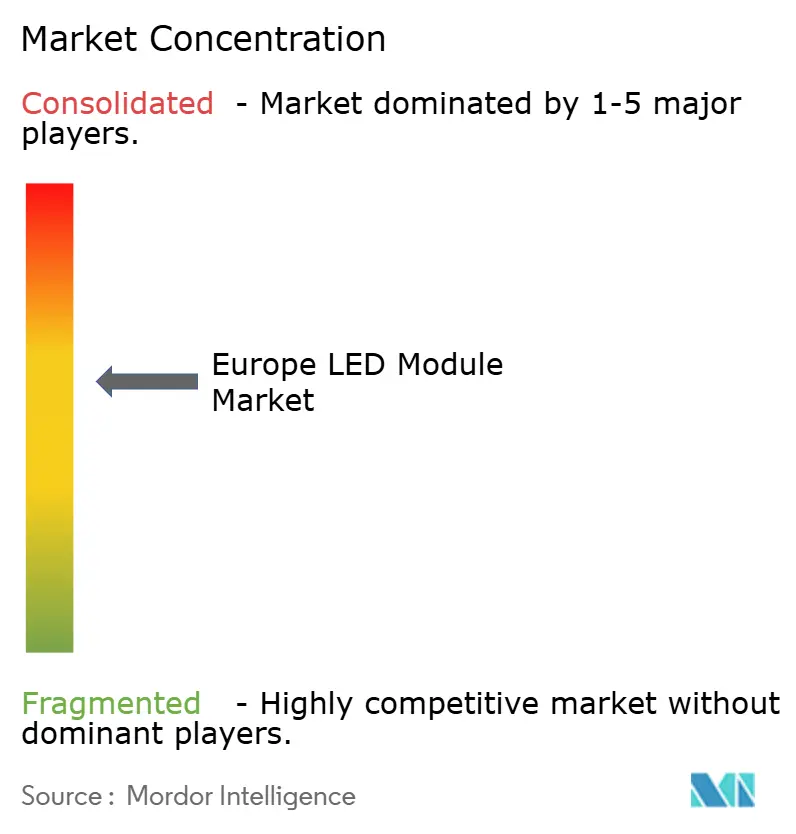

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe LED Module Market Analysis by Mordor Intelligence

The Europe LED Module Market size is projected to be USD 1.45 billion in 2025, USD 1.64 billion in 2026, and reach USD 3.43 billion by 2031, growing at a CAGR of 15.89% from 2026 to 2031. The Europe LED Module Market is moving away from legacy lighting toward intelligent and energy-optimized systems as public policy, procurement rules, and retrofit economics increasingly favor modular LED formats over conventional lamps and fixed luminaires. This shift is supported by the European Green Deal target to reduce energy consumption by 11.7% by 2030 and by public funding programs that are steering municipal lighting budgets toward retrofit projects with measurable savings and upgrade flexibility. Regulatory requirements have also tightened product entry conditions, which has reduced room for lower-tier suppliers and pushed demand toward manufacturers that can meet efficacy, flicker, and repairability expectations. Competitive activity remains active rather than overcrowded, with established suppliers using vertical integration, automotive programs, smart-city pilots, and product ecosystems to defend premium positions while lower-cost entrants increase pressure in commodity categories. The market still offers room in flexible modules, display backlighting, horticulture lighting, and connected street-lighting systems, where performance, software compatibility, and application-specific design matter more than simple unit price.

Key Report Takeaways

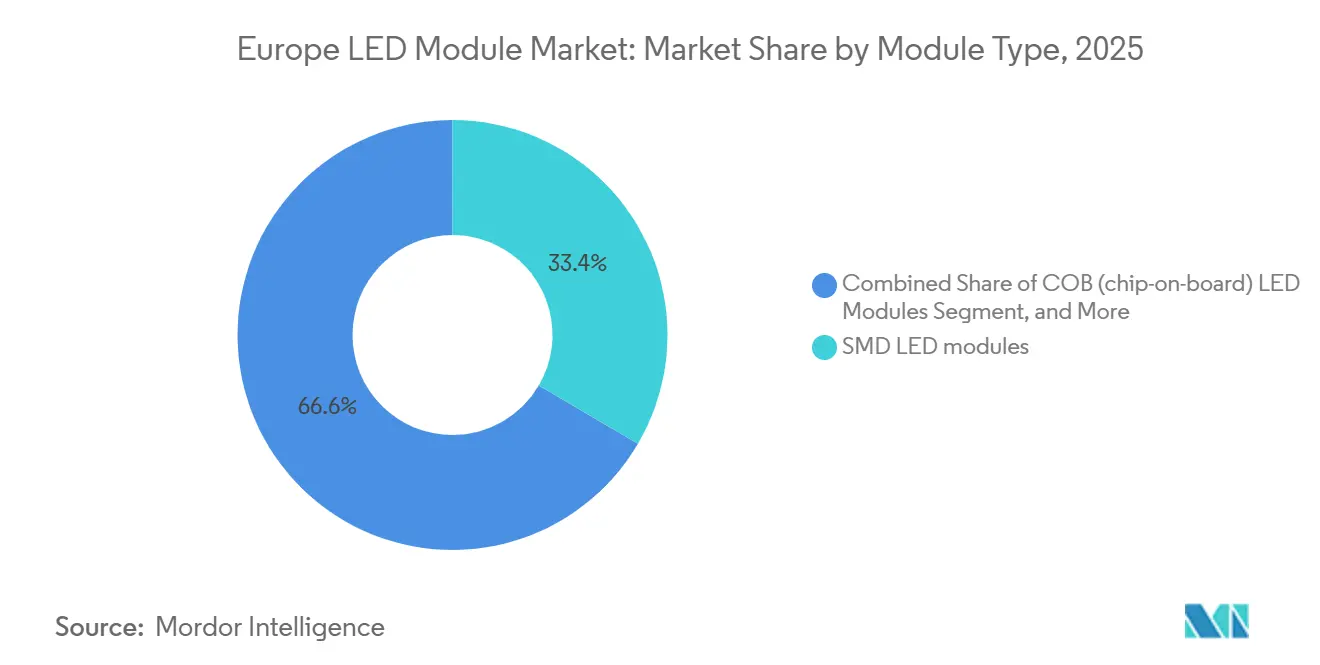

- By module type, SMD LED Modules held 33.43% of the Europe LED Module Market share in 2025, while Backlight Modules are projected to expand at a 16.43% CAGR through 2031.

- By application, General Lighting accounted for 42.72% of the Europe LED Module Market size in 2025, while Display and Backlighting are expected to grow at a 16.78% CAGR through 2031.

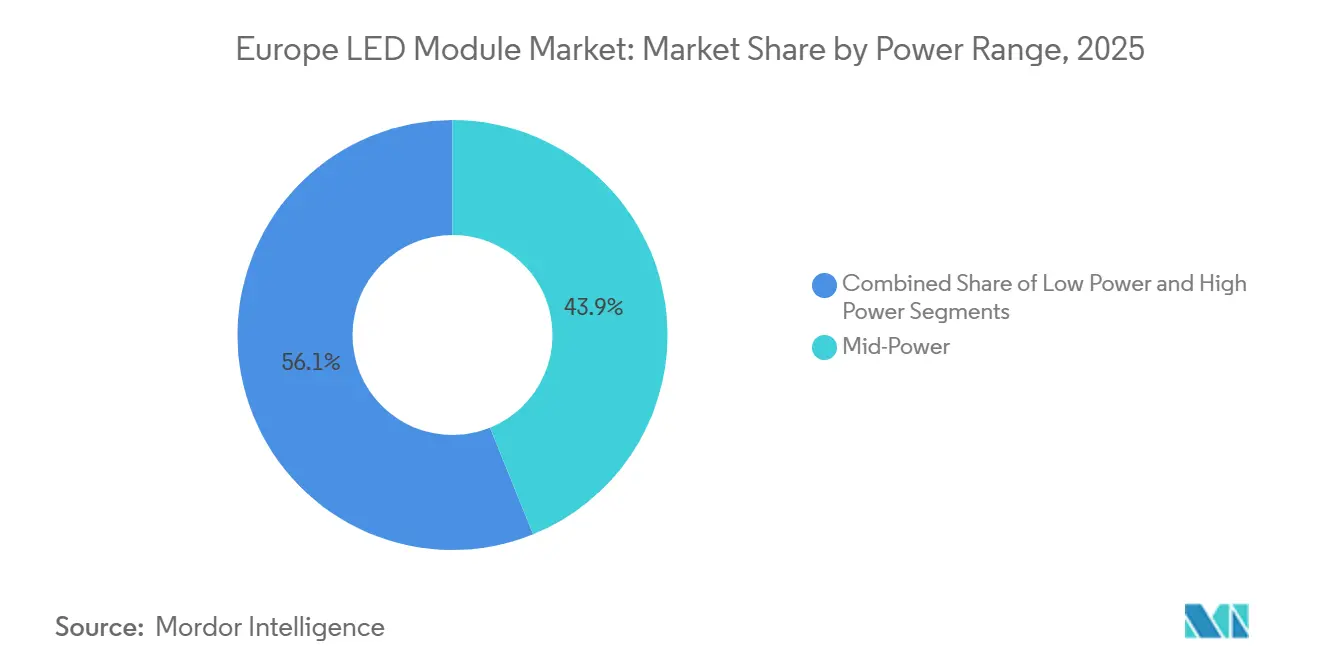

- By power range, Mid Power modules held 43.88% of revenue in 2025, while High Power modules are projected to record the highest CAGR at 16.84% through 2031.

- By form factor, Rigid modules represented 80.39% of revenue in 2025, while Flexible modules are expected to expand at a 16.71% CAGR through 2031.

- By country, Germany held 27.35% of regional revenue in 2025, while France is projected to grow at a 16.55% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe LED Module Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid phasing out of incandescent lighting across EU | +3.2% | EU-wide, accelerated in Germany, France, Nordics | Medium term (2-4 years) |

| Energy efficiency targets under European Green Deal | +2.8% | EU-wide, priority in Western and Northern Europe | Long term (≥ 4 years) |

| Declining LED cost per lumen | +2.5% | Global, strongest impact in price-sensitive Southern and Eastern Europe | Short term (≤ 2 years) |

| Surge in European Commission funding for smart city retrofits | +2.1% | Urban centers, Germany, France, Spain, Poland | Medium term (2-4 years) |

| Growing preference for human-centric tunable white modules in office spaces | +1.6% | Germany, Nordics, UK, Benelux | Medium term (2-4 years) |

| Demand spike from vertical farming facilities in Nordics | +1.2% | Denmark, Netherlands, Sweden, Norway | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Phasing Out Of Incandescent Lighting Across EU

The mandatory withdrawal of incandescent and halogen lamps under Ecodesign Regulation (EU) 2019/2020, reinforced by energy-label rescaling in September 2024, removed legacy options from retail channels and pushed the Europe LED Module Market further toward LED-based replacement cycles in residential, commercial, and municipal uses. This change has favored modular LED products because facility managers and electrical contractors can replace modules more easily than complete luminaires, which lowers downtime and reduces spare-part complexity across installed fleets.[1]European Commission, “Energy Efficiency Directive,” European Commission, energy.ec.europa.euWedemark municipality in Germany showed how this shift works in practice when it retrofitted 4,300 LED lanterns, cut energy use by 80%, reduced annual consumption by 900,000 kWh, and avoided EUR 270,000 (USD 305,000) in costs, with module life rated at 120,000 hours.[3]enercity, “Wedemark LED Street Lighting Retrofit,” enercity, enercity.de The transition has been especially favorable for SMD and COB suppliers because these formats fit common retrofit requirements for standardized sockets and thermal management across a wide set of luminaires. National enforcement by authorities such as Germany's Bundesnetzagentur and France's DGCCRF continues to support compliant suppliers by limiting the room for non-compliant imports and gray-market products in the Europe LED Module Market.

Energy Efficiency Targets Under European Green Deal

The European Green Deal target to reduce final energy consumption by 11.7% by 2030, backed by the Energy Efficiency Directive (EU) 2023/1791, creates a long-duration demand base for the Europe LED Module Market because LED modules can deliver up to 90% energy savings against incandescent alternatives. The policy framework also raises annual savings obligations to 1.9% during 2028-2030, which keeps lighting upgrades on procurement agendas for public bodies and commercial building operators across member states. European Commission assessments linked lighting upgrades to 41.9 TWh of annual electricity savings by 2030 and EUR 52 billion (USD 58.6 billion) in consumer savings, which keeps LED modules positioned as one of the lowest-cost pathways for abatement in buildings and municipal infrastructure. Article 8 procurement rules favor top energy-performance classes, which gives compliant module suppliers a clearer path into public tenders while keeping halogen and fluorescent options out of the main replacement cycle. Munich's adaptive street-lighting pilot, which tested tunable correlated color temperature from 3,000K to 1,700K and dimming profiles, showed energy reductions of up to 93% during low-traffic periods and pushed attention beyond simple lamp replacement toward networked LED systems with controls.[2]City of Munich, “Munich Street Lighting Retrofit Program,” City of Munich, muenchen.de

Declining LED Cost Per Lumen

Manufacturing scale and yield gains in gallium-nitride epitaxy have lowered LED module cost per lumen by 15% annually since 2020, which improved payback periods and made retrofits cash-flow positive within 18-24 months for many commercial and industrial users. This trend held even as aluminum prices moved above RMB 21,000 per ton and copper stayed near USD 9,800 per ton because suppliers reduced substrate thickness, optimized phosphor loadings, and expanded chip-on-board designs that remove packaging steps.[4]Joost M. van Gaalen and J. Chris Slootweg, “From Critical Raw Materials to Circular Raw Materials,” ChemSusChem, doi.orgThe drop has been strongest in mid-power SMD modules, where Chinese manufacturers used automated die-bonding and molding equipment to cut bill-of-materials costs by 20% since 2024, which forced European suppliers to compete more on thermal management, driver integration, and dimming capability than on bare component price. Signify's FY2025 results showed how strong this pressure had become, with OEM revenue declining 16.5% year over year to EUR 355 million (USD 400 million) as Chinese overcapacity weighed on margins in commodity SMD segments. The cost curve has flattened more in high-power and specialty modules because phosphor chemistry, thermal interfaces, and color binning still support 25% to 35% gross margins in applications with strict CRI or spectral-tuning requirements.

Surge In European Commission Funding For Smart City Retrofits

The EU Recovery and Resilience Facility and Horizon Europe programs have directed more than EUR 200 million (USD 225 million) into smart-city lighting projects since 2024, including EUR 69.6 million (USD 78.5 million) for Bulgaria's street-lighting retrofit and EUR 1.89 million (USD 2.1 million) for the RESONANCE project across 9 member states during 2025-2029. These programs favor modular LED systems that can work with IoT sensors, mesh networking, and central management software, which gives an advantage to suppliers with DALI-2 and Zhaga Book 18 certified portfolios. Signify's March 2026 Cologne Tunable Beam pilot showed how funding-backed street-lighting projects are shifting from passive replacement to intelligent infrastructure, with 20-25 streetlights delivering 30% additional energy savings beyond static LED upgrades. Project eligibility rules that require a minimum 30% energy reduction and lifecycle savings have reduced the appeal of proprietary or non-upgradable luminaire designs and increased demand for field-replaceable LED modules with standardized mechanical and electrical interfaces. The focus on circularity and digital product passports under the Ecodesign for Sustainable Products Regulation also supports repairable module architectures, which aligns with Signify's target for circular revenues to reach 27.5% by 2030.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High initial capital expenditure for LED module manufacturing | -1.8% | EU-wide, acute in Eastern Europe and smaller member states | Medium term (2-4 years) |

| Supply chain disruptions for semiconductor chips | -1.5% | Global, concentrated impact in Germany, France, Italy | Short term (≤ 2 years) |

| Intellectual property disputes over LED packaging patents | -0.9% | Germany, Netherlands, UK, litigation hubs | Long term (≥ 4 years) |

| Stringent Ecodesign regulations limiting hazardous substance use | -0.7% | EU-wide, compliance costs highest in Southern and Eastern Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Initial Capital Expenditure For LED Module Manufacturing

Building a competitive LED module line in Europe still requires EUR 50 million to EUR 150 million (USD 56 million to USD 169 million) in upfront spending on die-bonding tools, reflow ovens, automated optical inspection, and environmental chambers, which limits new entry and keeps capacity concentrated among established suppliers. This burden is heavier because technology shifts can strand equipment within 3-5 years as demand moves across power classes, substrates, and optical architectures. Smaller assemblers in Southern and Eastern Europe face a narrower financing window, and European Investment Bank lending for LED manufacturing totaled only EUR 250 million (USD 282 million) in 2025, which remains below what would be needed to support stronger domestic scaling. ams OSRAM's commitment of EUR 588 million (USD 663 million) through 2030 for its Austria expansion shows that the capital barrier is manageable mainly for companies with balance-sheet strength, policy support, or strategic semiconductor relevance The burden is felt more sharply in flexible and specialty segments because lower volumes and custom formats do not spread fixed costs as efficiently as general-lighting lines do in the Europe LED Module Market.

Supply Chain Disruptions For Semiconductor Chips

Gallium-nitride substrate shortages and longer lead times for LED driver ICs stretched procurement cycles to 26 weeks in 2025, which tightened output and raised spot prices for high-brightness COB and automotive-qualified modules by 12% to 18%. The problem is rooted in concentrated midstream processing, with China refining 99% of gallium and 95% of high-purity silicon, while export controls on gallium, germanium, and rare earths have increased allocation uncertainty for European manufacturers. The European Court of Auditors found in 2026 that 10 of 26 critical raw materials used in energy technologies, including gallium and germanium, had no EU recycling capacity, while permitting timelines for new projects averaged 15.7 years, which leaves little room for near-term relief. Producers have responded with dual sourcing, broader material tolerances, and 6-12 months of pre-purchased inventory, but those steps raise working-capital needs and increase the risk of holding parts that may become obsolete. The February 2025 EU Chips Act grant of EUR 227 million (USD 256 million) to ams OSRAM will help reduce dependency over time, but the Austria facility is not expected to reach full capacity until 2028, which leaves the Europe LED Module Market exposed during the current planning cycle.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Module Type: Backlight Density Drives Premium Tier

SMD LED Modules held 33.43% of Europe LED Module Market share in 2025, which reflected their entrenched use in residential and commercial general lighting where standardized footprints such as 3528, 5050, and 2835 packages support automated assembly and interchangeability across luminaire brands. Backlight Modules are projected to grow at a 16.43% CAGR through 2026-2031 as consumer-electronics manufacturers shift toward mini-LED and micro-LED architectures that support higher contrast and denser local dimming. Philips underlined this shift with the October 2026 launch of the MLED981 RGB Mini-LED TV, which featured 11,520 local dimming zones and 2,500-nit peak brightness. COB modules continue to serve industrial high-bay and retail spotlight applications where thermal performance and lumen density support a 15% to 25% premium over SMD alternatives. Linear LED modules remain important in architectural cove lighting and under-cabinet installations because continuous-run formats fit narrow installation spaces and simplify the visual effect of uninterrupted light lines.

High-power LED modules above 30 W are also gaining traction in vertical farming, where photosynthetically active radiation efficacies of up to 3.5 μmol/J help Nordic facilities run controlled crop cycles across the year. Other module formats, including flexible strips, mini-LED arrays, and custom assemblies, are serving more specialized projects such as Arena Milano, where 54,560 bespoke linear LED bars spanning 50 km were specified for the 2026 Winter Olympics venue with IP67-rated RGBW modules and DMX512 control across 3,785 universes. Thermal management and color quality are shaping competitive positions inside this mix, because COB modules remain strong in applications that need CRI of 95 or more and R9 values above 80, while lower-cost SMD products continue to dominate utility lighting where CRI 80 is sufficient. Backlight modules face separate design demands such as sub-1 mm height limits and precise coupling with quantum-dot films, which keeps investments focused on flip-chip attachment and micro-lens arrays. Ecodesign compliance around flicker limits and minimum efficacy has pushed lower-tier SMD suppliers out of higher-quality categories and concentrated volume around Tier-1 manufacturers with stronger driver and thermal design capabilities in the Europe LED Module Market.

By Application: Display Backlighting Outpaces Commodity Segments

General Lighting accounted for 42.72% of the Europe LED Module Market size in 2025, as LED modules replaced fluorescent troffers, downlights, and high-bay fixtures across residential, commercial, and industrial settings. Display and Backlighting is expected to advance at a 16.78% CAGR through 2026–2031 as screen makers and vehicle manufacturers move toward local-dimming architectures in premium televisions, instrument clusters, and center-information displays. Premium TV demand in Western Europe supported this trend, with 65-inch and larger screens accounting for 38% of unit sales in 2025, which kept pressure on suppliers to deliver denser and brighter backlight systems.

Automotive Lighting remains a strategic segment because matrix LED headlamps and digital-light projection systems require sub-millisecond switching and automotive-grade qualification, which narrows the field of suppliers that can serve global OEM programs. ams OSRAM reported more than EUR 500 million (USD 564 million) in design wins for its Digital Light platform, showing how application-specific capability can outweigh volume economics in the Europe LED Module Market.

Signage and Advertising continue to depend on outdoor-rated modules with IP65 or IP67 protection and brightness levels above 10,000 nits for daylight readability, which keeps this segment tied to performance rather than only cost. Other applications span architectural façade lighting, horticulture modules optimized for 450 nm and 660 nm peaks, UV-C disinfection modules operating at 265–280 nm, and surgical lighting with adjustable CCT from 3,000K to 6,500K. The application mix now shows a clear split between commodity general-lighting programs and specialty niches such as automotive, horticulture, and display backlighting, where margins are supported by tighter tolerances, longer qualification periods, and stronger optical requirements. General lighting remains the volume base, but specialty applications keep a larger share of technical value because they demand qualification testing, spectral tuning, and system integration that are harder to replicate quickly.

By Power Range: High-Power Modules Capture Industrial Upgrades

Mid-power modules, ranging from 5 W to 30 W, accounted for 43.88% of the Europe LED Module Market in 2025 because they meet the lumen needs of residential lamps, commercial downlights, and many street-lighting retrofits, with output levels from 800 lm to 2,000 lm. High Power modules above 30 W are projected to grow at a 16.84% CAGR through 2026-2031 as industrial high-bay replacement, sports lighting, and vertical farming demand stronger photon output and longer operating cycles. These products are now moving into applications that once relied on metal-halide systems, especially where photon flux densities of 400 μmol/m²/s to 800 μmol/m²/s are needed in controlled-environment agriculture. Low Power modules at 5 W and below still serve accent lighting, under-cabinet strips, and decorative use cases, but that part of the mix is more mature and grows closer to renovation and housing activity than to structural technology change. Efficacy gains are also reshaping the category boundary because newer mid-power modules at 180 lm/W can now reach lumen packages that previously required high-power architectures, which reduces system cost and heat-sink requirements in some retrofit designs.

High-power modules still carry the stricter engineering burden because junction temperature needs to stay below 85°C to limit lumen depreciation and protect long-life performance. I-Valo's XENRE series, rated from 83 W to 272 W and from 12,700 lm to 36,200 lm, uses copper-core MCPCB construction and vapor-chamber spreading to keep thermal resistance below 0.5°C/W while maintaining 150 lm/W efficacy at full output. LIGHTS' Lucid sirius platform spans 100 W to 500 W, reaches 70,800 lm, and uses active thermal monitoring with current derating to extend L90 lifetimes beyond 100,000 hours in industrial duty cycles. Low-power modules, by contrast, face growing commoditization because their simpler architecture leaves little room for differentiation beyond price, packaging, and minor optical refinement in the Europe LED Module Market.

By Form Factor: Flexible Modules Unlock Architectural Creativity

Rigid LED Modules represented 80.39% of revenue in 2025, which reflected their strength in downlight engines, troffer retrofits, and street-lighting applications where mechanical stability, standardized mounting, and cost discipline matter more than shape adaptability. Flexible LED Modules are expected to expand at a 16.71% CAGR through 2026-2031 as architectural and event-driven installations increasingly need curved forms, irregular geometries, and pixel-level control across large surfaces. Arena Milano became a clear example of this shift through its use of 54,560 linear LED bars across 50 km for the 2026 Winter Olympics venue, where IP67-rated RGBW strips and DMX control were essential to the design brief. Inventronics added to the ecosystem in October 2025 with the TEC FLEX NeoGen driver, a Europe-manufactured product optimized for flexible strip loads, which shows that supporting electronics are also moving in step with form-factor demand. OSRAM's LINEARlight Colormix Flex, with IP67 protection and 72 W RGB output, targets hospitality and retail façade work where weather resistance and dynamic color effects justify a higher selling price than rigid boards can command.

The trade-off is thermal performance, because polyimide and polyester substrates used in flexible modules carry higher thermal resistance than aluminum MCPCBs, which limits current density and total lumen output per meter. Suppliers manage that constraint by using lower LED densities and lower junction temperatures, which extends L70 lifetimes to 30,000-50,000 hours even if initial brightness per meter is lower than that of rigid strips. Flexible systems also depend on specialized interconnects such as solderless snap connectors or conductive adhesives, which raise connection cost and add failure points under repeated thermal cycling. Even with those limits, designers continue to specify flexible products for cove lighting, handrail lighting, and three-dimensional signage because bend radii below 25 mm allow shapes that rigid boards cannot deliver, and this has made the category one of the more distinct growth pockets in the Europe LED Module Market.

Geography Analysis

Germany held 27.35% of Europe LED Module Market share in 2025, supported by its automotive OEM base and by large municipal retrofit programs that kept both premium and volume demand active. Munich's street-lighting rollout covered 48,000 street luminaires and 20,000 foot-and-cycle-path lights, which helped deliver 60% energy savings, 1,650 MWh of annual reductions, and 875 tonnes of CO₂ abatement. The city also showed the value of intelligent controls, as adaptive pilots using tunable CCT from 3,000K to 1,700K and occupancy-based dimming reached savings of up to 93% during low-traffic periods. Germany's regulatory discipline further supports certified suppliers because market surveillance removed 14% of sampled LED products in 2025 for failing flicker or efficacy thresholds. The country's industrial base, especially automotive, chemical, and pharmaceutical manufacturing, also keeps demand strong for flicker-free and high-CRI modules in production and cleanroom environments.

France is the fastest-growing geography, with the Europe LED Module Market size for the country set to rise at a 16.55% CAGR through 2026-2031 as smart-city spending and automotive-lighting demand continue to build. Paris deployed 20,000 connected LED streetlights with DALI-2 controls and real-time energy monitoring, while smaller municipalities continued to use EU Recovery and Resilience Facility support for projects targeting 30% energy reduction. France's RE2020 building rules, which cap primary-energy use for new construction at 12 kWh/m²/year, support stronger uptake of efficient mid-power and tunable-white modules in commercial and residential buildings. The United Kingdom kept LED module imports stable in 2025, but post-Brexit customs friction and tariff uncertainty still lengthened lead times by 5-10 days and pushed some distributors to hold buffer inventory inside the EU27.

Rest of Europe includes Scandinavian vertical-farming clusters in Denmark, the Netherlands, and Sweden, Southern European solar-hybrid street-lighting projects in Spain, Italy, and Greece, and Eastern European retrofit programs funded through EU cohesion mechanisms, which together keep demand broad even outside the largest markets. Regional buying patterns are split, with Western and Northern Europe emphasizing tunable white, high CRI, and smart controls, while Southern and Eastern Europe focus more on payback speed and cost-efficient module lines. The Critical Raw Materials Act targets of 10% domestic extraction, 40% processing, and 25% recycling by 2030 are intended to reduce dependence on single-country supply, but current EU processing capacity is only 24% of need and recycling rates for gallium and indium remain below 5%. That gap will remain important because strategic projects such as ams OSRAM's Austria GaN expansion will not reach full capacity until 2028, which leaves the Europe LED Module Market exposed to import dependence and periodic spot-price pressure for several more years.

Competitive Landscape

The Europe LED Module Market remained moderately concentrated in 2025, with Signify, ams OSRAM, Samsung Electronics, Nichia, and Lumileds collectively accounting for an estimated 45% to 50% of revenue, while the rest of the market stayed fragmented across regional integrators, contract manufacturers, and lower-cost entrants. These leading suppliers defend their positions through vertical integration, in-house phosphor and driver work, and deeper patent portfolios rather than through price alone. Nichia's March 2025 lawsuit against Everlight in Düsseldorf, seeking EUR 2.5 million (USD 2.8 million) in damages over YAG phosphor patent infringement, showed how important intellectual property remains in white-LED module competition. Signify also used system-level differentiation when it launched the Cologne Tunable Beam pilot in March 2026, where dynamic beam shaping delivered 30% additional energy savings beyond static LED replacements. ams OSRAM strengthened its position in automotive applications with more than EUR 500 million (USD 564 million) in Digital Light design wins, which reflects the value of application-specific capability in a market where automotive qualification cycles are long and demanding.

Open space remains in flexible architectural modules, horticulture-optimized products, and UV-C disinfection systems because those areas require optical, thermal, or spectral specialization that is harder to standardize. Chinese competition is still becoming more relevant, especially after San'an Optoelectronics completed the acquisition of Lumileds for USD 239 million in August 2025 and strengthened its position in automotive LED supply. That ownership change gives San'an a stronger base for European expansion because scale in Asia-Pacific can be used to support more aggressive pricing into OEM channels. Suppliers with stronger human-centric lighting portfolios are also capturing office retrofits, as shown by Zumtobel's ATP Christiansbro Copenhagen installation of more than 5,000 PANOS infinity downlights with 129 lm/W efficacy, 95 CRI, and WELL Building Standard compliance.

Ecodesign Regulation (EU) 2019/2020 continues to raise barriers because minimum efficacy thresholds of 85-120 lm/W and flicker limits of Pst LM ≤1.0 reduce room for lower-tier imports that cannot pass compliance testing. Suppliers with ISO/IEC 17025 accredited laboratories and stronger internal testing therefore hold an advantage in the Europe LED Module Market because they can move faster through qualification and public-procurement filters. Price pressure is still strongest in commodity SMD products, while specialty segments such as display backlighting, automotive modules, and horticulture lighting retain better margin structure because qualification cycles are longer and optical demands are stricter. The competitive picture therefore combines global scale, technical compliance, application design capability, and project execution support rather than simple price competition alone.

Europe LED Module Industry Leaders

Signify N.V.

Osram Opto Semiconductors GmbH

Samsung Electronics Co., Ltd.

Nichia Corporation

Lumileds Holding B.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Signify launched the Cologne Tunable Beam pilot, deploying 20 to 25 streetlights with dynamic beam-shaping capabilities that achieved 30% additional energy savings beyond static LED replacements, demonstrating the potential for intelligent optics to unlock second-wave efficiency gains in municipal retrofits.

- October 2025: Inventronics introduced the TEC FLEX NeoGen driver, manufactured in Europe and optimized for flexible LED strip loads, signaling growing ecosystem support for non-rigid form factors in architectural and facade lighting applications.

- September 2025: Signify updated its Philips Hue ecosystem with the Bridge Pro, Essential line, and OmniGlow CSP strips, expanding its consumer smart-lighting portfolio and reinforcing its platform strategy in the residential segment.

Europe LED Module Market Report Scope

An LED Module is a pre-assembled, integrated lighting component consisting of one or more light-emitting diodes (LEDs) mounted on a printed circuit board or substrate, along with essential electrical and thermal management elements such as current-limiting circuitry and heat-dissipation structures, designed to operate as a functional light source when incorporated into a luminaire and powered by an appropriate electrical supply.

The Europe LED Module Market Report is segmented by Module Type (COB (chip-on-board) LED modules, SMD LED modules, Linear LED modules, LED backlight modules, High-power LED modules, and Other module types including flexible, mini, and custom assemblies), Application (General lighting with Residential, Commercial, and Industrial sub-segments; Automotive lighting; Display and backlighting; Signage and advertising; and Other applications including architectural, horticulture, UV, and specialty lighting), Power Range (Low power less than or equal to 5 W, Mid power (greater than 5 W to (less than or equal to 30 W), and High power (greater than 30 W), Form Factor (Rigid LED modules and Flexible LED modules), and Country (United Kingdom, Germany, France, and Rest of Europe). The market forecasts are provided in terms of value (USD).

| COB (chip-on-board) LED modules |

| SMD LED modules |

| Linear LED modules |

| LED backlight modules |

| High-power LED modules |

| Other module types (flexible, mini, custom assemblies) |

| General lighting | Residential |

| Commercial | |

| Industrial | |

| Automotive lighting | |

| Display and backlighting | |

| Signage and advertising | |

| Other applications (architectural, horticulture, UV, specialty lighting) |

| Low Power (less than or equal to 5 W) |

| Mid Power (greater than 5 W to less than or equal to 30 W) |

| High Power (greater than 30 W) |

| Rigid LED modules |

| Flexible LED modules |

| United Kingdom |

| Germany |

| France |

| Rest of Europe |

| By Module Type | COB (chip-on-board) LED modules | |

| SMD LED modules | ||

| Linear LED modules | ||

| LED backlight modules | ||

| High-power LED modules | ||

| Other module types (flexible, mini, custom assemblies) | ||

| By Application | General lighting | Residential |

| Commercial | ||

| Industrial | ||

| Automotive lighting | ||

| Display and backlighting | ||

| Signage and advertising | ||

| Other applications (architectural, horticulture, UV, specialty lighting) | ||

| By Power Range | Low Power (less than or equal to 5 W) | |

| Mid Power (greater than 5 W to less than or equal to 30 W) | ||

| High Power (greater than 30 W) | ||

| By Form Factor | Rigid LED modules | |

| Flexible LED modules | ||

| By Country | United Kingdom | |

| Germany | ||

| France | ||

| Rest of Europe | ||

Key Questions Answered in the Report

What is the size of the Europe LED Module Market in 2026 and where is it expected to reach by 2031?

The Europe LED Module Market stands at USD 1.64 billion in 2026 and is forecast to reach USD 3.43 billion by 2031, growing at a CAGR of 15.89% during 2026-2031.

Which module type leads revenue in Europe and which one is growing the fastest?

SMD LED Modules led with 33.43% share in 2025, while Backlight Modules are projected to grow the fastest at a 16.43% CAGR through 2031.

Why is display backlighting growing faster than general lighting in Europe?

Display and Backlighting is expanding at a 16.78% CAGR because premium televisions, automotive displays, and local-dimming architectures are increasing demand for denser and brighter backlight modules.

Which country is the largest contributor and which one is expanding the fastest?

Germany held 27.35% of regional revenue in 2025, while France is projected to post the fastest growth at a 16.55% CAGR through 2031.

What is driving demand for high-power LED modules in Europe?

Upgrades, sports lighting, and vertical farming, and the segment is forecast to grow at a 16.84% CAGR through 2031.

What are the main risks affecting suppliers in this space?

The main risks are semiconductor and gallium-related supply disruptions, rare-earth phosphor price volatility, high manufacturing capex, and IP disputes that can raise cost and delay supply.

Page last updated on: