Asia-Pacific Gaming GPU Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

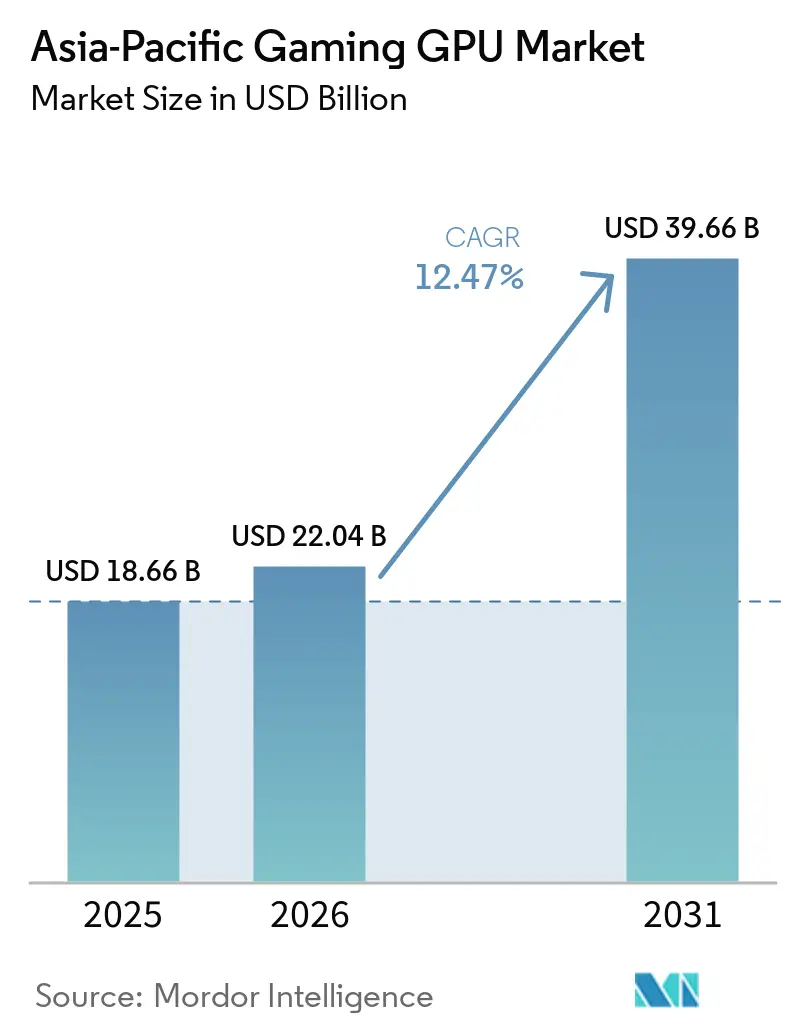

| Base Year Market Size (2025) | USD 18.66 Billion |

| Market Size (2026) | USD 22.04 Billion |

| Market Size (2031) | USD 39.66 Billion |

| Growth Rate (2026 - 2031) | 12.47% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Gaming GPU Market Analysis by Mordor Intelligence

The Asia-Pacific gaming GPU market size is expected to grow from USD 18.66 billion in 2025 to USD 22.04 billion in 2026 and is forecast to reach USD 39.66 billion by 2031 at 12.47% CAGR over 2026-2031. Growth rests on the combined effect of larger esports infrastructure, wider use of AI-led rendering tools, and a clear consumer move toward higher visual quality across PCs, laptops, and mobile devices. A less visible but important link comes from the premium mobile chipset race, where hardware ray tracing in flagship SoCs is shaping performance expectations that later influence discrete GPU buying behavior in China, India, and Southeast Asia. Supply conditions are also affecting spending patterns, because pressure on GDDR memory availability has raised the cost of lower-tier boards and pushed more buyers toward mid-range and premium products. China remains the largest country market because of its PC cafe base, local board manufacturing depth, and ongoing domestic chip investment, while India is set to record the fastest expansion over the forecast period. The competitive picture remains concentrated at the silicon level, and software-led performance features such as frame generation are making mid-tier products more capable and shortening upgrade decisions in price-sensitive parts of the region.

Key Report Takeaways

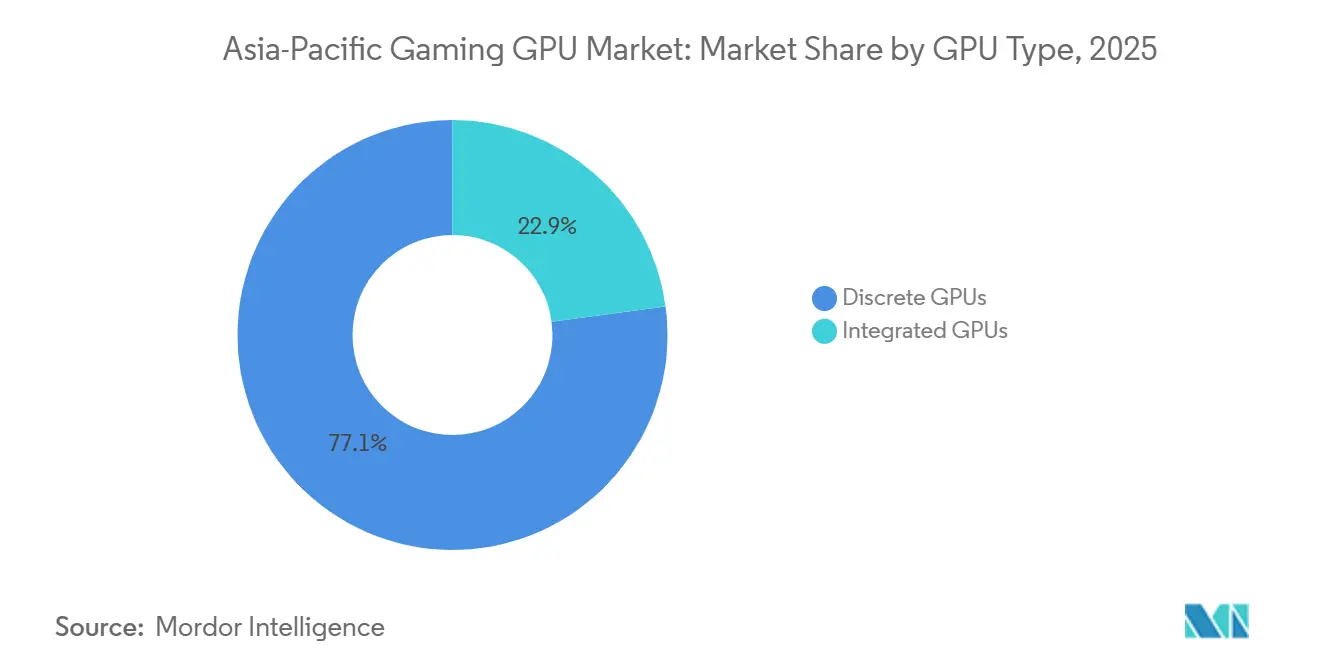

- By GPU type, discrete GPUs are projected to expand at a 13.02% CAGR from 2026 to 2031, making them the fastest-growing category in the Asia-Pacific gaming GPU market.

- By device type, gaming desktops held 45.61% of the Asia-Pacific gaming GPU market size in 2025, while gaming laptops are projected to expand at a 12.98% CAGR through 2031.

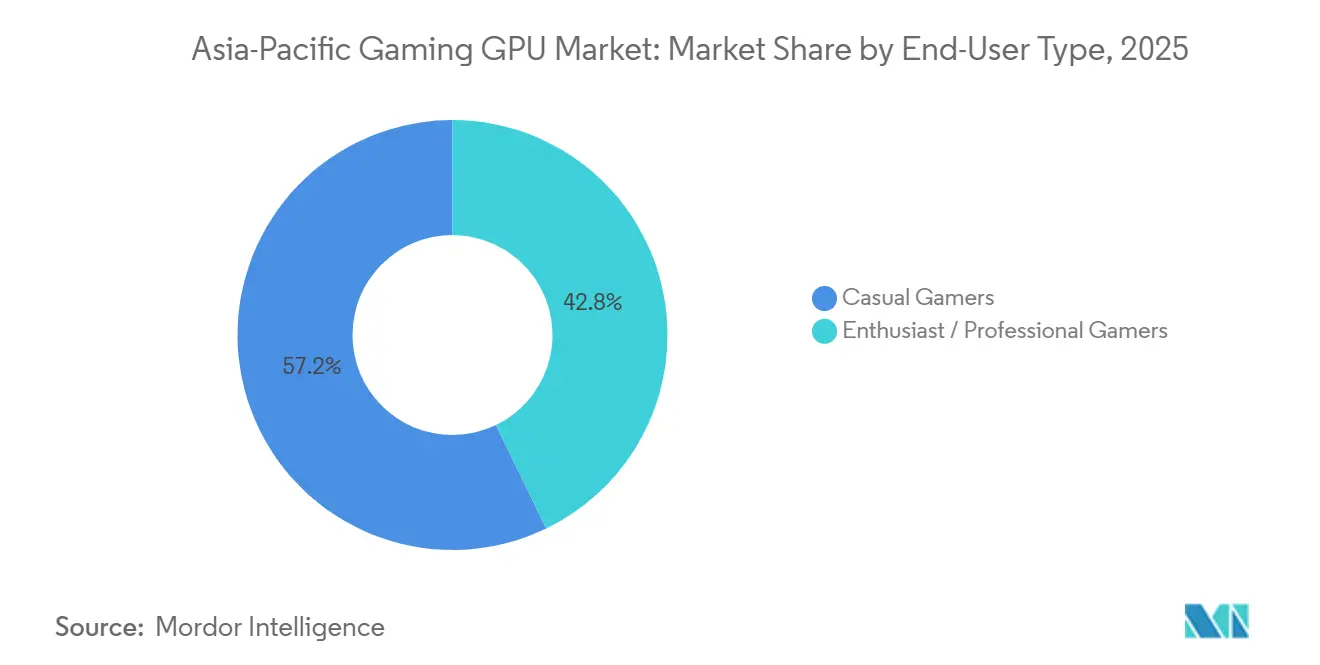

- By end-user type, casual gamers held 57.18% of the Asia-Pacific gaming GPU market share in 2025, while enthusiast and professional gamers are expected to record the highest CAGR at 13.66% from 2026 to 2031.

- By memory type, GDDR6X is projected to post the fastest growth at a 13.93% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Asia-Pacific Gaming GPU Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Esports Prize Pools And Campus Leagues Expanding GPU Upgrade Cycles | +3.2% | APAC-wide, highest impact in Southeast Asia and India | Short term (≤ 2 years) |

| AI Upscaling And Frame Generation Raising Mid-Tier GPU Utility | +2.8% | Global driver, concentrated benefit in APAC mid-tier discrete GPU segments | Medium term (2-4 years) |

| Cloud Gaming Rollouts Broadening Access To High-Fidelity Play | +2.2% | Southeast Asia, India, spillover to broader APAC | Medium term (2-4 years) |

| Premium Mobile SoCs Bringing Hardware Ray Tracing To Mobile Games | +1.8% | China, India, Southeast Asia | Medium term (2-4 years) |

| Handheld PC Spillover Lifting Demand For Laptop-Class GPUs | +1.4% | Japan, South Korea, China, Australia | Short term (≤ 2 years) |

| China Localization Efforts Diversifying Gaming GPU Supply | +1.0% | China | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Esports Prize Pools And Campus Leagues Expanding GPU Upgrade Cycles

Structured esports competition is acting as a hardware demand engine across the region, especially through campus formats that make high-performance gaming more visible to students. OPPO's Hyper Legend Cup x Mobile Legends Bang Bang Campus Series 2026 drew more than 1,400 team registrations across Indonesia, the Philippines, Malaysia, and Singapore, and the prize pool reached USD 100,000, up from USD 52,000 in the prior cycle. Acer's Predator League Asia-Pacific 2026 also reinforced this pattern, because a regional event with teams from more than 14 APAC territories gave sponsored hardware stronger visibility among players and spectators. As prize structures become more formal, buyers start to view GPU upgrades as a practical requirement for training and competition rather than a discretionary purchase. That effect is especially relevant in the Asia-Pacific gaming GPU market, where first exposure to premium gaming hardware often happens in school labs, tournaments, and organized gaming venues.

AI Upscaling And Frame Generation Raising Mid-Tier GPU Utility

AI upscaling has changed the value equation for mid-range gaming cards, especially in markets where buyers compare frame output closely against total system cost. NVIDIA introduced DLSS 4.5 in 2026 with a second-generation transformer model for super resolution and a 6x Multi Frame Generation mode for GeForce RTX 50 Series GPUs.[1]NVIDIA Corporation, “NVIDIA DLSS 4.5 Delivers Super Resolution Upgrades and New Dynamic Multi Frame Generation,” NVIDIA Technical Blog, developer.nvidia.com AMD answered in May 2026 by extending FSR 4 hardware-accelerated upscaling to older RDNA 3 and RDNA 3.5 products, including the Radeon RX 7000 series, with rollout starting in July.[2]Advanced Micro Devices, Inc., “AMD Brings FSR 4 Hardware-Accelerated Upscaling to Radeon RX 7000 Series GPUs,” AMD GPUOpen, gpuopen.com This shift delays replacement for some casual buyers, because existing hardware can now deliver better image quality and frame rates through software improvements. At the same time, it accelerates upgrades among enthusiasts in the Asia-Pacific gaming GPU market, because the newest frame generation features still require current-generation hardware to unlock their full value.

Cloud Gaming Rollouts Broadening Access To High-Fidelity Play

Cloud gaming is lowering the entry barrier to high-fidelity play in markets where discrete hardware still carries a high upfront cost. Xbox Cloud Gaming expanded to India in November 2025 and said usage had risen 45% year over year, with additional in-region server capacity added to reduce wait times. In Southeast Asia, Radian Arc worked with VNPT in Vietnam in March 2026 and with True Corporation in Thailand in May 2026 to deploy carrier-embedded GPU cloud platforms serving premium game catalogs through local network infrastructure. These rollouts do not remove the case for local GPUs, because they widen the total gamer pool and raise expectations for visual quality. Over time, that creates a larger base of users who are more willing to move from streamed gaming into local gaming devices, which supports the Asia-Pacific gaming GPU market in later upgrade cycles.

Premium Mobile SoCs Bringing Hardware Ray Tracing To Mobile Games

Hardware ray tracing in flagship mobile chips is setting a new visual baseline for a very large gaming audience in Asia-Pacific. Arm introduced the Mali G1-Ultra in 2026 and said its RTUv2 unit delivered 2x the ray tracing performance of the previous generation.[3]Arm, “Mali G1-Ultra, Next-Generation Flagship GPU for Mobile Gaming,” Arm, arm.com Arm also disclosed that MediaTek's Dimensity 9400 on the Immortalis-G925 architecture delivered a 40% lift in ray tracing performance and a 41% peak GPU performance gain over the prior generation. Apple said its M5, launched in October 2025, included a third-generation ray tracing engine and delivered up to 45% graphics performance improvement in ray-tracing-enabled applications.[4]Apple Inc., “Apple Unleashes M5, the Next Big Leap in AI Performance for Apple Silicon,” Apple Newsroom, apple.com Once users experience those gains on phones and tablets, integrated graphics in lower-cost notebooks can feel less sufficient, which strengthens demand for higher-capability gaming systems in the Asia-Pacific gaming GPU market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Export Controls On Advanced GPUs And Interconnects | -2.8% | China primarily, spillover to global supply reallocation | Medium term (2-4 years) |

| Advanced Packaging And VRAM Tightness Inflating Board Costs | -2.1% | Global driver, concentrated near-term impact across APAC | Short term (≤ 2 years) |

| Integrated And Unified Memory Designs Compressing Entry-Tier Demand | -1.2% | Japan, South Korea, India, markets with high laptop-GPU substitutability | Long term (≥ 4 years) |

| Power And Thermal Limits In Compact Gaming Devices | -0.8% | APAC-wide, most acute in handheld PC and ultra-thin laptop categories | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Export Controls On Advanced GPUs And Interconnects

Export controls remain the clearest structural risk to the Asia-Pacific gaming GPU market because they narrow product availability and reshape regional supply priorities. The U.S. Bureau of Industry and Security issued a final rule on January 15, 2026, that revised export licensing for advanced computing semiconductors to China and Macau under stricter compliance conditions. Even when gaming products are not the direct target, changes in certification and review requirements affect the same supply chains used by board partners, OEMs, and channel distributors. This makes the premium end of the China business less predictable and can shift volumes toward lower-tier products or non-China markets. The result is a more uneven regional growth pattern, with high-end availability increasingly shaped by compliance rules rather than only by consumer demand.

Advanced Packaging And VRAM Tightness Inflating Board Costs

Memory and component constraints are the most immediate cost-side headwind for the Asia-Pacific gaming GPU market in the near term. AMD said in its first-quarter 2026 results that higher memory and component costs were pressuring PC and gaming demand, and it guided for a greater-than-20% gaming revenue decline in the second half of 2026. That comment matters because it shows cost pressure is not limited to one product tier and is already affecting vendor expectations. When board costs rise, entry-level buyers in markets such as India, Indonesia, and Vietnam tend to extend replacement cycles first. Premium buyers still spend, but the lower end contributes less unit growth, which slows the broader pace of expansion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By GPU Type: Discrete GPUs Support The Core Performance Cycle

Discrete GPUs are projected to advance at a 13.02% CAGR from 2026 to 2031, which keeps them at the center of the Asia-Pacific gaming GPU market. Their position remains strong in premium and mainstream PC gaming because competitive play, higher refresh displays, and AI-led rendering features still require more graphics headroom than integrated solutions can usually provide. The segment also benefits from the organized PC gaming culture in several APAC countries, where gaming venues and heavy-use players refresh systems more often than casual households. That pattern supports repeat demand even when entry-tier consumer spending becomes uneven.

NVIDIA's Blackwell generation, including the GeForce RTX 5090 and RTX 5080, introduced in January 2025, lifted the performance ceiling for gaming systems and raised expectations for new hardware cycles. NVIDIA reported fiscal 2025 revenue of USD 130.5 billion, up 114% year over year, with gaming remaining the largest contributor within its Graphics segment alongside a rapidly scaling data center business. Integrated GPUs are gaining more ground at the low end of the Asia-Pacific gaming GPU industry, because newer client processors have narrowed the performance gap for entry gaming and mixed-use laptops. AMD reported Client and Gaming revenue of USD 3.6 billion in the first quarter of 2026, up 23% year over year, but it also warned that gaming demand would face pressure from higher memory and component costs later in the year.

By Device Type: Desktops Lead While Laptops Gain Ground

Gaming desktops held 45.61% of the Asia-Pacific gaming GPU market size in 2025, which reflected the region's strong base of dedicated gaming setups, esports venues, and upgradable systems. Desktops continue to benefit from modular upgrades, because buyers can replace the graphics card without replacing the full device. That lowers refresh costs for individuals and for institutional buyers such as gaming cafes, training centers, and local esports venues. In the Asia-Pacific gaming GPU market, this replacement model keeps desktop demand durable even when premium flagship cards move out of reach for many buyers.

Gaming laptops are forecast to expand at a 12.98% CAGR from 2026 to 2031, and that pace shows how quickly portable performance is improving. ASUS announced the Zephyrus Duo in January 2026 as a 16-inch dual-screen OLED gaming laptop with up to an NVIDIA GeForce RTX 5090 Laptop GPU at 135W TGP, which showed how close premium mobile systems had moved toward desktop-class performance expectations. ASUS also introduced refreshed Zephyrus G14 and G16 models with Intel, AMD, and NVIDIA options, which widened the choice set for buyers seeking portability without leaving the high-performance bracket. Smartphones, tablets, and handheld PCs remain important to the Asia-Pacific gaming GPU industry, but their economics differ because premium SoCs and integrated graphics platforms drive more of their value than discrete add-in boards.

By End-User Type: Enthusiast Spending Is Expanding Faster Than Volume Demand

Casual gamers held 57.18% of the Asia-Pacific gaming GPU market share in 2025, which shows that the broad user base still sits at the lower end of spending intensity. This cohort remains important because it supports volume demand for mainstream graphics cards, gaming laptops, and mobile gaming hardware. The region's consumer profile is still heavily mobile-led, so many players enter the gaming hardware funnel through phones and then move gradually toward higher-performance devices. That keeps the installed base wide even when premium spending is concentrated among a smaller group.

Enthusiast and professional gamers are projected to record the fastest growth at a 13.66% CAGR from 2026 to 2031, and that shift is central to the premiumization taking place in the Asia-Pacific gaming GPU market. AMD reported record full-year 2025 revenue of USD 34.6 billion, up 34% year over year, with gaming demand from higher-frequency upgraders contributing to the broader momentum. Organized competition, creator workflows, and the need to run modern rendering features smoothly are pushing this group toward faster replacement cycles and higher price bands. The result is a clearer split between the buyers who drive unit volume and the buyers who drive revenue across the Asia-Pacific gaming GPU market.

By Memory Type: GDDR6X Holds The Strongest Premium Growth Position

GDDR6X is projected to post the fastest growth at a 13.93% CAGR through 2031, which places it at the premium end of the Asia-Pacific gaming GPU market size expansion. Its appeal comes from stronger bandwidth delivery in upper-mainstream and high-end gaming cards, where buyers want better performance without moving all the way into the most constrained product tiers. That makes GDDR6X well-suited to the part of the region where demand sits between affordability and premium visual quality. It also aligns with the continued strength of discrete cards in enthusiast desktops and gaming laptops.

The memory type is supported by a broad AIB ecosystem that includes ASUS, MSI, and Palit, which use cooling design, distribution reach, and bundled software to compete around the same core silicon platforms. Standard GDDR6 still anchors volume demand in emerging markets, but it faces pressure from above as GDDR6X becomes more accessible and from below as integrated and unified memory designs improve. Apple's M5 and new mobile graphics platforms show how unified memory and advanced on-chip graphics are redefining the lower boundary of what users can accept from non-discrete systems. That leaves GDDR6X in a favorable position inside the Asia-Pacific gaming GPU market, because it captures buyers seeking a clear performance step-up without relying on the most supply-sensitive frontier products.

Geography Analysis

China held the largest share of the Asia-Pacific gaming GPU market in 2025 and 2026, supported by its large installed gaming hardware base, strong PC cafe presence, and deep local board manufacturing network. The country also matters because domestic GPU development is no longer a side story and is becoming part of the long-term supply structure. Moore Threads used its MUSA 2025 developer summit to outline the Lushan and Huashan GPU architecture roadmap, including claims around DirectX 12 Ultimate support and full hardware ray tracing. At the same time, export compliance remains a constraint on the higher end of the addressable product range for China-bound supply. Japan and South Korea remain smaller country markets than China, but both support premium demand because replacement cycles are more established and performance expectations remain high.

India is the fastest-growing geography in the Asia-Pacific gaming GPU market over 2026-2031, helped by a widening user base, more formal gaming infrastructure, and better access to cloud-delivered high-quality play. Xbox Cloud Gaming expanded to India in November 2025 and identified the country as one of its most important growth markets, with usage up 45% year over year. Southeast Asia is developing along a dual path, because cloud access is expanding at the same time that urban consumers continue to buy local gaming hardware. Carrier-linked GPU cloud deployments in Vietnam and Thailand in 2026 showed how infrastructure partners were broadening access to premium gaming experiences without requiring immediate hardware ownership.

Australia, New Zealand, and the rest of Asia-Pacific track closer to Western premium hardware patterns, with stronger per-capita spending on high-performance gaming systems. Microsoft said in 2025 that it was expanding cloud infrastructure in Asia through new launches in Malaysia and Indonesia and planned expansions in India and Taiwan in 2026, which improves the regional backbone for cloud gaming and AI-assisted graphics workloads. The wider regional picture is therefore uneven, because mature markets mostly refresh existing hardware and emerging markets are still adding first-time buyers. That mix keeps the Asia-Pacific gaming GPU market broad based, but growth is increasingly shifting toward India, Southeast Asia, and sub-premium product tiers that balance performance with cost.

Competitive Landscape

The Asia-Pacific gaming GPU market remains highly concentrated at the silicon layer even though consumers see many retail brands on store shelves. NVIDIA sets the pace for product cycles, software features, and performance positioning across most of the discrete gaming space. AMD remains the only meaningful alternative in many APAC gaming builds, especially in DIY-oriented channels and value-focused performance tiers. Intel's Arc presence is still limited across the region and has not materially changed the competitive balance. AIB brands such as ASUS, MSI, ZOTAC, Palit, SAPPHIRE, TUL, and ASRock mostly compete through cooling, design, distribution, and bundled software rather than core silicon differentiation.

NVIDIA strengthened its software lead in 2026 through DLSS 4.5 and 6x Multi Frame Generation, which raised the practical value of RTX 50 Series hardware for buyers who want more frames without moving to the very highest price bands. AMD responded by bringing FSR 4 hardware-accelerated upscaling to older RDNA 3 and RDNA 3.5 cards, which was a clear attempt to improve the installed base proposition and limit switching pressure toward. ASUS kept pushing premium form factors, including the ROG NUC 16 and the ROG Strix SCAR 18, to capture buyers who want compact or mobile systems without giving up top-tier graphics capability. These moves show that the competitive fight in the Asia-Pacific gaming GPU market is increasingly shaped by software and system engineering, not only by raw chip specifications.

The clearest white space remains in the USD 250-400 discrete GPU bracket, where demand in India and Southeast Asia is real but supply and margin priorities have often favored higher-priced products. That leaves room for channel gains by vendors that can bring stable availability and strong software support into mid-range price points. China's domestic GPU push adds a longer-run risk to incumbent suppliers, because Moore Threads has moved beyond proof-of-concept positioning and is trying to build a fuller gaming stack around its own architecture roadmap. Even so, the near-term competitive center of gravity in the Asia-Pacific gaming GPU market is still defined by NVIDIA's platform lead, AMD's selective pressure in value segments, and the execution ability of AIB and OEM partners across local retail channels.

Asia-Pacific Gaming GPU Industry Leaders

NVIDIA Corporation

Qualcomm Technologies, Inc.

Advanced Micro Devices, Inc.

Apple Inc.

MediaTek Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: ASUS announced the ProArt GeForce RTX 5090 in Malaysia, a professional-grade 2.5-slot Blackwell card targeting creators and AI developers, with Malaysian retail availability expected in June 2026. The launch signals the convergence of professional AI workload and gaming GPU infrastructure among APAC's creator-consumer segment.

- May 2026: ASUS Republic of Gamers announced the ROG NUC 16, a compact gaming PC powered by up to an NVIDIA GeForce RTX 5080 Laptop GPU with support for DLSS 4.5 machine learning-based frame generation. The product targets APAC consumers seeking desktop-class GPU performance in a form factor suitable for living room and small-space gaming configurations.

- May 2026: ASUS ROG announced the Strix SCAR 18 (2026), a flagship gaming laptop powered by up to an NVIDIA GeForce RTX 5090 Laptop GPU at 320W sustained total system power, establishing a new performance ceiling for APAC gaming laptop hardware. The product is positioned as a benchmark configuration for competitive and enthusiast APAC gaming consumers through 2027.

- January 2026: The U.S. BIS issued a final rule revising export licensing for advanced computing semiconductors, including the NVIDIA H200 and AMD MI325X, to China and Macau, shifting from a presumption of denial to case-by-case review under strict compliance conditions including U.S. third-party testing and KYC safeguards. The rule indirectly affects gaming GPU procurement channels for China-based hardware vendors operating in the same supply chain.

Asia-Pacific Gaming GPU Market Report Scope

The Asia-Pacific Gaming GPU Market refers to the market for graphics processors used in gaming PCs, laptops, consoles, and cloud gaming systems across Asia-Pacific countries. These GPUs are designed to speed up image rendering, support high frame rates, and handle large volumes of data in parallel for smoother and more immersive gameplay.

The Asia-Pacific Gaming GPU Market Report is Segmented by GPU Type (Discrete GPUs, and Integrated GPUs), Device Type (Gaming Desktops, Gaming Laptops, and Smartphones and Tablets (Mobile Gaming)), End-User Type (Casual Gamers, and Enthusiast and Professional Gamers), Memory Type (GDDR6, GDDR6X, Other Memory Types, and Unified Memory), and Country. The Market Forecasts are Provided in Terms of Value (USD).

| Discrete GPUs |

| Integrated GPUs |

| Gaming Desktops |

| Gaming Laptops |

| Smartphones and Tablets (Mobile Gaming) |

| Casual Gamers |

| Enthusiast and Professional Gamers |

| GDDR6 |

| GDDR6X |

| Legacy Graphics Memory |

| Unified Memory |

| By GPU Type | Discrete GPUs |

| Integrated GPUs | |

| By Device Type | Gaming Desktops |

| Gaming Laptops | |

| Smartphones and Tablets (Mobile Gaming) | |

| By End-User Type | Casual Gamers |

| Enthusiast and Professional Gamers | |

| By Memory Type | GDDR6 |

| GDDR6X | |

| Legacy Graphics Memory | |

| Unified Memory |

Key Questions Answered in the Report

What is the current and forecast value of the Asia-Pacific gaming GPU market?

The Asia-Pacific gaming GPU market was valued at USD 18.66 billion in 2025, is projected at USD 22.04 billion in 2026, and is forecast to reach USD 39.66 billion by 2031 at a 12.47% CAGR.

Which device category leads spending across the region?

Gaming desktops led the device mix with a 45.61% share in 2025, supported by upgradeable systems and strong demand from gaming venues and dedicated PC users.

Which end-user group is growing the fastest?

Enthusiast and professional gamers are expected to grow the fastest, at a 13.66% CAGR from 2026 to 2031, because they upgrade more often and spend more on premium performance.

Why are mid-tier graphics cards becoming more attractive in APAC?

AI upscaling and frame generation have improved the practical output of mid-range hardware, which makes performance gains more accessible in price-sensitive markets.

Why is India becoming such an important growth area?

India combines a broad gaming base, improving infrastructure, and expanding cloud gaming access, which supports both first-time premium users and later hardware upgrades.

What is shaping competition among GPU vendors and AIB brands?

Core competition is still set by NVIDIA and AMD at the silicon level, but retail execution depends heavily on software features, cooling design, product form factor, and local channel strength.

Page last updated on: