Europe GPU Immersion Cooling Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

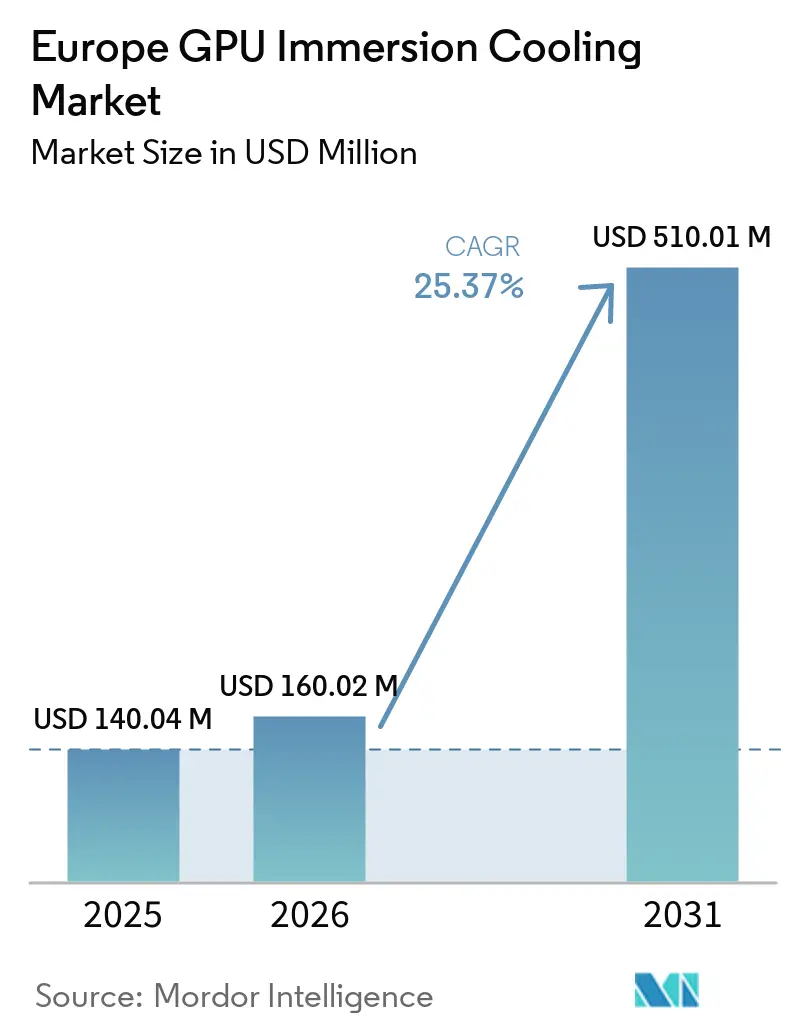

| Base Year Market Size (2025) | USD 140.04 Million |

| Market Size (2026) | USD 160.02 Million |

| Market Size (2031) | USD 510.01 Million |

| Growth Rate (2026 - 2031) | 25.37% CAGR |

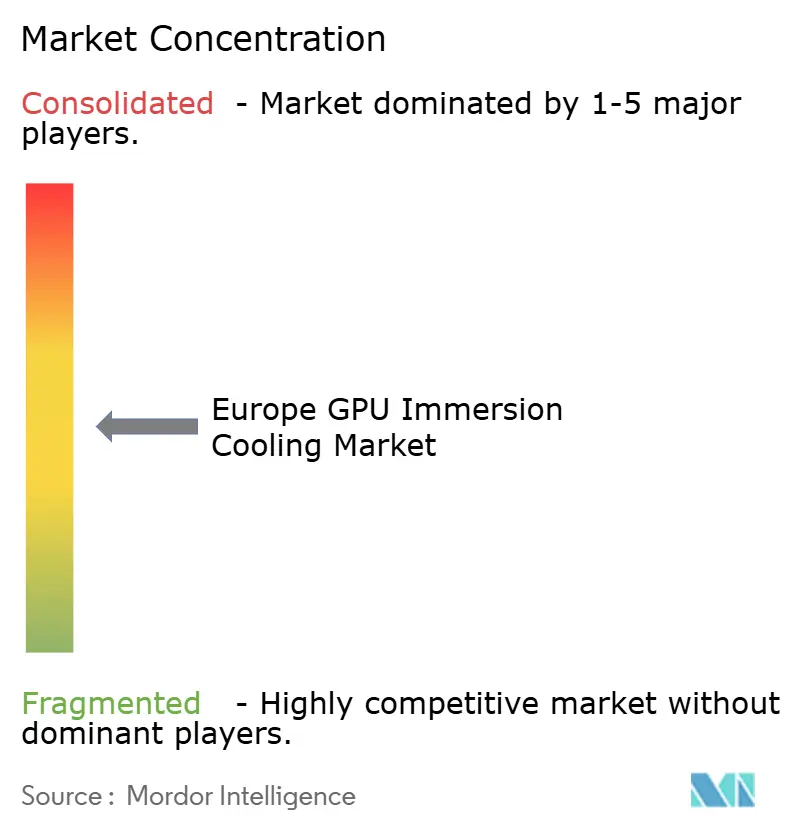

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe GPU Immersion Cooling Market Analysis by Mordor Intelligence

The Europe GPU immersion cooling market size is expected to be USD 140.04 million in 2025, USD 160.02 million in 2026, and reach USD 510.01 million by 2031, growing at a CAGR of 25.37% from 2026 to 2031. Steadily climbing rack densities above 100 kilowatts, escalating electricity tariffs, and mandatory efficiency reporting have combined to make immersion cooling the preferred path for next-generation AI and high-performance computing clusters. Although only a small minority of European facilities had fully submerged servers by late 2025, nearly half had already introduced other forms of direct liquid cooling, signalling an addressable pipeline that will expand as GPU power envelopes move beyond 700 watts. Germany’s hyperscale expansions, France’s sovereign-AI mandates, and a wave of EuroHPC projects are anchoring regional demand, while a widening set of turnkey server SKUs lowers integration risk for enterprises that lack in-house thermal-engineering expertise.

Key Report Takeaways

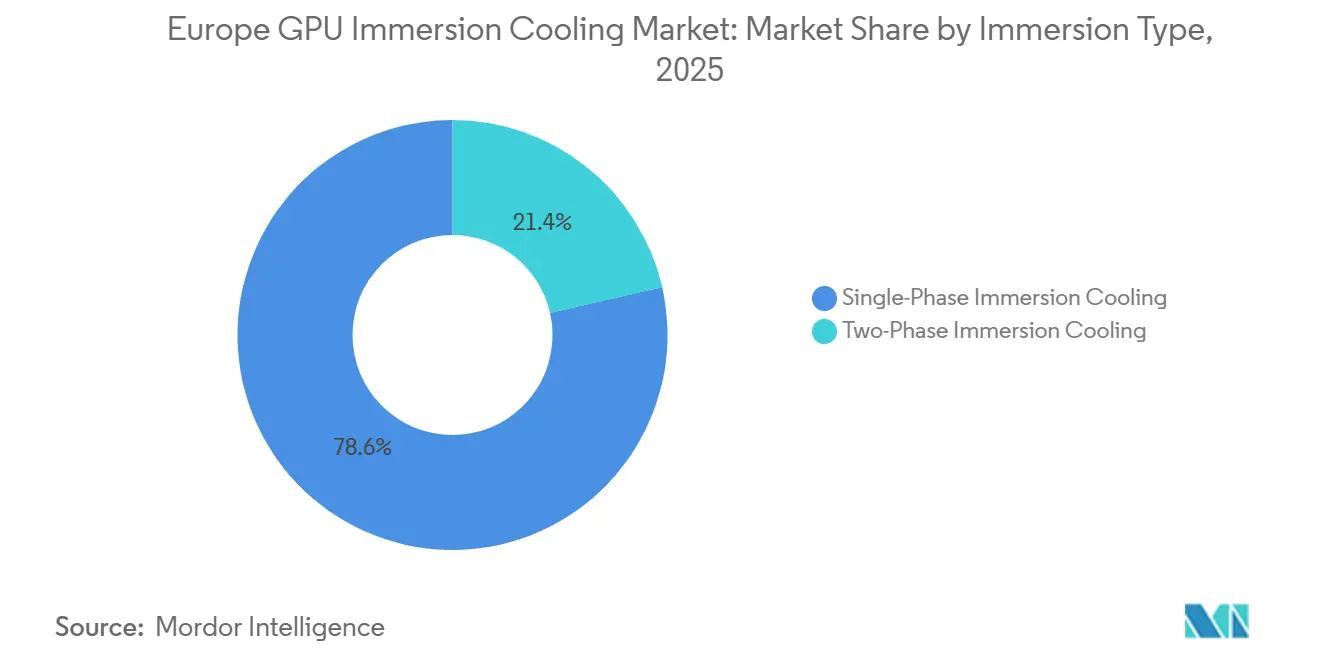

- By immersion type, single-phase systems led with 78.56% of revenue in 2025, while two-phase configurations are projected to advance at a 25.55% CAGR through 2031.

- By solution type, tanks and ancillary systems captured 55.34% of 2025 spend, whereas immersion-optimized GPU servers are forecast to post the fastest growth at 25.63% during 2026-2031.

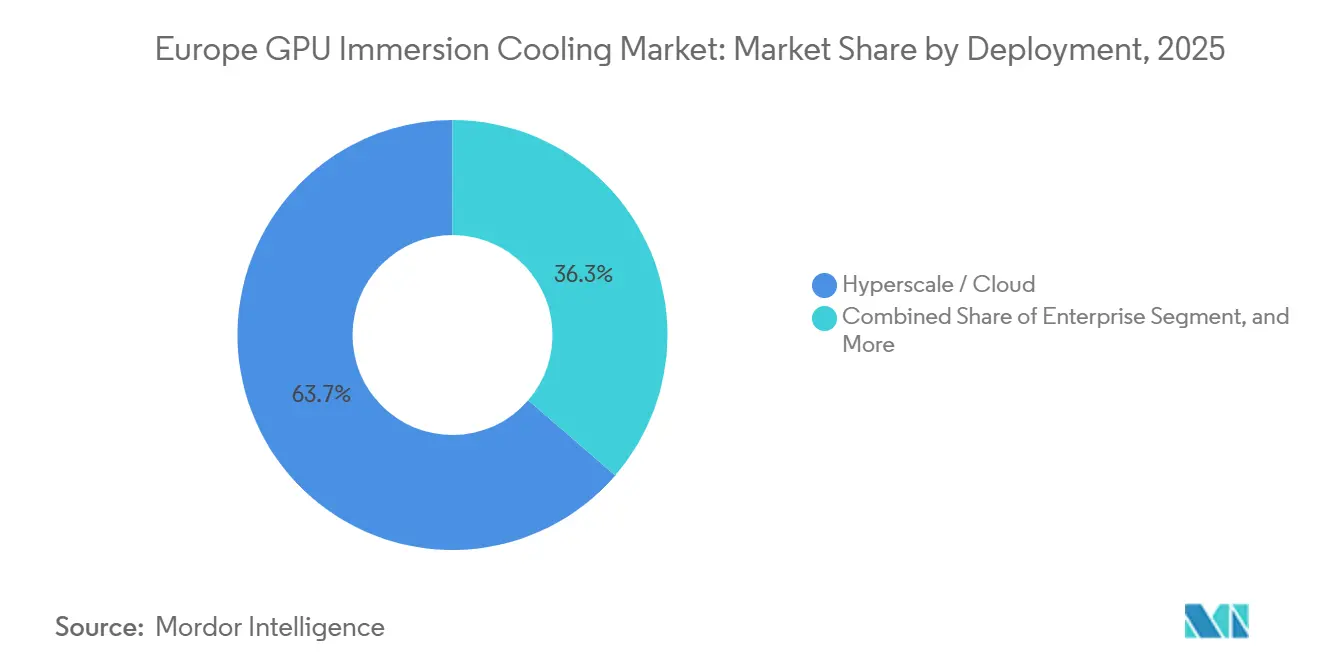

- By deployment, hyperscale and cloud sites accounted for 63.67% of revenue in 2025; the enterprise segment is on track for a 25.68% CAGR as urban data-center operators retrofit space-constrained facilities.

- By GPU power density, the 300-watt-to-700-watt bracket held 51.34% of 2025 sales and the above-700-watt bracket is expected to expand at 25.74% through 2031.

- By region, Germany controlled 27.34% of 2025 revenue while France is set to grow fastest at 26.05% on the back of exascale and sovereign-AI initiatives.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe GPU Immersion Cooling Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging AI and HPC Workloads Driving Higher‑Density GPU Deployments | +8.5% | Key markets including Germany, France, the Netherlands, and the United Kingdom | Medium term (2-4 years) |

| EU Data‑Center Sustainability Regulations and Carbon‑Reduction Targets | +6.2% | Western Europe, driven by EU‑wide climate policies | Long term (≥ 4 years) |

| Escalating Electricity Prices Encouraging Energy‑Efficient Cooling Adoption | +5.1% | Germany, Italy, the United Kingdom, and Belgium | Short term (≤ 2 years) |

| Rapid Decline in Dielectric Fluid Costs | +3.4% | Pan‑European impact across both hyperscale and colocation markets | Medium term (2-4 years) |

| Increased Venture Funding for European Immersion Cooling Startups | +1.6% | Innovation hubs in the Netherlands, Spain, the United Kingdom, and Poland | Short term (≤ 2 years) |

| Growing Preference for Edge Data Centers in Urban Europe | +0.9% | Major metropolitan areas across Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging AI and HPC Workloads Driving Higher-Density GPU Deployments

Generative-AI training racks built around NVIDIA H100 and H200 accelerators routinely exceed 120 kilowatts, a level that outstrips the economic ceiling of raised-floor air cooling.[1]NVIDIA Corporation, “NVIDIA Investor Relations,” investor.nvidia.com National and pan-European research initiatives have funded billion-euro infrastructure projects that specify liquid cooling from day one, creating reference blueprints that enterprises can emulate. EuroHPC-backed supercomputers in Hungary and Sweden, both announced in 2025, openly mandate immersion-ready designs to cope with petaflop-scale heat loads. These flagship systems reinforce a virtuous cycle of volume commitments that lower technology risk for commercial buyers. As the forthcoming B-series GPU family pushes individual chip power past 1 kilowatt, immersion transitions from an experimental option to a necessity for maintaining rack throughput without a parallel rise in facility power.

EU Data Center Sustainability Regulations and Carbon Targets

The delegated regulation under the Energy Efficiency Directive compels sites above 500 kilowatts to publish annual power-usage-effectiveness and water-usage-effectiveness metrics beginning in 2025, a disclosure regime that favors immersion-equipped plants achieving PUE near 1.05.[2]European Commission, “EU Delegated Regulation on Data Center Energy Efficiency,” ec.europa.eu Parallel commitments under the Climate Neutral Data Centre Pact demand net-zero operations by 2030, effectively hard-coding liquid cooling into expansion blueprints. Operators such as Asperitas have demonstrated single-phase designs that deliver coolant temperatures high enough for direct district-heating export, addressing waste-heat clauses within the Pact. Newly approved IEC standards covering natural-ester dielectric fluids provide certification pathways that streamline tender procedures, further accelerating adoption.

Escalating Electricity Prices in Western Europe Encouraging Energy-Efficient Cooling

Non-household power averaged EUR 0.1902 (USD 0.205) per kilowatt-hour in 2025, but exceeded EUR 0.27 (USD 0.291) in Germany, turning energy savings into a primary return-on-investment lever.[3]Eurostat, “Electricity Prices for Non-Household Consumers, 2025,” ec.europa.eu/eurostat Immersion can trim facility-level consumption by up to 3 megawatts for every 10-megawatt IT load, translating into seven-figure annual savings in high-tariff markets. Independent TCO models for a 12-megawatt facility in Rotterdam showed 50% footprint reduction and USD 75.6 million in operating savings over 10 years versus air cooling. These economics resonate most in urban Germany and northern Italy, where expensive real estate and grid constraints co-exist with aggressive sustainability targets.

Rapid Decline in Dielectric Fluid Costs

Shell, ExxonMobil, and Perstorp each launched sub-USD 100-per-liter fluids between 2025 and 2026, shrinking one of immersion’s historical cost barriers. Fluid lifespan now extends beyond 15 years, cutting annualized expense to the low-thousands of dollars per tank. Intel, Dell, and other OEMs have published compatibility matrices that shorten validation cycles, enabling bulk-purchase contracts that further depress unit prices. Lower fluid overheads open the door for mid-market enterprises and edge operators that previously viewed immersion as financially prohibitive.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Up‑Front CAPEX Compared to Traditional Air Cooling | −4.8% | Pan‑European across hyperscale and colocation facilities | Short term (≤ 2 years) |

| Limited Availability of GPU‑Qualified, Immersion‑Ready Warranty Support | −3.2% | EU‑wide, affecting enterprise and hyperscale adoption | Medium term (2-4 years) |

| Fragmented Dielectric Fluid Standards Across European Union Markets | −1.7% | Cross‑border deployments within the EU | Medium term (2-4 years) |

| Supply‑Chain Constraints for High‑Performance Immersion Tanks and Sealing Components | −0.9% | Core markets including Germany, France, the Netherlands, and the United Kingdom | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Up-Front Capex Versus Traditional Air Cooling

Turnkey immersion racks cost USD 30,000-50,000, dwarfing the USD 1,000-2,000 price of a conventional rack, even though whole-facility comparisons can favor immersion when scale effects are considered. Retrofit pilots often face a 40% cost premium because owners must re-plumb chilled-water loops, upgrade floor loading, and commission dielectric-compatible monitoring systems. Cash-constrained enterprises that operate under three-year payback rules struggle to reconcile those economics, particularly when incremental air-cooling upgrades deliver near-term relief. Cooling-as-a-service and leasing schemes are emerging but remain embryonic, limiting near-term impact on capital allocations.

Limited Availability of GPU-Qualified Immersion-Ready Warranties

Most server OEM guarantees do not automatically cover submerged deployments, forcing end users to navigate custom qualification regimes that can stretch procurement cycles by half a year. While the OCP warranty template published in 2024 established baseline test procedures, NVIDIA’s H100 and H200 units still require case-by-case approval. Enterprise buyers in regulated sectors such as finance and healthcare often demand blanket warranty alignment, so lengthened qualification windows translate into delayed revenue recognition for solution providers. Partnerships like the February 2026 agreement between Asperitas and UNICOM Engineering illustrate how bundled server-plus-tank offerings can ease that pain point. Nonetheless, until GPU vendors issue default immersion coverage, perception of risk will continue to cap adoption in conservative verticals.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Immersion Type: Single-Phase Dominance Reflects Risk Aversion

Single-phase immersion cooling held 78.56% of the Europe GPU immersion cooling market share in 2025, underscoring widespread confidence in its fluid stability and simple operations. The Europe GPU immersion cooling market size tied to single-phase designs is expanding steadily as suppliers such as Shell and Perstorp bring PFAS-free hydrocarbon fluids to market, reducing both cost and regulatory risk. Enterprises value the compatibility of these systems with existing chilled-water loops, a factor that shortens retrofit timelines. In urban edge sites, pumpless natural-convection variants demonstrated by Asperitas are proving attractive because they operate quietly and generate 55-degree-Celsius outlet temperatures suitable for district heating.

Two-phase systems are on track for a 25.55% CAGR through 2031, yet they remain concentrated in hyperscale and research settings where rack densities cross 150 kilowatts. Fluorocarbon fluid loss, pressure-control complexity, and specialised seals have limited penetration outside those niches. The CoolHeatDC project, co-funded by SINTEF, aims to commercialise two-phase modules tied directly to heat pumps, a configuration that could broaden appeal if field trials validate maintenance expectations. As GPUs inch toward 1 kilowatt per device, two-phase designs will likely capture incremental share, though single-phase is set to maintain the majority position for the remainder of the decade.

By Solution Type: Integrated Servers Close the Procurement Gap

Tanks and heat-exchange systems represented 55.34% of the Europe GPU immersion cooling market size in 2025 because early adopters sourced enclosures and servers separately. That procurement model is shifting as Dell, Hewlett Packard Enterprise, Lenovo, and Supermicro release immersion-optimized SKUs that bundle server chassis, cold plates, and certified fluid compatibility. Europe GPU immersion cooling industry observers note that these turnkey offers compress deployment cycles and eliminate warranty disputes, positioning integrated servers for the strongest growth at 25.63% through 2031.

Fluid suppliers are differentiating through sustainability metrics, with Perstorp’s PFAS-free Synmerse range and Oleon’s plant-based formulations highlighting the trend. Tank manufacturers such as DCX and Baltimore Aircoil have responded by publishing standardised module footprints, cutting lead times to under two months for high-volume orders. Analysts expect that once server OEMs finish extending liquid-ready lines across their full GPU portfolios, the balance of revenue will tilt toward integrated systems, while standalone tanks will retain relevance for hyperscale custom builds and facility retrofits.

By Deployment: Enterprises Take Center Stage

Hyperscale platforms captured 63.67% of revenue in 2025, yet the enterprise cohort is forecast to expand at a 25.68% CAGR, outpacing cloud operators. A growing number of banks, automakers, and pharmaceutical firms are installing immersion tanks in confined city footprints to avoid costly site expansions. Germany’s high-tariff market in particular incentivises immersion retrofits that convert power savings into sub-two-year payback intervals. Those economics underpin the decision by Intermax to pilot cassette-based enclosures at NorthC’s Rotterdam campus, an approach likely to be replicated in other metropolitan hubs.

Government and research HPC facilities continue to progress, but their share of the Europe GPU immersion cooling market will increase more modestly because most tier-one projects have already committed budgets. Hyperscale purchasers, meanwhile, negotiate bespoke fluid formulas and tank geometries to suit campus-level energy-recovery schemes. The contrasting procurement styles suggest that vendors capable of straddling both off-the-shelf enterprise packages and made-to-order hyperscale contracts will be best placed to ride the next demand wave.

By GPU Power Density: Above-700-Watt Bracket Gains Momentum

The 300-watt-to-700-watt class retained 51.34% of revenue in 2025 due to the installed base of NVIDIA A100 and early H100 rollouts. Yet the above-700-watt tier is projected to log a 25.74% CAGR as NVIDIA’s H200, forthcoming B-series accelerators, and AMD’s MI300 family push thermal profiles into air-cooling exclusion zones. Operators deploying NVL72 racks rated at 120 kilowatts are effectively forced to select immersion or advanced cold-plate liquid lines.

Vendors such as Panasonic and KAYTUS launched coolant distribution units and 100-cabinet reference builds in early 2026 to serve this ultra-dense segment. Below-300-watt GPUs will continue to rely on rear-door exchangers or air cooling, but that slice of the Europe GPU immersion cooling market is expected to erode as AI inference workloads migrate onto more efficient silicon.

Geography Analysis

Germany’s hold over the Europe GPU immersion cooling market stems from Frankfurt’s dense cluster of more than 1,000 facilities, sustained hyperscale construction, and aggressive carbon goals that push operators toward sub-1.2 PUE designs. Deutsche Telekom’s USD 1.13 billion AI program emphasises immersion as a path to meet its 2030 neutrality pledge, while AtlasEdge’s urban edge deployment in Leverkusen proves that fully submerged racks can coexist with stringent space and noise limitations.

Across the Channel, the United Kingdom is accelerating liquid-cooling adoption through the GBP 11 billion National AI Research Resource, which allocated funds to Durham University’s immersion-equipped HPC in 2025 and to Imperial College London’s project with Digital Realty in early 2026. Channel integrators such as Computacenter have partnered with technology providers to build turnkey offerings, broadening access for public-sector bodies and mid-market enterprises.

France, Italy, and the Netherlands each combine policy and economic triggers. Paris-based AI Green Bytes employed plant-based dielectric fluid to satisfy environmental objectives, while Brescia’s Qarnot-A2A venture illustrates how immersion tanks can double as district-heating assets in southern Europe. The Netherlands continues to champion waste-heat reuse mandates that align neatly with immersion’s high outlet temperatures. Spain, Belgium, and Poland form the growth fringe: Barcelona’s planned BCN 01 campus will open with immersion-ready halls, Belgium’s elevated tariffs sustain clear power-offset incentives, and Polish manufacturer DCX underpins regional supply by adding an 8-megawatt fluid distribution unit factory line.

Competitive Landscape

The vendor field remains moderately fragmented, with no company holding more than 15 percent of revenue. European pioneers Submer, Asperitas, and Iceotope compete with North American challengers such as Green Revolution Cooling and LiquidStack, the latter now owned by Trane Technologies after a February 2026 purchase. Consolidation among traditional HVAC majors continues: Schneider Electric closed its Motivair acquisition in 2025; Vertiv bought PurgeRite in December 2025 and STL in April 2026; and Ecolab folded CoolIT into its water-treatment arm for USD 4.75 billion in March 2026.

Partnership activity is equally intense. Dell, Hewlett Packard Enterprise, Lenovo, and Supermicro each rolled out immersion-ready GPU servers between 2024 and 2026, bundling hardware with certified fluid matrices to simplify warranty compliance. Asperitas secured UNICOM Engineering as a single-contract integrator, while Submer signed UK-focused distribution deals with Hammer and Boston Ltd. Fluid innovators such as Perstorp and Oleon differentiate on PFAS-free chemistry, anticipating tightening EU standards.

Technical roadmaps increasingly focus on heat reuse and modularity. Asperitas champions a pumpless convection tank producing 55-degree-Celsius coolant for district networks, and SINTEF’s CoolHeatDC two-phase platform couples evaporative modules to industrial heat pumps. Vendors that can package these innovations into factory-assembled, warranty-harmonized solutions are expected to gain ground as enterprises without in-house engineering depth enter the market.

Europe GPU Immersion Cooling Industry Leaders

Submer Technologies SL

Asperitas BV

Iceotope Technologies Limited

Green Revolution Cooling Inc.

Schneider Electric SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: The Open Compute Project released Immersion Requirements Rev. 2.1, standardizing fluid and tank certifications across Europe.

- April 2026: Accelsius and Computacenter agreed to jointly market immersion solutions to UK public-sector and enterprise clients.

- April 2026: Vertiv finalised its purchase of STL, deepening its liquid-cooling portfolio after the PurgeRite deal four months earlier.

- March 2026: Panasonic unveiled modular coolant distribution units and chillers for racks surpassing 700 watts per GPU.

Europe GPU Immersion Cooling Market Report Scope

The Europe GPU Immersion Cooling Market pertains to the regional industry segment in Europe dedicated to the adoption and development of immersion cooling technologies for Graphics Processing Units (GPUs).

The Europe GPU Immersion Cooling Market Report is Segmented by Immersion Type (Single-Phase, Two-Phase), Solution Type (Tanks/Systems, Dielectric Fluids, Immersion-Optimized GPU Servers), Deployment (Hyperscale/Cloud, Enterprise, Government and Research HPC), GPU Power Density (Below 300W, 300W-700W, Above 700W), and Geography (Germany, United Kingdom, France, Italy, Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

| Single-Phase Immersion Cooling |

| Two-Phase Immersion Cooling |

| Immersion Cooling Tanks / Systems |

| Dielectric Fluids |

| Immersion-Optimized GPU Server Systems |

| Hyperscale / Cloud |

| Enterprise |

| Government and Research (HPC) |

| Below 300W |

| 300W - 700W |

| Above 700W |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe |

| By Immersion Type | Single-Phase Immersion Cooling | |

| Two-Phase Immersion Cooling | ||

| By Solution Type | Immersion Cooling Tanks / Systems | |

| Dielectric Fluids | ||

| Immersion-Optimized GPU Server Systems | ||

| By Deployment | Hyperscale / Cloud | |

| Enterprise | ||

| Government and Research (HPC) | ||

| By GPU Power Density | Below 300W | |

| 300W - 700W | ||

| Above 700W | ||

| By Region | Europe | Germany |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

Key Questions Answered in the Report

What is the current value of the Europe GPU immersion cooling market?

The Europe GPU immersion cooling market is valued at USD 160.02 million in 2026 and is projected to reach USD 510.01 million by 2031, reflecting a 25.37% CAGR (2026-2031).

How fast are two-phase immersion systems growing in Europe?

Two-phase immersion cooling systems are expected to grow at a 25.55% CAGR through 2031, driven by high-density racks exceeding 150 kW and the need to achieve PUE below 1.05.

Which country is expected to record the fastest growth through 2031?

France is projected to grow at a 26.05% CAGR, supported by sovereign AI initiatives and projects such as the Alice Recoque exascale program.

Why are enterprises adopting immersion cooling more quickly now?

Adoption is accelerating due to turnkey server SKUs with integrated warranties, rising urban electricity costs, and the need to avoid expensive data-center expansions, leading to a projected 25.68% CAGR for enterprise adoption.

What is the main cost barrier to wider immersion deployment?

High upfront capital expenditure remains the key barrier, typically 15-25× higher than traditional rack systems, despite lower long-term operating costs.

Which vendors recently strengthened their immersion cooling portfolios?

Companies such as Vertiv, Ecolab, and Trane Technologies have expanded their capabilities through acquisitions since 2025, adding immersion tanks, fluid management solutions, and full system offerings to their portfolios.

Page last updated on: