North America GPU Immersion Cooling Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

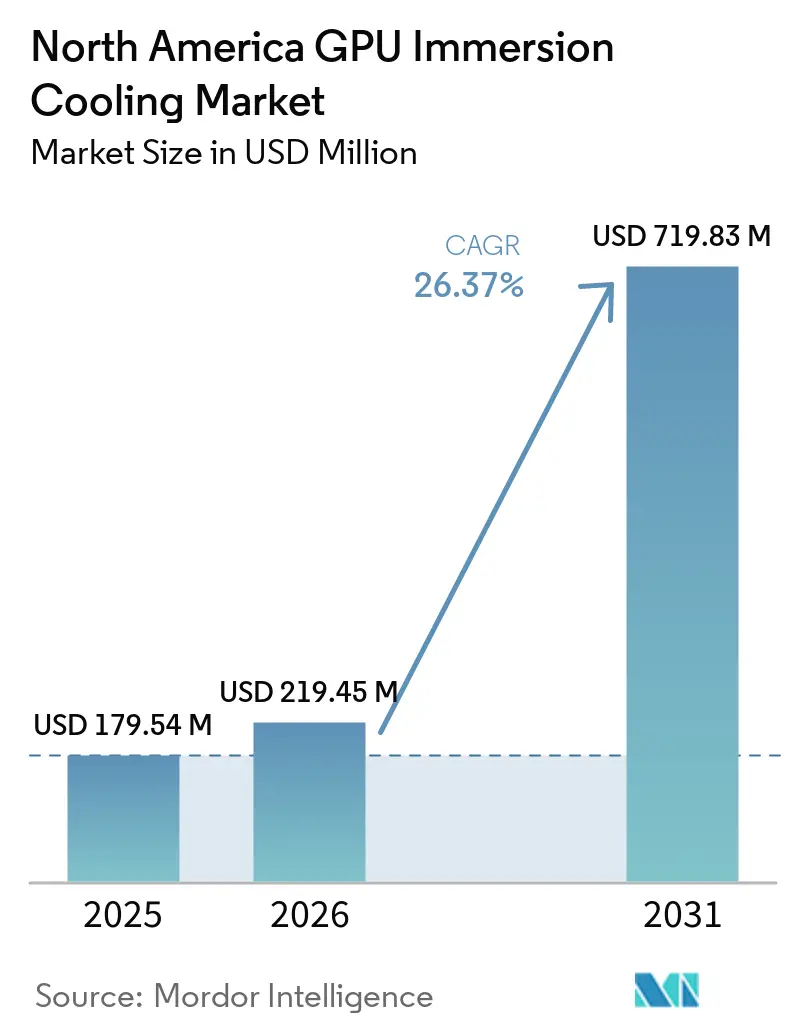

| Base Year Market Size (2025) | USD 179.54 Million |

| Market Size (2026) | USD 219.45 Million |

| Market Size (2031) | USD 719.83 Million |

| Growth Rate (2026 - 2031) | 26.37% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America GPU Immersion Cooling Market Analysis by Mordor Intelligence

The GPU immersion cooling market size is expected to increase from USD 179.54 million in 2025 and USD 219.45 million in 2026 to USD 719.83 million by 2031, growing at a CAGR of 26.37% over 2026-2031. Hyperscale operators are scaling 100-kilowatt-plus racks for generative AI clusters, and enterprise retrofit activity is compressing payback periods as electricity tariffs rise. Dielectric-fluid shortages following 3M’s exit are nudging buyers toward long-term supply contracts, while Open Compute Project (OCP) standardization has trimmed 30% from hardware switching costs. As two-phase designs become viable for inference workloads, fluid suppliers and condenser-loop specialists are jockeying to secure preferred-vendor status with GPU original equipment manufacturers (OEMs). Growing heat-reuse incentives and federal power-usage-effectiveness (PUE) mandates are further catalyzing adoption of immersion architectures across North America.

Key Report Takeaways

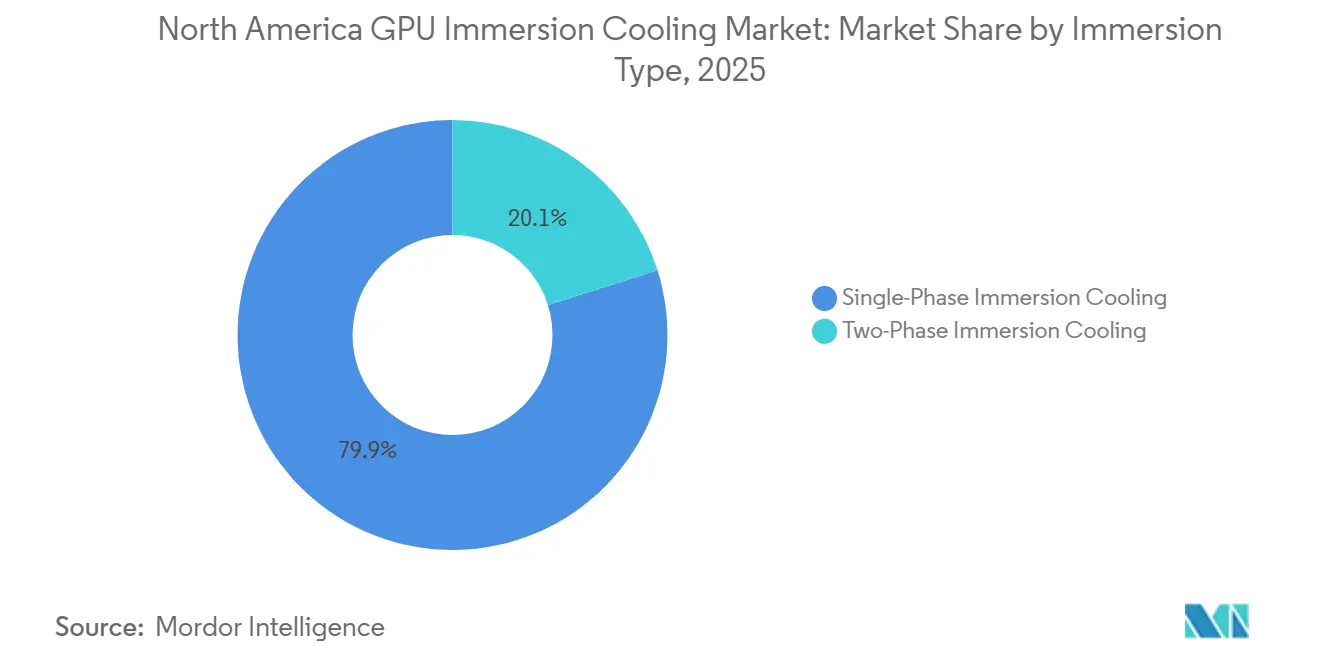

- By immersion type, single-phase solutions held 79.87% revenue share in 2025, while two-phase systems are projected to expand at 26.44% CAGR through 2031.

- By solution type, tanks and systems captured 55.23% of 2025 spending, whereas immersion-optimized GPU server platforms are advancing at a 26.56% CAGR to 2031.

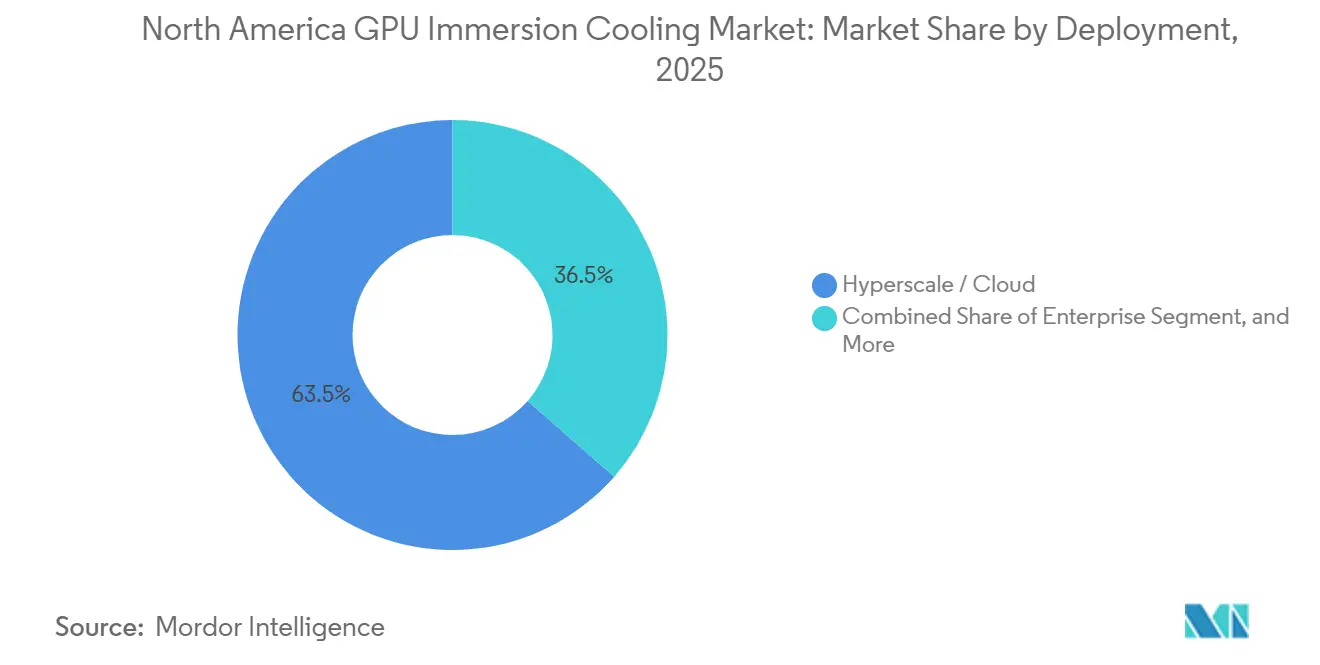

- By deployment, hyperscale and cloud installations delivered 63.54% revenue share of the North America (NA) GPU immersion cooling market size in 2025, but enterprise retrofits are the fastest-growing use case at 26.74% CAGR through 2031.

- By GPU power density, the 300-watt to 700-watt class commanded 51.22% share of the North America GPU immersion cooling market size in 2025, yet accelerators above 700 watts will post the highest 26.56% CAGR to 2031.

- By region, the United States secured 86.45% share of the NA GPU immersion cooling market share in 2025, though Canada is on track for the quickest 26.66% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America GPU Immersion Cooling Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Demand for High‑Density GPU Compute for Generative AI Workloads | +8.2% | North American AI corridors, including Northern Virginia, Silicon Valley, and Québec | Short term (≤ 2 years) |

| Expanding Deployment of Liquid‑Cooled Hyperscale Data Centers by U.S. Cloud Providers | +6.5% | United States, with spillover into Canada and Mexico near‑shore data‑center hubs | Medium term (2-4 years) |

| Energy‑Efficiency Regulations by the U.S. Department of Energy Targeting PUE Reductions | +4.8% | U.S. federal projects and key states such as California, Washington, and New York | Medium term (2-4 years) |

| Vendor‑Led Open Hardware Standards (e.g., OCP Advanced Cooling Solutions) Accelerating Adoption | +3.6% | Global, with early traction among U.S. hyperscalers and Canadian colocation providers | Long term (≥ 4 years) |

| Rising Electricity Tariffs in Northern Virginia and Silicon Valley | +2.1% | Dominion Energy and PG&E service territories | Short term (≤ 2 years) |

| Heat‑Reuse Incentives Supporting Data‑Center Waste‑Heat Recovery | +1.3% | Canadian municipalities in Québec, Ontario, and British Columbia with district‑heating infrastructure | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for High-Density GPU Compute for Generative AI Workloads

Training and inference clusters are already fielding NVIDIA H100 GPUs rated at 700 watts, and the leap to 1,000-watt Blackwell B200 silicon pushes rack power toward 120 kilowatts. Immersion cooling allows operators to crest these density thresholds without chiller upgrades, keeping PUE near 1.1. xAI’s Memphis supercomputer reached 100,000 liquid-cooled H100S and logged a PUE of 1.09, setting a performance baseline other hyperscalers now chase.[1]Data Center Dynamics staff, “xAI Deploying Massive Liquid-Cooled Supercomputer in Memphis,” datacenterdynamics.com With trillion-parameter language models standardizing, even enterprise labs accept that air cooling throttles utilization, cementing immersion as the pragmatic path to GPU (Graphics Processing Unit) saturation.

Expanding Deployment of Liquid-Cooled Hyperscale Data Centers by U.S. Cloud Providers

Amazon, Microsoft, Google, and Oracle have each publicized liquid-cooling roadmaps that convert every new availability zone after 2025 into either direct-to-chip or immersion builds. CoreWeave’s 300-megawatt Québec campus illustrates the economic upside of combining immersion tanks with district heating loops, offsetting cooling costs through municipal energy sales. These high-profile commitments reassure CFOs that immersion is not an experiment but an industry baseline, strengthening the upgrade narrative inside Fortune 500 IT departments.

Energy-Efficiency Regulations by U.S. Department of Energy Targeting PUE Reductions

In 2024, the Department of Energy established a best-practice guideline that sets a maximum Power Usage Effectiveness (PUE) of 1.15 for data halls receiving federal funding. Additionally, California's updates to Title 24 introduce depreciation penalties for air-cooled facilities that exceed a PUE of 1.4, creating a financial disincentive for less efficient cooling systems. In contrast, Washington State has implemented tax rebate incentives for data centers that achieve a PUE below 1.2, encouraging the adoption of more energy-efficient technologies. These regulatory measures collectively shift the total cost of ownership dynamics in favor of immersion cooling solutions, particularly in areas where wholesale electricity rates are on the rise, further enhancing the economic viability of such systems in the NA Graphics Processing Unit immersion cooling market.

Vendor-Led Open Hardware Standards Accelerating Adoption

OCP has introduced standardized tank footprints and fluid connectors as part of its 2024 immersion cooling requirements. This initiative is designed to enhance operational efficiency and provide buyers with greater flexibility by enabling compatibility across multiple vendors. By standardizing these components, OCP has also streamlined processes, significantly reducing qualification cycles and accelerating deployment timelines. Intel has further validated the credibility of this approach by offering a warranty rider specifically for single-phase immersion cooling deployments that utilize Shell's DLC S3 fluid. This endorsement underscores the reliability and effectiveness of the OCP framework in addressing industry needs. Furthermore, Taiwanese Original Design Manufacturers (ODMs), such as Wiwynn, have capitalized on this development by introducing white-box immersion trays at highly competitive double-digit discounts. This strategic pricing approach not only lowers the entry barrier for potential adopters but also drives increased adoption rates, thereby contributing to the rapid growth and expanding demand within the NA GPU immersion cooling market.[2]Open Compute Project, “Immersion Cooling Requirements Revision 2.1,” opencompute.org

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Availability of Synthetic Dielectric Fluids with UL and EPA Approvals | -3.2% | United States, with the strongest impact following the withdrawal of 3M Novec fluids | Short term (≤ 2 years) |

| Capital‑Intensive Retrofit Requirements for Legacy Enterprise Data Halls | -2.7% | Financial‑services and pharmaceutical campuses in major U.S. metropolitan areas | Medium term (2-4 years) |

| Uncertain Long‑Term GPU Warranty Policies for Two‑Phase Immersion Fluids | -1.5% | North American early adopters of boiling‑fluid and two‑phase immersion designs | Medium term (2-4 years) |

| Supply‑Chain Concentration of Immersion Tank Manufacturing in East Asia | -0.9% | North America, causing lead‑time extensions of up to ~16 weeks | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited Availability of Synthetic Dielectric Fluids with UL and EPA Approvals

In 2025, 3M announced its decision to exit the Novec product line, a move that significantly reduced the number of approved chemistries available in the market from seven to four. This reduction in options triggered a 40% increase in secondary-market pricing, creating additional cost pressures for operators. As a result, operators are now required to undergo a re-qualification process with alternative fluids supplied by Solvay, Chemours, or Shell. This process, which typically spans six to nine months, presents operational challenges and carries the potential risk of voiding GPU warranties unless vendors explicitly provide immersion riders to address compatibility concerns. Adding to these complexities, the Environmental Protection Agency (EPA) has implemented stricter thresholds for volatile organic compounds (VOCs), further limiting the range of candidate fluids available. These regulatory changes coincide with a surge in demand, intensifying supply constraints and creating a challenging environment for market participants.[3]Alliance Chemical, “Market Impact of 3M Novec Discontinuation,” alliancechemical.com

Capital-Intensive Retrofit Requirements for Legacy Enterprise Data Halls

Retrofitting raised-floor halls for immersion generally involves costs ranging from USD 800 to 1,200 per kilowatt, which is approximately three times the premium associated with constructing new facilities. These elevated costs arise primarily from the necessity to reinforce floor loads and comply with insurance carrier requirements to redesign sprinkler systems when Class IIIB combustible liquids are present on-site. Additionally, financial services towers located in seismic-prone areas such as New York and San Francisco face additional challenges. These include seismic-bracing surcharges that can reach up to USD 300,000 per installation, further extending the payback periods when compared to hyperscale greenfield projects.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Immersion Type: Two-Phase Systems Gain Despite Single-Phase Dominance

Single-phase designs captured 79.87% of 2025 North America GPU immersion cooling market revenue by leveraging simpler plumbing and broader fluid options. Enterprises favor atmospheric-pressure operation, while hyperscalers pilot two-phase tanks to chase sub-1.05 PUE targets and sub-ambient silicon temperatures. The NA Graphics Processing Unit immersion cooling market size for two-phase architectures is projected to climb steadily as warranty coverage matures and condenser automation trims maintenance overhead. Yet single-phase vendors retain an edge on ease of use, exemplified by GRC’s plug-and-play ICEraQ Series 3, which ships with recirculation and monitoring baked in.

Hyperscale buyers are willing to train technicians on boiling-fluid dynamics, expecting latency cuts that shave cost-per-inference. Submer’s SmartPodX Gen 2 already bundles vapor recovery and closed-loop condensers, positioning it for AI inference farms that prize every extra degree of cooling headroom. Meanwhile, Intel’s oil-based warranty rider signals OEM readiness to normalize single-phase deployments, but GPU manufacturers have yet to extend similar guarantees for two-phase chemistries, limiting some operators to pilot-scale deployments until broader warranty frameworks emerge.

By Solution Type: Optimized Server Systems Outpace Commodity Tanks

In 2025, tanks and ancillary infrastructure commanded 55.23% of revenue of the North America GPU immersion cooling market, but immersion-optimized servers are outrunning at a 26.56% CAGR through 2031. ODMs now pre-install thermal interface pads, fluid manifolds, and out-of-band sensors, avoiding costly field retrofits. For example, Supermicro’s DLC-3 platform supports 150-kilowatt racks and ships immersion-ready for H200, MI325X, and Gaudi 3 accelerators. As a result, the GPU immersion cooling market size tied to integrated server platforms will narrow the gap with tank revenue by the decade’s close.

Tanks continue to benefit from modular 50-kilowatt blocks that colocation landlords deploy incrementally, but fluid revenue is flattening as operators install on-site reclamation skid packages that extend service life by two years. Dielectric suppliers thus pivot to bundled analytics, embedding inline spectroscopy to upsell predictive-maintenance subscriptions, a move that keeps them tethered to the GPU immersion cooling market even as raw-fluid volumes plateau.

By Deployment: Enterprise Retrofit Wave Drives Fastest Growth

Hyperscalers owned 63.54% of 2025 spend, yet enterprise adoption shows the sharpest 26.74% CAGR outlook thanks to data-sovereignty mandates and rising colocation power rates. Banking and pharmaceutical operators previously constrained to 20-kilowatt racks now accelerate immersion retrofits to host on-premises generative AI clusters. The North America Graphics Processing Unit immersion cooling market share disparity will shrink as enterprises compress decision cycles from 18 months to six and negotiate volume discounts with integrators.

Government research labs add steady demand because the 1.15 PUE federal target leaves little room for air cooling in new builds. Hyperscalers keep their pricing edge by signing multiyear capacity deals with tank vendors, often locking in 20% hardware discounts. Yet tight lead times mean enterprise buyers increasingly leverage turnkey partners that package structural engineering, fire-suppression redesign, and staff training, services pure-play immersion firms historically overlooked.

By GPU Power Density: Ultra-High-Wattage Accelerators Reshape Cooling Economics

Graphics Processing Units in the 300 to 700 watt band still owned 51.22% of 2025 revenue of the North America GPU immersion cooling market, but devices above 700 watts will be the main engine of future growth. Accelerators such as Blackwell B200 and MI325X require cooling coefficients conventional air or cold-plate loops cannot reach, funneling procurement budgets into immersion systems purpose-built for 1000-watt TDP silicon. In contrast, sub-300-watt accelerators fade as operators decommission V100 and A100 clusters in favor of denser racks that extract greater performance per square foot.

NVIDIA’s GB200 NVL72 rack demonstrates the shift, shipping liquid cooling as the default solution and reinforcing that future accelerators will demand immersion readiness out of the box. The GPU immersion cooling market thus orients around above-700-watt skews, where each incremental watt amplifies thermal headroom complexity, making immersion cooling the economically rational choice.

Geography Analysis

The United States generated 86.45% of 2025 revenue of the North America GPU immersion cooling market and will grow at a 26.37% CAGR through 2031. Loudoun County in Northern Virginia and Santa Clara in Silicon Valley dominate because utilities embedded demand-charge penalties that punish inefficient cooling at more than USD 20 per kilowatt-month. Federal guidance capping PUE at 1.15 for new government data halls cements immersion cooling as the de facto standard for research supercomputers. Texas and the Carolinas are emerging contributors, leveraging cheap renewables and relaxed zoning to lure next-wave hyperscalers.

Canada exhibits the fastest 26.66% CAGR, buoyed by Québec’s Waste Heat Recovery program offering 75% capex rebates, up to CAD 40 million (USD 29.4 million), for immersion deployments that feed district heating. CoreWeave’s 300-megawatt campus will channel heat to 10,000 homes, saving CAD 12 million (USD 8.8 million) annually while showcasing circular-energy economics. Ontario and British Columbia replicate policy blueprints, stacking property-tax abatements onto hydroelectric power incentives to court AI workloads.

Mexico holds under 3% share but targets 25.8% CAGR as Querétaro and Monterrey carve out nearshore AI hubs. A 10-year property-tax holiday for facilities exceeding 50 megawatts and proving PUE below 1.2 signals political commitment, though dielectric-fluid import permits add friction. Proximity to Texas grid interconnects and established electronics manufacturing attract U.S. cloud providers looking to diversify beyond congested U.S. metros.

Competitive Landscape

Fragmentation defines the Graphics Processing Unit immersion cooling market in North America, with the top five suppliers, GRC, Submer, LiquidStack, Engineered Fluids, Vertiv, controlling roughly 45-50% of 2025 revenue. HVAC conglomerates are racing to bolt on immersion expertise: Trane’s LiquidStack acquisition and Schneider Electric’s EcoStruxure integration exemplify how incumbents bundle tanks with power distribution and software to lock customers into lifecycle contracts. OCP standardization slashes vendor-lock premiums, letting Taiwanese ODMs undercut tank pricing by up to 20% without sacrificing compatibility.

GPU OEMs now see thermal management as a differentiator. NVIDIA’s Vertiv alliance co-develops cooling modules for Blackwell GPUs, embedding immersion as a standard design element rather than a retrofit. Dell’s IR7000 rack marries direct-to-chip and immersion in one chassis, competing for hyperscale and enterprise bids alike. On the fluid side, Shell and ExxonMobil leverage petrochemical prowess to certify dielectric blends with CPU warranties, but GPU coverage gaps leave operators juggling multiple fluids until OEM testing concludes.

Technological differentiation centers on condenser automation, vapor containment, and inline analytics. Submer and LiquidStack invest in closed-loop two-phase platforms promising PUE below 1.05, whereas GRC and Vertiv emphasize one-vendor simplicity and single-phase stability. Supply-chain diversity remains a weak spot; more than 70% of tank welding capacity sits in East Asia, exposing North American schedules to 16-week lead times and shipping volatility.

North America GPU Immersion Cooling Industry Leaders

GRC (Green Revolution Cooling)

Submer Technologies SL

LiquidStack Holding Pte. Ltd.

Engineered Fluids Inc.

Dell Technologies Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: NVIDIA began volume shipments of the 1200-watt Blackwell B300 GPU with liquid cooling as the default solution. Over 80% of initial orders specify immersion or direct-to-chip architectures.

- February 2026: Microsoft committed to immersion cooling across all Azure AI regions announced after 2026, beginning with sites in Des Moines and San Antonio, targeting PUE below 1.10.

- January 2026: Supermicro released the DLC-3 immersion-optimized server platform for H200, MI325X, and Gaudi 3 accelerators, enabling 150-kilowatt rack densities.

- November 2025: Intel and ExxonMobil certified a synthetic dielectric fluid for Xeon processors, including a warranty rider for single-phase immersion deployments.

North America GPU Immersion Cooling Market Report Scope

The North America GPU Immersion Cooling Market pertains to the regional industry segment dedicated to the implementation of immersion cooling technologies for Graphics Processing Units (GPUs). These technologies are utilized in data centers, artificial intelligence workloads, blockchain operations, gaming, and high-performance computing environments across NA.

The North America GPU Immersion Cooling Market Report is Segmented by Immersion Type (Single-Phase Immersion Cooling, and Two-Phase Immersion Cooling), Solution Type (Immersion Cooling Tanks / Systems, Dielectric Fluids, and Immersion-Optimized GPU Server Systems), Deployment (Hyperscale / Cloud, Enterprise, and Government and Research (HPC)), GPU Power Density (Below 300W, 300W-700W, and Above 700W), and Region (United States, Canada, and Mexico). The Market Forecasts are Provided in Terms of Value (USD).

| Single-Phase Immersion Cooling |

| Two-Phase Immersion Cooling |

| Immersion Cooling Tanks / Systems |

| Dielectric Fluids |

| Immersion-Optimized GPU Server Systems |

| Hyperscale / Cloud |

| Enterprise |

| Government and Research (HPC) |

| Below 300W |

| 300W-700W |

| Above 700W |

| North America | United States |

| Canada | |

| Mexico |

| By Immersion Type | Single-Phase Immersion Cooling | |

| Two-Phase Immersion Cooling | ||

| By Solution Type | Immersion Cooling Tanks / Systems | |

| Dielectric Fluids | ||

| Immersion-Optimized GPU Server Systems | ||

| By Deployment | Hyperscale / Cloud | |

| Enterprise | ||

| Government and Research (HPC) | ||

| By GPU Power Density | Below 300W | |

| 300W-700W | ||

| Above 700W | ||

| By Region | North America | United States |

| Canada | ||

| Mexico | ||

Key Questions Answered in the Report

What is the 2026 value of the GPU immersion cooling market?

The GPU immersion cooling market is valued at USD 219.45 million in 2026.

Which immersion type leads adoption?

Single-phase immersion cooling led the market with an 79.87% revenue share in 2025, driven by simpler operation, easier maintenance, and broader GPU warranty support.

Why are two-phase systems gaining traction?

Hyperscale operators are adopting two-phase immersion systems to achieve sub-ambient chip temperatures and PUE below 1.05, which is critical for latency-sensitive inference and dense AI workloads.

Which geography will grow fastest through 2031?

Canada is forecast to record the fastest growth, with a 26.66% CAGR through 2031, supported by generous waste-heat-reuse incentives and abundant hydroelectric power.

How are dielectric-fluid shortages affecting deployments?

The exit of 3M's Novec fluids tightened market supply, extending qualification timelines and pushing operators to secure multi-year sourcing agreements with suppliers such as Shell, Solvay, and Chemours.

What share do the top five vendors hold?

The top five vendors control approximately 45-50% of 2025 revenue, indicating a market with moderate concentration rather than dominance by a single supplier.

Page last updated on: