Asia Pacific GPU Immersion Cooling Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

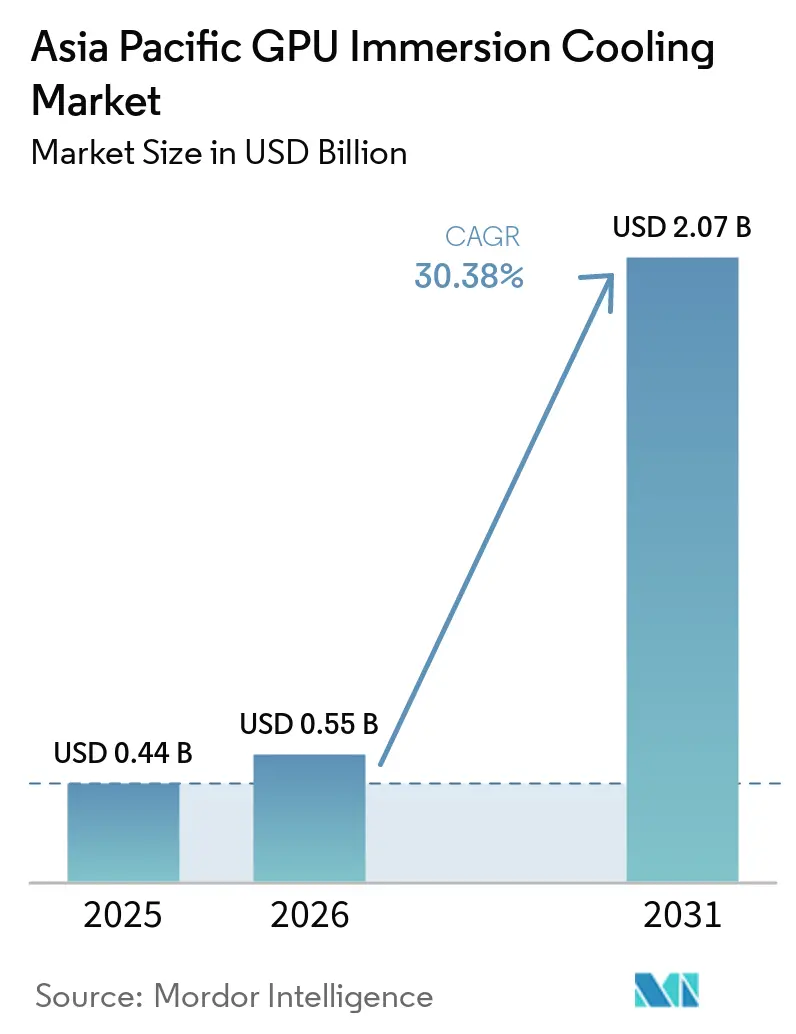

| Base Year Market Size (2025) | USD 0.44 Billion |

| Market Size (2026) | USD 0.55 Billion |

| Market Size (2031) | USD 2.07 Billion |

| Growth Rate (2026 - 2031) | 30.38% CAGR |

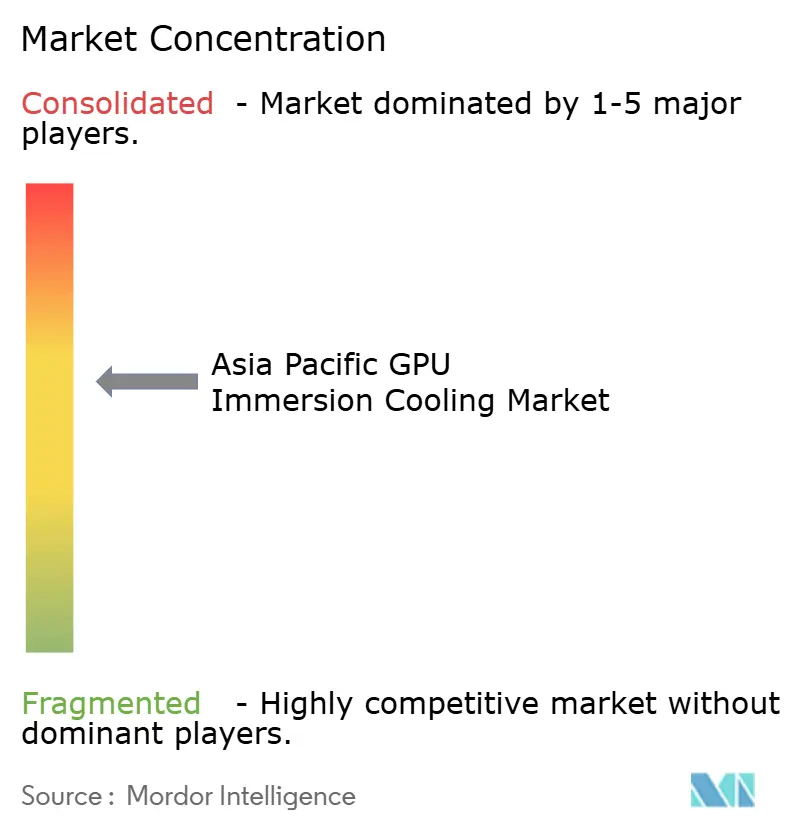

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia Pacific GPU Immersion Cooling Market Analysis by Mordor Intelligence

The Asia Pacific GPU immersion cooling market size is expected to grow from USD 0.44 billion in 2025 to USD 0.55 billion in 2026 and is forecast to reach USD 2.07 billion by 2031 at a 30.38% CAGR over 2026-2031. Operators are pivoting toward immersion solutions because next-generation accelerators already exceed the 300 W-700 W thermal envelope that air handling can manage cost-effectively. Large cloud platforms are front-loading capital into liquid-ready campuses, while stricter power-usage-effectiveness (PUE) rules are making legacy HVAC retrofits economically unattractive. Water stress in major metros is another accelerant, steering developers toward closed-loop designs that cut evaporative consumption. At the same time, domestic incentives in China, India, Japan, and South Korea are nurturing local supply chains for tanks, fluids, and immersion-optimized servers, compressing lead times and lowering total cost of ownership. Competitive activity is intensifying as HVAC multinationals and chemical majors purchase immersion specialists to deliver chip-to-plant portfolios, signaling a market on the cusp of scale.

Key Report Takeaways

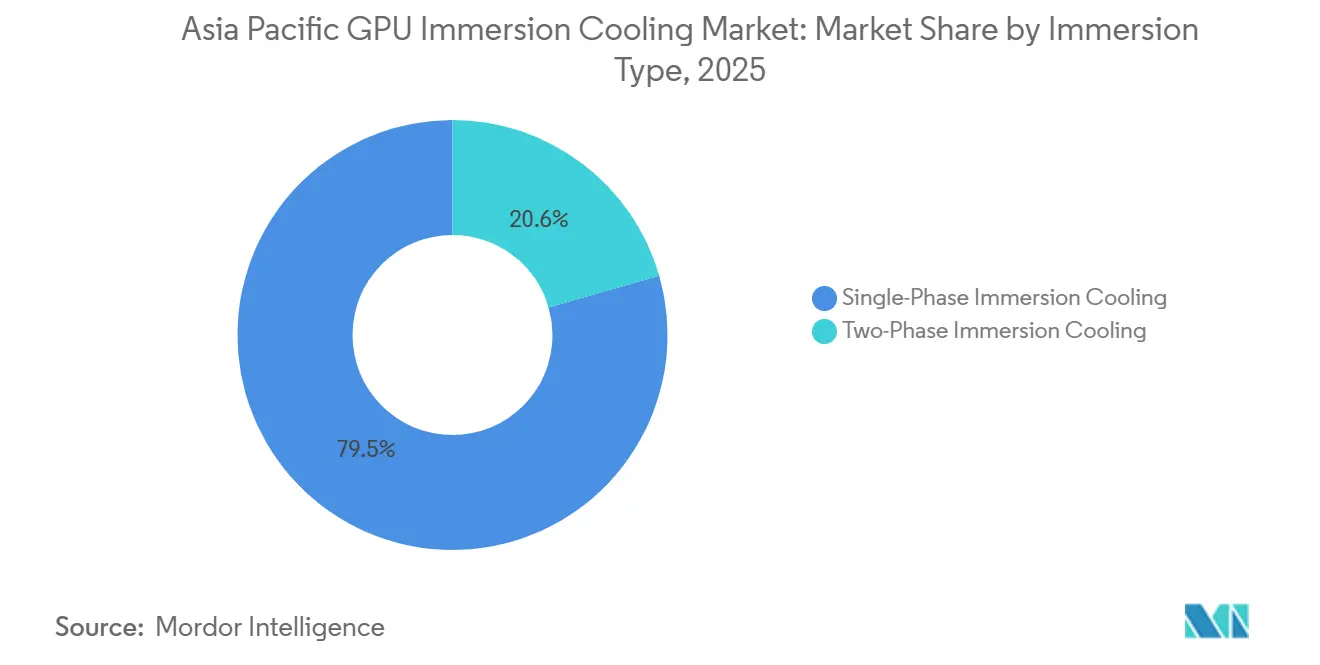

- By immersion type, single-phase systems led with 79.45% of Asia Pacific GPU immersion cooling market share in 2025, while two-phase architectures are advancing at a 30.78% CAGR through 2031.

- By solution type, tanks and systems accounted for 55.34% of the Asia Pacific GPU immersion cooling market size in 2025, and immersion-optimized GPU servers are projected to expand at a 30.85% CAGR to 2031.

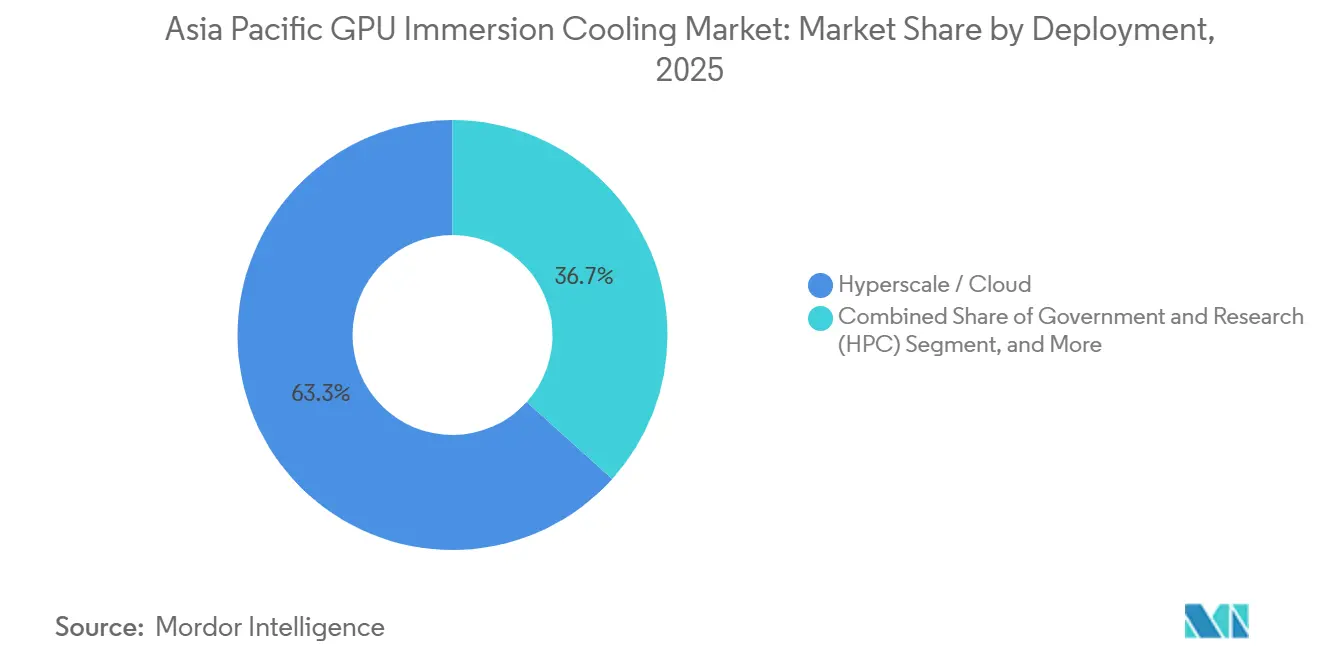

- By deployment, hyperscale and cloud claimed 63.32% revenue share in 2025, whereas enterprise installations are set to record a 30.67% CAGR during 2026-2031.

- By GPU power density, the 300 W-700 W bracket captured 51.43% of the Asia Pacific GPU immersion cooling market size in 2025, the above-700 W tier is forecast to grow at a 30.62% CAGR to 2031.

- By region, China dominated with 47% of market share in 2025, and India is anticipated to post the fastest 30.84% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Asia Pacific GPU Immersion Cooling Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in AI and HPC GPU Deployments Across Hyperscale Data Centers | +8.5% | China, India, South Korea, Japan, Singapore | Short term (≤ 2 years) |

| Stringent Energy-Efficiency Regulations and PUE Targets | +6.2% | Japan, Singapore, Beijing, Shanghai, Seoul | Medium term (2-4 years) |

| Scarcity of Water Resources in Major Asian Metros | +5.8% | India, Singapore, Jakarta, Beijing, Shanghai | Medium term (2-4 years) |

| Accelerated Adoption of Edge Immersion Micro-Data Centers | +4.3% | South Korea, Japan, China, Southeast Asia | Long term (≥ 4 years) |

| Government-Funded National Supercomputing and Sovereign AI Clusters | +3.7% | China, Japan, South Korea, India | Medium term (2-4 years) |

| Local Manufacturing Incentives for Immersion Hardware and Fluids | +2.3% | India, China, South Korea, Thailand | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in AI and HPC GPU Deployments Across Hyperscale Data Centers

Hyperscalers are acquiring record volumes of accelerators, pushing rack power beyond 100 kW and forcing a rapid pivot to immersion solutions. ByteDance committed USD 14 billion for GPU procurement in 2025, while Alibaba Cloud earmarked USD 100 billion for AI infrastructure, both sizing their halls around 700 W-class devices.[1]Bloomberg News, “ByteDance and Alibaba Pour Billions Into AI Chips,” Bloomberg.com Naver’s 4,000-unit NVIDIA B200 roll-out and SK Telecom’s 1,000-unit deployment show that sustained operation at nameplate performance requires liquid capture of chip heat. Japan’s USD 12 billion GMI Cloud campus explicitly mandates immersion tanks for Blackwell-generation clusters. Because NVIDIA roadmaps indicate devices surpassing 1,000 W TDP within two product cycles, immersion is no longer a niche efficiency play, it is the thermal pre-requisite for competitive AI training throughput.

Stringent Energy-Efficiency Regulations and PUE Targets

Governments are weaponizing PUE caps to curb data-center electricity demand. Japan requires existing sites to hit 1.4 by 2030 and new builds to meet 1.3 from 2029, backed by subsidies up to JPY 114.6 billion (USD 1.0 billion) for immersion projects.[2]Ministry of Economy, Trade and Industry, “Data Center Energy-Efficiency Subsidy Program,” meti.go.jp Singapore limits new facilities to PUE more than 1.3 and is drafting a dedicated liquid-cooling code for 2026. Beijing, Shanghai, and Guangdong already enforce thresholds between 1.2 and 1.3. Demonstrated immersion fields routinely deliver PUE near 1.02, eliminating CRAH fans and ductwork while slashing cooling power by up to 90%. The policy trajectory suggests air cooling will be non-compliant across tier-1 metros well before the end of the decade.

Scarcity of Water Resources in Major Asian Metros Driving Liquid Cooling Adoption

Evaporative towers consume roughly 25 million liters of water per megawatt annually in India, yet three-quarters of current and planned capacity sits in high-stress basins.[3]World Resources Institute, “Aqueduct Water Risk Atlas,” wri.org Similar constraints halted new permits in Malaysia’s Johor state during 2025, triggering design revisions toward immersion platforms. Shell and Keppel validated a tank system in Singapore that cut water use by 99% versus chilled-water loops. Cargill’s plant-based NatureCool and Shell’s gas-to-liquid synthetics allow single-phase loops to reject heat through dry coolers, removing dependence on municipal supply. As utilities tighten industrial allocations, water-independent immersion architectures become decisive for site selection.

Accelerated Adoption of Edge Immersion Micro-Data Centers for 5G Densification

LiquidStack’s 250 kW EdgeTank enclosure ships with PUE as low as 1.02, enabling telcos to host AI inference at cell-tower shelters without chilled water. Taiwan’s ITRI, working with KDDI, achieved PUE 1.07 and a 40% footprint cut inside a subtropical pilot. China Unicom’s Chongqing edge site operates at PUE 1.12 using Alibaba Cloud’s single-phase solution, lowering energy by 36.3%. COOLBLOCK reports 80-150 kW racks in sealed street-side enclosures, making immersion the only feasible thermal path where airflow and water loops are impractical.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Capital Expenditure Versus Air Cooling | -3.2% | India, Southeast Asia, smaller enterprises across Asia Pacific | Short term (≤ 2 years) |

| Limited Industry Standards and Hardware Certification | -2.1% | China, India, Southeast Asia | Medium term (2-4 years) |

| Uncertain Long-Term Environmental Rules on Fluorinated Fluids | -1.4% | Japan, South Korea, Singapore, Australia | Long term (≥ 4 years) |

| Skill Shortages in Immersion-Specific Maintenance | -0.9% | India, Southeast Asia, tier-2 cities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Capital Expenditure Versus Air Cooling

Total cost of ownership favors immersion above 50 kW per rack, yet many enterprise budgets still focus on initial price tags. Indian operators pay 10-20% more at commissioning because tanks, pumps, and imported fluids inflate procurement outlays. Fluid alone can add USD 6,000-60,000 per rack, depending on formulation and tank volume. Although Shell and Keppel showed 40% life-cycle savings in Singapore, enterprises operating on 18-month payback horizons hesitate to approve the switch. Reliance on imported components further widens the gap through tariffs and logistics, particularly in South Asia.

Limited Industry Standards and Hardware Certification

The Open Compute Project guidelines remain voluntary, and most Asian regulators have yet to codify immersion benchmarks. Singapore’s SS 697 excludes liquid systems until a 2026 revision, leaving early adopters without a statutory compliance route. Intel’s November 2025 warranty rider covers only ExxonMobil-approved fluids, creating a patchwork of vendor-specific assurances. In India, the Bureau of Indian Standards lacks immersion test protocols, forcing buyers to rely on vendor declarations. The resulting uncertainty lifts insurance premiums and extends procurement cycles, slowing mid-tier rollouts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Immersion Type: Shift Toward Two-Phase Systems as Power Density Climbs

Single-phase designs held 79.45% of Asia Pacific GPU immersion cooling market share in 2025. They remain popular because mineral-oil and synthetic-ester fluids let operators submerge standard servers without sealed lids, easing maintenance and retrofit projects. Asperitas attracted USD 55.5 million in Series C funding and began rolling out such systems in Thailand’s tropical climate. Yet next-wave GPUs topping 700 W are eroding the headroom of convection-only loops. Two-phase solutions, which vaporize low-boiling-point fluids for superior heat flux, are scaling as hyperscalers chase rack densities above 150 kW. Sabey Data Centers is integrating OptiCool refrigerant loops portfolio-wide, bypassing chilled water entirely.

Looking ahead, NVIDIA’s Blackwell parts are expected to push per-device TDP near 1,000 W, at which point two-phase will mainstream among cloud builders. SLiquid’s C8000 cabinet already claims 200 W/cm² dissipation and 220 kW loads. Nevertheless, single-phase will not disappear; enterprises with <700 W accelerators still favor its lower complexity, and edge nodes prize direct technician access to submerged boards. The Asia Pacific GPU immersion cooling market therefore bifurcates: convection loops dominate mid-power deployments, while phase-change tanks anchor ultra-dense AI training farms.

By Solution Type: Immersion-Optimized Servers Outpace Retrofit Tanks

Tanks and ancillary systems represented 55.34% of Asia Pacific GPU immersion cooling market size in 2025 because they are the starting point for any liquid build. Green Revolution Cooling’s CarnotJet units, for example, are now shipping under a Samsung C&T alliance across multiple APAC campuses. OEMs, however, are unveiling boards purpose-engineered for submerged use. Fujitsu, Supermicro, and Nidec co-developed fan-less chassis that shed heatsinks and blowers, cutting bill of materials by up to 15%. Wiwynn invested in LiquidStack manufacturing lines to embed immersion readiness at design time.

Such integrated offerings eliminate warranty disputes about fluid compatibility and support higher GPU counts per node, translating to better performance per rack. As a result, immersion-optimized servers are projected to outgrow tanks at a 30.85% CAGR. Tanks will persist as the delivery vehicle, but value capture migrates up-stack toward pre-validated compute modules that slash integration risk for hyperscale and enterprise buyers.

By Deployment: Enterprises Accelerate After Early Hyperscale Dominance

Hyperscalers, leveraging their extensive AI fleets, have captured 63.32% of the projected 2025 revenue. This dominance is attributed to their ability to amortize investments in custom plant infrastructure across large-scale gigawatt campuses, ensuring operational efficiency and cost-effectiveness. For instance, Alibaba Cloud, as part of its substantial USD 100 billion AI expansion plan, is strategically deploying single-phase tanks across multiple provinces to enhance its infrastructure capabilities. However, enterprises operating under water constraints are progressively closing the gap with innovative approaches. Infosys, for example, is integrating ExxonMobil fluids with its Topaz optimization suite, aiming to promote immersion cooling solutions within financial services and telecom on-premises clusters.

Meanwhile, CtrlS has committed a significant investment of USD 2 billion to develop 350 MW of predominantly liquid-cooled data halls, addressing the growing mid-market colocation demand in India. With rack power requirements nearing 100 kW, even in corporate laboratory environments, immersion cooling technology is enabling operators to achieve double the density without the need for constructing additional buildings. This technological advancement is a key driver behind the robust 30.67% (CAGR) projected for the enterprise segment.

By GPU Power Density: Above-700 W Tier Enters Hyper-Growth

The 300 W-700 W power bracket continues to dominate the market; however, it is expected to gradually lose its share as advancements in accelerators push power consumption beyond the kilowatt threshold. This shift is driven by the increasing demand for higher computational power to support advanced applications. A notable development in this regard is SK Telecom’s Haein cluster, which successfully validated immersion cooling for over 1,000 B200 units, demonstrating its capability to support 700 W chips effectively and paving the way for broader adoption of high-power solutions. Additionally, LiquidStack’s DataTank product lines are engineered to accommodate 16-32 Blackwell GPUs per rack, achieving an impressive Power Usage Effectiveness (PUE) of less than 1.05, which underscores the efficiency of these systems in managing high-density workloads. Consequently, the market segment for devices exceeding 700 W is anticipated to experience significant growth, with a projected (CAGR) of 30.62%, reflecting the industry's transition towards higher power thresholds.

On the other hand, devices operating below 300 W are expected to maintain their presence at the edge of the market, where cost efficiency and operational simplicity take precedence over peak computational performance. These devices are likely to remain relevant in specific use cases where lower power consumption aligns with operational priorities. Despite this, mainstream AI training facilities are projected to standardize the adoption of four-digit wattage per socket well before the year 2030, reflecting a broader industry trend towards accommodating the growing power requirements of advanced AI workloads.

Geography Analysis

China, strengthened by its "Eastern Data and Western Computing" initiative, strategically redirects coastal workloads to inland regions under strict Power Usage Effectiveness (PUE) caps ranging between 1.2 and 1.3. This program underscores the country's commitment to optimizing energy efficiency in data center operations. ByteDance has allocated a substantial USD 14 billion budget for GPUs, while Alibaba Cloud continues to expand its immersion cooling capabilities. These developments collectively drive a self-sustaining cycle of localized tank and fluid production, further solidifying China's position as a pivotal market in the global data center landscape.

India, recognized as the fastest-growing market in the region, faces significant challenges due to acute water shortages affecting 75% of its data-center districts. In response, the 2026 budget introduces a tax exemption on select foreign cloud income, effective until 2047, which has triggered a wave of hyperscale land acquisitions. Additionally, the Production Linked Incentive (PLI) 2.0 scheme provides subsidies to boost domestic manufacturing of servers and chassis. These policy measures, combined with a robust USD 70 billion investment pipeline, are expected to drive a remarkable compound annual growth rate (CAGR) of 30.84%, positioning India as a key player in the global data center market.

Japan is proactively fostering innovation by offering subsidies of up to USD 1.0 billion while enforcing mandatory PUE thresholds. These measures are designed to encourage the adoption of liquid cooling solutions in all new data center facilities, ensuring compliance with energy efficiency standards. In South Korea, the Ministry of Science and ICT is actively funding GPU-as-a-Service clusters, which leverage SK Enmove’s YUBASE fluids for enhanced performance. Furthermore, HD Hyundai Oilbank has successfully validated its XTeer coolant in government laboratories, reinforcing the country's focus on advanced cooling technologies.

Southeast Asia is prioritizing edge computing growth, with Singapore implementing a PUE standard of less than 1.3 and expediting the development of a national liquid-cooling framework. In Indonesia, NeutraDC has inaugurated an 18 MW immersion-ready facility in Batam, strategically designed to accommodate increasing cross-border AI workloads. This initiative highlights the strategic approach of developers in targeting regions with abundant grid capacity and comparatively lower land costs, thereby optimizing operational efficiency and cost-effectiveness.

Competitive Landscape

HVAC industry leaders are increasingly acquiring immersion cooling specialists, reflecting a strategic shift towards achieving a fully integrated thermal management ecosystem. For instance, Trane is poised to complete its acquisition of LiquidStack in February 2026, a move that will consolidate chillers and immersion tanks under a single operational framework. Similarly, Ecolab is strategically expanding its portfolio by incorporating CoolIT into its water-chemicals division through a significant USD 4.75 billion transaction, which is expected to close in the third quarter of 2026.

Eaton's substantial USD 9.5 billion bid to acquire Boyd Corporation's thermal division highlights the growing recognition among electrical equipment manufacturers of liquid cooling as a complementary and strategic addition to their power-train product lines. On a regional scale, oil refiners such as SK Enmove and HD Hyundai Oilbank are intensifying their efforts to establish partnerships for dielectric fluid production, aiming to reduce Asia's reliance on imported cooling fluids and enhance local supply chain resilience.

At the same time, disruptive innovators are actively reshaping the competitive landscape. Accelsius has successfully raised USD 65 million in funding from prominent investors, including Johnson Controls and Legrand, to accelerate the commercialization of its NeuCool two-phase cooling plates, which are specifically designed to meet the demands of AI-driven gigawatt-scale data centers.

Asperitas, focusing on the unique requirements of Southeast Asia's humid climate, is developing customized modular immersion cooling systems, supported by a USD 55.5 million Series C funding round. The pursuit of leadership in industry standards is also intensifying; Intel's fluid certification program provides ExxonMobil with a distinct marketing advantage, while the Open Compute Project's immersion cooling specifications establish a foundational framework for cross-vendor warranty agreements. In conclusion, competitive advantage in this evolving market is increasingly favoring companies that secure original equipment manufacturer (OEM) design partnerships, develop localized fluid blending capabilities, and effectively navigate the complexities of regional regulatory frameworks to deliver comprehensive, warranty-supported turnkey solutions.

Asia Pacific GPU Immersion Cooling Industry Leaders

Submer Technologies, S.L.

LiquidStack Inc.

Green Revolution Cooling Inc.

Fujitsu Limited

Vertiv Group Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: CtrlS Datacenters unveiled a USD 2 billion plan for 350 MW of new Indian capacity, specifying immersion and chilled-water hybrids for AI halls.

- March 2026: Ecolab agreed to acquire CoolIT Systems for USD 4.75 billion, aiming to bundle chemistry and liquid cooling platforms.

- March 2026: Submer partnered with Hammer to roll out SmartPod tanks for AI and HPC clusters in Asia Pacific.

- February 2026: Trane Technologies moved to buy LiquidStack, integrating tanks with chiller controls in a plant-to-chip portfolio.

Asia Pacific GPU Immersion Cooling Market Report Scope

The Asia Pacific GPU Immersion Cooling Market pertains to the regional industry segment within Asia Pacific that emphasizes the adoption and advancement of immersion cooling technologies specifically designed for Graphics Processing Units (GPUs).

The Asia Pacific GPU Immersion Cooling Market Report is Segmented by Immersion Type (Single-Phase Immersion Cooling, Two-Phase Immersion Cooling), Solution Type (Immersion Cooling Tanks and Systems, Dielectric Fluids, Immersion-Optimized GPU Server Systems), Deployment (Hyperscale and Cloud, Enterprise, Government and Research HPC), GPU Power Density (Below 300W, 300W-700W, Above 700W), and Geography (China, Japan, South Korea, India, Southeast Asia, Rest of Asia Pacific). The Market Forecasts are Provided in Terms of Value (USD).

| Single-Phase Immersion Cooling |

| Two-Phase Immersion Cooling |

| Immersion Cooling Tanks / Systems |

| Dielectric Fluids |

| Immersion-Optimized GPU Server Systems |

| Hyperscale / Cloud |

| Enterprise |

| Government and Research (HPC) |

| Below 300W |

| 300W - 700W |

| Above 700W |

| Asia Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Southeast Asia | |

| Rest of Asia Pacific |

| By Immersion Type | Single-Phase Immersion Cooling | |

| Two-Phase Immersion Cooling | ||

| By Solution Type | Immersion Cooling Tanks / Systems | |

| Dielectric Fluids | ||

| Immersion-Optimized GPU Server Systems | ||

| By Deployment | Hyperscale / Cloud | |

| Enterprise | ||

| Government and Research (HPC) | ||

| By GPU Power Density | Below 300W | |

| 300W - 700W | ||

| Above 700W | ||

| By Region | Asia Pacific | China |

| Japan | ||

| South Korea | ||

| India | ||

| Southeast Asia | ||

| Rest of Asia Pacific | ||

Key Questions Answered in the Report

What is the current Asia Pacific GPU immersion cooling market size and its projected CAGR?

The market is valued at USD 0.55 billion in 2026 and is forecast to reach USD 2.07 billion by 2031, registering a 30.38% CAGR according to Mordor Intelligence.

Which immersion type is growing fastest in the region?

Two-phase systems are expected to expand at a 30.78% CAGR as GPUs surpass 700 W heat loads, making phase-change heat removal more attractive.

Why are hyperscalers shifting to immersion cooling?

Accelerators such as NVIDIA's Blackwell family exceed air cooling limits, and immersion delivers PUE near 1.02 while supporting rack densities above 150 kW.

How do PUE regulations affect adoption?

China, Japan, and Singapore cap new-build PUE between 1.2 and 1.3, effectively making immersion or other liquid solutions a compliance requirement for high-density halls.

Which country will witness the fastest growth through 2031?

India is projected to record a 30.84% CAGR, driven by water scarcity, tax holidays for foreign cloud operators, and domestic manufacturing incentives.

Are purpose-built immersion servers cost-effective compared with retrofits?

Yes, removing fans and bulky heatsinks cuts bill of materials by up to 15%, and pre-validation with dielectric fluids reduces warranty risk, narrowing total deployment cost gaps for operators.

Page last updated on: