Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

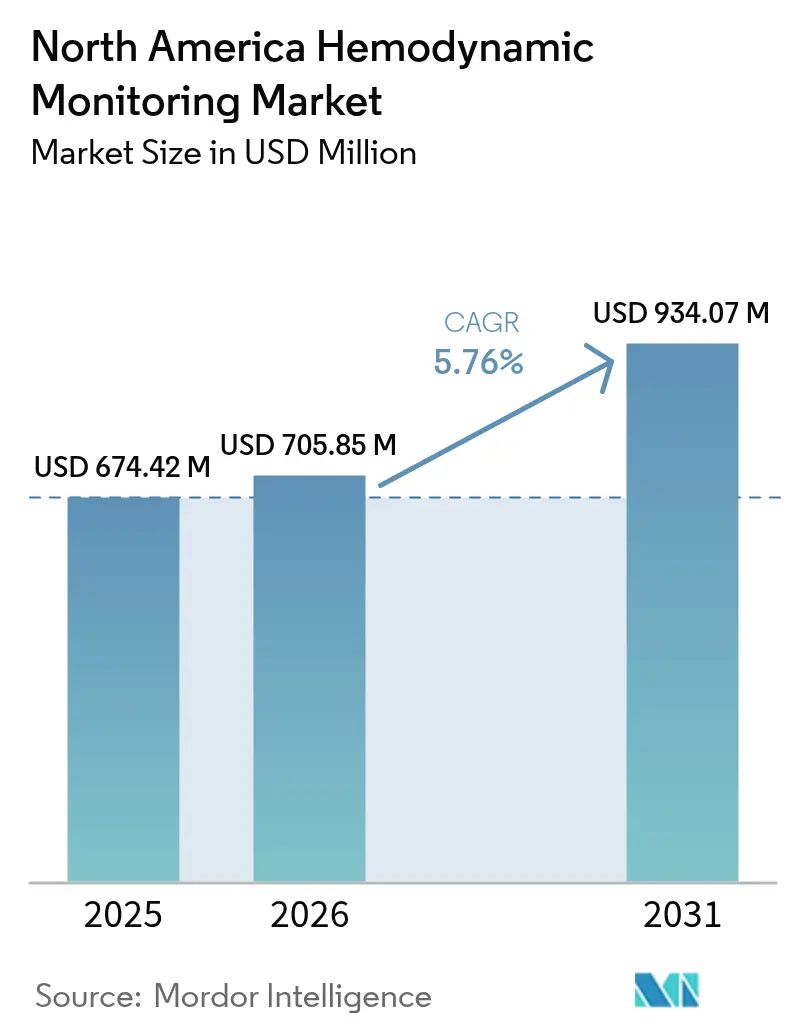

| Base Year Market Size (2025) | USD 674.42 Million |

| Market Size (2026) | USD 705.85 Million |

| Market Size (2031) | USD 934.07 Million |

| Growth Rate (2026 - 2031) | 5.76% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Hemodynamic Monitoring Market Analysis by Mordor Intelligence

The North America Hemodynamic Monitoring Market size is expected to increase from USD 674.42 million in 2025 to USD 705.85 million in 2026 and reach USD 934.07 million by 2031, growing at a CAGR of 5.76% over 2026-2031.

Rising heart-failure prevalence, updated sepsis protocols, and reimbursement that now covers implantable wireless sensors are redirecting capital from catheter-based systems toward minimally invasive and non-invasive platforms. Hospitals increasingly invest in centralized dashboards that apply machine-learning to arterial-waveform data, while tele-ICU networks extend continuous monitoring to community facilities. Competition is intensifying as startups add wearable patches and AI-driven alarm filtering, challenging incumbents whose portfolios revolve around invasive hardware. Mexico’s hospital-modernization program and Canada’s tele-ICU expansion add geographic momentum, yet high equipment costs and staff shortages temper adoption in smaller centers.

Key Report Takeaways

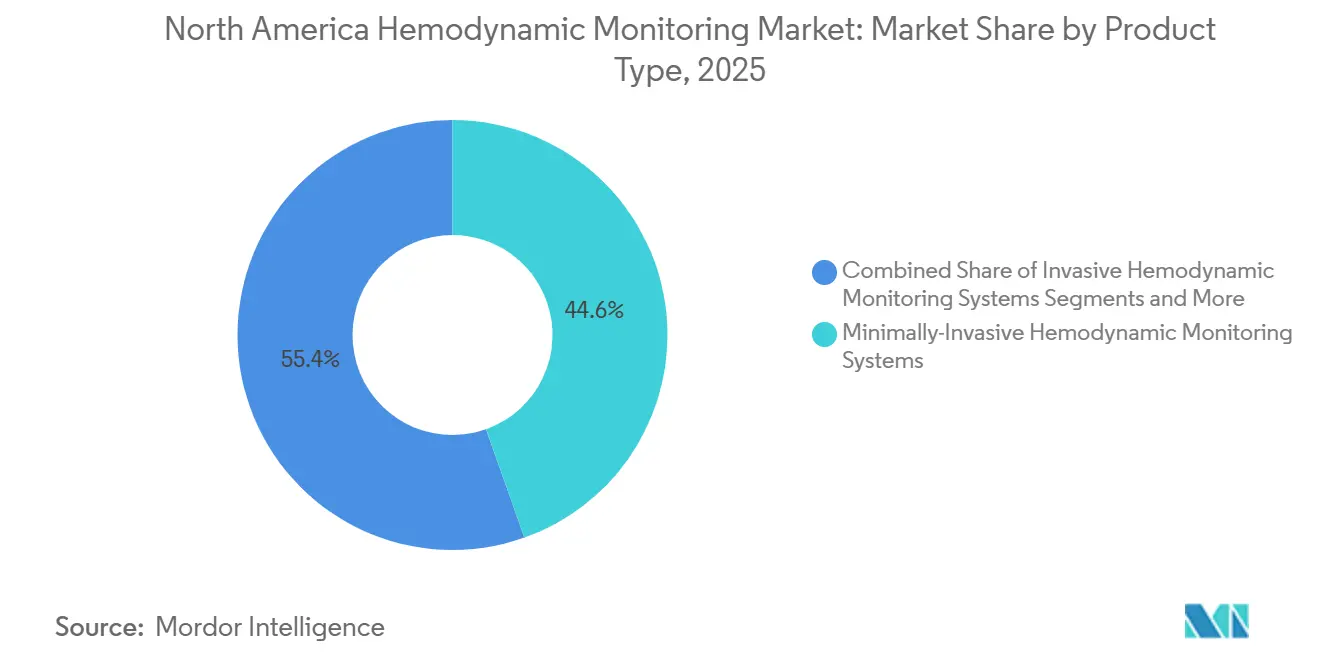

- Minimally invasive systems led with 44.56% of 2025 revenue, while non-invasive platforms are advancing at an 8.46% CAGR through 2031, the fastest in the product segment.

- Software and data-management platforms recorded the highest component-level growth, expanding at a 9.25% CAGR.

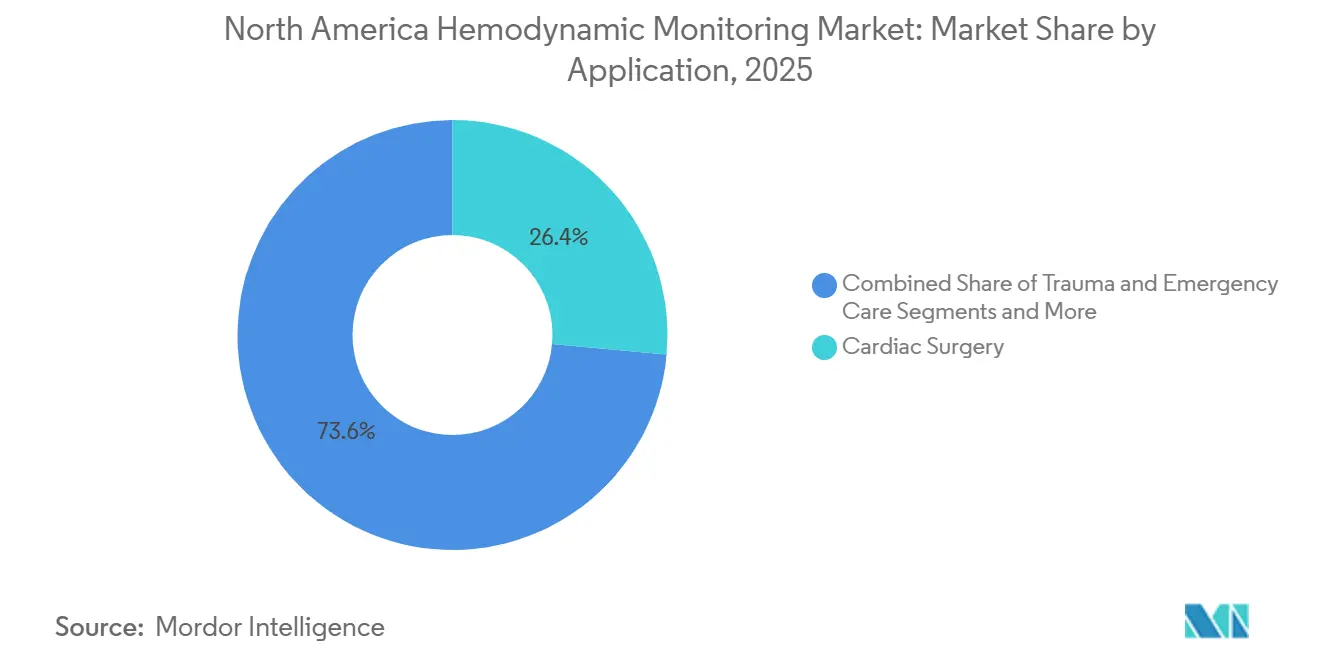

- Sepsis management is the quickest growing application, rising at a 7.73% CAGR, whereas cardiac surgery accounted for 26.44% of 2025 revenue.

- Tissue-oxygenation monitoring is projected to post an 8.23% CAGR, outpacing cardiac-output and blood-pressure parameters.

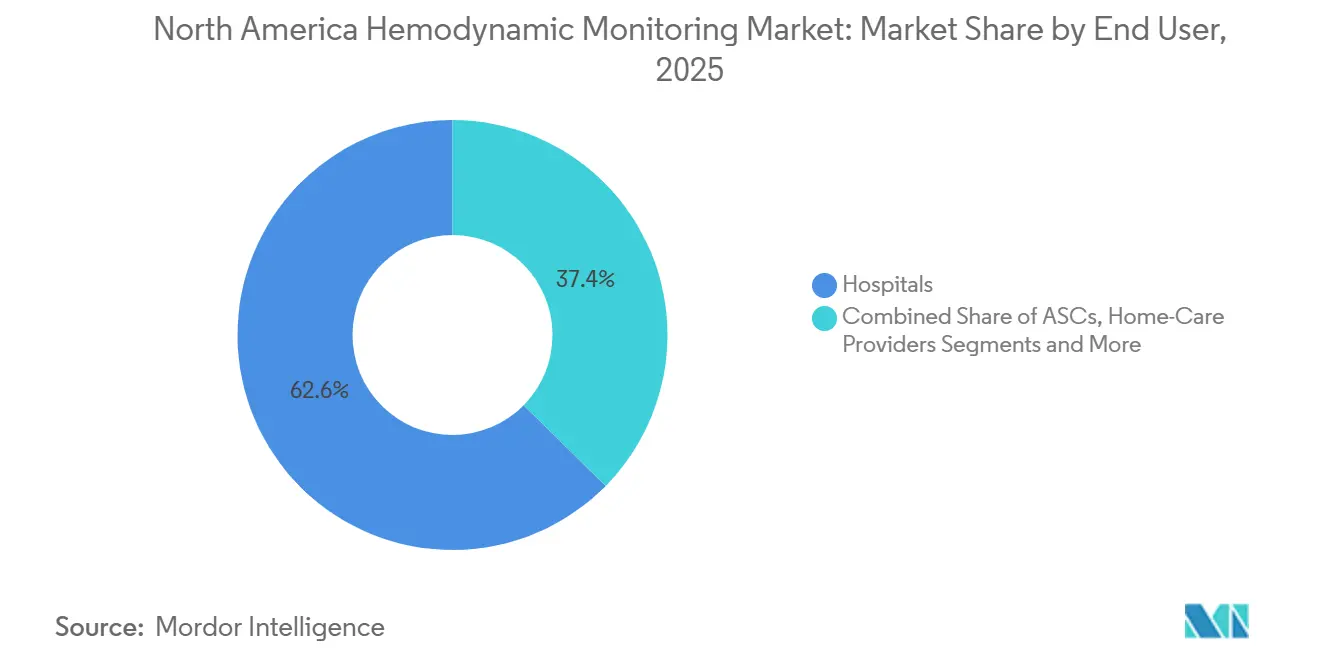

- Home-care providers held the fastest end-user trajectory at a 9.13% CAGR, although hospitals retained 62.62% of 2025 revenue.

- The United States contributed 76.78% of 2025 sales; Mexico is the regional growth leader at an 8.64% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Hemodynamic Monitoring Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Cardiovascular & Critical-Care Caseload | +1.2% | United States, Canada, spillover to Mexico | Long term (≥ 4 years) |

| Advances in Minimally Invasive Technologies | +1.4% | United States academic medical centers, regional diffusion | Medium term (2-4 years) |

| Rapidly Growing Elderly Population | +0.9% | United States, Canada | Long term (≥ 4 years) |

| Favorable U.S. Reimbursement Policies | +0.8% | United States | Short term (≤ 2 years) |

| AI-Guided Fluid-Management Analytics | +1.0% | United States, early use in Canada | Medium term (2-4 years) |

| Expansion of Tele-ICU Platforms | +0.7% | Rural United States and Canadian provincial networks | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Cardiovascular & Critical-Care Caseload

Heart disease caused 702,880 U.S. deaths in 2022, and 6.7 million adults lived with heart failure in 2024; projections place the cohort at 8.7 million by 2030, extending ICU stays and favoring sensors that remain in-situ for days without infection risks.[1] Sepsis guidelines that mandate hemodynamic assessment within one hour further load ICUs, accelerating demand for pulse-contour and bioreactance monitors.[2] Mitchell M. Levy, “Surviving Sepsis Campaign: International Guidelines for Management of Sepsis and Septic Shock 2024,” Society of Critical Care Medicine, sccm.org

Advances in Minimally Invasive Monitoring Technologies

Fourth-generation FloTrac algorithms cleared in 2025 employ machine-learning corrections that narrow error margins during vasoplegic shock, while esophageal Doppler gained U.S. endorsement for guiding fluid therapy in major surgery.[3]U.S. Food and Drug Administration, “510(k) Premarket Notification K243781 – FloTrac System,” U.S. Food and Drug Administration, fda.gov Vendors that bundle sensors with cloud-connected decision support are displacing standalone hardware as clinicians prioritize workflow integration.

Rapidly Growing Elderly Population

Adults ≥ 65 years will reach 21.6% of the U.S. population by 2040, and the 85-plus group already consumes disproportionate ICU resources. Older cardiac-surgery patients exhibit longer hypotension episodes, driving continuous monitoring, and remote pulmonary-artery sensors now target chronic heart-failure management in this cohort.

Favorable U.S. Reimbursement Policies

CMS introduced coverage-with-evidence-development for implantable hemodynamic sensors in 2025, encouraging hospitals to collect outcomes data in return for payment. Commercial insurers mirrored the policy, reimbursing cardiologists USD 60-90 monthly for device-generated data review, which stimulates outpatient adoption.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital & Consumable Costs | -0.9% | U.S. community hospitals, Mexico public facilities | Short term (≤ 2 years) |

| Procedure-Related Infection & Complication Risks | -0.6% | North America, notably invasive catheter use | Medium term (2-4 years) |

| Clinician Alarm Fatigue & Data Overload | -0.5% | United States, Canada ICUs | Short term (≤ 2 years) |

| Shortage of Skilled Critical-Care Nurses | -0.4% | Rural United States and Canada | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital & Consumable Costs

A fully configured HemoSphere unit costs USD 35,000-50,000, and a 20-bed ICU may invest up to USD 600,000 before disposables; smaller hospitals struggle to justify this outlay, while Mexico’s IMSS budgets only USD 12,000 per ICU bed for all monitoring gear.

Procedure-Related Infection & Complication Risks

Central-line infections occur at 0.8 per 1,000 line-days and cost USD 45,000 per episode, while pulmonary-artery rupture carries 50% mortality, prompting clinicians to shift toward minimally invasive technologies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Non-Invasive Platforms Gain Share

Minimally invasive systems held 44.56% of 2025 revenue, anchored by pulse-contour and esophageal Doppler devices that avoid pulmonary-artery catheterization while supplying beat-to-beat data. However, non-invasive platforms are growing at an 8.46% CAGR through 2031 as tele-ICU models favor sensors that work without arterial lines. The North America hemodynamic monitoring market size for non-invasive platforms is expected to expand steadily under this momentum. Wearable patches under development correlate strongly with arterial-line measurements, suggesting future clearance will accelerate bedside replacement of invasive hardware.

The North America hemodynamic monitoring market share commanded by invasive catheters persists in complex cardiac cases, yet FDA approval of the Cordella pulmonary-artery sensor in 2024 validated ambulatory hemodynamics and pressured bedside-monitor vendors to match home-care capabilities. Vendors that integrate cloud connectivity, predictive analytics, and minimal consumable requirements are positioned to capture the next wave of procurement.

By Component: Software Platforms Accelerate

Monitors delivered 34.72% of 2025 component revenue, but software and data-management suites are advancing at a 9.25% CAGR, the quickest component trajectory. Hospitals regard predictive algorithms that alert clinicians 15 minutes before hypotension as essential rather than optional, redefining purchasing criteria. Open APIs that welcome third-party sepsis or ventilator-weaning algorithms differentiate platforms and encourage ecosystem stickiness.

Sensors and disposables still underpin recurring revenue, yet price pressure mounts as hospitals scrutinize total cost of ownership. The North America hemodynamic monitoring market size attributed to services remains stable because multi-year maintenance contracts accompany every capital sale. Vendors now emphasize analytic-software subscriptions to lock in annuity streams and offset hardware commoditization.

By Application: Sepsis Management Surges

Cardiac surgery accounted for 26.44% of 2025 revenue, thanks to high-acuity valve and bypass volumes that require real-time preload and afterload optimization. Updated Surviving Sepsis Campaign recommendations, however, propelled sepsis management to the fastest 7.73% CAGR, as dynamic fluid-responsiveness indices replace static pressure targets in emergency departments. Hospitals invest in bioreactance and pulse-contour devices to satisfy CMS’s SEP-1 quality measures, tying technology adoption directly to reimbursement retention.

General surgery and trauma applications continue to rely on non-invasive systems for goal-directed therapy, and interventional cardiology uses hemodynamics to monitor for tamponade and heart-failure flares. The North America hemodynamic monitoring market share linked to sepsis is projected to broaden as quality-metric compliance shapes purchasing decisions.

By Monitoring Parameter: Tissue Oxygenation Emerges

Cardiac output metrics led with 39.16% of 2025 parameter revenue, yet tissue oxygenation is projected to rise at an 8.23% CAGR. Near-infrared spectroscopy now tracks cerebral and somatic oxygen saturation during cardiac surgery, reducing postoperative stroke by 32% and delirium by 28% in 2024 trials. Regional perfusion insights complement systemic signals, giving clinicians an early warning of microcirculatory deficits that global pressures can miss.

Volume-status metrics, such as stroke-volume variation derived from pulse-contour analysis, anchor fluid-management protocols. Continuous blood-pressure monitoring remains ubiquitous, but algorithms that synthesize multi-parameter trends enhance interpretability and reduce false alarms, key aspirations for the North America hemodynamic monitoring market.

By End User: Home Care Accelerates

Hospitals retained 62.62% of 2025 revenue, yet home-care providers will see a 9.13% CAGR through 2031 as Medicare reimburses implantable sensor data reviews. Cordella-monitored patients recorded 38% fewer heart-failure admissions and saved the system USD 8,000-12,000 per patient annually, building a robust economic case.

Ambulatory surgical centers adopt minimally invasive devices selectively for high-risk cases, and specialty cardiology clinics leverage pulmonary-artery sensors for outpatient titration. Telehealth platforms that deliver actionable hemodynamic insights in the home setting promise to re-shape the North America hemodynamic monitoring market size allocation across care sites.

Geography Analysis

The United States generated 76.78% of 2025 revenue, buoyed by 95,000 ICU beds and a reimbursement framework that bundles monitoring into DRG payments. Tele-ICU beds grew to cover 18% of capacity in 2024, trimming ICU mortality by 11% and stay length by 0.8 days, justifying subscription fees and spurring additional sensor purchases. AI-driven platforms and wearable patches intensify vendor competition, but high product penetration has also increased price sensitivity among group purchasing organizations.

Canada contributes a smaller yet steady portion, anchored by provincial funding aimed at tele-ICU expansion. Ontario budgeted CAD 120 million (USD 88 million) for ICU upgrades in 2024, prioritizing pulse-contour and Doppler devices for fluid-guided therapy. Centralized purchasing slows rollouts, but once value is proven through CADTH assessments, adoption scales rapidly across provincial networks.

Mexico is advancing at an 8.64% CAGR, propelled by a USD 1.2 billion upgrade across IMSS hospitals that adds advanced monitoring to new ICUs. Diabetes prevalence at 16.9% swells cardiovascular load, yet high capital costs limit adoption outside private urban hospitals. Regulatory streamlining has cut device approval times to 9-12 months, but discount negotiations keep pricing pressure high, influencing vendor margin strategies within the North America hemodynamic monitoring market.

Regulatory Landscape

In the United States, hemodynamic monitoring devices are commonly regulated as Class II devices under FDA special controls, including requirements tied to 21 CFR 870.2220 and the 510(k) pathway for substantial equivalence. Regulatory activity in 2025-2026 continued to validate algorithm-led and non-invasive workflows, including FDA clearance of updated pulse-contour software (for example, FloTrac algorithm updates referenced in 2025 clearances) and January 2026 clearance activity around next-generation monitoring configurations such as Edwards Lifesciences HemoSphere Nano Monitor (K253186). This supported hospital adoption of less-invasive monitoring backed by predicate devices.

For connected and software-driven systems, compliance expectations increased around clinical performance evidence and quality systems. In January 2026, FDA issued draft guidance for clinical performance testing and evaluation of cuffless non-invasive blood pressure measuring devices, which directly affects wearable continuous-BP and waveform-derived platforms that overlap with hemodynamic monitoring use cases. FDA also moved away from QSIT to a new device inspection model starting February 2, 2026, requiring manufacturers and contract manufacturers to align internal audit readiness and CAPA processes with the updated inspection approach. In Canada, Health Canada continued aligning submissions with IMDRF formats, and on June 17, 2026, enacted amendments modernizing the Medical Device Establishment Licensing (MDEL) framework, affecting distributors, importers, and service organizations that support installed bases across provincial health systems.

Value Chain Analysis

The North America hemodynamic monitoring value chain covers sensor and disposable manufacturing (catheters, pressure transducers, tubing/flush sets, and wearable sensing elements), monitor and platform OEMs, and software layers that convert waveform and physiologic signals into indices used in sepsis, surgery, and cardiogenic shock pathways. On the supply side, vendors increasingly differentiate through algorithms, cloud connectivity, and interoperability with incumbent bedside ecosystems such as GE CARESCAPE and Philips IntelliVue. As a result, middleware, APIs, cybersecurity, and EHR integration are important value-added steps alongside traditional hardware assembly and calibration.

Downstream, distribution is shaped by large integrated delivery networks, group purchasing organizations, and provincial purchasing bodies in Canada, while clinical adoption depends on ICU/OR protocols and guideline-supported workflows. Health-system standardization is becoming a scaling lever for wearable and wireless solutions, highlighted by the expanded use of FloPatch wearable ultrasound technology within Sutter Health sites for sepsis-focused fluid management. Services (installation, training, biomed maintenance, and analytics subscriptions) increasingly accompany capital sales as hospitals roll out centralized dashboards and tele-ICU models, while consumables remain a recurring-revenue backbone for invasive and minimally invasive systems.

Competitive Landscape

Market concentration is moderate. Edwards Lifesciences, GE HealthCare, and Philips sustain strongholds through catheter and monitor franchises, but Masimo expands non-invasive territory with hemoglobin and perfusion analytics. Abbott’s Cordella system opened the home-monitoring frontier, while startups such as Gauss Surgical tackle alarm-noise reduction with AI. Software dominance is the new battleground: Edwards filed 14 machine-learning patents in 2024, and Masimo submitted nine covering fluid-responsiveness algorithms. Vendors offering open APIs win hospital favor by enabling integration of third-party sepsis predictors and ventilator-weaning tools, differentiators that pure-hardware manufacturers lack.

White-space opportunities cluster around home-based heart-failure care, AI-guided decision support, and tele-ICU compatible non-invasive systems. FDA guidance on SaMD tightened clearance requirements yet validated the clinical value of algorithmic platforms, giving data-rich incumbents a protective moat while raising entry costs for newcomers. Overall, suppliers must pivot from hardware specs to end-to-end clinical solutions to defend share in the evolving North America hemodynamic monitoring market.

North America Hemodynamic Monitoring Industry Leaders

Getinge AB

GE Healthcare

Koninklijke Philips N.V.

BD

ICU Medical

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Hospital and health-system programs that standardize sepsis pathways and extend monitoring through tele-ICU networks create whitespace for non-invasive and minimally invasive platforms that reduce line placement burden and simplify deployment across mixed-acuity facilities. Evidence of system-level adoption supports this opportunity, with Sutter Health reporting deployment of wearable ultrasound technology (FloPatch) for personalized fluid management in sepsis care, and Flosonics Medical securing a Vizient Innovative Technology contract in 2026. This procurement channel can accelerate multi-hospital adoption when clinical and economic criteria are met.

A second opportunity is software and data-management growth tied to alarm-fatigue reduction and early instability detection, as procurement shifts from standalone monitors toward integrated platforms that run alongside existing multiparameter monitors and IT stacks. Regulatory and quality-system shifts also shape near-term product roadmaps and commercialization playbooks: FDA draft guidance in January 2026 for cuffless non-invasive blood pressure performance testing raises the bar for wearable continuous-BP solutions that feed hemodynamic indices, while Health Canada modernization of establishment licensing in June 2026 tightens the compliance environment for in-country distribution and servicing. Consolidation and portfolio integration, including BD bringing Edwards critical care assets into a broader smart connected care strategy, further supports cross-sell opportunities where vendors package sensors, analytics, and enterprise monitoring integration under multi-year contracting.

Recent Industry Developments

- April 2026: BD launched the HemoSphere Stream Module, expanding access to continuous, noninvasive arterial blood pressure waveform insights via the VitaWave Plus System on compatible multiparameter monitors. The release aligns hemodynamic data with mainstream bedside monitoring workflows, supporting broader deployment in settings that avoid arterial lines while still needing beat-to-beat visibility.

- October 2025: Getinge and Philips announced a collaboration to integrate Getinge Flow Family anesthesia machines with Philips IntelliVue patient monitoring technology. The integration focuses on operating-room workflow efficiency and strengthens the interoperability value proposition that increasingly influences capital and software platform decisions.

- June 2024: BD signed a definitive agreement to acquire Edwards Lifesciences Critical Care product group for USD 4.2 billion, bringing established hemodynamic monitoring franchises and algorithms into BD's smart connected care portfolio. The transaction reshaped competitive dynamics by combining a large installed base of advanced monitoring platforms with a broader distribution footprint and a connected-care roadmap.

Research Methodology Framework and Report Scope

Market Definition and Coverage

We define the North America hemodynamic monitoring market as the revenue generated from systems, components, and related offerings used to measure and trend cardiovascular status in clinical care, including invasive, minimally invasive, and non-invasive approaches across key care settings.

Scope exclusions: We exclude general patient monitors without hemodynamic measurement capability and non-clinical wellness wearables that are not used for medical decision-making.

Segmentation Overview

- By Product Type

- Invasive Hemodynamic Monitoring Systems

- Catheters

- Pressure Transducers

- Consumables (pressure tubing, flush sets, etc.)

- Minimally-Invasive Hemodynamic Monitoring Systems

- Pulse-Contour Analysis Devices

- Esophageal Doppler Monitors

- Non-Invasive Hemodynamic Monitoring Systems

- Impedance/ Bioreactance Cardiology Systems

- Wearable Continuous-BP & CO Patch Sensors

- Invasive Hemodynamic Monitoring Systems

- By Component

- Monitors

- Sensors / Transducers

- Disposables & Accessories

- Software and Platforms

- Services

- By Application

- Cardiac Surgery

- General & Orthopedic Surgery

- Interventional Cardiology

- Trauma & Emergency Care

- Sepsis and Septic Shock Management

- By Monitoring Parameter

- Cardiac Output & Derived Indices (CI, SV, SVV, PPV)

- Continuous Blood Pressure (ART/NIBP)

- Volume Status / Fluid Responsiveness Metrics

- Tissue Oxygenation (StO₂, rSO₂)

- By End User

- Hospitals

- Ambulatory Surgical Centers

- Home-Care Providers

- Specialty Cardiology & Critical-Care Clinics

- By Country

- United States

- Canada

- Mexico

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with building the demand context for acute and procedural care where hemodynamic monitoring is most used, then mapping procurement and utilization behavior across the United States, Canada, and Mexico. Public sources were reviewed for anchors such as procedure volumes, ICU and surgical capacity, and clinical guideline direction, which helped keep the assumptions realistic for adoption timing.

For this, we relied on reputable non-paywalled sources such as the US CDC, CMS datasets, FDA device databases and safety communications, OECD health statistics, and peer-reviewed clinical journals that report adoption patterns and outcomes in critical care and perioperative settings. We also checked company filings, investor presentations, association websites, and trusted press coverage to understand product cycles, pricing commentary, and channel shifts. Where available, a paid subscription covering company financials and another covering patent activity were used to sense-check supplier direction and technology refresh timing. These desk research sources are illustrative only, and many other references were used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on interviews and surveys with hospital procurement and clinical stakeholders, as well as distributors and service partners that support monitoring installations and disposables flow. To close data gaps, we used these discussions to confirm what gets purchased as capital equipment versus what is consumed as recurring disposables, and how utilization shifts by setting (ICU, OR, cath lab, and step-down units) across North America.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 32% | CXOs: 15% | |

| Mid tier: 53% | Functional/Unit leaders: 27% | |

| Smaller Players: 15% | Managers: 58% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach where procedure volumes and monitored patient pools were reconstructed, then applying setting-level adoption rates for invasive, minimally invasive, and non-invasive hemodynamic methods. Once that demand pool was in place, average pricing assumptions were applied separately for monitors, sensors, disposables, software, and services, because their replacement and purchasing behavior differs.

To keep the totals grounded, the outputs were cross-checked with selective bottom-up approximations such as sampled price per disposable set multiplied by estimated annual cases, and channel checks on capital replacement cycles for monitors. Key inputs used in the model included ICU and OR utilization signals, cardiac and general surgery volumes, interventional cardiology activity, sepsis and trauma case mix indicators, and observable replacement timing linked to equipment age and service contracts. Where direct data was thin, gaps were handled using conservative adoption ranges that were narrowed through interviews, and then applied consistently across countries with local calibration.

Forecasting leaned on scenario analysis supported by expert feedback, since adoption and pricing can shift quickly with reimbursement changes, procurement constraints, and technology upgrades. In the forecast, we carried forward realistic ASP progression and utilization trends, then adjusted for expected mix shifts toward minimally invasive and non-invasive monitoring where clinically appropriate.

Data Validation & Update Cycle

Validation was done by triangulating model outputs against independent signals such as reported procedure trends, hospital capital budget direction, and recurring disposable consumption logic. When large variances appeared by country or setting, the assumptions were rechecked, and follow-up outreach was triggered to confirm whether the issue was adoption, pricing, or an inclusion mismatch.

Before sign-off, the work goes through multi-step analyst reviews where calculations, unit consistency, and year-over-year movements are checked for anomalies. Reports are refreshed annually, and interim updates are made when material events occur, such as major regulatory actions, reimbursement shifts, or clear procurement pattern changes. Right before delivery, we run a fresh pass on the key inputs so clients receive the latest updated view.

Mordor Intelligence's North America Hemodynamic Monitoring Market Market Size Versus Other Published Estimates

Published market values for hemodynamic monitoring in North America can differ even when they use the same words, because the counted items and timing assumptions are often not aligned. Differences usually show up around whether disposables and software are included, how invasive versus non-invasive methods are treated, and which year is taken as the real base for pricing and volumes.

The main gap comes from whether recurring disposables, sensors, and service revenue are counted alongside capital monitors, and Mordor Intelligence includes these only when they are directly tied to hemodynamic monitoring use in hospital, ASC, home care, and specialty clinic settings across the United States, Canada, and Mexico. Some estimates also push aggressive adoption into the base year, while others hold pricing flat or use different currency timing, which changes the value even if unit volumes look similar.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 0.67 B (2025) | |

| Market Publisher A | USD 0.52 B (2024) | Uses an earlier base year and a narrower segmentation lens that can undercount recurring disposable pull-through and software/service revenue tied to installed systems. |

| Digital Research Desk B | USD 1.51 B (2025) | Appears to apply a broader device definition that can fold in adjacent patient monitoring categories and inflate totals without clearly separating hemodynamic-specific utilization and pricing. |

The spread across published numbers mostly traces back to what is included in the revenue stack and how adoption and ASP movement are carried into the base year. By keeping scope tied to hemodynamic-specific monitoring workflows and then checking totals against procedure-driven demand and recurring consumable logic, the final estimate stays transparent and repeatable for planning.

Key Questions Answered in the Report

How large is the North America hemodynamic monitoring market in 2026?

It stood at USD 705.85 million in 2026 and is projected to reach USD 934.07 million by 2031.

Which product type grows fastest through 2031?

Non-invasive platforms, expanding at an 8.46% CAGR as tele-ICU and home-care usage rises.

Why is sepsis management a key growth application?

Updated guidelines require continuous cardiac-output monitoring early in treatment, driving a 7.73% CAGR for sepsis-focused deployments.

How are AI tools changing hemodynamic monitoring?

Predictive algorithms now forecast hypotension up to 15 minutes in advance, reducing complications and guiding fluid therapy.

Which country offers the highest growth rate in the region?

Mexico, advancing at an 8.64% CAGR due to hospital modernization and a high diabetes-related cardiac burden.

What is the main restraint on market adoption?

High capital and consumable costs, especially for community hospitals and public facilities, limit widespread deployment.

Page last updated on: