Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

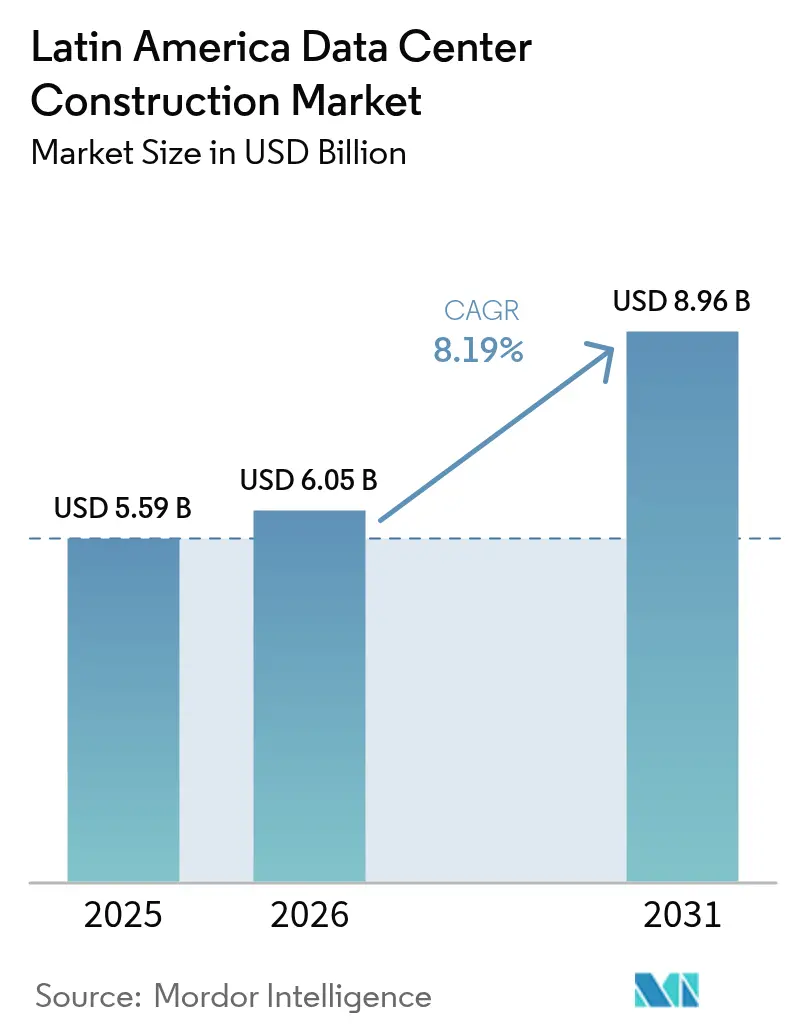

| Base Year Market Size (2025) | USD 5.59 Billion |

| Market Size (2026) | USD 6.05 Billion |

| Market Size (2031) | USD 8.96 Billion |

| Growth Rate (2026 - 2031) | 8.19% CAGR |

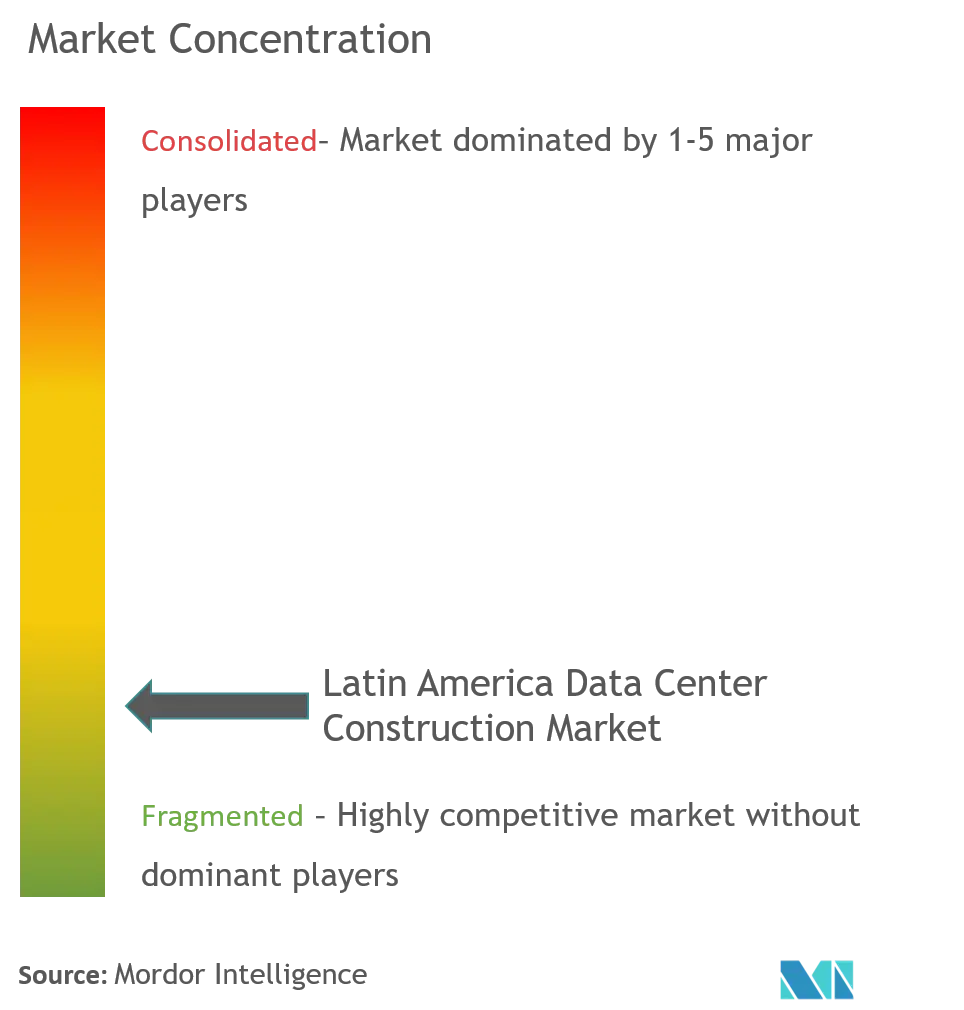

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Latin America Data Center Construction Market Analysis by Mordor Intelligence

The Latin America Data Center Construction market size is expected to grow from USD 5.59 billion in 2025 to USD 6.05 billion in 2026 and is forecast to reach USD 8.96 billion by 2031 at 8.19% CAGR over 2026-2031. Robust investment momentum stems from sovereign-cloud mandates, hyperscale campus build-outs by United States cloud majors, and mounting artificial-intelligence workloads that require specialized, high-density facilities. Brazil leads regional spending with 40% of total 2024 investments, while Mexico’s Querétaro corridor attracts fresh capital thanks to proximity to U.S. demand and state incentives. Mechanical infrastructure dominated 2024 spending at 38% because tropical heat loads elevate cooling requirements, yet IT infrastructure posts the quickest gains at an 8.52% CAGR through 2030. Tier III sites prevailed with 62% share in 2024, but Tier IV projects advance at an 8.90% CAGR as hyperscalers insist on fault-tolerant uptime. Supply-chain bottlenecks and grid constraints lengthen project cycles; however, sweeping deregulation in Chile and abundant renewable-energy opportunities across Brazil, Chile, and Colombia sustain a positive investment outlook.

Key Report Takeaways

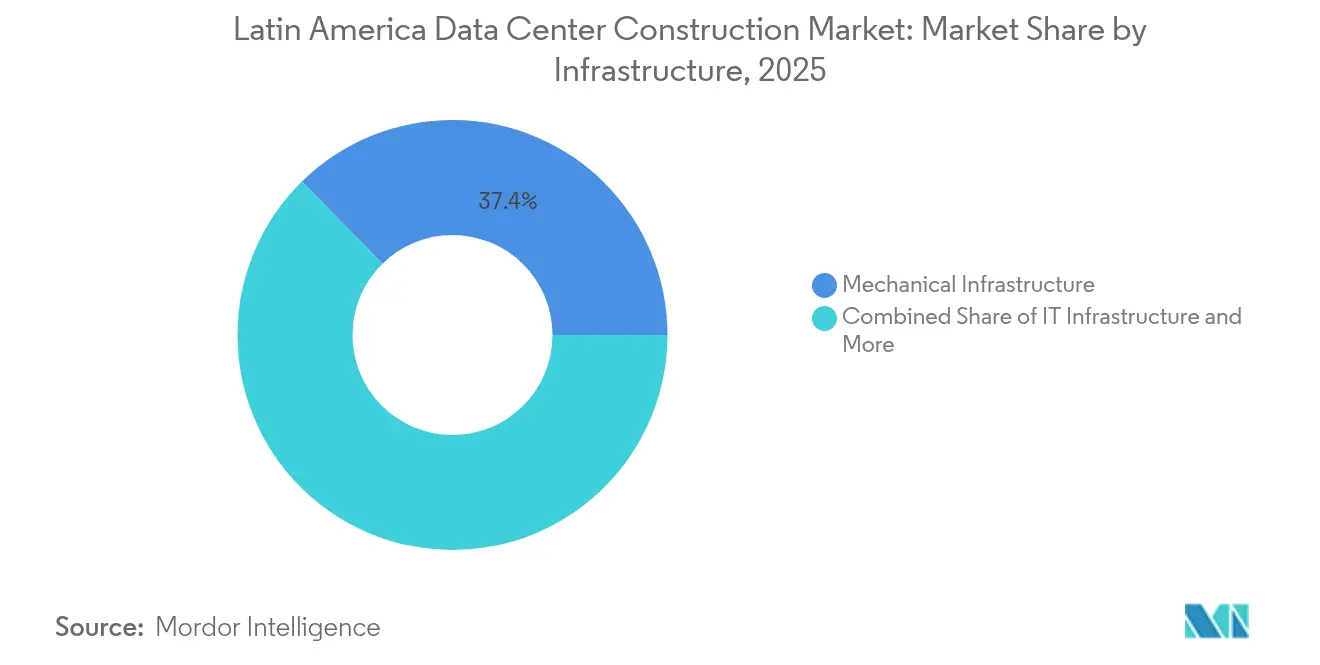

- By infrastructure, mechanical systems led with 37.35% of the Latin America Data Center Construction market share in 2025

- By tier standard, Tier III commanded 61.10% share of the Latin America Data Center Construction market size in 2025

- By end-user industry, IT and telecommunications held 48.40% of the Latin America Data Center Construction market share in 2025

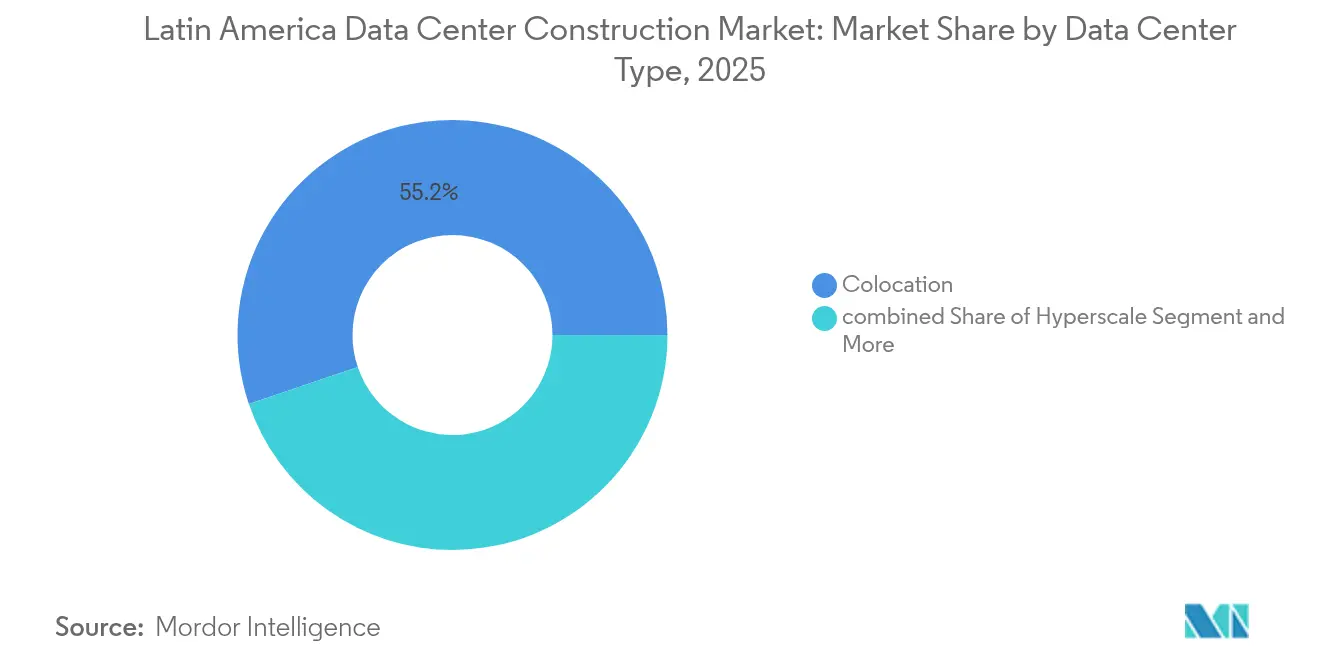

- By data center type, colocation facilities captured 55.20% of the Latin America Data Center Construction market size in 2025

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Latin America Data Center Construction Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Accelerating cloud, AI and big-data workloads | +2.1% | Brazil, Mexico, Chile | Medium term (2-4 years) |

| Hyperscale campus build-outs by U.S. cloud majors | +1.8% | Brazil, Mexico, Colombia | Short term (≤ 2 years) |

| 5G-driven edge-DC demand in secondary metros | +1.4% | Brazil, Mexico, Colombia, Peru | Long term (≥ 4 years) |

| Sovereign-cloud and data-residency regulations | +1.6% | All LATAM countries | Medium term (2-4 years) |

| Power-purchase agreement availability for renewables | +0.9% | Brazil, Chile, Colombia | Long term (≥ 4 years) |

| Modular and prefabricated construction adoption | +0.7% | Brazil, Mexico | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Accelerating cloud, AI and big-data workloads

Artificial-intelligence applications now demand three to five times the power density of legacy computing, compelling operators to redesign thermal architectures and electrical topologies. Microsoft’s USD 2.7 billion Brazil investment and Scala’s USD 50 billion AI City illustrate the scale of new requirements.[1]Stephen Nellis, Data center companies investing in Brazil, Reuters, reuters.com Liquid-cooling adoption accelerates, with locally manufactured Delta Cube systems reducing energy usage in ODATA sites. Regional policy makers regard AI infrastructure as a pillar of digital competitiveness, prompting expedited permits and targeted tax breaks. Contractors report surging bids for high-density MEP packages, and suppliers of busway, pumps, and plate-heat exchangers scale up regional production footprints.

Hyperscale campus build-outs by U.S. cloud majors

Amazon Web Services, Microsoft Azure, and Google Cloud collectively earmark more than USD 10 billion for Latin America by 2030. Multi-gigawatt campuses in São Paulo, Querétaro, and Bogotá require redundant 400 kV utility feeds, advanced fire suppression, and prefabricated power rooms that cut commissioning cycles to 12-18 months. Regional fiber conglomerate V.tal alone budgets USD 1 billion to deliver hyperscale-ready shells in Brazil. The build-to-suit model favors EPC firms proficient in integrated design-build, and demand spills into secondary metros as power availability tightens in first-tier cities.

5G-driven edge-DC demand in secondary LATAM metros

Claro Peru’s 5G-Advanced tests hit 10 Gbps download speeds, underscoring latency-sensitive use cases that require distributed micro-data centers nearer to end users.[2]Claro Peru & Huawei, 5G-A field trial hits 10 Gbps, rcrwireless.com EdgeUno rolls out prefabricated 0.5-2 MW sites in cities such as Arequipa and Mérida, while Colombian authorities cite ten submarine fiber-optic cables as an anchor for edge expansion. Construction differs from hyperscale models, focusing on modular skids, carrier-neutral meet-me rooms, and remote management platforms that cut staffing overhead.

Sovereign-cloud and data-residency regulations

Brazil’s General Data Protection Law, recent rules on cross-border data transfer, and Chile’s National Data Center Plan force multinationals to process data in-country.[3]Maria Pérez, Brief comments on Chile deregulation, terraforminglatam.net Argentina’s RIGI law sweetens terms for USD 200 million-plus builds, including tax holidays and forex protections. These measures lock in local construction demand, shape design specifications around security zones, and encourage partnerships with domestic utilities for renewable power supply.

Restraints Impact Analysis*

| RESTRAINTS | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Grid-power bottlenecks and surging electricity tariffs | -1.9% | Mexico, Argentina primary; Brazil, Colombia secondary | Short term (≤ 2 years) |

| Scarcity of Tier-III/IV-certified MEP labour | -1.2% | Regional, with acute shortages in secondary markets | Medium term (2-4 years) |

| Water-stress curbing liquid-cooling deployments | -0.8% | Chile, Mexico, Argentina; urban centers in Brazil | Long term (≥ 4 years) |

| Lengthy environmental licensing and community opposition | -0.6% | Brazil, Chile primary; Mexico, Colombia secondary | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Grid-power bottlenecks and surging electricity tariffs

Mexico struggles with 18-month utility-interconnection queues, pushing developers to procure diesel generation that adds up to 25% to project CAPEX and inflates operating expenses. Argentina’s macro-economic volatility amplifies tariff risk, while localized transmission congestion in São Paulo forces developers toward Campinas and Porto Alegre. AI workloads multiply power density, stressing grids originally designed for commercial office loads. Operators increasingly sign 15-year renewable PPAs to secure predictable pricing, but smaller enterprises lack the balance-sheet to pursue such deals, slowing adoption in mid-market segments.

Scarcity of Tier-III/IV-certified MEP labor

Mission-critical construction now outpaces the talent pipeline, with certified electricians and HVAC technicians commanding premiums that lift labor cost 20-30% above conventional builds. Visa delays for imported specialists extend schedules, while secondary metros such as Barranquilla and Córdoba face acute shortages that push projects into Tier II specifications. Industry associations propose apprenticeship programs, yet uptake remains modest. Developers therefore lean on modular-prefabricated components to minimize on-site specialized labor hours.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Infrastructure: Cooling Dominates in Tropical Climates

Mechanical infrastructure contributed 37.35% to the Latin America Data Center Construction market size in 2025, as hot-humid conditions across Brazil, Peru, and Colombia require robust chilled-water loops, evaporative cooling, and custom containment systems. Power distribution units, switchgear, and UPS arrays within electrical infrastructure stay essential for banking and telecom uptime mandates. General construction captures resilient shell-and-core outlays, including seismic bracing and hurricane-rated envelopes that safeguard mission-critical halls.

IT infrastructure is the fastest-growing category with an 8.16% CAGR, driven by servers optimized for AI inference, NVMe storage arrays, and 400 Gbps networking fabric. Hyperscale clients standardize on high-density racks requiring direct-to-chip liquid manifolds, which boosts demand for stainless-steel piping and redundant coolant pumps. Services such as consulting, commissioning, and facility management add value by ensuring regulation compliance and PUE optimization. The Latin America Data Center Construction market share within energy-efficiency consulting rises as carbon disclosure norms tighten in stock exchanges across the region.

By Tier Standard: Reliability Premium Fuels Tier IV

Tier III sites held 61.10% of the Latin America Data Center Construction market share in 2025, balancing 99.982% availability against manageable capex. Banks, insurers, and public clouds select this level for core workloads that tolerate brief maintenance windows. Conversely, content-delivery networks and regional edge nodes often deploy Tier II to limit cost while placing nodes closer to users.

Tier IV construction will grow 8.55% CAGR through 2031 on the back of hyperscalers and fintech platforms seeking 99.995% service-level commitments. Multiple independent distribution paths, fault-tolerant chillers, and concurrently maintainable generators inflate capital budgets by up to 60%, yet clients accept the premium to satisfy uptime-linked revenue clauses. Builders partner with certification bodies early in design to avoid late-stage retrofit costs that have plagued first-time entrants.

By Data Center Type: Hyperscale Momentum Builds

Colocation data centers represented 55.20% of the Latin America Data Center Construction market share in 2025, providing immediate entry points for enterprises without the balance-sheet for self-builds. Operators like Equinix opened Rio 3 to capture latent demand from fintech and gaming clients. Service differentiation now leans on cross-connect density and sustainability metrics such as PUE and water-usage effectiveness.

Hyperscale/self-built campuses are accelerating at a 9.85% CAGR to 2031, propelled by cloud majors seeking sovereign compliance and latency gains. Microsoft’s São Paulo hub and CloudHQ’s Querétaro project both exceed 200 MW when fully built. Developers secure 400 kV substation access and multi-terabit terrestrial fiber rings, cementing long-run cost advantages versus multi-tenant models. Enterprise, edge, and modular data centers fill niche latency and disaster-recovery needs, benefiting local integrators skilled in rapid site roll-outs.

By End-User Industry : Healthcare Surges on Telemedicine Adoption

IT and telecommunications customers retained 48.40% share of the Latin America Data Center Construction market size in 2025, channeling investment into carrier hotels, IP transit nodes, and private-cloud expansions. BFSI workloads remain steady, with Banrisul’s storage upgrade illustrating steady refresh cycles to meet digital-banking growth. Government ministries award contracts for sovereign-cloud zones that isolate classified networks within domestically controlled cabinets.

Healthcare tops growth charts at 8.12% CAGR as telemedicine platforms, imaging archives, and electronic health records balloon data volumes. Hospitals deploy edge micro-data centers for real-time diagnostics, while national e-health regulations mandate on-shore processing. System integrators bundle HIPAA-equivalent compliance modules into new builds, expanding professional-services revenue streams. Other verticals such as manufacturing and media adopt smart-factory analytics and streaming distribution that further diversify demand for facility configurations.

Geography Analysis

Brazil held 39.20% of regional capital outlays in 2025 and remains the anchor of the Latin America Data Center Construction market. Eighty-five percent renewable-energy penetration and a stable regulatory regime reduce long-term operating risk. São Paulo alone concentrates 80% of national capacity, but developers increasingly select Campinas and Porto Alegre for land and power availability. Public banks earmark BRL 2 billion in credit lines, and Patria’s USD 1 billion platform signals ongoing domestic-investor confidence.

Mexico leverages near-shoring dynamics and US-MCA trade certainty, with Querétaro’s state government offering discounted land leases and streamlined permits. CloudHQ’s greenfield project highlights cross-border fiber synergies, yet power shortages around Mexico City create siting challenges. Chile positions itself through deregulation that exempts data-center projects from environmental impact assessments, while providing government-backed land plus 1 million-liter diesel storage thresholds that cut permitting by six months. Equinix’s USD 130 million Santiago build illustrates international appetite.

Colombia controls 9.35% revenue share and posts 12.6% annual growth as Bogotá benefits from cool temperatures and plentiful submarine-cable landings. KIO’s 6 MW launch with an option to double underscores institutional confidence. Argentina’s new RIGI incentives lure USD 200 million-plus investors to Buenos Aires and Bahía Blanca with 30 MW guaranteed power and tax relief. Peru and the rest of Latin America serve as emerging hotspots where 5G advances and digital-inclusion funds accelerate micro-facility adoption.

Competitive Landscape

The contractor ecosystem shows moderate fragmentation as global EPC majors vie with regional builders and niche modular specialists. AECOM, Turner, and Jacobs capitalize on certified project-delivery frameworks to win hyperscale contracts, whereas Andrade Gutierrez and Queiroz Galvão leverage utility-interconnection know-how and municipal relationships. No single firm exceeds 10% regional revenue, keeping bargaining power dispersed.

Competition increasingly hinges on sustainability credentials and modular-delivery track records. Scala Data Centers pairs 100% wind PPAs with prefabricated power rooms, cutting schedule risk while meeting net-zero pledges. V.tal’s design-build model integrates substation erection, accelerating time-to-service for U.S. cloud tenants. Contractors adopt BIM and digital twins to improve clash-detection and reduce re-work by 20%, a key advantage amid skilled-labor shortages.

Secondary markets open white-space for local firms adept in mid-tier builds. Grupo Marhnos pivots from commercial real estate into 5-10 MW edge hubs, emphasizing rapid deployment and low OPEX. International utilities such as Iberdrola explore joint ventures that bundle renewable generation with build-transfer-operate data-center shells, adding a fresh competitive dimension.

Latin America Data Center Construction Industry Leaders

AECOM

Turner Construction

DPR Construction

Jacobs Solutions

Fluor Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Scala Data Centers and Serena announce Latin America’s largest renewable-energy deal for data-center wind power self-supply.

- July 2025: Iberdrola forms a USD 1.63 billion joint venture with Echelon to develop 144 MW in Madrid Sur, pointing to possible Latin American replication.

- May 2025: Patria launches a USD 1 billion Brazilian data-center platform targeting hyperscale customers.

- April 2025: Equinix commits USD 130 million for a new Santiago, Chile facility

Latin America Data Center Construction Market Report Scope

Datacenter construction materially builds a data center facility connecting construction standards data center operational environment needs. The market comprises Tier-1, Tier-2, Tier-3, and Tier-4, which are used in small, medium, and large-scale enterprises.

The Latin America data center construction market is segmented into infrastructure type (electrical infrastructure, mechanical infrastructure, general construction), tier type (tier-I and -II, tier-III, and tier-IV), size of enterprise (small and medium-scale enterprises, large-scale enterprises), end user (BFSI, IT and telecommunications, government and defense, healthcare), and country (Mexico, Brazil, Argentina, Rest of Latin America). The report offers market forecasts and size in value (USD) for all the above segments.

By Infrastructure

| By Electrical Infrastructure | Power Distribution Solutions | Power Distribution Unit |

| Switchgears | ||

| Others Electrical Infrastructure | ||

| Power Backup Solutions | UPS | |

| Generators | ||

| By Mechanical Infrastructure | Cooling Systems | Liquid-based Cooling |

| Air-based Cooling | ||

| Racks and Cabinets | ||

| Other Mechanical Infrastructure | ||

| By IT Infrastructure | Servers | |

| Storage | ||

| Other IT Infrastructure | ||

| General Construction | ||

| Services | Design and Consulting | |

| Integration | ||

| Support and Maintenance | ||

By Tier Standard

| Tier I and II |

| Tier III |

| Tier IV |

By End-User Industry

| Banking, Financial Services and Insurance |

| IT and Telecommunications |

| Government and Defense |

| Healthcare |

| Other End Users |

By Data Center Type

| Colocation Data Centers |

| Hyperscale / Self-built Data Centers |

| Others (Enterprise / Edge / Modular) |

By Geography

| Brazil |

| Chile |

| Argentina |

| Rest of Latin America |

| By Infrastructure | By Electrical Infrastructure | Power Distribution Solutions | Power Distribution Unit |

| Switchgears | |||

| Others Electrical Infrastructure | |||

| Power Backup Solutions | UPS | ||

| Generators | |||

| By Mechanical Infrastructure | Cooling Systems | Liquid-based Cooling | |

| Air-based Cooling | |||

| Racks and Cabinets | |||

| Other Mechanical Infrastructure | |||

| By IT Infrastructure | Servers | ||

| Storage | |||

| Other IT Infrastructure | |||

| General Construction | |||

| Services | Design and Consulting | ||

| Integration | |||

| Support and Maintenance | |||

| By Tier Standard | Tier I and II | ||

| Tier III | |||

| Tier IV | |||

| By End-User Industry | Banking, Financial Services and Insurance | ||

| IT and Telecommunications | |||

| Government and Defense | |||

| Healthcare | |||

| Other End Users | |||

| By Data Center Type | Colocation Data Centers | ||

| Hyperscale / Self-built Data Centers | |||

| Others (Enterprise / Edge / Modular) | |||

| By Geography | Brazil | ||

| Chile | |||

| Argentina | |||

| Rest of Latin America | |||

Key Questions Answered in the Report

How large is the Latin America Data Center Construction market in 2026?

The market stands at USD 6.05 billion in 2026 and is projected to reach USD 8.96 billion by 2031.

Which infrastructure category captures the biggest outlay?

Mechanical infrastructure leads with 37.35% share because tropical climates elevate cooling and power-distribution costs.

What is driving the surge in Tier IV facilities?

Hyperscale cloud providers and fintech platforms demand 99.995% uptime, pushing Tier IV builds to grow at 8.55% CAGR.

Why is healthcare the fastest-growing vertical?

Telemedicine expansion and electronic health records require secure, on-shore processing, resulting in 8.12% CAGR through 2031.

Which country dominates investment?

Brazil accounts for 39.20% of 2025 spending due to abundant renewable power, stable regulation, and a deep contractor base.

How are power constraints being addressed?

Developers sign long-term renewable PPAs and integrate on-site generation to mitigate grid bottlenecks and tariff volatility.

Page last updated on: