Market Overview

| Study Period | 2020 - 2031 |

|---|---|

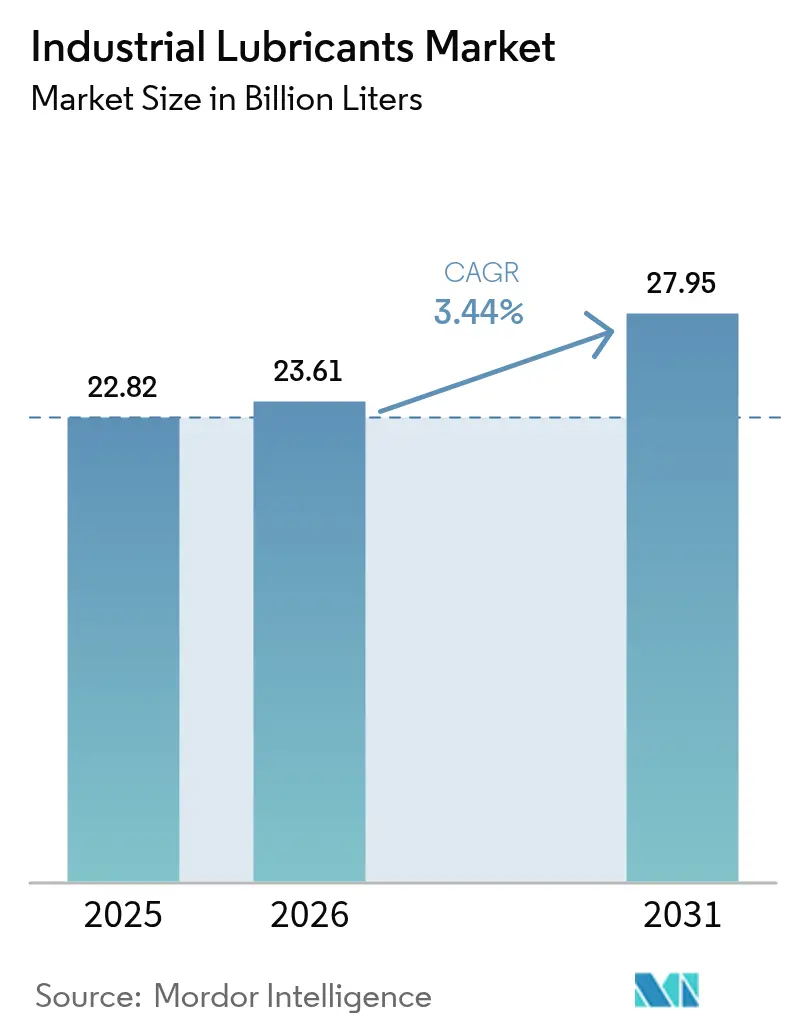

| Market Volume (2026) | 23.61 Billion liters |

| Market Volume (2031) | 27.95 Billion liters |

| Growth Rate (2026 - 2031) | 3.44% CAGR |

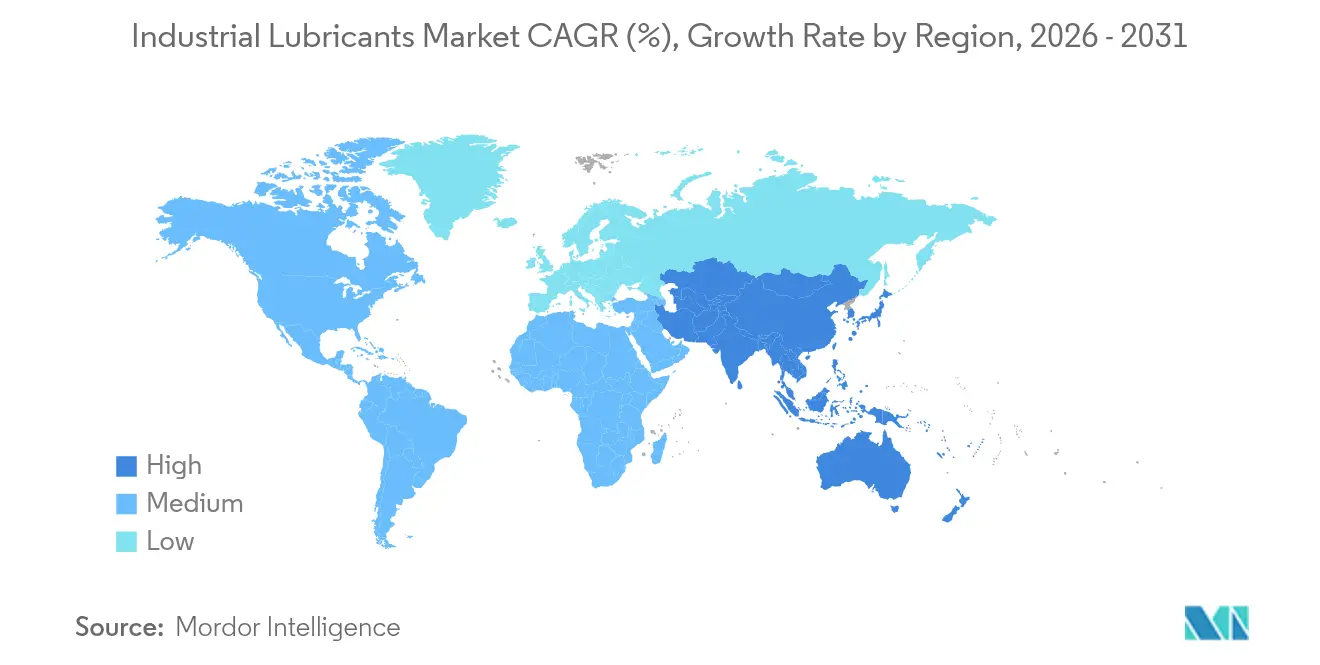

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Industrial Lubricants Market Analysis by Mordor Intelligence

The Industrial Lubricants Market size market is expected to grow from 22.82 billion liters in 2025 to 23.61 billion liters in 2026 and is forecast to reach 27.95 billion liters by 2031 at 3.44% CAGR over 2026-2031. This steady trajectory shows the sector’s shift from bulk commodity sales to tailor-made fluids that maximize equipment uptime and energy efficiency. Rapid wind-turbine installations and Industry 4.0 upgrades are expanding lubricant performance requirements beyond legacy specifications, spurring demand for synthetic and bio-based chemistries. Asia-Pacific dominates current consumption thanks to large-scale manufacturing investments and integrated refinery-petrochemical complexes that capture higher-value lubricant margins. Producers worldwide are also channeling R&D toward PFAS-free additives and condition-monitoring-ready fluids in response to tightening environmental rules and predictive-maintenance adoption.

Key Report Takeaways

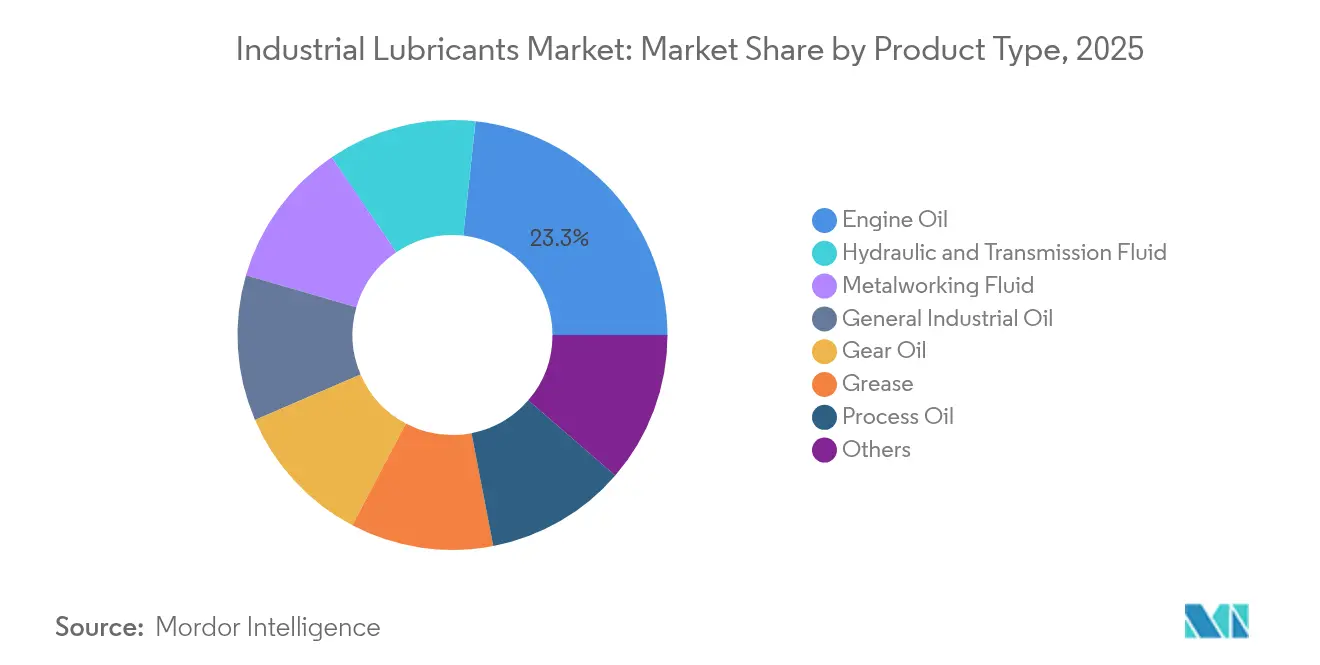

- By product type, engine oil led with 23.29% of the industrial lubricants market share in 2025; hydraulic and transmission fluid is projected to advance at a 3.92% CAGR through 2031.

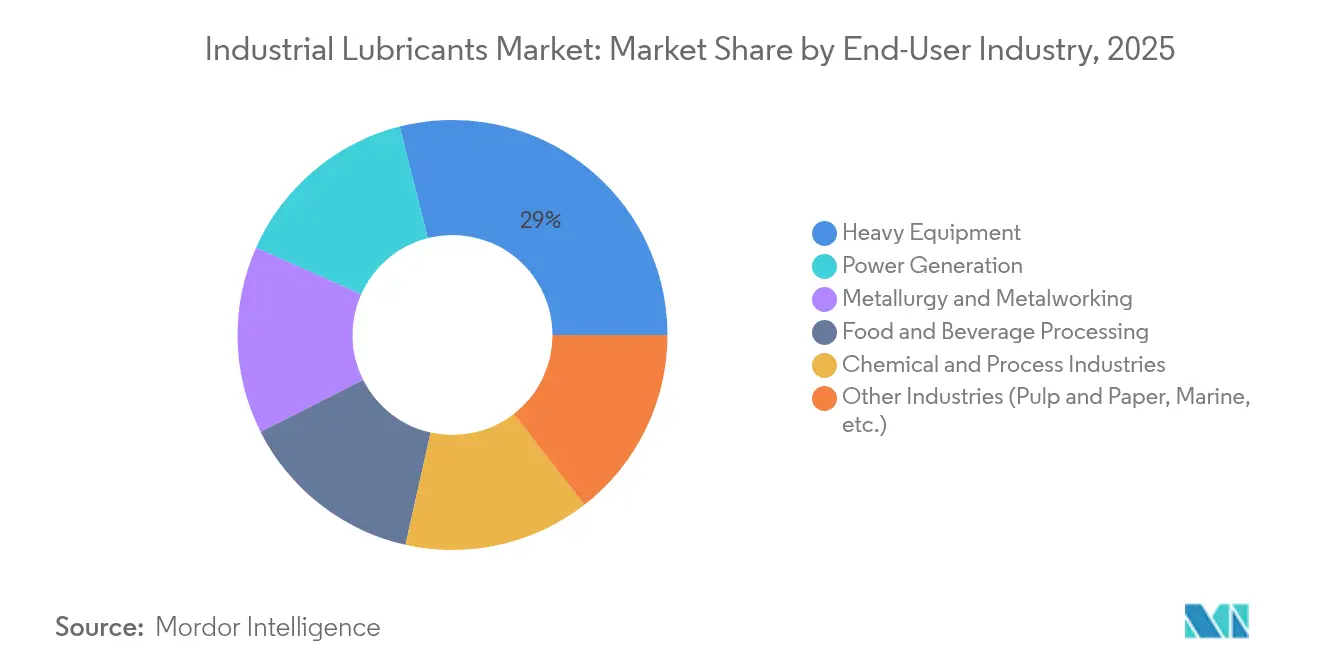

- By end-user industry, heavy equipment accounted for a 28.96% share of the industrial lubricants market size in 2025; power generation is forecast to expand at a 4.27% CAGR through 2031.

- By geography, Asia-Pacific commanded a 46.88% share in 2025 and delivered the fastest regional growth at a 3.61% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Industrial Lubricants Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging wind-turbine gearbox lubricant demand | +0.8% | Global, concentrated in APAC and Europe | Medium term (2-4 years) |

| Industrial automation and Industry 4.0 lubrication intensity | +0.6% | North America & EU, expanding to APAC | Long term (≥ 4 years) |

| Shift toward synthetic and semi-synthetic long-drain oils | +0.5% | Global, led by developed markets | Medium term (2-4 years) |

| Expansion of mining and construction equipment fleets | +0.4% | APAC core, spill-over to MEA and South America | Short term (≤ 2 years) |

| Carbon-pricing pull for ultra-low-friction bio-lubricants | +0.3% | EU & North America, pilot programs in APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Wind-Turbine Gearbox Lubricant Demand

Global wind-power build-outs are multiplying specialized gearbox-oil requirements that standard fluids cannot satisfy. China’s installed wind capacity reached 440 GW by December 2023, with many turbine failures traced to lubrication shortcomings. Synthetic oils fortified with anti-wear and corrosion inhibitors extend service intervals from 6 months to 3 years, trimming offshore maintenance costs. Robust water-separation properties are essential because remote turbines must minimize helicopter-based servicing. Developers increasingly specify ISO VG 320-460 PAO blends that preserve viscosity across wide temperature swings, protecting multi-megawatt gearsets during harsh gust events. Each 15-MW offshore turbine can consume over 800 liters per service cycle, so the industrial lubricants market sees a direct volume lift from larger unit ratings.

Industrial Automation and Industry 4.0 Lubrication Intensity

Smart factories deploy precision equipment that runs hotter and faster, demanding fluids with narrow viscosity tolerances and negligible sensor interference. Automated lubrication systems meter doses based on real-time analytics, cutting consumption 30%-40% while boosting uptime. Fluids must keep tribological stability when exposed to magnetic-plug or infrared debris monitoring, so additive solubility and metal-ion content are tightly specified. Artificial-intelligence platforms now adjust formulation recommendations by reading vibration and temperature feeds, pushing suppliers to create modular additive packages for on-site customization. These developments anchor a long-term upward mix shift within the industrial lubricants market toward premium synthetic and hybrid products.

Shift Toward Synthetic and Semi-Synthetic Long-Drain Oils

Industrial maintenance teams facing labor shortages favor oils that last 8,000-12,000 hours compared with 2,000-4,000 hours for mineral grades. Group III and PAO bases deliver oxidation stability that suppresses sludge even at 120 °C sump temperatures. Semi-synthetic variants balance cost and performance, gaining traction in price-sensitive operations such as cement mills and textile plants. Extended drain intervals shrink waste oil volumes by up to 70%, aligning with waste-reduction policies and lowering disposal fees. This transition dovetails with corporate net-zero pledges, further cementing synthetic uptake in the industrial lubricants market.

Expansion of Mining and Construction Equipment Fleets

Infrastructure packages across India, Indonesia, and Gulf states are deploying high-horsepower excavators and haul trucks that operate in abrasive dust and fluctuating climates. OEMs specify zinc-free hydraulic fluids with boosted film strength to comply with Tier 4F emission systems. In open-pit mining, biodegradable greases formulated with calcium sulfonate complexes protect bucket pins that endure 300-ton static loads. Service intervals of 1,000 hours are becoming standard to reduce downtime in remote sites. These heavy-duty demands translate into sustained volume growth for viscosity-grade 46-68 fluids within the industrial lubricants market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter waste-oil and spill regulations | -0.4% | Global, strictest in EU and North America | Short term (≤ 2 years) |

| Crude-derived base-oil price volatility | -0.3% | Global, most impactful in price-sensitive markets | Short term (≤ 2 years) |

| Dry-drive electric motors reducing oil demand | -0.2% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stricter Waste-Oil and Spill Regulations

PFAS-phaseout mandates in the EU and several U.S. states force formulators to redesign long-standing products[1]Ready-Market Online Corp., “The Connection Between PFAS and Industrial Oils: Exploring Sustainable Alternatives,” hai-lu-oil.com. Certification of alternative chemistries slows time-to-market and inflates R&D budgets. At the user level, collection systems must now document cradle-to-grave traceability, lifting disposal costs and capital outlays for containment. Spill-prevention directives require double-walled tanks and real-time leak alarms, raising infrastructure costs for small workshops. While these hurdles dampen short-term demand, they also open niches for compliant, higher-margin formulations within the industrial lubricants market.

Crude-Derived Base-Oil Price Volatility

Group II and Group III base-stock prices swing with refinery outages and geopolitical shocks, compressing blender margins. Buyers resist quarterly price adjustments, prompting suppliers to hedge inventory or renegotiate contracts monthly. Volatility steers some users toward lower-spec fluids, risking premature equipment wear and undercutting lifecycle savings from synthetics. Integrated oil majors counteract volatility by upgrading resid streams, as seen in ExxonMobil’s Singapore project that added 20,000 barrels per day of premium stocks[2]ExxonMobil, “Preparing for 2025: Singapore Refinery’s Latest Milestones,” exxonmobil.com. However, independents without upstream assets face higher working-capital needs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Engine-Oil Leadership Sustains, Hydraulic Fluids Accelerate

Engine oil contributed 23.29% of 2025 sales, safeguarding critical generators and stationary compressors across heavy industries. This share underscores deep-rooted maintenance routines that favor monograde SAE 40 and 15W-40 multigrades compatible with legacy engines. Yet demand plateaus as OEMs pivot to gas engines with longer drain specifications. Hydraulic and transmission fluids, in contrast, are set to grow at a 3.92% CAGR as robotics, injection-molding machines, and wind-turbine pitch systems expand. Metalworking fluids benefit from Asia-Pacific machine-tool investments, and ionic-liquid cutting oils deliver longer tool life than mineral benchmarks.

Synthetic grease blends incorporating molybdenum disulfide and graphite are grabbing share in extreme-pressure bearings exposed to 200 °C kiln outlets. Meanwhile, demand for process oils ties directly to petrochemical debottlenecking in China, India, and the U.S. Up-and-coming electric-motor cooling oils illustrate how evolving machinery profiles continuously reshape the industrial lubricants market.

By End-User Industry: Heavy Equipment Leads, Power Generation Gains Pace

Heavy equipment retained 28.96% of volumes in 2025, serving construction loaders, surface-mining trucks, and agriculture harvesters that operate in abrasive dust and high-shock cycles. These machines require high-dispersion engine oils and zinc-free hydraulic fluids capable of sustaining 5,000 psi pressures. Power generation ranks as the fastest-growing consumer with a 4.27% CAGR to 2031, spurred by wind-turbine rollouts and gas-engine peaker plants that backstop renewables. Food and beverage processors adopt NSF-H1 fluids that can cost 30% more but mitigate contamination risk, while metal-forming shops keep metal-removal fluids in steady demand. Overall, equipment-longevity goals and grid-expansion projects ensure balanced growth patterns within the industrial lubricants market.

Geography Analysis

Asia-Pacific accounted for 46.88% of 2025 volumes and is tracking a 3.61% CAGR through 2031, where Chinese refiners integrate chemicals to lift lubricant margins. India draws heavy foreign investment, with Lubrizol earmarking USD 200 million for a new Aurangabad plant that will be its second-largest worldwide. Southeast Asian countries welcome factory relocations and renewable-energy projects, driving hydraulic and gear oil uptake. Japan and South Korea sustain above-average synthetic penetration due to precision manufacturing and stringent energy-saving targets.

North America and Europe concentrate on PFAS-free formulations and carbon-linked efficiency gains. The U.S. leverages shale-derived feedstocks, yet EV adoption gradually curbs traditional engine oil demand. Europe leads the policy push that elevates bio-lubricants, compelling rapid formulation shifts. Canada’s oil-sands mining keeps high-temperature lubricant requirements active, whereas Mexico’s automotive investments broaden local demand.

The Middle-East and Africa rely on hydrocarbon extraction projects that underpin base oil supply and diversify into chemicals. A new additive plant from the Richful–Farabi venture in Saudi Arabia will shorten supply lines for regional blenders. South Africa’s deep-level mining and Nigeria’s refining upgrades contribute niche opportunities. South America shows pockets of high growth around Brazilian petrochemical debottlenecking and Chilean copper expansions, cementing its role as an important albeit smaller outlet for industrial lubricants market suppliers.

Competitive Landscape

Global leadership remains moderately fragmented. Regional independents capture share through custom formulations and agile technical service, particularly in Asia-Pacific, where proximity reduces lead times. IoT-compatible lubricants and AI-driven blending represent emerging differentiators as users seek lifecycle cost cuts. PFAS-free, biodegradable, and e-mobility thermal fluids form key white-space arenas where newcomers can leapfrog legacy products. Mergers and acquisitions momentum continues, exemplified by Valvoline acquiring Oil Changers for USD 630 million to reinforce downstream channel reach.

Industrial Lubricants Industry Leaders

Shell plc

Exxon Mobil Corporation

BP p.l.c. (Castrol)

Chevron Corporation

TotalEnergies SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Fuchs Lubricants announced an investment of BRL 220 million (~USD 41.30 million) in a new industrial plant in Sorocaba, São Paulo, aiming to double its market share in Brazil and strengthen its presence across Latin America. By 2030, the facility is projected to reach a production capacity of over 50,000 tons annually.

- July 2025: Shell acquired 100% equity in Raj Petro Specialities Pvt. Ltd. from Germany’s Brenntag Group. This acquisition enhances Shell’s product portfolio with high-value specialty products such as transformer oils, white oils, petroleum jellies, and waxes, catering to fast-growing sectors including pharmaceuticals, personal care, and power transmission.

- January 2024: Shell plc's subsidiary, Shell Lubricants, completes the acquisition of the United Kingdom-based MIDEL and MIVOLT from Manchester-based M&I Materials Ltd to manufacture, distribute, and market the MIDEL and MIVOLT product lines as part of Shell’s global lubricants portfolio.

Global Industrial Lubricants Market Report Scope

A lubricant is a substance that is applied to surfaces with relative motion between them as it reduces friction and wear between surfaces. However, in addition to these primary functions, a lubricant can include other functions or roles, such as sealing agent, heat transfer agent, and corrosion prevention agent. Lubricants can be found in many forms, from liquid, semi-solid, dry, and gaseous lubricants. The most common lubricants are oils and gases.

The industrial lubricants market is segmented by product type, end-user industry, and geography. By product type, the market is segmented into engine oil, transmission and hydraulic fluid, metalworking fluid, general industrial oil, gear oil, grease, process oil, and other product types. The end-user industry is segmented into power generation, heavy equipment, food and beverage, metallurgy and metal working, chemical manufacturing, and other end-user industries. The report also covers the market size and forecasts for the industrial lubricants market in 33 countries across major regions. For each segment, the market sizing and forecasts are done on the basis of volume (liters).

By Product Type

| Engine Oil |

| Hydraulic and Transmission Fluid |

| Metalworking Fluid |

| General Industrial Oil |

| Gear Oil |

| Grease |

| Process Oil |

| Others |

By End-user Industry

| Power Generation |

| Heavy Equipment |

| Food and Beverage Processing |

| Metallurgy and Metalworking |

| Chemical and Process Industries |

| Other Industries (Pulp and Paper, Marine, etc.) |

By Geography

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Indonesia | |

| Thailand | |

| Vietnam | |

| Malaysia | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle-East and Africa |

| By Product Type | Engine Oil | |

| Hydraulic and Transmission Fluid | ||

| Metalworking Fluid | ||

| General Industrial Oil | ||

| Gear Oil | ||

| Grease | ||

| Process Oil | ||

| Others | ||

| By End-user Industry | Power Generation | |

| Heavy Equipment | ||

| Food and Beverage Processing | ||

| Metallurgy and Metalworking | ||

| Chemical and Process Industries | ||

| Other Industries (Pulp and Paper, Marine, etc.) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Indonesia | ||

| Thailand | ||

| Vietnam | ||

| Malaysia | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large is the industrial lubricants market in 2026?

Sales reached 23.61 billion liters in 2026, and the industrial lubricants market size is projected to rise to 27.95 billion liters by 2031 at a 3.44% CAGR.

Which region buys the most industrial lubricants?

Asia-Pacific leads with 46.88% of 2025 volume and is still the fastest-growing region.

Which product category grows the quickest?

Hydraulic and transmission fluids will expand at a 3.92% CAGR through 2031 as automation and wind-turbine fleets expand.

Why are synthetic oils gaining share?

They allow 8,000-12,000-hour drain intervals, cut waste oil by up to 70%, and support Industry 4.0 condition monitoring.

How are green policies affecting lubricant demand?

Carbon pricing and PFAS bans encourage bio-based, ultra-low-friction, and PFAS-free formulations, shifting demand toward premium chemistries.

Page last updated on: