North America GPU Liquid Cooling Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

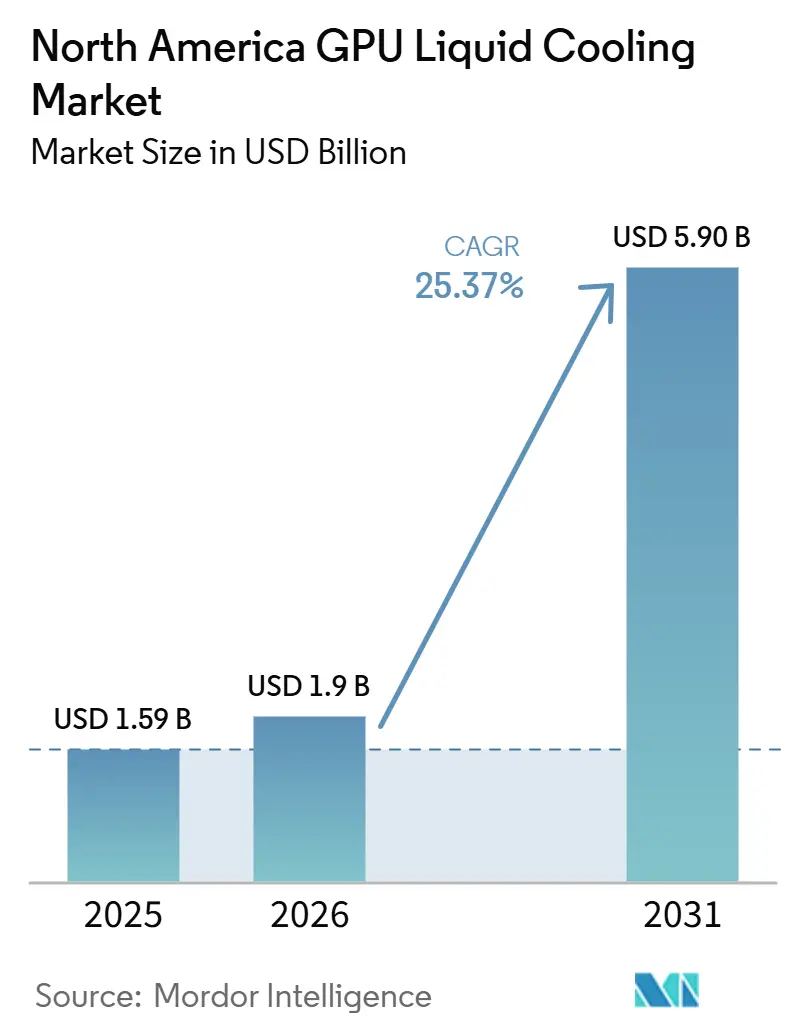

| Base Year Market Size (2025) | USD 1.59 Billion |

| Market Size (2026) | USD 1.9 Billion |

| Market Size (2031) | USD 5.90 Billion |

| Growth Rate (2026 - 2031) | 25.37% CAGR |

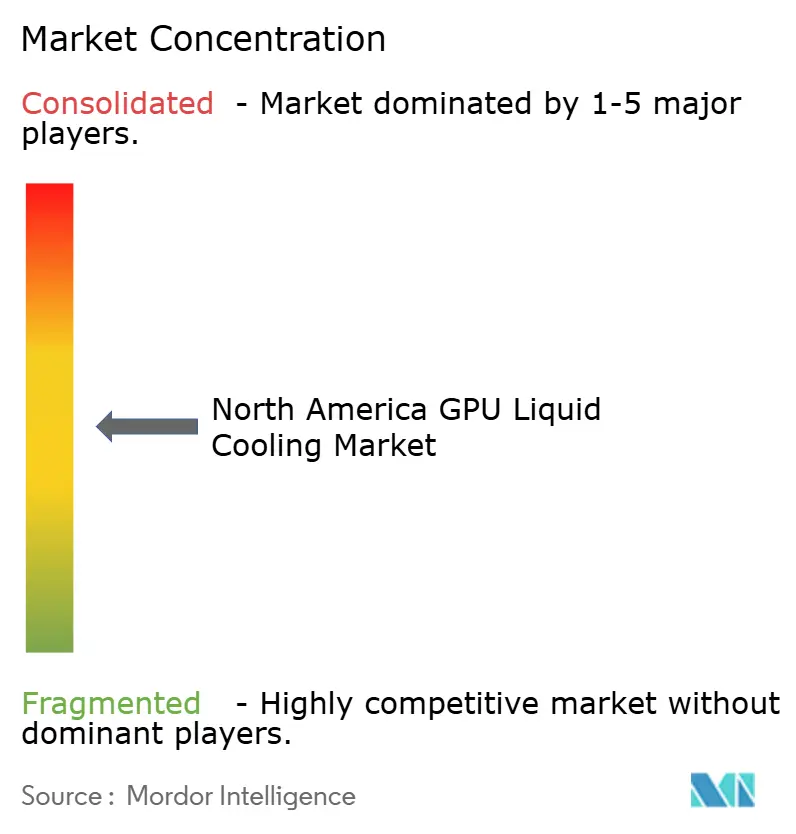

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America GPU Liquid Cooling Market Analysis by Mordor Intelligence

The North America GPU liquid cooling market size is projected to expand from USD 1.59 billion in 2025 and USD 1.90 billion in 2026 to USD 5.90 billion by 2031, registering a CAGR of 25.37% between 2026 to 2031. The growth path is being set by a basic hardware limit, because GPU thermal loads have moved beyond the point where air cooling can remain the primary design for dense AI systems at scale. Rack power is rising so quickly that operators now need liquid-ready electrical, thermal, and facility layouts from the start, which shifts spending from optional upgrades to core infrastructure. Hyperscale buyers are also shortening adoption cycles for the broader North America GPU liquid cooling market by treating liquid cooling as a standard requirement in new AI deployments rather than as a pilot technology. Policy pressure around energy and water use is adding another layer of urgency, especially for facilities that need to meet tighter efficiency expectations while supporting higher compute intensity. Competition is tightening as larger industrial and thermal management companies move in through acquisitions, which raises barriers for smaller specialists even as it expands the commercial scale of the North America GPU liquid cooling market.

Key Report Takeaways

- By cooling type, single-phase liquid cooling led with 74.13% revenue share in 2025, while two-phase cooling is projected to expand at a 28.47% CAGR through 2031.

- By cooling level, component-level cooling accounted for 56.27% share in 2025, while server and rack-level cooling is projected to grow at a 28.23% CAGR through 2031.

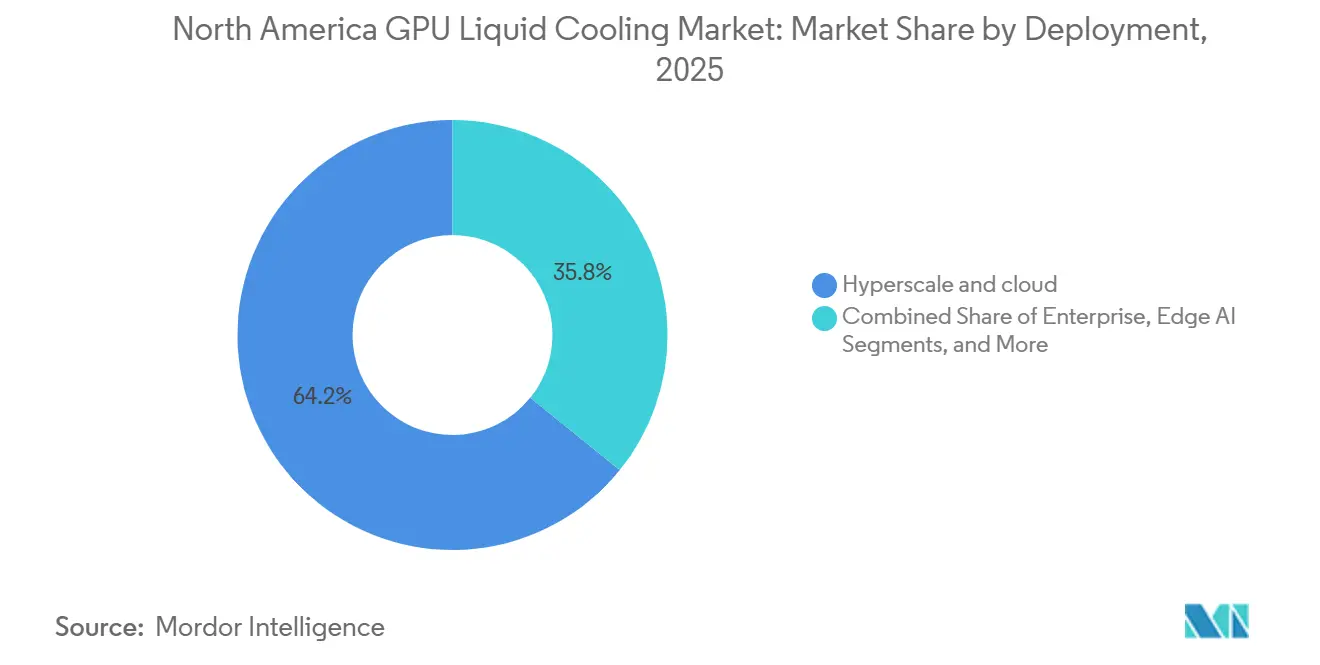

- By deployment, hyperscale and cloud environments held 64.19% of the North America GPU liquid cooling market share in 2025, while enterprise deployments are projected to expand at a 27.89% CAGR through 2031.

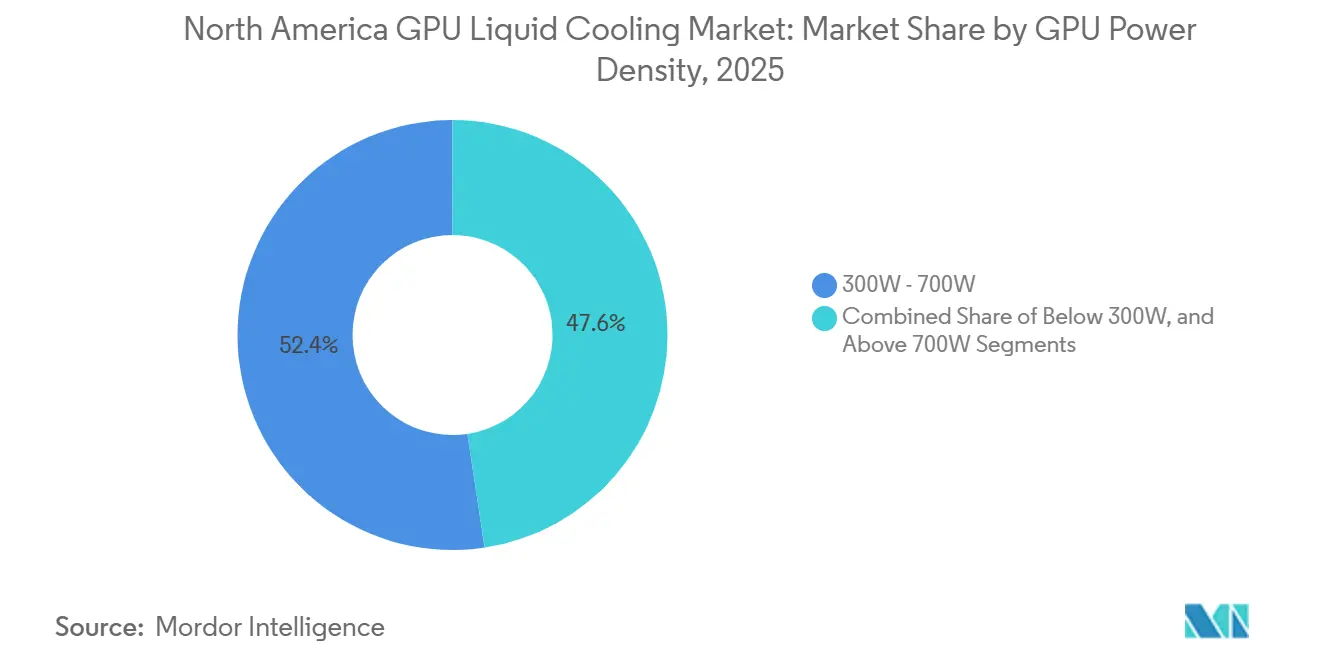

- By GPU power density, the 300W-700W tier captured 52.38% share in 2025, while the above-700W tier is projected to grow at a 27.64% CAGR through 2031.

- By geography, the United States led with 87.61% revenue share in 2025, while Canada is projected to expand at a 27.41% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America GPU Liquid Cooling Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Adoption Of High-Density GPUs In Data Centers | +7.5% | Global, concentrated in US hyperscale corridors such as Northern Virginia, Texas, and Arizona | Short term (≤ 2 years) |

| Acceleration Of AI Training Requiring Advanced Thermal Management | +6.0% | US and Canada, with spillover to Mexico nearshore campuses | Short term (≤ 2 years) |

| Energy-Efficiency Mandates Driving Liquid Cooling Adoption | +4.2% | North America, with early gains in California, New York, and Washington | Medium term (2-4 years) |

| Rising Carbon-Neutral Commitments By Hyperscalers | +3.3% | Global, with US and Canada most affected by operator decarbonization programs | Medium term (2-4 years) |

| Availability Of Utility Incentives For Water-Saving Cooling Solutions | +2.1% | US Pacific Northwest, Texas, and Canadian provinces with clean-power availability | Medium term (2-4 years) |

| Emergence Of GPU-Powered Edge Micro Data Centers | +1.6% | Distributed across North America, with early traction in US tier-2 cities and Canadian urban centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Adoption Of High-Density GPUs In Data Centers

GPU thermal design power has moved into a range where liquid cooling is now a structural requirement for the North America GPU liquid cooling market, not a premium feature. NVIDIA stated that the H100 SXM5 operated at 700W, which already placed dense AI nodes near the practical ceiling for air cooling in many facilities. Microsoft stated in April 2026 that the GB200 NVL72 rack-scale system draws around 120kW at full load and that the Vera Rubin NVL72 platform has no air-cooled configuration, which confirms that future high-end GPU systems are being designed around liquid cooling from the outset. NVIDIA also highlighted DOE-backed COOLERCHIPS work aimed at lowering cost and improving efficiency versus traditional air-cooled designs, which shows that public-sector validation is moving in the same direction as vendor roadmaps. This means operators that already built liquid-ready facilities for earlier GPU generations are now in a better position to absorb Blackwell and post-Blackwell systems, and that advantage is accelerating procurement across the North America GPU liquid cooling market in 2026.

Acceleration Of AI Training Requiring Advanced Thermal Management

Large AI training clusters place GPUs under sustained full-load conditions for long periods, and that makes thermal stability a reliability issue as much as an energy issue for the North America GPU liquid cooling market. Amazon stated in 2025 that its custom direct-to-chip closed-loop liquid cooling system moved from prototype to production in 11 months, raised compute power by 12%, and cut energy use by up to 46% against earlier air-cooled designs.[1]Amazon Web Services, “AWS Rolls Out Liquid Cooling in Data Centers,” About Amazon, aboutamazon.comAmazon also stated that the system circulates coolant in a sealed loop without increasing net water consumption, which directly addresses water sensitivity in many U.S. locations. Microsoft stated in April 2026 that it had deployed hundreds of thousands of liquid-cooled NVIDIA Grace Blackwell GPUs across Azure in under one year and had become the first hyperscale provider to power NVIDIA Vera Rubin NVL72 systems. Supermicro stated in May 2025 that its DLC-2 platform can reduce data center power use by up to 40% and lower the total cost of ownership by up to 20%, which shows the supply chain is now matching hyperscale demand with deployable commercial systems.

Energy-Efficiency Mandates Driving Liquid Cooling Adoption

Energy and water performance rules are becoming a stronger adoption trigger for the North America GPU liquid cooling market because higher-density AI systems are harder to support within older efficiency assumptions. Washington enacted HB 2515 in 2025, which requires large emerging energy-use facilities to move toward 100% clean energy over time and to disclose water and refrigerant information, pushing data center design closer to measurable operating accountability.[2]Washington State Legislature, “HB 2515, Relating to Emerging Large Energy Use Facilities,” Washington State Legislature, leg.wa.gov The ENERGY STAR program for data centers continues to set a performance benchmark around a PUE of 1.4 or better, which adds pressure on operators whose thermal designs cannot hold efficiency at higher rack densities.[3]U.S. Environmental Protection Agency, “ENERGY STAR for Data Centers,” ENERGY STAR, energystar.gov Schneider Electric stated in January 2026 that raising the technology cooling system supply temperature by 20°C can reduce total cooling energy use by 40% and lower water use by up to 60%, which strengthens the business case for liquid-based thermal designs that can operate at warmer temperatures.[4]Schneider Electric, “When Air Isn’t Enough, The Liquid Cooling Revolution,” Schneider Electric Insights, se.comAs these reporting and performance expectations spread, compliance is increasingly influencing equipment selection early in the design cycle, which supports steady growth in the North America GPU liquid cooling market.

Rising Carbon-Neutral Commitments By Hyperscalers

Sustainability targets are influencing cooling architecture choices in the North America GPU liquid cooling market because large operators now need solutions that reduce both energy use and water draw. Microsoft stated in December 2024 that it redesigned its next-generation data centers to consume zero water for cooling through closed-loop chip-level systems, and it began piloting that approach in Phoenix, Arizona, and Mount Pleasant, Wisconsin, in 2026. Microsoft later stated in its 2025 Environmental Sustainability Report that it remained on track to replenish more water than it consumes globally across operations, which ties the cooling redesign to a broader operating target rather than a single pilot. Meta stated in December 2025 that it is pursuing a 2030 water-positive goal and is sharing water stewardship progress around its data center footprint, which reinforces that thermal design now sits inside wider environmental planning. These commitments are steadily pushing buyers away from evaporative-heavy approaches and toward closed-loop direct-to-chip and advanced liquid systems, which strengthen long-run demand across the North America GPU liquid cooling market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Initial Capital Expenditure For Liquid Cooling Infrastructure | -3.2% | North America-wide, with the sharpest impact in brownfield enterprise retrofits | Short term (≤ 2 years) |

| Limited Industry Standards For Two-Phase Coolants | -1.5% | Global, with particular impact on US and Canadian enterprise and government segments | Medium term (2-4 years) |

| Skill Gap In Liquid Cooling Maintenance Workforce | -1.1% | North America-wide, concentrated in US tier-2 and tier-3 data center markets | Medium term (2-4 years) |

| Perceived Risk Of Coolant Leakage In Mission-Critical Servers | -0.8% | Global, with the strongest caution in US financial services and government HPC environments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Initial Capital Expenditure For Liquid Cooling Infrastructure

Upfront project cost still slows parts of the North America GPU liquid cooling market, especially where operators must retrofit older buildings instead of designing for liquid from the start. Liquid cooling requires added equipment such as coolant distribution units, manifolds, piping, cold plates, and control systems, and those layers make first-pass budgets heavier than comparable air-cooled programs. Open Compute Project guidance for modular thermal control systems also shows that CDU design needs a capacity margin for redundancy and future density growth, which can increase infrastructure scope before operators even reach full utilization. Schneider Electric stated in January 2026 that reference designs for NVIDIA GB300 NVL72 systems already support up to 142kW per rack, which illustrates the scale of thermal infrastructure now being planned into high-end AI deployments. Vendors are responding with modular and scalable CDU platforms, but the need to commit capital early still slows adoption among enterprises and public-sector buyers, which tempers the pace of the North America GPU liquid cooling market outside hyperscale environments.

Limited Industry Standards For Two-Phase Coolants

Two-phase systems remain one of the most promising areas in the North America GPU liquid cooling market, but procurement confidence is still limited by the lack of broad standards around coolant choice, circuit design, and operating safeguards. Vertiv stated in 2025 that pumped two-phase direct-to-chip cooling can reduce cooling energy consumption by up to 82%, which explains why interest is rising so quickly despite the remaining hesitations. Open Compute Project stated in its 2024 white paper that two-phase refrigerant-based direct liquid cooling requires careful implementation because corrosion and leak risks can be higher than in single-phase approaches. That leaves many buyers relying on vendor-specific testing instead of broadly transferable standards, which increases switching risk in regulated or mission-critical environments. Open Compute Project's work on modular thermal control systems shows that the standards base is moving forward, but until it matures further, this issue will continue to moderate adoption in parts of the North America GPU liquid cooling market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment: Hyperscale Keeps The Lead, While Enterprise Adoption Broadens

Hyperscale and cloud deployments captured 64.19% of the North America GPU liquid cooling market share in 2025, which reflects the spending power and build pace of the largest cloud operators. Amazon stated in 2025 that it developed a custom direct-to-chip closed-loop liquid cooling design that increased compute power by 12% and cut energy use by up to 46%, which shows why hyperscale operators are standardizing around liquid systems instead of treating them as experimental. Microsoft stated in April 2026 that it had already deployed hundreds of thousands of liquid-cooled Grace Blackwell GPUs across Azure, which confirms that cloud-scale implementation is now happening at commercial speed. These deployments shape the wider North America GPU liquid cooling market because supplier roadmaps, validation work, and facility design choices often follow hyperscale demand first. The North America GPU liquid cooling industry is therefore still being led by buyers that can move entire fleets toward a liquid-first standard.

Enterprise is projected to grow at a 27.89% CAGR through 2031, making it the fastest-growing deployment segment as procurement barriers begin to ease. The main shift is that liquid cooling is no longer viewed only as a hyperscale solution, because proven performance data from cloud deployments has started to reduce perceived execution risk for private operators. Government and research buyers are also getting clearer signals from DOE-backed cooling efforts that support next-generation modular thermal systems and better efficiency than legacy air-cooled setups. Edge AI remains the smallest deployment group, but GRC stated in November 2025 that its ICEraQ Nano system was built specifically for smaller data rooms and communications closets, which shows that the North America GPU liquid cooling market is beginning to extend beyond core campuses into distributed inference locations.

By Cooling Level: Component-Level Precision Leads, While Rack-Level Platforms Expand Faster

Component-level cooling held 56.27% share in 2025 and remained the largest cooling level in the North America GPU liquid cooling market because cold-plate direct-to-chip designs match the heat profile of modern GPUs and CPUs with far greater precision than room-level airflow management. This approach keeps cooling focused on the devices that generate most of the heat, which improves thermal control without forcing the entire room into a higher-cost cooling model. Frore Systems stated in May 2026 that lowering GPU temperature by 8°C below the thermal limit can help sustain compute throughput, which explains why chip-level thermal stability is directly tied to performance value. That direct link between temperature and usable performance has helped component-level solutions retain leadership even as rack power keeps climbing. The North America GPU liquid cooling market still depends heavily on these cold-plate architectures because they offer the clearest path for both greenfield and retrofit programs.

Server and rack-level cooling is projected to expand at a 28.23% CAGR, which makes it the fastest-growing cooling level as AI systems move toward denser rack-scale integration. Microsoft stated in April 2026 that NVIDIA Vera Rubin NVL72 is designed as a fully liquid-cooled platform with no air-cooled option, which supports the shift from individual component decisions to larger rack-level thermal design choices. LiquidStack stated in May 2026 that its GigaModular CDU platform supports deployments up to 14MW, which reflects how vendors are building for whole-system and multi-rack thermal management rather than single-node optimization alone. CoolIT Systems stated in February 2026 that its manufacturing and engineering work supports AI chips above 4,000W and server racks above 500kW, which signals that higher-capacity fluid management is moving to the center of product design. Open Compute Project guidance reinforces that CDU systems need scalability and redundancy, so rack-level procurement is becoming more strategic across the North America GPU liquid cooling market.

By Cooling Type: Single-Phase Still Sets The Base, While Two-Phase Gains Momentum

Single-phase cooling accounted for 74.13% of the North America GPU liquid cooling market size in 2025, which shows how strongly it remained tied to present deployment models. Its lead comes from a practical advantage, because water-glycol direct-to-chip systems fit more easily with chilled-water infrastructure that many operators already understand. Schneider Electric stated in January 2026 that its reference designs for NVIDIA GB300 NVL72 support up to 142kW per rack through single-phase liquid-to-chip architecture, which shows the format can already scale to current AI system requirements. That matters for the North America GPU liquid cooling market because buyers are still balancing high thermal performance with manageable deployment risk, especially in retrofits and phased expansions. Single-phase systems also remain easier to explain to procurement and operations teams, which keeps them in a strong position as organizations move from pilot projects to routine buildouts.

Two-phase cooling is projected to grow at a 28.47% CAGR through 2031, making it the fastest-moving cooling type in the North America GPU liquid cooling market. Vertiv stated in 2025 that pumped two-phase direct-to-chip systems can cut cooling energy use by up to 82%, which gives the segment a clear performance argument where electricity and thermal density are both under pressure. Frore Systems stated in May 2026 that advanced liquid thermal designs can support inlet temperatures as high as 53°C and can eliminate the need for mechanical chillers in some use cases, which points to a broader operating advantage when facilities are designed around liquid first. Open Compute Project has also acknowledged the move toward wider adoption of modular thermal control systems, so the North America GPU liquid cooling industry is likely to keep single-phase as its near-term base while two-phase steadily takes more strategic deployments.

By GPU Power Density: Mid-Range Volume Supports Spend, While Ultra-High Density Lifts Growth

The 300W-700W tier represented 52.38% of the North America GPU liquid cooling market size in 2025, which reflects the broad installed base of H100-generation hardware across AI training and inference clusters. NVIDIA stated that the H100 SXM5 operated at 700W, and that power range became a key point where many dense AI racks moved beyond practical air-cooling limits. This tier should continue to support a large share of spending because installed systems will keep generating retrofit, service, expansion, and replacement demand through the forecast period. The below-300W segment still matters for lower-density inference deployments where hybrid cooling setups remain workable, and capital intensity must be controlled. Even so, the North America GPU liquid cooling market is increasingly being defined by platforms that sit at the top of the power curve rather than by the lowest-density installed base.

The above-700W tier is projected to grow at a 27.64% CAGR through 2031, which makes it the strongest value-creation band in the market. Microsoft stated in April 2026 that GB200 NVL72 racks draw around 120kW and that Vera Rubin systems are being delivered without air-cooled options, which confirms that ultra-high density platforms are being designed around liquid infrastructure from the rack level upward. NVIDIA stated in April 2025 that the Blackwell platform offers more than 300x better water efficiency than traditional air-cooled architectures at the rack level, which strengthens the case for liquid deployment in sites facing tighter sustainability and reporting pressure. That means value growth in the North America GPU liquid cooling market comes from two directions at once, because more systems are moving into this density band and each rack requires higher-capacity thermal hardware. This shift is also changing how the North America GPU liquid cooling industry prices performance, because thermal headroom is now tied directly to rack design, uptime, and usable compute output.

Geography Analysis

The United States held 87.61% of North America GPU liquid cooling market share in 2025, which kept it far ahead of the rest of the region in deployed thermal infrastructure and active project volume. The country’s lead reflects the concentration of hyperscale campuses in major AI and cloud corridors such as Northern Virginia, Silicon Valley, Phoenix, Chicago, and Dallas-Fort Worth, where high-density GPU clusters are being installed at commercial scale. Microsoft stated in December 2024 that it redesigned next-generation facilities to use zero water for cooling and began piloting that design in Phoenix, Arizona, and Mount Pleasant, Wisconsin, in 2026, which shows that the U.S. is also serving as the main proving ground for new thermal architectures. Vertiv stated in April 2026 that it would expand its Ironton, Ohio facility to raise U.S. production capacity for advanced liquid cooling and chilled water systems by around 45%, which adds domestic supply depth to the North America GPU liquid cooling market. Schneider Electric also stated in January 2026 that its NVIDIA-validated reference designs support up to 142kW per rack for GB300 NVL72 systems, which helps shorten deployment cycles across U.S. hyperscale builds.

Canada is projected to grow at a 27.41% CAGR through 2031, making it the fastest-growing geography in the North America GPU liquid cooling market. Accelsius stated in November 2025 that DarkNX agreed to deploy a 300MW NeuCool-enabled AI data center campus in Ontario, which points to unusually large-scale adoption for a market that still has a smaller installed base than the United States. Telehouse Canada stated in May 2026 that it deployed direct liquid-to-chip cooling at its downtown Toronto campus with cabinet densities up to 120kW per rack and heat transfer into district energy systems, which shows that commercial implementation is spreading beyond new greenfield sites. Bell Canada also stated in 2026 that its Saskatchewan 300MW data center project carries CAD 1.7 billion (USD 1.24 billion) in total investment, with CAD 1.3 billion (USD 0.95 billion) expected to be deployed in 2026, and that the site uses a closed-loop cooling system that draws no municipal water.

Mexico remains a smaller part of the North America GPU liquid cooling market, but its role is improving as U.S. operators look for nearshore capacity where domestic power constraints and permitting delays are becoming harder to manage. Its opportunity is linked less to immediate scale and more to adjacency, because colocation and enterprise operators can use Mexican sites to serve North American latency needs while avoiding some of the bottlenecks seen in core U.S. hubs. Early demand is likely to favor closed-loop and dry-cooler-based systems that can perform without heavy dependence on municipal water supply. That means Mexico should stay behind the United States and Canada in total value, but it is still likely to add incremental demand as regional deployment patterns diversify.

Competitive Landscape

The North America GPU liquid cooling market remains moderately concentrated at the system-integration level, and competition is moving from standalone hardware toward broader thermal platforms that combine facility infrastructure, controls, and chip-level engineering. Trane Technologies completed its acquisition of LiquidStack in March 2026, which added direct-to-chip, single-phase, and two-phase immersion cooling, and modular CDU capabilities to its commercial thermal portfolio. Vertiv then acquired Strategic Thermal Labs in April 2026, extending its capabilities into cold plate design and server-side thermal validation, which strengthens the link between facility cooling systems and chip-level heat rejection. Schneider Electric had already acquired a controlling interest in Motivair in February 2025, giving it a liquid cooling portfolio that spans CDUs, rear-door heat exchangers, cold plates, and chillers. These moves show that the North America GPU liquid cooling market is becoming harder for smaller independent specialists to navigate on their own, because customers increasingly want integrated supply and service depth.

Competitive differentiation is also being shaped by validation and manufacturability, not just thermal performance claims. Schneider Electric stated in January 2026 that its reference designs were validated for NVIDIA GB300 NVL72 deployments, which gives it an advantage with buyers that want shorter deployment timelines and lower integration risk. CoolIT Systems stated in February 2026 that it had delivered triple-digit production capacity growth over two years and supported cooling for AI chips above 4,000W and racks above 500kW, which shows how manufacturing scale is becoming a competitive filter in the North America GPU liquid cooling market. Motivair by Schneider Electric also launched the MCDU-70 in January 2026 with scaling capability to 10MW and beyond, which indicates that vendors are positioning around AI factory deployments rather than isolated rack upgrades.

At the same time, the field is not closed, because specialist vendors still have room where standards are unsettled or deployment needs are more specialized. Two-phase direct-to-chip remains one of the clearest openings, since Open Compute Project guidance shows the category is progressing while still lacking a fully mature standards base. Edge AI thermal management is another opening, because chassis-based precision cooling, immersion systems, and compact rack platforms are still competing without one model taking clear control. GRC stated in November 2025 that ICEraQ Nano was built for smaller rooms and closets, while its March 2026 partnership with UNICOM Engineering aimed to simplify industrial-scale immersion deployments, which shows how specialists are trying to defend focused niches within the North America GPU liquid cooling market.

North America GPU Liquid Cooling Industry Leaders

CoolIT Systems Inc.

Asetek Inc.

LiquidStack Inc.

GRC (Green Revolution Cooling)

Submer Technologies S.L.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Telehouse Canada deployed direct liquid-to-chip cooling across its downtown Toronto metro data center campus, with rack densities up to 120kW per rack. The deployment, the first of its kind in a Canadian carrier hotel, includes heat transfer to Enwave's district energy system for repurposing as municipal heating.

- April 2026: Vertiv acquired Strategic Thermal Labs, a specialist in advanced liquid cooling, specifically cold plate design and server-side thermal validation. The acquisition strengthened Vertiv's engineering capability at the interface between server-side liquid cooling and facility infrastructure.

- April 2026: Vertiv announced the expansion of its Ironton, Ohio, manufacturing facility to increase production capacity for advanced liquid cooling and chilled water systems by approximately 45%, with operations expected in Q2 2027.

North America GPU Liquid Cooling Market Report Scope

GPU liquid cooling is a thermal management solution in which a liquid coolant, typically water or a dielectric fluid, is circulated through a closed-loop system to dissipate heat generated by a graphics processing unit. The system generally comprises a cold plate mounted on the GPU, a pump, tubing, a radiator, and fans; the coolant absorbs heat from the GPU and transfers it to the radiator, where it is released into the surrounding air. Compared to traditional air cooling, liquid cooling offers superior thermal efficiency, reduced operating temperatures, and lower noise levels, thereby enabling higher performance, improved stability, and extended component lifespan, particularly in high-performance computing, gaming, and data center applications.

The North America GPU Liquid Cooling Market Is Segmented By Cooling Type (Single-Phase, and Two-Phase), Cooling Level (Component-Level, and Server/Rack-Level), Deployment (Hyperscale/Cloud, Enterprise, Government And Research (HPC), and Edge AI), GPU Power Density (Below 300W, 300W-700W, and Above 700W), And Geography (United States, Canada, and Mexico). The Market Forecasts Are Provided In Terms Of Value (USD).

| Single-Phase Liquid Cooling |

| Two-Phase Liquid Cooling |

| Component-Level Cooling |

| Server / Rack-Level Cooling |

| Hyperscale / Cloud |

| Enterprise |

| Government & Research (HPC) |

| Edge AI |

| Below 300W |

| 300W - 700W |

| Above 700W |

| North America |

| United States |

| Canada |

| Mexico |

| By Cooling Type | Single-Phase Liquid Cooling |

| Two-Phase Liquid Cooling | |

| By Cooling Level | Component-Level Cooling |

| Server / Rack-Level Cooling | |

| By Deployment | Hyperscale / Cloud |

| Enterprise | |

| Government & Research (HPC) | |

| Edge AI | |

| By GPU Power Density | Below 300W |

| 300W - 700W | |

| Above 700W | |

| By Geography | North America |

| United States | |

| Canada | |

| Mexico |

Key Questions Answered in the Report

What is the North America GPU liquid cooling market size through 2031?

The North America GPU liquid cooling market is valued at USD 1.90 billion in 2026 and is projected to reach USD 5.90 billion by 2031, growing at a 25.37% CAGR over 2026-2031.

Why is liquid cooling becoming necessary for GPU deployments in North America?

GPU power density has risen to levels where air cooling is no longer practical for dense AI racks. Systems such as GB200 NVL72 and future Vera Rubin platforms are being built around liquid cooling from the start.

Which cooling type leads current spending and which one is growing fastest?

Single-phase cooling led with 74.13% share in 2025 because it fits existing infrastructure more easily. Two-phase cooling is growing fastest, with a projected 28.47% CAGR through 2031.

Which customer group is driving most spending on these systems?

Hyperscale and cloud deployments accounted for 64.19% of revenue in 2025. Large cloud providers are setting the technical and procurement standard for the rest of the region.

Which country is growing the fastest in this region?

Canada is the fastest-growing geography, with a projected 27.41% CAGR through 2031. Growth is being supported by large AI data center investments and early direct liquid cooling rollouts.

What is the main barrier to wider adoption outside hyperscale sites?

The biggest restraint is the high upfront cost of liquid-ready infrastructure, especially in brownfield retrofits. Buyers also remain cautious where standards for two-phase coolants are still evolving.

Page last updated on: