North America GPU Cooling Solutions Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

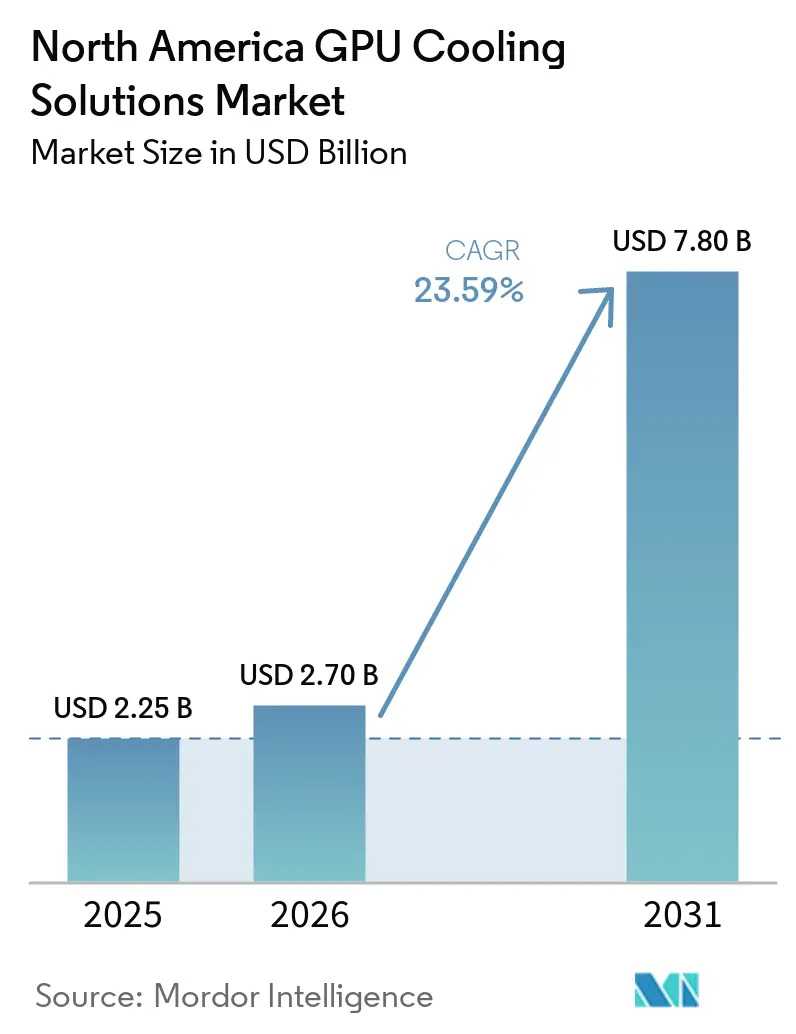

| Base Year Market Size (2025) | USD 2.25 Billion |

| Market Size (2026) | USD 2.70 Billion |

| Market Size (2031) | USD 7.80 Billion |

| Growth Rate (2026 - 2031) | 23.59% CAGR |

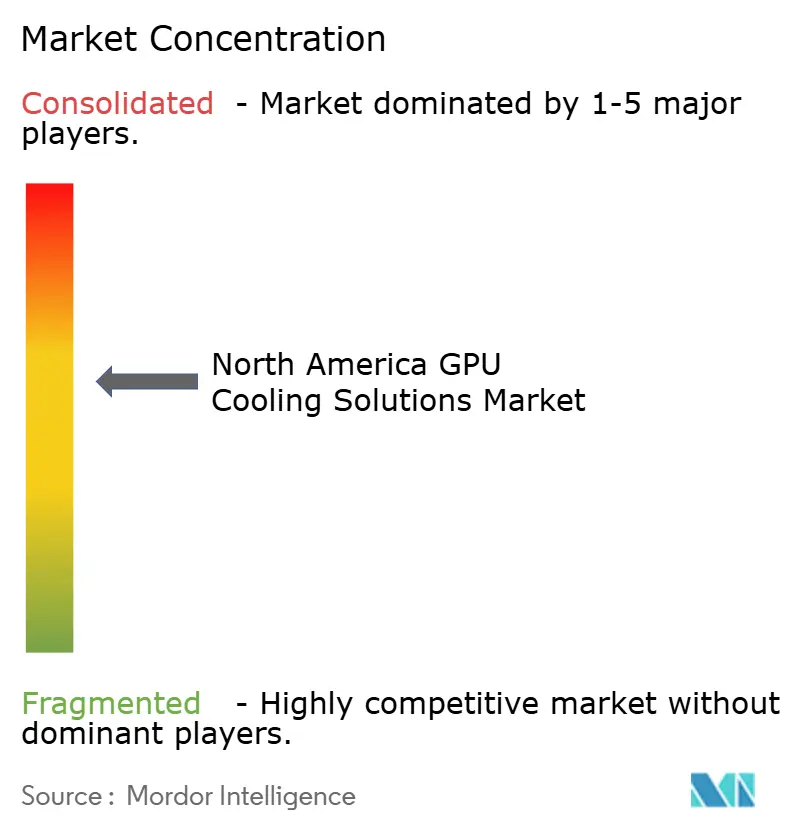

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America GPU Cooling Solutions Market Analysis by Mordor Intelligence

The North America GPU cooling solutions market size is projected to expand from USD 2.25 billion in 2025 and USD 2.70 billion in 2026 to USD 7.80 billion by 2031, registering a CAGR of 23.59% between 2026 to 2031. The market is moving beyond incremental thermal upgrades because current AI clusters are being designed around continuous high-heat GPU operation rather than occasional performance peaks. Cooling has become a core infrastructure decision because operators now evaluate thermal systems by their effect on power use, rack density, uptime, and deployment speed. The North America GPU cooling solutions market is also being shaped by a clear shift toward liquid-ready architecture, modular coolant distribution, and rack-level design standards that align with next-generation GPU platforms. Competitive activity is centered on validated reference designs, multi-supplier qualification, and faster commercialization of liquid cooling systems that can support denser racks without full facility redesign. Adoption still faces friction from retrofit economics and supply chain pressure, but these factors are shifting the timing of demand rather than weakening the long-term expansion of the North America GPU cooling solutions market.

Key Report Takeaways

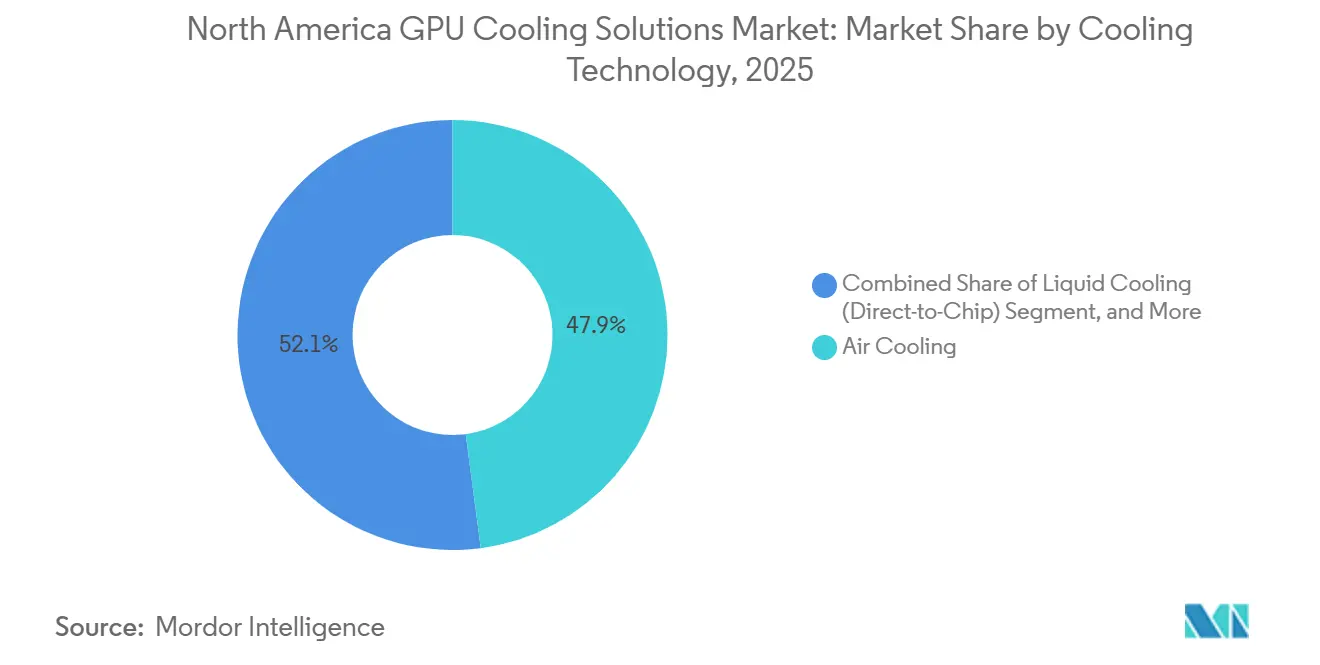

- By cooling technology, air cooling led with a 47.90% share in 2025, while immersion cooling is projected to expand at the 24.12% pace through 2031.

- By cooling level, server and rack-level cooling held 59.35% share in 2025 and is also expected to record the highest growth through 2031.

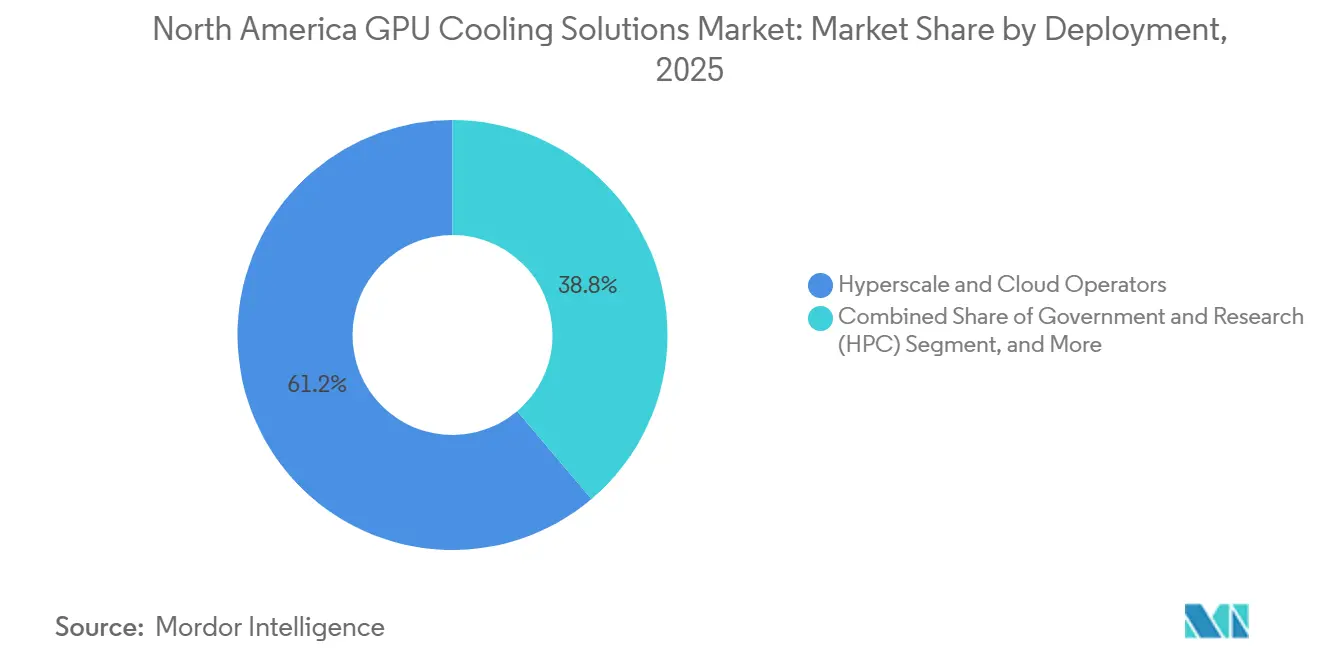

- By deployment, hyperscale and cloud operators represented 61.20% share of the North America GPU cooling solutions market in 2025, while enterprise deployments are projected to post the 25.14% CAGR through 2031.

- By GPU power density, the 300 W-700 W tier accounted for 49.65% share in 2025, while above-700 W systems are expected to expand at the 26.12% over 2026-2031.

- By country, the United States accounted for 87.45% share in 2025, while Canada is projected to be the fastest-growing at 25.59% country market through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America GPU Cooling Solutions Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge In GPU Workloads For Generative AI And Large Language Models | +6.5% | Global, with North America as primary epicenter, concentrated in Northern Virginia, Texas, and the Pacific Northwest | Short term (≤ 2 years) |

| Growing Adoption Of Liquid Cooling To Reduce Data Center PUE | +5.0% | North America and EU, hyperscale clusters in Oregon, Ohio, and Calgary | Short term (≤ 2 years) |

| Increased Preference For Modular, Scalable Cooling Architectures | +3.5% | North America, early gains in Dallas and Northern Virginia colocation corridors | Medium term (2-4 years) |

| Advances In Heat Pipe And Vapor Chamber Technologies | +2.5% | Global supply chain, US R&D centers and Taiwan OEM manufacturing partnerships | Medium term (2-4 years) |

| Data Center Sustainability Mandates And Carbon-Neutral Targets | +2.0% | California, Colorado, federal US agencies, Canadian provinces | Long term (≥ 4 years) |

| Government Incentives For Edge Data Centers In Rural Areas | +1.0% | Rural US, including Wyoming, Iowa, and Montana, and Canadian provinces including Saskatchewan and Alberta | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge In GPU Workloads For Generative AI And Large Language Models

The strongest demand trigger in the North America GPU cooling solutions market is the move from traditional cloud workloads to AI factory deployments built around high-density accelerators. NVIDIA Blackwell Ultra raises thermal design power to around 2,000 W per GPU, compared with around 700 W for the earlier A100 generation, which pushes many legacy air-cooled layouts beyond their practical operating range. That shift matters because operators are no longer cooling short training bursts alone; they are preparing for sustained inference activity that keeps thermal stress high for far longer periods. A 2025 study on H100 systems found that liquid-cooled nodes delivered around 17% higher TFLOPS per GPU under sustained load than comparable air-cooled systems, which shows that thermal design is now tied directly to usable compute output. In the North America GPU cooling solutions market, cooling decisions are increasingly being made alongside GPU procurement because thermal architecture now affects throughput, reliability, and power efficiency at the same time.[1]NVIDIA, “NVIDIA Blackwell Platform Boosts Water Efficiency by Over 300x,” NVIDIA Blog, blogs.nvidia.com

Growing Adoption Of Liquid Cooling To Reduce Data Center PUE

Liquid cooling has moved from an efficiency upgrade to a design requirement for facilities that intend to support current AI platforms at commercial scale. NVIDIA stated in 2025 that its Blackwell platform can improve water efficiency by more than 300x in liquid-cooled deployments, which reinforces why operators are treating liquid systems as part of core infrastructure planning rather than optional optimization. Vertiv also reported that its reference architecture for the NVIDIA GB300 NVL72 platform reduced annual energy consumption by 25% and lowered the power footprint by 30%, which gives buyers a clearer operating case for large-scale deployment. These gains are changing colocation economics because facilities that can prove lower power overhead and better thermal control are better positioned in hyperscaler and enterprise procurement cycles. The North America GPU cooling solutions market is therefore being pulled forward by the combined effect of denser racks, tighter energy targets, and buyer preference for cooling systems that improve both uptime and facility efficiency.[2]Vertiv, “Vertiv Develops Energy-Efficient Cooling and Power Reference Architecture for the NVIDIA GB300 NVL72 Platform,” Vertiv, vertiv.com

Increased Preference For Modular, Scalable Cooling Architectures

Cooling systems are now being planned around uncertain future expansion because GPU generations are moving quickly, and rack power demand can change within a short deployment cycle. This is increasing the appeal of modular coolant distribution systems that let operators add capacity in stages instead of redesigning the full plant. In January 2026, Motivair by Schneider Electric launched the MCDU-70 as a 2.5 MW CDU that can scale to 10 MW and beyond through EcoStruxure integration, which reflects growing demand for expandable liquid infrastructure. In March 2026, DCX Liquid Cooling Systems launched an enterprise CDU portfolio ranging from 600 kW to 2.6 MW in standard rack and in-row formats, aimed directly at operators entering direct-to-chip cooling for the first time. In the North America GPU cooling solutions market, modularity is lowering adoption friction because it turns liquid cooling from a large one-time commitment into a staged capacity decision.

Advances In Heat Pipe And Vapor Chamber Technologies

Component-level thermal design is still advancing quickly, even as direct liquid cooling and immersion systems gain more attention in high-density deployments. Frore Systems introduced LiquidJet Nexus in 2026 for half-U AI server trays and reported 75% higher heat transfer efficiency, no tray-level hoses or connectors, and a 65% reduction in thermal stack weight, which shows how much performance remains to be unlocked inside the server itself. A March 2026 paper in Communications Engineering reported that direct-to-package microfluidic cooling channels achieved a coefficient of performance above 10³ at a delta T of 60°C while using much less coolant volume than traditional heat sink approaches. These developments matter because they improve thermal headroom, serviceability, and package-level efficiency across increasingly dense GPU systems. The North America GPU cooling solutions market continues to reward suppliers that can improve component-level heat movement because those advances shape what can be achieved at the server and rack levels.[3]Frore Systems, “Frore Systems Introduces LiquidJet Nexus - Defining the AI Thermal Stack for Next-Generation 1-2 U AI Server Systems Like NVIDIA Kyber,” Frore Systems, froresystems.com

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Capex For Immersion Cooling Retrofits | -1.8% | North America, with highest burden in legacy East Coast and Midwest colocation facilities | Short term (≤ 2 years) |

| Supply Chain Volatility In Coolant Fluids And Pump Components | -1.2% | Global sourcing, APAC manufacturing hubs directly affecting North America deployments | Medium term (2-4 years) |

| Skill Gap In Designing And Maintaining Liquid-Cooled Racks | -0.8% | US enterprise and mid-market segments, Canada secondary markets | Medium term (2-4 years) |

| Reliability Concerns Around Dielectric Fluid Contamination | -0.5% | North America, particularly enterprise retrofits with legacy metal infrastructure | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Capex For Immersion Cooling Retrofits

Immersion cooling still faces a clear adoption barrier in retrofit settings because older halls were not built for the floor loading, piping layout, and service model these systems demand. That challenge is most visible in enterprise and colocation sites where operators need to add AI capacity without shutting down the broader facility. A loaded immersion configuration can also require structural reinforcement, which pushes the retrofit decision closer to a major building project rather than a simple equipment swap. This is why the North America GPU cooling solutions market shows faster immersion uptake in greenfield hyperscale builds than in legacy enterprise environments. Direct-to-chip systems often become the preferred first step because they offer a lower-disruption path into liquid cooling while still supporting higher GPU density.

Supply Chain Volatility In Coolant Fluids And Pump Components

Supply chain risk remains a real restraint because critical pump assemblies, fluid couplings, and qualified coolant options are still concentrated across a limited set of suppliers and production locations. The pressure increased after the exit of key fluorinated fluid capacity, which forced operators to rethink sourcing for two-phase immersion programs and pushed more attention toward alternative chemistries. In January 2026, Infinium introduced its Edge immersion cooling platform and positioned its proprietary fluids around sustained thermal performance and lower contamination risk, which shows how vendors are trying to widen the approved fluid base. The North America GPU cooling solutions market also remains exposed to longer qualification cycles because operators want proven compatibility across cold plates, fluids, manifolds, and racks before committing to scale. Suppliers with broader sourcing options and certified fluid portfolios are therefore gaining an advantage as buyers put more weight on long-term serviceability and procurement security.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Cooling Technology: Air Cooling Leads By Installed Base, But Immersion Gains Momentum

Air cooling retained a 47.90% share of the North America GPU cooling solutions market size in 2025, supported by the large installed base of enterprise and colocation facilities that were not originally designed for liquid infrastructure. That position reflects existing capacity more than new design preference, because the North America GPU cooling solutions market is now being built around far denser GPU clusters than earlier halls could support. Once racks move into current high-density AI configurations, the physical limit of air cooling becomes much harder to manage without large power and space penalties. This is why most new hyperscale AI deployments now start with liquid-ready or fully liquid-cooled plans instead of treating liquid systems as a later upgrade.

Direct-to-chip liquid cooling has consolidated its position as the main deployment path for current high-density GPU systems because it balances thermal performance with manageable facility change. Product launches across the vendor base show that supply-side readiness has moved well beyond pilot status in the North America GPU cooling solutions market. Vertiv published a validated reference architecture for the NVIDIA GB300 NVL72 platform in 2025, and Supermicro expanded its liquid-cooled portfolio around NVIDIA Blackwell systems, which together point to a clear commercial shift toward liquid-first infrastructure. Immersion cooling is still the fastest-growing at 24.12% technology category because frontier AI clusters are moving beyond 100 kW per rack and need more aggressive heat removal strategies. Hybrid designs also remain relevant in the North America GPU cooling solutions industry because many operators must support mixed GPU generations and varied thermal profiles within the same hall.

By Cooling Level: Rack-Scale Design Becomes The Primary Unit Of Choice

Server and rack-level cooling held 59.35% of the North America GPU cooling solutions market share in 2025 and is also the fastest-growing cooling level through 2031. That dual position shows how buyers now treat the rack, rather than the individual component, as the main thermal and procurement unit for AI infrastructure. The North America GPU cooling solutions market is reinforcing this shift because GPU packages, memory, and interconnects are being designed as one tightly linked thermal zone. DCX reflected that direction in January 2026 when it introduced its 8 MW Facility Distribution Unit for warm-water cooling in next-generation NVIDIA deployments, replacing multiple smaller legacy CDUs with a centralized design.

Component-level cooling still matters because each server node needs tighter thermal control as power density rises inside standard footprints. In March 2026, ZutaCore said its OmniTherm cold plate enabled waterless two-phase cooling for NVIDIA RTX PRO 6000 Blackwell Server Edition GPUs in a single-slot PCIe form factor, which shows that precision cooling remains a commercial differentiator. Accelsius added to that trend in May 2026 with the NeuCool IR150, a rack-level solution that combines a two-phase CDU, 42U of rack space, and integrated manifolds in a single enclosure supporting up to 150 kW. The boundary between component and rack-level cooling is therefore becoming less rigid because suppliers increasingly package both functions into one deployable system. This is one of the clearer signs that the North America GPU cooling solutions industry is moving toward integrated thermal platforms rather than isolated cooling parts.

By Deployment: Hyperscale Sets The Base, While Enterprise Expands Faster

Hyperscale and cloud operators represented 61.20% of the North America GPU cooling solutions market share in 2025, which reflects the scale of capital deployment required for dense AI clusters. This part of the North America GPU cooling solutions market continues to lead because hyperscalers can build around liquid systems from day one and qualify new GPU platforms faster than most other buyer groups. NVIDIA stated in 2025 that AWS data centers using liquid-cooling solutions developed with NVIDIA reduced energy consumption by 46% while increasing compute power by 12%, which strengthens the case for liquid-first design in large cloud environments. The result is a deployment pattern where hyperscalers still anchor total demand, even as the next phase of growth broadens across other customer groups.

Enterprise deployments are the fastest-growing segment at 25.14% over 2026-2031 because more organizations are placing AI inference workloads inside private or colocated environments. Unlike hyperscalers, most enterprise operators need solutions that fit within existing halls, existing service teams, and tighter staged budgets. That dynamic favors direct-to-chip CDUs, modular rollout, and liquid-ready rack upgrades instead of full immersion conversions at the outset. Government and high-performance computing deployments also retain strategic importance because public research programs help set technology benchmarks that later influence commercial procurement. HRL Laboratories stated in February 2026 that its Low-Chill single-phase cooling technology, developed under the US Department of Energy ARPA-E COOLERCHIPS program, can deliver a 40% increase in cooling capability or more than 10x lower pumping power, which supports further adoption across the North America GPU cooling solutions market.

By GPU Power Density: The 300 W-700 W Range Dominates, While Above 700 W Drives The Next Wave

The 300 W-700 W tier held 49.65% share of the North America GPU cooling solutions market size in 2025, making it the broadest deployed density band across inference accelerators, training systems, and enterprise AI hardware. This segment remains important because it gives buyers flexibility to choose between advanced air cooling and direct-to-chip liquid systems, depending on facility readiness. It also serves as the main entry point for first-time liquid adopters who want better thermal control without rebuilding the full environment. In February 2026, HRL Laboratories said its Low-Chill direct liquid cooling technology was designed to support high heat flux GPU applications while improving cooling capability and reducing pumping power, which fits well with this density range.

The above-700 W tier is the fastest-growing at 26.12% band because the latest GPU platforms are moving beyond the thermal limits that earlier hybrid approaches could still manage. Supermicro stated in May 2026 that its DCBBS platform for NVIDIA Vera Rubin NVL72 and related systems was built on a full direct-liquid-cooling stack and targeted 10x throughput per watt compared with prior Blackwell solutions, which captures how quickly thermal requirements are escalating. That means the North America GPU cooling solutions market is no longer planning around whether liquid cooling is needed at the highest densities, but around which liquid architecture best fits each deployment. The below-300 W tier remains relevant for edge inference and constrained environments, where compact solutions can still preserve usable GPU performance without broad facility water infrastructure. Frore Systems and ZutaCore both show that smaller-format thermal innovation still has room in the North America GPU cooling solutions industry, even as the commercial spotlight stays on the highest-density systems.

Geography Analysis

The United States accounted for 87.45% of the North America GPU cooling solutions market size in 2025, which keeps it far ahead of the rest of the region in both installed base and new high-density deployment activity. The country remains the anchor of the North America GPU cooling solutions market because hyperscale operators, cloud platforms, GPU server vendors, and supporting power and thermal suppliers are concentrated there. That scale advantage is reinforced by the pace of reference design validation around current NVIDIA platforms, which has kept many first-wave liquid cooling deployments centered in the United States. Vertiv’s validated GB300 NVL72 cooling architecture and Supermicro’s direct-liquid-cooled Vera Rubin platform both show how much of the region’s commercialization path is still being set in the US market. Public research support also matters because programs tied to the US Department of Energy continue to influence cooling system performance targets and vendor road maps.

Canada is the fastest-growing sub-market in the North America GPU cooling solutions market over 2026-2031 because operators see a combination of available power, cooler climate conditions, and room for large-scale AI buildouts. In March 2026, BCE committed CAD 1.7 billion (USD 1.24 billion) to build a 300 MW AI data center in Saskatchewan with Cerebras and CoreWeave as signed tenants, and the project specified closed-loop liquid cooling with no municipal water draw. Alberta is also gaining relevance, with eStruxture naming CoreWeave as anchor tenant for its CAL-3 AI-ready facility in March 2026. British Columbia is part of the same trend, where HIVE’s Buzz HPC expanded its liquid-cooled AI data center footprint in 2026 and positioned the site for more than 4,000 next-generation GPUs. These moves show why Canada is shifting from a secondary option to an active capacity destination within the North America GPU cooling solutions market.

Mexico remains the smallest geography in the North America GPU cooling solutions market, even though Monterrey, Mexico City, and Querétaro continue to attract interest for larger data center campuses. Its appeal is tied to lower land costs and useful proximity to key connectivity routes linked to the United States. At the same time, grid reliability differences, a less mature support ecosystem for advanced cooling, and more limited local supply options are slowing adoption of the most complex liquid architectures. Mexico is therefore likely to remain a gradual growth market where cooling sophistication rises over time as AI inference demand expands across the wider region.

Competitive Landscape

The North America GPU cooling solutions market remains moderately fragmented, with competition spread across thermal infrastructure vendors, specialized liquid cooling firms, server OEMs, and GPU ecosystem partners. Large suppliers are not competing on hardware alone; they are competing on validated reference designs, service readiness, and their ability to support faster deployment of dense AI racks. Vertiv strengthened its position in March 2026 by providing simulation-ready digital power and cooling assets for NVIDIA Vera Rubin DSX AI factories, which help customers move from design to deployment more quickly. Schneider Electric’s Motivair business also advanced its role in January 2026 with a scalable CDU platform built for next-generation AI factories, which supports customers who need multi-stage liquid expansion rather than a one-time build. These actions show that the North America GPU cooling solutions market increasingly rewards vendors that can connect design validation, hardware scale, and operating efficiency in one offer.

Smaller and emerging companies are also gaining ground by solving narrower problems that matter in real deployments. ZutaCore secured qualification in March 2026 for waterless two-phase cooling of NVIDIA RTX PRO 6000 Blackwell Server Edition GPUs, which gives it a path into enterprise racks that cannot easily accept water inside the server. Accelsius used a different route by launching the NeuCool HyperStart program with the NeuCool IR150 in May 2026, giving hyperscale operators a faster validation path for two-phase direct-to-chip cooling. Frore Systems added pressure at the component level by targeting half-U AI server trays, which shows that new competition is entering well below the full-facility layer. In the North America GPU cooling solutions market, this mix of large-system vendors and focused specialists keeps the field active and prevents the competitive structure from consolidating too quickly.

Server OEMs are responding by qualifying more than one cooling partner at the same time so they can reduce lead-time exposure and preserve bargaining flexibility. That approach matters because buyers want certified interoperability across cold plates, manifolds, fluids, and rack-level distribution without depending on a single vendor stack. Environmental compliance is also becoming a quieter procurement filter, especially where fluid chemistry and long-term material compatibility can affect approval cycles. Suppliers with strong validation records, scalable product families, and broader sourcing options are therefore better positioned as the North America GPU cooling solutions market expands across hyperscale and enterprise demand.

North America GPU Cooling Solutions Industry Leaders

NVIDIA Corporation

Dell Technologies Inc.

Hewlett Packard Enterprise Company

Lenovo Group Limited

Super Micro Computer, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Accelsius announced general availability of the NeuCool IR150, described as the first fully integrated rack-level cooling solution combining a two-phase CDU, 42U of IT rack space, and built-in liquid and vapor manifolds in a single 800 mm-wide enclosure supporting up to 150 kW, alongside the NeuCool HyperStart program to accelerate hyperscale operator validation of two-phase direct-to-chip cooling at scale.

- March 2026: BCE (Bell Canada) is committed to investing CAD 1.7 billion (approximately USD 1.24 billion) in a 300 MW AI data center in Saskatchewan, with Cerebras and CoreWeave signed as anchor tenants. The project specifies closed-loop liquid cooling that draws no municipal water and is exploring a district energy system to reuse waste heat for nearby university campuses.

- March 2026: Vertiv announced its role in NVIDIA Vera Rubin DSX AI factory reference design, delivering simulation-ready digital power and cooling assets and validated infrastructure building blocks designed to compress time from design to deployment for AI factory operators.

- March 2026: DCX Liquid Cooling Systems launched its ECDU portfolio of enterprise CDUs spanning 600 kW to 2.6 MW in standard rack and in-row footprints, specifically designed for mid-market AI pilot clusters, colocation tenants, and regional cloud providers adopting direct-to-chip liquid cooling for the first time.

North America GPU Cooling Solutions Market Report Scope

GPU Cooling Solutions are integrated systems and technologies designed to dissipate heat generated by graphics processing units (GPUs) during operation, thereby maintaining optimal thermal performance, reliability, and longevity. These solutions encompass a range of methods, including air cooling, liquid cooling (direct-to-chip), immersion cooling, and hybrid approaches, and are implemented at various levels, such as component-level or server/rack-level architectures. They are critical in high-performance computing environments, data centers, hyperscale cloud platforms, and AI/ML workloads, where GPU power densities often exceed 300W, requiring efficient thermal management to prevent throttling and hardware failure and to ensure sustained computational throughput.

The North America GPU Cooling Solutions Market Report is Segmented by Cooling Technology (Air Cooling, Liquid Cooling (Direct-to-Chip), Immersion Cooling, and Hybrid Cooling), Cooling Level (Component-Level Cooling and Server / Rack-Level Cooling), Deployment (Hyperscale / Cloud, Enterprise, Government and Research (HPC), and Edge), GPU Power Density (Below 300W, 300W - 700W, and Above 700W), and Geography (United States, Canada, and Mexico). The Market Forecasts are Provided in Terms of Value (USD).

| Air Cooling |

| Liquid Cooling (Direct-to-Chip) |

| Immersion Cooling |

| Hybrid Cooling |

| Component-Level Cooling |

| Server / Rack-Level Cooling |

| Hyperscale / Cloud |

| Enterprise |

| Government and Research (HPC) |

| Edge |

| Below 300W |

| 300W - 700W |

| Above 700W |

| United States |

| Canada |

| Mexico |

| By Cooling Technology | Air Cooling |

| Liquid Cooling (Direct-to-Chip) | |

| Immersion Cooling | |

| Hybrid Cooling | |

| By Cooling Level | Component-Level Cooling |

| Server / Rack-Level Cooling | |

| By Deployment | Hyperscale / Cloud |

| Enterprise | |

| Government and Research (HPC) | |

| Edge | |

| By GPU Power Density | Below 300W |

| 300W - 700W | |

| Above 700W | |

| By Country | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

What is the size of the North America GPU cooling solutions market?

The North America GPU cooling solutions market was valued at USD 2.25 billion in 2025, reaches USD 2.70 billion in 2026, and is forecast to reach USD 7.80 billion by 2031 at a 23.59% CAGR.

Which cooling technology currently leads regional demand?

Air cooling led in 2025 with a 47.90% share, mainly because many enterprise and colocation sites still operate on legacy thermal infrastructure.

Which cooling approach is growing the fastest through 2031?

Immersion cooling is the fastest-growing technology category as AI rack densities move beyond what conventional air systems can support efficiently.

Why are hyperscale operators still the largest buyers?

Hyperscale and cloud operators held 61.20% share in 2025 because they can fund liquid-ready builds from day one and deploy dense AI clusters faster than other user groups.

What power-density tier matters most today, and what comes next?

The 300 W-700 W band held 49.65% share in 2025, but above-700 W systems are expanding fastest as new GPU generations move into much higher thermal ranges.

Which country is creating the biggest new growth opportunity after the United States?

Canada is the fastest-growing country market through 2031, supported by large AI data center commitments in Saskatchewan, Alberta, and British Columbia and a stronger fit for liquid-cooled expansion.

Page last updated on: