Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

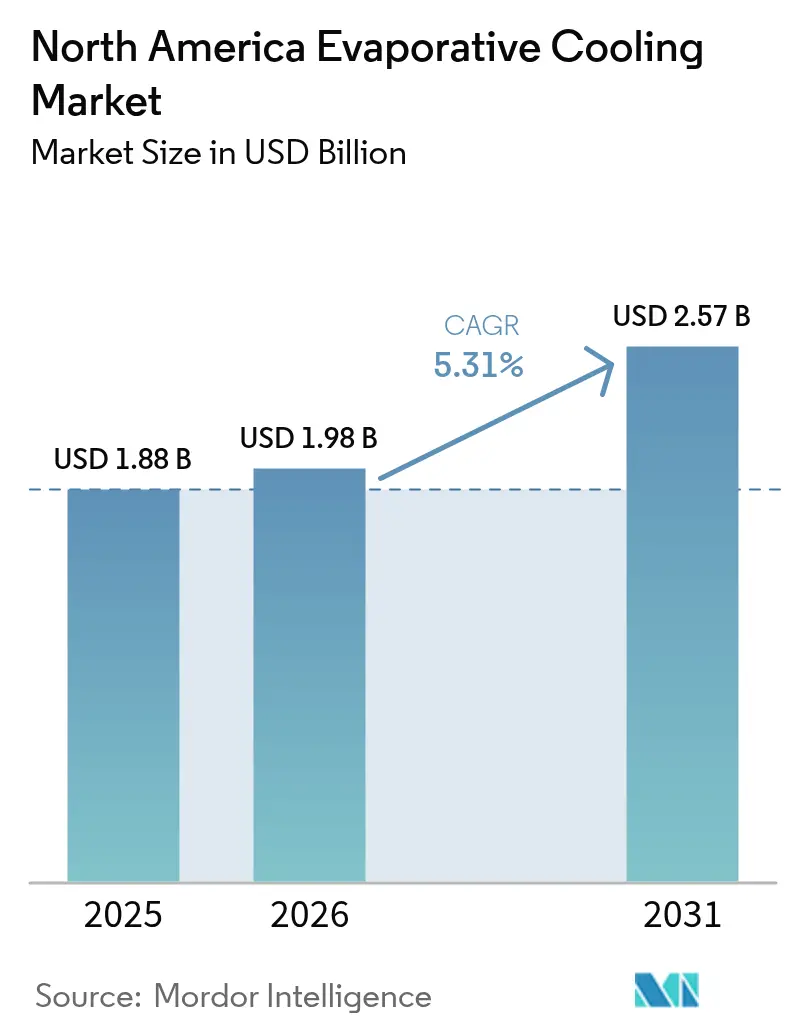

| Base Year Market Size (2025) | USD 1.88 Billion |

| Market Size (2026) | USD 1.98 Billion |

| Market Size (2031) | USD 2.57 Billion |

| Growth Rate (2026 - 2031) | 5.31% CAGR |

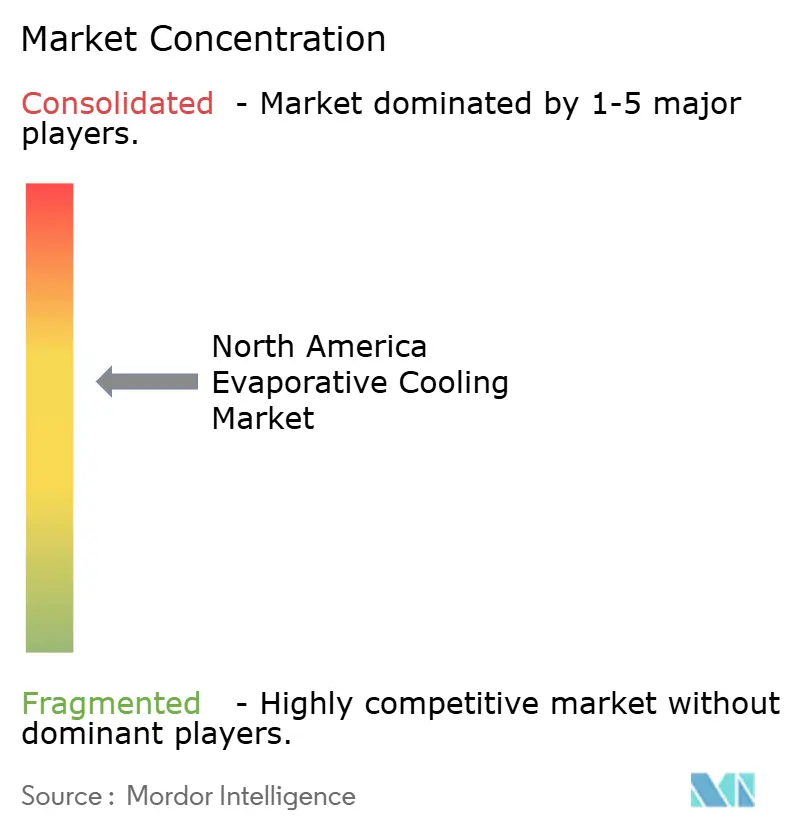

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Evaporative Cooling Market Analysis by Mordor Intelligence

The North America evaporative cooling market size was valued at USD 1.88 billion in 2025 and estimated to grow from USD 1.98 billion in 2026 to reach USD 2.57 billion by 2031, at a CAGR of 5.31% during the forecast period (2026-2031). This growth trajectory reflects the region's accelerating shift toward energy-efficient cooling solutions, driven by escalating data center demands and stringent environmental regulations. The market's expansion centers on three critical macro forces: data center operators pursuing sub-1.1 PUE targets, industrial facilities complying with energy efficiency mandates, and water-scarce regions implementing cooling restrictions that favor hybrid adiabatic systems over traditional evaporative towers.

Key Report Takeaways

- By cooling method, direct evaporative systems led with 63.20% revenue share in 2025, while two-stage indirect-direct units are forecast to post the highest 5.69% CAGR through 2031.

- By application, industrial facilities captured 36.60% of the North America evaporative cooling market size in 2025; data centers are projected to expand at a 5.34% CAGR to 2031.

- By component, equipment such as coolers and towers held a 70.30% share in 2025, whereas pads and media are expected to grow at a 11.05% CAGR over the forecast period.

- By sales channel, HVAC contractors and integrators commanded 48.00% revenue share in 2025, with online retail and e-commerce anticipated to record a 15.4% CAGR through 2031.

- By geography, the United States accounted for 79.10% of 2025 regional sales, while Mexico is on track for the fastest 5.21% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Evaporative Cooling Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-center shift to low-PUE cooling | +1.8% | United States, Canada | Medium term (2-4 years) |

| Industrial and commercial energy-efficiency mandates | +1.2% | North America | Long term (≥ 4 years) |

| CAP-ex advantage vs. compressor-based HVAC | +0.9% | Global | Short term (≤ 2 years) |

| Renewable-microgrid + evaporative hybrid roll-outs | +0.7% | United States, Mexico | Long term (≥ 4 years) |

| Cannabis and controlled-environment agriculture demand | +0.5% | United States, Canada | Medium term (2-4 years) |

| Bio-based/hydrogel pads extending maintenance cycles | +0.3% | North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data-center shift to low-PUE cooling

Hyperscale operators are deploying adiabatic precooling modules that shave condenser inlet temperatures by up to 40 °F, freeing as much as 14 MW for IT loads in a 300 MW campus.[1]Peak Plus Energy, “Design Day. Peak PUE. Utilization,” peakplus.energy Microsoft’s closed-loop zero-water designs and NREL’s underground thermal energy storage trials highlight an ecosystem focused on water-neutral, power-lean architectures.[2]National Renewable Energy Laboratory, “Reducing Data Center Peak Cooling Demand...,” nrel.gov Immersion-ready evaporative towers licensed by Baltimore Aircoil further illustrate convergence between liquid and air side solutions.[3]Baltimore Aircoil Company, “BAC Secures Exclusive Rights…,” baltimoreaircoil.com As AI workloads heighten rack densities, indirect-direct stages deliver tighter thermal bands without compressor lift, placing evaporative cooling at the core of digital-infrastructure expansion.

Industrial and commercial energy-efficiency mandates

Title 24 in California now stipulates 350 Btuh/W minimums for evaporative-cooled condensers above 8,000 MBH and requires wet-bulb responsive variable-speed fans. Federal refrigerant rules that phase out GWP > 750 options accelerate the adoption of natural refrigerant systems feedable by evaporative rejectors. Natural Resources Canada mirrors U.S. thresholds, enabling cross-border equipment harmonization. Together, these policies lock in minimum performance levels that favor adiabatic or hybrid towers capable of 75% energy savings versus direct expansion chillers.[4]MDPI, “Measuring the Energy Efficiency of Evaporative Systems…,” mdpi.com

CAP-ex advantage vs. compressor-based HVAC

Direct systems consume 0.3-1.2 kW/ton versus 3-5 kW/ton for mechanical refrigeration, shrinking electrical infrastructure needs in brownfield revamps. Cambridge Air’s ESC-Series underscores the economic edge, delivering 60-80% energy cuts while supplying 100% outside air for improved indoor quality. EVAPCO’s adiabatic coolers remove chemical treatment costs and trim pump maintenance, reinforcing a total-cost-of-ownership narrative that resonates as carbon pricing escalates.

Renewable-microgrid + evaporative hybrid roll-outs

Photovoltaic-powered indirect/direct units have achieved coefficients of performance above 35 in pilot studies leveraging underground water sources. GE Vernova’s AirJoule venture blends atmospheric water harvesting with evaporative cooling, targeting self-regenerating HVAC deployments. California healthcare microgrids pairing solar thermal with desiccant-enhanced evaporative cooling documented 20% utility savings during grid outages. These integrations position evaporative platforms as anchor assets within distributed-energy ecosystems that seek carbon-neutral resilience.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Climate humidity dependency | -0.8% | Southeastern United States | Long term (≥ 4 years) |

| Escalating water-scarcity regulations | -1.1% | Western United States | Short term (≤ 2 years) |

| Wildfire-smoke IAQ compliance hurdles | -0.6% | Western United States, Canada | Medium term (2-4 years) |

| Skilled-labor shortages for scale-control and hygiene | -0.4% | North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Climate humidity dependency

Evaporative effectiveness declines sharply when relative humidity climbs above 60%, leaving southeastern states reliant on hybrid desiccant-evaporative pairs. Simulations for Mexicali confirm viability only during seasonal low-humidity windows, necessitating backup dehumidification in peak months. Although dew-point indirect stages extend performance envelopes, added complexity narrows the Cap-ex gap that defines the North America evaporative cooling market advantage.

Water-scarcity regulations

Las Vegas now blocks new evaporative permits, while Texas data centers drew 400 million gallons in 2024, spurring community pushback. Codes in Nevada cap usage at 3.5 gal/ton-hour and demand overflow alarms with automatic shutoffs. Municipal mandates for reclaimed water in Los Angeles and Phoenix reinforce a transition toward primarily dry adiabatic modes, compelling vendors to redesign pads and spray cycles for minimal consumption. The tighter rules temper growth in the North America evaporative cooling market even as they push innovation toward closed-loop and atmospheric-source designs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Cooling Method: Direct Systems Dominate Despite Hybrid Innovation

Direct units retained a 63.20% foothold in the North America evaporative cooling market in 2025, reflecting decades of installation across arid western facilities. Indirect towers held 23.70%, favored in food processing and pharmaceuticals that prohibit direct air-water contact. Two-stage indirect-direct designs recorded the fastest 5.69% CAGR, propelled by data-center and high-heat industrial retrofits that need sub-dewpoint delivery without excessive water draw.

Performance gaps are narrowing as perforated dew-point heat exchangers raise indirect effectiveness, enabling supply-air ratios below 0.5 while maintaining low pressure drops. As these materials mature, two-stage platforms are eclipsing single-stage gear in design-build specifications, a trend expected to lift their slice of the North America evaporative cooling market size by 2031. Vendors now integrate chemical-free water treatment and antimicrobial films, extending pad life and alleviating the labor bottleneck facing large campus operators.

By Application: Industrial Leadership Faces Agricultural Innovation

Industrial plants generated 36.60% of 2025 revenue, driven by food, chemical, and general-manufacturing loads that prioritize robust operation and energy savings. Data centers, although smaller, are growing at a 5.34% CAGR as AI accelerates rack heat densities beyond what air-conditioned CRAC units can manage. Controlled-environment agriculture, greenhouses, and confinement farming chart a 8.74% CAGR, benefiting from the legalization of cannabis and vertical-farm momentum that positions evaporative solutions as low-energy, humidity-tunable alternatives to compressor coils.

Commercial buildings capture a 24.30% share through retail and office retrofits tied to sustainability certifications, while residential adoption advances at a modest 5.12% CAGR, largely confined to dry-climate locales. Agricultural uptake is expected to raise its chunk of the North America evaporative cooling market share beyond 10.5% by 2031 as growers seek low-carbon, low-water HVAC that protects crop transpiration profiles without costly desiccant wheels.

By Component: Equipment Dominance Faces Media Innovation

Equipment, principally coolers and towers, controlled 70.30% of 2025 revenue, underscoring how the capital cost of the primary unit still defines most customer budgets. Pads and other media, however, represent the bright spot: the sub-segment is on track for an 11.05% CAGR through 2031 as bio-based fibers and antimicrobial coatings extend pad life from one season to multiple years. Water-distribution hardware claimed 18.30% of sales thanks to its role in keeping flow even across large heat-exchange surfaces, while intelligent controls and automation made up 6.70% as facility managers look for plug-and-play optimization.

Technology gains sharpen the story. Hydrogel inserts have recorded cooling densities of 320 W/m², and reinforced cellulose pads now survive several cycles before swap-out, trimming labor costs that previously eroded the North America evaporative cooling market size advantage. Service and maintenance, a 4.70% slice today, should expand as smart sensors call for periodic calibration rather than annual overhauls. Suppliers such as EVAPCO are layering antimicrobial treatments directly into the pad matrix, while chemical firms refine additive packages that cut scale build-up and keep hygiene under control. Together, these upgrades improve reliability and lower total cost, easing the skilled-labor bottleneck that has slowed rollouts in some western states.

By Sales Channel: Contractors Lead Despite Digital Disruption

Contractors and integrators held 48.00% of 2025 transactions, a reflection of the design-build expertise required for code compliance and site-specific sizing. Distribution and wholesale partners followed with 31.70%, serving smaller installers that lack factory-direct ties. Direct manufacturer deals, often tied to custom engineering for data centers and process plants, made up 6.10%.

Online retail is the headline mover. E-commerce registered the fastest 15.4% CAGR and is drawing first-time residential buyers who prefer standardized portable coolers that ship ready to plug in. Even so, large commercial jobs still lean on contractors for permitting, commissioning, and long-term service, an edge that cushions them from pure-play digital rivals. Distributors continue to add value through local inventory and 24-hour parts delivery, especially during heat waves when the North American evaporative cooling market share for replacement pads and pumps spikes. The emerging picture is omnichannel: manufacturers cultivate web stores for small orders while nurturing contractor networks for multi-unit projects that demand stamped drawings and on-site startup assistance.

Geography Analysis

The North American evaporative cooling market shows pronounced regional skew driven by humidity profiles, water policy, and industrial composition. Western U.S. deserts, stretching from Arizona through Nevada, deliver the healthiest order pipelines thanks to 10 °F or greater wet-bulb depressions that unlock high EERs absent heavy water use. Title 24’s stringent efficiency clauses and state-level GWP phasedowns reinforce the pivot to hybrid adiabatic towers integrated with natural-refrigerant chillers. Southern states along the Gulf Coast face adoption barriers tied to 70%-plus summertime humidity, prompting interest in liquid-desiccant add-ons that retain some evaporative benefit while managing latent loads.

Canada’s prairie provinces exploit wide diurnal temperature swings, supporting indirect towers in food and agribusiness plants seeking carbon-neutral certification by 2030. Natural Resources Canada’s alignment with U.S. test procedures simplifies cross-border sourcing and encourages multinational operators to standardize on evaporative platforms. Water-quality research underway through federal climate-security programs is expected to produce guidance on reclaimed-water integration, further strengthening the technology’s position in resource-conscious provinces.

Mexico’s northern manufacturing corridor, anchored by Nuevo León and Chihuahua, provides arid conditions ideal for direct towers that cut peak demand at maquiladora campuses. Federal solar incentives and ongoing grid-modernization initiatives enable cost-effective deployment of photovoltaic-powered evaporative coolers in industrial parks. Meanwhile, central plateau cities leverage moderate humidity and high solar irradiance, supporting adoption of solar-assisted indirect coolers in commercial buildings. Collectively, these geographic nuances shape differentiated go-to-market strategies across the North America evaporative cooling market.

Regulatory Landscape

Evaporative cooling in North America is shaped primarily through broader commercial HVAC efficiency and test-regime requirements, rather than standalone evaporative-only rules. In the United States, the Department of Energy (DOE) administers testing, certification, and enforcement frameworks under 10 CFR Part 429 and related equipment standards, while code compliance in many commercial buildings references ASHRAE Standard 90.1 and AHRI procedures to substantiate efficiency claims.

State and provincial requirements for water and energy compliance also influence product design choices. California requirements for evaporative cooling installations and documentation, via California Energy Commission compliance pathways, along with appliance standards addressing water management and performance testing, are reinforcing a shift toward controlled, sensor-driven water quality management and hybrid adiabatic designs in water-stressed areas. In Canada, Natural Resources Canada administers Energy Efficiency Regulations (SOR/2016-311) for large air conditioners and condensing units, supporting cross-border harmonization by building on aligned test methods and performance baselines that affect equipment selection for industrial sites and data center mechanical plants.

Value Chain Analysis

The value chain starts with upstream materials and components, including cellulose-based or engineered media pads, heat-exchanger surfaces, corrosion-protected metal housings, pumps, valves, and variable-speed motor and fan assemblies, along with controls and sensors that manage water quality and part-load operation. Midstream manufacturers and system integrators package direct units, indirect/two-stage systems, and adiabatic fluid coolers into site-specific solutions, with increasing integration into data center heat-rejection architectures alongside liquid cooling loops (such as condenser water and coolant distribution interfaces).

Downstream, HVAC contractors and integrators stay central to specification, permitting, installation, commissioning, and ongoing maintenance, including water treatment, scale control, hygiene, and media replacement. Distribution and wholesale networks support service parts availability (pads, pumps, nozzles, and controls), while large projects increasingly emphasize local and regional sourcing to manage lead times and supply continuity for hyperscale and industrial expansions. Service providers and chemical-free water conditioning offerings, including EVAPCO’s positioning around chemical-free conditioning, add recurring revenue tied to regulatory water constraints and uptime requirements in mission-critical facilities.

Competitive Landscape

Competition is moderate, with the top 5 vendors controlling roughly one-third of revenue. Baltimore Aircoil Company’s license for DUG Technology’s immersion coolers expands its footprint into high-density data-center racks, complementing traditional open-loop towers. Condair’s USD 313.5 million purchase of Kuul secures in-house pad manufacturing and adds a 400,000 ft² Virginia plant that shortens supply lines to eastern hyperscalers. Munters’ partnership with ZutaCore underscores a broader convergence between evaporative reject and liquid direct-to-chip cooling, a hybrid approach increasingly favored by AI workloads.

EVAPCO stands out with its Pulse~Pure chemical-free conditioning, targeting facilities lacking on-site water-chemical expertise. This innovative approach eliminates the need for traditional chemical treatments, reducing environmental impact and operational costs while ensuring effective water conditioning. SPX Cooling Technologies, recognizing the dwindling number of technicians, invests in antimicrobial textured media to extend service intervals. This technology not only enhances system efficiency but also minimizes maintenance requirements, addressing the growing labor shortage in the industry. While new entrants are venturing into gravity-powered and atmospheric-water-harvesting systems, high capital expenditures hinder widespread adoption, even with enticing promises of water neutrality. These systems, though promising in terms of sustainability, face challenges in scaling due to their initial costs and infrastructure demands.

Looking ahead, the depth of portfolios in hybrid adiabatic designs and adherence to tightening water regulations will be pivotal in determining market leaders in North America's evaporative cooling sector.

North America Evaporative Cooling Industry Leaders

Condair Group AG

Munters Group AB

Baltimore Aircoil Company Inc. (BAC)

SPX Cooling Technologies

Delta Cooling Towers Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Data centers continue to drive commercialization for higher-value indirect and hybrid evaporative designs that reduce compressor runtime while tightening thermal control. A concrete example is Munters Oasis indirect evaporative cooling deployed at Sabey Data Center Properties Intergate.Quincy Campus (Washington), using polymer heat exchangers to reject heat without adding moisture to the data hall, illustrating how the approach can scale in climates and applications where humidity management and contamination control are more stringent.

Water constraints are simultaneously limiting legacy open-loop approaches and creating room for hybrid adiabatic equipment, closed-loop concepts, and tighter water-use monitoring at the unit level. The market also has room for faster adoption of advanced pads and media (bio-based, antimicrobial, and extended-life designs) because the pad/media segment is the fastest-growing component category in the current segmentation set, and it directly targets labor and hygiene bottlenecks through longer maintenance cycles. Standards and guidance that influence data center energy performance, including ASHRAE Standard 90.4 and DOE best-practice guidance for energy-efficient data center design, keep evaporative and adiabatic strategies in consideration for both new-build and retrofit mechanical plants, particularly for operators balancing energy targets with local water policy requirements.

Recent Industry Developments

- June 2026: Baltimore Aircoil Company opened a new manufacturing facility near Monterrey, Mexico (Cienega de Flores), following a May 27, 2026, grand opening. The added regional footprint supports shorter lead times and closer project support for Mexico and the US Southwest, where industrial parks and data center buildouts increasingly specify hybrid and adiabatic heat-rejection equipment under tighter water-use requirements.

- April 2026: Munters announced a BSEK 2.0 order for a modular AI cooling solution for a US colocation data center provider, including coolant distribution units (CDUs) and over-the-rack computer room air handlers (CRAHs). The win reinforces the shift toward integrated liquid and air-side architectures in high-density facilities, increasing pull-through for heat-rejection systems where evaporative and adiabatic approaches help reduce compressor dependence.

- October 2024: Wieland completed the acquisition of Onda S.p.A., expanding its heat-exchanger capabilities relevant to efficient cooling and heat-rejection systems used in sustainable retrofit projects. A broader heat-exchanger supply base supports OEMs and integrators as they redesign coils and dry-to-wet hybrid sections to meet evolving energy and water constraints in North American deployments.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenue generated from evaporative cooling solutions sold and installed across North America, including complete units and related parts and services used to deliver cooled air using water evaporation.

Scope exclusions: Refrigerant-based air conditioning and heat pump systems, along with general ventilation equipment that does not use evaporative cooling, are excluded.

Segmentation Overview

- By Cooling Method

- Direct

- Indirect

- Two-Stage (Indirect-Direct)

- By Application

- Residential

- Commercial (Retail, Offices, Hospitality)

- Industrial (Food and Beverage, Chemical, Manufacturing)

- Confinement Farming and Greenhouses

- Others

- By Component

- Equipment (Coolers and Towers)

- Pads and Media

- Water Distribution Systems

- Controls and Automation

- Services and Maintenance

- By Sales Channel

- Direct (Manufacturer to End-User)

- HVAC Contractors / Integrators

- Distribution and Wholesale

- Online Retail / E-Commerce

- By Country

- United States

- Canada

- Mexico

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the market boundary and to collect stable reference indicators that can be tracked year to year. We used public sources such as US Census construction and manufacturing releases, the US Energy Information Administration for electricity and regional demand context, USGS water use publications for water availability signals, and NOAA climate normals to understand where evaporative cooling is technically favored.

To translate those indicators into a usable sizing model, we also reviewed import and export statistics from official customs portals, building and energy code publications (including efficiency standards updates), and publicly available association materials related to HVAC and building performance. Company filings, investor presentations, and trusted industry press were used to cross-check product mix and channel structure, and paid subscriptions for company financials and shipment-level trade data were referenced where public detail was missing. The sources listed above are illustrative only, and many other public documents and data points were also used for clarification and validation.

Primary Interviews and Surveys

Primary work focused on validating what portion of cooling demand is realistically served by evaporative systems in different climates, and how pricing moves across equipment, pads or media, controls, and services. We spoke with manufacturers, distributors, HVAC contractors and integrators, and commercial and industrial buyers across the US, Canada, and Mexico, so assumptions around channel margins, replacement cycles, and project timing could be tested against on-the-ground buying behavior.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 17% | |

| Mid tier: 56% | Functional/Unit leaders: 38% | |

| Smaller Players: 17% | Managers: 45% |

Market-Sizing & Forecasting

The core model starts with a top-down demand pool built from cooling equipment spend and installation activity, and then it is filtered using climate suitability and adoption logic for evaporative systems by end-use. Once the demand pool is formed, we apply price and mix assumptions across direct, indirect, and two-stage systems and then reconcile totals with selective bottom-up checks.

Key inputs used in the model include new construction and renovation activity, heat and humidity patterns by sub-region (which affects where systems can perform), data center and industrial cooling needs where relevant, replacement timing for installed equipment, and an average selling price path by component group (equipment versus pads or media, water distribution parts, controls, and services). Where public data is thin, sampled channel checks were used to approximate volumes and margins, and gaps were handled by using conservative ranges that were then narrowed through interview feedback.

For forecasting, scenario analysis was used because the market is sensitive to weather variability, energy price signals, and capital spending cycles. The base case follows consensus expectations from interviewees on adoption trends and pricing, while alternate cases test faster retrofit uptake in drier states and a slower path in humid zones where performance limits are more pronounced.

Data Validation & Update Cycle

Results were validated through multiple cross-checks so the final number remains consistent with observable market signals. We compared model outputs with independent indicators such as construction activity, trade flows for relevant product categories, and reported channel movement, and then unusual jumps were reviewed until the driver was clearly explained.

Before sign-off, the work is reviewed in steps, starting from scope confirmation, followed by assumption checks, and then a final consistency pass across years and currencies. Reports are refreshed annually, with interim updates triggered by material events such as sharp pricing changes, policy shifts that affect energy efficiency adoption, or visible demand disruptions. Right before delivery, a fresh pass is completed so clients receive the latest updated view.

Mordor Intelligence's North America Evaporative Cooling Market Size Compared Against Other Published Estimates

Published market sizes for North America evaporative cooling can look far apart because the scope boundary and the year used as the anchor point are not always aligned. Differences also come from how pricing is treated, especially when parts, controls, and service revenue are either bundled into the total or left out.

When pricing is refreshed frequently and converted using consistent currency timing, the model is less likely to overstate year-to-year growth from inflation alone, which is where Mordor Intelligence keeps the estimate anchored. Other estimates may lean on older price points, extend the forecast to a different horizon, or include adjacent air-cooler categories without clearly separating two-stage and indirect systems from simpler units.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.88 B (2025) | |

| Regional Consultancy A | USD 3.80 B (2026) | Uses a different start year and longer forecast window, and the scope appears to be broader by application coverage and possible inclusion of wider cooling categories, which can lift the total. |

| Trade Journal B | USD 0.86 B (2022) | Anchored to an earlier year and may not fully reflect later price increases and channel expansion, and it typically emphasizes system types and applications without a detailed add-on for parts and services. |

The spread across sources is largely explained by year alignment and what is counted beyond the main equipment sale. By keeping the scope clear and by tying pricing and mix assumptions to current validation checks, we aim to provide a practical number that can be replicated with visible inputs.

Key Questions Answered in the Report

How large is the North America evaporative cooling market in 2026?

The market stands at USD 1.98 billion in 2026 and is poised to reach USD 2.57 billion by 2031, reflecting a 5.31% CAGR.

Which cooling method grows the fastest through 2031?

Two-stage indirect-direct systems show the highest 5.69% CAGR due to rising data-center and industrial adoption.

Where is geographic growth strongest?

Mexico leads with a 5.21% CAGR through 2031, supported by expanding HVAC exports and arid northern climates optimally suited to evaporative performance.

What regulatory trends are driving adoption?

California’s Title 24 efficiency code, the U.S. refrigerant phasedown, and aligned Canadian standards set performance baselines favoring evaporative designs.

Page last updated on: