Market Overview

| Study Period | 2020 - 2031 |

|---|---|

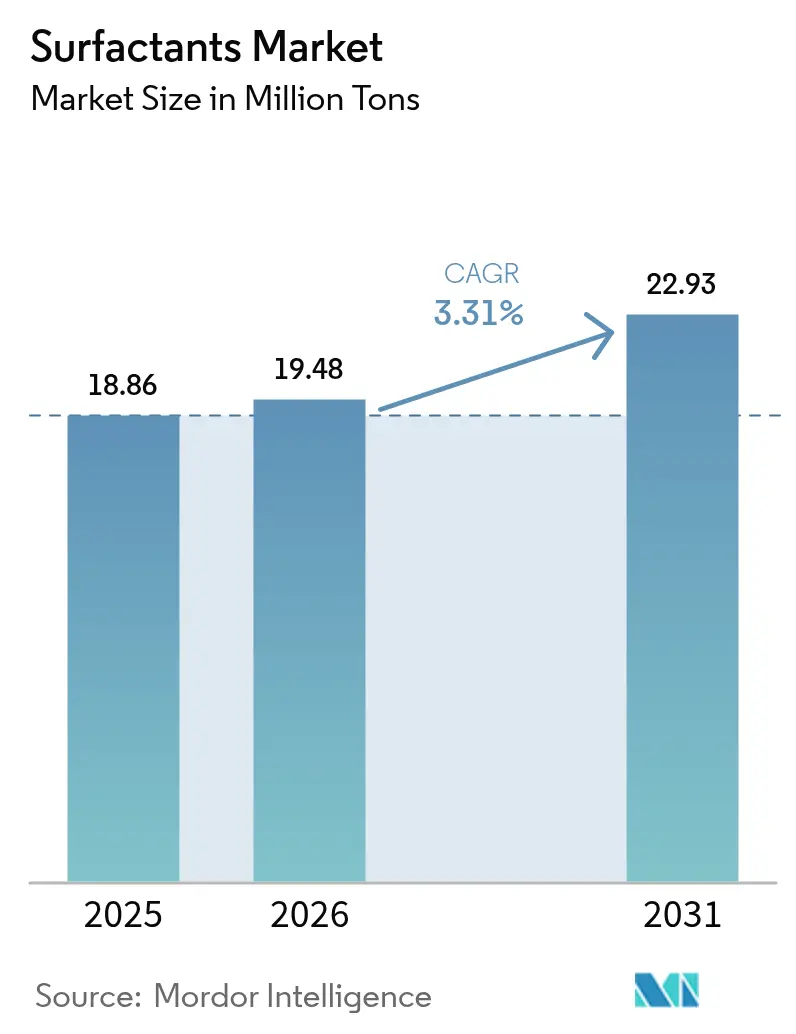

| Market Volume (2026) | 19.48 Million tons |

| Market Volume (2031) | 22.93 Million tons |

| Growth Rate (2026 - 2031) | 3.31% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Surfactants Market Analysis by Mordor Intelligence

Surfactants market size in 2026 is estimated at 19.48 Million tons, growing from 2025 value of 18.86 Million tons with 2031 projections showing 22.93 Million tons, growing at 3.31% CAGR over 2026-2031. Adoption of multifunctional mild surfactants in premium personal-care formats, cold-water laundry detergents that cut energy use, and bio-based feedstocks that satisfy tightening sustainability rules are setting the competitive agenda. Meanwhile, persistent price volatility tied to China’s periodic overcapacity cycles and long-chain alcohol supply swings keeps cost discipline front-of-mind for producers. Integrated players leverage global supply chains and research and development depth to defend share, but specialty biosurfactant suppliers and agile regional firms in Asia-Pacific are steadily eroding historical advantages.

Key Report Takeaways

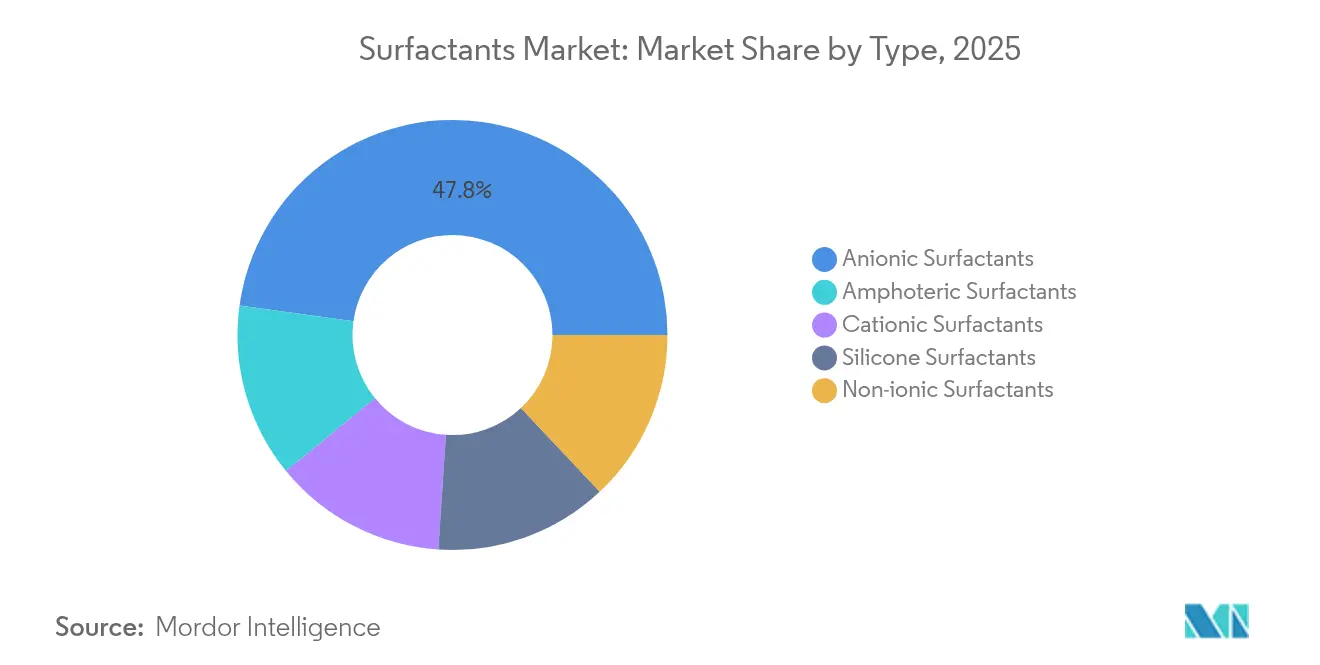

- By type, anionic surfactants held 47.80% of surfactants market share in 2025, whereas amphoteric surfactants are projected to advance at a 4.30% CAGR through 2031.

- By origin, synthetic surfactants accounted for 82.05% of surfactants market size in 2025; bio-based variants are forecast to expand at a 4.17% CAGR to 2031.

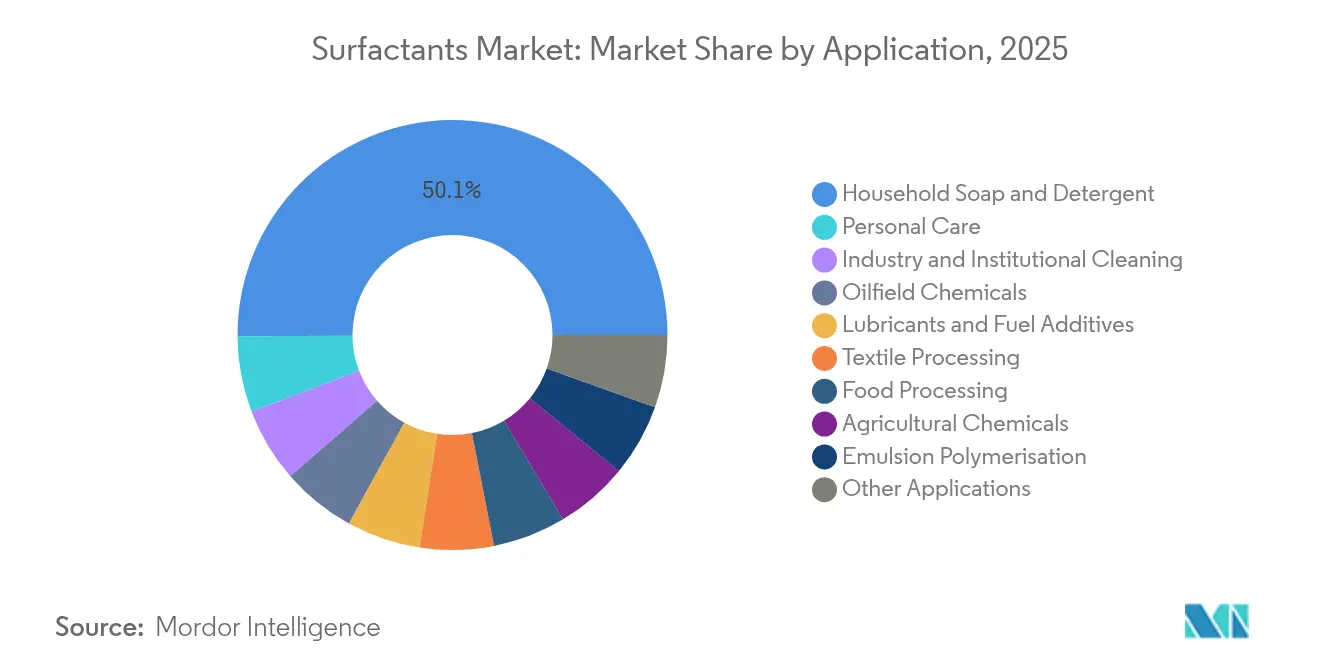

- By application, household detergents commanded 50.10% of surfactants market size in 2025, while personal-care products are expected to post the fastest 4.60% CAGR to 2031.

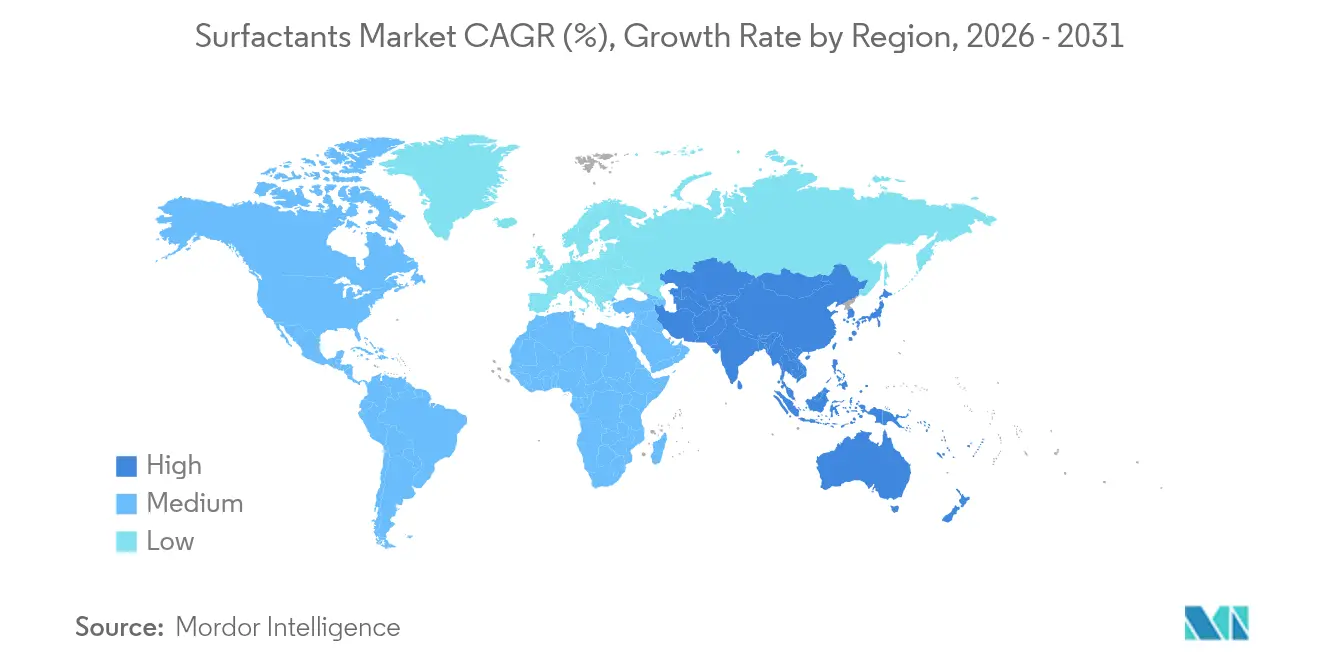

- By geography, Asia-Pacific led with 48.40% surfactants market share in 2025 and is set to outpace all regions with a 4.24% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Surfactants Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Multifunctional mild surfactants in water-less personal-care formats | +0.8% | Global; early gains in North America and Europe | Medium term (2-4 years) |

| Low-temperature laundry detergents demanding high-performance anionics | +0.6% | Asia-Pacific core; spill-over to North America | Short term (≤ 2 years) |

| Shift to bio-based feedstocks via C6–C12 fatty-acid over-supply | +0.5% | Europe and North America; expanding to Asia-Pacific | Long term (≥ 4 years) |

| Enhanced-oil-recovery projects in Middle East Africa and China | +0.4% | Middle East Africa and China | Medium term (2-4 years) |

| On-site sophorolipid fermentation at contract formulators | +0.3% | Global; concentrated in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Multifunctional Mild Surfactants in Water-less Personal-Care Formats

Brands are prioritizing skin compatibility and environmental credentials, prompting formulators to shift from traditional sulfate systems to glucamides and isethionates that deliver gentle cleansing and conditioning in concentrated bars, sticks, and powders. Clariant’s studies show these molecules cut rinse-water volume and energy use while maintaining foaming sensory cues valued by consumers[1]Clariant Ltd Basel, “Mild Surfactants: From Cleansing to Caring,” clariant.com. North American and European shoppers pay premiums for such formats, encouraging BASF to widen its EcoBalanced betaine line that trims product carbon footprints by as much as 30% compared with petro-based counterparts. Rapid ingredient iteration and targeted marketing around water stewardship are preparing the surfactants market for sustained adoption once Asian consumers gravitate toward solid cleansers.

Shift to Bio-Based Feedstocks Enabled by C6–C12 Fatty-Acid Over-Supply

Indonesia’s B35 biodiesel mandate and similar programs unlock abundant medium-chain fatty acids priced competitively with naphtha-based chains, tipping the economics toward renewable surfactant routes. European producers deploy biomass-balance approaches that substitute fossil carbon with renewable inputs without rebuilding assets, while Evonik’s new rhamnolipid plant in Slovakia demonstrates scalable fermentation on European corn sugar. Policy drivers such as the EU’s Deforestation-Free Regulation and Scope 3 carbon accounting sharpen the cost of staying fossil-based, edging synthetic incumbents in the surfactants industry toward mixed portfolios that better align with brand sustainability pledges.

Rise of Enhanced-Oil-Recovery (EOR) Projects in MEA and China

Chemical EOR techniques seek ultra-low interfacial tension and rock wettability alteration to liberate trapped barrels in mature reservoirs. Mixed-charge surfactants tailored for high-temperature carbonate formations cut oil–water interfacial tension from 10 mN/m to below 0.01 mN/m, unlocking recovery factors that extend field life in Oman, Abu Dhabi, and western China. Specialty suppliers command premium pricing thanks to demanding reservoir chemistries, though project approvals fluctuate with crude price cycles. Collaboration between service firms and chemical majors accelerates field trials, positioning the surfactants market for consistent, if episodic, high-margin volumes.

On-Site Fermentation of Sophorolipids at Contract Formulators

Contract manufacturers in the surfactants industry are installing modular bioreactors that convert waste sugar streams into sophorolipids on demand, trimming transport-related emissions and offering brand owners just-in-time supply for niche personal-care launches. Early adopters in Western Europe report lead-time cuts of up to 40% and reduced cold-chain reliance, enhancing resilience against logistics disruptions. The approach also satisfies traceability requirements under evolving ESG audits, making localized biosurfactant production an attractive hedge against geopolitical supply shocks.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| PFAS phase-out driving reformulation costs | −0.4% | Europe and North America; expanding globally | Short term (≤ 2 years) |

| Long-chain alcohol volatility tied to biodiesel policy swings | −0.3% | Global; acute impact in Asia-Pacific | Medium term (2-4 years) |

| Chinese capacity additions triggering price wars | −0.5% | Global; epicenter in Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent PFAS Phase-Out Accelerating Reformulation Costs

Regulators in the EU and the United States have fast-tracked restrictions on per- and polyfluoroalkyl substances, directly affecting roughly 38% of current surfactant end-uses. DIC has already commercialized PFAS-free defoamers for electric vehicle lubricants that match the legacy performance envelope, but the required research and development investment raises unit costs across multiple downstream markets. Reformulation cascades force new stabilizer and processing regimes, stretching technical resources at smaller firms and accelerating consolidation. Early-moving suppliers able to certify compliance win preferred-vendor status even if price premiums persist, influencing the surfactants market.

Long-Chain Alcohol Volatility Linked to Biodiesel Policy Swings

C8–C18 alcohols serve as core building blocks for ethoxylates and sulfates in the surfactants industry, yet their pricing now hinges on rapidly changing biofuel blending mandates. Sudden quota increases divert feedstock away from oleochemical streams, leading to double-digit price spikes that compress margins in commodity anionics. Asian producers most exposed to spot markets endure frequent production cutbacks, prompting formulators to seek chain-length flexibility and dual-sourcing strategies that complicate inventory management.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Anionic Dominance Faces Amphoteric Challenge

Anionic surfactants retained a commanding 47.80% surfactant market share in 2025 as linear alkylbenzene sulfonate (LAS) remained cost-effective and widely approved for household detergents. LAS volumes surpassed 4 million tons, benefiting from scale economies and established supply chains. However, amphoteric molecules such as betaines and amino oxides are projected to record a 4.30% CAGR, the fastest among all types, propelled by their mildness across pH ranges and ability to stabilize complex formulations in premium personal care. The surfactants market is already witnessing major players brandishing eco-certified betaines that secure higher margins while meeting retailer clean-beauty scorecards.

Cationic segments remain small but indispensable in fabric softening and antimicrobial quaternary blends, whereas silicone surfactants carve out niches in textile finishing, enhanced oil recovery, and high-stretch polyurethane foams where their spreadability outperforms carbon-based analogs.

By Origin: Synthetic Dominance Erodes as Bio-Based Gains Momentum

Synthetic chemistries captured an 82.05% surfactants market share in 2025, reflecting decades-old investments in ethylene oxide chains and sulfonation loops that deliver predictable quality and scale efficiencies. Plant footprints across the United States, Western Europe, and coastal China routinely exceed 100 kilotons per site, assuring downstream formulators of steady supplies. Yet bio-based surfactants are projected to outpace at a 4.17% CAGR through 2031 as feedstock assurance, carbon accounting, and consumer sentiment converge.

The emerging rhamnolipid platform underscores a pivot: Evonik’s Slovakian line leverages European corn sugar and modular fermentation, signaling commercial viability for fully biodegradable, high-activity glycolipids that rival premium ethoxylates in mildness. Cost parity remains elusive for high-volume detergent grades, but hybrid approaches in which partial replacement reduces fossil intensity without impairing performance are winning early adopters.

By Application: Household Detergents Lead While Personal Care Accelerates

Household soaps and detergents accounted for 50.10% surfactants market size in 2025, reflecting their entrenched role in daily hygiene. Powder and liquid formats continue to rely on LAS and alcohol ethoxysulfates due to unmatched cost-to-performance ratios, and population growth in South Asia maintains baseline demand. Value-tier SKUs dominate rural channels, cementing high-volume throughput for anionic producers even as premium cold-water pods carve out urban niches. Institutional cleaning for healthcare and food services maintains regulatory-driven stability, though value capture hinges on tailored blends that reduce cleaning cycles and antimicrobial load.

Personal care stands out with a forecast 4.60% CAGR, buoyed by premiumization and skin-health awareness that elevate mild surfactants into mainstream shampoos, facial cleansers, and baby care. Retailers’ “clean label” shelves and social-media influencer campaigns amplify consumer scrutiny of ingredient lists, directing formulators toward amphoteric and glycolipid systems. Premium SKUs fetch price points multiple times the mass-market average, translating limited volume gains into disproportionate revenue impact across the surfactants market.

Geography Analysis

Asia-Pacific held 48.40% of the total surfactants market share in 2025 and is projected to expand at a 4.24% CAGR to 2031, underpinned by China’s dominant manufacturing base, India’s rising middle class, and Southeast Asia’s rapid urban migration. China alone supplies more than half of global LAS output, enabling aggressive pricing that feeds both domestic detergents and overseas exports.

The EU’s deforestation-free sourcing rules and pending green-claim directives push brand owners to validate traceable feedstocks, bolstering biosurfactant pilots financed via corporate sustainability budgets. The United States emphasizes performance gains, particularly in concentrated laundry liquids and all-purpose wipes that trim packaging waste. Both regions bear the brunt of PFAS reformulation costs yet house the research hubs capable of fast-tracking compliant alternatives, reinforcing their roles as launch pads for next-generation chemistries that later migrate to emerging markets in the surfactants market.

Surfactant-polymer flooding campaigns in Abu Dhabi and Oman open premium avenues for high-temperature, high-salinity blends, while Nigeria and Kenya witness rising consumption of packaged detergents as urbanization accelerates. Brazil leverages its ample fatty-acid by-products from soy and sugarcane biofuels to back-integrate renewable surfactants, offering cost relief against foreign exchange volatility. Infrastructure gaps, logistics costs, and economic cycles remain hurdles, yet manufacturers partnering with local tollers and distributors mitigate exposure and deepen the surfactants market footprint.

Competitive Landscape

The surfactants market exhibits high fragmentation. Sustainability differentiators are reshaping portfolio strategies. Evonik’s first-to-market rhamnolipid plant confers a technological moat in glycolipids, and early-stage production capacity is already booked under multi-year supply agreements with leading detergent brands. Competitive intensity remains especially high in Asia-Pacific where local firms operate single-reactor facilities tuned to national detergent giants. These players leverage proximity advantages to navigate tariff regimes and just-in-time shipping, challenging multinationals to localize faster or cede low-end volumes.

Surfactants Industry Leaders

Evonik Industries AG

BASF

Dow

Syensqo

Stepan Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2024: Evonik Industries launched the world’s first industrial-scale rhamnolipid biosurfactant plant in Slovakia, supplying fully biodegradable surfactants for cleaning and personal-care use.

- January 2024: Nouryon introduced Berol Nexus, a multifunctional hydrotrope designed to elevate performance in household and, Industrial and Institutional cleaning formulations.

Global Surfactants Market Report Scope

Surfactant is a substance that, when added to a liquid, reduces its surface tension, thereby increasing its spreading and wetting properties. They are mainly used in household soap and detergent and personal care applications.

The surfactants market is segmented by type, application, and geography. By type, the market is segmented into anionic surfactants, cationic surfactants, non-ionic surfactants, amphoteric surfactants, and silicone surfactants. By application, the market is segmented into household soaps and detergents, personal care, lubricants and fuel additives, industry and institutional cleaning, food processing, oilfield chemicals, agricultural chemicals, textile processing, emulsion polymerization, and other applications. The report also covers the market size and forecasts for the surfactants market in 15 countries across major regions. For each segment, the market sizing and forecasts are provided on the basis of volume (kilotons).

By Type

| Anionic Surfactants | Linear Alkylbenzene Sulfonate (LAS or LABS) |

| Alcohol Ether Sulfates (AES) | |

| Alpha Olefin Sulfonates (AOS) | |

| Secondary Alkane Sulfonate (SAS) | |

| Methyl Ester Sulfonates (MES) | |

| Sulfosuccinates | |

| Others (Lignosulfonates, etc.) | |

| Cationic Surfactants | Quaternary ammonium compound |

| Others | |

| Non-ionic Surfactants | Alcohol ethoxylate |

| Ethoxylated Alkyl-phenols | |

| Fatty acid ester | |

| Others | |

| Amphoteric Surfactants | |

| Silicone Surfactants |

By Origin

| Synthetic Surfactants |

| Bio-based Surfactants |

By Application

| Household Soap and Detergent |

| Personal Care |

| Lubricants and Fuel Additives |

| Industry and Institutional Cleaning |

| Food Processing |

| Oilfield Chemicals |

| Agricultural Chemicals |

| Textile Processing |

| Emulsion Polymerisation |

| Other Applications |

By Geography

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Type | Anionic Surfactants | Linear Alkylbenzene Sulfonate (LAS or LABS) |

| Alcohol Ether Sulfates (AES) | ||

| Alpha Olefin Sulfonates (AOS) | ||

| Secondary Alkane Sulfonate (SAS) | ||

| Methyl Ester Sulfonates (MES) | ||

| Sulfosuccinates | ||

| Others (Lignosulfonates, etc.) | ||

| Cationic Surfactants | Quaternary ammonium compound | |

| Others | ||

| Non-ionic Surfactants | Alcohol ethoxylate | |

| Ethoxylated Alkyl-phenols | ||

| Fatty acid ester | ||

| Others | ||

| Amphoteric Surfactants | ||

| Silicone Surfactants | ||

| By Origin | Synthetic Surfactants | |

| Bio-based Surfactants | ||

| By Application | Household Soap and Detergent | |

| Personal Care | ||

| Lubricants and Fuel Additives | ||

| Industry and Institutional Cleaning | ||

| Food Processing | ||

| Oilfield Chemicals | ||

| Agricultural Chemicals | ||

| Textile Processing | ||

| Emulsion Polymerisation | ||

| Other Applications | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the 2026 volume of the global surfactants market?

The surfactants market size reached 19.48 million tons in 2026.

Which product type leads in volume terms?

Anionic surfactants hold the largest 47.80% share of total demand.

Which application segment is expanding fastest in surfactants industry?

Personal-care formulations are projected to grow at a 4.60% CAGR to 2031.

Why are bio-based surfactants gaining traction?

Regulatory pressure, abundant medium-chain fatty acids from biofuels, and consumer demand for sustainable ingredients support a 4.17% CAGR for bio-based variants.

Which region offers the highest growth potential in surfactants industry?

Asia-Pacific dominates current share and is forecast to outpace all regions with a 4.24% CAGR through 2031.

Page last updated on: