Industrial Gearbox Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 31.65 Billion |

| Market Size (2031) | USD 38.49 Billion |

| Growth Rate (2026 - 2031) | 3.99% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

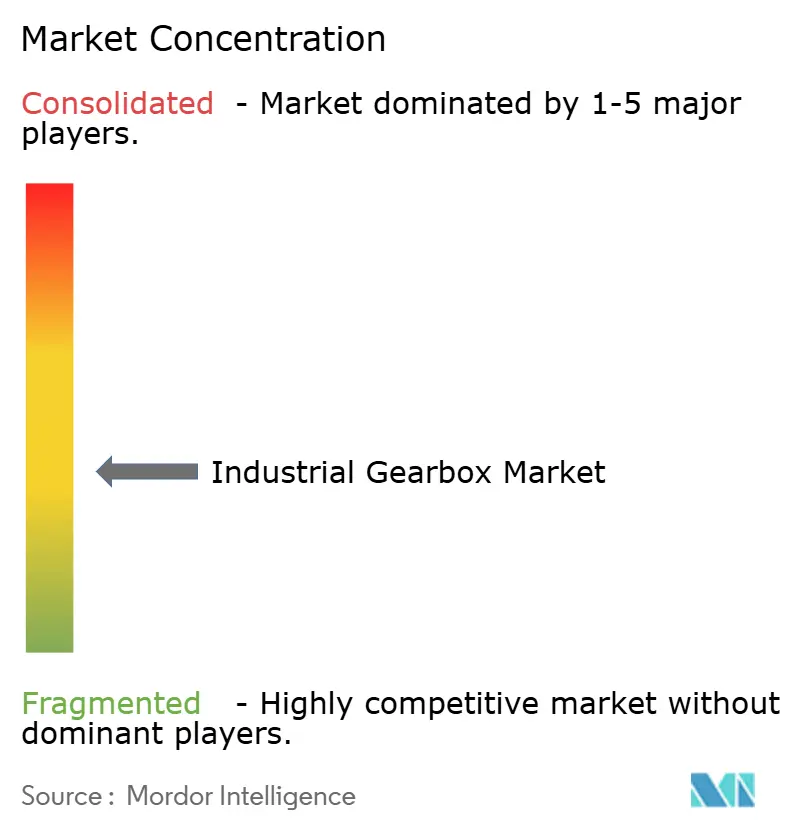

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Industrial Gearbox Market Analysis by Mordor Intelligence

The Industrial Gearbox Market size is expected to grow from USD 30.41 billion in 2025 to USD 31.65 billion in 2026 and is forecast to reach USD 38.49 billion by 2031 at 3.99% CAGR over 2026-2031.

Ongoing factory-floor digitalization is turning gearboxes into edge-intelligent assets that collect vibration, temperature, and load data, feeding predictive-maintenance algorithms and lowering unscheduled downtime by 20-25%. Planetary designs are growing quickly on the back of robot, precision machine-tool, and solar-tracker demand, while helical units remain the workhorse for conveyors, mixers, and general-purpose machinery. Wind-turbine build-outs, intralogistics automation, and green-hydrogen programs are pulling incremental volume, especially in Asia-Pacific, where supportive industrial policies and infrastructure pipelines underpin fresh capacity. Competitive intensity is moderate because the top 20 suppliers command only 55-60% of global revenue, leaving space for regional specialists that compete on service responsiveness and application know-how.

Key Report Takeaways

- By type, helical configurations led with 37.58% of the industrial gearbox market share in 2025, while planetary designs are forecast to expand at a 4.71% CAGR through 2031.

- By end-user, manufacturing and machine tools accounted for 33.21% of the industrial gearbox market size in 2025, whereas the energy sector is projected to post the fastest 4.92% CAGR to 2031.

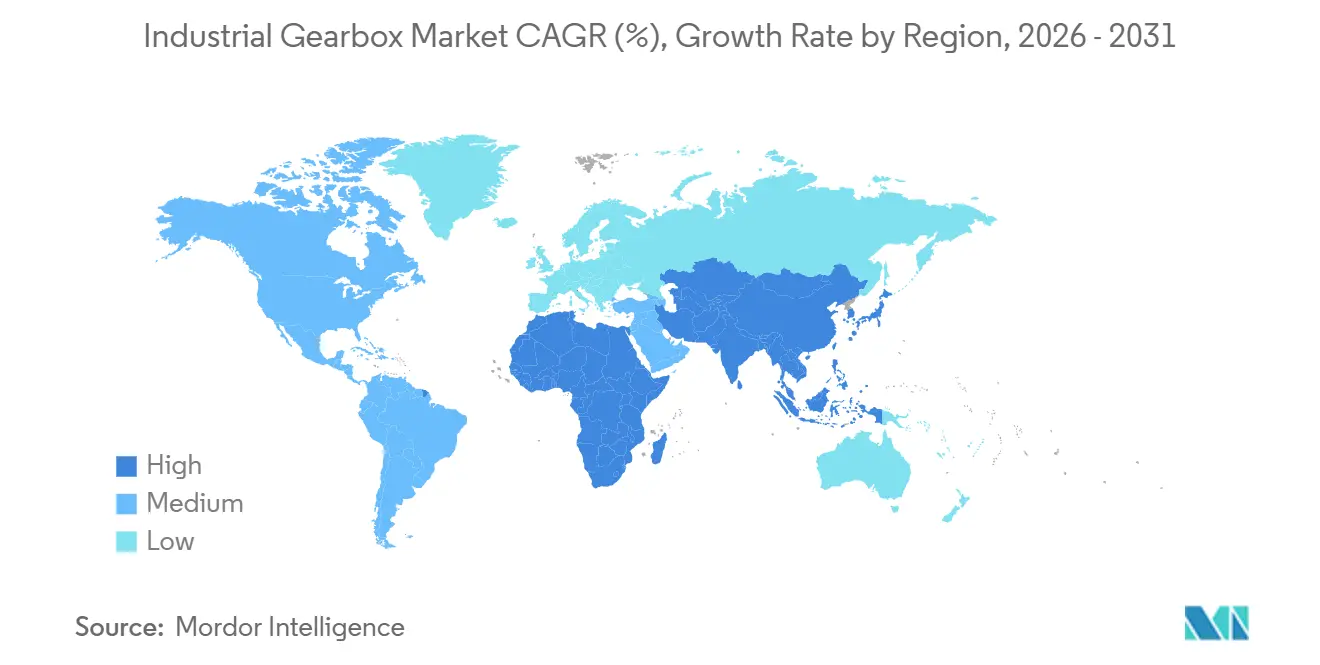

- By geography, Asia-Pacific captured 43.63% of 2025 revenue and is anticipated to grow at a 4.68% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Industrial Gearbox Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising adoption of Industry 4.0-enabled automation | 1.2% | Global, with Asia-Pacific and Europe leading, early adoption in North America manufacturing hubs | Medium term (2-4 years) |

| Surging wind-turbine gear demand | 0.9% | Global, concentrated in China, Europe (Germany, UK, Denmark), North America (US offshore), emerging in Asia-Pacific (Taiwan, Japan) | Long term (≥ 4 years) |

| Rapid expansion of intralogistics and warehouse automation | 0.8% | North America (US, Canada), Europe (Germany, Netherlands, UK), Asia-Pacific e-commerce hubs (China, Japan, South Korea, Singapore) | Short term (≤ 2 years) |

| Growing construction and mining equipment output | 0.6% | Asia-Pacific (China, India, Indonesia), Middle East (Saudi Arabia, UAE), South America (Brazil, Chile, Peru), Africa (South Africa) | Medium term (2-4 years) |

| Data-driven predictive-maintenance contracts boosting upgrades | 0.5% | Global, early adoption in North America and Europe, expanding to Asia-Pacific mining and energy sectors | Medium term (2-4 years) |

| Shift to modular, 3D-printed gear components | 0.4% | North America (US, Canada), Europe (Germany, UK, France), early pilots in Asia-Pacific (Japan, South Korea) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Industry 4.0-enabled automation

Condition-monitoring sensors, IO-Link interfaces, and edge-compute modules are being embedded inside gearboxes, enabling closed-loop control strategies that trim installation time by 40% on modular platforms launched in 2025.[1]SEW-Eurodrive, “Industrial Gearbox and Drive Solutions,” sew-eurodrive.com Wireless vibration and temperature nodes paired with smart lubrication systems have extended service intervals beyond 10,000 hours in remote mines and offshore wind farms. Cloud-based digital twins ingest live telemetry to predict remaining useful life with up to 90% accuracy, letting operators align replacements with planned shutdowns. The roll-out of 5G low-latency networks supports on-machine analytics that dynamically adapt gear ratios to workpiece hardness, boosting throughput without hardware changes. As a result, the industrial gearbox market is pivoting from passive power transmission toward data-rich mechatronic subsystems.

Surging wind-turbine gear demand

Global offshore wind capacity hit 83.2 GW in 2024 and is forecast to swell by more than 350 GW between 2025 and 2034.[2]Global Wind Energy Council, “Global Offshore Wind Report 2024,” gwec.net Multi-megawatt turbines now require main gearboxes that withstand torque loads exceeding 10,000 kN-m over 15-20 year lifecycles, spurring orders for large-diameter planetary stages. Germany has earmarked EUR 8 billion for offshore expansion, with 7-9 GW of auctions scheduled between 2025 and 2027. Medium-speed geared drivetrains held 91.3% market share in 2024, underlining gearbox relevance despite rising direct-drive adoption. Electrolyser projects for green hydrogen also specify 98%-efficiency compressor-train gearboxes, broadening the demand base beyond wind.

Rapid intralogistics and warehouse expansion

Fulfillment centers added more than 500,000 autonomous mobile robots (AMRs) in 2025, each integrating up to four precision gearboxes for wheel drives and lifts. Amazon incorporated 75,000 additional drive units in its 2025 sortation network, handling peak throughput above 1 million parcels per hour.[3]Amazon, “2025 Sustainability Report,” amazon.com Shuttle-based automated storage and retrieval systems now demand zero-backlash hypoid gears that support 1 million start-stop cycles without efficiency loss. Synthetic lubricants stretching maintenance windows beyond 10,000 hours are being adopted to sustain 24/7 operations. A new 60 mm modular gearmotor released in 2025 trimmed commissioning time by 40%, underscoring the pace of design iteration.

Growth in construction and mining output

Infrastructure pipelines across Asia-Pacific and South America are lifting demand for high-horsepower gearboxes in mills, crushers, and conveyors, with predictive-maintenance contracts cutting unplanned downtime by up to 22% at major miners. Sensor-equipped planetary units tied to cloud dashboards accurately forecast remaining life in Chilean copper operations. India’s USD 1.4 trillion National Infrastructure Pipeline is stimulating orders for helical and bevel-helical units in cranes, mixers, and tunnel-boring machines. Middle East desalination megaprojects such as NEOM are specifying stainless-steel housings with NSF/ANSI 61-approved lubricants to handle seawater corrosion. The shift supports a consistent flow of large-frame gearbox orders through the medium term.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in raw-material steel prices | -0.7% | Global, acute in Europe (energy-driven cost pressures) and North America, moderate impact in Asia-Pacific due to regional supply chains | Short term (≤ 2 years) |

| Extended replacement cycles in mature industries | -0.5% | North America and Europe, particularly in legacy manufacturing, automotive, and heavy machinery sectors with aging installed base | Long term (≥ 4 years) |

| Torque-dense electro-hydraulic actuators cannibalizing compact gearboxes | -0.4% | Aerospace and mobile equipment in North America and Europe, emerging substitution in Asia-Pacific construction equipment | Medium term (2-4 years) |

| Cybersecurity certification delays for smart gearboxes | -0.3% | Global, regulatory focus in Europe (EU Machinery Regulation 2027) and North America, compliance requirements spreading to Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Steel-price volatility

Hot-rolled coil swung between USD 620 and USD 900 per metric ton during 2024-2025, cutting gross margins by 2-3 percentage points for assemblers lacking hedging programs. Alloy-steel surcharges added USD 0.15-0.25 per kilogram in 2025, triggering selective substitution of case-hardened carbon steels at the expense of 10-15% fatigue-life reduction. Vertically integrated suppliers offset swings through captive gear-cutting and heat-treatment capacity. Additive-manufacturing platforms are driving modular designs that slash scrap from 18-22% to below 5%, compressing prototype lead times from eight weeks to five days. Although price risk is expected to moderate, it remains a near-term drag on the industrial gearbox market.

Electro-hydraulic actuator substitution

Electro-hydraulic actuators deliver 50-100 N-m per kilogram, roughly double the torque density of planetary units, and are penetrating aerospace, construction, and robotics where weight premiums are justified. Moog disclosed a 12% share in commercial-aircraft rotary drives by 2025, eroding demand for worm and bevel-helical gearboxes. Integrated hydraulic modules absorb shock loads without backlash, whereas mechanical alternatives need separate dampers. Fluid reservoirs, filtration, and thermal management raise complexity, limiting uptake in food-processing and pharma facilities. Gearbox vendors are prototyping hybrid electro-mechanical actuators that pair planetary stages with hydraulic dampers in a bid to reclaim share.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Planetary Gains as Robotics Scales

Planetary gearboxes are forecast to expand at a 4.71% CAGR through 2031 as robotics, precision machine tools, and solar trackers require high torque density in tight envelopes. Nabtesco controls over 60% of precision reduction gears, shipping strain-wave-free RV reducers that exceed 1 million cycles with zero backlash. Helical configurations delivered 37.58% of 2025 revenue, reflecting their versatility in conveyors, agitators, and general-purpose machinery.

The industrial gearbox market continues to prize helical designs for efficiency, low noise, and ease of maintenance, yet customers increasingly specify integrated sensors and IO-Link connectivity. Worm units retain niche roles where self-locking or extreme ratios are vital, such as elevator brakes and valve actuators. Bevel-helical styles transmit right-angle power for cooling-tower fans and vertical mixers, while cycloidal drives gain favor in precision indexing because of zero backlash and shock-load resilience. Online configurators launched in 2024 allow users to tailor torque, orientation, and lubrication, shrinking quote cycles from three days to one hour. Additive-manufactured, topology-optimized gear blanks further cut weight by 15-20%, enhancing power-to-mass ratios.

By End-User: Energy Sector Outpaces Manufacturing

Manufacturing and machine tools held 33.21% of the industrial gearbox market share in 2025, anchored by CNC centers, injection-molding presses, and lathes that embed helical and planetary units in spindle and axis drives. The energy sector, however, is projected to log the fastest 4.92% CAGR through 2031 as offshore wind, pipeline compression, and green-hydrogen electrolyser projects proliferate.[4]Global Wind Energy Council, “Global Offshore Wind Report 2024,” gwec.net

Multi-megawatt turbines rated at 15-20 MW require planetary stages with main bearings exceeding 4 m in diameter, stretching forging capacity, and supporting new investments such as Flender’s EUR 120 million Bocholt expansion. Oil-and-gas midstream operators specify 98%-efficiency gearbox trains to curb parasitic compressor losses. Electric-vehicle manufacturers are transitioning to single-speed reduction gears, standardizing on 9:1–11:1 coaxial helical designs that reach 96-97% efficiency. Mining, water, and wastewater plants continue to demand corrosion-resistant housings and IP66-plus ingress protection for harsh environments, though these segments grow at more modest rates tied to commodity cycles and municipal budgets.

Geography Analysis

Asia-Pacific generated 43.63% of global revenue in 2025 and is projected to grow at a 4.68% CAGR through 2031, benefiting from China’s 330,000 industrial-robot installations in 2024 and the region’s dominant offshore-wind pipeline. India’s USD 1.4 trillion National Infrastructure Pipeline fosters demand for construction gearboxes, while the country’s wind capacity target of 140 GW by 2030 opens new opportunities for domestic suppliers. Japan and South Korea specialize in precision reducers for semiconductor tools and collaborative robots, and Vietnam has emerged as a lower-cost export base following Sumitomo’s 40,000 m² plant launch in 2024.

Germany, Italy, and France are anchoring machine-tool and turbine supply chains in Europe. Germany’s EUR 8 billion offshore-wind program and the EU Machinery Regulation taking effect in 2027 drive uptake of IEC 62443-compliant smart gearboxes. Italy’s packaging-machinery cluster favors compact planetary units for high-speed filling lines, while Nordic electrolyser investments demand 98%-efficiency compressor gears to curb energy consumption. European suppliers increasingly use additive manufacturing to shorten prototype cycles and localize spare-part production.

Demand in North America is buoyed by warehouse-automation roll-outs, shale-gas infrastructure, and EV production ramp-ups. The U.S. Inflation Reduction Act’s 45X credit reimburses up to 25% of eligible gearbox manufacturing costs, catalyzing a USD 75 million Wisconsin expansion by Regal Rexnord in 2024. Canadian miners retrofit sensor-equipped drives to cut downtime, while Mexico’s EV transition fuels orders for single-speed reductions in battery-electric trucks. South America and the Middle East & Africa markets are dominated by Brazilian iron ore, Chilean copper, and Gulf desalination projects that demand corrosion-resistant gear trains.

Competitive Landscape

The industrial gearbox market remains moderately concentrated: the top 20 vendors hold about 55-60% of revenue, implying neither oligopoly nor fragmentation. Flender, Bonfiglioli, SEW-Eurodrive, and ZF maintain vertically integrated value chains encompassing gear cutting, heat treatment, and assembly, using digital-twin software to trim prototype iterations by up to 40%. Their global service footprints and mass-customization capabilities underpin customer loyalty in wind, factory automation, and e-mobility.

Regional specialists such as Elecon Engineering and Nanjing High Accurate Drive leverage localized service depots and cost-optimized helical designs to respond swiftly to demand spikes in mining, cement, and steel mills. Additive manufacturing is emerging as a white-space play: Renault Trucks cut helical-gear lead times from eight weeks to five days in 2025, validating on-demand production for obsolete or long-lead-time spares. Compliance with IEC 62443 cybersecurity standards has become a gating factor for smart-gearbox launches, favoring incumbents with in-house firmware teams.

Substitution risk from electro-hydraulic actuator vendors such as Parker Hannifin and Moog is noteworthy in aerospace and mobile equipment, where weight savings justify the 20-30% cost premium. Moog reached a 12% share of commercial-aircraft rotary drives in 2025, prompting gearbox makers to explore hybrid electromechanical concepts that integrate hydraulic dampers with planetary stages. Overall, pricing discipline, digital services, and rapid-response spare-parts logistics are key competitive levers.

Industrial Gearbox Industry Leaders

Sumitomo Drive Technologies

Flender International GmbH

ZF Friedrichshafen AG

Bonfiglioli Riduttori SpA

SEW-Eurodrive

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Bonfiglioli committed INR 3.2 billion to expand its Indian industrial gearbox operations, aiming for INR 19 billion revenue by 2027.

- August 2024: FAVI, a French production partner, showcased the Saga motor gearbox, highlighting its capabilities. The company offers extensive services, including R&D, co-design, industrialization, parts production, and complete set assembly for third parties.

- June 2024: Siemens Mobility opened a new gearbox line in Cornellà, Spain, with an annual capacity of 500 heavy rail drives.

- November 2024: ZF partnered with a Chinese EV builder to co-develop two-speed electric axles slated for 97% efficiency at the 2027 launch.

- September 2025: SEW-Eurodrive unveiled a modular planetary platform featuring IO-Link sensors and 18 ratio options across 60–200 mm frames.

Global Industrial Gearbox Market Report Scope

Industrial gearboxes are mechanical devices that are necessary components of machinery used by various industries. An enclosed housing containing a series of shafts and gears transfers power between devices within a system. Gearboxes increase torque, lower the rotation speed of the prime mover output shaft, and convert mechanical energy to usable form.

The industrial gearbox market is segmented by type, end user, and geography. By type, it is segmented into worm gearbox, helical gearbox, bevel helical gearbox, planetary gearbox, and others. By end user, it is segmented into automotive, energy, manufacturing, mining, water treatment, and other end users. The report also covers the market size and forecasts for the industrial gearbox market across major regions. The market size and forecasts have been done for each segment based on revenue (USD).

| Worm |

| Helical |

| Bevel-Helical |

| Planetary |

| Other Types |

| Automotive and E-Mobility |

| Energy |

| Manufacturing and Machine Tools |

| Mining and Metallurgy |

| Water and Waste-water Treatment |

| Other End-Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Type | Worm | |

| Helical | ||

| Bevel-Helical | ||

| Planetary | ||

| Other Types | ||

| By End-user | Automotive and E-Mobility | |

| Energy | ||

| Manufacturing and Machine Tools | ||

| Mining and Metallurgy | ||

| Water and Waste-water Treatment | ||

| Other End-Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will the industrial gearbox market be by 2031?

It is expected to reach USD 38.49 billion, reflecting a 3.99% CAGR from 2026 to 2031.

Which gearbox type is growing the fastest?

Planetary units are projected to expand at 4.71% CAGR, driven by robot and precision-machine applications.

What end-use sector offers the strongest growth prospects?

The energy segment, including wind turbines and green-hydrogen compressors, is forecast to post the highest 4.92% CAGR to 2031.

Which region dominates demand for industrial gearboxes?

Asia-Pacific generated 43.63% of global revenue in 2025 and is poised to grow at 4.68% CAGR, maintaining regional leadership.

What is the main technology trend shaping new gearbox designs?

Integration of sensors and edge-compute modules that enable predictive maintenance and Industry 4.0 connectivity is redefining product roadmaps.

How are steel-price swings affecting manufacturers?

Volatile coil pricing shaved 2-3 percentage points off margins in 2024-2025 for firms without hedging, prompting greater use of additive manufacturing to reduce material waste.

Page last updated on: