North America Data Center Immersion Cooling Fluid Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

| Market Size (2025) | USD 0.95 Billion |

| Market Size (2030) | USD 1.54 Billion |

| Growth Rate (2025 - 2030) | 9.99% CAGR |

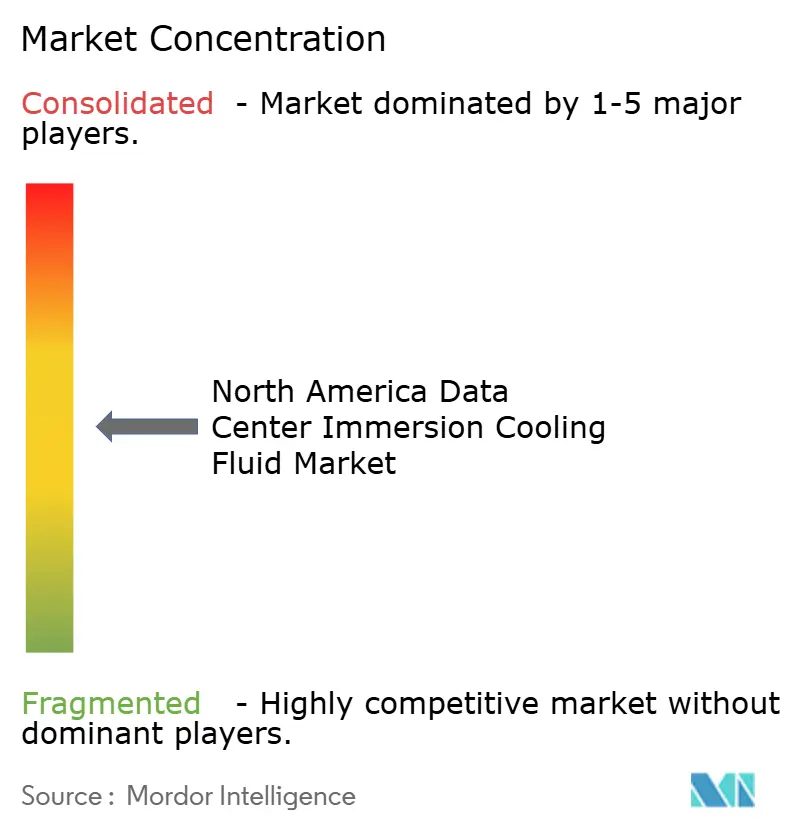

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Data Center Immersion Cooling Fluid Market Analysis by Mordor Intelligence

The data center immersion cooling fluid market size in North America is valued at USD 0.95 billion in 2025 and is forecast to reach USD 1.54 billion by 2030, advancing at a 9.99% CAGR over the period. Continued AI and machine-learning adoption is pushing rack densities beyond 100 kW, making liquid cooling a necessity rather than an option for hyperscale and edge operators. Sustainability mandates, looming PFAS regulation and tax incentives further accelerate the shift toward dielectric fluids that combine thermal efficiency with low global-warming potential. Supply-chain volatility around synthetic hydrocarbons and emerging bio-based esters influences procurement strategies, while fluctuations in semiconductor memory pricing indirectly affect overall data center capital spending. Competitive dynamics remain fluid as established chemical majors and specialized cooling vendors race to certify new chemistries compliant with evolving EPA oversight.

Key Report Takeaways

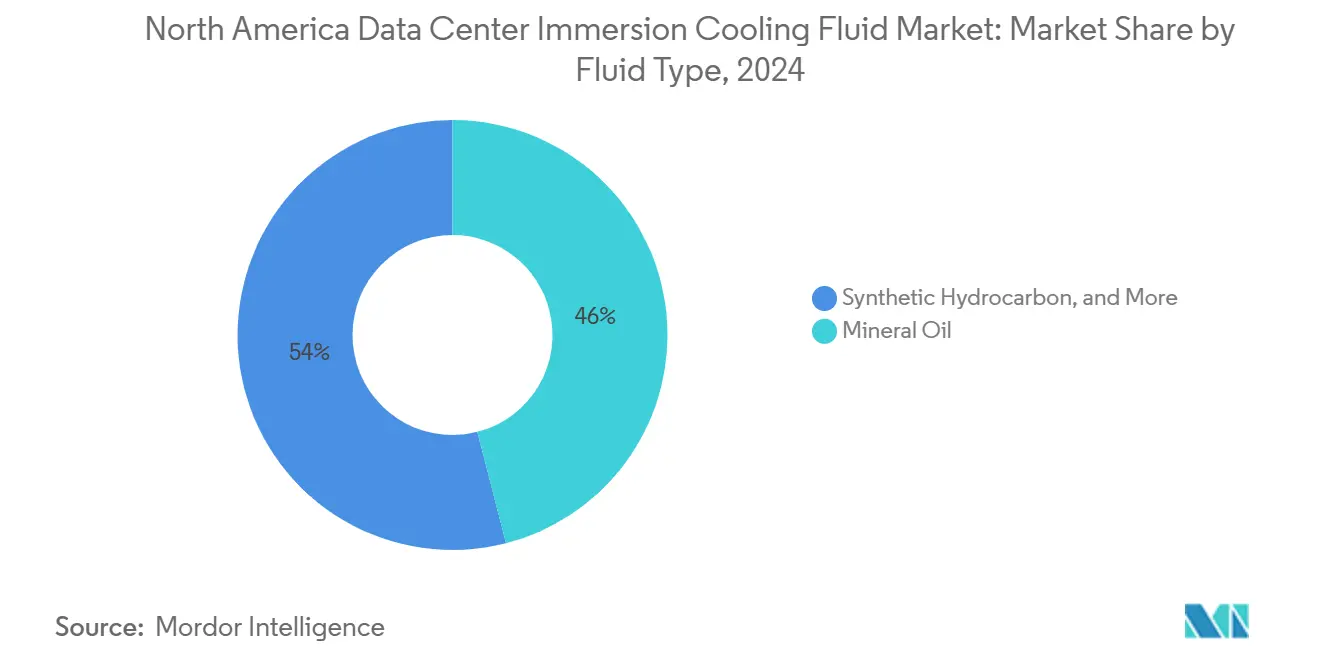

- By fluid type, mineral oil led with 46% of the north america data center immersion cooling fluid market share in 2024, while bio-based esters recorded the fastest CAGR at 12.5% through 2030.

- By phase type, single-phase systems accounted for 71% share of the north america data center immersion cooling fluid market size in 2024; two-phase solutions are expanding at an 18% CAGR to 2030.

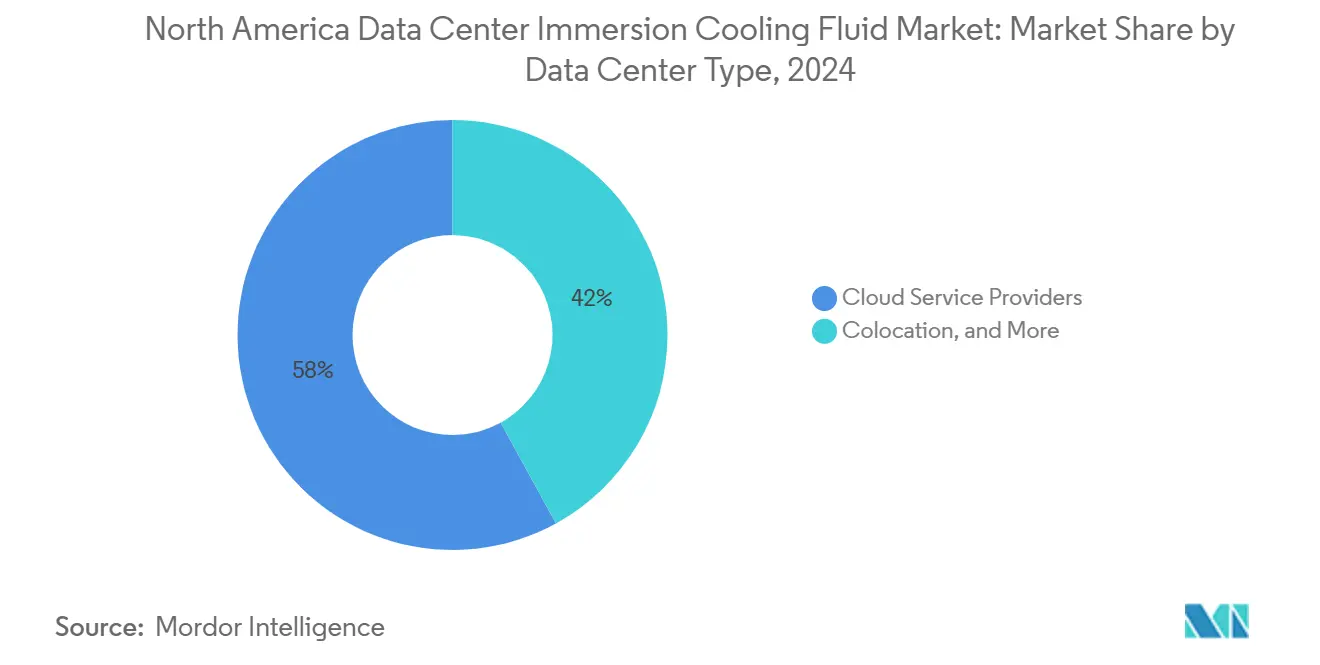

- By data center type, cloud service providers commanded 58% share of the north america data center immersion cooling fluid market size in 2024, whereas edge facilities are projected to post an 11% CAGR through 2030.

- By end-user industry, IT/ITES accounted for 38.00% share of the north america data center immersion cooling fluid market size in 2024; and is expanding at an 15.60% CAGR to 2030.

- By geography, the United States captured 88% share of the north america data center immersion cooling fluid market size in 2024 and Mexico is advancing at a 13.3% CAGR to 2030.

North America Data Center Immersion Cooling Fluid Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging rack densities exceeding 100 kW | +2.80% | United States hyperscale corridors | Medium term (2-4 years) |

| Escalating energy-cost differentials | +2.10% | High-electricity-cost regions across North America | Long term (≥ 4 years) |

| Water-use restrictions in drought-prone states | +1.70% | Western and Southwestern United States | Short term (≤ 2 years) |

| Federal tax incentives | +1.30% | United States | Medium term (2-4 years) |

| Rise of AI/ML workloads | +1.90% | U.S. AI innovation hubs | Short term (≤ 2 years) |

| Corporate net-zero commitments | +1.10% | Multinational cloud operators across North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Rack Densities Exceeding 100 kW

AI-optimized clusters now post rack loads up to 120 kW, compelling operators to abandon air cooling that was designed for 10–15 kW envelopes. Microsoft’s in-field tests showed immersion technology holding chip temperatures within safe limits even as power densities approached 120 kW per rack [1].Microsoft Corp., “Microsoft Build 2024: The Era of the AI PC,” Microsoft Blog, microsoft.comWhen cooling infrastructure crosses 40% of operating expense, immersion becomes economically rational, and that threshold is increasingly common in AI-centric builds. Next-generation GPUs further amplify heat loads by packing more transistors into a fixed footprint, raising per-square-inch dissipation above 1,000 W. Under these conditions, dielectric fluids are the only scalable path to maintain thermal compliance at hyperscale.

Escalating Energy-Cost Differentials Driving TCO Savings

Facilities that pay more than USD 0.12 per kWh can trim cooling energy 30–45% by moving to immersion, cutting PUE from 1.4 to roughly 1.15 in Intel–Shell validation trials [2].Intel Corp., “Shell and Intel Collaborate on Immersion Cooling,” Intel Newsroom, intel.com With carbon-pricing frameworks broadening across North America, energy savings translate directly into lower Scope 2 emissions and compliance credits. Operators in high-tariff jurisdictions realize 18–24-month paybacks once reduced air-handling systems, smaller electrical rooms and lower chiller loads are considered. This economic calculus widens adoption beyond hyperscale into colocation and enterprise builds that target aggressive return-on-capital hurdles.

Data Center Water-Use Restrictions in Drought-Prone States

California’s emergency rule keeps data center water consumption at 2019 baselines, effectively disqualifying new evaporative towers. Arizona layered tiered tariffs that render water-intensive cooling financially untenable. Immersion eliminates roughly 1.8 million gallons a year for a 10-MW data center, allowing developers to secure permits in constrained basins without offset schemes. Municipalities beyond the Southwest are following suit, prompting developers to pre-emptively specify closed-loop liquid cooling to future-proof assets against evolving ordinances.

Rise of AI/ML Workloads Demanding Thermal Stability

Temperature swings beyond ±2 °C degrade neural-network accuracy; NVIDIA’s H100 GPUs operate optimally in a narrow band that immersion easily meets. During large-language-model training, even micro-fluctuations extend runtime by weeks, materially impacting service rollouts. Edge AI applications such as autonomous driving or remote diagnostics impose similar constraints in uncontrolled environments. Immersion’s thermal inertia keeps component temperatures within ±1 °C, ensuring deterministic performance and safeguarding SLAs across distributed architectures.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited field data on long-term degradation | -1.40% | Early U.S. adopters | Medium term (2-4 years) |

| Higher upfront CAPEX | -1.80% | Small and mid-size operators across North America | Short term (≤ 2 years) |

| Supply-chain uncertainties | -1.20% | Global with U.S. distribution pinch-points | Short term (≤ 2 years) |

| Pending PFAS phase-out | -1.60% | United States, under EPA oversight | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited Field Data on Long-Term Fluid Degradation

Most immersion deployments have fewer than five years of runtime, insufficient against the 15–20-year lifecycle expected for data center infrastructure. Insurers demand surcharges or exclusions until longer operating data proves dielectric stability. Concerns range from oxidation to particulate contamination that may erode ESD envelopes. 3M’s accelerated-aging trials offer partial reassurance, but operators still view first-generation fluids as comparatively untested [3].3M Co., “Form 10-K Annual Report,” sec.gov

Higher Upfront CAPEX Versus Legacy Air Cooling

Immersion systems run USD 800–1,200 per kW versus USD 400–600 for CRAC installations. The delta includes tanks, pumps, heat exchangers, sensors and the fluid itself. Dow’s financial filings show that specialty dielectric blends remain priced at a premium to commodity refrigerants [4].Dow Inc., “Form 10-K Annual Report,” sec.gov While TCO economics soften the gap, enterprises with capital-expense ceiling limits find it hard to justify the switch on initial cash-flow metrics alone.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Fluid Type: Bio-Based Solutions Challenge Mineral Oil Dominance

Mineral oil retained the largest slice of the data center immersion cooling fluid market size with 46% share in 2024, primarily because it is affordable, readily available and well-understood by facility engineers. Operators value its dielectric reliability in single-phase environments, especially during pilot migrations from air cooling. However, expanding EPA scrutiny and ESG scorecards intensify the focus on renewability and end-of-life disposal. Bio-based esters, projecting a 12.5% CAGR, meet both performance and sustainability criteria. Cargill’s NatureCool demonstrates equal heat-transfer coefficients to synthetic hydrocarbons while delivering full biodegradability, a combination that has led hyperscale RFPs to mandate bio-ester options in their 2026 procurement cycles.

Rapid commercialization of next-generation esters also lowers viscosity by up to 15%, improving pump efficiency in high-density tanks and squeezing additional gains out of already aggressive PUE targets. In parallel, synthetic hydrocarbons remain a stable intermediary choice, providing drop-in compatibility for existing mineral oil infrastructure while registering GWP values well below legacy refrigerants. Fluorocarbon-based fluids, despite stellar two-phase characteristics, face PFAS headwinds. Collectively, these trends suggest the data center immersion cooling fluid market will see a gradual rebalancing, with bio-esters closing the share gap by the decade’s end.

By Phase Type: Two-Phase Systems Gain Momentum Despite Single-Phase Dominance

Single-phase installations accounted for 71% of the data center immersion cooling fluid market share in 2024, favored for mechanical simplicity and easier retrofits into raised-floor rooms. Tank designs require fewer moving parts, and operators used to CRAC systems find the learning curve manageable. Nevertheless, AI racks exceeding 150 kW expose single-phase thermal limits. Two-phase solutions, expected to grow at 18% CAGR, cope with heat fluxes up to 200 W/cm² via boiling and condensation cycles. Chemours’ Opteon 2P50, validated for such workloads, shows vapor-phase transport coefficients that outperform single-phase conduction by multiples.

Although concerns remain around fluid management, especially topping-up after boil-off, the technology roadmap points toward integrated condenser plates that reclaim vapor internally, minimizing maintenance touches. As design guides mature and reference deployments prove reliability, two-phase systems will increasingly anchor new hyperscale pods. The data center immersion cooling fluid market therefore evolves along a curves-crossing dynamic where incumbent single-phase retains scale, but two-phase captures incremental growth tied to bleeding-edge compute.

By Data Center Type: Edge Computing Drives Fastest Expansion

Cloud service providers held 58% share of the data center immersion cooling fluid market size in 2024, owing to the sheer capacity of hyperscale builds targeting large-language-model training. Their predictable refresh cadence and centralized procurement give them considerable influence over fluid-chemistry roadmaps. Edge facilities, however, exhibit the steepest trajectory at 11% CAGR. LiquidStack’s DataTank 4U illustrates why: the compact enclosure packages immersion benefits into micro-modular footprints suitable for 5G tower bases and retail outlets.

Edge deployments impose logistical constraints such as limited floor space, variable ambient temperatures and remote operation. Immersion’s sealed-tank design mitigates dust and humidity risks while minimizing acoustics—an advantage for telco roadside cabinets and hospital wards. As real-time AI inference migrates closer to users, it brings rack densities that small footprints cannot dissipate via air. This reinforces the edge-immersion linkage, ensuring the data center immersion cooling fluid market captures diversified demand beyond centralized hyperscale campuses.

By End-User Industry: Healthcare Leads Growth Through AI-Driven Applications

The healthcare segment is on pace for a 15.6% CAGR through 2030 as hospitals deploy AI-assisted imaging and bedside analytics that demand consistent performance and strict uptime. Medical-device OEMs integrate immersion-cooled edge boxes into diagnostic suites, ensuring GPU clusters run within ±1 °C to avoid inference errors in CT and MRI analytics. IT/ITES, though mature and sprawling, continues to retrofit legacy halls for higher rack densities, maintaining baseline volume even as growth moderates. BFSI finds immersion attractive for latency-sensitive algorithmic trading farms where millisecond jitter maps directly to revenue. Government and defense users emphasize resilience and security, mandating sealed dielectric baths for sensitive servers deployed in mobile shelters. Media and entertainment players adopt immersion in rendering farms for real-time streaming and post-production that now target 8K workflows.

Two clear patterns emerge: industries with real-time compute at the edge prioritize immersion for deterministic thermal envelopes, while sectors with massive centralized workloads employ fluid cooling to conserve energy and floor space. In both cases, sustainability reporting becomes a unifying selection criterion, reinforcing the momentum behind bio-esters and low-GWP synthetics across all verticals.

Geography Analysis

The United States captured 88% of the data center immersion cooling fluid market size in 2024 as Virginia’s “Data Center Alley,” Texas’ renewable-powered campuses and Oregon’s enterprise zones lured hyperscale expansions. Federal and state tax credits, plus accelerated depreciation under the Inflation Reduction Act, shortened ROI cycles and de-risked large-scale transitions from air to liquid. PFAS rulemaking by the EPA steered procurement toward low-GWP chemistries, giving domestic chemical producers with compliant portfolios a commercial advantage. Electricity-price spreads from USD 0.07 in Oregon to beyond USD 0.15 in New York produced regional arbitrage that amplified immersion economics in premium-tariff grids.

Mexico is the fastest-growing territory, projected to deliver 13.3% CAGR through 2030. Nearshoring manufacturing stimulates local compute demand, exemplified by Foxconn’s NVIDIA server facility that couples production with on-site test labs needing advanced cooling. Google Cloud’s Querétaro region activation and AWS expansion underline hyperscale interest amid attractive land costs and improving fiber connectivity. Water scarcity across industrial corridors also tilts architects toward immersion to avoid high-tariff potable use and to satisfy municipal permitting requirements.

Canada maintains steady expansion backed by low-carbon hydroelectric grids in Quebec and British Columbia. Cold ambient temperatures permit economizer modes that synergize with immersion loops, allowing operators to push annualized PUE below 1.10 even without mechanical chilling. Carbon-pricing legislation further nudges facilities toward low-GWP or bio-based coolants to avoid rising emissions levies.

Competitive Landscape

The North American data center immersion cooling fluid market is moderately fragmented. Chemical conglomerates such as Chemours and Shell deploy scale advantages in feedstock sourcing and regulatory compliance. Specialized firms like LiquidStack and Green Revolution Cooling differentiate through turnkey tanks and control software that shorten deployment timelines. Patent vigor influences bargaining power; Chemours’ two-phase intellectual-property moat complicates generic entry, while 3M holds critical dielectric formulations even after announcing an exit from PFAS commercial production.

White-space opportunities lie in bio-ester R and D. Castrol and TotalEnergies have launched renewable feedstock fluids aimed at hyperscalers committing to net-zero supply chains. Vertiv’s USD 150 million expansion in Ohio boosts domestic manufacturing capacity for tanks and heat exchangers, signaling rising demand confidence. Meanwhile, regional distributors such as Engineered Fluids extend logistics networks into Mexico and Central America to mitigate lead-time risks tied to cross-border shipping.

Price competition remains secondary to lifetime performance, sustainability credentials and vendor support. Hyperscalers award contracts contingent on multi-year fluid warranty and end-of-life reclamation programs, raising barriers for smaller entrants without service infrastructure. The resulting competitive posture favors incumbents with integrated production, R and D and after-sales capabilities.

North America Data Center Immersion Cooling Fluid Industry Leaders

The Dow Chemical Company

Exxon Mobil Corporation

The Chemours Company

3M

Schneider Electric

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Vertiv earmarked USD 150 million to expand its Westerville, Ohio plant for immersion-cooling system production, adding automated lines aimed at AI-ready data center deployments.

- December 2024: Shell introduced DLC Fluid S3, a synthetic hydrocarbon that improves thermal conductivity 25% over mineral-oil baselines, targeting single-phase hyperscale installations.

- November 2024: Castrol rolled out ON Direct Liquid Cooling PG 25, a fully biodegradable bio-ester meeting enterprise uptime requirements.

- October 2024: FUCHS SE opened a USD 50 million R and D center in Michigan focused on next-generation dielectric fluids for automotive and data center use.

- September 2024: HF Sinclair launched a budget-oriented fluid line for edge-computing operators seeking cost-effective alternatives.

North America Data Center Immersion Cooling Fluid Market Report Scope

| Mineral Oil |

| Synthetic Hydrocarbon |

| Fluorocarbon-based Fluids |

| Bio-based Esters |

| Single-Phase |

| Two-Phase |

| Cloud Service Providers |

| Colocation |

| On-Premise/Enterprise/Edge |

| IT/ITES |

| BFSI |

| Healthcare |

| Government and Defense |

| Media and Entertainment |

| Other End Users |

| United States |

| Canada |

| Mexico |

| By Fluid Type | Mineral Oil |

| Synthetic Hydrocarbon | |

| Fluorocarbon-based Fluids | |

| Bio-based Esters | |

| By Phase Type | Single-Phase |

| Two-Phase | |

| By Data Center Type | Cloud Service Providers |

| Colocation | |

| On-Premise/Enterprise/Edge | |

| By End-User Industry | IT/ITES |

| BFSI | |

| Healthcare | |

| Government and Defense | |

| Media and Entertainment | |

| Other End Users | |

| By Country | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

How fast is North America adopting immersion fluids for AI data centers?

The data center immersion cooling fluid market in the region is growing at a 9.99% CAGR from 2025 to 2030, reflecting accelerated AI rack deployments.

Which fluid type is gaining the most share against mineral oil?

Bio-based esters are the fastest climber with a 12.5% CAGR, driven by sustainability mandates.

What makes two-phase cooling attractive for hyperscalers?

Two-phase systems manage heat flux up to 200 W/cm² and are advancing at an 18% CAGR, meeting densities above 150 kW per rack.

Why are edge sites important to future demand?

Edge facilities post an 11% CAGR because immersion enables compact, dust-proof cooling in remote or space-constrained locations.

How will PFAS regulation affect fluid choices?

EPA phase-out timelines pressure operators to shift toward low-GWP synthetics or bio-esters, reshaping future procurement.

Page last updated on: