Asia Pacific Data Center Immersion Cooling Fluid Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

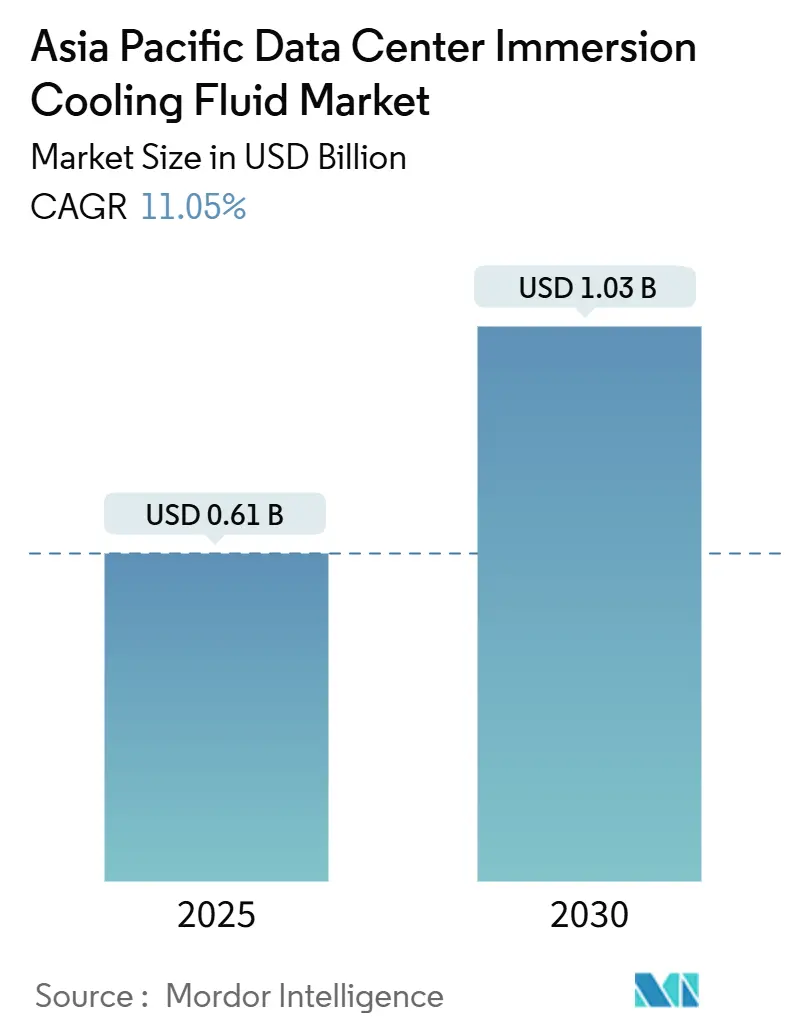

| Market Size (2025) | USD 0.61 Billion |

| Market Size (2030) | USD 1.03 Billion |

| Growth Rate (2025 - 2030) | 11.05% CAGR |

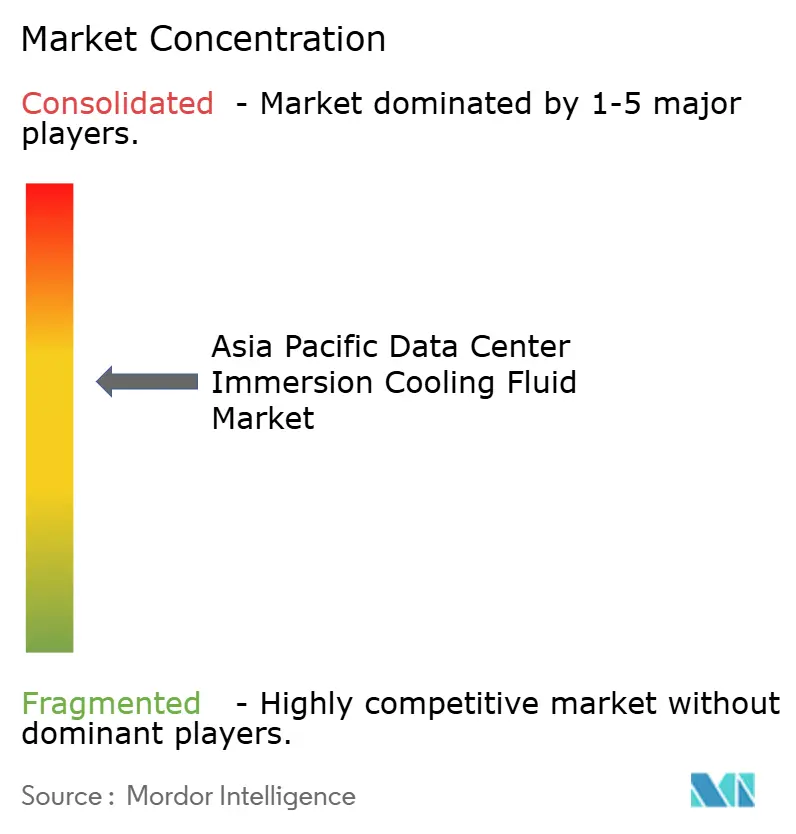

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia Pacific Data Center Immersion Cooling Fluid Market Analysis by Mordor Intelligence

The Asia Pacific data center immersion cooling fluid market size is USD 0.61 billion in 2025 and is forecast to reach USD 1.03 billion by 2030, translating into an 11.05% CAGR for the review period. Persistent rack-density escalation, mounting electricity costs, and water-scarcity regulations position immersive fluids ahead of air-cooling, compressing operating expenses while aligning with regional sustainability frameworks. Large hyperscale facilities already exceed 100 kW per rack, and impending generative-AI deployments will raise density thresholds further, forcing operators to abandon legacy chilled-air designs. The Asia Pacific data center immersion cooling fluid market also benefits from green-taxonomy incentives in Japan and South Korea, alongside rapidly expanding edge infrastructure tied to 5G standalone rollouts. Competitive activity centers on vertically integrated solutions in which chemical majors supply dielectric fluids and system specialists deliver turnkey tanks, pumps, and heat-recovery modules, creating a moderate but tightening vendor landscape.

Key Report Takeaways

- By fluid type, synthetic hydrocarbons led with 46% revenue share of the Asia Pacific data center immersion cooling fluid market in 2024; fluorocarbon-based products are projected to grow at a 15.5% CAGR through 2030.

- By phase type, single-phase immersion accounted for 71% of the Asia Pacific data center immersion cooling fluid market share in 2024, while two-phase solutions are advancing at a 17% CAGR to 2030.

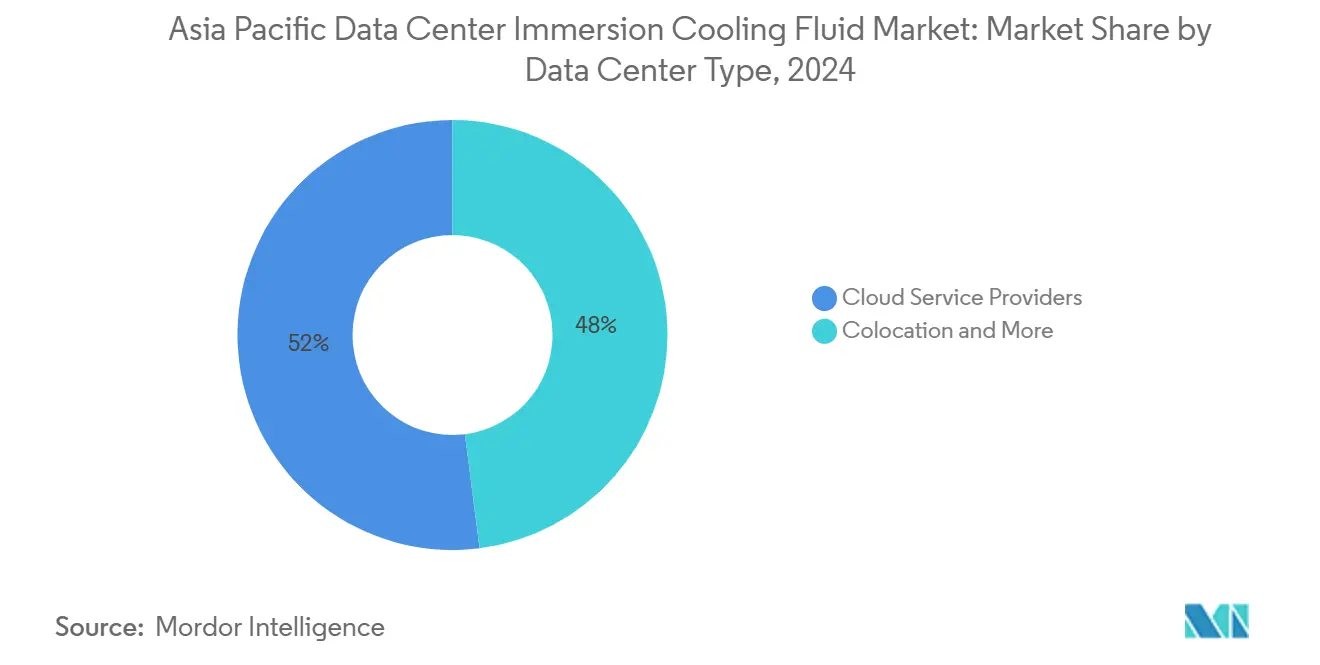

- By data center type, cloud service providers captured 52% of the Asia Pacific data center immersion cooling fluid market size in 2024; edge micro data centers are poised for a 14.2% CAGR between 2025 and 2030.

- By end-user industry, IT/ITES retained 38% share in 2024, whereas media and entertainment is forecast to expand at a 14.8% CAGR to 2030.

- By geography, China dominated with 40.5% share of the Asia Pacific data center immersion cooling fluid market in 2024; India is expected to accelerate at a 20% CAGR through 2030.

Asia Pacific Data Center Immersion Cooling Fluid Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rack power densities > 100 kW | +2.50% | China, Japan, Singapore | Medium term (2-4 years) |

| Escalating electricity tariffs | +1.80% | Singapore, Japan, South Korea, urban China | Short term (≤ 2 years) |

| Water-scarcity regulations | +1.20% | India, Australia, Southeast Asia | Long term (≥ 4 years) |

| Edge micro-data center rollout | +0.90% | South Korea, Japan, dense urban Asia Pacific markets | Medium term (2-4 years) |

| Green-taxonomy subsidies for low-GWP fluids | +0.70% | Japan, South Korea with spillover to wider Asia Pacific | Long term (≥ 4 years) |

| Mandatory waste-heat reuse targets | +0.60% | Japan, Singapore, key Chinese municipalities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Rack Power Densities Drive Thermal Management Revolution

Rack densities that now breach 100 kW per rack displace chilled-air architectures and accelerate the Asia Pacific data center immersion cooling fluid market transition. AI and HPC clusters regularly hit 200–300 kW per rack, overloading CRAC units and creating thermal gradients that jeopardize hardware reliability [1].NVIDIA, “DGX Systems for AI and HPC Workloads,” nvidia.com Immersion fluids remove heat directly from components, supporting 10–20 × the heat flux of air. Recent deployments, including Supermicro’s USD 280 million server contract for X.AI, illustrate densities impossible under conventional cooling. Semiconductor roadmaps toward denser node geometries intensify local hot spots, rendering direct-liquid contact essential for stable operation. Consequently, hyperscale operators are specifying immersion as a baseline for AI training halls, thereby increasing fluid demand throughout the forecast horizon

Escalating Electricity Tariffs Accelerate Operational Efficiency Focus

Electricity prices in Asia Pacific hubs such as Singapore have surpassed USD 0.20 per kWh, sharpening focus on power-usage effectiveness. Immersion cooling typically delivers PUE values between 1.05 and 1.10, compared with 1.40–1.60 for air systems, unlocking 25–35% energy savings [2].Iceotope, “Precision Liquid Cooling Solutions,” iceotope.com Kaiser Permanente reported a 20% energy reduction after switching to immersion, substantiating the economic case even with higher upfront spend. Expanding carbon-pricing frameworks in Japan and China further incentivize efficient cooling, reinforcing adoption across hyperscale and colocation facilities.

Water Scarcity Regulations Reshape Cooling Infrastructure Strategies

Evaporative cooling consumes up to 2.5 liters of water per kWh of IT load, conflicting with drought conditions in India and Australia [3].Australian Government Department of Climate Change, “National Renewable Energy Reporting,” dcceew.gov.auImmersion systems operate in closed loops, eliminating water draw and ensuring continuity during municipal restrictions. Operators in Chennai and Bangalore have documented water savings exceeding 80%, propelling immersion deployments that align with corporate conservation targets.

Edge Micro-Data Center Proliferation Demands Distributed Cooling Solutions

5G standalone networks require compute nodes in densely populated areas where space and noise regulations constrain HVAC installs. Immersion tanks operate silently, fit within telecom cabinets, and manage 40–80 kW loads in footprints suitable for sidewalk or rooftop enclosures. NTT Data’s USD 10.1 billion regional infrastructure plan includes liquid-cooled edge sites that must withstand ambient temperatures from −10 °C to 45 °C without mechanical refrigeration.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront CAPEX | −1.5% | Region-wide, most acute in cost-sensitive markets | Short term (≤ 2 years) |

| Limited fluid/material longevity data | −0.8% | Japan, Singapore, regional regulators | Medium term (2-4 years) |

| Imminent PFAS bans | −0.6% | Japan, Australia with knock-on across Asia Pacific | Long term (≥ 4 years) |

| Scarcity of immersion-skilled technicians | −0.4% | Emerging Asia Pacific economies | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Capital Investment Creates Adoption Barriers

Immersion racks cost USD 18,000–25,000, double that of chilled-air counterparts, due to fluid tanks, CDU loops, and premium dielectric liquids [4].Schneider Electric, “Data Center Liquid Cooling Solutions,” se.com Cold-plate retrofits and CDU procurement can push project paybacks beyond three years, restricting uptake among tier-II colocation providers and government entities with constrained capital budgets. Rental models and as-a-service financing are emerging to dilute CAPEX barriers, but uptake remains uneven across the Asia Pacific data center immersion cooling fluid market.

PFAS Regulatory Restrictions Threaten Fluorocarbon Fluid Supply

Australia’s PFAS National Environmental Management Plan and Japan’s F-Gas amendments tighten import and usage thresholds for PFAS-laden fluorocarbons. Two-phase cooling depends heavily on such chemistries; reformulation may elevate costs or degrade performance, risking supply interruptions for new deployments. Fluid vendors are accelerating HFO research, yet commercial availability at scale remains two to three years away, damping near-term confidence among prospective adopters.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Fluid Type: Synthetic Hydrocarbons Lead Despite Fluorocarbon Innovation

Synthetic hydrocarbons command 46% market share in 2024 through proven thermal performance and established supply chains, while fluorocarbon-based fluids achieve 15.5% CAGR through 2030 despite regulatory headwinds affecting PFAS-containing formulations. Polyalphaolefins (PAO) and alkylbenzene-based fluids dominate single-phase applications due to superior oxidation stability and wide operating temperature ranges that accommodate varying thermal loads without fluid degradation Chevron Phillips Chemical. For example, Castrol's collaboration with China Telecom Corporation demonstrates how PAO-based fluids enable reliable operation in demanding telecommunications infrastructure where thermal cycling occurs frequently Castrol. Mineral oils maintain cost advantages in price-sensitive applications but face performance limitations at higher power densities, while bio-based esters gain traction through sustainability mandates despite higher procurement costs.

By Phase Type: Single-Phase Dominance Faces Two-Phase Challenge

Single-phase immersion systems maintain 71% market share in 2024 through operational simplicity and lower maintenance requirements, while two-phase systems accelerate at 17% CAGR through superior heat transfer coefficients that enable higher rack power densities. Single-phase systems circulate dielectric fluid without phase change, providing predictable thermal management and easier system integration that appeals to operators prioritizing reliability over maximum performance. The University of Maryland's deployment achieved 5.5% PUE improvement using single-phase mineral oil systems, demonstrating measurable efficiency gains without complex vapor management requirements. Maintenance advantages include simplified fluid handling, reduced pumping complexity, and elimination of vapor condensation systems that require specialized technical expertise.

Two-phase immersion cooling gains momentum through exceptional heat transfer capabilities that enable rack densities exceeding 200 kW while maintaining component temperatures within acceptable ranges. These systems leverage fluid boiling and condensation cycles to transport heat more efficiently than single-phase circulation, creating opportunities for extreme density deployments that would be impossible with conventional cooling approaches.

By Data Center Type: Cloud Providers Drive While Edge Accelerates

Cloud service providers represent 52% market share in 2024 through massive scale deployments and thermal density requirements that justify immersion cooling investments, while edge micro data centers achieve 14.2% CAGR through space constraints and distributed computing demands. Hyperscale operators like Digital Realty and Global Switch implement immersion cooling in high-density zones where AI and machine learning workloads generate thermal loads exceeding traditional cooling capacity. These deployments benefit from economies of scale that amortize higher upfront costs across thousands of servers, while operational expertise enables complex fluid management systems that smaller operators cannot support effectively.

By End-User Industry: IT Services Lead While Media Accelerates

IT/ITES maintains 38% market share in 2024 through cloud computing infrastructure and software development workloads that generate consistent thermal loads, while media and entertainment achieves 14.8% CAGR through content creation and streaming infrastructure demanding high-performance computing capabilities. Traditional IT workloads benefit from immersion cooling's ability to maintain stable operating temperatures that improve server reliability and extend component lifecycles, creating total cost of ownership advantages that justify higher cooling investments. For instance, major cloud service providers report 15-25% improvement in server mean time between failures when operating in immersion cooling environments compared to air-cooled facilities.

Geography Analysis

China leads the Asia Pacific data center immersion cooling fluid market through aggressive cloud-service expansion and state energy-efficiency targets mandating sub-1.3 PUE for facilities launched after 2025. Alibaba Cloud and Tencent have validated single-phase PAO baths in Tier IV campuses across Beijing and Guangzhou, catalyzing domestic supply chains for synthetic fluids. Cloud operators also pilot waste-heat reuse by redirecting 35 °C outlet fluid into district heating, meeting municipal carbon-reduction quotas.

India’s ascent mirrors digital-public-infrastructure initiatives and extreme water-stress events. Operators in Mumbai and Chennai document 80% water savings by replacing adiabatic coolers with immersion tanks, enabling continuity during rationing. Rising electricity tariffs compound the business case, as immersion fluid systems achieve 1.08 PUE against the 1.45 averages of coastal air-chilled halls.

Japan and South Korea combine technology leadership with policy carrots. Tokyo’s green-taxonomy framework offers 0.4 percentage-point interest rebates on loans covering low-GWP cooling, while Seoul’s industrial digitalization grants reimburse up to 20% of immersion CAPEX. In parallel, Singapore’s tight land constraints and carbon taxes push colocation providers to adopt high-density immersion pods that double compute per square foot without violating heat-island guidelines.

Competitive Landscape

The Asia Pacific data center immersion cooling fluid market remains moderately concentrated. 3M, Exxon Mobil, Shell, and Dow Chemical collectively supply more than half of regional dielectric volumes, leveraging decades of fluid-engineering experience and safety certifications 3M.COM. Vertical alliances are proliferating: Castrol pairs its synthetic hydrocarbons with rack-integrated tanks through partnerships with telecom carriers, while Shell invests in service franchises to deliver fluid recycling onsite.

System integrators such as LiquidStack, Submer Technologies, and Green Revolution Cooling focus on turnkey deployments, bundling heat exchangers, software dashboards, and warranty services. Patent filings surged 22% in 2025 as vendors race to introduce PFAS-free chemistries and modular tank geometries optimized for 45U server stacks. Smaller regional entrants struggle with compliance overhead and supply-chain coordination, signaling potential consolidation through M&A or joint-venture licensing.

Colocation providers increasingly demand performance-based contracts, paying vendors per kilowatt of heat removed, which shifts revenue from one-time hardware sales to recurring service models. Chemical majors respond by offering fluid-as-a-service, pricing dielectric replenishment and monitoring bundles that lock in multi-year commitments and raise switching costs.

Asia Pacific Data Center Immersion Cooling Fluid Industry Leaders

Sinopec Juhua Fluorochemicals

Petronas Lubricants International

LiquidStack Ltd.

3M

Exxon Mobil Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Vertiv Holdings formed a strategic alliance with the Open Compute Project to codify immersion specifications that cut cooling infrastructure costs by 30%.

- August 2025: STT GDC partnered with Firmus to roll out USD 50 million in immersion solutions across Southeast Asia, targeting sustainability gains.

- June 2025: Supermicro delivered a USD 280–290 million AI server shipment employing immersion racks rated above 200 kW per rack.

- May 2025: BAC Technologies and DUG Technology deployed immersion cooling for 150 kW HPC workloads in resource exploration.

- June 2025: Nidec raised production of cooling components from 200 to 3,000 units per month to satisfy regional demand.

Asia Pacific Data Center Immersion Cooling Fluid Market Report Scope

| Mineral Oil |

| Synthetic Hydrocarbon (PAO/Alkylbenzenes) |

| Fluorocarbon-Based |

| Bio-Based Esters |

| Single-Phase |

| Two-Phase |

| Cloud Service Providers |

| Colocation |

| Enterprise / Edge |

| IT/ITES |

| BFSI |

| Healthcare |

| Government and Defense |

| Media and Entertainment |

| Other End Users |

| China |

| Japan |

| India |

| South Korea |

| Southeast Asia (Singapore, Indonesia, Malaysia, Thailand, Vietnam, Philippines) |

| Australia and New Zealand |

| Rest of Asia Pacific |

| By Fluid Type | Mineral Oil |

| Synthetic Hydrocarbon (PAO/Alkylbenzenes) | |

| Fluorocarbon-Based | |

| Bio-Based Esters | |

| By Phase Type | Single-Phase |

| Two-Phase | |

| By Data Center Type | Cloud Service Providers |

| Colocation | |

| Enterprise / Edge | |

| By End-User Industry | IT/ITES |

| BFSI | |

| Healthcare | |

| Government and Defense | |

| Media and Entertainment | |

| Other End Users | |

| By Country | China |

| Japan | |

| India | |

| South Korea | |

| Southeast Asia (Singapore, Indonesia, Malaysia, Thailand, Vietnam, Philippines) | |

| Australia and New Zealand | |

| Rest of Asia Pacific |

Key Questions Answered in the Report

What is the projected value of the Asia Pacific data center immersion cooling fluid market by 2030?

The market is expected to reach USD 1.03 billion by 2030, reflecting an 11.05% CAGR.

Which fluid type currently leads adoption in Asia Pacific immersion cooling?

Synthetic hydrocarbons hold 46% revenue share due to thermal stability and established supply chains.

Why are two-phase immersion systems gaining interest despite higher complexity?

They can dissipate heat at rack densities beyond 200 kW, serving AI clusters that exceed single-phase capacity.

How do water-scarcity regulations influence cooling technology choices in India?

Municipal water restrictions make evaporative cooling untenable, encouraging operators to adopt waterless immersion systems that cut water use by 80%.

Which country is forecast to grow the fastest in immersion cooling fluid consumption through 2030?

India is projected to expand at a 20% CAGR, driven by digitalization and sustainability requirements.

What impact will PFAS bans have on immersion cooling fluids?

Restrictions will pressure suppliers to replace fluorocarbon formulations, potentially raising costs and constraining two-phase system growth until compliant alternatives scale.

Page last updated on: