Europe Data Center Immersion Cooling Fluid Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

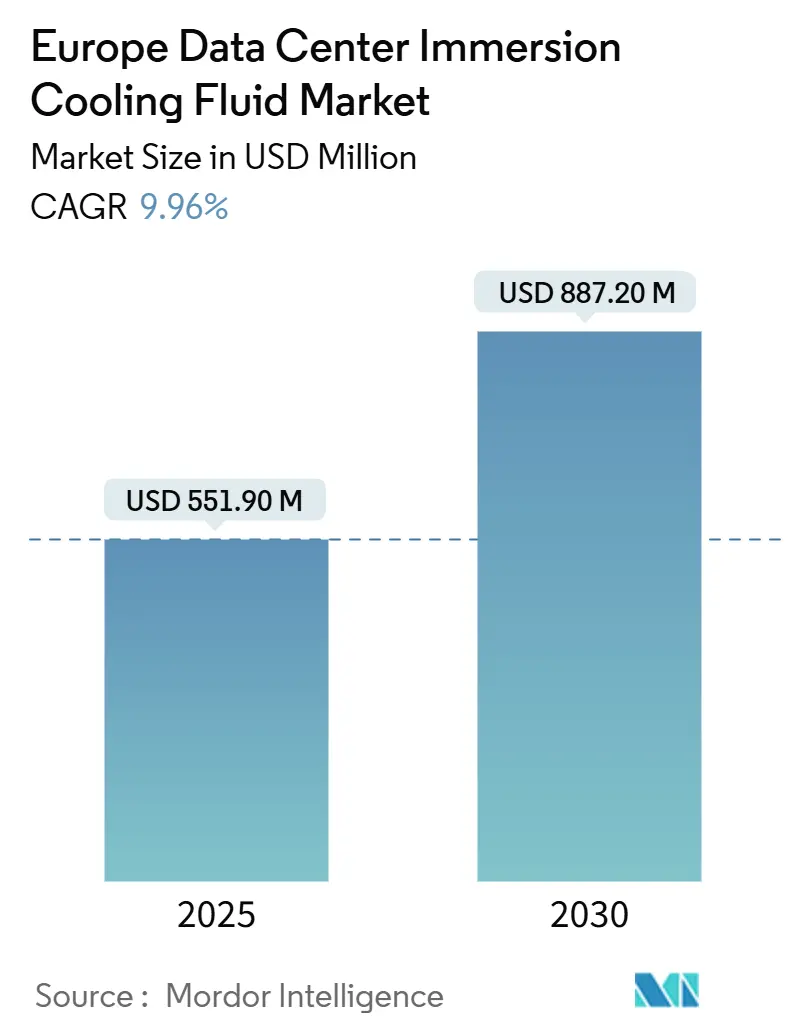

| Market Size (2025) | USD 551.90 Million |

| Market Size (2030) | USD 887.20 Million |

| Growth Rate (2025 - 2030) | 9.96% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Data Center Immersion Cooling Fluid Market Analysis by Mordor Intelligence

The Europe data center immersion cooling fluid market size stood at USD 551.9 million in 2025 and is projected to reach USD 887.2 million by 2030, translating to a 9.96% CAGR across the forecast period. Growing rack densities that exceed 100 kW, electricity prices ranging between EUR 0.25-0.30/kWh, and policy mandates that require waste-heat reuse combine to push operators toward immersion technology. Synthetic hydrocarbon fluids dominate early deployments because of familiar supply chains, but bio-based esters are gaining momentum as EU PFAS restrictions tighten. Operators continue to favor single-phase systems that offer simpler maintenance even though two-phase alternatives deliver marginally higher thermal efficiency. Fluid suppliers, tank makers, and cooling distribution specialists are moving toward vertical integration to reduce deployment friction, and the Open Compute Project immersion specification v2.0 now shortens OEM qualification cycles from as long as 24 months to less than 9 months.

Key Report Takeaways

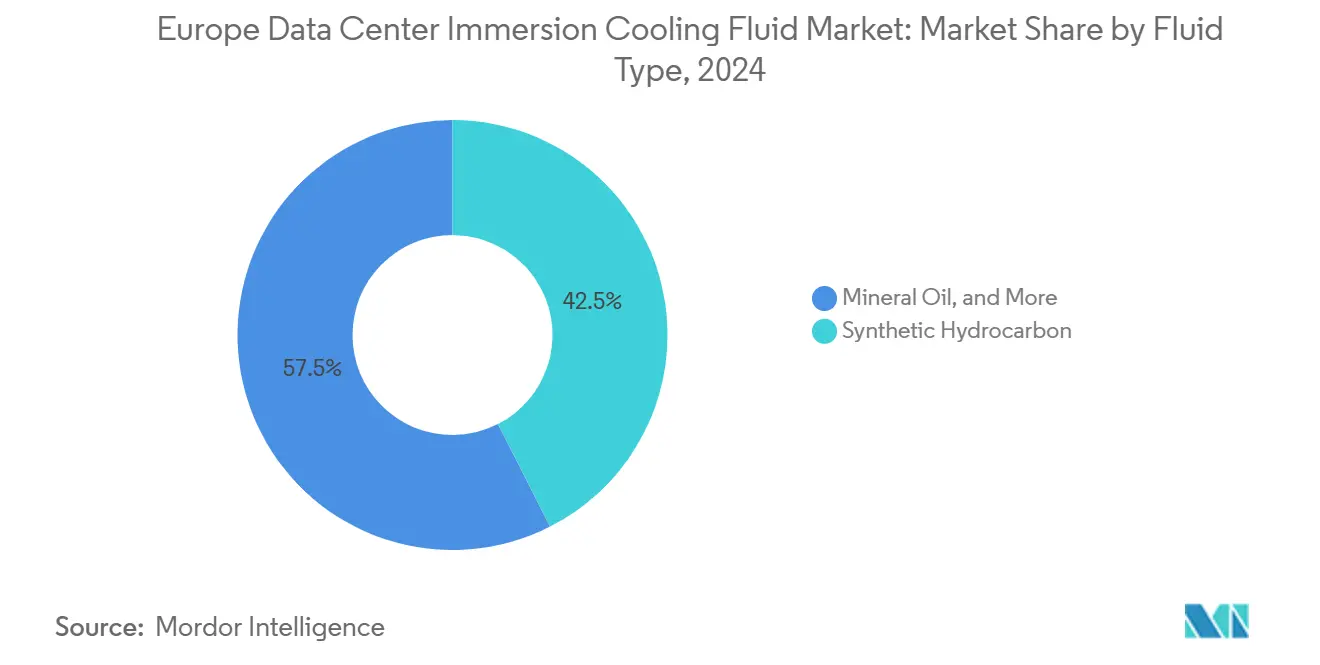

- By fluid type, synthetic hydrocarbons led with 42.5% Europe data center immersion cooling fluid market share in 2024.

- By phase type, single-phase systems maintained a 61% share of the Europe data center immersion cooling fluid market size in 2024.

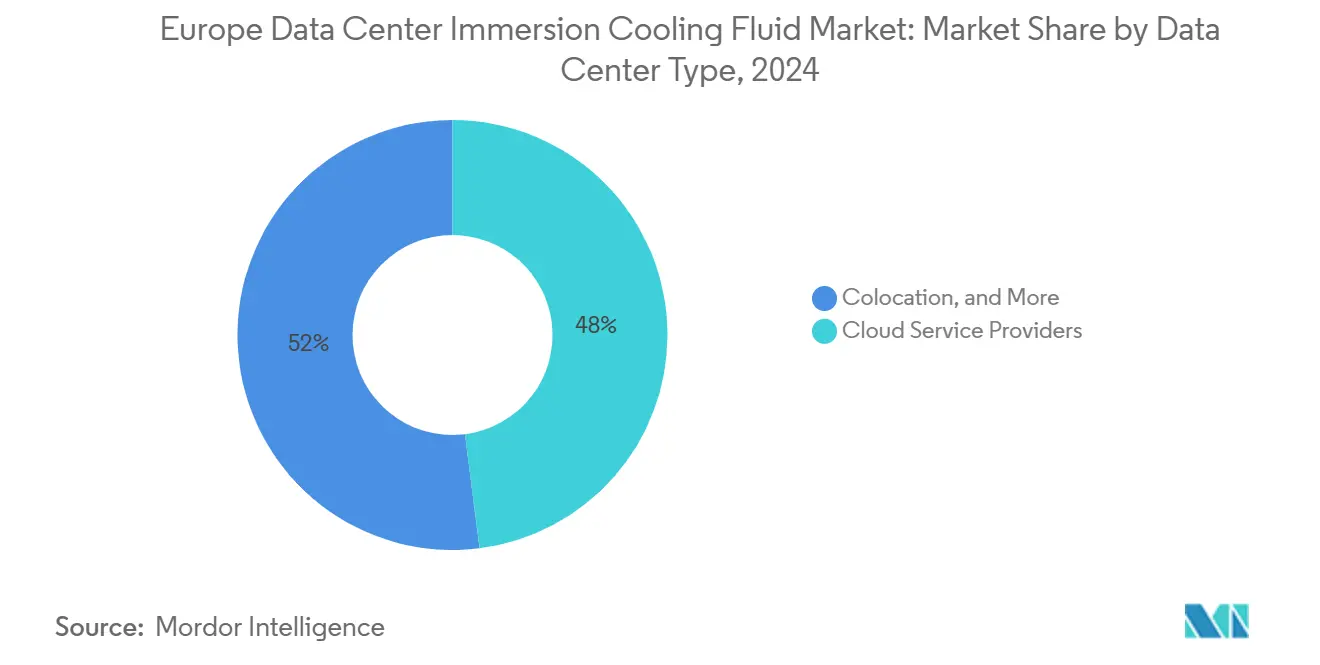

- By data center type, cloud service providers accounted for 48% of the Europe data center immersion cooling fluid market size in 2024.

- By end-user industry, IT and telecommunications commanded 37% share of the Europe data center immersion cooling fluid market size in 2024.

- By geography, Ireland is forecast to expand at a 17.5% CAGR through 2030.

Europe Data Center Immersion Cooling Fluid Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hyperscale-AI rack densities >100 kW accelerating liquid coolant adoption | +2.10% | Global, concentrated in DE, NL, IE hyperscale hubs | Short term (≤ 2 years) |

| Rising European electricity prices amplifying TCO savings vs. air cooling | +1.80% | EU-wide, particularly DE, ES, IT with highest rates | Medium term (2-4 years) |

| EU water-stress regulations curbing evaporative cooling in FL and ES sites | +1.20% | Southern Europe (ES, IT, FR), expanding to Central EU | Medium term (2-4 years) |

| Pending EU-wide PFAS restrictions spurring shift to hydrocarbon/ester fluids | +1.50% | EU-wide regulatory compliance, early adoption in DE, NL | Long term (≥ 4 years) |

| Heat-reuse incentives rewarding 50°C fluid return | +0.90% | DE (EnEfG), expanding to Nordic countries | Long term (≥ 4 years) |

| Open Compute Project immersion spec v2.0 catalyzing OEM qualification | +1.10% | Global hyperscale operators, concentrated in EU data center hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Hyperscale-AI Rack Densities Accelerating Liquid Coolant Adoption

AI workloads now push racks beyond 100 kW, well above the 40-50 kW ceiling of air cooling, and GPU clusters such as NVIDIA H100 consume 700 W each, doubling the heat load of prior generations [1].Microsoft Sustainability Team, “Water-Free Cooling for AI Clusters,” Microsoft, microsoft.com Single-phase immersion removes up to 95% of that heat while also eliminating fan power that previously represented 15-20% of a rack’s electrical draw. The new OCP v2.0 specification standardizes tank footprints and fluid tests, cutting qualification lead-times to nine months and accelerating hyperscale rollouts. In Germany, this density shift supports compliance with the Energy Efficiency Act because hotter return fluids enable viable district-heating connections.

Rising European Electricity Prices Amplifying TCO Savings

Average prices at EUR 0.25-0.30/kWh equate to energy savings of EUR 2-3 million each year for a 10 MW facility when immersion cooling trims consumption by up to 40% [2]JLL Analysts, “European Data Center Report 2024,” JLL, jll.com. Operators like Digital Realty now market liquid-ready colocation suites that promise PUE values of 1.05 compared with 1.25 in traditional halls. Electricity is 60-70% of total operating cost, so even incremental efficiency gains materially improve EBITDA margins while simultaneously lowering Scope 2 emissions.

EU Water-Stress Regulations Curbing Evaporative Cooling

Spain’s Catalonia region and Italy’s Po Valley restrict new water permits for data centers, complicating evaporative designs that consume 1.8-2.5 L/kWh [3].European Environment Agency, “Water Stress and Climate Adaptation,” European Environment Agency, eea.europa.eu Immersion cooling is therefore an attractive alternative because it is effectively water-free and still supports 45-55 °C return temperatures suitable for local district-heating grids. Disclosure mandates within the EU Corporate Sustainability Reporting Directive further highlight water usage, adding reputational pressure that accelerates adoption.

Pending EU-Wide PFAS Restrictions Spurring Fluid Innovation

The European Chemicals Agency has proposed banning fluorocarbons by 2027. 3M will cease Novec production after Q4 2025, removing up to 30% of supply [4].3M Company, “Novec Product Discontinuation Notice,” 3M Company, 3m.com Synthetic hydrocarbons and bio-based esters now fill the gap even though their prices sit 10-15% higher. Shell, ExxonMobil, and Reliance Specialty Products leverage existing REACH registrations to move product to market faster than smaller entrants.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited 5-year reliability datasets for in-tank electronics and cable jackets | -1.40% | Global, particularly affecting conservative EU enterprise segments | Medium term (2-4 years) |

| CAPEX premium for tank, pump and CDU retrofits in legacy halls | -1.10% | Established EU markets (DE, UK, FR) with aging infrastructure | Short term (≤ 2 years) |

| EU chemical-registration lead-times delaying new dielectric formulations | -0.80% | EU-wide regulatory compliance, affecting fluid innovation cycles | Long term (≥ 4 years) |

| Supply-chain exposure to single-source fluorocarbons post-3M exit | -1.20% | Global, concentrated in early-adopter facilities using Novec fluids | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited Reliability Datasets Constraining Enterprise Adoption

Mission-critical operators demand five-to-seven-year component studies, yet most commercial sites only began immersion pilots in 2019. Concerns persist around PVC cable-jacket softening and gasket swelling, which could raise downtime risk beyond accepted 99.995% thresholds. Government pilots, such as the Department of Defense Asetek deployment, are helping to close the knowledge gap but full enterprise confidence is still two-to-three years away.

CAPEX Premium Deterring Legacy Infrastructure Retrofits

A retrofit can add USD 150,000-250,000 per MW compared with enhanced air cooling. Load-bearing floors, upgraded pumps, and revised fire-suppression systems often stretch conversion projects to nine months. Legacy halls built before 2015 therefore face unfavorable payback periods, encouraging operators to reserve immersion for greenfield builds or high-density expansions only.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Fluid Type: Synthetic Hydrocarbons Anchor Early Adoption

Synthetic hydrocarbons captured 42.5% of the Europe data center immersion cooling fluid market share in 2024 because they slot into existing petroleum supply channels and already hold REACH approval. The Europe data center immersion cooling fluid market size for this segment is projected to reach USD 370 million by 2030 as operators leverage viscosity stability from -40 °C to 200 °C and predictable component compatibility. Bio-based esters advance at a 13.0% CAGR, benefitting from decarbonization narratives and PFAS phase-outs. Mineral oils keep a foothold in sub-50 kW racks where budget constraints matter most but suffer performance penalties at higher densities. Fluorocarbon demand is already contracting following 3M’s strategic withdrawal.

Growing alliances underscore supplier repositioning. Shell works with Penguin Solutions to integrate synthetic PAO blends that hold viscosity across wide temperature swings, while Castrol and Submer co-design fluids around server-level optimizations. Established refiners thus gain first-mover advantages because REACH approval cycles for new formulas can extend past 18 months, limiting smaller entrants’ timelines.

By Phase Type: Simplicity Trumps Peak Efficiency

Single-phase solutions held 61% of the Europe data center immersion cooling fluid market in 2024, and unit shipments continue climbing even as two-phase installs post a 20% annual growth rate. Operators favor straightforward circulation loops and lower maintenance overhead. Two-phase technology boasts heat-transfer coefficients up to 25,000 W/m²K and has notched PUE scores near 1.03 in LiquidStack pilots, yet vapor-management hardware adds USD 75,000-100,000 to the bill of materials. The Europe data center immersion cooling fluid market size linked to two-phase systems is still expected to double by 2030 as AI racks surpass 150 kW density thresholds.

The Open Compute Project’s new spec addresses both phases, yet single-phase platforms benefit from plug-and-play familiarity across server generations. As more high-density workloads proliferate, the trade-off between operational ease and marginal kilowatt savings will continue to shape adoption patterns.

By Data Center Type: Cloud Dominates While Edge Surges

Cloud service providers drove 48% of shipments in 2024, relying on huge economies of scale to validate immersion. The Europe data center immersion cooling fluid market size within the cloud segment should pass USD 430 million by 2030 as hyperscalers stretch air cooling limits. Edge facilities record the fastest growth at 11.7% CAGR because 5G latency requirements demand local processing nodes that often reside in space-constrained environments. Colocation players cautiously introduce liquid-ready suites to meet customer demand without overhauling their entire floor. Enterprise on-premise deployments lag due to limited in-house expertise although early health-care and financial pilots are narrowing that gap.

Digital Realty now offers immersion racks on a service basis, bundling infrastructure and fluids under one monthly fee, which helps smaller tenants sidestep upfront complexity. Microsoft also highlights a water-free edge-module design for rural sites where municipal supply is scarce.

By End-User Industry: IT Retains Lead but Healthcare Accelerates

IT and telecom entities claimed 37% of demand in 2024, a figure buoyed by AI training clusters and content-delivery networks. Healthcare workloads grow at 19% CAGR thanks to imaging, genomics, and real-time diagnostics, making them the fastest riser in the Europe data center immersion cooling fluid market. BFSI institutions investigate immersion for latency-sensitive trading while government and defense bodies seek resilience and operational secrecy. Media-streaming giants deploy immersion in render farms but adoption remains concentrated among a handful of studios.

Pharmaceutical facilities now run drug-discovery models on GPU clusters cooled by synthetic hydrocarbons, shortening simulation cycles and enabling 24 × 7 utilization. These use cases build an evidence trail that other regulated industries can follow over the next five years.

Geography Analysis

Germany led with 22% share in 2024 as EnEfG rules mandate waste-heat reuse and electricity prices reach EUR 0.32/kWh. Frankfurt financial exchanges rely on Europe data center immersion cooling fluid market solutions to secure microsecond latency while freeing mechanical room capacity for additional servers. Munich’s automotive sector uses immersion to model autonomous driving scenarios at rack power profiles that exceed 120 kW. Operators monetize 50 °C return heat at EUR 25-35/MWh, offsetting utility costs.

Ireland posts the fastest 17.5% CAGR. A 12.5% corporate tax rate, 40% renewable grid penetration, and robust submarine cables make Dublin a magnet for hyperscalers. Immersion accommodates densification inside constrained real-estate envelopes while proving attractive for scope-3 carbon accounting metrics.

The United Kingdom, France, and the Netherlands hold mature footprints. France benefits from lower-carbon nuclear generation at EUR 0.18-0.22/kWh, and operators there leverage immersion to amplify sustainability credentials. Spain and Italy rise as new centers because water-stress rules hamper evaporative towers and encourage sealed liquid systems that consume no potable water. Switzerland and the Nordics integrate heat-reuse loops for district networks, showcasing the circular-energy narrative.

Competitive Landscape

The ecosystem spans fluid producers, tank manufacturers, and CDU vendors, yet end users increasingly prefer vertically integrated bundles. Submer joins with Castrol and Supermicro to offer turnkey racks that arrive factory-validated. ExxonMobil and Shell exploit refining economies to supply synthetic hydrocarbons that already carry REACH numbers, positioning them as safe bets since 3M’s PFAS discontinuation. Reliance Specialty Products and EnviroTech Europe penetrate early adopters with PFAS-free esters but still need longer operating histories to assure risk-averse enterprises.

Patents reveal focus areas: LiquidStack claims innovations in vapor containment that cut two-phase installation footprints, while TMGcore files for modular edge cabinets. Market entry barriers now shift from hardware to chemical stewardship, and suppliers that document five-year compatibility across gasket, PCB, and cable assemblies will command greater share. M&A chatter suggests upcoming consolidation as bigger chemicals firms acquire niche formulators to secure feedstock diversity.

Europe Data Center Immersion Cooling Fluid Industry Leaders

LiquidStack

Schneider Electric

The Chemours Company

Exxon Mobil Corp.

3M

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Stellium completed an OCP-compliant immersion deployment with Submer that runs 150 kW racks at 1.05 PUE.

- December 2024: Best Technology launched PFAS-free synthetic esters with -40 °C to 200 °C operating range.

- October 2024: Submer, Castrol, and Supermicro unveiled an integrated immersion rack for hyperscalers.

- May 2024: Digital Realty introduced direct liquid cooling services across Europe.

- March 2025: 3M accepted final Novec orders ahead of Q4 2025 production end.

- February 2025: CNRS expanded the Jean Zay supercomputer to 150 kW racks using immersion.

Europe Data Center Immersion Cooling Fluid Market Report Scope

| Mineral Oil |

| Synthetic Hydrocarbon (Isoparaffin/PAO) |

| Fluorocarbon-Based Fluids |

| Bio-Based Esters |

| Single-Phase |

| Two-Phase |

| Cloud Service Providers |

| Colocation |

| On-Premise / Enterprise / Edge |

| IT/ITES |

| BFSI |

| Healthcare |

| Government and Defense |

| Media and Entertainment |

| Other End Users |

| Germany |

| United Kingdom |

| France |

| Netherlands |

| Ireland |

| Spain |

| Italy |

| Switzerland |

| Russia |

| Rest of Europe |

| By Fluid Type | Mineral Oil |

| Synthetic Hydrocarbon (Isoparaffin/PAO) | |

| Fluorocarbon-Based Fluids | |

| Bio-Based Esters | |

| By Phase Type | Single-Phase |

| Two-Phase | |

| By Data Center Type | Cloud Service Providers |

| Colocation | |

| On-Premise / Enterprise / Edge | |

| By End-User Industry | IT/ITES |

| BFSI | |

| Healthcare | |

| Government and Defense | |

| Media and Entertainment | |

| Other End Users | |

| By Country | Germany |

| United Kingdom | |

| France | |

| Netherlands | |

| Ireland | |

| Spain | |

| Italy | |

| Switzerland | |

| Russia | |

| Rest of Europe |

Key Questions Answered in the Report

What is the projected value of the Europe data center immersion cooling fluid market by 2030?

The market is forecast to reach USD 887.2 million by 2030.

Which fluid type currently holds the largest share?

Synthetic hydrocarbons lead with 42.5% share in 2024.

Why is Ireland the fastest-growing country?

High renewable penetration, favorable tax policy, and hyperscale data center concentration drive a 17.5% CAGR through 2030.

How do PFAS restrictions affect fluid selection?

Pending EU bans eliminate fluorocarbon options and shift demand toward synthetic hydrocarbons and bio-based esters.

What rack densities trigger immersion adoption?

Densities above 100 kW per rack surpass practical air-cooling limits and motivate liquid cooling deployment.

Page last updated on: